Fast Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

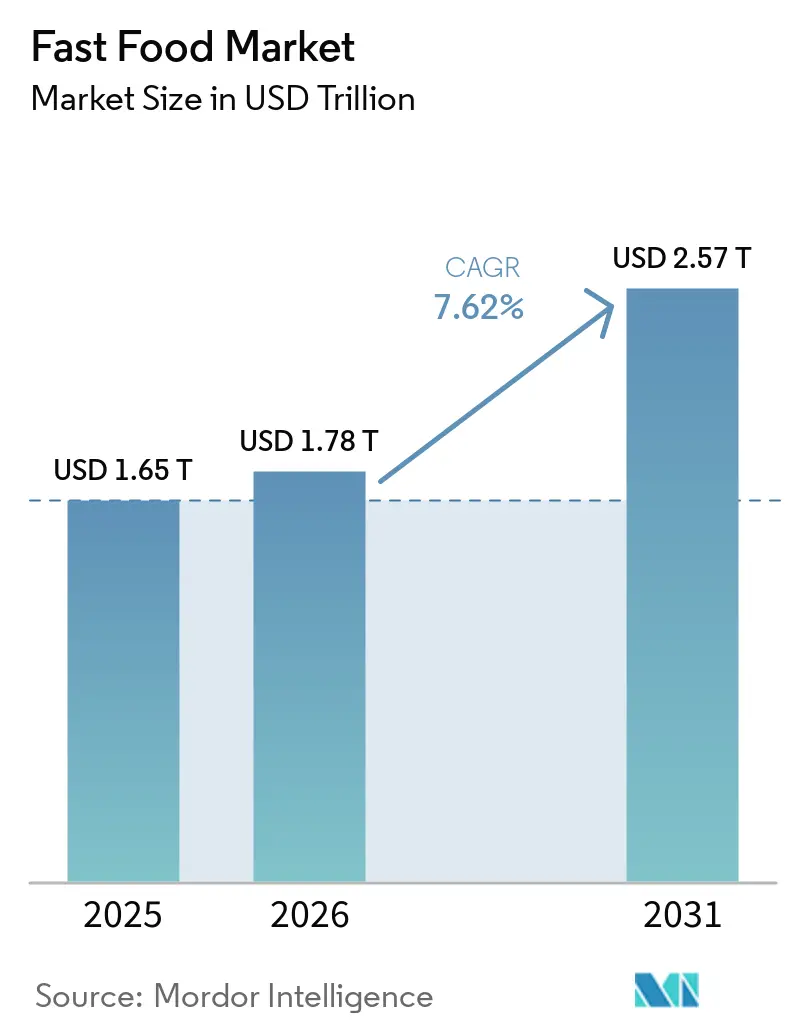

| Market Size (2026) | USD 1.78 Trillion |

| Market Size (2031) | USD 2.57 Trillion |

| Growth Rate (2026 - 2031) | 7.62% CAGR |

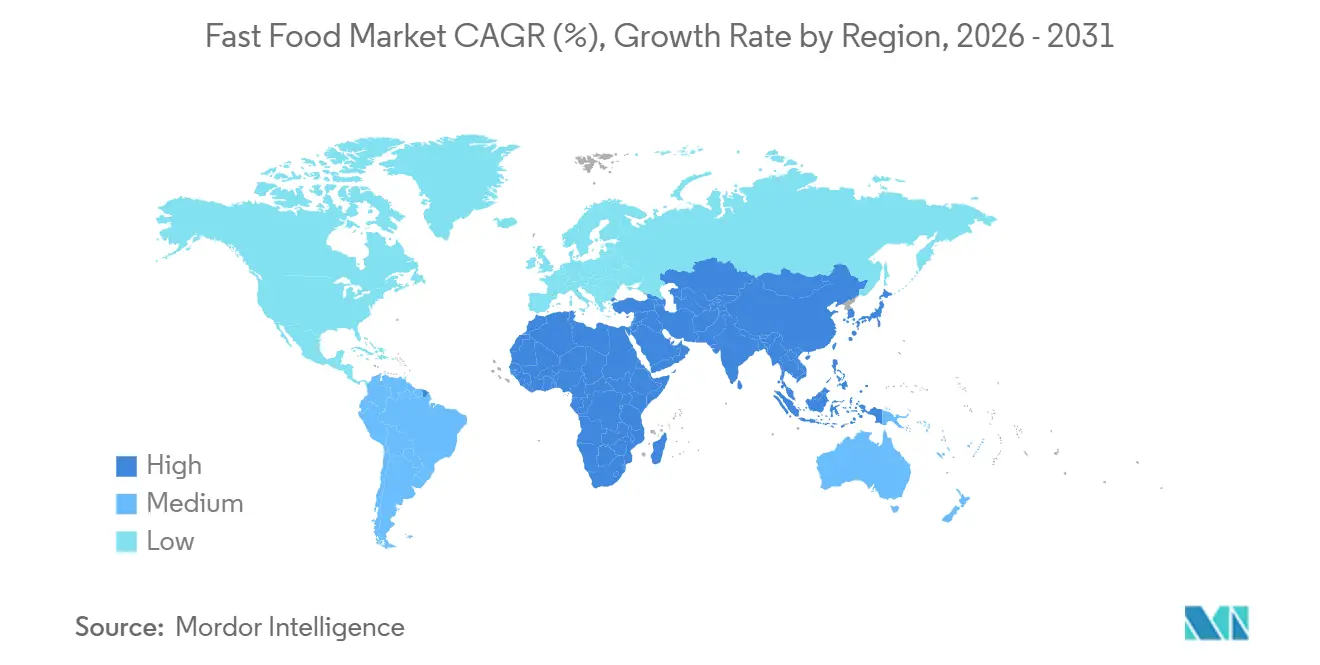

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fast Food Market Analysis by Mordor Intelligence

The fast food market is projected to grow significantly, increasing from USD 1.65 trillion in 2025 to USD 1.78 trillion in 2026 and reaching USD 2.57 trillion by 2031, reflecting a CAGR of 7.62% over the 2026-2031 period. This growth is driven by consumers spending more of their discretionary income on convenient meal options, enabling fast food chains to raise prices despite rising input costs. Innovations such as QR-code menus, mobile payment systems, and AI-assisted order-taking are enhancing customer experiences by reducing wait times and improving efficiency during peak hours. In terms of product types, pizza continues to leverage its digital advantage over traditional staples, while Asian cuisines are gaining popularity, particularly among millennials, due to their unique offerings. Fast-casual restaurants are closing the gap with quick-service restaurants (QSRs) by offering a balance of quality and convenience. The market remains highly fragmented, with numerous players competing to capture consumer demand in this evolving landscape.

Key Report Takeaways

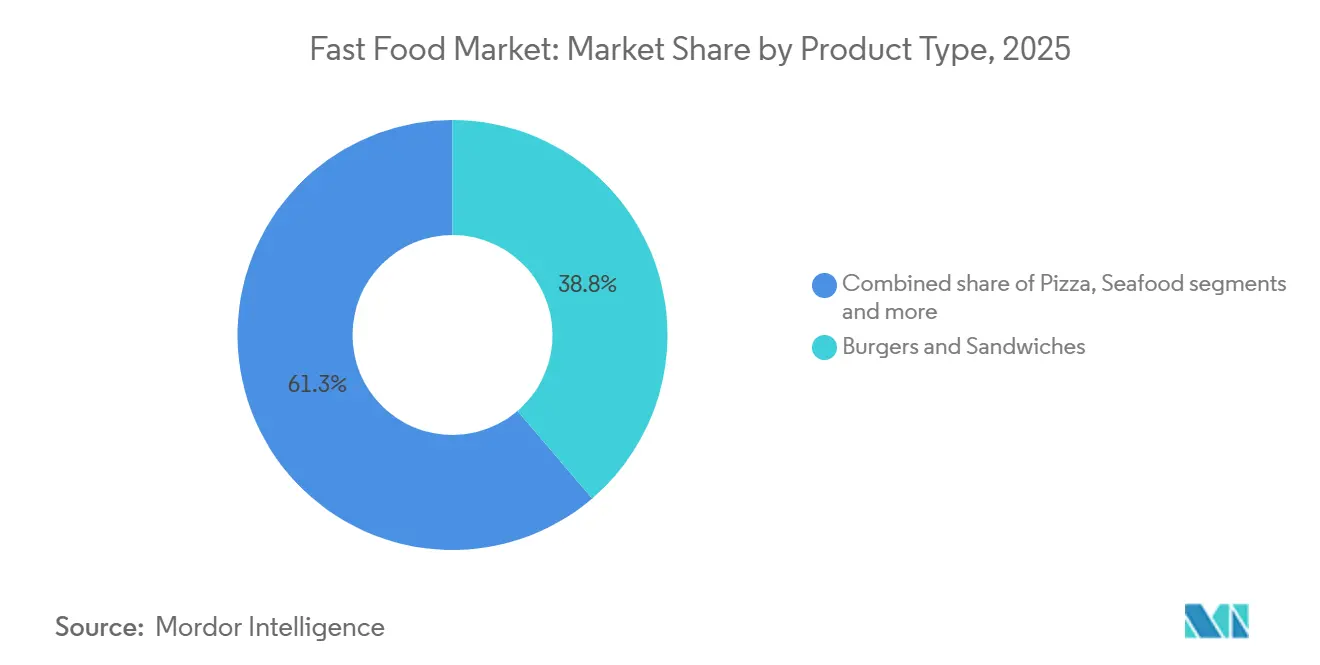

- By product category, burgers and sandwiches held 38.75% of fast food market share in 2025, while pizza is projected to advance at an 8.18% CAGR through 2031.

- By cuisine type, American fare accounted for 42.54% of 2025 revenue, and Asian flavors are forecast to grow at a 9.58% CAGR through 2031.

- By restaurant format, quick service restaurants accounted for 58.17% of 2025 sales, whereas fast-casual units are on track for an 8.24% CAGR over 2026-2031.

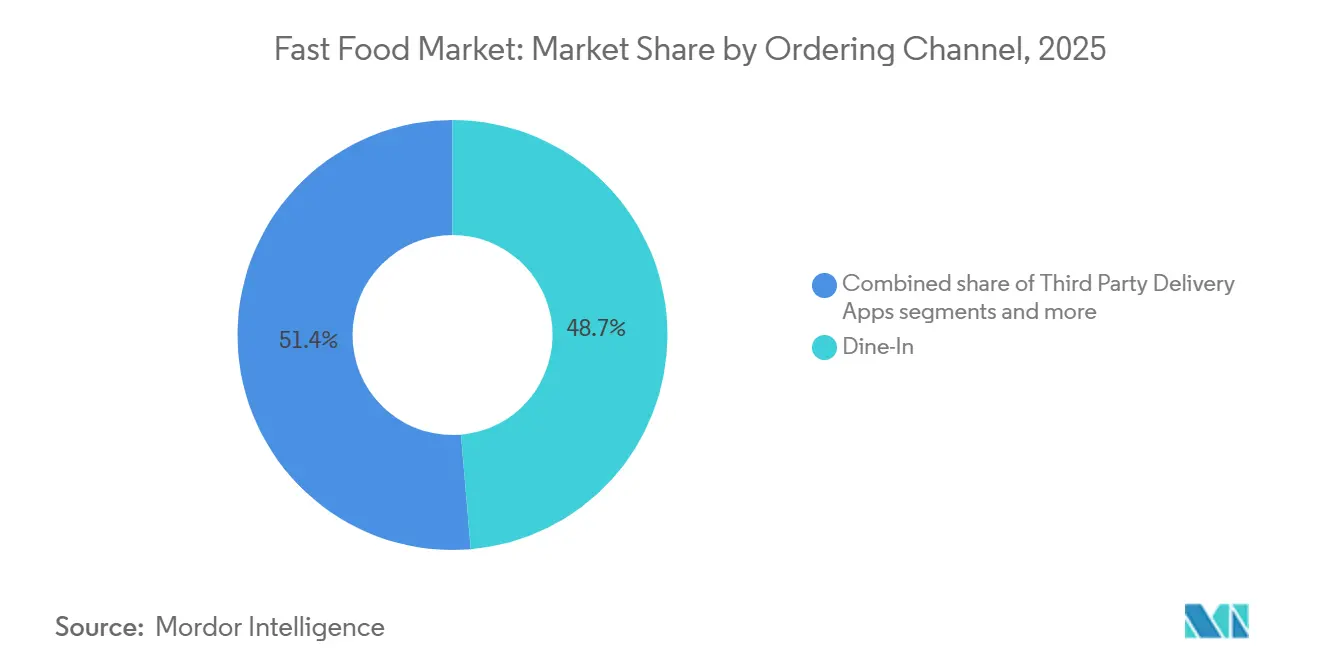

- By ordering channel, dine-in accounted for 48.65% of 2025 orders, yet third-party delivery apps are set to grow at an 8.51% CAGR through 2031.

- By outlet ownership, independent stores accounted for 61.47% of 2025 turnover, but chained formats will grow at a 7.14% CAGR through 2031.

- By geography, Asia-Pacific accounted for 43.82% of 2025 sales, whereas the Middle East and Africa are on track for an 8.95% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fast Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasingly hectic lifestyles driving demand for convenient, ready-to-eat meal options | +1.2% | Global, with peak intensity in North America, Asia-Pacific urban centers | Long term (≥ 4 years) |

| Strong branding, promotional strategies, and value meal offerings | +1.0% | Global, concentrated in North America and Europe | Short term (≤ 2 years) |

| Continuous menu innovation, including healthier and fusion options | +0.9% | Global, with early adoption in North America and Asia-Pacific | Medium term (2-4 years) |

| Growing exposure to global cuisines and western food culture | +0.8% | Asia-Pacific, Middle East and Africa, Latin America | Long term (≥ 4 years) |

| Aggressive expansion of quick service restaurant chains | +1.1% | Asia-Pacific, Middle East and Africa, emerging markets | Medium term (2-4 years) |

| Technological advancements such as mobile ordering, digital payments, and self-service kiosks | +0.7% | Global, with North America and Asia-Pacific leading adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasingly hectic lifestyles are driving demand for convenient, ready-to-eat meal options

Increasing employment levels and busier lifestyles are driving global demand for convenient, ready-to-eat fast food options. With global employment projected to reach 95.1% in July 2025, according to the Organisation for Economic Co-operation and Development, more dual-income households and longer commutes are reducing the time available for home cooking, leading consumers to replace full meals with snacks[1]Source: Organisation for Economic Co-operation and Development, "OECD Unemployment Rate Remained Stable at 4.9% in July 2025", oecd.org. To address this trend, operators are introducing portable, high-protein products, such as protein cups, for on-the-go consumption. Chains such as Chipotle launched high-protein bowls in December 2025 to meet rising demand for quick, protein-rich meals. Similarly, Starbucks expanded its protein beverage lineup, offering options with up to 30 grams per serving to attract consumers seeking convenient nutrition. Furthermore, modular menu strategies enable large chains to quickly adjust offerings across dayparts, aligning with a broader market trend favoring portability and convenience over traditional dine-in experiences.

Technological advancements such as mobile ordering, digital payments, and self-service kiosks

Technological advancements, including mobile ordering, digital payments, AI, and self-service kiosks, are reshaping efficiency and the customer experience in the fast food market. According to Phys.org, approximately two-thirds of American consumers used a food-ordering app at least once for takeout or delivery in 2024, demonstrating strong digital adoption[2]Source: Phys Org, "Consumer Food Insights Report Highlights Increasing Use of Food-Ordering Apps", phys.org. Operators are expanding these capabilities, with Yum! Brands are processing over 2 million AI-powered voice orders across 300 Taco Bell locations in 2024. Additionally, McDonald’s reported digital sales surpassing USD 10 billion in 2025, accounting for nearly 20% of system revenue, while Starbucks implemented Smart Queue sequencing and AI-based scheduling to cut peak service times to under four minutes, as noted by Starbucks. These digital systems improve accuracy, reduce labor dependency, and provide valuable customer insights, positioning them as key growth drivers in the fast food market.

Global Cuisine Offerings Attract Adventurous And Diverse Customer Bases

Ongoing menu innovation, integrating healthier formulations with trend-driven fusion offerings, is fueling growth in the fast food market. As of February 2026, approximately 88 million people globally, or nearly 1.1% of the population, identify as vegans, according to the World Animal Foundation[3]Source: World Animal Foundation, "How Many Vegans Are in the World in 2026? Latest Vegan Stats", worldanimalfoundation.org. This has led to a growing demand for healthier plant-based food options. Brands are addressing this shift by balancing nutrition with indulgence. For instance, Starbucks introduced the viral Iced Dubai Chocolate Matcha in 2025, Chipotle plans to launch limited-time protein options in 2026, and KFC India unveiled its “Smarter Indulgence” menu in October 2025, featuring grilled and plant-based items. These strategies cater to changing dietary preferences, enhance consumer engagement, and allow fast food chains to expand their appeal across various customer segments.

Growing exposure to global cuisines and western food culture

Exposure to global cuisines and Western food culture continues to expand the fast food market, especially in emerging economies. Social media and digital platforms are driving awareness of international dining trends, encouraging urban consumers to explore cross-cuisine options. This trend is evident in aggressive expansion plans, such as Lawson's goal to establish 10,000 stores in India by 2050, catering to the demand for Japanese-style grab-and-go formats. Similarly, Chick-fil-A entered Singapore in November 2025 with a significant investment, while Chipotle plans to expand into Singapore and South Korea in 2026 through a joint venture, tailoring its menu to local preferences. These localization efforts enable global chains to access middle-income markets while remaining competitive with domestic players.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising concerns regarding obesity, diabetes, and lifestyle-related diseases | -0.6% | Global, with regulatory intensity highest in North America and Europe | Medium term (2-4 years) |

| Increasing competition from healthier alternatives such as home-cooked meals and meal kits | -0.5% | North America, Europe, select Asia-Pacific urban markets | Short term (≤ 2 years) |

| Stringent government regulations related to food safety, labeling, and nutritional disclosures | -0.4% | Global, with North America and Europe enforcing front-of-pack labeling | Short term (≤ 2 years) |

| Fluctuations in raw material prices, including edible oils, meat, and dairy | -0.3% | Global, with acute pressure in import-dependent markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising concerns regarding obesity, diabetes, and lifestyle-related diseases

Growing concerns about obesity, diabetes, and other lifestyle-related diseases are hindering the growth of the fast food market. According to the World Obesity Federation’s 2025 Atlas, the number of adults with obesity is expected to rise by over 115%, from 524 million in 2010 to 1.13 billion by 2030, increasing public health scrutiny[4]Source: World Obesity Federation, "World Obesity Atlas 2025", worldobesity.org. In response, governments are implementing stricter regulations. For instance, the U.S. Food and Drug Administration's plans to introduce front-of-pack labeling rules in spring 2026, requiring clear icons for saturated fat, sodium, and added sugars. Similarly, Canada implemented comparable warning measures in January 2026. While fast food chains are introducing healthier options, such as high-protein and reduced-sugar products, these reformulations increase costs. Additionally, heightened consumer awareness is driving a shift toward healthier alternatives, such as meal kits, thereby limiting growth in fast food demand.

Increasing competition from healthier alternatives such as home-cooked meals, and meal kits

Growing competition from healthier alternatives, such as home-cooked meals, meal kits, and premium fast-casual dining formats, is increasingly challenging the fast food market. Companies like Nomad Foods are capitalizing on the demand for clean-label frozen meals by offering products with minimal additives, appealing to health-conscious consumers who are also pressed for time. Similarly, fast-casual and premium sandwich chains, including Jersey Mike’s, are attracting customers by emphasizing freshness and higher-quality ingredients, which are often perceived as healthier than traditional fast food options. This shift in consumer preferences toward nutrition, transparency, and quality is driving a notable change in the competitive landscape. To remain relevant and retain market share, fast food operators must adapt by enhancing their health-focused offerings, such as introducing more nutritious menu items, reformulating existing products, and communicating ingredient transparency.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pizza Extends Digital Advantage Over Legacy Staples

Burgers and sandwiches accounted for the largest share of the fast food market in 2025, contributing 38.75% of total revenue. This breakdown shows that consumers prefer quick, portable meal options, though there is growing interest in diverse menu choices. Despite the rise of niche offerings, traditional fast food items like burgers and pizza continue to dominate the market due to their widespread popularity and convenience.

Looking ahead, pizza is expected to grow the fastest, with a CAGR of 8.18% during 2026–2031. This growth is driven by innovations in flavors and premium product offerings. Burgers and sandwiches are projected to grow steadily, supported by consistent consumer demand and new product launches by major brands. On the other hand, niche categories such as meat-based snacks and seafood are likely to grow more slowly. This slower growth is primarily due to challenges in managing supply chains and maintaining consistent quality across multiple outlets, which makes scaling these categories more difficult.

By Cuisine Type: Asian Menus Capture Millennial Curiosity

In 2025, American-style fast food accounted for 42.54% of the market share. This was largely due to the widespread appeal of items like burgers, fried chicken, and fries. Italian food, including pizza and pasta, also captured a significant portion of the market, thanks to its global popularity and suitability for delivery services. The remaining market share was split between Asian cuisines and other categories, such as Middle Eastern, fusion, and emerging regional options. This distribution highlights the strong presence of Western fast food while also showcasing the growing interest in diverse food choices.

Asian cuisine is expected to grow the fastest through 2031, with a projected CAGR of 9.58%. This growth is driven by increasing demand for bold flavors and the perception of healthier meal options. Italian food is expected to grow at a moderate pace, supported by the continued popularity of pizza across delivery channels. Meanwhile, American fast food is likely to see steady but slower growth as consumers explore a wider variety of cuisines. These trends indicate a gradual shift in global fast food preferences, with more people seeking diverse, unique dining experiences.

By Restaurant Type: Fast-Casual Narrows the Gap With QSR

In 2025, quick service restaurants (QSRs) led the global fast food market, accounting for 58.17% of total market share. Their dominance was driven by affordability, fast service, and global availability. Fast-casual restaurants, while accounting for a smaller share, showed steady growth as they attracted customers seeking better-quality ingredients and a more upscale dining experience. Other formats, such as food trucks, kiosks, cafeterias, and virtual kitchens, accounted for the rest of the market, highlighting the growing variety in how fast food is delivered to consumers. This mix of traditional and newer formats reflects customers' evolving preferences worldwide.

Between 2026 and 2031, fast-casual restaurants are expected to grow at a strong CAGR of 8.24%, surpassing the growth rate of QSRs. This growth is fueled by rising demand for personalized meals, healthier food options, and premium dining experiences. Mobile formats such as food trucks and kiosks are also expected to grow moderately, benefiting from their convenience and lower operating costs. However, virtual-only brands may face short-term challenges due to market consolidation and difficulties achieving profitability, making their growth less predictable than in other segments.

By Ordering Channel: Delivery Platforms Maintain Momentum Despite Fees

In 2025, dine-in orders accounted for 48.65% of the fast food market, maintaining the largest share despite the growing popularity of convenience-focused options. Drive-thru and takeaway services followed closely, driven by the growing need for quick, portable meal solutions. Additionally, third-party delivery platforms and brand-owned digital apps, while holding a smaller share, showed rapid growth as more consumers embraced digital ordering. This trend highlights a mix of traditional dining preferences and the shift toward modern, tech-enabled consumption habits.

Looking ahead, third-party delivery apps are expected to grow the fastest, with a 8.51% CAGR through 2031, surpassing all in-store formats. Drive-thrus, takeaways, and brand-owned digital platforms are also projected to grow steadily, supported by technological advancements and the demand for convenience. On the other hand, dine-in services are likely to grow more slowly as operators focus on improving the in-store experience to attract customers. These changes underscore the growing importance of digital and hybrid service models in shaping the future of the fast food industry.

By Outlet Type: Chain Economics Outflank Independents

In 2025, independent outlets led the global fast food market, accounting for 61.47% of total market share. Their dominance was largely due to their strong presence in local and regional areas, catering to specific consumer preferences. On the other hand, franchised and company-owned chains accounted for 38.53% of the market. These chains benefited from their ability to maintain consistent quality, leverage brand recognition, and expand operations more efficiently. This division shows the balance between localized offerings and the growing popularity of organized chains.

Between 2026 and 2031, chained formats are expected to grow at a CAGR of 7.14%, gradually closing the gap with independent outlets. This growth will be driven by investments in advanced technology, streamlined supply chains, and consistent branding efforts. Independent outlets, however, are projected to grow more slowly due to challenges such as stricter regulations and the rising costs of adopting digital tools. This trend suggests a gradual shift in the fast food market toward more structured, scalable business models, favoring larger chains over smaller, standalone operators.

Geography Analysis

Asia-Pacific led the global fast food market in 2025, accounting for 43.82% of total revenue. This dominance is due to the region's large urban population and growing demand for convenient food options. The rapid growth of organized fast food chains and the increasing presence of international brands are key drivers of this market. Additionally, rising disposable incomes and changing eating habits are boosting demand. The region's market position is further strengthened by the continuous opening of new outlets and consolidation among players, making it the most dynamic contributor globally.

The Middle East and Africa are expected to grow the fastest in the fast food market, with a projected CAGR of 8.95% over the forecast period. This growth is fueled by a young, growing population and increasing urbanization. Global fast food companies are investing heavily in the region, supported by favorable business conditions. Lower real estate and operational costs are also helping brands expand more easily. As a result, the region is becoming a key focus for fast food companies seeking high-growth opportunities.

North America remains a mature and highly competitive market, supported by strong brand presence and a dense network of outlets. Growth in this region is driven by menu innovations, value-based offerings, and efforts to improve customer experiences. Europe is expected to see steady growth, driven by premiumization trends and shifting consumer preferences, despite regulatory challenges. In South America, urbanization and a growing middle class are contributing to gradual market expansion. The increasing presence of international fast food chains in these regions is further supporting stable and consistent growth.

Competitive Landscape

The global fast food market is highly fragmented, with major players such as McDonald’s Corporation and Yum! Brands, Inc., Restaurant Brands International Inc., Domino’s Pizza, Inc., and Starbucks Corporation are competing alongside numerous regional chains and independent outlets. This fragmentation means no single company dominates the market, leading to intense competition. As a result, both global and local brands are constantly innovating their menus and services to attract customers and gain a competitive edge. This dynamic environment allows smaller players to challenge established brands by offering unique products or localized options.

Partnerships, mergers, and localization strategies are shaping the competitive landscape of the fast food market. Companies are forming joint ventures and collaborations to expand into high-growth regions and adapt to local consumer preferences. Consolidation efforts are helping businesses streamline operations, reduce costs, and strengthen their market presence. However, simply achieving scale is not enough. Companies must also focus on building strong customer loyalty and maintaining consistent engagement to ensure long-term success in this competitive market.

Technology is becoming a critical factor in the fast food market, with companies investing heavily in digital platforms, automation, and AI-driven tools. These advancements are improving operational efficiency and enhancing the customer experience, such as through faster ordering and personalized recommendations. Meanwhile, fast-casual brands like Jersey Mike’s Subs and Xiao Noodle are gaining popularity by targeting specific customer segments and creating strong brand identities. Moving forward, businesses that effectively use technology, innovate their offerings, and form strategic partnerships will be better positioned to achieve sustained growth and market leadership.

Fast Food Industry Leaders

-

McDonald's Corporation

-

Starbucks Corporation

-

Yum! Brands, Inc

-

Restaurant Brands International Inc.

-

Domino’s Pizza Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: McDonald’s opened a new outlet in Ludhiana, expanding its presence in North India and focusing on growing urban markets. This step was part of its plan to target Tier II and III cities while improving the customer experience through digitally enabled store formats.

- March 2025: Wendy's announced expansion plans to open 1,000 new restaurants globally by 2028, with 70% of growth focused outside the U.S., adding nearly 300 foreign restaurants in the past three years and targeting 2,000 international locations within four years

- May 2025: In-N-Out Burger opened 7 new locations, focusing on areas where it already operates in the United States. This strategy aimed to strengthen its presence in familiar markets rather than expanding too quickly into new ones.

- August 2024: Popeyes reported expansion from over 500 international locations generating USD 300 million in annual sales in 2017 to nearly 1,300 locations with over USD 1 billion in systemwide sales, with same-store sales increasing 19.4% in Q2 2024.

Global Fast Food Market Report Scope

Fast food refers to commercially prepared meals that are quickly cooked, served, and designed for convenient consumption, often with standardized ingredients and processes. The global fast food market is classified by product type, cuisine type, restaurant type, ordering channel, outlet type, and geography. Based on product type, the market is classified into burgers and sandwiches, meat-based products, seafood, pasta and noodles, pizza, desserts and ice-creams, and others. Based on cuisine type, the market is classified into asian, American, Italian, Chinese, Mexican, and others. Based on restaurant type, the market is classified into quick-service restaurants (QSRs), fast-casual restaurants, food trucks and mobile units, cafeterias and buffets, kiosks and vending, and delivery-only virtual kitchens. Based on ordering channels, the market is classified into dine-in, drive-thru/takeaway, third-party delivery apps, and first-party brand apps. Based on outlet type, the market is classified into independent and chained. Based on geography, the market is classified into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market forecasts are provided in terms of value (USD).

| Burgers and Sandwiches |

| Meat-Based Products |

| Seafood |

| Pasta and Noodles |

| Pizza |

| Desserts and Ice-Creams |

| Others |

| Asian |

| American |

| Italian |

| Chinese |

| Mexican |

| Others |

| Quick Service Restaurants (QSRs) |

| Fast Casual Restaurants |

| Food Trucks and Mobile Units |

| Cafeterias and Buffets |

| Kiosks and Vending |

| Delivery-Only Virtual Kitchens |

| Dine-In |

| Drive Thru/Takeaway |

| Third Party Delivery Apps |

| First Party Brand Apps |

| Independent Outlets |

| Chained Outlets |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Burgers and Sandwiches | |

| Meat-Based Products | ||

| Seafood | ||

| Pasta and Noodles | ||

| Pizza | ||

| Desserts and Ice-Creams | ||

| Others | ||

| By Cuisine Type | Asian | |

| American | ||

| Italian | ||

| Chinese | ||

| Mexican | ||

| Others | ||

| By Restaurant Type | Quick Service Restaurants (QSRs) | |

| Fast Casual Restaurants | ||

| Food Trucks and Mobile Units | ||

| Cafeterias and Buffets | ||

| Kiosks and Vending | ||

| Delivery-Only Virtual Kitchens | ||

| By Ordering Channel | Dine-In | |

| Drive Thru/Takeaway | ||

| Third Party Delivery Apps | ||

| First Party Brand Apps | ||

| By Outlet Type | Independent Outlets | |

| Chained Outlets | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big will the fast food market be by 2031?

It is anticipated to reach USD 2.57 trillion by 2031 and is forecasted to grow at a CAGR of 7.62% during the forecast period from 2026 to 2031.

Which product category is growing the fastest?

Pizza is projected to grow at a CAGR of 8.18% through 2031, fueled by advancements in delivery-focused technologies and the adoption of loyalty applications.

Why are delivery apps important to restaurant sales?

Third-party platforms are anticipated to grow at a CAGR of 8.51% and are forecasted to process over USD 70 billion in annual orders for major brands.

What region offers the highest growth potential?

The Middle East and Africa are projected to achieve a CAGR of 8.95%, driven by a growing young population and increased franchise investments fueling unit expansions.

Page last updated on: