Food & Beverage

2nd MayMarket Analysis of Synthetic Food Colorants for a Beverage Leader

5 Min Read

The Free-From Food Market Report is Segmented by Free-From Type (Gluten-Free, Dairy-Free/Lactose-Free, Meat-Free, Sugar-Free/Low-GI, Other Types), Product Category (Bakery and Cereal Products, Meat Substitutes, Beverages, Baby Foods, Snacks, Other Products), Nature (Conventional, Organic), Distribution Channel (On-Trade, Off-Trade), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

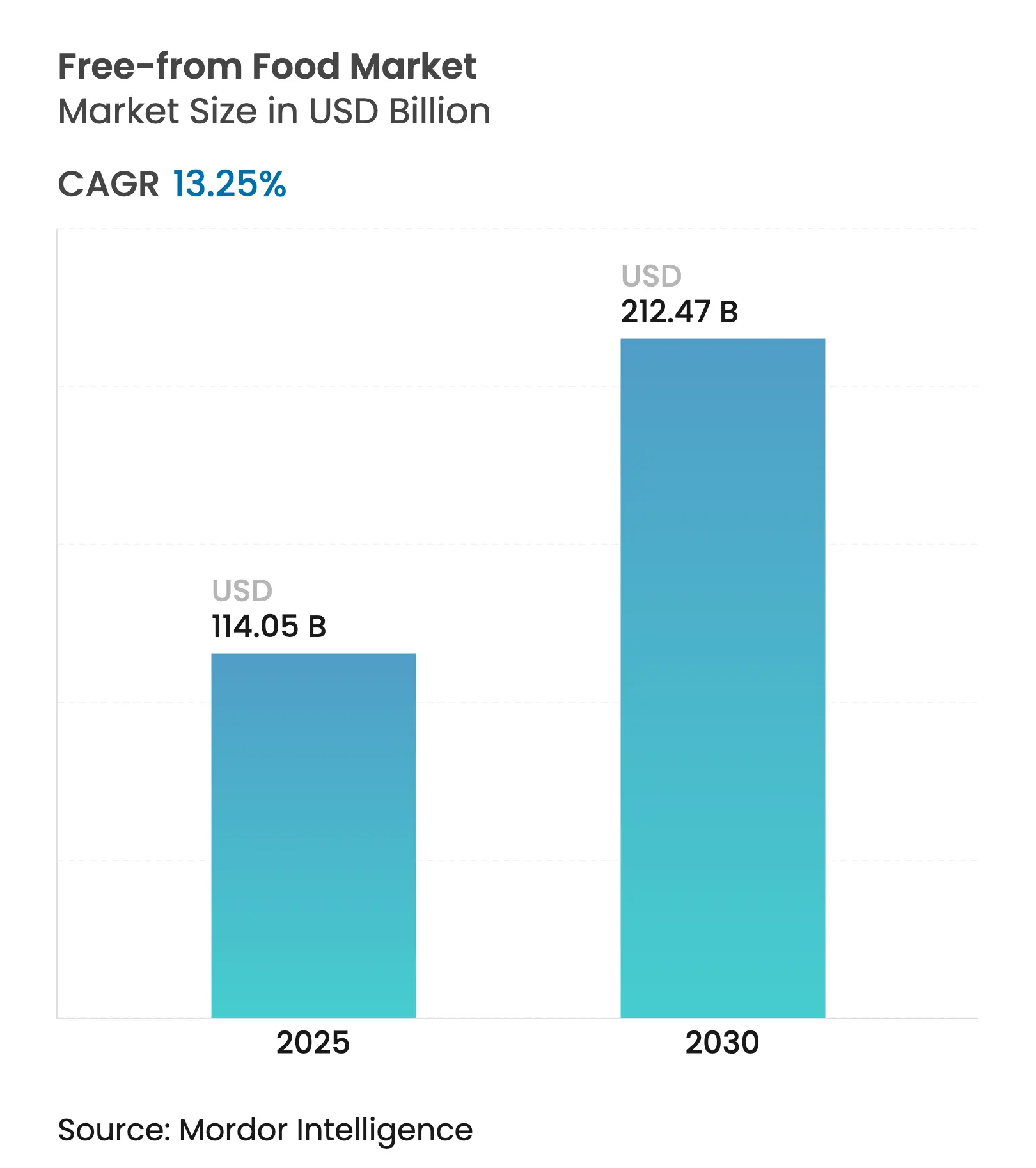

| Market Size (2025) | USD 114.05 Billion |

| Market Size (2030) | USD 212.47 Billion |

| Growth Rate (2025 - 2030) | 13.25 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The free-from food market reached USD 114.05 billion in 2025 and is projected to reach USD 212.47 billion by 2030, delivering a robust 13.25% CAGR that reflects accelerating consumer migration toward allergen-conscious and dietary-restriction products. This growth trajectory positions free-from foods as one of the fastest-expanding segments within the global food industry, driven by regulatory mandates like the FDA's FASTER Act implementation of sesame as the ninth major allergen and rising food allergy prevalence. The market's expansion reflects a fundamental shift from niche dietary accommodation to mainstream consumer preference, with clean-label positioning becoming a competitive necessity rather than premium differentiation.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Prevalence of food allergies and intolerances

Prevalence of food allergies and intolerances

| +3.2% | Global, with highest impact in North America and Europe | Long term (≥ 4 years) |

(~) % Impact on CAGR Forecast

:

+3.2%

|

Geographic Relevance

:

Global, with highest impact in North America and Europe

|

Impact Timeline

:

Long term (≥ 4 years)

|

Clean-label wellness preference shift

Clean-label wellness preference shift

| +2.8% | Global, led by developed markets | Medium term (2-4 years) | |||

Dietary inclusivity and personalization

Dietary inclusivity and personalization

| +2.1% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) | |||

Growth of plant-based and vegan diets

Growth of plant-based and vegan diets

| +2.5% | Global, with early adoption in North America and Europe | Long term (≥ 4 years) | |||

Product development innovation

Product development innovation

| +1.9% | Global, concentrated in innovation hubs | Short term (≤ 2 years) | |||

Influence of social media and food bloggers

Influence of social media and food bloggers

| +1.0% | Global, particularly strong in Asia-Pacific | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Prevalence of Food Allergies and Intolerances

Food allergy prevalence has reached epidemic proportions, with the CDC documenting that food allergies affect 1 in 13 children, fundamentally reshaping institutional food service procurement and manufacturing protocols[1]Source: U.S. Centers for Disease Control and Prevention, “Food Allergies in Schools,” cdc.gov. The FDA's March 2025 updated Food Allergen Q&A Guidance (Fifth Edition) now includes sesame as the ninth major allergen under FALCPA, expanding mandatory labeling requirements and creating compliance costs that favor larger manufacturers with sophisticated allergen control systems[2]Source: U.S. Food and Drug Administration, “Nutrition, Food Labeling, and Critical Foods - Food Allergies,” fda.gov. This regulatory expansion creates barriers for smaller manufacturers while simultaneously expanding the addressable market for compliant free-from products. Cross-reactivity patterns between allergens drive consumers toward multiple-allergen-free products, explaining why dedicated facilities command premium pricing despite higher operational complexity. The medical necessity of allergen avoidance creates price-inelastic demand that insulates free-from manufacturers from economic downturns, unlike discretionary wellness products.

Clean-Label Wellness Preference Shift

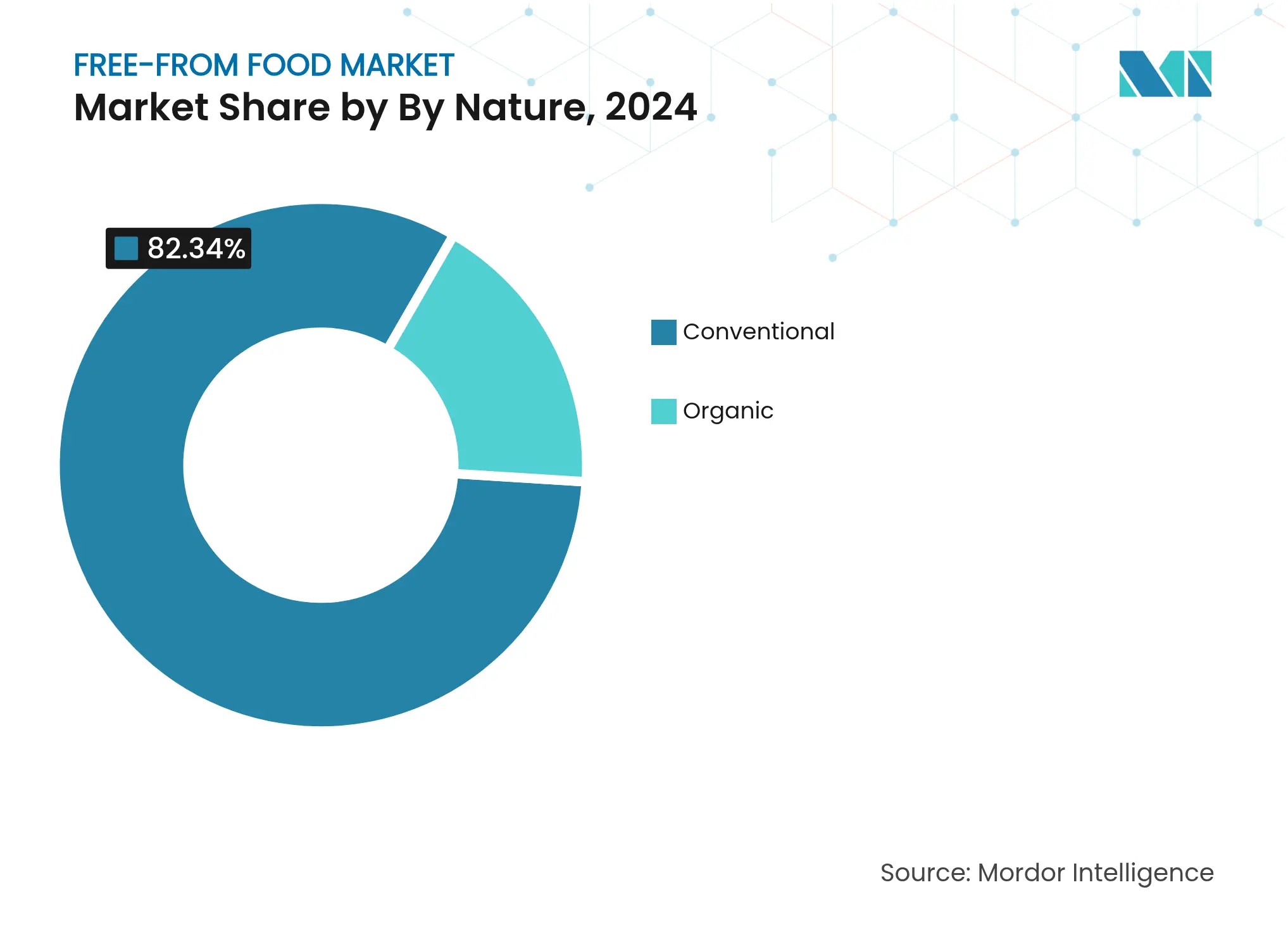

Consumer demand for recognizable ingredients has evolved beyond simple organic certification to encompass processing method transparency and supply chain traceability, with consumers willing to pay premiums for products with fewer than 5 ingredients. Clean-label positioning intersects with free-from claims to create compound value propositions, where gluten-free products also eliminate artificial preservatives and synthetic emulsifiers to appeal to broader wellness-conscious demographics. This convergence explains why conventional free-from products maintain 82.34% market share despite organic alternatives growing faster, consumers prioritize ingredient simplicity over organic certification when forced to choose. Manufacturing complexity increases exponentially when combining multiple clean-label requirements with allergen-free protocols, creating competitive moats for companies that master both simultaneously. The clean-label trend also drives innovation in alternative binding agents and texture enhancers, as traditional wheat-based and dairy-based functional ingredients become unavailable in free-from formulations.

Dietary Inclusivity and Personalization

Personalized nutrition platforms now integrate genetic testing, microbiome analysis, and food sensitivity screening to create individualized dietary recommendations that often include multiple free-from requirements, expanding the addressable market beyond traditional allergy sufferers. This trend transforms free-from foods from medical necessity products to lifestyle optimization tools, explaining the 15.84% CAGR growth in organic free-from segments where health positioning commands higher margins. Corporate wellness programs increasingly accommodate diverse dietary restrictions in cafeteria offerings and catered events, creating institutional demand channels that bypass traditional retail distribution. The intersection of dietary personalization with cultural and religious dietary laws creates complex formulation requirements that favor manufacturers with diverse ingredient sourcing capabilities. Technology-enabled customization allows direct-to-consumer brands to offer personalized free-from product combinations, disrupting traditional one-size-fits-all retail assortments.

Growth of Plant-Based and Vegan Diets

Plant-based diet adoption has transcended ethical motivations to encompass environmental sustainability and health optimization, with the Good Food Institute documenting USD 8.1 billion in U.S. retail plant-based food sales in 2023 despite category maturation challenges[3]Source: Good Food Institute, “2023 State of the Industry Report Plant-based Meat, Seafood, Eggs, and Dairy,” gfi.org. The convergence of plant-based and free-from positioning creates products that simultaneously address multiple consumer concerns, allergen avoidance, environmental impact, and health optimization, explaining why meat-free alternatives achieve a 14.11% CAGR despite representing a smaller current market share. Precision fermentation technologies enable the production of animal-identical proteins without allergens, creating opportunities for products that deliver familiar taste profiles while meeting free-from requirements. Government support for alternative protein research, including Canada's CAD 150 million investment and similar commitments across Europe and Asia, accelerates innovation cycles and reduces time-to-market for novel plant-based free-from products. The plant-based trend also drives ingredient diversification beyond traditional soy and wheat alternatives, with companies exploring hemp, pea, and algae proteins that naturally avoid common allergens.

Restraints Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Premium pricing vs. conventional products

Premium pricing vs. conventional products

| -2.1% | Global, most pronounced in price-sensitive emerging markets | Medium term (2-4 years) |

(~)% Impact on CAGR Forecast

:

-2.1%

|

Geographic Relevance

:

Global, most pronounced in price-sensitive emerging

markets

|

Impact Timeline

:

Medium term (2-4 years)

|

Manufacturing cross-contamination recalls

Manufacturing cross-contamination recalls

| -1.5% | Global, with highest impact in North America and Europe | Short term (≤ 2 years) | |||

Taste and texture challenges

Taste and texture challenges

| -1.8% | Global, particularly affecting plant-based segments | Long term (≥ 4 years) | |||

Inconsistent allergen labeling laws and regulatory

standards

Inconsistent allergen labeling laws and regulatory

standards

| -0.9% | Global, with regional variation in enforcement | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Premium Pricing vs. Conventional Products

Free-from products command price premiums that can exceed 400% for staple items like bread, with Coeliac UK documenting that gluten-free loaves cost 4.5 times more than conventional alternatives, creating affordability barriers that limit market penetration among price-sensitive demographics. Manufacturing economics drive these premiums through specialized ingredient sourcing, dedicated production lines, extensive testing protocols, and smaller production volumes that prevent economies of scale. The pricing gap creates vulnerability to economic downturns and limits adoption among households where free-from products represent discretionary rather than medical spending. Private label strategies by major retailers attempt to address price sensitivity through volume purchasing and simplified formulations, yet quality compromises often reinforce consumer perceptions that affordable free-from products deliver inferior experiences. Scale advantages increasingly favor large manufacturers who can amortize specialized equipment costs across multiple product lines and geographic markets, creating consolidation pressure within the industry.

Manufacturing Cross-Contamination Recalls

Cross-contamination incidents trigger costly recalls and permanent brand damage, with even trace allergen presence creating life-threatening reactions that expose manufacturers to significant liability risks and regulatory penalties. The complexity of maintaining allergen-free environments increases exponentially with facility size and product diversity, explaining why dedicated single-allergen facilities often outperform multi-product operations despite higher fixed costs. Advanced testing protocols and environmental monitoring systems represent significant capital investments that create barriers to entry for smaller manufacturers while favoring companies with sophisticated quality management systems. Supplier qualification and ingredient traceability requirements extend contamination risks throughout the supply chain, creating dependencies on specialized ingredient suppliers who command premium pricing. The recall risk also drives insurance costs and working capital requirements higher for free-from manufacturers compared to conventional food producers, affecting overall profitability and investment attractiveness.

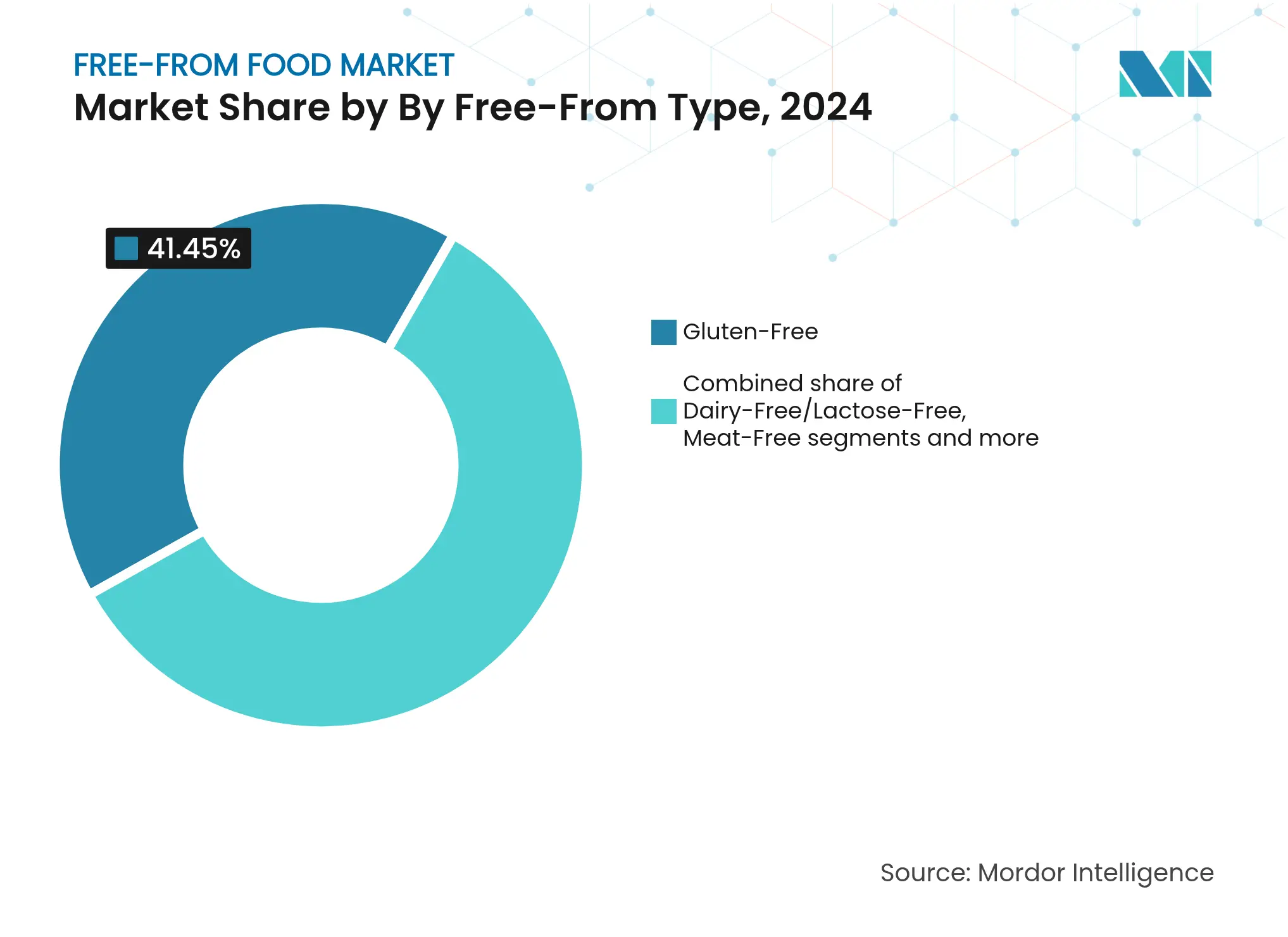

By Free-From Type: Plant-Based Proteins Drive Category Evolution

Meat-free (plant-based) alternatives accelerate at a 14.11% CAGR through 2030, outpacing the established gluten-free segment's 41.45% market share in 2024, indicating consumer willingness to experiment with protein diversification beyond traditional allergen avoidance. The plant-based surge reflects technological breakthroughs in texture replication and flavor enhancement, with companies like Cargill investing in fermented mycoprotein ingredients that deliver meat-like experiences without common allergens.

Sugar-free and low-GI alternatives benefit from diabetes prevalence and weight management trends, yet face formulation challenges in replicating sweetness profiles without artificial ingredients that conflict with clean-label positioning. The convergence of multiple free-from attributes in single products, such as gluten-free, dairy-free, and plant-based combinations, creates premium positioning opportunities that justify higher manufacturing costs through expanded addressable markets.

Note: Segment shares of all individual segments available upon report purchase

By Product Category: Meat Substitutes Reshape Protein Consumption

Meat substitutes and analogues surge at a 15.04% CAGR, challenging the dominance of bakery and cereal products' 24.56% market share in 2024, as protein alternatives expand beyond traditional vegetarian demographics to include flexitarian and health-conscious consumers. The acceleration reflects technological advances in extrusion processing and precision fermentation that enable animal-identical taste and texture profiles without allergens, with companies like Ingredion partnering with Lantmännen to develop pea protein isolates specifically for European markets.

Baby and infant foods represent a critical growth segment where allergen-free requirements intersect with nutritional completeness demands, creating complex formulation challenges that favor specialized manufacturers with pediatric nutrition expertise. Snacks and ready-to-eat meals benefit from convenience trends and portion control positioning, yet face shelf-life challenges when eliminating traditional preservatives to maintain clean-label profiles. The category evolution reflects meal occasion expansion, where free-from products transition from specialty dietary accommodation to mainstream meal solutions across breakfast, lunch, dinner, and snacking occasions.

By Nature: Organic Premium Positioning Accelerates

Organic free-from products accelerate at 15.84% CAGR despite conventional alternatives maintaining 82.34% market share in 2024, indicating consumer willingness to pay compound premiums for products that combine allergen-free and organic certifications. The organic acceleration reflects supply chain maturation as specialized ingredient suppliers develop certified organic alternatives to traditional wheat, dairy, and egg-based functional ingredients, reducing formulation compromises that historically limited organic free-from product quality. Regulatory compliance factors favor organic positioning as USDA Organic standards inherently exclude many synthetic additives and processing aids that conflict with clean-label consumer expectations.

The price sensitivity dynamic creates market segmentation where organic free-from products serve affluent health-conscious demographics while conventional free-from products address medically-necessary allergen avoidance across broader income levels. Manufacturing complexity increases when combining organic certification with allergen-free protocols, as organic ingredient sourcing often involves smaller suppliers with limited capacity for dedicated allergen-free production runs. The organic trend also drives innovation in alternative sweeteners and binding agents derived from organic sources, creating intellectual property opportunities for ingredient suppliers who develop novel organic functional ingredients.

By Distribution Channel: E-Commerce Disrupts Traditional Retail

Online retail channels surge at 15.76% CAGR while supermarkets/hypermarkets maintain 48.34% share in 2024, reflecting direct-to-consumer strategies that enable specialized free-from brands to bypass traditional retail markup structures and shelf space limitations. The e-commerce acceleration benefits from subscription models that provide predictable revenue streams for manufacturers while offering convenience and cost savings for consumers who require consistent access to specialized products. Specialty stores continue serving discovery and education functions where knowledgeable staff help consumers navigate complex ingredient lists and cross-contamination concerns.

Convenience stores represent an emerging opportunity as grab-and-go free-from snacks align with busy lifestyle patterns, yet face challenges in maintaining product freshness and variety within limited shelf space. The distribution evolution reflects changing consumer shopping behaviors where online research precedes in-store purchases, creating omnichannel requirements that favor brands with strong digital marketing capabilities and retail partnerships. Off-trade channels benefit from private label expansion as major retailers develop house-brand free-from products to capture margin opportunities while offering lower-priced alternatives to national brands.

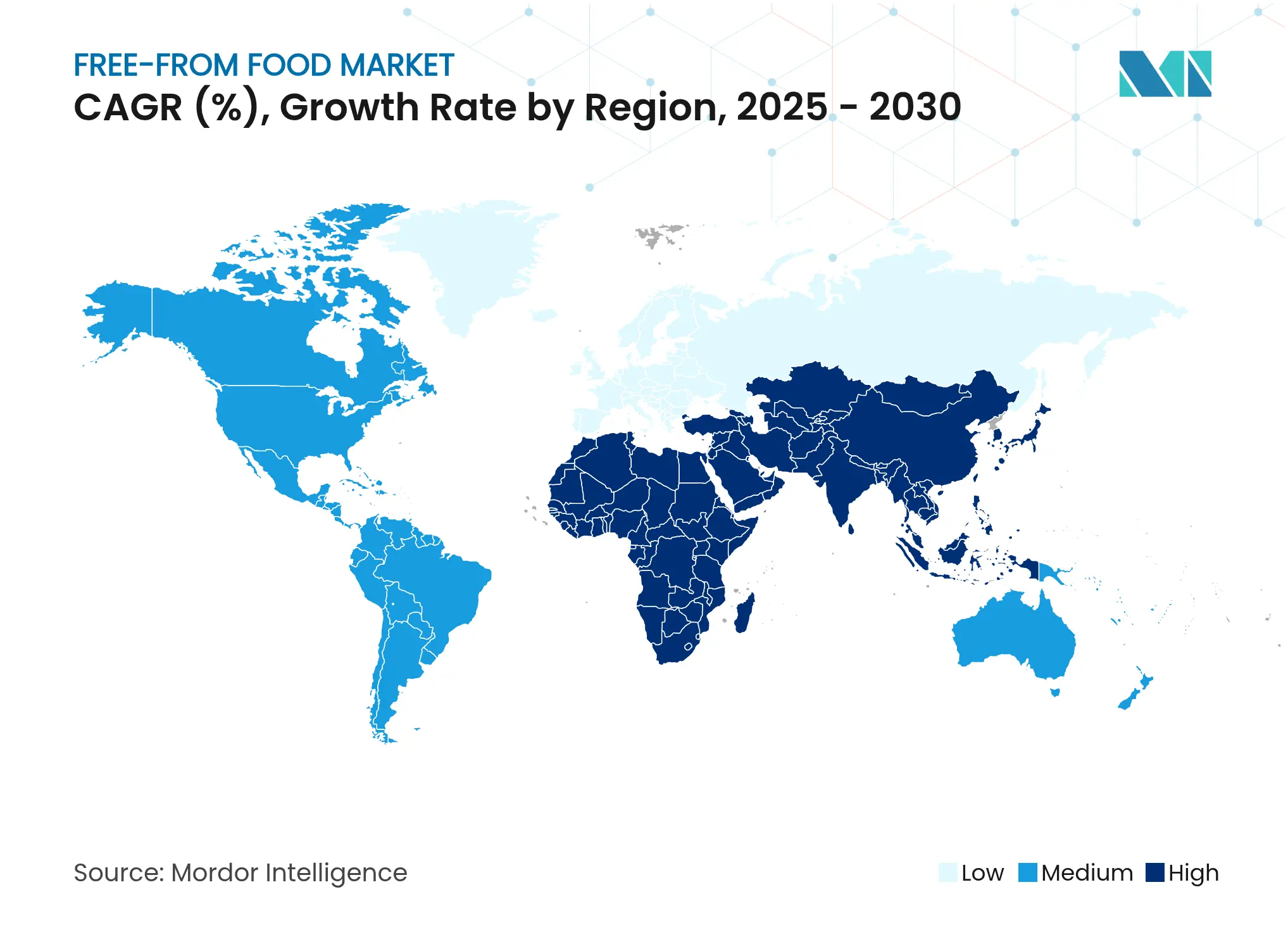

North America commands 34.31% market share in 2024, driven by sophisticated regulatory frameworks, including the FDA's FASTER Act implementation and extensive food allergy awareness campaigns that create institutional demand across schools, healthcare facilities, and corporate foodservice operations. The region benefits from established supply chains for alternative ingredients and consumer willingness to pay premiums for specialized products, yet faces market maturation challenges as growth rates moderate in established categories.

Asia-Pacific emerges as the fastest-growing region with 15.43% CAGR through 2030, reflecting rising disposable incomes, urbanization trends, and increasing food allergy awareness in countries like China, India, and Japan, where traditional diets historically provided natural allergen avoidance. Singapore's 2024 amendments to gluten-free food regulations demonstrate regulatory sophistication that enables premium product positioning, while creating compliance requirements that favor established international brands over local manufacturers.

Europe leverages stringent EFSA allergen guidelines to create premium positioning opportunities for compliant manufacturers, while regulatory harmonization across EU member states enables efficient cross-border distribution of specialized products. The region's focus on sustainability intersects with free-from positioning to create compound value propositions, particularly in plant-based segments where environmental benefits justify premium pricing. Brexit complications create supply chain challenges for United Kingdom-based manufacturers who previously relied on EU ingredient sourcing, driving localization investments and alternative supplier relationships that may ultimately strengthen supply chain resilience.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Market Concentration

The free-from food market is moderately fragmented. This fragmentation creates opportunities for multinational food companies to acquire smaller players and expand their allergen-free product portfolios to meet increasing consumer demand. Strategic patterns reveal three distinct competitive approaches: multinational incumbents like Nestlé and General Mills leverage global distribution networks and manufacturing scale to acquire innovative free-from brands, while specialized pure-play companies focus on product innovation and direct-to-consumer channels to build premium brand positioning.

Technology adoption becomes a critical competitive differentiator, with companies investing in precision fermentation, advanced extrusion processing, and cross-contamination prevention systems to achieve superior product quality and manufacturing efficiency. White-space opportunities emerge in institutional foodservice channels where dietary accommodation requirements create predictable demand volumes, yet few manufacturers have developed specialized distribution capabilities for healthcare, education, and corporate catering markets.

Emerging disruptors leverage direct-to-consumer e-commerce platforms and subscription models to bypass traditional retail intermediaries, enabling higher margins and direct customer relationships that provide valuable consumption data for product development. The competitive landscape increasingly favors companies that can navigate complex regulatory requirements across multiple jurisdictions while maintaining cost competitiveness against conventional alternatives, creating consolidation pressure that benefits larger players with sophisticated compliance capabilities and manufacturing scale advantages.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Free-from foods are foods made without ingredients like gluten, dairy, or nuts.

The global free-from food market is segmented by type, end product, distribution channel, and geography. Based on type, the market is segmented into gluten-free, dairy-free, meat-free, and other types. Based on the end product, the market is segmented into baby food, dairy-free foods, meat substitutes, beverages, and other end products. Based on the distribution channel, the market is segmented into supermarkets/hypermarkets, online retail stores, convenience stores, and other distribution channels. Moreover, the study provides an analysis of the free-from food market in emerging and established markets across the world, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The report offers market size and forecasts for the free-from food market in value (USD million) for all the above segments.

Market Analysis of Synthetic Food Colorants for a Beverage Leader

5 Min Read

Strategic Expansion in the Russia Laundry Appliances Market

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.