Document Management Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

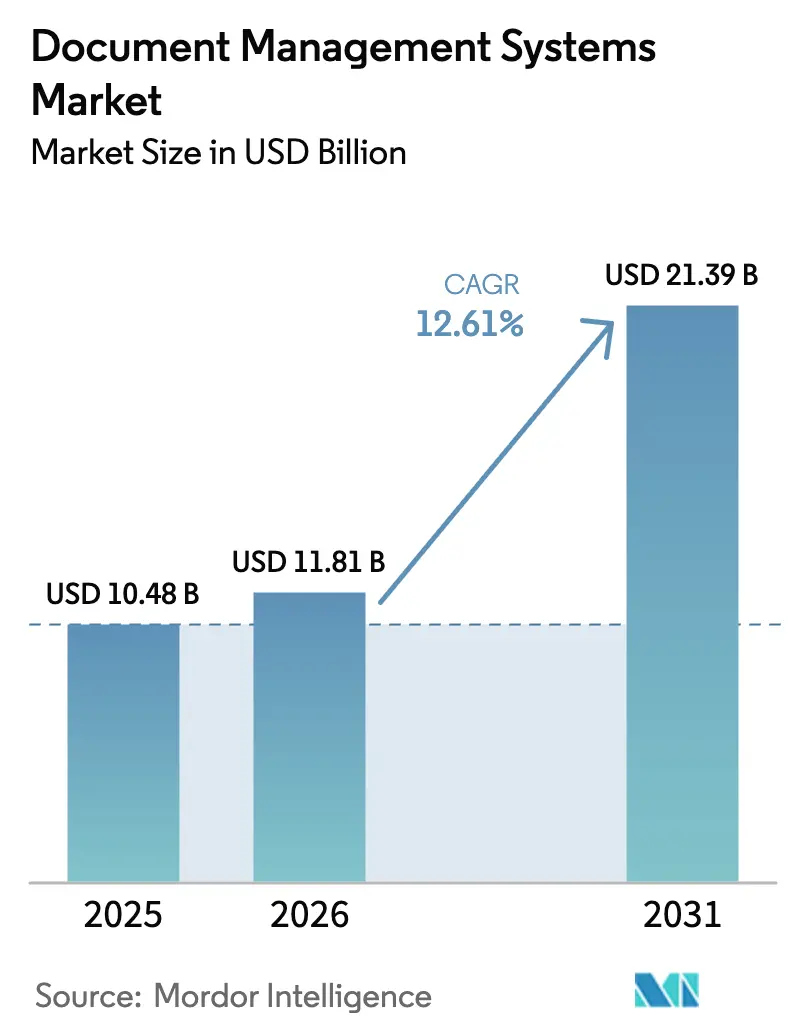

| Market Size (2026) | USD 11.81 Billion |

| Market Size (2031) | USD 21.39 Billion |

| Growth Rate (2026 - 2031) | 12.61% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Document Management Systems Market Analysis by Mordor Intelligence

The Document Management Systems Market size is projected to expand from USD 10.48 billion in 2025 and USD 11.81 billion in 2026 to USD 21.39 billion by 2031, registering a CAGR of 12.61% between 2026 to 2031. Rapid growth stems from enterprises retiring legacy repositories in favor of cloud-native platforms that embed AI copilots inside everyday collaboration tools. At the same time, data-sovereignty laws in Europe and Asia Pacific obligate vendors to stand up in-region hosting with end-to-end encryption, broadening the customer base even as it fragments infrastructure footprints. Competitive heat is intensifying as hyperscalers bundle storage into collaboration suites, compressing standalone software pricing and steering pure-play providers toward vertical templates that slash deployment time. Buyers overwhelmingly favor cloud deployment for elastic capacity and automatic upgrades, yet air-gapped on-premise systems endure in defense and other sovereign sectors.

Key Report Takeaways

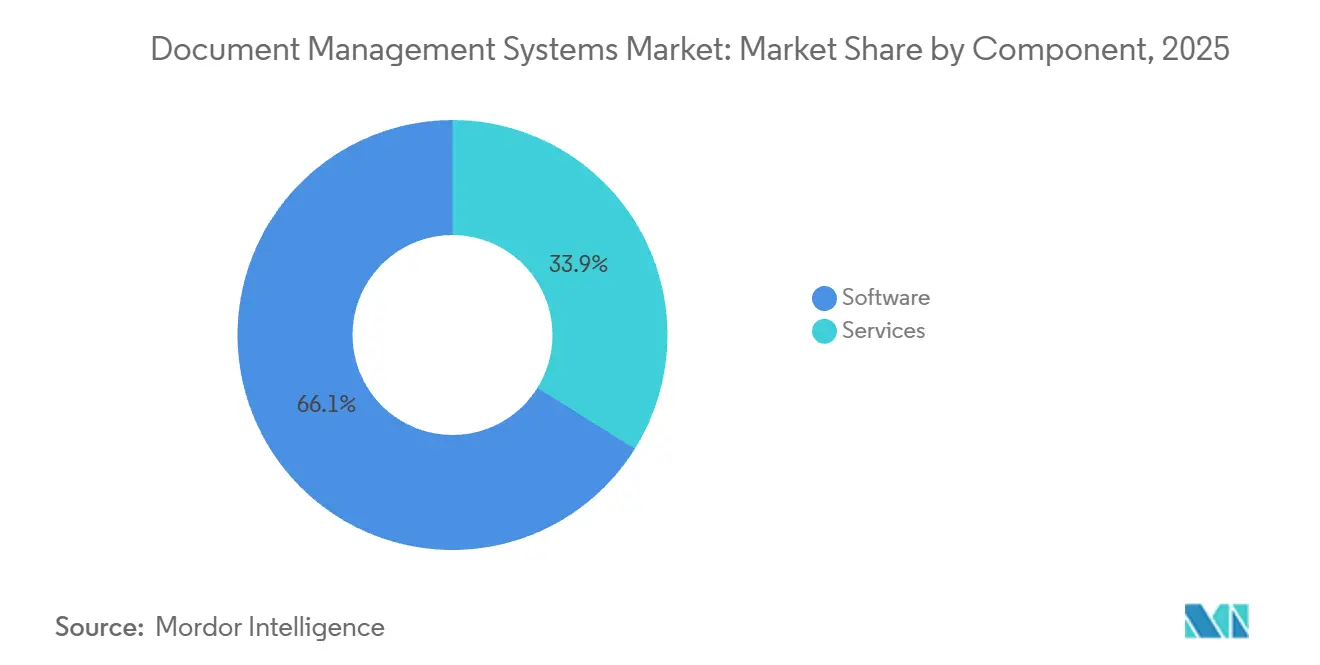

- By component, software licenses held a 66.12% market share in document management systems in 2025, while services are set to expand at a 17.21% CAGR to 2031.

- By deployment mode, cloud captured 70.34% of 2025 revenue and is advancing at an 18.34% CAGR, far outpacing on-premise installations.

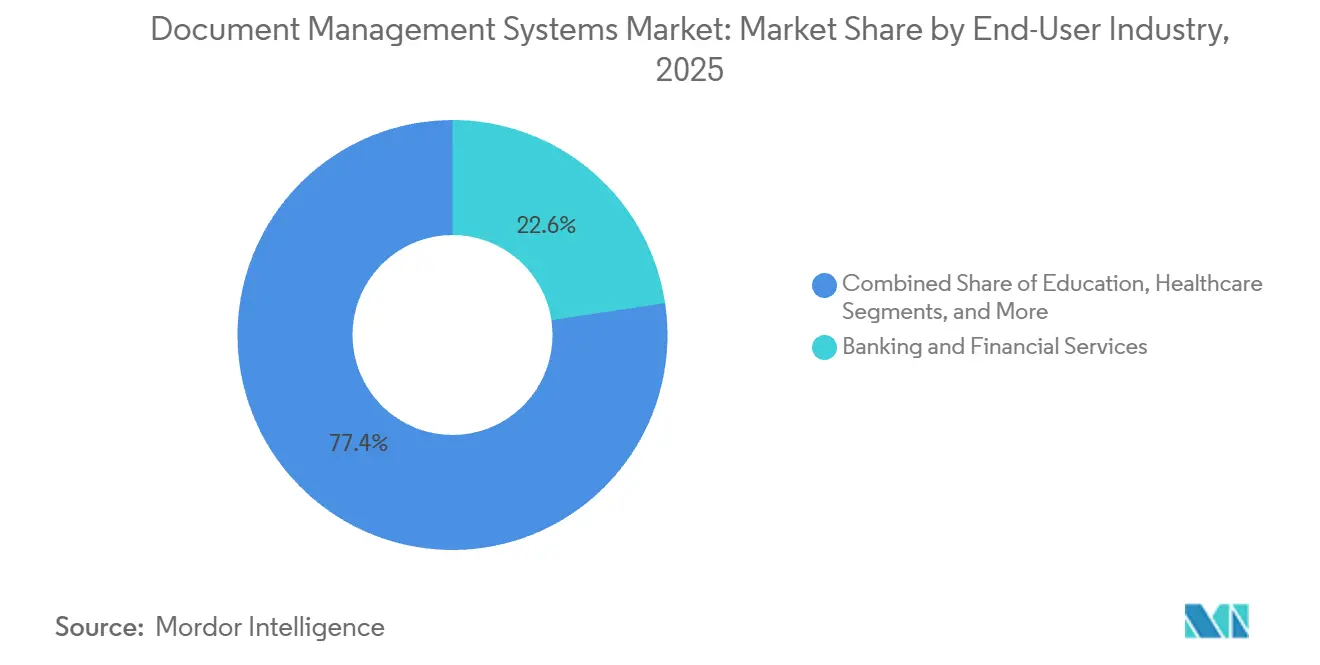

- By end-user industry, banking and financial services led with 22.63% revenue share in 2025, whereas healthcare is forecast to rise at a 17.69% CAGR through 2031.

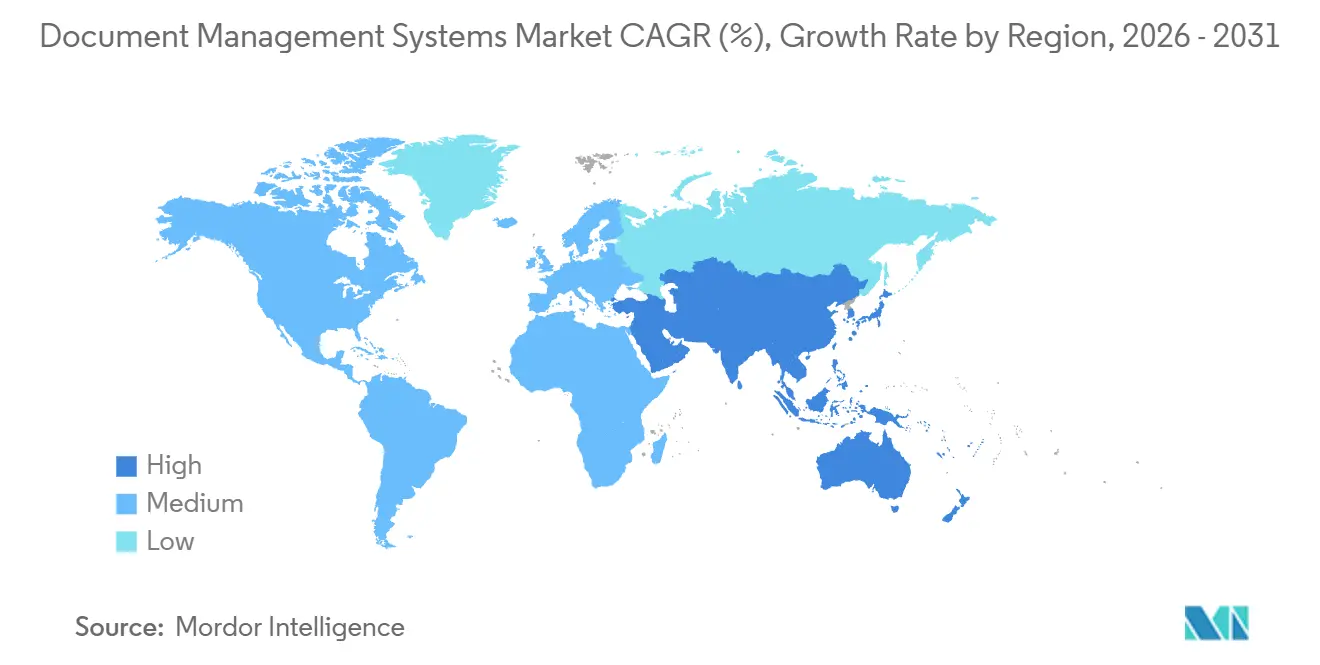

- By geography, North America commanded 37.53% of the document management systems market size in 2025, whereas Asia Pacific is expected to post the highest regional CAGR of 18.43% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Document Management Systems Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Shift Toward Paper-Free Processes | +2.8% | Global, with early momentum in North America and Europe | Medium term (2-4 years) |

| Cloud-Native DMS Platforms Bundled Inside Collaboration Suites | +3.1% | North America and Europe core, expanding to Asia Pacific | Short term (≤ 2 years) |

| Surge in AI-Enhanced Search and Auto-Classification Accuracy | +2.4% | Global, led by North America and Western Europe | Medium term (2-4 years) |

| Strict Data-Sovereignty Rules Driving Compliant Roll-Outs | +2.6% | Europe (GDPR), Asia Pacific (China, India), Middle East | Long term (≥ 4 years) |

| Rise of Industry-Specific Templates Shortening Deployment Cycles | +2.2% | Global, with vertical concentration in BFSI, Healthcare, Manufacturing | Medium term (2-4 years) |

| Generative-AI Copilots Unlocking Content-in-Context Workflows | +2.3% | North America and Europe early adopters, Asia Pacific following | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Shift Toward Paper-Free Processes

Government mandates are accelerating digital conversion far faster than voluntary sustainability initiatives. The U.S. National Archives requires every federal agency to digitize permanent records by December 2026.[1]First-name Last-name, “Electronic Records Archives 2.0,” National Archives and Records Administration, archives.gov Japan’s Digital Agency ordered all prefectures to adopt paperless workflows by April 2025, triggering a 35% jump in procurements. Canon processed 18 billion pages through its cloud-scanning service in 2025, up 22% from 2024, illustrating the flood of analog content entering repositories. Rising capture volumes trim storage costs but inflate metadata-tagging labor, a trade-off that favors AI-driven auto-classification over manual indexing. Enterprises therefore prioritize platforms with built-in machine-learning enrichers that satisfy compliance while slashing operating expense.

Cloud-Native DMS Platforms Bundled Inside Collaboration Suites

Hyperscalers now embed repositories directly in collaboration tools, bypassing lengthy procurement. Microsoft launched SharePoint Embedded in March 2024; by January 2025, more than 200 ISVs had adopted the service. Box deepened integration with Google Workspace in June 2025, and pilot clients recorded 40% fewer version-control errors. Bundled offerings command 15-20% price premiums because they deliver seamless interoperability, forcing pure-play vendors to compete on vertical depth rather than horizontal features.

Surge in AI-Enhanced Search and Auto-Classification Accuracy

Large language models now cut metadata entry labor by up to 70%, yet regulated sectors still demand near-perfect precision. Microsoft 365 Copilot trimmed manual tagging by 65% for 500 pilot enterprises. IBM’s partnership with Unstructured.io pushed domain-specific accuracy to 97%, narrowing the gap to compliance thresholds.[2]First-name Last-name, “Content Assistant Partnership,” IBM Corporation, ibm.com Most organizations run hybrid workflows where AI proposes tags and humans approve them, balancing productivity gains with risk controls.

Strict Data-Sovereignty Rules Driving Compliant Roll-Outs

The European Union’s Data Governance Act prohibits most cross-border transfers of public-sector data. China’s Personal Information Protection Law imposes similar constraints on critical-infrastructure operators. Anticipated Indian legislation is expected to follow suit. Hyperscalers can absorb the capital cost of multiple regional clouds, but mid-tier vendors must partner locally or exit, splitting the market between global platforms and single-country specialists.

Restraints Impact Analysis of Document Management Systems Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent User-Change Resistance in Regulated Back-Office Functions | -1.4% | Global, acute in Europe and North America legacy enterprises | Medium term (2-4 years) |

| High E-Discovery Costs From Poor Metadata Hygiene | -1.2% | North America and Europe litigation-intensive sectors | Long term (≥ 4 years) |

| Cyber-Insurance Premiums Rising After DMS-Centred Ransomware Events | -0.9% | Global, concentrated in Healthcare and BFSI | Short term (≤ 2 years) |

| Vendor Lock-In Concerns Slowing Migration From Legacy ECMs | -1.1% | Global, particularly North America and Europe mid-market | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent User-Change Resistance in Regulated Back-Office Functions

Deloitte found that 38% of financial-services compliance staff still print filings for manual review, doubting the evidentiary strength of digital signatures. Civil-law jurisdictions that require notarized deeds maintain hybrid processes, prolonging change-management programs to two years and inflating training budgets to USD 0.5-2 million per enterprise. Resistance delays ROI and moderates cloud-migration momentum.

High E-Discovery Costs From Poor Metadata Hygiene

Thomson Reuters valued U.S. e-discovery at USD 18,000 per gigabyte in 2024. A Fortune 500 manufacturer spent USD 12 million reviewing 8 terabytes for one dispute, a burden attributable to untagged legacy files. AI enrichment tools promise relief, but retrofitting tags to petabyte-scale archives remains a multi-year endeavor that tempers immediate savings.

Restraints Impact Analysis of Document Management Systems Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| User-change resistance in regulated functions | -1.70% | Global; higher in traditional industries | Medium term (2-4 years) |

| High e-discovery costs from poor metadata | -1.20% | North America, Europe | Short term (≤ 2 years) |

| Rising cyber-insurance premiums post-ransomware | -0.90% | Global; higher in North America and Europe | Medium term (2-4 years) |

| Vendor lock-in concerns | -1.10% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Document Management Systems Market Segment Analysis

By Component:

Services Edge Ahead as Complexity EscalatesServices are growing at a 17.21% CAGR because migration complexity, AI tuning, and compliance mapping outstrip in-house skills. KnowledgeLake migrated 450 million federal documents to SharePoint Online in six weeks, remapping retention policies on the fly. EY and Adobe deliver Basel III audit trails in only 12 weeks through a bundled advisory and e-signature package. Software licenses held a 66.12% market share in 2025. Software remains indispensable, yet license fees fall 10-15% annually under hyperscaler price pressure.

As buyers seek turnkey outcomes, vendors with strong consulting arms, such as IBM, Hyland, and OpenText, capture stickier revenue. Managed services likewise appeal to mid-market firms lacking 24-hour IT coverage; DocuWare’s cloud service bundles backup and patching to cut the total cost of ownership by 30%. Consequently, the document management systems market size for services is expanding faster than license revenue and reshaping vendor business models.

By Deployment Mode:

Cloud Dominates, Hybrid Gains Regulatory TractionCloud deployments generated 70.34% of 2025 revenue and are advancing at 18.34% through 2031, propelled by elastic storage and continuous feature releases. Azure-hosted SharePoint processed more than 1 trillion files in 2025, showcasing scale that on-premise systems struggle to match. Enterprises also value built-in disaster recovery and global accessibility, especially for distributed teams. Still, sovereign sectors retain on-premise instances for air-gapped networks, sustaining a sizable legacy footprint.

Hybrid is emerging as a compliance bridge. Hyland’s OnBase Hybrid Cloud synchronizes metadata to Azure for AI search while holding binaries on customer servers, satisfying data-residency laws without sacrificing modern features. Similar architectures are poised to spread across defense, healthcare, and public-sector accounts, ensuring the document management systems market continues to accommodate multiple deployment choices.

By End-User Industry:

Healthcare Accelerates on Telehealth MandatesBanking and financial services commanded 22.63% revenue in 2025, driven by know-your-customer, anti-money-laundering, and Basel III reporting. However, healthcare is on track to be the fastest-growing vertical at a 17.69% CAGR, propelled by telehealth expansion and electronic health record integration. The Centers for Medicare and Medicaid Services link reimbursements to digital interoperability, pushing hospitals to embed repositories inside Epic and Cerner workflows. Consequently, the document management systems market size tied to healthcare use cases is projected to double in five years.

Manufacturing, construction, education, and retail are also scaling adoption. Autodesk’s ISO 19650-certified template shortens BIM documentation from nine months to six weeks, while Walmart processes 500,000 supplier invoices weekly through an AI-enabled repository. Such vertical depth illustrates how domain-specific templates unlock new budget pools and reduce deployment risk across diverse industries.

Geography Analysis

North America Document Management Systems Market

North America delivered 37.53% of 2025 revenue, helped by U.S. federal digitization deadlines and a Canadian directive that all federal departments move to cloud repositories by March 2027. High Microsoft 365 penetration speeds deployment, yet growth moderates as enterprises stretch platform life cycles and focus on AI add-ons rather than replacements.

APAC Document Management Systems Market

Asia Pacific will grow at 18.43% through 2031. India’s Digital India program earmarked INR 14,903 crore (USD 1.8 billion) for e-governance in its 2025-2026 budget.[3]First-name Last-name, “Digital India Programme,” Government of India, digitalindia.gov.in China’s Digital Silk Road funds state-enterprise deployments to standardize cross-border trade documents. Japan mandated paperless prefectures by April 2025, spurring a 35% order increase. Australia’s amended Privacy Act requires breach notification within 72 hours, pushing organizations toward real-time audit trails.

EMEA Document Management Systems Market

Europe, the Middle East, and Africa form a patchwork shaped by GDPR and localization rules. The EU Data Governance Act obliges vendors to run regional data centers. Germany’s cybersecurity agency advises on-premise or hybrid deployments for critical infrastructure. Gulf smart-city programs such as Dubai Smart 2030 embed repositories into e-government services. South Africa’s POPIA drives banks and telecoms toward consent-managed archives.

Regulatory Landscape

Document management systems (DMS) vendors are operating under tightening expectations around records integrity, electronic trust services, and data residency, which show up in sector and public-sector procurement requirements. In the United States, NARA rules and guidance (including 36 CFR 1236 Subpart E and digitization success criteria issued in 2023) set expectations for digitizing permanent federal records, including metadata and process documentation, which supports demand for retention controls, audit trails, and defensible disposition workflows.

In Europe, compliance requirements are broadening beyond GDPR into alignment between interoperable electronic identity and trust services under the eIDAS framework. Commission Implementing Regulation (EU) 2026/248 (February 2026) establishes recognized formats for advanced electronic signatures and seals, while Regulation (EU) 2025/2532 requires Member States to provide at least one European Digital Identity Wallet by December 2026, increasing the focus on standardized, cross-border recognition of digital documents. Alongside these, ISO standards for records governance and risk (ISO 18128:2024) and for sensitive document classification and handling (ISO 4669-2:2025), plus the ongoing ISO/DIS 30301 update process (inquiry phase as of March 2026), are raising the compliance bar for vendors serving regulated and public-sector buyers.

Value Chain Analysis

The DMS value chain runs from content capture and digitization (scanning and ingestion) to core repository software and records governance (metadata, retention, legal hold). It then extends to security and trust services (encryption, signatures, sealing, archiving), AI and automation layers (OCR, ML extraction, LLM-based classification and search), and integration into line-of-business systems via APIs, including ERP and procurement workflows. Distribution increasingly relies on cloud marketplaces and suite ecosystems, with hyperscalers embedding repositories in collaboration tools, while pure-play and legacy ECM vendors lean on vertical templates, compliance tooling, and implementation speed.

Delivery is typically supported by services and ecosystem partners such as systems integrators, advisory firms, and managed service providers that handle migrations, policy mapping, and model tuning, consistent with a shift toward services-led outcomes. Platform dependencies also shape the chain, since multi-cloud options (AWS, Google Cloud, IBM Cloud, and Azure) influence hosting decisions and enterprise platforms affect integration patterns, including SAP and Oracle-centric deployments. In June 2026, SAP published an updated reference architecture for SAP Document AI on SAP Business Technology Platform, which shows how document intelligence is being packaged as a platform capability that DMS providers and integrators can build around for end-to-end document processing across enterprise applications.

Competitive Landscape

The document management systems market is moderately concentrated, with the top five suppliers controlling 45% of 2025 revenue. Microsoft leverages Teams and SharePoint to embed repositories in day-to-day workflows; over 200 ISVs integrated SharePoint Embedded within a year of launch, widening Microsoft’s reach into vertical software. Box defends share by offering multi-cloud flexibility across AWS, Google Cloud, and IBM Cloud, appealing to organizations wary of single-vendor lock-in.

Adobe partners with EY to bundle Acrobat Sign with compliance advisory, giving regulated banks a turnkey path to Basel III documentation. OpenText’s Micro Focus acquisition enlarged its portfolio but stretched integration resources, allowing nimble rivals such as M-Files and Laserfiche to win mid-market deals. Vertical specialists enhance differentiation: Autodesk dominates construction BIM workflows following ISO 19650 certification, while Thomson Reuters leads legal case management through embedded Federal Rules processes.

Technology roadmaps now converge on generative AI copilots that surface relevant documents within transactions, cutting the 20-30% search tax knowledge workers shoulder. Vendors that blend AI innovation with strict compliance controls are best placed to secure long-term contracts, while pure-play laggards risk relegation to tactical niches. Acquisition pipelines remain active as software-only firms buy consulting practices to deliver full-stack offerings, accelerating consolidation yet preserving space for specialists that solve high-value vertical pain points.

Document Management Systems Industry Leaders

Microsoft Corporation

OpenText Corporation

IBM Corporation

Hyland Software Inc.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Document Management Systems Market Companies Covered in this Report

- Microsoft Corporation

- OpenText Corporation

- IBM Corporation

- Hyland Software Inc.

- Oracle Corporation

- Box Inc.

- Adobe Inc.

- Laserfiche

- M-Files Corp.

- Alfresco (Hyland)

- Dropbox Business

- Zoho Corporation

- DocStar (Epicor)

- AODocs

- LogicalDOC Srl

- Agiloft Inc.

- Synergis Technologies

- Everteam

- FileHold Systems

- PaperSave

- DocuWare GmbH

- Newgen Software Technologies

- Canon Inc.

- Xerox Holdings Corporation

Market Opportunities and Future Outlook

Public-sector digitization programs and identity frameworks are creating repeatable deployment opportunities where retention governance and auditability are required. The US federal digitization deadline for permanent records by December 2026, along with the EU requirement for Member States to provide at least one European Digital Identity Wallet by December 2026, is pushing agencies toward standardized digital-document handling, stronger metadata discipline, and trusted electronic interactions. In July 2026, the Philippines Department of the Interior and Local Government launched a nationwide Document Management System for local government units (DMS4LGUs), indicating active budget allocation and scaled rollouts in government that go beyond single-agency pilots.

In enterprise adoption, whitespace is shifting from basic repository replacement toward AI-enabled content operations that can function across collaboration suites, ERPs, and other line-of-business applications without recreating content silos. Vendor roadmaps reflect this pivot: OpenText released Cloud Editions updates in 2026 (CE 26.1 in March 2026 and Content Management 26.2 in June 2026) with agentic capabilities and migration tools targeting the movement of on-premises content into OpenText Private Cloud, while Hyland emphasizes its Content Innovation Cloud architecture for unified content, enrichment, and orchestration layers. These changes support near-term demand for migration and modernization services (content cleanup, policy mapping, and model governance), and for hybrid patterns that keep sensitive content under tighter control while still enabling AI-driven classification, discovery, and workflow automation.

Recent Industry Developments in Document Management Systems Market

- June 2026: Hyland announced a strategic collaboration with Microsoft to bring the Hyland Content Innovation Cloud to Microsoft Azure, supported by a joint go-to-market and co-sell motion. The update brings Hyland's content platform closer to where customers deploy collaboration and AI workloads, while building on existing Azure enterprise commitments.

- July 2025: OpenText launched Cloud Editions (CE) 25.3 with AI-focused updates in OpenText Core Content Management and premium qualification for SAP S/4HANA Public Cloud. The tighter alignment with SAP cloud environments strengthens OpenText's fit for document-heavy finance and procurement processes that depend on ERP-native integration patterns.

- July 2024: OpenText announced Cloud Editions (CE) 24.3 product innovations spanning information management, security, and AI. The release reinforced the vendor cadence of frequent cloud updates, supporting buyers that prioritize continuous upgrades and integrated security controls over large, infrequent platform refresh cycles.

Document Management Systems Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the market covers document management systems used to capture, store, organize, secure, retrieve, and manage business documents across their life cycle, delivered as cloud or on-premises software and related services.

Scope exclusions: Basic file sync and storage tools and pure web content management tools are excluded when they do not provide dedicated document governance functions.

Segments Covered in This Report

- By Component

- Software

- Services

- By Deployment Mode

- Cloud

- On-Premise

- By End-User Industry

- Banking and Financial Services

- Manufacturing and Construction

- Education

- Healthcare

- Retail

- Legal

- Other End-User Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Kenya

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting structure of the market and to anchor assumptions that can be checked in public data. We reviewed official and open sources such as US SEC filings, US Bureau of Labor Statistics series related to digital workplace roles, Eurostat enterprise ICT usage indicators, OECD digital economy datasets, and cybersecurity and privacy guidance from bodies such as NIST.

Along with those, we referenced company annual reports, product documentation, investor presentations, and credible press coverage to understand pricing logic, delivery models, and adoption signals by customer size. Paid subscriptions were used selectively for company financials and for patent and innovation checks, mainly to verify the direction of product capabilities and M&A timelines. The sources listed above are illustrative only, and additional public and paid sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to test what was learned from desk research, especially around how buyers define a document management system versus adjacent tools, and how spending is split between software and services. We spoke with a mix of solution providers, channel partners, and enterprise and mid-market buyers across APAC, EMEA, and the Americas so assumptions on adoption, deal sizes, and cloud migration timelines could be refined before final modeling.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 13% | APAC: 46% |

| Mid tier: 48% | Functional/Unit leaders: 31% | EMEA: 35% |

| Smaller Players: 22% | Managers: 56% | Americas: 19% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool build where enterprise software spending and digital transformation intensity are mapped to document-centric workflows, then translated into a DMS revenue pool using adoption and replacement rates. To keep the model grounded, results are corroborated with selective bottom-up checks, such as sampled license and subscription price points multiplied by estimated active user volumes, and channel input on typical deal bands by customer size.

Key inputs (illustrative) include the share of enterprises using cloud collaboration and content tools, regulated document retention requirements, the pace of scanning and digitization in paper-heavy functions, cloud versus on-prem deployment mix, and implementation and managed service attach rates. When a bottom-up check has gaps, totals are adjusted using conservative ranges validated in interviews, and the assumption is then applied consistently across regions and end users.

For forecasting, we used scenario analysis supported by simple trend extrapolation on the core drivers, and then stress-tested outcomes with primary feedback on budget cycles, compliance-led buying, and AI-assisted search and classification adoption. When drivers moved in opposite directions, the main clause was kept for the end of the reasoning, so the forecast remains traceable back to the inputs.

Data Validation & Update Cycle

Outputs are checked through triangulation across independent signals, including vendor commentary, public financial disclosures, and adoption indicators from official ICT datasets. Variances are reviewed in multiple steps, starting with unit and currency consistency checks, followed by regional reasonableness tests, and then peer review by another analyst before sign-off.

If a major mismatch is found, the team re-contacts relevant interviewees to confirm whether the issue comes from scope, pricing, or a deployment mix change. Reports are refreshed annually, with interim updates triggered by material events such as large acquisitions, major regulatory changes, or visible pricing resets. Before delivery, a final pass is done so the numbers reflect the latest available public information.

Mordor Intelligence's Document Management Systems Market Size Versus Other Published Estimates

Published market sizes for document management systems often differ because the product boundary is not consistent across studies, and because the base year and currency timing vary by publisher. Differences also show up when some estimates lean more on vendor revenue roll-ups, while others rely more on adoption indicators and buyer-side spend patterns.

Basic file sync and storage tools sit outside Mordor Intelligence's scope for this market, which is a common reason some published totals look lower or higher depending on whether they combine DMS with adjacent collaboration and content tools. Other gaps come from how services are treated (implementation and managed services included versus partially counted), how cloud subscriptions are annualized, and whether the model assumes aggressive AI-driven expansion in average selling prices versus steadier price progression.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 11.81 B (2026) | |

| Global Consultancy A | USD 7.68 B (2024) | Uses a different base year and a narrower revenue capture window, and it can understate services where they are bundled into broader IT transformation contracts rather than tagged to DMS line items. |

| Industry Publisher B | USD 7.16 B (2024) | Press-release figures often reflect a specific segment map and can blend DMS with selected adjacent content tools, and the sizing can be more sensitive to assumed cloud subscription ramp and currency conversion timing. |

The spread in the table is largely explained by what is counted as a DMS, the year used for the snapshot, and how recurring cloud revenues and services are annualized. By keeping scope rules explicit and then cross-checking adoption signals against pricing and deal patterns, the estimate stays balanced and repeatable for planning.

Key Questions Answered in the Report

What is the current value of the document management systems market?

The global market stands at USD 11.81 billion in 2026.

How fast is the document management systems market expected to grow?

It is forecast to expand at a 12.61% CAGR, reaching USD 21.39 billion by 2031.

Why are services growing faster than software in this space?

Migration complexity, AI configuration, and compliance mapping require specialized expertise, driving a 17.21% CAGR for services versus slower license growth.

Which deployment mode is gaining the most traction?

Cloud dominates with 70.34% of 2025 revenue and an 18.34% CAGR, though hybrid models are rising in regulated sectors.

Which industry will be the fastest adopter over the next five years?

Healthcare is projected to rise at a 17.69% CAGR due to telehealth documentation mandates and EHR integration.

Who are the leading vendors in the field?

Microsoft, OpenText, IBM, Hyland, and Oracle collectively control about 45% of global revenue, with Box and Adobe also holding notable positions.

Page last updated on: