Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 37.55 Billion |

| Market Size (2031) | USD 47.42 Billion |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

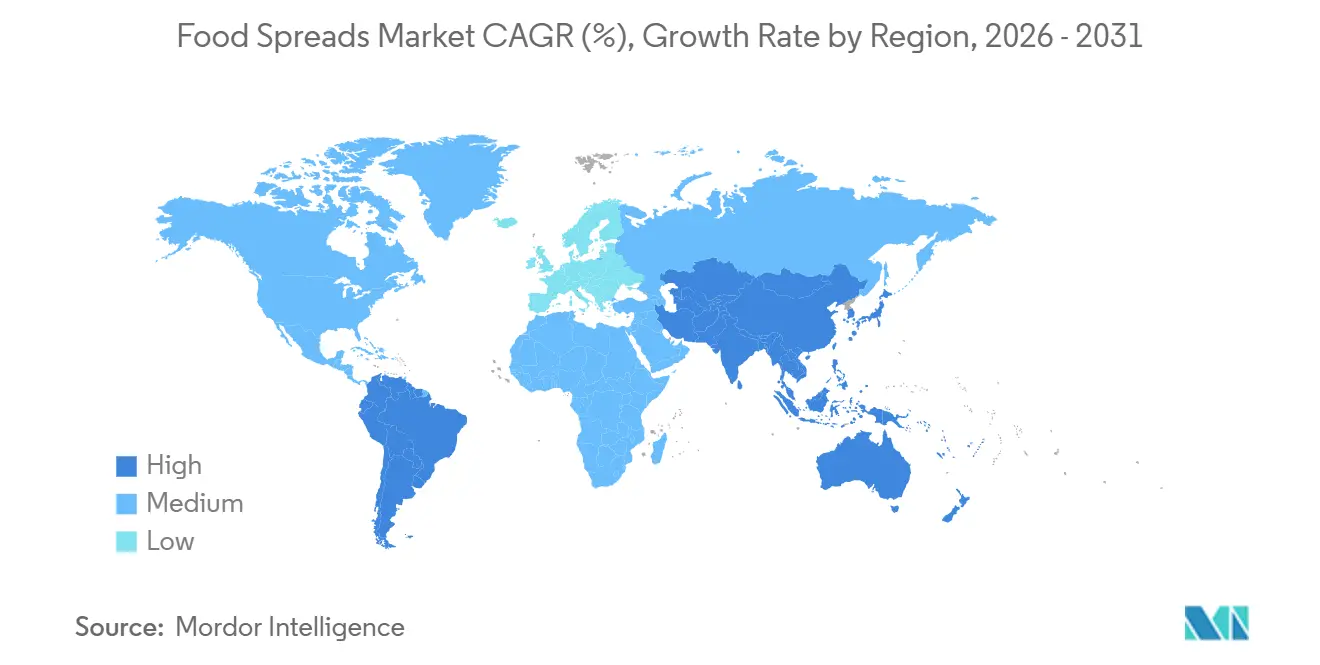

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

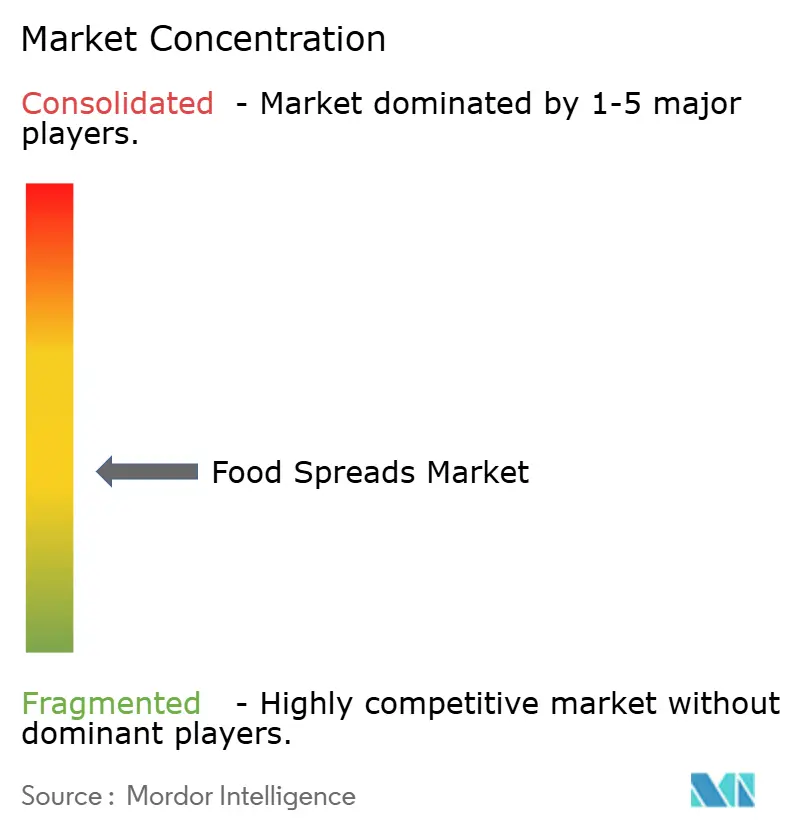

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Food Spreads Market Analysis by Mordor Intelligence

The Food Spreads Market size is projected to increase from USD 35.84 billion in 2025 to USD 37.55 billion in 2026, and reach USD 47.42 billion by 2031, growing at a CAGR of 4.78% from 2026 to 2031. This growth is mainly driven by higher disposable incomes, a growing focus on healthy eating, and the shift of spreads from being simple condiments to versatile meal ingredients. Europe remains the leading market due to its strong breakfast traditions, premium private-label products, and widespread supermarket networks. On the other hand, the Asia-Pacific region is becoming the fastest-growing market, supported by urbanization, higher protein consumption, and the adoption of Western-style breakfasts. Honey is the largest and fastest-growing product segment, thanks to its natural qualities and health benefits. E-commerce is growing twice as fast as traditional retail, encouraging companies to strengthen their omnichannel distribution strategies. Additionally, innovations in packaging, such as recyclable pouches, are gaining popularity for their convenience and eco-friendly appeal, especially among younger consumers.

Key Report Takeaways

- By product type, honey dominated the food spreads market with a 31.56% share in 2025 and is expected to grow at a 7.23% CAGR through 2031.

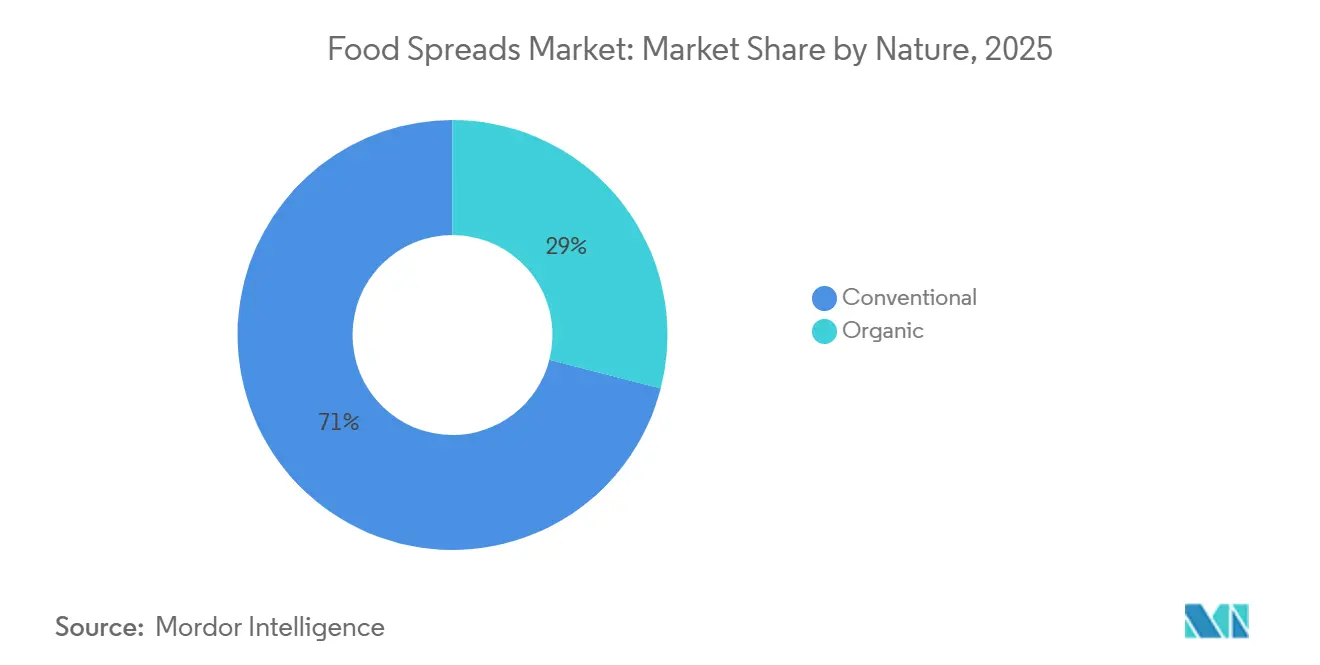

- By nature, the conventional segment accounted for 71.02% of the food spreads market in 2025, while the organic segment is projected to grow at a 9.84% CAGR during 2026-2031.

- By packaging type, jars represented 47.37% of the food spreads market in 2025, with sachets and pouches expected to grow at a 6.94% CAGR through 2031.

- By distribution channels, supermarkets/hypermarkets generated 55.81% of revenue in 2025, while online retail is expected to grow at an 11.72% CAGR through 2031.

- By geography, Europe held the largest market share at 34.01% in 2025, while Asia-Pacific is projected to grow at a 9.01% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Food Spreads Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Busy lifestyles increase the preference for convenient and versatile food options | +1.2% | Global, with higher impact in North America and Europe | Short term (≤ 2 years) |

| Rising demand for exotic and regionally sourced fruit flavors drives product innovation | +0.8% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Growing popularity of plant-based diets fuels demand for vegan spreads | +0.7% | Europe, North America, and urban centers in Asia-Pacific | Medium term (2-4 years) |

| Aggressive marketing and branding influences market growth | +0.5% | Global | Short term (≤ 2 years) |

| Increasing popularity of snacking between meals enhances usage of spreads in diverse formats | +0.6% | North America, Europe, and urban Asia | Short term (≤ 2 years) |

| Flavor innovations attract consumers seeking diverse taste experiences | +0.4% | Global, with higher impact in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Busy lifestyles increase the preference for convenient and versatile food options

Households spend an average of USD 165 weekly on groceries, according to the Food Industry Association's 2024 data [1]Source: Food Industry Association, "Consumers' weekly grocery expenditure in the United States", fmi.org. Modern lifestyles have increased the use of spreads, expanding their role from just breakfast to lunch boxes, office snacks, and quick meals because of their convenience. In households with dual incomes, where time is limited, spreads play an essential role in meal preparation. Manufacturers are introducing creative packaging, with single-serve formats growing at twice the rate of family-size options. New spread varieties are being developed to suit different meal occasions and dietary needs. Companies are promoting spreads as flexible meal options, supported by the growing popularity of all-day breakfast foods. This trend has driven more investments in product innovation and marketing to showcase the versatile use of spreads in today’s meals.

Rising demand for exotic and regionally sourced fruit flavors drives product innovation

Consumer tastes are shifting toward spreads with unique flavors and regional ingredients, transforming meals into distinctive experiences. The 2025 flavor forecast highlights brown sugar as the "Flavor of the Year," reflecting a trend toward complex taste profiles blending sweetness with complementary notes [2]Source: T. Hasegawa Co. Ltd., "Flavor Trends 2025", thasegawa.com. Limited-edition and seasonal varieties featuring local and exotic fruits are opening up opportunities for premium pricing. These unique flavors are also seen as healthier, as consumers connect exotic fruits with added nutrition and health benefits. It is important to combine new and familiar elements, creating products that are interesting yet easy to try. Hot honey varieties are a good example, blending the familiar sweetness of honey with an unexpected spicy twist.

Growing popularity of plant-based diets fuels demand for vegan spreads

The plant-based movement is driving innovation in spreads, with manufacturers removing animal-derived ingredients while maintaining taste and texture. USDA data shows German plant-based food consumption reached 1.58 billion in 2023 [3]Source: The United States Department of Agriculture, "Germany: Plant-Based Food Goes Mainstream in Germany", fas.usda.gov. Brands are not just removing ingredients; they're emphasizing sustainability, ethical sourcing, and health benefits. Plant-based spreads, marketed as premium products, come with a higher price tag, reflecting consumers' preference for eco-friendly and health-centric choices. The market is on the rise, with nut-based spreads, including cashew and almond, along with seed-based varieties, emerging as popular protein-rich alternatives to dairy. In May 2024, Ferrero introduced a plant-based version of Nutella, crafted from chickpea and rice syrup.

Aggressive marketing and branding influences market growth

In the highly competitive food spreads market, brand positioning and marketing strategies play a crucial role in standing out. Companies use digital platforms to build stronger connections with consumers, focusing on more than just product features. These brands aim to engage meaningfully by showcasing their unique strengths. They connect with consumers by promoting sustainability, ensuring transparent supply chains, and sharing interesting stories about their products' origins. Zespri, a New Zealand brand known for its kiwifruit products, launched a campaign featuring “furry fruits” with the tagline “Feel Alive.” This campaign used television, digital platforms, and out-of-home (OOH) advertising to grab attention and engage audiences. Its humor and energy appealed especially to younger consumers, helping Zespri strengthen its market position. At the same time, social commerce platforms have changed how brands interact with consumers, making these interactions more direct, genuine, and aligned with changing expectations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns over high sugar and fat content in certain spreads restrict growth | -0.7% | North America and Europe | Medium term (2-4 years) |

| Intense competition from private labels and regional players impacts profitability | -0.5% | Global, with higher impact in Europe | Medium term (2-4 years) |

| Price volatility in fruits affects food spreads market growth | -0.4% | Global, with higher impact in fruit-based spread producing regions | Short term (≤ 2 years) |

| Consumer scepticism over preservatives or palm oil usage restricts some product segments | -0.3% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health concerns over high sugar and fat content in certain spread restricts growth

Consumers are becoming more aware of the nutritional content in their food, putting pressure on traditional spreads that are high in sugar and fat. Manufacturers now face the challenge of improving these products without losing the flavors that encourage repeat purchases. In 2024, the George Institute for Global Health analyzed 53,315 packaged foods and found that only 34% met the Health Star Rating for 'healthier' products. This highlights significant nutritional issues in categories like spreads. The market is dividing into two segments: indulgent spreads promoted as occasional treats and healthier spreads for everyday use, with the latter growing 1.5 times faster. Regulatory measures, such as front-of-pack nutritional labeling, are adding to the challenge by making sugar and fat content more visible to consumers. To address these issues, manufacturers are focusing on using alternative sweeteners, healthier fats, and functional ingredients to improve nutrition and position spreads as a healthier part of the diet.

Intense competition from private labels and regional players impacts profitability

Retailers are changing the food spreads market by using consumer insights and efficient supply chains to create private label products that compete with national brands, often at lower prices. Regional players add to the competition by sourcing ingredients locally and producing nearby, which helps them offer authentic and affordable options. In response, national brands are focusing on innovation, better quality, and their brand reputation to justify higher prices. However, this strategy is challenging in price-sensitive segments. To adapt, established brands might need to simplify their product ranges to highlight high-margin, unique items and consider collaborating with retailers for co-manufacturing. This could help them maintain production levels while adjusting to the shifting market trends.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Honey Leads Through Functional Versatility

In 2025, honey makes up 31.56% of the food spreads market, driven by its versatility and image as a healthy choice. From 2026 to 2031, it is projected to grow at the fastest rate among spreads, with a CAGR of 7.23%, as more consumers shift away from refined sugars. Premium types like Manuka and Kanuka are priced higher because of their health benefits and limited availability. The market is also growing due to new product launches, such as Apis India's organic honey, introduced in January 2024. This honey, sourced from certified organic farms in Kashmir, is priced at INR 240 for a 450g glass bottle.

Nut and seed-based spreads are gaining popularity due to the increasing focus on protein-rich diets and plant-based eating trends. Innovations in texture and flavor are further boosting their appeal. Dairy and cheese spreads remain steady in the market, offering convenience despite rising competition from plant-based alternatives. Fish, meat-based, and vegan spreads are carving out niche markets by catering to specific dietary preferences. Across all categories, premium products are becoming more popular, with factors like origin, high-quality ingredients, and production methods driving higher prices and adding value.

By Nature: Organic Growth Outpaces Conventional

In 2025, the conventional segment accounted for a significant 71.02% market share, supported by its wide availability, strong brand loyalty, and affordable pricing. On the other hand, the organic segment is expected to grow at a CAGR of 9.84% from 2026 to 2031, driven by increasing consumer preference for clean labels and eco-friendly production methods. The UK organic food and drink market demonstrates this trend, reaching GBP 3.7 billion in 2025, with a 7.3% increase in sales marking its thirteenth consecutive year of growth [4]Source: Soil Association, "Organic Market Report 2025", soilassociation.org.

The price difference between organic and conventional spreads is shrinking as organic supply chains become more efficient. Online sales of organic spreads are significantly higher, with digital purchases being twice as much as those of conventional spreads. Major retailers are making organic products more accessible by increasing shelf space and launching private-label organic options. Successful organic brands focus on highlighting the specific benefits of organic certification in their marketing, rather than relying only on the certification itself to attract consumers.

By Packaging Type: Sachets Challenge Jar Dominance

In 2025, jars hold a dominant 47.37% market share due to their ease of scooping, resealing ability, and clear visibility on store shelves. Sachets and pouches are gaining popularity for their portability, portion control, and lower environmental impact, with a strong CAGR of 6.94% expected from 2026 to 2031. Additionally, global regulations introduced in 2025 to reduce waste and support sustainability are driving changes in food spread packaging.

Tubs provide a good balance of convenience and product protection, while formats like cups, cans, and tetra packs serve specific regional and niche markets with a smaller but stable share. Packaging innovations now focus on using recyclable materials, lightweight designs, and improved barriers to extend shelf life without adding preservatives. In October 2024, Crofter's Organic, North America’s largest organic fruit spread producer, launched recyclable squeeze pouches. Modern packaging also includes QR codes that give consumers information about product origins, usage, and sustainability, improving engagement.

By Distribution Channel: Online Retail Disrupts Traditional Models

In 2025, supermarkets and hypermarkets held 55.81% of the market share. This dominance comes from their wide availability, large variety of products, and in-store promotions that encourage impulse buying. Their success is further supported by their extensive geographic reach, a mix of branded and private-label products, and strategic shelf placements that attract customers. Additionally, these stores are popular for one-stop shopping, especially for regular household food purchases.

In contrast, online retail is predicted to grow the fastest, with a CAGR of 11.72% projected for 2026-2031. This growth is driven by consumers seeking convenience, easy product comparisons, and access to unique items not commonly found in physical stores. The increasing use of e-grocery platforms, time-saving home delivery options, and the ability to compare prices, ingredients, and nutritional details are key factors behind this trend. Online platforms also offer premium, imported, and niche food spreads that are often unavailable in physical stores, contributing to their faster growth despite a smaller current market share.

Geography Analysis

Europe holds the largest regional market share at 34.01% in 2025, supported by established consumption patterns and advanced retail infrastructure that enables product discovery and premiumization. To attract consumers' attention, new premium quality sweet spread products with eco-friendly packaging are being introduced in the European market. The trend of baking at home has also contributed to the growth of the food spread market, as spreads are used in various baking operations throughout the day. However, sweet spreads face a challenge in terms of health and wellness, as they are often high in sugar, except for honey, which is still popular due to its anti-bacterial properties. European regulatory requirements for nutritional labeling and sustainable packaging continue to influence product formulation and packaging decisions.

Asia-Pacific leads market growth with a projected CAGR of 9.01% from 2026-2031, influenced by urbanization, increased disposable incomes, and western dietary adoption in major markets. China and India drive this growth as their expanding middle classes incorporate spreads into breakfast routines. Japan's market offers opportunities through its distinct distribution system and high food import dependence. E-commerce expansion enables brands to reach consumers in smaller cities without extensive physical retail networks.

North America maintains a mature market focused on innovation, with the United States emphasizing premium and specialty spreads that meet convenience and health requirements. The market features a distinct split between value-focused private label products and premium branded offerings with specialized ingredients or functional properties. South America, and Middle East and Africa show growth potential through increasing urbanization and Western dietary influence. Brazil dominates South American production in honey and fruit-based spreads, while the United Arab Emirates and Saudi Arabia lead Middle Eastern growth, supported by expatriate communities and tourism-driven international food demand.

Competitive Landscape

The food spreads market demonstrates moderate concentration, with multinational companies competing with regional manufacturers and new market entrants. Unilever PLC, The Hershey Company, Ferrero International S.A., Hormel Foods LLC, and The J.M. Smucker Company are some of the major players in the global market. The competitive environment continues to evolve as consumer preferences shift toward healthier and more diverse product options. Large global companies focus on portfolio optimization and economies of scale, while specialized producers emphasize flexibility and authentic brand messaging to attract consumers seeking alternative products.

The market presents significant growth opportunities in innovative products that combine elements of spreads, dips, toppings, and functional foods. New entrants are expanding through direct-to-consumer sales channels, capitalizing on changing consumer shopping behaviors and digital platforms. Established companies increasingly use data analytics and AI to enhance product development and marketing strategies, enabling them to respond quickly to market trends and consumer demands.

Private label products continue to gain market share in the food spreads segment, as retailers utilize consumer data and efficient supply chains to offer competitively priced alternatives to branded products. These private label offerings often match or exceed the quality of national brands while maintaining lower price points, appealing to value-conscious consumers. The expansion of private labels has intensified competition, forcing branded manufacturers to differentiate through innovation, quality, and marketing initiatives.

Food Spreads Industry Leaders

-

The J. M. Smucker Company

-

Unilever PLC

-

Ferrero International S.A.

-

The Hershey Company

-

Hormel Foods LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Ferrero North America introduced Nutella Peanut, a new product that combines its cocoa hazelnut spread with roasted peanuts. This innovative blend merges the traditional Nutella spread's rich cocoa-hazelnut flavor with the distinct taste of roasted peanuts, offering consumers a new flavor experience.

- May 2025: Sweet Freedom introduced a nut-free chocolate hazelnut-flavored spread to meet the growing consumer demand for allergen-free products. The spread offers a safe alternative for consumers with nut allergies while maintaining the authentic taste of traditional hazelnut spreads. The product is sweetened naturally with apple and carob, eliminating the need for artificial sweeteners and aligning with the increasing preference for clean-label products.

- May 2025: Pip & Nut introduced a new Chocolate Hazelnut Spread to its product portfolio in the United Kingdom. The spread contains 63% nuts and offers higher protein content and lower sugar levels compared to conventional chocolate spreads. This product aligns with the company's focus on natural, healthier, and sustainable alternatives in the spreads and snacks market.

- January 2025: Country Delight launched Farm Honey, which underwent Nuclear Magnetic Resonance (NMR) testing at a certified laboratory in Germany. The NMR testing validates the authenticity and purity of the honey product for Indian consumers.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the food spreads market as all ready-to-eat, semi-solid preparations, honey, fruit preserves, chocolate toppings, nut or seed butters, and dairy-based cheese spreads that consumers typically smear on bread, crackers, or similar carriers for flavor, convenience, or nutrition. The scope follows how retailers label the "spreads" shelf and mirrors HS codes tracked by FAO and UN Comtrade.

Scope exclusion: Items promoted mainly as dips, cooking sauces, powdered mix-ins, or confectionery coatings sit outside this study.

Segmentation Overview

-

By Product Type

- Honey

- Chocolate-based Spreads

- Fruit-based Spreads

- Nut- and Seed-based Spreads

- Dairy and Cheese Spreads

- Other Product Types

-

By Nature

- Conventional

- Organic

-

By Packaging Type

- Jars

- Tubs

- Sachets/Pouches

- Others

-

By Distribution Channel

- Supermarkets/Hypermarkets

- Convenience Stores

- Online Retail Stores

- Other Distribution Channels

-

By Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Netherlands

- Poland

- Belgium

- Sweden

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Indonesia

- South Korea

- Thailand

- Singapore

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Colombia

- Chile

- Peru

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Nigeria

- Egypt

- Morocco

- Turkey

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts hold structured calls and online surveys with spread makers' procurement heads, grocery category buyers across North America, Europe, and Asia, and export brokers trading honey or nut pastes. These direct views validate consumption ratios, packaging shifts, and average selling prices that secondary data alone cannot capture.

Desk Research

We rely on public datasets such as FAOStat crop output, UN Comtrade trade flows, USDA ERS honey tables, and Codex additive limits to frame supply, demand, and rules. Trade bodies, for example, the International Nut and Dried Fruit Council and the International Dairy Federation, publish shipment bulletins that help our team benchmark ingredient availability. Company 10-Ks, investor decks, and news portals like FoodNavigator reveal price moves and product launches. Subscription resources, including D&B Hoovers and Dow Jones Factiva, speed access to manufacturer financials. The sources named illustrate our desk work, yet many others are also reviewed.

Market-Sizing & Forecasting

Our model begins with a top-down rebuild. Global output of fruit, nuts, dairy fat, cocoa, and honey is converted into spreadable volumes, which are then tested against retail penetration checks. Targeted bottom-up roll-ups of leading producer revenues and sampled ASP × volume data keep totals realistic. Key variables include per-capita bakery intake, supermarket private-label share, e-commerce share of packaged foods, sugar-reduction policies, and disposable income growth. A multivariate regression projects each driver to 2030, after which experts stress-test the baseline.

Data Validation & Update Cycle

Outputs pass two analyst reviews; variance triggers reopen datasets, and flagged anomalies are discussed with experts before sign-off. Reports refresh each year, with interim updates when recalls, tariffs, or policy shifts materially change the outlook.

Why Mordor's Food Spreads Baseline Numbers Stay Reliable

Published estimates often diverge because firms pick different product baskets, price bases, and refresh rhythms. Our disciplined scope plus yearly updates guard comparability even when retail mixes evolve.

Key gap drivers include some publishers folding savory dips into spreads, others tracking only jams, and several converting currencies at spot rates that distort longer trends. A few stretch linear growth without ingredient cost checks, which inflates distant forecasts.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 37.55 B (2025) | Mordor Intelligence | - |

| USD 80.68 B (2024) | Global Consultancy A | Includes dips and savory sauces, limited primary validation |

| USD 1.41 B (2024) | Regional Consultancy B | Counts jams only, narrow retail subset |

| USD 85 B (2021) | Trade Journal C | Older base year, spot FX, linear trend projection |

Taken together, the comparison shows how our clearly defined scope, variable-level modeling, and frequent refresh deliver a balanced, transparent baseline decision makers can trust.

Key Questions Answered in the Report

What is the current value of the food spreads market?

The food spreads market size is estimated at USD 37.55 billion in 2026 and is projected to grow at a CAGR of 4.78% to reach USD 47.42 billion by 2031.

How fast is the organic segment growing within food spreads?

Organic spreads are advancing at a 9.84% CAGR, outpacing conventional products due to stronger clean-label demand.

Why are sachets and pouches gaining popularity for spreads?

They offer portability, portion control and lighter environmental footprints, driving a 6.94% CAGR that challenges traditional jar dominance.

What competitive factors define success in the food spreads industry?

Innovation in reduced-sugar recipes, compelling origin stories and omnichannel presence are key, while private-label competition intensifies price pressure.

Page last updated on: