HR Tech Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 47.51 Billion |

| Market Size (2031) | USD 77.74 Billion |

| Growth Rate (2026 - 2031) | 10.35% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

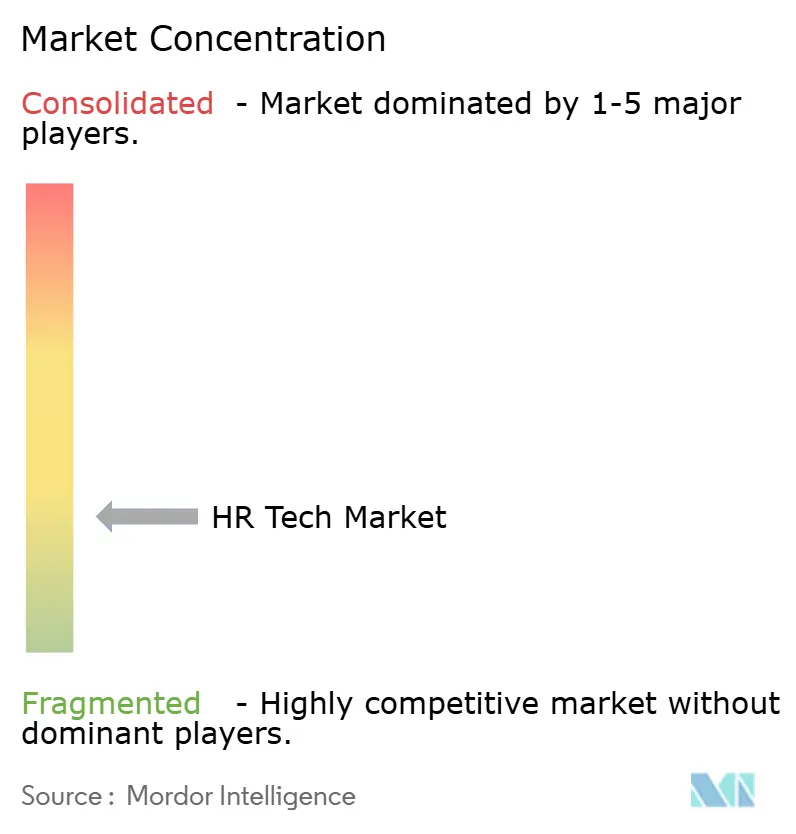

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

HR Tech Market Analysis by Mordor Intelligence

The HR Tech Market size is projected to expand from USD 42.34 billion in 2025 and USD 47.51 billion in 2026 to USD 77.74 billion by 2031, registering a CAGR of 10.35% between 2026 to 2031. Strong demand for data-rich talent insights, escalating ESG disclosure mandates, and the shift to distributed work are moving purchasing decisions away from basic automation toward advanced analytics and generative-AI features. Cloud platforms keep deployment cycles short, while regulators in the European Union and the United States elevate human-capital metrics to the same compliance tier as financial reporting. Incumbent HCM suites face pressure from vertical specialists that focus on single pain points such as global payroll compliance, mental-health benefits, or internal skill marketplaces. Cyber-security diligence now sits at the top of vendor shortlists, underscoring a wider board-level focus on data stewardship.

Key Report Takeaways

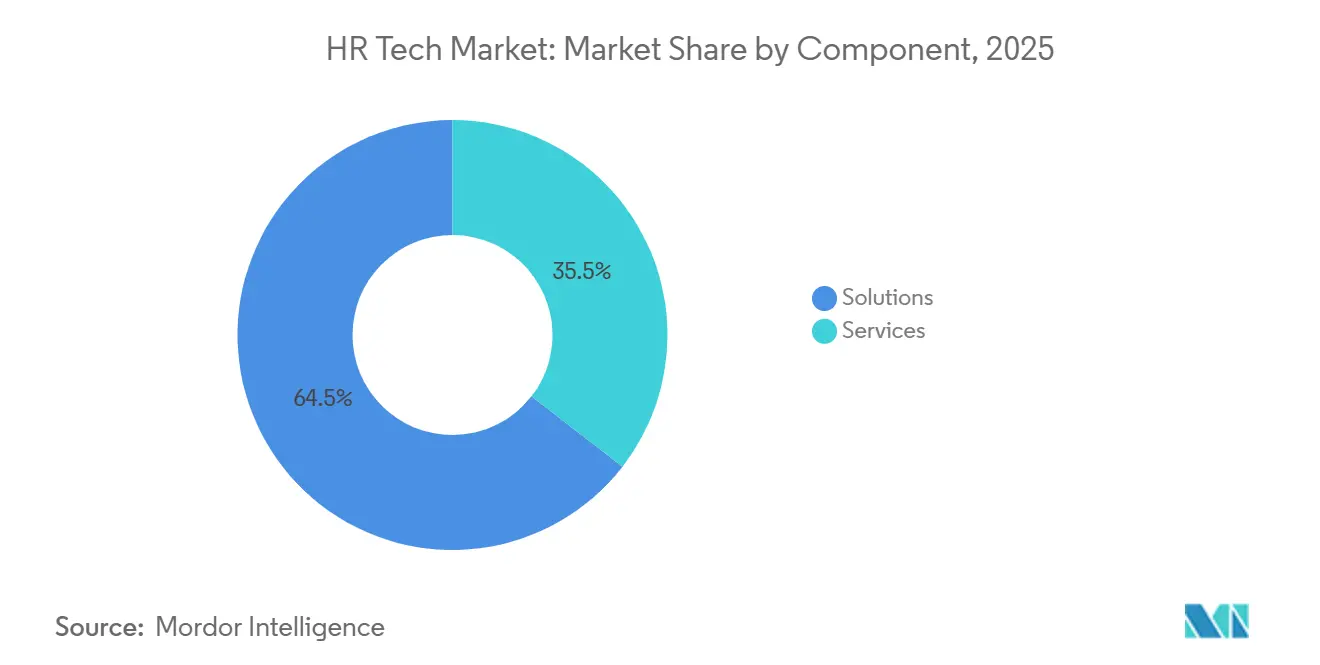

- By component, solutions led with 64.5% revenue share in 2025 and are advancing at a 12.21% CAGR through 2031.

- By deployment mode, cloud platforms held 88.2% of the HR tech market share in 2025, while the same segment is accelerating at a 12.56% CAGR through 2031.

- By organization size, large enterprises captured 58.1% of spending in 2025, yet small and medium enterprises represent the fastest growth at a 12.34% CAGR.

- By application, payroll management accounted for 26.2% of the HR tech market size in 2025, and employee wellness and benefits administration applications are expanding at a 12.34% CAGR through 2031.

- By end user, IT and telecom delivered 23.8% of 2025 revenue, whereas healthcare and life sciences are growing at a 12.43% CAGR.

- By geography, North America commanded 45.8% of 2025 revenue, but Asia-Pacific is on track for the highest regional CAGR at 12.54% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global HR Tech Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Cloud-Based HR Platforms for Scalability | 3.2% | Global, strongest in North America and Asia-Pacific | Short term (≤ 2 years) |

| Digital Transformation of HR Functions | 2.8% | Global, with North America and Europe leading adoption | Medium term (2-4 years) |

| AI-Driven Internal Talent-Marketplace and Skills Platforms | 2.1% | North America, Asia-Pacific core (India, Singapore), spill-over to Europe | Medium term (2-4 years) |

| Growing Demand for Automation and Streamlining Processes | 1.9% | Global, particularly strong in the manufacturing and retail sectors | Short term (≤ 2 years) |

| ESG and Human-Capital Disclosure Mandates | 1.5% | Europe (CSRD), North America (SEC proposals), and emerging in Asia-Pacific | Long term (≥ 4 years) |

| Hybrid/Remote Work Models Boosting Engagement Tools | 1.2% | North America and Europe, expanding to Asia-Pacific urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital Transformation of HR Functions

Enterprises are extending supply-chain-grade data discipline to people processes, replacing siloed spreadsheets with unified dashboards that support predictive workforce planning. Core HCM, payroll, and performance data now feed algorithms that flag attrition risks and skill gaps in real time, allowing managers to rebalance teams before productivity dips. Adoption is most visible in technology-intensive industries where certifications and project allocations change quickly. The ISO 30414 framework provides a common metric set for turnover, diversity, and training, guiding both vendors and employers toward standardized reporting[1]ISO, “ISO 30414:2018 Human Resource Management,” iso.org . Leading platforms expose open APIs that integrate HR data with finance and supply-chain systems, setting a foundation for cross-functional analytics that senior management can act upon quickly.

AI-Driven Internal Talent-Marketplace and Skills Platforms

Machine-learning models map verified skills to open projects, prompting employees to apply for short-term gigs that sharpen capabilities while meeting urgent business needs. Workday embedded this functionality by acquiring HiredScore in 2025, and early adopters report quicker redeployment of existing staff. Vertical specialist Eightfold AI has achieved roughly one-third reductions in time-to-fill for clients by prioritizing internal candidates. Skills-based assignments appeal to cost-sensitive employers seeking to curb external recruiting costs and to employees seeking career mobility without leaving the company. Cultural norms still temper uptake in countries where seniority heavily influences promotion decisions, but a gradual shift toward merit-based progression is underway.

Shift Toward Cloud-Based HR Platforms for Scalability

Hybrid work cemented a requirement for anytime, anywhere access to payroll, benefits, and learning modules. Vendors such as SAP SuccessFactors note that nearly four-fifths of their 2025 customer additions opted for cloud-only deployments[2]SAP, “Human Capital Management,” sap.com. Subscription economics eliminate capital expenditure, shorten implementation cycles, and transfer patch management to the vendor. Multi-cloud strategies are common in heavily regulated industries: sensitive data stay on private clouds, while less-regulated workloads run on multi-tenant SaaS to capture cost benefits. Start-ups like Gusto showcase pay-as-you-grow models that average under USD 10 per employee each month, popularizing sophisticated HR functionality among resource-constrained SMEs.

ESG and Human-Capital Disclosure Mandates

The European Union’s Corporate Sustainability Reporting Directive obliges large companies to document workforce composition, pay equity, and training hours in audited statements, elevating HR data to board-level scrutiny. Similar rules are moving through the U.S. Securities and Exchange Commission. In response, major suites now ship ESG dashboards that aggregate diversity ratios, voluntary turnover, and corporate travel emissions. Audit-ready trails increase platform stickiness because once data governance policies are embedded, switching vendors becomes costly and risky. Small and mid-cap firms face phased compliance dates through 2028, creating a multi-year runway for HR analytics modules tailored to disclosure workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy and Cyber-Security Concerns | -1.8% | Global, most acute in Europe (GDPR) and North America (state laws) | Short term (≤ 2 years) |

| Integration Complexity and Data Silos | -1.3% | Global, particularly in enterprises with legacy ERP systems | Medium term (2-4 years) |

| High Upfront Cost and Change-Management Hurdles | -0.9% | Global, most pronounced in SMEs and public-sector organizations | Medium term (2-4 years) |

| Vendor Consolidation Risk and Lock-In | -0.7% | North America and Europe, where vendor concentration is highest | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Cyber-Security Concerns

HR databases hold compensation details, health records, and performance reviews, making them prime ransomware targets. The United Kingdom’s Information Commissioner’s Office registered a double-digit increase in breaches tied to HR systems during 2024[3]UK Information Commissioner’s Office, “UK GDPR Guidance and Resources,” ico.org.uk. GDPR and newer U.S. state laws require vendors to enable data portability and granular consent, adding engineering overhead and slowing feature releases. Procurement teams now demand SOC 2 Type II and ISO 27001 certifications, effectively raising the barrier to entry for smaller providers. Fines for non-compliance can reach 4% of global revenue in the European Union, prompting multinational firms to add data-residency clauses to service contracts.

Integration Complexity and Data Silos

Many manufacturers, hospitals, and public agencies still run ERP versions that pre-date modern API standards. HR suites must therefore interface through nightly batch files, delaying analytics and inflating IT labor costs. Vendors are shipping pre-built connectors and integration marketplaces: Workday launched more than 400 certified connectors in 2025, while UKG embedded iPaaS functions into its workforce-management suite. Even so, custom workflows in regulated sectors often require tailored bridges that stretch project timelines beyond one year and divert budgets from new functionality. Until legacy ERP deployments sunset, integration friction will dampen the pace of HR tech market upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Extend Feature Depth While Services Contract

The HR tech market size allocated 64.5% of 2025 revenue to software solutions, a slice that is widening at a 12.21% CAGR through 2031. Growth centers on modular SaaS architectures that let clients toggle on payroll, recruiting, analytics, or wellness with minimal configuration. Self-service deployment wizards from BambooHR and Rippling enable seven in ten customers to go live without outside consultants, removing cost barriers for new adopters. A swelling pipeline of AI layers, such as talent-marketplace algorithms and generative-content engines, keeps refresh cycles brisk.

Services take the remaining share, but their growth lags as platform vendors bake configuration templates, regulatory updates, and user-education content directly into the product. Outsourcing retains relevance for complex global payroll or merger-driven data harmonization, yet margins are tightening. Implementation partners are pivoting toward strategic change-management engagements rather than transactional configuration work, which is increasingly automated.

By Deployment Mode: Cloud Dominance Reshapes Economics

Cloud models controlled 88.2% of the HR tech market share in 2025 and are racing ahead at a 12.56% CAGR to 2031. Multi-tenant SaaS delivers quarterly updates, ensuring rapid compliance with new labor laws and tax tables in multiple jurisdictions. Ceridian’s Dayforce, for instance, automatically applies payroll-tax changes, saving customers from manual maintenance cycles.

On-premise deployments persist in defense, public safety, and certain financial institutions that face strict data-sovereignty rules. Vendors have responded with private-cloud and hybrid options that mimic SaaS economics while meeting audit demands. Still, R&D dollars overwhelmingly favor cloud-native functionality, so feature gaps between deployment modes are widening and reinforcing the market shift toward cloud subscriptions.

By Organization Size: SMEs Benefit from Bundled SaaS

Large enterprises still generate 58.1% of billings in 2025, chiefly through multi-year global HCM deals with Workday, Oracle, and SAP. Consolidation of point solutions onto unified suites is the dominant theme as CIOs chase lower integration overhead.

SMEs, however, log the strongest 12.34% CAGR as vendors craft all-in-one bundles that blend payroll, benefits, and IT provisioning within a single per-employee fee. Gusto and BambooHR promise same-day onboarding that auto-configures tax withholdings and benefit enrollments. Lower up-front costs and rapid go-live dates attract professional-services firms, retail chains, and hospitality providers with thin IT staffs. This democratization of enterprise-grade HR functionality unlocks an enormous long-tail growth opportunity for the HR tech market.

By Application: Wellness and Benefits Administration Surpass Core Payroll Growth

Payroll retained the largest revenue pool at 26.2% in 2025, mirroring its high regulatory burden. Yet employee-wellness and benefits-administration modules are expanding at a 12.34% CAGR, reflecting corporate commitments to mental health. Oracle folded third-party meditation and therapy apps into its suite during 2025, broadening the definition of employee experience.

Generative-AI tools inside recruitment suites such as Greenhouse draft job posts and interview guides, lightening recruiter workloads. Talent management is blurring into learning and performance as continuous feedback replaces annual reviews. Workforce management applications stay critical in shift-driven sectors that need real-time scheduling and overtime forecasting. Finally, analytics modules are gaining traction because executives want the same data rigor for people decisions that they apply to capital allocation, pulling users toward integrated dashboards.

By End User: Healthcare and Life Sciences Take the Growth Lead

IT and telecom companies accounted for 23.8% of 2025 outlays, driven by rapid innovation cycles that require continuous skill development. Healthcare and life sciences, however, record the highest 12.43% CAGR thanks to chronic nurse shortages and rigid credential-tracking mandates. UKG’s AI-driven shift-bid optimizer helped hospital groups curb overtime by almost one-fifth in 2025.

Retail and e-commerce platforms emphasize applicant-tracking systems able to screen and onboard hundreds of seasonal workers within weeks. Manufacturers adopt workforce-planning tools that sync shop-floor data with labor availability, cutting unplanned downtime. The public-sector and education segments lag due to procurement complexity, yet cloud adoption is rising as governments roll out digital service agendas that require modern talent systems.

Geography Analysis

North America generated 45.8% of 2025 revenue, riding mature U.S. adoption and state-level pay-transparency laws that nudge employers toward real-time compensation analytics. Canada bolsters regional totals through provincial labor-law digitization, while Mexico’s near-shoring boom draws multinationals that deploy unified payroll engines to manage maquiladora labor pools.

Asia-Pacific is the fastest-growing region at a 12.54% CAGR. India’s Digital India program, China’s labor-law modernization, and ASEAN directives for cross-border payroll interoperability form a conducive policy backdrop. Darwinbox capitalized on this momentum by reaching unicorn valuation in 2025 and rolling out localized compliance modules across Southeast Asia.

Europe’s outlook is defined by GDPR stringency and the Corporate Sustainability Reporting Directive. Germany, France, and the United Kingdom lead purchasing activity as works councils gradually accept cloud deployments that respect data-residency norms. In the Middle East and Africa, Saudi Arabia and the United Arab Emirates fast-track HR modernization under Vision 2030, whereas South Africa, Nigeria, and Egypt represent early-stage hotspots amid bandwidth and currency constraints.

Competitive Landscape

The HR tech market remains moderately fragmented as the top five suppliers, Workday, SAP, Oracle, ADP, and UKG, capture roughly 35% of global revenue, leaving ample headroom for niche innovators. Suite vendors pitch unified data models that lower integration friction, whereas best-of-breed players tout feature depth in domains like global payroll or talent intelligence. Workday’s 2025 acquisitions of HiredScore and Evisort demonstrate a land-and-expand tactic that embeds AI models deeper into customer workflows and raises switching costs.

Specialists such as Eightfold AI and Deel chip away at discrete pain points, skills inference and multi-country contractor payments, often landing in one department before radiating outward. Generative-AI functionality is becoming table stakes: SAP’s Joule assistant, Ceridian’s tax-update automation, and Oracle’s wellness plug-ins illustrate a race to convert large language models into routine HR actions. Cybersecurity certifications, once differentiators, are now minimum thresholds as enterprise buyers elevate data governance in vendor scorecards.

Partnerships are redrawing ecosystem boundaries. Microsoft’s Viva integrations layer engagement analytics onto existing collaboration suites, while Salesforce pushes CRM data into employee-experience modules, signaling convergence between HR, IT, and revenue platforms. The resulting landscape rewards vendors that can interoperate gracefully while maintaining robust domain expertise.

HR Tech Industry Leaders

ADP Inc.

Oracle

SAP HR Solutions (SAP HR)

UKG INC.

HI BOB INC.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Ceridian reported processing more than USD 200 billion in global payroll across 5 million employees, attributing growth to automated compliance updates.

- November 2025: Oracle expanded its Oracle ME platform to include mental-health and wellness modules that integrate third-party meditation, therapy, and financial-planning apps.

- October 2025: Rippling extended its global payroll engine to cover contractor payments in 150 countries, automating tax withholding and compliance checks.

- August 2025: Greenhouse rolled out generative-AI tools that write job descriptions and propose interview questions, cutting recruiter workload by one-third.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the HR technology market as the total global spend on packaged software and related cloud services that digitize core HR, payroll, talent acquisition, performance, learning, analytics, and workforce management workflows. Deployment models span public-cloud, private-cloud, hybrid, and licensed on-premise environments, and the model tracks revenue booked from new licenses, subscriptions, and mandatory support renewals during the calendar year.

Hardware peripherals, pure professional staffing services, and stand-alone collaboration or ERP modules not marketed for HR use are outside this scope.

Segmentation Overview

- By Component

- Solutions

- Core HR / HCM

- Payroll and Compliance

- Talent Acquisition (ATS, CRM)

- Talent/Performance Management

- Workforce Management

- Learning and Development / LMS

- Employee Experience / Engagement Platforms

- HR Analytics and People Insights

- Services

- HR Outsourcing (BPO)

- Implementation and Integration

- Managed and Support Services

- Consulting and Advisory

- Solutions

- By Deployment Mode

- Cloud (SaaS, PaaS, Hybrid)

- On-Premise

- By Organization Size

- Small and Medium Enterprises

- Large Enterprises

- By Application

- Payroll Management

- Talent Management

- Recruitment and ATS

- Workforce Management

- Performance and Engagement

- Learning and Development

- Analytics and Reporting

- Employee Wellness and Benefits Administration

- By End User

- BFSI

- IT and Telecom

- Healthcare and Life Sciences

- Public Sector and Education

- Manufacturing

- Retail and E-commerce

- Hospitality and Tourism

- Professional Services

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts scheduled structured interviews with HR software product managers, implementation partners, and CHROs across North America, Europe, and Asia Pacific. These conversations tested adoption assumptions, average contract values, and cloud migration timelines, letting us refine model variables and reconcile desk findings.

Desk Research

We began by mining open statistics from bodies such as the International Labor Organization, UN Comtrade, and national statistics portals that release employer counts, average wages, and ICT spend. Trade groups such as the HR Open Standards Consortium, SHRM, and Eurostat ICT surveys supplied adoption ratios by company size, while company filings on EDGAR and regional registries revealed product revenue splits and pricing clues. Subscription databases, D&B Hoovers for vendor financials and Dow Jones Factiva for deal trackers, helped cross-check growth narratives. This list is illustrative; many additional public and proprietary documents underpinned data collection and clarification.

Market-Sizing & Forecasting

We use a top-down build that scales employment and ICT spend pools, applies HR-software penetration rates, and adjusts for average subscription price trends. Select bottom-up checks, supplier channel reads and sampled price × seat counts, inform calibration. Key model levers include global employee headcount growth, the portion of enterprises running cloud HR suites, average per-employee subscription rates, implementation cost deflators, regulatory reporting mandates, and AI-driven upsell premiums. A multivariate regression links these drivers to historic vendor revenue patterns, then an ARIMA overlay projects five-year trajectories. Data gaps in vendor disclosures are bridged by interpolating peer averages vetted through expert calls.

Data Validation & Update Cycle

Outputs pass variance tests against independent spending trackers and quarterly earnings signals. Senior reviewers interrogate anomalies before sign-off. The dataset refreshes yearly, with interim tweaks whenever large acquisitions, regulatory shifts, or price shocks occur, so clients always receive our latest view.

Why Mordor's HR Tech Baseline Stands Up to Scrutiny

Estimates from different publishers often diverge because each firm selects unique segment mixes, price assumptions, and refresh cadences.

Key gap drivers include whether services revenue is folded in, how cloud price erosion is treated, and the year chosen as a baseline. Mordor's model locks scope early, weights regional adoption evidence more heavily than aspirational vendor targets, and resets currency conversions at purchasing-power parity, which moderates extremes seen elsewhere.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 42.5 B (2025) | Mordor Intelligence | - |

| USD 40.1 B (2024) | Global Consultancy A | Excludes learning platforms; uses constant FX rates |

| USD 38.99 B (2025) | Industry Association B | Omits services revenue and hybrid deployments |

| USD 40.45 B (2024) | Regional Consultancy C | Applies uniform 9% CAGR without vendor cross-checks |

In sum, our disciplined variable selection and annual reality checks give decision-makers a balanced, transparent baseline they can trace back to clear workforce and pricing metrics.

Key Questions Answered in the Report

How large is the HR tech market in 2026?

The HR tech market size reached USD 47.51 billion in 2026 and is forecast to grow at a 10.35% CAGR to 2031.

Which deployment model is growing fastest within HR tech?

Cloud platforms lead the growth curve, accounting for 88.2% of 2025 revenue and advancing at a 12.56% CAGR.

Why are wellness modules expanding quickly in HR systems?

Employers view mental-health support as a core retention tool, which drives a 12.34% CAGR for wellness and benefits administration applications.

Which region shows the highest growth rate for HR technology adoption?

Asia-Pacific posts the fastest regional expansion at a 12.54% CAGR, propelled by digital-government initiatives and labor-law modernization.

Page last updated on: