Healthy Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.05 Trillion |

| Market Size (2031) | USD 1.67 Trillion |

| Growth Rate (2026 - 2031) | 9.76% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthy Food Market Analysis by Mordor Intelligence

The healthy food market size was valued at USD 0.95 trillion in 2025 and estimated to grow from USD 1.05 trillion in 2026 to reach USD 1.67 trillion by 2031, at a CAGR of 9.76% during the forecast period (2026-2031). Preventive nutrition has moved closer to an everyday spending priority as obesity, diabetes, and diet-related disease concerns have become more visible in public health policy and household choices across major economies. The healthy food market is also benefiting from tighter product qualification standards, especially after the U.S. FDA updated the voluntary healthy claim rule in December 2024 and aligned qualification more closely with limits on added sugars, saturated fat, and sodium. The rise in GLP-1 weight-loss medication use is reshaping product development across the healthy food market, as food makers are now building more protein-rich, fiber-rich, and micronutrient-dense formats to address muscle maintenance and appetite management needs. The healthy food market also continues to attract investment, as digital retail, direct-to-consumer nutrition models, and faster reformulation cycles help brands reach consumers more efficiently across premium and mass channels. Even so, raw material cost inflation, the persistent price premium for healthier diets over ultra-processed foods, and tighter enforcement of health claims remain important constraints on margin expansion and mass adoption in the healthy food market.

Key Report Takeaways

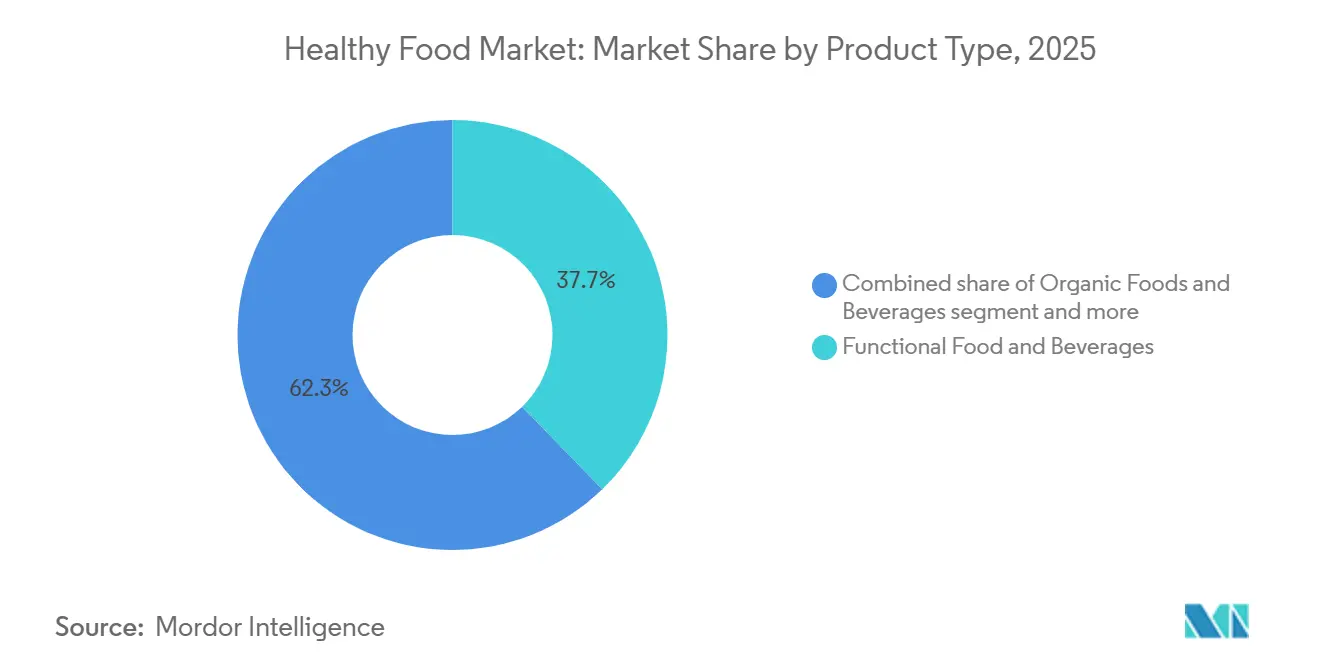

- By product type, functional foods and beverages led with a 37.73% share in 2025, while organic foods and beverages are projected to expand at a 11.67% CAGR through 2031.

- By category, non-vegetarian held 43.56% of the healthy food market share in 2025, while vegan is expected to record the highest projected CAGR at 10.75% through 2031.

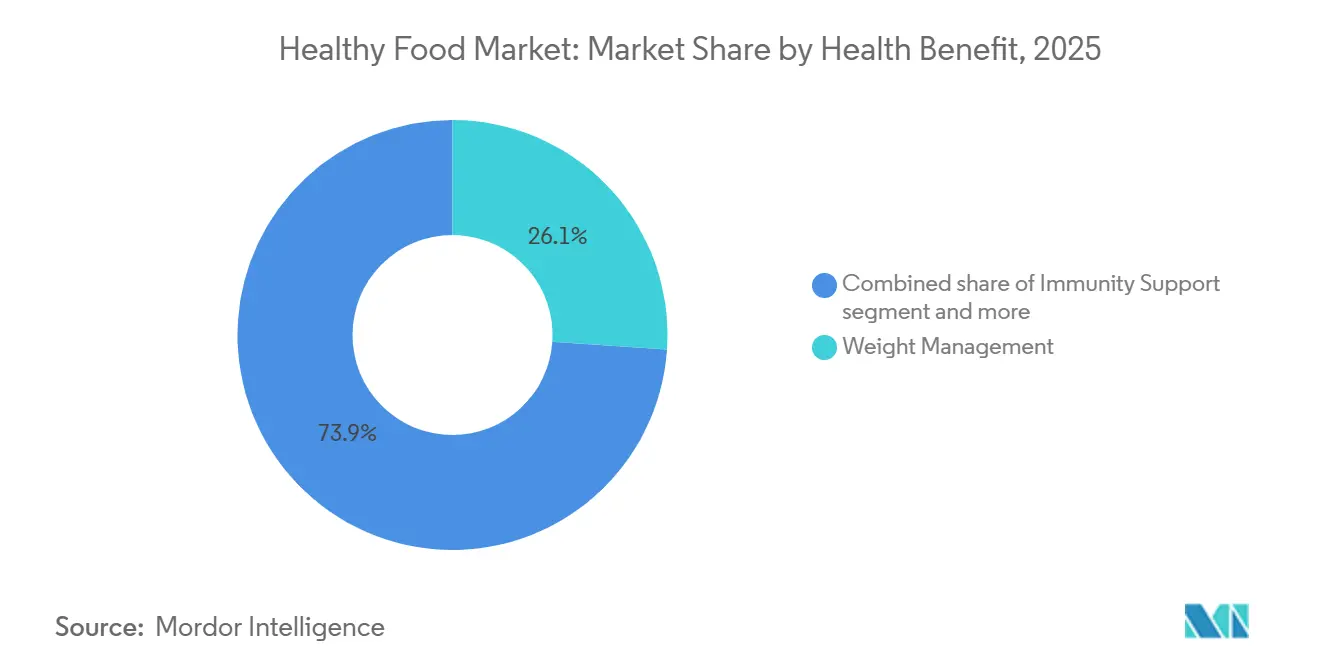

- By health benefit, weight management accounted for 26.08% of the healthy food market in 2025, while immunity support is advancing at a 10.19% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets captured 56.36% of the market in 2025, while online retailers are forecast to grow at a 11.38% CAGR through 2031.

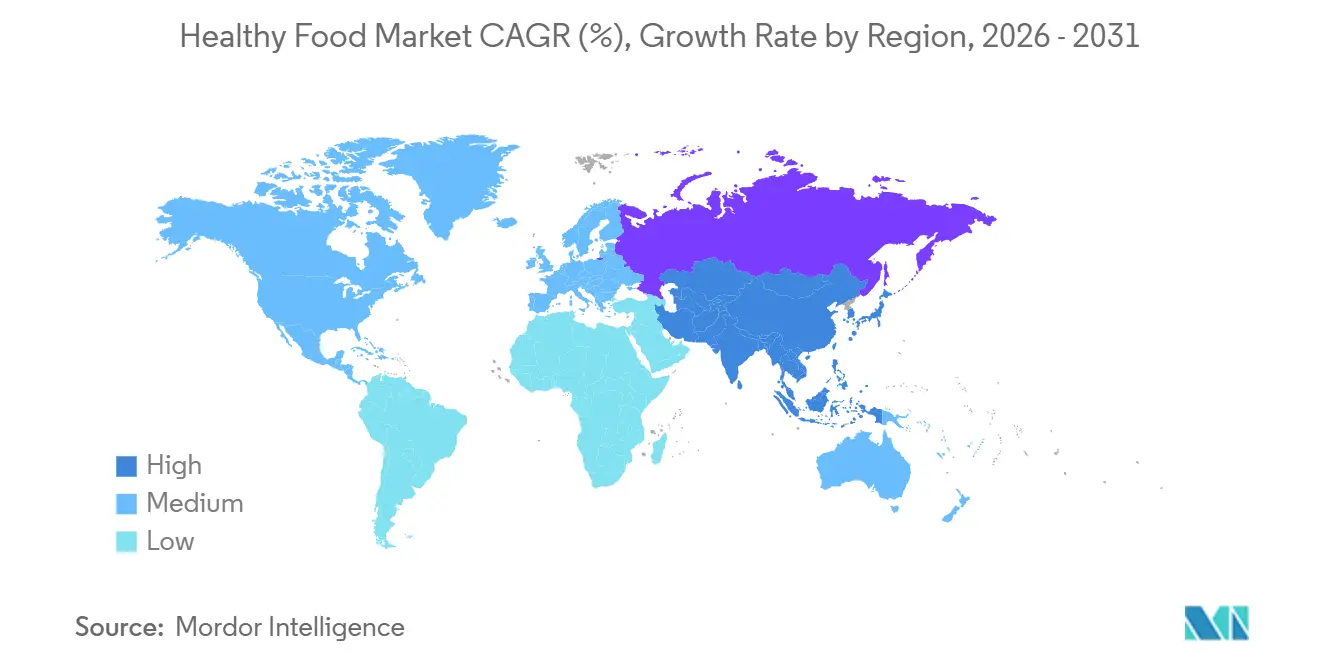

- By geography, North America held 32.46% of the healthy food market share in 2025, while the Asia-Pacific is projected to expand at 10.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthy Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand For Functional and Fortified Foods | +2.8% | Global, with strongest uptake in North America and APAC core | Medium term (2-4 years) |

| Clean-Label and Ingredient Transparency Preference | +1.4% | North America and Europe, with spillover to premium urban APAC centers | Short term (≤ 2 years) |

| Growth Of Plant-Based and Flexitarian Eating Habits | +1.2% | Europe core, with spillover to North America and East Asia | Medium term (2-4 years) |

| Preventive Health Adoption Across Ageing Populations | +1.1% | Japan, Germany, South Korea, China, and early gains in North America | Long term (≥ 4 years) |

| Increasing Obesity, Diabetes and Lifestyle Disease Concerns | +1.5% | Global, strongest in North America, APAC, and MEA | Medium term (2-4 years) |

| Expansion Of High-Protein And High-Fiber Foods | +1.3% | North America and Europe, with growing traction in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for functional and fortified foods

Functional food and beverages accounted for 37.73% of the healthy food market share in 2025, underscoring how strongly consumers now judge food by its nutritional value. The healthy food market is benefiting from broader fortification efforts, as micronutrient deficiency concerns continue to support enrichment programs and everyday health positioning across staples, snacks, dairy, and beverages. The healthy food market is also being reshaped by GLP-1 use, since people using these medicines need products that support protein and micronutrient intake and help preserve muscle while managing reduced appetite. Nestlé and Danone moved early into this space with complete nutrition and protein-led products, which signals that fortified foods are moving closer to medically adjacent nutrition rather than remaining a narrow wellness niche. The FDA’s broader review of ingredient transparency and post-market oversight is likely to favor brands in the healthy food market that can support their functional claims with stronger evidence and clearer formulation standards.

Clean-label and ingredient transparency preference

Consumer demand for ingredient transparency has escalated from a marketing differentiator to a regulatory compliance threshold in 2026. The FDA's 2026 Food Safety priorities explicitly target chemical transparency in the U.S. food supply, including GRAS post-market safety reviews and Front-of-Package (FOP) nutrition labeling rulemaking, creating a durable regulatory tailwind for clean-label positioned products. A 2026 Acosta Group consumer study found that 71% of U.S. shoppers believe the United States should follow Europe's restrictions on artificial ingredients, with 58% supporting bans on synthetic food dyes and 62% of Walmart shoppers demanding greater ingredient transparency. The Consumer Brands Association (CBA) launched its second annual National Consumer Transparency Week in 2026, signaling that major food industry trade groups now frame transparency as a competitive differentiator rather than a compliance burden. A non-obvious implication is that state-level disclosure mandates in the U.S. are creating formulation fragmentation: brands operating nationally must either reformulate to the strictest state standard or maintain separate SKU runs, both of which compress margins and create structural advantages for clean-label specialists over legacy incumbents.

Growth of plant-based and flexitarian eating habits

Global retail sales of plant-based meat, seafood, and dairy reached USD 28.9 billion in 2025, a 3% increase from 2024, as per the Good Food Institute's 2026 State of the Industry report, with cumulative government investment in alternative protein ecosystems reaching USD 2.5 billion globally, up from USD 700 million in 2021[1]Source: Good Food Institute, “2026 State of the Industry Report, Plant-Based,” Good Food Institute, gfi.org. In Europe, plant-based food and drink grew by 5.1% year-on-year from 2024 to 2025, with Germany and Spain leading with 7.2% and 7.5% value growth, respectively, per Circana POS data analyzed by GFI Europe. The critical second-order insight is that flexitarians, not committed vegans, are the structural engine: only 11% of Europeans identify as vegan or vegetarian, yet flexitarianism reached 31% in Europe in 2024, per GFI Europe's 2026 analysis. In the U.S., at least 95% of plant-based meat shoppers also purchased conventional meat in 2025, per the Plant Based Foods Institute's 2025 Regional Retail Insights report, reframing the competitive battle as a meal-occasion fight against conventional protein rather than an ideological conversion. This fundamentally changes the logic of research and development investment: taste parity, price competition, and convenience will determine which plant-based brands achieve structural household penetration through 2031.

Preventive health adoption across ageing populations

By 2030, 1 in 6 people globally will be aged 60 or older, creating a structurally durable demand pool for preventive nutrition products per WHO population projections cited in Frost & Sullivan's 2026 Healthspan Economy whitepaper. Japan represents the most mature institutional expression of this trend, the FOSHU system has normalized preventive health food claims since the 1990s and creates consistent premium pricing for clinically substantiated products. The OECD's 2025 publication The Economic Benefit of Promoting Healthy Aging and Community Care documents that healthcare systems benefit economically from upstream preventive nutrition investment, a framing increasingly influencing government dietary guidance and public procurement across 27 OECD member countries[2]Source: OECD, “The Economic Benefit of Promoting Healthy Ageing and Community Care,” OECD, oecd.org. A non-obvious implication is that the aging population's nutritional priorities diverge significantly from the weight-loss narrative that currently dominates category communications: bone health, cardiovascular function, cognitive maintenance, and immune resilience are structurally higher-value need states for 60+ consumers, and remain materially underpenetrated by current mainstream healthy food product portfolios.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Premium Versus Conventional Food Categories | -1.8% | Global; disproportionate in low-to-middle income brackets across APAC, LATAM, and MEA | Medium term (2-4 years) |

| Shorter Shelf Life and Higher Waste Risk | -0.8% | Global; acute in emerging markets with limited cold chain infrastructure | Long term (≥ 4 years) |

| Consumer Skepticism Toward Health Claims | -0.6% | North America and EU | Short to medium term (1-4 years) |

| Certification and Label Compliance Burden For Smaller Brands | -0.5% | Global; most acute in EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price premium versus conventional food categories

The healthy food market still faces its clearest demand barrier in the price gap between healthier options and conventional food. FAO data showed that healthy diets remained 47% more expensive than ultra-processed alternatives on a calorie-equivalent basis globally in 2024, with the cost of a healthy diet at USD 4.46 PPP per person per day[3]Source: Food and Agriculture Organization of the United Nations, “The State of Food and Agriculture 2024,” Food and Agriculture Organization of the United Nations, fao.org. Academic evidence from Austria in 2026 also found that the minimum diet cost of certified organic produce was 75% higher on average than that of conventionally produced food, reinforcing how hard it is to close the premium gap at scale. This cost pressure matters across the healthy food market because it limits repeat purchases among lower-income households, even when awareness and intent are high. Retailer private labels are responding by building better-for-you ranges at lower premiums, but that also increases pressure on branded margins and weakens pricing power for smaller specialists. The healthy food market can still expand under these conditions, but affordability remains the central issue for broader household penetration.

Shorter shelf life and higher waste risk

Minimally processed, clean-label, and organic food products inherently lack the artificial preservatives and stabilizers that extend shelf life in conventional alternatives, exposing both retailers and consumers to a higher risk of spoilage across the supply chain. The European Union alone generates over 59 million tonnes of food waste annually, 132 kilograms per person, with fresh and natural food categories contributing disproportionately, per European Commission food waste data. At the distribution level, perishable healthy foods require cold chain infrastructure that is unevenly developed across high-growth emerging markets, particularly in Southeast Asia and Sub-Saharan Africa, creating a structural access barrier in the very geographies with the highest long-term volume potential. Research into mitigation technologies is accelerating: a 2026 Frontiers in Nutrition study demonstrated that plasma-activated water combined with edible coatings achieves over 5-log reductions in microbial levels and measurably extends the shelf life of fresh produce. Until shelf life extension technology scales cost-effectively to mass-market retail, the waste risk remains a near-term margin and inventory challenge for organic and natural food specialists operating at high freshness standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Functional Dominance Masks Organic’s Structural Momentum

Functional food and beverages accounted for 37.73% of the healthy food market in 2025, making them the largest product group by a wide margin. The healthy food market supports this position because fortified beverages, probiotic dairy, protein-rich snacks, and complete nutrition formats are now part of everyday shopping rather than occasional wellness use. Organic foods and beverages are the fastest-growing product type, projected to expand at a 11.67% CAGR through 2031, reflecting both premium demand and greater trust in certified production systems. Better-for-you foods are also benefiting from pressure to reduce sugar and reformulation efforts driven by front-of-pack labeling reform, which keeps reformulation active across mainstream snack and beverage portfolios.

Plant-based foods add another important layer to the healthy food market, as they move away from awareness-led growth toward performance in taste, texture, and value. European retail sales of plant-based food reached EUR 16.3 billion in 2025, which shows that the category already has meaningful scale in developed grocery systems, according to the Good Food Institute Europe. Superfoods remain more premium and more digital in their route to market, while the broader Others group continues to expand through fortified staples and enrichment-led products in regions where nutritional gaps remain a policy concern. This leaves the healthy food industry with a clear split between large daily-use functional formats and faster-growing certified or plant-led niches that are still building volume. In product terms, the healthy food market is therefore broadening at both ends, with mainstream utility on one side and trusted premium positioning on the other.

By Category: Non-Vegetarian Leads, But Vegan Accelerates On Flexitarian Tailwinds

Non-vegetarian products held 43.56% of the healthy food market share in 2025, indicating that the largest volume still sits in reformulated mainstream protein categories. The healthy food market continues to drive spending toward organic meat, fortified dairy, omega-3 eggs, and functional seafood, as these formats already have household familiarity and retail scale. Vegan products are the fastest-growing category and are projected to rise at 10.75% CAGR through 2031, but the stronger audience is made up of flexible buyers rather than fully committed vegan consumers. The healthy food market is responding to this behavior, as at least 95% of plant-based meat shoppers in the United States also bought conventional meat in 2025, confirming that the category competes within mixed diets, according to the Plant Based Foods Association. Government support also matters here, since alternative protein investment reached USD 2.5 billion globally by 2025 and created a stronger supply-side base for future price improvement, according to the Good Food Institute Europe.

Vegetarian products occupy a more stable middle position in the healthy food market because fermented dairy products, probiotic formats, and everyday meat-light diets support steady repeat purchases. Vegan growth in the healthy food market is therefore not replacing non-vegetarian demand outright, but it is expanding the set of acceptable protein choices during regular meal planning. That mix matters because brands can grow faster when they position plant-based products as additions to household rotation rather than total replacements. Across category lines, the healthy food industry is becoming less ideological and more practical, with convenience, nutrition density, and sensory quality driving the next round of adoption.

By Health Benefit: Weight Management Anchors Scale While Immunity Keeps Expanding

Weight management accounted for 26.08% share of the healthy food market size in 2025, making it the largest health benefit platform. The healthy food market is seeing this category change shape because GLP-1 use has turned weight management into a more medically guided nutrition need that includes protein, satiety support, and muscle preservation. Danone, Nestlé, and Conagra all moved into this space with products designed around complete nutrition or GLP-1-adjacent routines, which shows how quickly the category has shifted. Immunity support is the fastest-growing health benefit, projected to expand at a 10.19% CAGR through 2031, supported by continued demand for probiotic, zinc, and vitamin-enriched formats. The healthy food market continues to show strong post-pandemic momentum, as consumers now treat immune support as a routine purchase driver rather than an occasional need.

Digestive and heart health also remain important pillars of the healthy food market, as they support both preventive care and daily symptom management. A 2025 Nature Medicine study linked long-term adherence to healthy dietary patterns with better aging outcomes, supporting broader demand for products tied to long-term well-being rather than short-term fixes. Energy and performance benefits are also spreading into normal beverage and snack formats as protein and fiber claims move beyond specialist channels and into mass consumption categories. The Others group, including cognitive health and bone health, remains smaller but strategically important because aging populations value function-specific nutrition that fits ordinary meals and snacks. Taken together, the healthy food market is moving from broad wellness messaging toward sharper need states that are easier to explain, test, and repeat.

By Distribution Channel: Supermarkets Dominate While Online Builds The Fastest Momentum

Supermarkets and hypermarkets accounted for 56.36% of the healthy food market in 2025, making them the main discovery and repeat-purchase channel. The healthy food market still depends on these stores because their scale, footfall, and private-label capabilities make them the easiest route to mainstream visibility. Shelf placement also matters more in this channel, as front-of-pack labeling becomes more important for fast product comparisons. Specialty stores remain important because they bring new functional, organic, and premium products to market earlier than larger chains in many cases. This keeps the healthy food market supplied with a pipeline of higher-value launches before wider supermarket rollout.

Online retailers are the fastest-growing channel and are projected to expand at a 11.38% CAGR through 2031, reflecting stronger direct-to-consumer nutrition models and repeat-order convenience. Danone’s acquisition of Huel highlights this point because Huel built much of its strength through digital complete nutrition sales before the transaction. Convenience stores are also expanding better-for-you options, especially in protein snacks and portable functional formats that support impulse purchases. As the healthy food market grows, channel roles are becoming more distinct, with supermarkets driving scale, specialty stores supporting innovation, and online platforms improving targeting and retention. That structure gives the healthy food market broader reach without forcing every brand into the same route-to-market model.

Geography Analysis

North America held 32.46% of the healthy food market share in 2025, which made it the largest regional contributor. The United States remained the anchor of the region's healthy food market, even as its organic sector grew twice as fast as the conventional market. The White House MAHA assessment brought diet quality and exposure to ultra-processed foods into the national policy debate, raising the reformulation stakes for major food companies. The FDA’s updated healthy claim rule and its 2026 priorities are also strengthening the operating framework for brands in the healthy food market that rely on front-of-pack health positioning. Canada is also shifting, with data from the Canadian Food Sentiment Index showing that omnivorous diets fell and flexitarian habits rose between late 2024 and spring 2026.

Europe remains a structurally important part of the healthy food market, but regional performance is uneven across countries and product groups. Germany’s organic market reached EUR 18.2 billion in 2025, or USD 19.5 billion, and Q1 2026 sales rose to EUR 4.91 billion, or USD 5.3 billion, which kept organic ahead of the wider food market, according to the German Federation of Organic Food Producers. The wider EU organic food and drink market reached EUR 58.7 billion in 2024, or USD 63.7 billion, while France and Italy remained major national contributors, according to the Research Institute of Organic Agriculture FiBL. The United Kingdom approached GBP 4 billion in organic sales in 2026, or USD 5.1 billion, and 83% of households bought organic products, which points to further room for penetration even from a low base of total food sales, as per The Soil Association.

Asia-Pacific is the fastest-growing region in the healthy food market and is projected to expand at 10.55% CAGR through 2031. China is the largest regional engine, with its organic food market reaching CNY 107 billion in 2024, or USD 15.5 billion, while policy support continues to encourage functional food development and premium health positioning, according to the Research Institute of Organic Agriculture FiBL. India adds growth through fortification programs, rising urban health awareness, and the spread of traditional wellness ideas into modern packaged formats. Japan remains important because its FOSHU system supports premium pricing for clinically substantiated products, while South America and the Middle East and Africa continue to open incremental room for the healthy food market as nutrition policy, premium retail, and cleaner-label demand improve across major urban centers.

Competitive Landscape

The healthy food market remains moderately fragmented, with Nestlé S.A., Danone S.A., PepsiCo, Inc., General Mills, Inc., and Mondelēz International holding meaningful positions but not controlling the field. The healthy food market is seeing acquisition activity accelerate because large food companies want faster access to complete nutrition, digital channels, plant-based formats, and science-backed premium products. Danone agreed to acquire Huel in March 2026 for strategic access to complete nutrition and digital direct-to-consumer reach across the United Kingdom, Europe, and the United States. Nestlé also moved deeper into premium nutrition by planning to acquire Yfood in full in 2026 and increasing its stake in Orgain in 2025. These moves show that the healthy food market rewards established companies that can add targeted growth platforms rather than relying only on legacy packaged food brands.

PepsiCo has taken a broad portfolio approach in the healthy food market by extending protein, fiber, and functional cues into snacks and beverages such as Doritos Protein, Quaker Protein Rice Crisps, Propel Clear Protein, and PopCorners Protein. Mondelēz is also broadening its health-and-wellness mix through zero-sugar, gluten-free, and protein bar formats, which points to a more deliberate adjacency strategy around better-for-you snacking. The healthy food market still leaves room for challengers such as Chobani, Oatly, SunOpta, and Hain Celestial because category growth is spread across many niches, channels, and price points. Technology is also becoming a stronger competitive tool as direct subscriptions, QR-based transparency, and personalized nutrition interfaces make it easier for specialist brands to retain consumers.

At the same time, the healthy food market is getting harder for mid-tier brands because compliance standards are rising and retailer expectations are becoming more demanding. Certifications, food safety systems, traceability, and claim substantiation now act as practical moats for larger companies that can absorb the cost more easily. The United Kingdom Competition and Markets Authority review of Danone’s Huel transaction also shows that regulators are paying closer attention to big-company acquisitions of fast-growing challenger brands. Overall, the healthy food market remains open enough for innovation-led specialists, but scale players have become more disciplined in using acquisitions, reformulation, and portfolio extension to defend relevance.

Healthy Food Industry Leaders

Nestlé S.A.

Danone S.A.

PepsiCo, Inc.

General Mills, Inc.

Mondelez International, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Nestlé announces the full acquisition of German smart food brand Yfood, completing a strategic process that began with a 49% stake in 2023. Yfood reported EUR 150 million in sales in 2025 with double-digit year-on-year growth. The deal strengthens Nestlé’s Nutrition pillar under its four-pillar restructuring strategy, and signals expanded competitive positioning in complete nutrition across Europe and North America.

- May 2026: Danone’s Danimals brand unveils an enhanced recipe for its Smoothies and Low Fat Yogurt Pouches, delivering a good source of calcium, vitamin D, and fiber for children. The product contains no artificial colors, no artificial flavors, no high fructose corn syrup, and is Non-GMO Project Verified, directly responding to stronger parental scrutiny of children’s food.

- April 2026: PepsiCo launches Quaker Protein Rice Crisps nationwide in the United States, delivering 6g protein and 9g whole grains per serving in Chocolate Caramel and Tangy Barbecue flavors. The launch is part of a broader portfolio shift that has added protein and fiber positioning to multiple Quaker and PepsiCo snack brands since 2025.

- March 2026: Danone enters a definitive agreement to acquire Huel for EUR 1 billion, or USD 1.2 billion. The transaction extends Danone’s portfolio into complete nutrition and strengthens digital direct-to-consumer capabilities across the United Kingdom, Europe, and the United States.

Global Healthy Food Market Report Scope

Healthy food refers to products formulated to provide nutritional benefits, support overall wellness, and help consumers maintain a balanced diet and a healthy lifestyle. The healthy food market is segmented by product type, category, health benefit, distribution channel, and geography. By product type, the market includes functional food and beverages, organic foods and beverages, better-for-you foods, plant-based foods, superfoods, and other healthy food products. Based on category, the market is segmented into vegan, vegetarian, and non-vegetarian products. In terms of health benefits, the market covers weight management, digestive health, heart health, immune support, energy and performance, and other benefits. Based on distribution channel, the market is categorized into supermarkets and hypermarkets, convenience stores, specialty stores, online retailers, and other distribution channels. Geographically, the report covers North America, Europe, Asia-Pacific, South America, and the Middle East and Africa, with market sizes and forecasts for each region. For each segment, market sizing and forecasts have been conducted on a value basis (USD).

| Functional Food & Beverages |

| Organic Foods & Beverages |

| Better-for-you Foods |

| Plant-based Foods |

| Superfoods |

| Others |

| Vegan |

| Vegetarain |

| Non-Vegetarian |

| Weight Management |

| Digestive Health |

| Heart Health |

| Immunity Support |

| Energy & Performance |

| Others |

| Supermarkets and Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Retailers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Rest of Middle East and Africa |

| By Product Type | Functional Food & Beverages | |

| Organic Foods & Beverages | ||

| Better-for-you Foods | ||

| Plant-based Foods | ||

| Superfoods | ||

| Others | ||

| By Category | Vegan | |

| Vegetarain | ||

| Non-Vegetarian | ||

| By Health Benefit | Weight Management | |

| Digestive Health | ||

| Heart Health | ||

| Immunity Support | ||

| Energy & Performance | ||

| Others | ||

| By Distribution Channel | Supermarkets and Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retailers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2026 size of the healthy food market?

The healthy food market stands at USD 1.05 trillion in 2026 and is projected to reach USD 1.67 trillion by 2031 at a 9.76% CAGR.

Which product category leads healthy food demand worldwide?

Functional food and beverages lead with 37.73% share in 2025, supported by stronger demand for fortification, protein, probiotics, and daily wellness formats.

Which category is growing fastest across food preferences?

Vegan products are projected to grow at 10.75% CAGR through 2031, although much of that growth is being driven by flexitarian households rather than strict vegan adoption.

Why is GLP-1 adoption affecting food companies?

GLP-1 use is increasing demand for products with more protein, fiber, and micronutrients, which is pushing companies such as Danone, Nestlé, and PepsiCo to launch more targeted nutrition formats.

Which sales channel matters most for healthy food brands?

Supermarkets and hypermarkets remain the largest channel with 56.36% share in 2025, while online retail is the fastest-growing channel at 11.38% CAGR through 2031.

Page last updated on: