Market Overview

| Study Period | 2021 - 2031 |

|---|---|

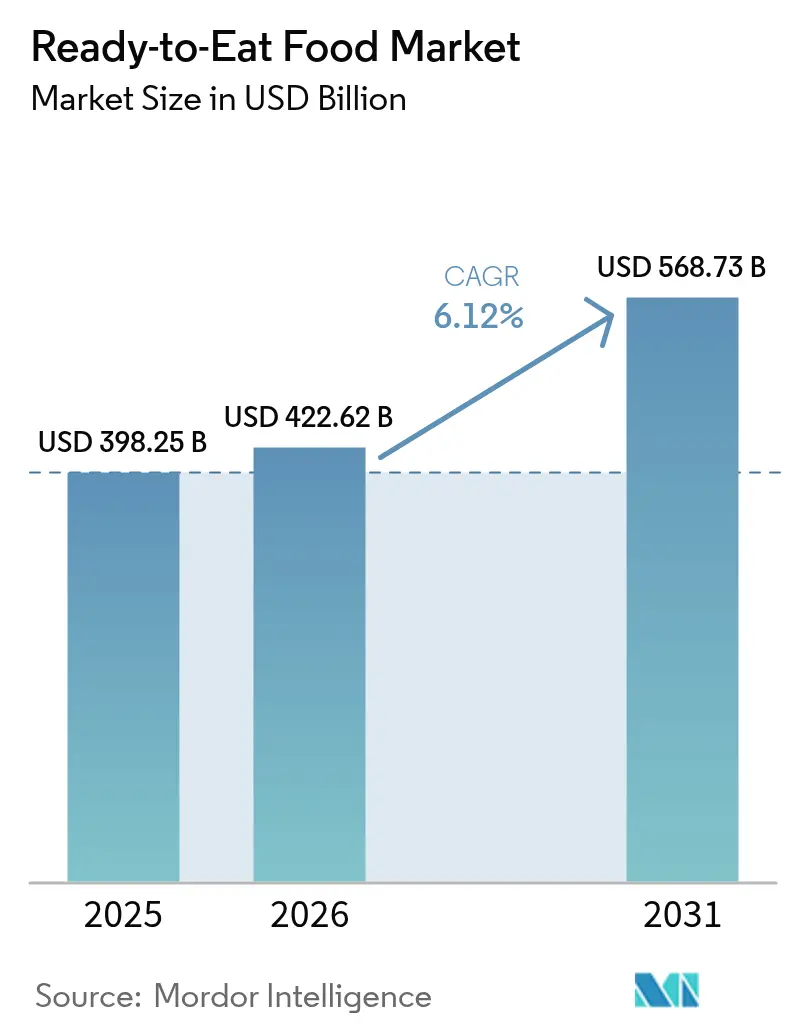

| Market Size (2026) | USD 422.62 Billion |

| Market Size (2031) | USD 568.73 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Ready-to-Eat Food Market Analysis by Mordor Intelligence

The ready-to-eat food market size was valued at USD 398.25 billion in 2025 and estimated to grow from USD 422.62 billion in 2026 to reach USD 568.73 billion by 2031, at a CAGR of 6.12% during the forecast period (2026-2031). This expansion reflects the sector's ability to align convenience with changing dietary trends. Urbanization, smaller household sizes, and the increase in dual-income families are fueling demand for shelf-stable or quickly heated meals, which significantly reduce preparation time. The Asia-Pacific region, with its strong manufacturing capabilities, ensures cost-efficient production. Simultaneously, advancements in packaging technology are improving shelf life without compromising flavor. However, stricter regulatory focus on ultra-processed foods is encouraging major brands to reformulate their products. These brands are also investing in quality systems, which inadvertently create higher entry barriers for smaller competitors. Although digital grocery platforms currently hold a smaller market share compared to traditional supermarkets, they are experiencing strong growth. This growth is driven by efficient fulfillment networks, AI-powered inventory management, and targeted promotions, making repeat purchases more convenient for consumers.

Key Report Takeaways

- By product type, baked goods held 34.15% of the ready-to-eat food market share in 2025, whereas instant soups and snacks are forecast to post the fastest 6.62% CAGR through 2031.

- By category, the conventional segment accounted for 75.32% share of the ready-to-eat food market size in 2025; organic and clean label alternatives are projected to expand at a 6.05% CAGR over the same period.

- By distribution channel, supermarkets and hypermarkets led with 45.62% revenue share in 2025, while online retail stores are set to grow at an 7.74% CAGR to 2031.

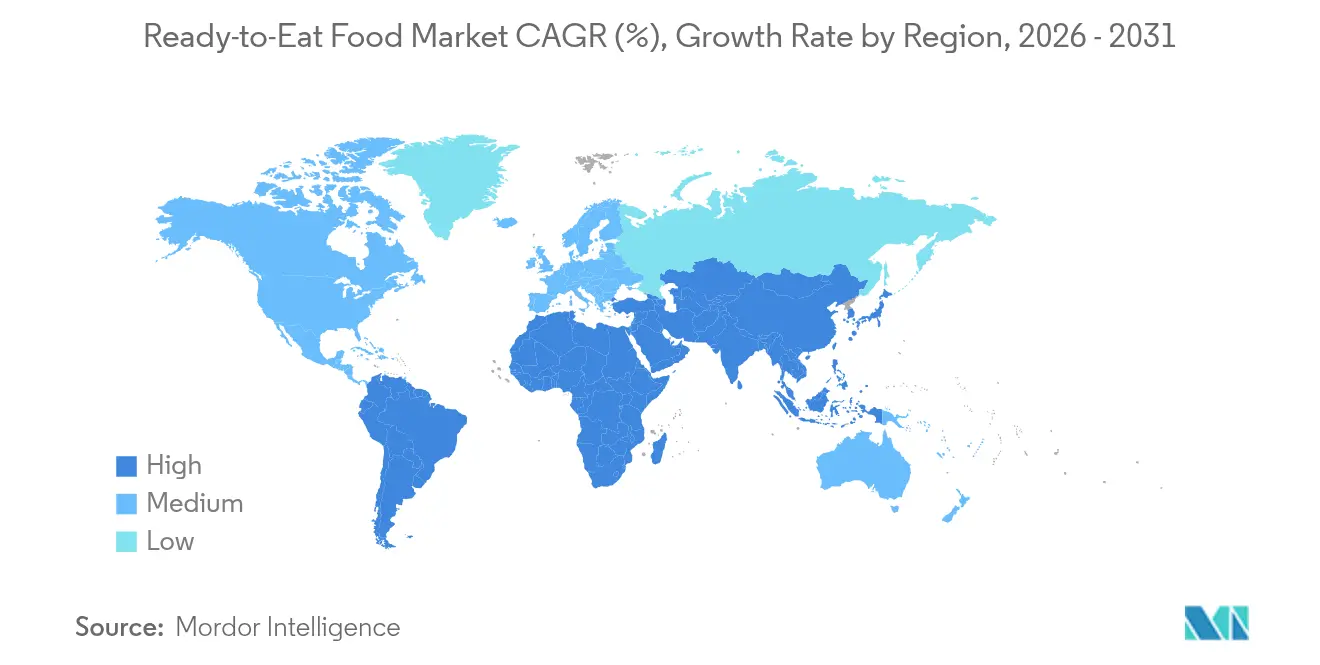

- By geography, Asia-Pacific dominated with a 41.20% share in 2025, and the Middle East and Africa region is advancing at a 6.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ready-to-Eat Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising number of single-person households and dual-income families | +1.2% | North America, Europe | Long term (≥ 4 years) |

| Rising penetration of e-grocery fulfillment | +0.8% | Asia-Pacific, North America | Medium term (2-4 years) |

| Changing consumer lifestyles | +0.7% | Urban Asia-Pacific, Middle East and Africa | Long term (≥ 4 years) |

| Growth in food processing industry | +0.6% | Manufacturing hubs in Asia-Pacific | Medium term (2-4 years) |

| Advancements in packaging technology | +0.4% | Global | Medium term (2-4 years) |

| Product innovation and flavor diversification | +0.5% | Developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising number of single-person households and dual-income families

As household sizes decrease, food consumption patterns are shifting, driving a steady demand for convenient, portion-controlled meal options. Single-person households increasingly prefer ready-to-eat meals and frozen instant foods that require minimal preparation. They often choose smaller portions or compact packaging designed for individual consumption, boosting the growth of the ready-to-eat (RTE) foods market. Families with working wives display distinct spending behaviors: higher-earning dual-income households tend to dine out, while moderate-income families favor convenience foods for home meals. In 2024, the Bureau of Labor Statistics reported that 49.6% of married couples in the U.S. had both spouses employed, a figure similar to the previous year. Additionally, 23.4% of these couples had only one spouse working[1]Source: Bureau of Labor Statistics, "Employment Characteristics of Families- 2024", bls.gov. USDA research highlights that affluent households with limited time are more likely to purchase convenience foods, balancing time savings with higher costs. This trend is especially evident in urban areas, where longer commutes and demanding careers exacerbate time constraints, leading to a permanent shift in food purchasing behaviors rather than temporary lifestyle changes.

Rising penetration of E-grocery and Q-commerce fulfilment

Innovations in cold-chain logistics and last-mile delivery are making ready-to-eat (RTE) foods more accessible than ever. Online platforms now showcase a diverse range of RTE products, from niche and premium selections to regional and international delicacies, many of which are absent from brick-and-mortar stores. This not only broadens consumer choices but also draws in a wider audience. E-grocery platforms frequently provide subscription or scheduled delivery for RTE meals, ensuring consistent consumer demand and added convenience. Quick commerce platforms are rooted in metropolitan areas, with giants like Walmart, Amazon, and Costco dominating the U.S. landscape. By integrating AI-driven demand forecasting with automated fulfillment centers, businesses are boosting inventory turnover for perishable RTE products, cutting down on waste, and enhancing availability. The surge in smartphone usage and internet access is propelling e-grocery growth in emerging markets, especially in countries like India, leading to a heightened demand for online RTE foods. In 2024, the International Telecommunication Union (ITU) reported that 5.5 billion people were using the internet[2]Source: International Telecommunication Union (ITU), "Internet Use", itu.int.

Growth in food processing industry

With the expansion of manufacturing and advancements in technology, production capacity increases while costs decrease, enabling broader market access for ready-to-eat products. AI is driving sustainable efficiency and quality assurance in food manufacturing. Machine learning systems effectively manage raw material variations, allowing for mass customization to meet personalized nutrition demands. Chef Robotics addresses labor shortages by deploying AI-powered robotic assembly systems, which utilize computer vision and robotics to deliver consistent output and reduce waste. Companies such as ADM and Cargill are advancing precision fermentation technologies to produce sustainable protein ingredients, addressing climate challenges and meeting the rising demand for protein. The Wholesale Price Index of processed ready-to-eat food across India was 146.3 in 2024, according to the Office of Economic Adviser (India)[3]Source: Office of Economic Adviser (India), "Annual Average of Monthly Index", eaindustry.nic.in. Rising WPI driven by demand-pull factors suggests growing consumer consumption and market expansion, encouraging processors to scale up RTE food production. The industry leverages automated systems for real-time adjustments, integrating sensor data, machine learning, and robotic actuators to improve product quality and reduce environmental impact. Additionally, investments in advanced packaging technologies, like JBT Marel's EA Retort sterilization, enhance product shelf life and safety while cutting production times and costs.

Advancements in packaging technology

Innovative packaging materials and processes enhance product shelf life, improve safety, and prioritize consumer convenience while addressing sustainability challenges. JBT Marel's Efficient Agitation Retort technology supports a variety of packaging types for ready-to-eat and ready-to-drink products. Its patented trapezoidal motion profiles enable efficient sterilization, and linear product agitation ensures consistent results. To tackle the 30-40% food waste occurring during distribution, Harvard researchers developed biodegradable food packaging systems. By utilizing Rotary Jet Spinning techniques and pullulan polymers, these systems extend the shelf life of fresh food and reduce microbial contamination risks. Sealed Air's Cryovac Simple Steps meal packaging provides vacuum-sealed, microwaveable solutions. Featuring steam-assisted technology for even heating and hermetically sealed designs, these packages are leak-proof and freezer-ready. Edible coatings are gaining traction as a sustainable packaging innovation. Biodegradable coatings are now incorporated into packaging systems to minimize waste and extend the shelf life of ready-to-eat seafood and meat products. The focus remains on ensuring food product compatibility, meeting regulatory requirements, and optimizing costs to achieve consumer acceptance and commercial feasibility.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing ultra-processed-food regulation momentum | -0.9% | North America, Europe | Medium term (2-4 years) |

| Health and nutritional transparency issues | -0.6% | Global | Long term (≥ 4 years) |

| Consumer skepticism about additives and preservatives | -0.4% | Developed markets | Medium term (2-4 years) |

| Stringent food safety and regulatory compliance | -0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing ultra-processed-food regulation momentum

Health authorities worldwide are tightening regulations on ultra-processed foods, citing links to chronic diseases. In a bid to boost consumer transparency and combat diet-related health issues, the FDA, USDA, and HHS are working together to define ultra-processed foods more clearly. Starting January 1, 2027, Texas will require warning labels on products with 44 specific additives. Meanwhile, Louisiana has taken a step further, banning 15 ingredients in school meals and requiring QR codes on certain additive-containing products, with the rules kicking in on January 1, 2028. The President's Make America Healthy Again Commission is zeroing in on childhood health, echoing concerns from studies that consistently tie ultra-processed foods to obesity, heart disease, and diabetes. While major brands with research and developments capabilities can easily adjust their formulations, smaller companies might find themselves forced to abandon categories due to the high compliance costs.

Health and nutritional transparency issues

As consumer demand for ingredient transparency and nutritional clarity increases, companies are encountering compliance challenges and higher reformulation costs. Consumers are placing greater emphasis on ingredient transparency, particularly regarding protein content, while brain health is becoming a significant focus in new product launches. To enhance consumer awareness, the FDA has proposed front-of-package warning labels for ultra-processed foods, which would identify high levels of fat, sugar, and sodium. This initiative is inspired by successful implementations in Mexico and Chile, where similar measures improved consumer awareness and influenced purchasing decisions. Reports from the Consumer Federation of America emphasize the need for public policy reforms to reduce ultra-processed food consumption. These reforms call for improved food labeling, educational initiatives, and regulatory measures to ensure food safety. The challenge is especially significant for ready-to-eat products, which must balance convenience with health perceptions. Addressing this requires substantial investments in reformulation and marketing to alleviate consumer skepticism. To meet transparency standards, companies are incurring increased costs for ingredient sourcing, testing, and documentation, while ensuring their products remain appealing and shelf-stable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Baked Goods Lead Convenience Revolution

Baked goods contributed 34.15% of the ready-to-eat food market share in 2025, buoyed by long ambient shelf life and the universal appeal of breads, buns and pastries. Investments in modified-atmosphere packaging sustain freshness across transcontinental shipping lanes, allowing Asian bakery giants to secure shelf idle times below eight days in U.S. specialty stores. The ready-to-eat food market size for baked goods is projected to climb steadily as sourdough, focaccia chips and protein-enriched banana breads penetrate breakfast and snack occasions.

Instant soups and snacks, forecast to record a 6.62% CAGR through 2031, satisfy rising office lunch demand where microwave access is limited. Innovations highlight freeze-dried barley, air-fried croutons, and collagen-infused broth bases, focusing on joint-health benefits. Ready meals continue to attract consumers by offering a rotating variety of global cuisines, such as Korean bibimbap, Nigerian jollof, and Peruvian lomo saltado, in portion-controlled bowls. Meat-centric SKUs utilize sous-vide cooking methods and recyclable, plastic-free trays to minimize resource usage. The combination of tradition, premium flavors, and functional ingredients sustains high category turnover, encouraging ongoing recipe development.

By Category: Clean Label Gains Momentum

Conventional recipes held 75.32% share of the ready-to-eat food market in 2025 as price-sensitive consumers favored familiar ingredients and multi-buy discounts. At the same time, the organic/clean-label segment is experiencing strong growth, with a 6.05% CAGR, supported by transparent sourcing and the removal of artificial dyes. Retailers are boosting the visibility of these products by creating dedicated natural aisles and using pastel color coding to indicate their “free-from” status.

Brands promoting regenerative farming practices are gaining advantages, such as premium end-caps and prominent online filters. However, they face challenges like higher input costs and shorter raw-material availability windows. The growth of clean-label SKUs in the ready-to-eat food market relies on increasing the supply of natural colors and heat-stable botanicals, a task made easier by cooperatives that unite smaller organic farms. Conventional players are mitigating risks by offering dual versions - original and simplified ingredient lists - while actively testing price elasticity.

By Distribution Channel: Digital Transformation Accelerates

In 2025, supermarkets and hypermarkets accounted for 45.62% of sales, leveraging perimeter chillers and in-store bakeries to promote grab-and-go meals. These supermarkets provide a diverse array of ready-to-eat (RTE) products, from meat-based and cereal-based to vegetarian options, all at competitive prices. However, online retail stores are on track to grow at a robust 7.74% CAGR. This growth is fueled by mobile apps enhancing substitution logic and optimizing time-slot accuracy. E-commerce is witnessing the swiftest rise in the ready-to-eat food market, with ride-sharing fleets doubling as food couriers, effectively reducing last-mile delivery costs.

Convenience stores are now equipped with smart fridges that not only stock heat-in-package bowls but also send receipts directly to loyalty apps via text. Quick-commerce platforms are expanding their offerings, now delivering frozen dumplings and drinkable soups within two hours, even bundling these with pharmacy items to boost average order values. In the Gulf region, government-backed investments in cloud kitchens are broadening online product assortments. Meanwhile, grocers in South America are leveraging WhatsApp for order capture and offering cash-on-delivery to cater to their unbanked clientele.

Geography Analysis

In 2025, the Asia-Pacific region leads with a 41.20% market share, driven by rapid urbanization, increasing disposable incomes, and a shift toward smaller households that prefer convenient meal options. The region's well-established manufacturing infrastructure and supply chain networks support cost-efficient production and distribution. In China, consumers are showing a growing preference for healthier choices, as reflected in higher spending on fresh produce. This trend coincides with a decline in discretionary food delivery spending, presenting refined market segmentation opportunities. India demonstrates strong spending patterns across both essential and discretionary categories, indicating a stable economic environment and rising middle-class consumption. In Japan and South Korea, omnichannel shopping is gaining traction, with consumers increasingly opting for online platforms due to their convenience and product variety. The food processing industry in the region is expanding, supported by AI and automation technologies that enhance production efficiency and reduce costs, enabling greater market penetration for ready-to-eat products.

The Middle East and Africa are experiencing the fastest growth, with a 6.95% CAGR projected through 2031. This growth is driven by demographic changes and urbanization, which sustain demand for convenient food solutions. Middle Eastern consumers purchase prepared foods and order takeaways at rates significantly higher than global averages, while also expressing concerns about the health implications of ultra-processed foods. In Africa, urbanization and a growing population are fueling demand for prepared cereals, creating substantial market opportunities. Additionally, the MENA grocery sector is rebounding strongly in modern trade, supported by rising disposable incomes and shifting dietary preferences.

North America, South America, and Europe are mature markets characterized by established consumption patterns and regulatory frameworks that influence product innovation and marketing strategies. These regions are facing increased regulatory scrutiny regarding ultra-processed foods. They benefit from advanced cold-chain logistics and sophisticated retail infrastructure, which enable premium product positioning and efficient distribution. Innovation efforts focus on health-oriented formulations, sustainable packaging, and flavor diversification to meet evolving consumer preferences while adhering to strict regulatory standards.

Competitive Landscape

The ready-to-eat food market is experiencing moderate consolidation, fueled by intense competition, strategic acquisitions, and advancements in technology. In August 2024, Mars, Incorporated acquired Kellanova, a leading company in global snacking. This acquisition strengthens global distribution networks and enhances product innovation capabilities. Such moves demonstrate how major players utilize financial resources to acquire complementary brands and distribution channels, creating obstacles for smaller competitors while expanding their market presence. To address labor shortages and improve efficiency, industry leaders are increasingly investing in AI-driven manufacturing systems and automated production lines.

Prominent companies in the ready-to-eat food sector, including Nestlé SA, Tyson Foods Inc., Conagra Brands, Mars Inc., and Kraft Heinz Company, are driving the industry forward through continuous innovation and strategic initiatives. These companies are making significant investments in research and development to introduce products that align with evolving consumer preferences. Key areas of focus include healthier options, plant-based alternatives, and ethnic flavors. Manufacturers are also prioritizing operational agility by expanding production capabilities and optimizing supply chains for efficient distribution.

Opportunities are emerging in clean label formulations, functional ingredients, and regional flavors that cater to specific demographic groups. New market entrants are concentrating on plant-based alternatives, precision fermentation technologies, and direct-to-consumer models that bypass traditional retail channels. The adoption of advanced technologies is accelerating through collaborations with robotics companies like Chef Robotics, which implement AI-driven assembly systems to improve production efficiency and reduce waste. Companies with strong quality management systems gain a competitive edge in meeting regulatory requirements, such as the FDA's Food Safety Modernization Act and HACCP systems. However, smaller players face increasing compliance costs, which may hinder their ability to enter or expand within the market.

Ready-to-Eat Food Industry Leaders

-

Conagra Brands, Inc.

-

Nestlé S.A.

-

General Mills, Inc.

-

Tyson Foods Inc.

-

Mars Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Tyson Foods launched Tyson Simple Ingredient Nuggets, a new product line focused on simplifying ingredients and meeting consumer demand for healthier options

- June 2025: Red Planet has unveiled ready-to-eat meals boasting a remarkable 25-year shelf life, harnessing freeze-drying technology to ensure taste and nutritional integrity, catering to essential sectors.

- February 2025: Bonduelle has unveiled its latest offering: Ready-to-Eat Lunch Bowls. These "Lunch Bowls" boast 100% plant-based ingredients and pack over 10 grams of protein.

- August 2024: Mars Incorporated acquired Kellanova for USD 35.9 billion, enhancing its position in the ready-to-eat food market with brands like Pringles, Cheez-It, and RXBAR, aiming to double Mars's snacking business in the next decade.

Global Ready-to-Eat Food Market Report Scope

Ready-to-eat foods are foods made for direct consumption and do not require much further processing. They are mostly consumed without prior preparation or cooking. The ready-to-eat food market is segmented by product type, distribution channel, and geography. Based on product type, the market is segmented into instant breakfast/cereals, instant soups and snacks, ready meals, baked goods, meat products, and other product types. Based on the distribution channel, the market is segmented into hypermarkets/supermarkets, convenience stores, online retail stores, and other distribution channels. Moreover, the study analyzes the ready-to-eat food market across geography, including North America, Europe, Asia-Pacific, South America, the Middle East, and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

By Product Type

| Instant Breakfast / Cereals |

| Instant Soups and Snacks |

| Ready Meals |

| Baked Goods |

| Meat Products |

| Other Product Types |

By Category

| Conventional |

| Organic/Clean Label |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Retail Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Instant Breakfast / Cereals | |

| Instant Soups and Snacks | ||

| Ready Meals | ||

| Baked Goods | ||

| Meat Products | ||

| Other Product Types | ||

| By Category | Conventional | |

| Organic/Clean Label | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Retail Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the ready-to-eat food market?

It was valued at USD 422.62 billion in 2026 and is projected to reach USD 568.73 billion by 2031.

Which region leads sales of ready-to-eat products?

Asia-Pacific captured 41.20% of 2025 global revenue, driven by rapid urbanization and manufacturing scale.

Which product segment grows fastest through 2031?

Instant soups and snacks are forecast to grow at a 6.62% CAGR, the quickest among major product types.

How quickly is online grocery impacting sales?

Online retail stores are set to grow at an 7.74% CAGR to 2031, outpacing other distribution channels.

Page last updated on: