Asia-Pacific Enterprise Content Management (ECM) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

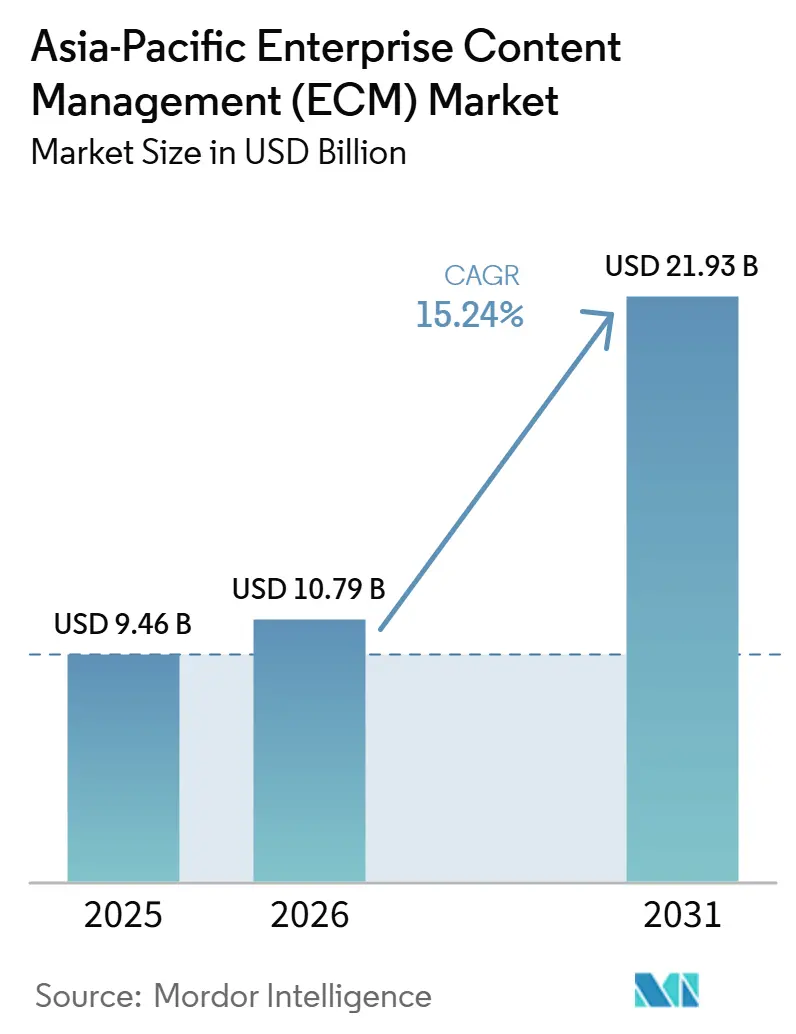

| Base Year Market Size (2025) | USD 9.46 Billion |

| Market Size (2026) | USD 10.79 Billion |

| Market Size (2031) | USD 21.93 Billion |

| Growth Rate (2026 - 2031) | 15.24% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Enterprise Content Management (ECM) Market Analysis by Mordor Intelligence

The Asia-Pacific enterprise content management (ECM) market size is expected to grow from USD 9.46 billion in 2025 to USD 10.79 billion in 2026 and is forecast to reach USD 21.93 billion by 2031 at 15.24% CAGR over 2026-2031. Growth is being sustained by cloud migration, AI-assisted content workflows, and new laws that are turning digital records management into a required capability across many public and regulated settings. Public-sector digitization programs across the region are also raising private-sector standards, as enterprises increasingly need the same auditability, retention controls, and retrieval speed that government buyers now expect. At the same time, the Asia-Pacific enterprise content management (ECM) market is still shaped by operational constraints, especially legacy repository cleanup and country-specific data localization rules that complicate cross-border deployments. Competition remains intense because global suite vendors bring scale and partner reach, while regional providers often move faster on local language support, in-country hosting, and sector-specific compliance needs. This leaves the clearest opportunity for AI-ready platforms to modernize content operations without forcing customers to choose between automation, sovereignty, and controlled migration risk.

Key Report Takeaways

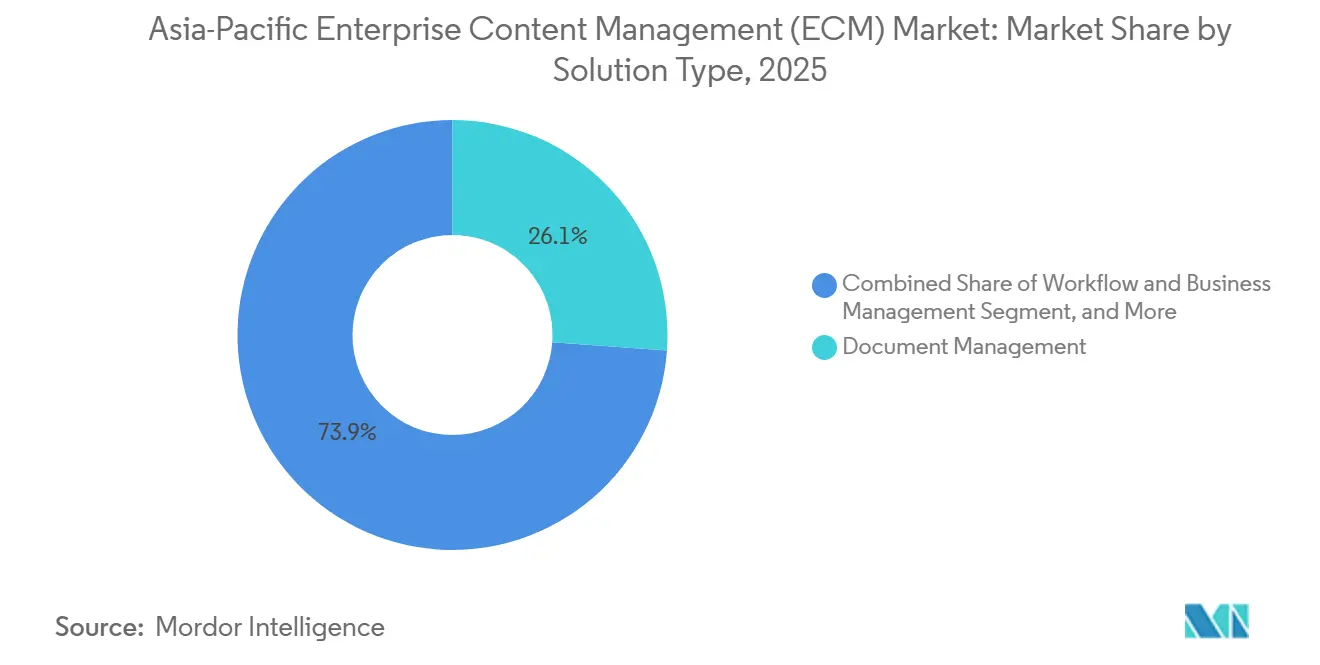

- By solution type, document management accounted for 26.14% of the Asia-Pacific enterprise content management (ECM) market size in 2025, while workflow and business process management is projected to expand at a 17.82% CAGR through 2031.

- By deployment mode, cloud held 73.41% of the Asia-Pacific enterprise content management (ECM) market share in 2025, and cloud is also projected to record the fastest growth at an 18.24% CAGR through 2031.

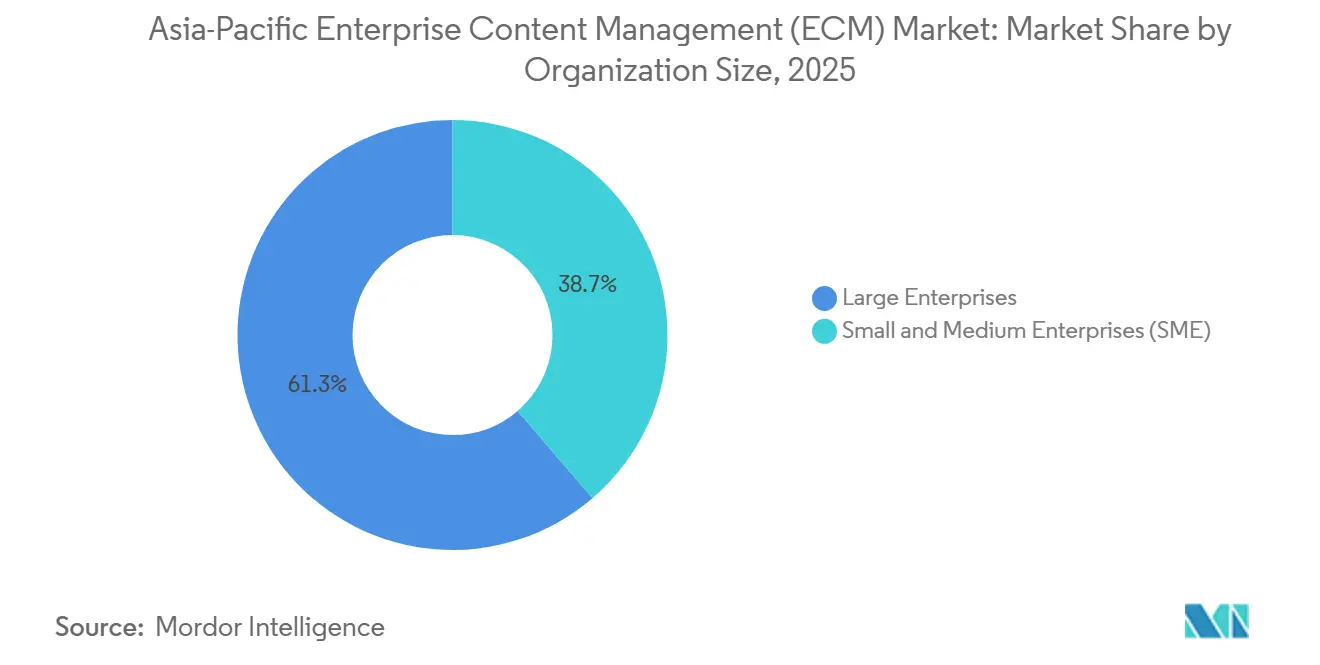

- By enterprise size, large enterprises held a 61.28% share in 2025, while SMEs are projected to expand at a 17.63% CAGR through 2031.

- By end-user industry, BFSI held a 24.53% share in 2025, while healthcare is projected to expand at an 18.41% CAGR through 2031.

- By geography, China held a 36.72% share of the Asia-Pacific enterprise content management (ECM) market in 2025, while India is projected to record the fastest growth at a 17.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Enterprise Content Management (ECM) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-First Content Architecture Modernization | +3.8% | Global, APAC core markets including India, Japan, and Australia | Short term (≤ 2 years) |

| GenAI-Assisted Classification and Search Automation | +3.2% | Global, with early gains in China, India, and South Korea | Short term (≤ 2 years) |

| Regulatory Digitization in Public Sector and Regulated Industries | +2.7% | APAC core markets including China, India, Japan, and Southeast Asia | Medium term (2-4 years) |

| Remote Work and Distributed Knowledge Access Requirements | +2.1% | Global, with strong relevance in APAC urban enterprise hubs | Short term (≤ 2 years) |

| Sovereign Data Residency and Localization Programmes | +1.8% | China, India, and Australia | Medium term (2-4 years) |

| Multilingual Content Operations Across Cross-Border Enterprises | +1.2% | ASEAN and North Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-First Content Architecture Modernization

Cloud adoption is no longer a trial path in the Asia-Pacific enterprise content management (ECM) market, because it has become the default starting point for many new deployments. Microsoft’s cloud investment program in Indonesia was part of a broader regional infrastructure push that encouraged enterprises to move content workflows closer to hyperscaler environments and to adopt AI-enabled productivity tools.[1]Microsoft, “Microsoft To Invest US1.7 Billion In Indonesia To Bring New Cloud And AI Infrastructure, AI Skilling Opportunities, And Support For The Developers Community,” Microsoft News, microsoft.com Japan Business Systems also launched a document management and electronic approval system for local governments in January 2025 that leveraged existing Microsoft 365 licenses, demonstrating how cloud adoption could be expanded without requiring buyers to fund a fully separate stack. In the Asia-Pacific enterprise content management market, this combination of infrastructure expansion and lower-friction procurement is shortening the time between modernization planning and live rollout. It also changes vendor selection because customers increasingly want built-in scalability, faster upgrades, and easier AI integration rather than long hardware refresh cycles. As a result, the Asia-Pacific enterprise content management (ECM) market is moving toward cloud-native operating models even in settings that previously preferred controlled on-premises estates.

GenAI-Assisted Classification and Search Automation

Generative AI is changing the role of platforms in the Asia-Pacific enterprise content management (ECM) market, as customers now expect systems to classify, tag, retrieve, and summarize content rather than simply store it. Microsoft’s SharePoint Embedded program in 2025 showed that ECM functions were being repositioned as AI infrastructure rather than just back-end repositories for document retention.[2]Microsoft, “SharePoint Embedded: Turn Your ECM/DMS Into AI Infrastructure,” Microsoft Community Hub, techcommunity.microsoft.com OpenText followed suit, aligning content management more closely with Microsoft Copilot and Guidewire in its June 2026 release cycle. Hitachi Solutions also upgraded its content lifecycle manager in November 2025 with generative AI-based attribute extraction and retrieval-augmented search, reflecting rising demand for governed search across existing document estates. This is raising the value of platforms that can work well with regional languages, local formats, and regulated workflows without forcing customers to bolt on separate AI tools after deployment. In turn, the Asia-Pacific enterprise content management market is shifting from repository-led buying toward decision support, search quality, and workflow intelligence.

Regulatory Digitization in Public Sector and Regulated Industries

Regulatory digitization is driving the Asia-Pacific enterprise content management (ECM) market forward, as public bodies and regulated enterprises are being asked to standardize records, approval flows, and retrieval practices. China issued GB/T 47229.2-2026 and GB/T 47229.3-2026 in February 2026 for electronic legal documents, signaling a more formal framework for technical requirements and exchange interfaces for official document handling. In Japan, local government digitization also advanced when Japan Business Systems introduced a document management and electronic approval system to lower implementation costs and close the digital transformation gap for municipalities.[3]Hitachi Solutions, “Substantially Reducing Manual Work In Document Management Through Generative AI,” Hitachi Solutions, hitachi-solutions.co.jp The public sector matters in the Asia-Pacific enterprise content management market because compliance-led buying is usually less exposed to short-term discretionary budget cuts than many private-sector projects. Vendors that already meet government security, records, and hosting expectations are therefore in a stronger position to capture repeat procurement cycles. This also means the Asia-Pacific enterprise content management (ECM) market is being shaped by policy calendars as much as by enterprise technology refresh plans.

Remote Work and Distributed Knowledge Access Requirements

Distributed work continues to influence the Asia-Pacific enterprise content management (ECM) market because organizations now need document access, approvals, and version control to work across offices, homes, and mobile settings. KDDI refreshed its company-wide approval workflow system for more than 10,000 employees in 2025 using SmartDB, explicitly tying the project to faster decision-making and a no-code operating model.[4]State Administration For Market Regulation, “GB/T 47229.2-2026 Electronic Documents Of Laws And Regulations, Part 2, Technical Requirements,” KPT Beijing, kpt-bj.com That example matters because the pressure is no longer limited to large headquarters teams, and it now extends to operating units that need faster turnaround on contracts, forms, and internal requests. The Asia-Pacific enterprise content management market is also seeing the effects of shadow repositories because line teams often adopt lightweight cloud tools before compliance functions can standardize them. Vendors with low-code configuration, mobile access, and simple rollout models are therefore better placed to consolidate these scattered document habits into governed workflows. In practical terms, the Asia-Pacific enterprise content management (ECM) market is gaining from remote work not only through top-down strategy, but also through bottom-up pressure to make content usable everywhere.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Repository Migration Complexity | -2.1% | Global, with concentration in Japan, China, and Australia | Medium term (2-4 years) |

| Integration Friction with ERP, CRM, and Line-of-Business Systems | -1.8% | Global, with strong relevance in APAC enterprise hubs | Short term (≤ 2 years) |

| Data Sovereignty Constraints on Cross-Border Cloud Rollouts | -1.5% | China, India, and Southeast Asia | Medium term (2-4 years) |

| ECM Skills Shortage and Implementation Dependency on Specialists | -1.1% | APAC broadly | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy Repository Migration Complexity

Legacy migration remains a significant brake on the Asia-Pacific enterprise content management (ECM) market because many organizations still maintain legacy repositories with weak metadata, inconsistent access rules, and incomplete process records. Research published in the Journal of Computational Analysis and Applications in November 2025 stated that moving low-quality content into cloud systems without governance clean-up can increase compliance risk, weaken AI outputs, and reduce adoption outcomes. That risk is especially important in the Asia-Pacific ECM market because many buyers are trying to modernize and automate simultaneously, leaving less room for a slow preparatory clean-up phase. Migration delays can also change buying behavior, as organizations that expected a platform project sometimes end up funding services, record remediation, and user training before the software's value becomes visible. This makes execution depth almost as important as product capability for vendors competing in large transformation programs. It also means the APAC ECM market can grow more slowly than headline demand suggests, as older repositories are deeper and messier than buyers first assumed.

Integration Friction With ERP, CRM, And Line-Of-Business Systems

Integration friction limits value in the Asia-Pacific ECM market because document systems are most useful when they appear within workflows where work is already being done. OpenText’s June 2026 release placed greater emphasis on Guidewire connectivity and Microsoft Copilot integration, demonstrating how vendors are responding to customer demand for governed content access from core business systems rather than isolated repositories. Newgen’s May 2026 orchestration layer also reflected this pressure, positioning content, processes, and AI logic within a single, managed operating flow rather than treating them as separate layers. The challenge is harder in APAC because enterprises often run mixed software estates that include domestic ERP products, older on-premises systems, and newer SaaS applications simultaneously. That makes region-wide standardization difficult and raises the cost of connector development, testing, and change control. As a result, the Asia-Pacific enterprise content management (ECM) market rewards vendors that bring proven integration assets rather than those that rely on lengthy custom-built projects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Document Management Anchors a Diversifying Portfolio

Document management accounted for 26.14% of the Asia-Pacific enterprise content management (ECM) market in 2025, making it the largest solution category and confirming that centralized repositories remain the foundation of most deployments. This position reflects a simple operational need across the Asia-Pacific enterprise content management industry, since enterprises and public bodies still need secure, searchable storage for large volumes of unstructured files before they can automate anything on top of them. Zhongshan City in China used a centralized document management platform to support more than 34,000 civil servants working on over 600,000 policy documents by 2026, which showed how repository strength can support wider government digitization at scale. Records management, case management, digital asset management, and web content management continue to serve distinct needs, especially when retention rules, case traceability, media handling, or publishing workflows differ across departments or sectors. In the Asia-Pacific ECM market, this means document management remains foundational even as adjacent modules become more specialized.

Workflow and business process management is projected to grow at a 17.82% CAGR from 2026 to 2031, which makes it the fastest-expanding solution category as buyers move from storage toward governed execution. That shift is visible in vendor strategy, as Newgen launched its Enterprise Orchestration Layer in May 2026 to embed AI agents into managed business processes rather than offering them as a separate overlay. The same direction appeared in Japan when Hitachi Solutions enhanced its content lifecycle manager with generative AI extraction and interactive search, both of which support faster action on accumulated document assets. Digital asset management is also gaining relevance in the Asia-Pacific enterprise content management market, where retail, media, and online commerce are placing greater pressure on version control and rapid content reuse. Over time, the category mix is becoming less about isolated point tools and more about how well each solution operates within a broader governance and workflow stack.

By Deployment Mode: Cloud Architecture Reshapes Content Infrastructure

Cloud accounted for 73.41% of the Asia-Pacific enterprise content management (ECM) market in 2025, making it the clear lead deployment model and confirming that new projects typically begin with a cloud-first assumption. In the APAC enterprise content management market, this share reflects more than just greenfield buying, as many customers are now replacing fragmented file servers and aging on-premises repositories with subscription-based platforms that can be continuously updated. Japan’s Air Self-Defense Force deployed Box across more than 47,000 personnel and 73 bases in July 2025, which showed that even security-sensitive institutions were willing to consolidate content operations on a cloud-native platform. The cloud model also aligns with demand for embedded AI, remote access, and lower infrastructure management burden, all of which matter more as content volumes rise. This is why the APAC ECM market increasingly views the cloud not as an alternative, but as the standard operating environment.

Cloud is also projected to expand at a 18.24% CAGR through 2031, indicating it remains the fastest-growing deployment path as existing estates continue to migrate. Hybrid demand remains important in the Asia-Pacific enterprise content management (ECM) market, as some buyers need sensitive records to remain in-country or on controlled infrastructure while workflow and collaboration layers run in the cloud. That pattern is especially relevant where sovereignty rules shape deployment choices more directly than cost comparisons do. It increases delivery complexity but can also boost contract value because vendors must manage policy controls, integration, and ongoing configuration across multiple environments. On-premises systems still play a stable role in defense, intelligence, and judicial workloads that have not fully moved to cloud authorization, so the transition to deployment remains uneven even as the long-term direction is clear.

By Enterprise Size: Large Enterprises Lead as SME Adoption Accelerates

Large enterprises captured 61.28% of revenue in 2025, reflecting heavier content loads, broader compliance requirements, and larger integration footprints that define the upper end of the Asia-Pacific enterprise content management (ECM) market. These organizations usually manage content across multiple countries, business units, and regulated workflows, which makes ECM spending harder to delay than many other software decisions. In the Asia-Pacific enterprise content management industry, large enterprise demand is also reinforced by the need to connect content controls with finance, customer, claims, and internal approval systems at scale. Financial institutions remain a strong example because document governance supports anti-money laundering checks, know-your-customer processing, retention controls, and audit readiness across large user bases. This gives established vendors room to secure multi-year contracts where deployment depth and service capability matter as much as license value.

SMEs are projected to grow at a 17.63% CAGR through 2031, making them the fastest-expanding segment in the Asia-Pacific ECM market. That growth is tied to SaaS pricing and lighter deployment models, since smaller firms can now adopt enterprise-grade controls without taking on the same capital burden that once favored only larger buyers. SMEs in APAC also face multilingual and cross-border document needs that are often more complex than their size suggests, especially when they work with suppliers, buyers, or regulators across multiple jurisdictions. Fasoo AI launched Wrapsody Core in July 2026 as an AI-ready document centralization platform that aligns with this shift toward lighter, yet still governed, adoption models. The result is that the Asia-Pacific enterprise content management (ECM) market is expanding downward into smaller accounts, but success still depends on simple deployment, local-language usability, and integration with existing security tools.

By End-User Industry: BFSI Leads While Healthcare Drives The Fastest Growth

BFSI held 24.53% of the Asia-Pacific enterprise content management (ECM) market in 2025, making it the largest end-user segment, as document control in banking and insurance is directly tied to compliance execution. Loan origination, know-your-customer files, claims handling, trade documentation, and audit trails all require retention discipline and access controls that make ECM a core operating layer rather than a supporting tool. The APAC ECM market, therefore, sees steady BFSI demand even when broader software spending is uneven, because regulated financial workflows cannot function effectively without robust record governance. Certifications such as ISO 27001 and SOC 2 Type II have also become more important in vendor review processes, which strengthens the position of suppliers already trusted in regulated settings. This gives the segment a stable demand base and helps explain why incumbency matters more in BFSI than in many other end-user groups.

Healthcare is projected to expand at a 18.41% CAGR through 2031, making it the fastest-growing end-user segment in the Asia-Pacific enterprise content management (ECM) market. Growth is supported by broader electronic health record adoption, interoperability needs, and the rising need to organize clinical and administrative records in a single, governed environment. That creates demand for platforms that can manage both structured and unstructured content while still supporting retrieval, privacy, and version control in daily care workflows. Government and public sector, IT and telecommunications, manufacturing, retail, media and entertainment, education, and energy and utilities also remain important demand pools because each uses ECM for a different operational purpose. Manufacturing and energy are notable because engineering documents and asset lifecycle records depend on precision retrieval and revision control, which keeps the APAC ECM market relevant far beyond office document use alone.

Geography Analysis

China accounted for 36.72% of the Asia-Pacific enterprise content management (ECM) market in 2025, making it the largest national market in the region by a clear margin. That position reflects long-running state-backed digitization programs and a domestic vendor base that operates effectively within strict localization expectations. China’s policy environment also pushes multinational firms toward in-country content stacks, limiting the practicality of a single regional deployment model and strengthening local delivery requirements. China added to that structure in February 2026 when it published GB/T 47229.2-2026 and GB/T 47229.3-2026 for electronic legal documents, with implementation scheduled for September 2026. Japan remains a major market because workforce pressure is making document automation harder to defer, and the 2025 Box deployment across the Air Self-Defense Force showed that cloud content platforms can now support security-sensitive operations at scale.

India is projected to record a 17.94% CAGR through 2031, which gives it the fastest growth profile in the region and the strongest expansion rate in the APAC enterprise content management market. Its growth path differs because it combines a large SME digitization opportunity with regulatory-driven changes in data handling. Localization requirements are encouraging hybrid content architectures that keep sensitive data inside national boundaries while still allowing workflow and collaboration layers to scale. South Korea has a different demand pattern because its mobile-ready enterprise environment and structured approval culture support the rapid adoption of governed content tools. Fasoo AI’s July 2026 launch of Wrapsody Core showed how domestic suppliers in South Korea are positioning around AI-readiness and rights-managed document control rather than competing only on basic storage capability.

Australia stands out for its records management frameworks, and national and state public bodies continue to set clear expectations for retention, control, and the handling of official documents. That structure keeps public-sector procurement active and increases the value of vendors that can deliver certified or policy-aligned configurations. The Rest of Asia-Pacific is moving from isolated pilots to broader adoption as digital government programs, formal enterprise activity, and improved cloud access spread across Southeast Asia, widening the addressable base of the APAC ECM market. As a result, the APAC enterprise content management market is becoming more geographically distributed, even though revenue remains concentrated in the largest economies.

Competitive Landscape

The Asia-Pacific enterprise content management (ECM) market has a layered competitive structure in which a small set of global platform vendors competes at the high end, while regional specialists excel in localization, hosting control, and faster execution. OpenText, Microsoft, and IBM remain important in larger enterprise and public-sector bids because they bring broad suites, partner ecosystems, and long experience with regulated information management. OpenText reinforced that position in February 2025 when it announced plans to add 2,500 people across APAC over three years and expand centers of excellence in research, professional services, and operations across major regional markets. In the Asia-Pacific enterprise content management market, such regional investment matters because customers often judge execution capacity as carefully as product breadth. It also raises the competitive bar for smaller vendors that may have strong products but thinner delivery networks.

Product strategy is also shifting quickly in the Asia-Pacific ECM market, as buyers want AI, workflow, and governance to work as a single operating layer. OpenText’s June 2026 Content Management CE 26.2 release expanded Microsoft Copilot integration and Guidewire connectivity, which showed how large vendors are tightening the link between content control and core business execution. Newgen moved in a similar direction in May 2026, introducing its Enterprise Orchestration Layer to position content and process management within a broader AI execution framework. Regional vendors are also finding room by solving narrower but harder problems, especially where language support, deployment sovereignty, or sector-specific workflows make generic suites less effective. This is why the APAC enterprise content management market still leaves white space at both ends: lightweight, SME-focused offerings and highly specialized platforms built for regulated document environments.

The competitive field remains fragmented because no single vendor narrative fits every country, hosting rule, and enterprise maturity level across APAC. Strategic moves such as OpenText’s regional capacity build-out, Box’s government-grade cloud deployment in Japan, and Fasoo AI’s AI-ready document centralization launch show that vendors are competing through delivery scale, trust, and product architecture rather than through price alone. Patent activity and platform convergence also suggest that the line between ECM, document intelligence, and process automation will continue to narrow. As that happens, the Asia-Pacific ECM market will likely see more partnership activity and targeted acquisitions from vendors seeking faster access to AI-native and region-specific capabilities.

Asia-Pacific Enterprise Content Management (ECM) Industry Leaders

Microsoft Corporation

OpenText Corporation

IBM Corporation

Hyland Software, Inc.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: OpenText released Content Management CE 26.2, introducing expanded AI-enabled Microsoft Copilot integration and Guidewire connector functionality, enabling regulated industries to access governed document workflows directly from their core business systems. The release is part of an 18-month AI roadmap unveiled at OpenText World 2025.

- January 2026: Box, Inc. announced the general availability of Box Extract, an AI-powered metadata extraction capability powered by generative AI models from Google, Anthropic, and OpenAI, combined with agentic orchestration features. Box Extract enables enterprises to convert unstructured content into structured, workflow-ready metadata at scale, directly addressing the classification and search automation gap in legacy ECM workflows.

- November 2025: OpenText unveiled its AI Data Platform (AIDP) at OpenText World 2025, an open, unified framework with a governance orchestration layer enabling AI agents to operate on enterprise content. The platform introduced an 18-month release roadmap and expanded integrations with SAP, Microsoft, Google, Salesforce, and Oracle, reinforcing OpenText's position in regulated enterprise markets across APAC.

- July 2025: apan's Ministry of Defense Air Self-Defense Force deployed Box for secure cloud content management across over 47,000 personnel spanning 73 bases. The deployment consolidates fragmented on-premises file servers across all bases under a centralized cloud content platform, with Box's ISMAP registration and FedRAMP High certification satisfying Japan's government cloud security requirements.

Asia-Pacific Enterprise Content Management (ECM) Market Report Scope

The Asia-Pacific enterprise content management (ECM) market comprises software solutions and services that systematically capture, manage, store, preserve, and deliver an organization's unstructured and structured content and documents. This includes technologies such as document management, records management, workflow, business process management, case management, digital asset management, and web content management. Deployed on-premises, in the cloud, or in hybrid models, these solutions cater to organizations of all sizes across diverse industries in the region, including BFSI, government, healthcare, manufacturing, and retail. Driven by rapid digital transformation, increasing data volumes, and stringent regulatory compliance requirements across APAC, ECM solutions enable businesses to streamline operations, enhance collaboration, ensure data security, and reduce reliance on manual, paper-based processes, thereby improving overall productivity and decision-making.

The Asia-Pacific Enterprise Content Management (ECM) Market Report is Segmented by Solution Type (Document Management, Records Management, Workflow and Business Process Management, Case Management, Digital Asset Management, Web Content Management, and Other Solutions), Deployment Mode (On-Premises, Cloud, and Hybrid), Enterprise Size (Small and Medium Enterprises (SME), and Large Enterprises), End-User Industry (BFSI, Government and Public Sector, Healthcare, IT and Telecommunications, Manufacturing, Retail, Media and Entertainment, Education, Energy and Utilities, and Other End-User Industries), and Geography (China, Japan, India, South Korea, Australia, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Document Management |

| Records Management |

| Workflow and Business Process Management |

| Case Management |

| Digital Asset Management |

| Web Content Management |

| Other Solutions |

| On-Premises |

| Cloud |

| Hybrid |

| Small and Medium Enterprises (SME) |

| Large Enterprises |

| BFSI |

| Government and Public Sector |

| Healthcare |

| IT and Telecommunications |

| Manufacturing |

| Retail |

| Media and Entertainment |

| Education |

| Energy and Utilities |

| Other End-User Industries |

| China |

| Japan |

| India |

| South Korea |

| Australia |

| Rest of Asia-Pacific |

| By Solution | Document Management |

| Records Management | |

| Workflow and Business Process Management | |

| Case Management | |

| Digital Asset Management | |

| Web Content Management | |

| Other Solutions | |

| By Deployment Mode | On-Premises |

| Cloud | |

| Hybrid | |

| By Enterprise Size | Small and Medium Enterprises (SME) |

| Large Enterprises | |

| By End-User Industry | BFSI |

| Government and Public Sector | |

| Healthcare | |

| IT and Telecommunications | |

| Manufacturing | |

| Retail | |

| Media and Entertainment | |

| Education | |

| Energy and Utilities | |

| Other End-User Industries | |

| By Geography | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current and forecast value of the Asia-Pacific enterprise content management (ECM) market?

The Asia-Pacific enterprise content management (ECM) market was valued at USD 9.46 billion in 2025, stands at USD 10.79 billion in 2026, and is forecast to reach USD 21.93 billion by 2031 at a 15.24% CAGR.

Which solution category leads revenue in Asia-Pacific ECM?

Document management led with a 26.14% share in 2025 because centralized and searchable repositories still form the base of most enterprise and public-sector deployments.

Which deployment model is growing fastest across APAC?

Cloud leads deployment with a 73.41% share in 2025 and is also the fastest-growing model with an 18.24% CAGR through 2031.

Why is BFSI the largest end-user group for enterprise content management in APAC?

BFSI held 24.53% of revenue in 2025 because lending, claims, trade, and compliance processes depend on controlled records, retention rules, and audit-ready document access.

Which country is driving the fastest expansion in the region?

India is projected to grow at a 17.94% CAGR through 2031, supported by SME digitization and stronger focus on localized data handling frameworks.

What is changing competition among ECM vendors in Asia-Pacific?

Competition is shifting toward AI-ready workflows, integration depth, and local hosting strength, which is why both global suite vendors and regional specialists remain relevant in the region.

Page last updated on: