Food And Beverage Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 9.79 Trillion |

| Market Size (2031) | USD 11.78 Trillion |

| Growth Rate (2026 - 2031) | 3.75% CAGR |

| Fastest Growing Market | Middle East and Africa |

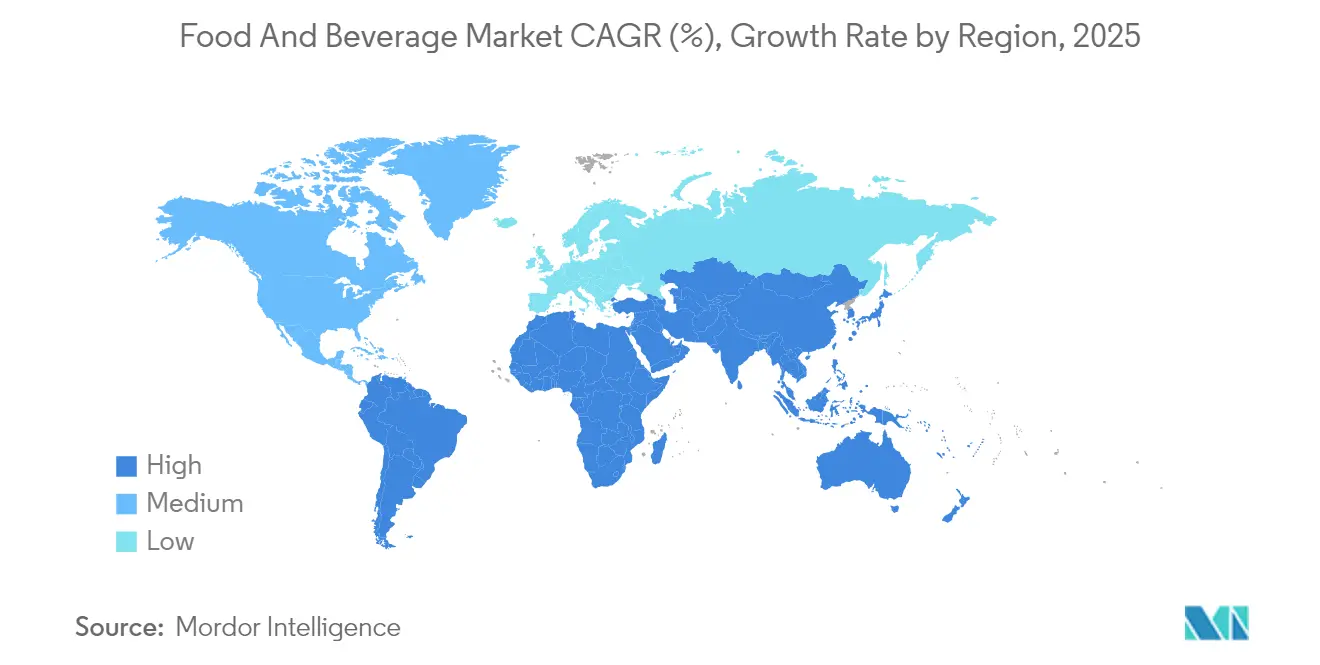

| Largest Market | Asia Pacific |

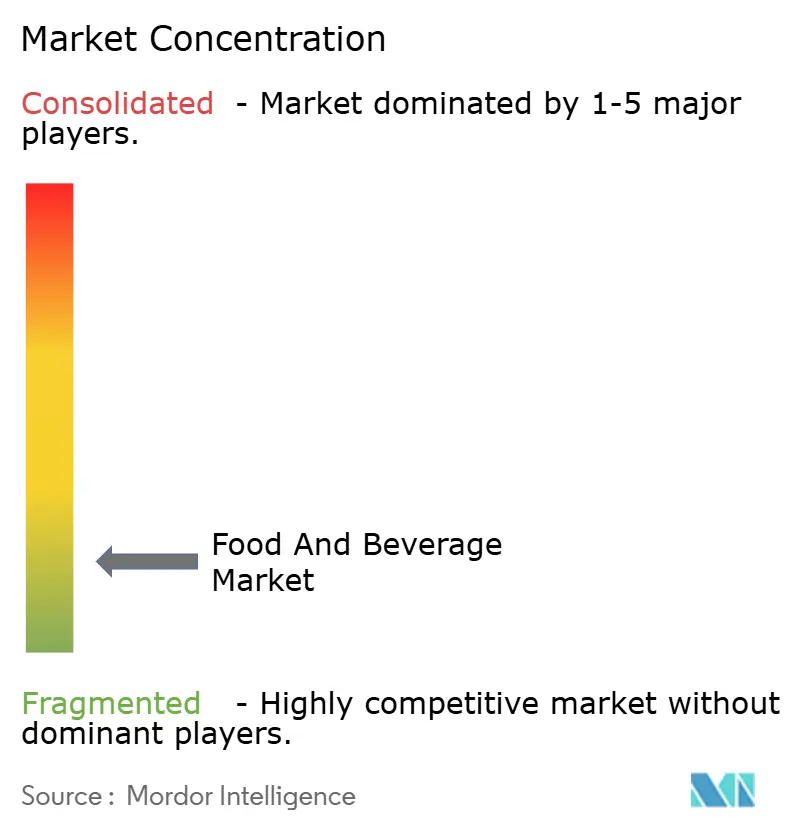

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Food And Beverage Market Analysis by Mordor Intelligence

food and beverage market size in 2026 is estimated at USD 9.79 trillion, growing from 2025 value of USD 9.44 trillion with 2031 projections showing USD 11.78 trillion, growing at 3.75% CAGR over 2026-2031. The sector is expanding even as consumer tastes shift toward wellness, digital convenience, and sustainability. The market for functional foods and beverages is expanding as consumers demand products with enhanced nutritional and performance benefits. Growth reflects robust demand for faster adoption of e-commerce, and ongoing packaging upgrades that align with circular-economy rules. Pricing pressures remain, yet manufacturers are offsetting higher costs through automation, supply-chain partnerships, and premium positioning in organic portfolios. Intensifying regulatory oversight is raising compliance investments, but companies that modernize traceability and safety systems are securing long-term competitive advantages. Overall, the food and beverage market continues to demonstrate resilience through data-driven innovation and careful portfolio balancing.

Key Report Takeaways

- By product category, food captured 63.85% of the food and beverage market share in 2025; beverages are projected to grow at a 4.42% CAGR to 2031.

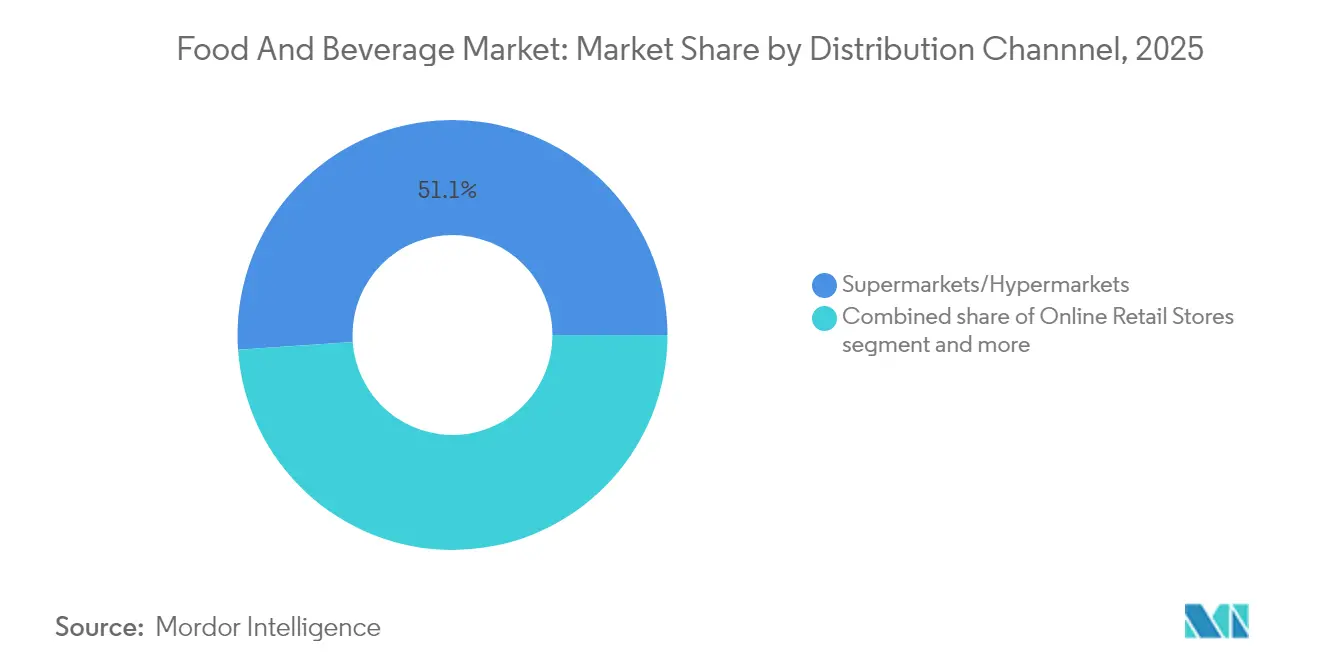

- By distribution channel, supermarkets/hypermarkets held 51.10% share of the food and beverage market in 2025, while online retail is advancing at a 5.63% CAGR through 2031.

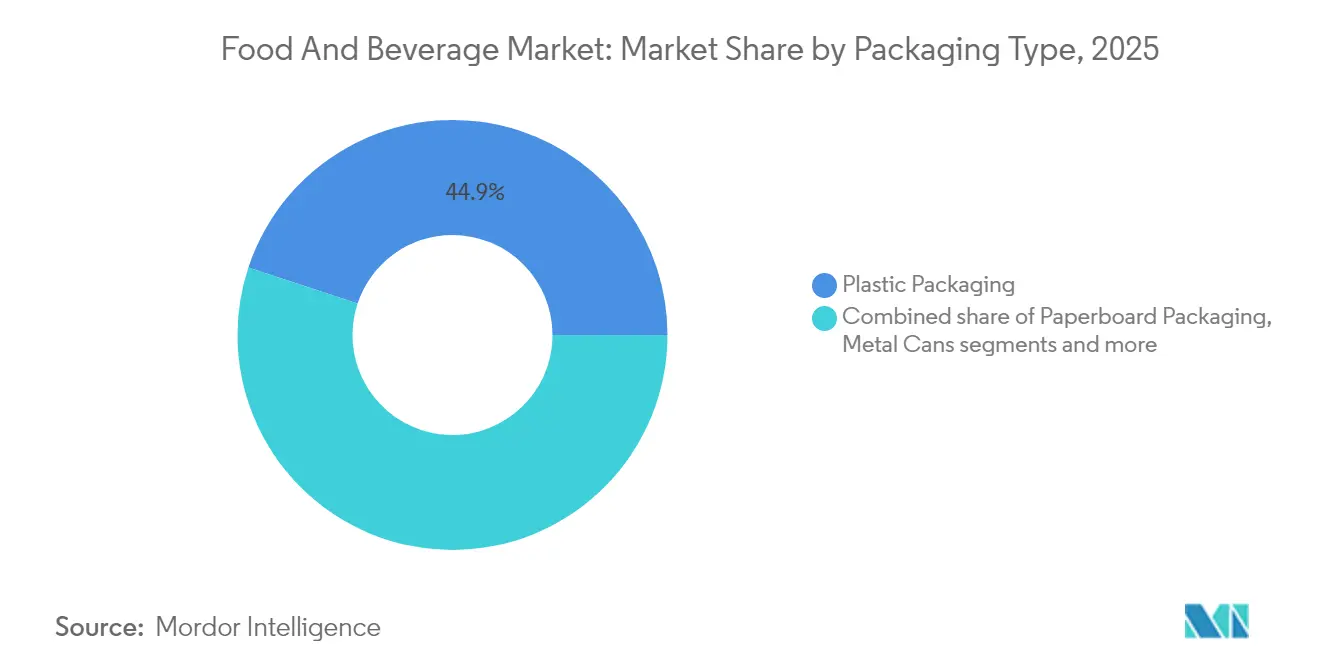

- By packaging type, plastic packaging accounted for 44.92% share of the food and beverage market in 2025; paperboard solutions are growing at a 5.12% CAGR to 2031.

- By nature, conventional products commanded 70.55% share of the food and beverage market in 2025, whereas the organic segment is expanding at a 5.41% CAGR through 2031.

- By geography, Asia-Pacific led with 40.88% share of the food and beverage market in 2025; the Middle East and Africa region is forecast to post the fastest 5.24% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Food And Beverage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing focus on health and wellness | +0.8% | Global, with premium growth in North America and European Union | Medium term (2-4 years) |

| Rising convenience and on-the-go consumption | +0.6% | Core Asia-Pacific, spill-over to Middle East and Africa | Short term (≤ 2 years) |

| Rising digitalization and e-commerce expansion | +0.7% | Global, accelerated in emerging markets | Short term (≤ 2 years) |

| Surge in food safety and quality technologies | +0.4% | North America and European Union, expanding to Asia-Pacific | Medium term (2-4 years) |

| Product innovation and customization | +0.5% | Global, led by developed markets | Long term (≥ 4 years) |

| Sustainability and eco-friendly packaging | +0.3% | European Union leading, global adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Focus on Health and Wellness

Consumer emphasis on health is transforming the global packaged food and beverage market, with purchasing decisions increasingly influenced by nutritional value, ingredient transparency, and functional benefits. As per bioMérieux, in 2024, 75% of consumers demonstrate a willingness to pay premium prices for products without synthetic additives, establishing significant market opportunities for clean-label and minimally processed foods [1]Source: bioMérieux SA, "What’s next in food safety? Key trends for 2025 and beyond", biomerieux.com. Functional foods, which deliver specific health advantages including immune support, digestive health, and increased energy, constitute the market's fastest-growing segment. Advanced nutrition technologies enable manufacturers to develop products aligned with specific dietary requirements. Generation Z drives this market evolution, supporting companies that incorporate plant-based ingredients and demonstrate transparent sourcing and nutritional information. The market demonstrates product innovation through prebiotic and probiotic-enhanced snacks, protein beverages, and specialized hydration products. Food and beverage companies implement faster product development cycles and increase investment in health-focused product portfolios. This strategic focus on health benefits addresses current consumer requirements while supporting market growth.

Rising Convenience and On-the-Go Consumption

The global packaged food and beverage market demonstrates significant changes due to consumer requirements for products compatible with mobile lifestyles. The market indicates increased demand for single-serve, ready-to-eat, and shelf-stable products that deliver both convenience and nutritional value. New packaging formats, including resealable pouches and compact snack packs, facilitate portion control while enabling premium pricing and minimizing food waste. The Asia-Pacific region, specifically in urban markets, exhibits substantial growth as increased disposable incomes and time constraints drive consumer preferences toward convenient, high-quality food options. Manufacturers are enhancing distribution infrastructure through investments in cold-chain logistics, refrigerated transport, and delivery network optimization. The integration of digital inventory management systems enables retailers to maintain stock levels and meet consumer demand. Product development emphasizes convenient options, including nutrient-dense snacks, fortified beverages, and meal kits. These market developments capture key consumer segments, including working professionals and urban millennials, while establishing new standards for product quality and accessibility in the packaged food and beverage industry.

Rising Digitalization and E-Commerce Expansion

Companies in the packaged food and beverage industry are implementing digital transformation through technology adoption in consumer engagement and operations. Companies use machine learning and AI analytics to forecast demand, provide product recommendations, and manage inventory, which helps reduce waste and increase revenue. Blockchain technology implementation improves supply chain transparency, meeting regulatory requirements and consumer demands for product traceability. Online-first brands are gaining market share by using digital marketing and social media to emphasize their sustainability initiatives and build consumer relationships. Traditional companies are developing omnichannel approaches, combining online sales platforms with physical retail locations to serve customers across all shopping channels. Moreover, partnerships with social media influencers help companies reach younger consumers who value convenience, ethical production, and product information accessibility. This digital integration improves supply chain efficiency and marketing capabilities while enabling companies to adapt to changing consumer preferences in the global market.

Surge in Food Safety and Quality Assurance Technologies

Food and beverage manufacturers are increasing investments in food safety and quality assurance technologies. The FDA's Food Traceability Rule, which becomes effective in January 2026, requires companies to implement enhanced tracking systems. This implementation requires 6-14 months of preparation time and substantial investments in technology [2]Source: U.S. Food and Drug Administration, "FSMA Final Rule on Requirements for Additional Traceability Records for Certain Foods", fda.gov. Companies are implementing IoT sensor networks to monitor temperature, humidity, and contamination across the supply chain, maintaining product quality from production to retail. Quality control laboratories now utilize whole-genome sequencing to identify pathogens more efficiently, enabling quick responses to safety concerns. These technological implementations reduce product recall risks and costs while building consumer confidence through improved safety measures and transparency. Companies that implement comprehensive digital traceability and monitoring systems are establishing new standards in the global packaged food and beverage market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent and evolving regulatory compliance | -0.5% | Global, most severe in European Union and North America | Medium term (2-4 years) |

| Rising raw material and input costs | -0.7% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Increased competition and market saturation | -0.3% | Developed markets, spreading globally | Long term (≥ 4 years) |

| Chronic labour shortages in food and beverage manufacturing | -0.4% | North America and European Union, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent and Evolving Regulatory Compliance

Regulatory requirements have become increasingly stringent for food and beverage manufacturers, creating operational challenges and higher costs. Compliance expenditure has increased by over 1,400% since 2006 across major agricultural and food production regions, requiring companies to update their processes and invest in quality assurance systems. The FDA's recent bans on ingredients like brominated vegetable oil and Red Dye No. 3, along with new labeling requirements, have compelled manufacturers to modify product formulations [3]Source: U.S. Food and Drug Administration, "FDA to Revoke Authorization for the Use of Red No. 3 in Food and Ingested Drugs", fda.gov. Additionally, regulations such as California's extended producer responsibility laws have introduced new fees and reporting requirements, increasing costs throughout the supply chain. While large multinational companies can manage these challenges through economies of scale and specialized regulatory teams, small and medium-sized enterprises (SMEs) face greater difficulties due to higher per-unit costs and limited resources. The increasingly strict global food safety and environmental standards continue to pose challenges for market participants, particularly affecting innovation and market access for smaller companies.

Chronic Labour Shortages in Food and Beverage Manufacturing

Manufacturing operations in the packaged food and beverage industry face significant workforce challenges as chronic labor shortages disrupt production schedules and limit growth potential. Companies experience difficulties in filling essential positions across processing, packaging, logistics, and quality control departments due to retiring experienced workers and declining interest from younger generations in manufacturing careers. These staffing challenges result in increased wage pressures, higher overtime expenses, decreased operational efficiency, and increased production bottlenecks. In addition, manufacturers are responding by investing in automation, robotics, and digital workforce management systems. However, implementing automated operations requires substantial initial investment and employee retraining, creating particular difficulties for small and medium-sized enterprises. The ongoing labor shortages also affect companies' capabilities in product innovation and rapid response to changing consumer preferences. Besides, companies that develop effective strategies for workforce recruitment, retention, and skill development will maintain a competitive advantage and strengthen their supply chain resilience in the packaged food and beverage industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Distribution Channel: Digital Transformation Reshapes Retail

Supermarkets/hypermarkets dominated the global food and beverage market in 2025, capturing 51.10% of the total market share. These retailers maintain their market dominance through wide product selections, competitive prices, and convenient one-stop shopping experiences. Their extensive retail footprint and efficient supply chain networks enable regular inventory replenishment and consistent product availability, which helps retain customer loyalty.

The online retail channel is growing at a 5.63% CAGR, driven by changing consumer preferences, particularly in suburban and rural areas with limited access to physical stores. E-commerce platforms are expanding their market reach by offering diverse product selections, personalized recommendations, and home delivery services. Retailers are improving their fulfillment capabilities through investments in dark stores and automated picking systems to reduce delivery times and enhance order accuracy. Moreover, the retail landscape is transforming as traditional stores integrate digital capabilities, including click-and-collect services and real-time inventory management. This evolution has intensified competition between physical and online retailers as they focus on improving convenience, value, and product variety. The ongoing integration of technology and logistics improvements continues to reshape consumer purchasing patterns, emphasizing the need for adaptable and customer-focused strategies in the sector.

By Product Category: Food Dominance Drives Market Scale

The food products segment captured 63.85% of the total food and beverage market share in 2025, reflecting the consistent demand for staples and diverse food sub-categories. This significant share stems from the fundamental necessity of food items and ongoing product development across bakery, confectionery, snacks, ready meals, and plant-based products. Bakery and confectionery manufacturers are modifying their formulations to meet sugar-reduction requirements and health standards, while ready meals continue to expand due to urban consumers' preference for convenient meal solutions. Meanwhile, beverage segment growth is projected at a CAGR of 4.42%, exceeding the food segment's expansion rate. Market demand continues to increase for premium hydration products, functional beverages with health benefits, and dairy alternatives. Collaborations between dairy companies and precision-fermentation startups, including Fonterra's partnerships, are creating new product opportunities in the alternative protein market.

Moreover, the snack segment is adapting by introducing fiber-rich and nutrient-dense products to meet consumer health preferences. The market for plant-based protein blends and meat hybrids is expanding due to growing interest from flexitarian consumers and sustainability-focused shoppers. These market changes are influencing product development and supporting growth across categories, as companies focus on health, sustainability, and convenience to increase their market presence in retail and online channels. The food and beverage market is expanding through innovation, lifestyle changes, and increased focus on wellness and environmental responsibility.

By Packaging Type: Innovation Drives Differentiation

Plastic packaging accounts for 44.92% of food and beverage packaging in 2025, driven by its versatility, durability, and lightweight characteristics. Regulatory pressures and consumer preferences for sustainable options are driving the transition to environmentally friendly alternatives. The paperboard packaging segment is growing at a CAGR of 5.12%, as companies adapt to single-use plastic regulations and increased demand for recyclable materials.

The sustainable packaging market is expanding as companies pursue net-zero commitments, driving investments in environmentally friendly materials and technologies. Companies are developing innovative packaging solutions, including cellulose-based films and water-soluble coatings that provide barrier protection while meeting recyclability and compostability requirements. Besides, metal cans remain preferred for premium beers and energy drinks due to their shelf stability and recyclability, while glass packaging serves specific segments like gourmet sauces and specialty beverages. Smart packaging technologies, including freshness sensors and QR codes, provide real-time product information, build consumer trust, and facilitate loyalty programs. These packaging innovations address regulatory and environmental requirements while enabling brands to differentiate themselves in the food and beverage market.

By Nature: Organic Premium Positioning Accelerates

The conventional product segment held 70.55% market share in 2025, maintaining its position through lower prices, widespread availability, and established consumer preferences. The organic/natural segment grew at a CAGR of 5.41%, driven by increasing consumer demand for traceable ingredients, clean labels, and transparent sourcing practices. These factors contributed to higher per-basket spending and increased brand loyalty, particularly among consumers focused on health and environmental considerations.

Furthermore, consumer demand for organic products is driving producers to implement dual-portfolio strategies that balance conventional product lines' scale and cost advantages with organic ranges' premium positioning. However, the limited supply of certified organic ingredients and complex third-party certification requirements create market entry barriers, benefiting companies with established grower relationships and reliable supply chains. The growing trend of clean-label reformulations is reducing the distinction between conventional and organic products, as traditional brands introduce products with fewer additives and more natural ingredients to reach a wider consumer base. This market evolution requires manufacturers to innovate across both conventional and organic portfolios to serve price-conscious consumers while targeting premium market segments. With organic/natural products growing faster than conventional alternatives, supply chain transparency and verified certifications remain important competitive advantages in the food and beverage market.

Geography Analysis

The food and beverage market in Asia-Pacific constituted 40.88% of the global market value in 2025, making it the largest regional market. The region's growth stems from increasing urbanization and higher disposable incomes, which drive demand for packaged and premium products. Digital retail infrastructure, including mobile payment systems and e-commerce platforms, has improved delivery services and payment options, particularly among younger consumers. The beverage segment shows strong performance in functional hydration products and new drink varieties, supported by health-conscious urban consumers and expanding brand options from both international and domestic companies. While modern retail and digital channels expand, traditional markets and convenience stores remain important sales channels, emphasizing the importance of diverse distribution networks. The region's combination of established retail practices and emerging trends requires companies to develop products that align with local preferences while adapting to various retail formats.

North America commands a sizeable slice of the food and beverage market, driven by innovation in plant-based meats and functional snacks. Labour shortages intensify automation funding, while complex label mandates raise reformulation costs. Besides, Europe shows strong adoption of organic assortments and eco-friendly packaging, aided by consumer willingness to pay green premiums and by stringent policy frameworks such as the Single-Use Plastic Directive.

The Middle East and Africa region is forecast to advance at a 5.24% CAGR, propelled by youthful demographics and rising food-import dependence. Also, infrastructure upgrades and cold-chain investments are critical to curb spoilage in hot climates. Moreover, South America leverages export-oriented farm output yet faces currency swings and logistical gaps that hinder domestic processing scale. Across all geographies, the food and beverage market continues to blend local tastes with global health and sustainability themes.

Mordor Intelligence provides coverage of the food and beverage market across other key regional markets. Detailed country-level analysis extends to Saudi Arabia incorporating local coverage and market participation, as required.

Competitive Landscape

The food and beverage industry remains highly fragmented, and no single player commands more than a single-digit global share. Leading manufacturers pursue vertical integration and large-scale mergers and acquisitions to secure inputs and broaden portfolios. For instance, in August 2024, Mars agreed to acquire Kellanova for USD 36 billion, a move aimed at synergies in confectionery and snacks. Similarly, in March 2025, PepsiCo entered functional soda with the USD 1.95 billion Poppi purchase, diversifying away from traditional colas.

Key players like Nestlé, PepsiCo, and The Coca-Cola Company are competing to meet consumer demand for healthier, sustainable, and convenient products. Companies are focusing on innovation through plant-based alternatives, personalized nutrition solutions, and food safety technologies. Additionally, sustainability and ethical sourcing practices have become essential factors as companies aim to attract environmentally conscious consumers while meeting stricter global regulations.

Digital tools are core to productivity gains. In 2024, Danone partnered with Microsoft to embed AI in demand planning, production scheduling, and energy optimization. Smaller disruptors use direct-to-consumer channels for rapid feedback loops and brand storytelling. Incumbents counter by backing accelerator programs and minority stakes in start-ups to secure innovation pipelines. Sustainability remains a unifying agenda, with packaging pilots and regenerative agriculture commitments differentiating brands within the competitive arena.

Food And Beverage Industry Leaders

-

Nestlé S.A.

-

The Coca-Cola Company

-

PepsiCo Inc.

-

Anheuser-Busch InBev SA/NV

-

JBS S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Chupa Chups expanded its jelly range with the launch of Pinkis in the United Kingdom. The new product featured a soft texture and pink color, and became available in stores from July 2024. This addition aimed to meet consumer demand for innovative confectionery products.

- July 2025: PepsiCo introduced a new product line, 'That's Nuts,' which integrated its crisp flavors with coated peanuts to establish a presence in the nut snack market. The product portfolio incorporated flavors from established brands, including Walkers, Doritos, and Wotsits, offering Salt & Vinegar, Smoky Bacon, Chilli Heatwave, and Flamin' Hot varieties.

- June 2025: Heineken inaugurated the Dr. H.P. Heineken Centre, a research and development facility in Zoeterwoude, Netherlands. The EUR 45 million investment in the 8,800 m² facility strengthened Heineken's capabilities in brewing and brewing technology. The research and development hub focused on advancing brewing techniques, developing new products, and addressing consumer preferences, particularly in flavor and sustainability.

- June 2025: Danone North America invested USD 65 million in a new production line at its Jacksonville, Florida, manufacturing facility. The 115,025-square-foot facility expansion enhanced production capacity for Danone's coffee and creamer portfolio, which included International Delight creamers and STōK Cold Brew Coffee.

Global Food And Beverage Market Report Scope

| Food | Dairy and Dairy Alternative Products | |

| Bakery | ||

| Confectionery | ||

| Meat, Poultry, Seafood, and Meat Substitute | ||

| Snacks | ||

| Breakfast Cereals | ||

| Ready Meals | ||

| Sauces and Spreads | ||

| Others (Baby Food, and others) | ||

| Beverage | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Others | ||

| Non-Alcoholic | Energy Drinks | |

| Sports Drinks | ||

| Juices | ||

| Bottled Water | ||

| RTD Tea and Coffee | ||

| Others | ||

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Speciality Stores |

| Other Distribution Channel |

| Plastic Packaging |

| Paperboard Packaging |

| Metal Cans |

| Glass Packaging |

| Others (Tetra Pak/Cartons, Pouches, etc) |

| Conventional |

| Organic/Natural |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Category | Food | Dairy and Dairy Alternative Products | |

| Bakery | |||

| Confectionery | |||

| Meat, Poultry, Seafood, and Meat Substitute | |||

| Snacks | |||

| Breakfast Cereals | |||

| Ready Meals | |||

| Sauces and Spreads | |||

| Others (Baby Food, and others) | |||

| Beverage | Alcoholic | Beer | |

| Wine | |||

| Spirits | |||

| Others | |||

| Non-Alcoholic | Energy Drinks | ||

| Sports Drinks | |||

| Juices | |||

| Bottled Water | |||

| RTD Tea and Coffee | |||

| Others | |||

| By Distribution Channel | Supermarkets/Hypermarkets | ||

| Convenience/Grocery Stores | |||

| Online Retail Stores | |||

| Speciality Stores | |||

| Other Distribution Channel | |||

| By Packaging Type | Plastic Packaging | ||

| Paperboard Packaging | |||

| Metal Cans | |||

| Glass Packaging | |||

| Others (Tetra Pak/Cartons, Pouches, etc) | |||

| By Nature | Conventional | ||

| Organic/Natural | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| Italy | |||

| France | |||

| Spain | |||

| Netherlands | |||

| Poland | |||

| Belgium | |||

| Sweden | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Indonesia | |||

| South Korea | |||

| Thailand | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Chile | |||

| Peru | |||

| Rest of South America | |||

| Middle East and Africa | South Africa | ||

| Saudi Arabia | |||

| United Arab Emirates | |||

| Nigeria | |||

| Egypt | |||

| Morocco | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

What is the current size of the food and beverage market?

The market is valued at USD 9.79 trillion in 2026 and is projected to reach USD 11.78 trillion by 2031 at a 3.75% CAGR.

Which region leads the food and beverage market?

Asia-Pacific holds the largest 40.88% share, supported by urbanization, income growth and strong e-commerce uptake.

What distribution channel is growing the fastest?

Online retail is the fastest, expanding at a 5.63% CAGR as consumers adopt mobile ordering and home delivery.

How is packaging evolving in the food and beverage market?

Paperboard and other eco-friendly formats are rising at a 5.12% CAGR as brands respond to sustainability mandates.

Page last updated on: