Green IT Software For BFSI Sector Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.15 Billion |

| Market Size (2031) | USD 2.99 Billion |

| Growth Rate (2026 - 2031) | 21.06% CAGR |

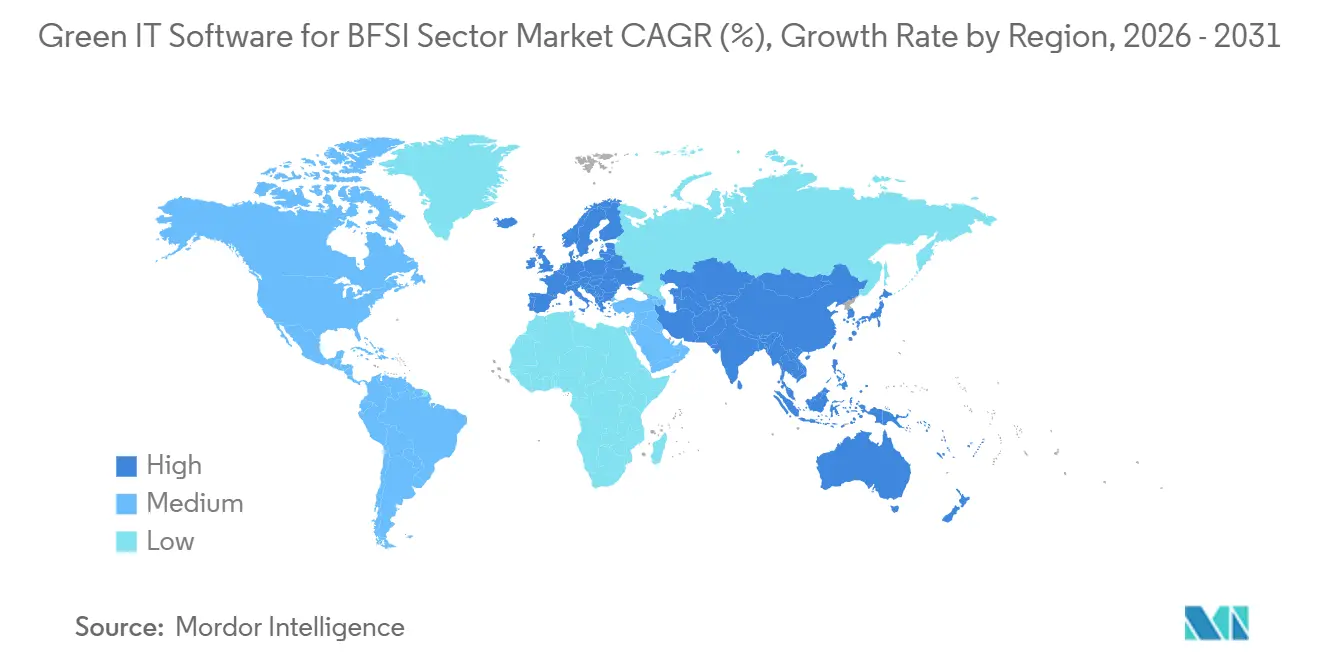

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

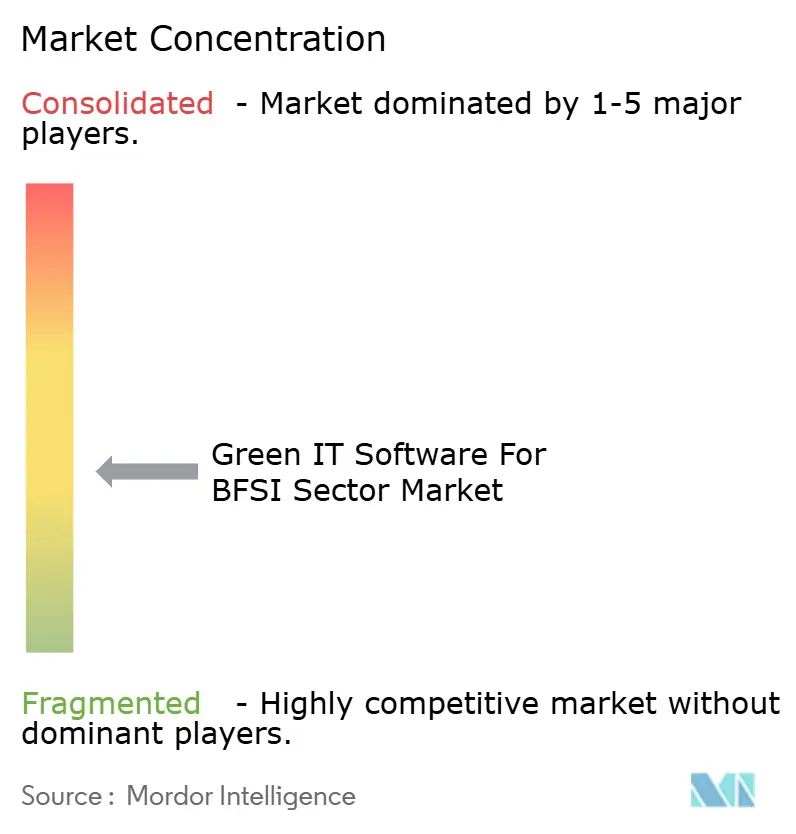

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Green IT Software For BFSI Sector Market Analysis by Mordor Intelligence

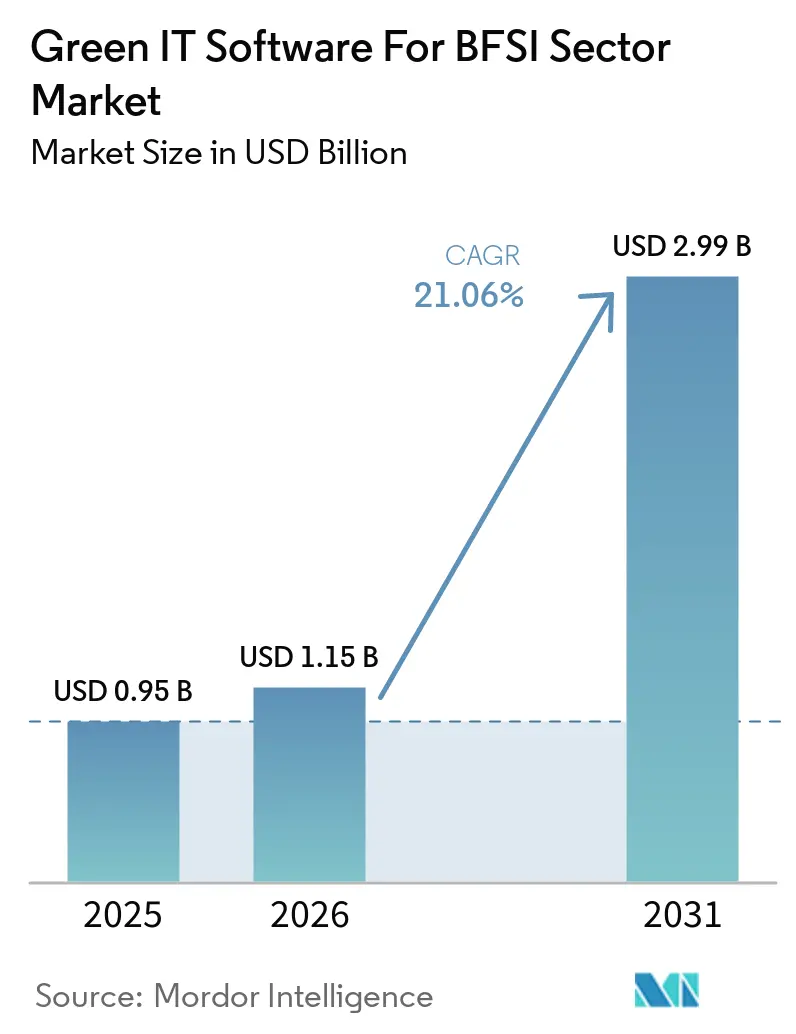

The Green IT software for BFSI sector market size is projected to be USD 0.95 billion in 2025, USD 1.15 billion in 2026, and reach USD 2.99 billion by 2031, growing at a CAGR of 21.06% from 2026 to 2031. The market is entering a phase in which regulated disclosure, external assurance, and financial reporting requirements are shaping software demand more directly than discretionary digital spending. This shift is strongest in financial services, where climate, financed emissions, and risk reporting now sit closer to core governance and treasury processes than to standalone sustainability programs. Different reporting frameworks across Europe, Asia-Pacific, and North America are also pushing buyers toward platforms that can collect data once and generate multiple reporting outputs without duplicating workflows. Competition is widening because large enterprise software vendors are using deeper integration to defend accounts, while specialist providers are winning interest with faster carbon analytics, supplier data ingestion, and framework-specific reporting capabilities. The near-term pace still depends on how companies respond to regulatory simplification in Europe, but the broader direction remains favorable because the compliance burden is spreading across more operating functions, more supplier networks, and more decision workflows.

Key Report Takeaways

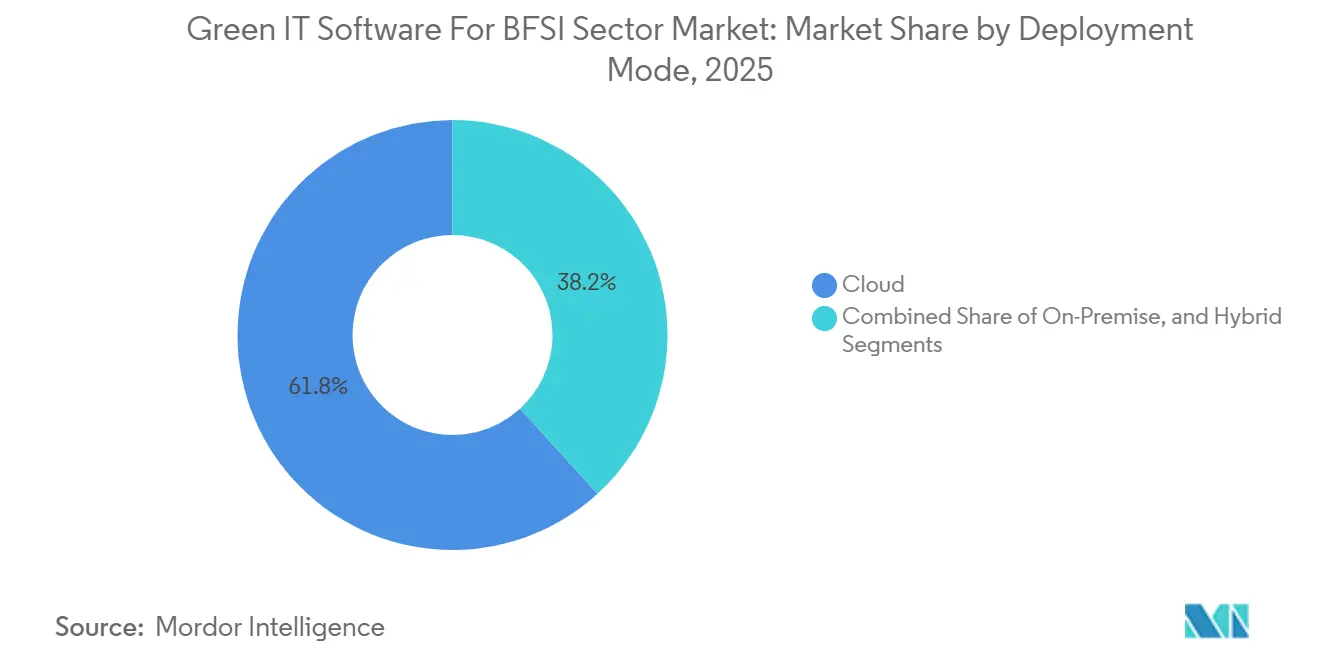

- By deployment mode, cloud-based platforms held 61.78% of the green IT software for BFSI sector market share in 2025, while hybrid deployment is projected to expand at a 21.32% CAGR through 2031.

- By software category, Sustainability Reporting and Management Software accounted for 39.45% share of the green IT software for BFSI sector market size in 2025, while Supply Chain Sustainability Software is projected to expand at a 23.28% CAGR through 2031.

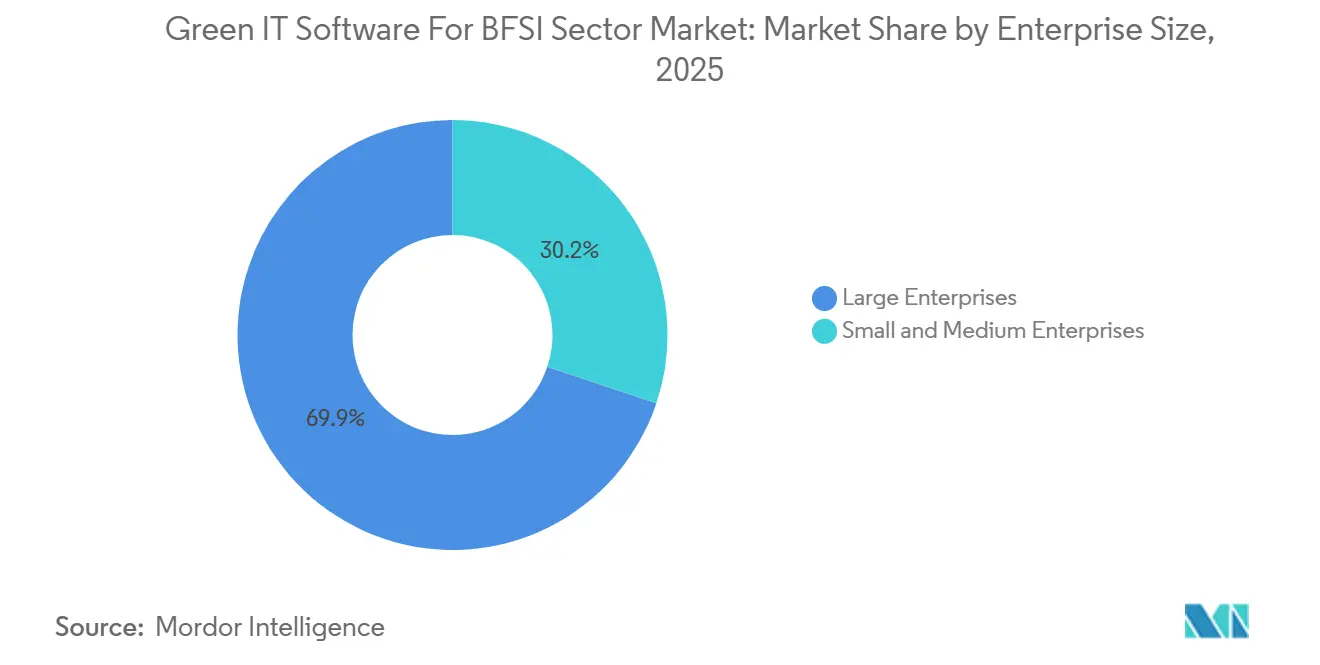

- By enterprise size, large enterprises held 69.85% share in 2025, while SMEs are projected to expand at a 21.22% CAGR through 2031.

- By geography, North America accounted for 41.62% share in 2025, while the Asia-Pacific is projected to expand at a 22.37% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Green IT Software For BFSI Sector Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Mandatory ESG Disclosure and Auditability in BFSI | +5.2% | Global, most intense in EU, Japan, China, and North America | Short term (≤ 2 years) |

| Financed Emissions Measurement Across Lending and Investment Books | +4.0% | Global, early adopters in EU, North America, and APAC | Medium term (2-4 years) |

| Cloud-Native Automation of Sustainability Data Workflows | +3.5% | Global | Short term (≤ 2 years) |

| AI-Driven Scope 3 Ingestion and Validation | +3.1% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Convergence of ESG, Risk, and Finance Platforms | +2.3% | North America and EU core, spillover to APAC | Medium term (2-4 years) |

| Green IT Cost Optimization for Branch, Data Center, and Workplace Operations | +1.5% | Global, data-center-dense markets in North America and APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory ESG Disclosure and Auditability in BFSI

Mandatory disclosure rules are the strongest immediate driver of the Green IT software for BFSI sector market, as regulated institutions can no longer treat sustainability reporting as a voluntary exercise. The 2026 EU Omnibus kept reporting obligations in place for Wave 1 public-interest entities and preserved the need for structured, audit-ready filings, even while later waves were narrowed to larger companies. Japan’s Financial Services Agency also formalized SSBJ-aligned disclosure in annual securities reports for large Prime Market companies, indicating that the Green IT software for BFSI sector market is supported by formal securities filing requirements rather than voluntary sustainability statements.[1] Financial Services Agency, “Sustainability Standards Board of Japan Disclosures in Annual Securities Reports,” Financial Services Agency, fsa.go.jp India extended BRSR Core assurance obligations from the top 250 to the top 500 listed companies from FY 2025-26, and planned to move to the top 1,000 from FY 2026-27, adding another layer of recurring implementation demand. The pressure is greater for institutions operating in more than one region because they must address double materiality, financial materiality, and local disclosure variations within a single reporting cycle. That is why the Green IT software for BFSI sector market is increasingly rewarding platforms that maintain a single underlying data model and generate multiple framework outputs without rebuilding controls each time.

Financed Emissions Measurement Across Lending and Investment Books

Financed emissions measurement is becoming a core growth engine for the Green IT software for the BFSI sector market, as banks and asset managers need portfolio-level carbon accounting that extends far beyond their own operational footprint. The supplied draft noted that financed emissions can exceed a financial institution’s direct footprint by a factor of 100 to 700, which makes Category 15 data more material than facility energy data for many BFSI users. PCAF expanded its standard in December 2025 to include additional asset classes and forward-looking transition finance metrics, making earlier estimation approaches less suitable for current review and assurance needs. SAP Fioneer responded by launching its Net Zero module in July 2025, and Rabobank adopted it to track climate performance at the portfolio, counterparty, asset, and individual loan levels inside banking workflows. This is changing the role of Green IT software in the BFSI sector, as financed emissions data is no longer used solely for external disclosure; it is now affecting credit assessments, capital allocation, and loan pricing logic. As that link strengthens, the Green IT software for BFSI sector market moves closer to risk management budgets and away from isolated reporting spend.

Cloud-Native Automation of Sustainability Data Workflows

Cloud-native architecture remains a major support factor for the Green IT software for BFSI sector market because frequent changes in disclosure rules are difficult to manage through slow upgrade cycles and fragmented on-premise deployments. SAP announced in May 2026 that several sustainability AI agents would become generally available by the end of 2026, and said these tools cut scenario simulation time from 1 day to 20 minutes and reduced packaging compliance review hours by more than 50%. IBM followed in April 2026 with the Envizi Emissions API, which lets companies embed Scope 1, 2, and 3 calculations directly into existing enterprise systems, eliminating the need to manage a separate reporting stream. The Green IT software for BFSI sector market benefits from this approach because regulatory logic, emissions calculations, and workflow controls can be updated in a single environment and shared across functions more quickly. Buyers also see cloud delivery as a way to connect sustainability programs with procurement, finance, and supplier management rather than leaving them in a separate compliance toolset. That shift is helping the Green IT software for BFSI sector market evolve from a reporting back-end to a broader operational layer that supports disclosure, controls, and decision workflows within the same system.

AI-Driven Scope 3 Ingestion and Validation

AI-led supplier data ingestion is another strong support factor for the Green IT software for BFSI sector market, as Scope 3 reporting still suffers from limited primary data coverage and heavy manual work. Watershed launched new AI capabilities in April 2026 for utility bill processing, emissions analysis, and report drafting, and early adopters reported saving up to 12 weeks of manual work each year. Persefoni introduced its Analytics Agent in May 2026, enabling users to query emissions data and identify footprint changes within the platform without leaving the workflow. EcoVadis and Watershed also formed a partnership in March 2026 to connect primary supplier carbon data with Watershed’s audit-ready calculations, which addresses a major weakness in proxy-based Scope 3 estimation. The Green IT software for BFSI sector market is gaining from this improvement because buyers can replace industry averages with more defensible supplier-level records and move closer to assurance-ready reporting. It also means the Green IT software for BFSI sector market is becoming more relevant to procurement scorecards, lending covenants, and supplier onboarding requirements rather than staying limited to annual reporting cycles.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented Legacy Data Across Core Banking and Risk Systems | -3.2% | Global, acute in legacy-heavy markets across South America and parts of APAC | Medium term (2-4 years) |

| Limited Availability of Financial-Grade Sustainability Data Talent | -2.4% | Global, most severe in emerging markets | Medium term (2-4 years) |

| High Integration Burden With Core Banking and Data Warehouses | -1.8% | Global, concentrated in EU and APAC | Medium term (2-4 years) |

| Data Sovereignty and Cross-Border Cloud Compliance Constraints | -1.3% | EU, APAC, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Legacy Data Across Core Banking and Risk Systems

Fragmented legacy system architecture is a meaningful brake on the green IT software for BFSI sector market because many financial institutions still store lending, risk, and accounting data across disconnected platforms that were never designed for sustainability metadata. PCAF’s own data quality scoring framework makes the issue clear because higher-quality financed emissions reporting depends on verified borrower-level information, while many institutions still rely on broad estimates and regional averages. The result is that implementation often needs costly extraction, transformation, and governance work before the green IT software for BFSI sector market can deliver value at enterprise scale. This slows time-to-deployment, raises integration costs, and makes software selection depend as much on data readiness as on product capability. The problem is even harder for banks operating in several jurisdictions because local system variations can block enterprise-wide consolidation for years rather than months. That is why the green IT software for BFSI sector market still faces friction in legacy-heavy environments, especially when institutions try to align risk, finance, and sustainability records within a single control framework.

Limited Availability of Financial-Grade Sustainability Data Talent

Limited specialist talent also constrains the green IT software for BFSI sector market because companies need people who understand sustainability disclosures, assurance expectations, and data engineering at the same time. NEC announced in April 2026 an AI-assisted disclosure service that can reduce annual securities report preparation time by up to 90%, and its launch reflects how buyers are using automation to address a shortage of qualified staff.[2]NEC, “AI-Assisted Sustainability Disclosure Service,” NEC, nec.com The staffing gap is more serious in emerging markets and smaller financial institutions, where budgets to hire scarce professionals are lower, and the reporting burden is still rising. This means the green IT software for BFSI sector market must often prove ease of implementation and guided workflow design before buyers will commit to wider rollouts. Vendors also face pressure because long onboarding cycles can reduce realized value and increase churn risk in smaller accounts. As a result, the green IT software for BFSI sector market is rewarding providers that tightly package templates, automation, and support services to reduce dependence on scarce internal expertise.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Dominance Intact as Hybrid Accelerates

Cloud deployment held 61.78% of the market in 2025, which gives it the largest share of the Green IT software for BFSI sector market size across deployment models. The leading position reflects how buyers in the Green IT software for BFSI sector market want regulatory updates, calculation changes, and reporting logic to be pushed across the user base without waiting for local infrastructure upgrades. Cloud delivery also reduces version fragmentation, which matters when institutions need consistent outputs across ESRS, PCAF, and SSBJ reporting cycles. This has made cloud platforms more attractive in organizations where sustainability data is moving closer to finance, risk, procurement, and supplier management processes. The preference is not only about infrastructure costs, because the main value now comes from the speed of updates, shared controls, and easier integration into enterprise workflows.

On-premises systems remain relevant in the ESG and sustainability software industry for state-owned banks, insurance providers, and government-adjacent entities that operate under strict data-residency or sovereign-hosting rules. In these cases, the buying decision is shaped by where sensitive financial and ESG records can be stored and how they are accessed during review and assurance. Hybrid deployment is the fastest-growing model and is forecast to expand at a 21.32% CAGR through 2031, which shows that the Green IT software for BFSI sector market is not moving in a simple one-way shift from local systems to public cloud. Institutions are building split architectures in which core financial data remains on-premises, while analytics, workflow automation, and reporting outputs run through cloud layers. AWS has demonstrated that cloud-based sustainability reporting environments can adapt to changing reporting requirements through configuration rather than full reimplementation, which supports the practical case for hybrid adoption in regulated settings.[3]Amazon Web Services, “Cloud Architectures for Sustainability Reporting and Regulatory Adaptation,” AWS, aws.amazon.com IBM’s API-first approach reinforces the same direction because buyers can add emissions logic to existing systems without forcing an immediate infrastructure replacement. This leaves the Green IT software for BFSI sector market with a durable role for hybrid models in sectors where control, auditability, and data sovereignty matter as much as speed. The deployment mix, therefore, reflects a market that values cloud resilience while still respecting operational boundaries set by regulators and internal risk teams.

By Software Category: Reporting Leads, Supply Chain Sustainability Grows Fastest

Sustainability Reporting and Management Software captured 39.45% of the 2025 Green IT software for BFSI sector market share, making it the largest category because structured disclosure remains the first mandatory purchase for many organizations. This lead position requires supporting audit-grade filings across CSRD, TCFD, GRI, and ISSB-aligned reporting frameworks, especially when companies must produce controlled and tagged outputs. Directive (EU) 2026/470 maintained the need for compliant filing structures for in-scope entities, which supports continued demand for platforms built around reporting controls and traceable workflows. The category also benefits from the fact that most companies still begin their sustainability systems journey with disclosure and management rather than with optimization tools. Workiva’s 2025 Intelligent Sustainability launch showed how vendors are expanding this category with agentic AI for materiality work, peer benchmarking, and multi-framework drafting inside finance and governance workflows.[4]Workiva, “Intelligent Sustainability,” Workiva, workiva.com

Carbon Management Software and Compliance and Risk Management Software continue to matter because the Green IT software for BFSI sector market increasingly needs systems that connect emissions accounting with policy control, risk review, and assurance requirements. Energy and Resource Optimization Software and EHS tools broaden the category mix further by serving industrial buyers that need sustainability workflows tied to operational performance, workplace safety, and facility-level resource use. Supply Chain Sustainability Software is projected to grow at a 23.28% CAGR through 2031, the fastest pace among software categories, as large-company Scope 3 obligations continue to spread through procurement networks. EcoVadis said in May 2026 that more than USD 2.5 trillion in procurement spend is already linked to sustainability risk insights through its network, demonstrating that supplier data has become part of purchasing logic rather than just disclosure activity. Schneider Electric’s Zeigo Hub, launched in July 2025, also points in the same direction by helping enterprises track supplier decarbonization and Scope 3 targets across wide vendor bases. The ESG and sustainability software industry is therefore seeing a widening addressable base as buyer demand shifts from filing support toward supplier engagement and commercial coordination. This pattern keeps reporting software in the lead today while giving supply chain tools the strongest forward momentum. It also means future category competition will depend on how well vendors integrate supplier data, calculation quality, and reporting outputs into a single environment. In practical terms, the Green IT software for BFSI sector market is rewarding products that turn external supplier records into decision-ready information rather than leaving them as static compliance documents.

By Enterprise Size: Large Enterprises Anchor Revenues, SMEs Close the Gap

Large enterprises represented 69.85% of the market in 2025, which shows that the biggest organizations still account for most revenue in the Green IT software for BFSI sector market size because they face the broadest regulatory and operational burden. These companies usually need multi-jurisdictional deployment, deeper integration with ERP and financial systems, and stronger control layers for third-party assurance and internal review. They also manage larger supplier networks and additional reporting frameworks simultaneously, which increases licensing, implementation, and services demand. This supports premium product strategies from vendors that can combine workflow automation, auditable data lineage, and cross-functional reporting within a single platform. The enterprise tier is also where most high-profile product launches have been aimed, including Workiva’s agentic AI enhancements, SAP’s sustainability AI agents, IBM’s emissions API, and Persefoni’s analytics tools.

Large account strategy in the ESG and sustainability software industry is increasingly built around value-chain connectivity rather than standalone reporting modules. EcoVadis and Workiva announced a partnership in May 2026 that linked supplier carbon data to reporting workflows, a good example of how enterprise buyers want stronger coordination across procurement and disclosure functions. The Green IT software for BFSI sector market is also seeing demand from large enterprises that need controlled supplier outreach under the newer VSME-style limits on what smaller suppliers can be asked to provide within European reporting chains. SMEs are projected to grow at a 21.22% CAGR through 2031, indicating that the next wave of demand is spreading beyond direct reporters into supplier ecosystems. Much of that growth comes from indirect pressure because larger customers now request emissions and sustainability data from smaller vendors, even when those vendors are not directly regulated. Providers serving SMEs are responding with modular SaaS tools, guided templates, and lighter implementation models that reduce cost and complexity. The commercial challenge is that SME accounts generate less revenue per customer while still requiring education, onboarding, and support. Even so, the Green IT software for BFSI sector market is gaining from this segment because smaller companies that build data systems early can move into higher-value plans as reporting expectations expand. That gives vendors a longer upgrade path and extends demand beyond the largest listed companies. It also means the market’s future customer base will be shaped by supply-chain compliance transmission as much as by direct regulation.

Geography Analysis

North America held 41.62% of the market in 2025, which gave it the largest regional position in the Green IT software for BFSI sector market share and kept it as the leading geography in 2026. The region’s scale reflects early enterprise adoption, strong investor pressure, and the role of state-level regulation in pushing reporting and emissions management into mainstream corporate systems. California’s SB-253 and SB-261 are particularly important because they extend disclosure obligations across large companies with material operations in the state, even when those firms are not defined by one federal listing route.[5]California State Legislature, “SB-253 and SB-261,” California Legislative Information, leginfo.legislature.ca.gov Canada also supports regional demand by providing climate risk guidance for federally regulated financial institutions and by promoting the broader adoption of disclosure practices in capital markets. The Green IT software for BFSI sector market in North America also benefits from the concentration of large platform vendors and the region’s role as the first testing ground for many product launches before wider global rollout.

Europe remains a structurally important part of the Green IT software for BFSI sector market size because the region still has the deepest formal reporting architecture even after the Omnibus revision. Directive (EU) 2026/470 narrowed the mandatory population for later waves, but it kept audit-grade obligations, structured filing requirements, and core alignment expectations in place for entities already inside scope. The EBA’s ESG risk management guidelines create an additional demand layer in banking that operates alongside disclosure requirements, which gives the European Green IT software for BFSI sector market a distinct BFSI purchasing base. Europe also remains a demanding region for vendors because regulatory changes force repeated platform updates and keep product depth, assurance support, and data controls at the center of buying decisions.

Asia-Pacific is forecast to expand at a 22.37% CAGR through 2031, making it the fastest-growing regional block in the Green IT software for BFSI sector market. Japan’s February 2026 FSA mandate for SSBJ-aligned disclosures in annual securities reports created a clear compliance timetable for large Prime Market companies, including mandatory climate reporting elements. China’s major exchanges also updated their sustainability reporting guidance in January 2026, requiring index-linked issuers to submit 2025 sustainability reports by April 30, 2026, and to meet more detailed environmental reporting expectations. India’s BRSR Core rollout is extending third-party assurance obligations incrementally, supporting a continuous procurement cycle as more listed companies enter the mandatory scope. South America contributes through Brazil’s developing disclosure framework and multinational supply-chain demands, while the Middle East is gaining relevance through net-zero commitments and sovereign capital priorities, and Africa retains momentum, with integrated reporting requirements already established in South Africa. Together, these conditions make Asia-Pacific the main growth frontier while keeping the broader emerging regional set active through supplier compliance transmission, capital market expectations, and the gradual formalization of reporting rules.

Competitive Landscape

The Green IT software for BFSI sector market is moderately fragmented, with global enterprise vendors such as SAP, IBM, Microsoft, and Salesforce competing alongside specialist providers including Workiva, EcoVadis, Persefoni, Watershed, and Cority. Large platforms usually compete on integration depth, enterprise account coverage, and the ability to connect sustainability data with ERP, finance, and risk systems. Specialists tend to compete on framework precision, faster product iteration, deeper carbon accounting, and supplier data connectivity. This split means one product model does not control the Green IT software for BFSI sector market, because customers buy for different workflow needs across disclosure, financed emissions, supply chain, and operational optimization. The result is a market where product architecture and use-case fit often matter more than brand scale alone.

Several strategic moves show how vendors are trying to widen their positions inside the Green IT software for BFSI sector market. Workiva’s Intelligent Sustainability launch in September 2025 added agentic AI, unified data automation, and multi-framework support within the Office of the CFO, thereby strengthening its position in controlled reporting workflows. IBM launched the Envizi Emissions API in April 2026 to embed emissions calculations into existing enterprise systems, giving IBM a way to participate even when clients use another reporting front end. EcoVadis built partnerships with Watershed and Workiva in 2026, which helped it turn supplier carbon data into a shared input across several reporting environments rather than a closed network asset.

There is still open space in the Green IT software for BFSI sector market, especially among regional banks and asset managers that sit below the largest public-company tier but still face climate, financed emissions, and governance requirements. Schneider Electric’s Resource Advisor+ launch in January 2026 is a useful example because it links energy management, carbon performance, and supply chain sustainability in a single consulting-led platform. SAP Fioneer’s Net Zero module is another example because it brought financed emissions tracking into banking, finance, and risk processes, which is a more specialized move than general disclosure software. ISO 14064 and ISO 14001 remain relevant in procurement reviews, especially where buyers expect external assurance and formal environmental management discipline. The Green IT software for BFSI sector market is therefore moving toward competition based on workflow depth, ecosystem connectivity, and sector fit rather than on a single winner-takes-all platform logic. Vendors that can connect supplier data, emissions methods, and filing-ready outputs are better positioned to defend accounts. Vendors that cannot demonstrate strong integration or a reliable methodology may struggle as enterprise buyers narrow their vendor lists. This keeps the competitive structure active and leaves room for both broad platforms and focused specialists. It also supports continued partnership activity because interoperability has become a selling point in its own right.

Green IT Software For BFSI Sector Industry Leaders

Microsoft Corporation

IBM Corporation

SAP SE

Salesforce, Inc.

Workiva Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Novara acquired Ensogo, an AI-native sustainability and ESG software company headquartered in Toronto, Canada, expanding Novara's environmental reporting, operational visibility, and ESG compliance capabilities across manufacturing, mining, energy, oil and gas, and construction sectors, while broadening its geographic presence into Canada. The transaction accelerates Novara's AI and analytics capabilities across industrial sustainability workflows.

- May 2026: SAP SE announced that five new sustainability AI agents, Sustainability Regulatory Readiness Agent, Footprint Optimization Agent, Packaging Compliance Agent, GHS Classification and Labeling Agent, and Workplace Safety Agent, will become generally available by the end of 2026, following beta testing. The agents reduce packaging compliance review hours by more than 50%, cut scenario simulation time from approximately one day to 20 minutes, and reduce manual GHS classification effort by up to 80%.

- May 2026: EcoVadis and Workiva Inc. announced a strategic partnership integrating EcoVadis' Carbon Data Network with Workiva Carbon, enabling mutual customers to replace industry-average Scope 3 emission estimates with granular, audit-ready supplier-specific carbon data within a single reporting environment. The partnership is part of EcoVadis' broader effort to build an interconnected carbon ecosystem across the 175,000+ companies in its supplier network.

- May 2026: Persefoni unveiled the Analytics Agent, an agentic AI tool designed to accelerate emissions analysis and root-cause attribution of footprint changes directly within the Persefoni platform. The agent targets BFSI and enterprise clients with PCAF financed emissions reporting requirements, enabling faster path-to-net-zero planning.

Global Green IT Software For BFSI Sector Market Report Scope

Green IT Software for the BFSI Sector refers to specialized digital platforms designed to help banks, financial institutions, and insurance companies implement and manage sustainability initiatives within their operations. These solutions incorporate functionalities such as carbon accounting, ESG compliance reporting, energy optimization for data centers and branches, and AI-driven Scope 3 emissions validation. By embedding these capabilities into core finance and risk workflows, BFSI enterprises can minimize their environmental impact while adhering to regulatory requirements and ensuring audit-ready disclosures.

The Green IT Software for BFSI Sector Market Report is Segmented by Deployment Mode (Cloud, On-Premise, and Hybrid), Software Category (Carbon Management Software, Sustainability Reporting and Management Software, Energy and Resource Optimization Software, Compliance and Risk Management Software, Supply Chain Sustainability Software, and Environment, Health, and Safety Software), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Cloud |

| On-Premise |

| Hybrid |

| Carbon Management Software |

| Sustainability Reporting and Management Software |

| Energy and Resource Optimization Software |

| Compliance and Risk Management Software |

| Supply Chain Sustainability Software |

| Environment, Health, and Safety Software |

| Large Enterprises |

| Small and Medium Enterprises |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Singapore | |

| Rest of Asia-pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Deployment Mode | Cloud | |

| On-Premise | ||

| Hybrid | ||

| By Software Category | Carbon Management Software | |

| Sustainability Reporting and Management Software | ||

| Energy and Resource Optimization Software | ||

| Compliance and Risk Management Software | ||

| Supply Chain Sustainability Software | ||

| Environment, Health, and Safety Software | ||

| By Enterprise Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Singapore | ||

| Rest of Asia-pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size and outlook for ESG and sustainability software?

The green IT software for BFSI Sector market stood at USD 0.95 billion in 2025, is valued at USD 1.15 billion in 2026, and is projected to reach USD 2.99 billion by 2031 at a 21.06% CAGR.

Which region leads global demand for ESG and sustainability software?

North America led with 41.62% share in 2025 and remained the largest regional market in 2026, supported by investor expectations, state-level disclosure rules, and strong enterprise software adoption.

Which region is growing the fastest through 2031?

Asia-Pacific is projected to record the fastest growth at a 22.37% CAGR through 2031 as Japan, China, and India continue to formalize disclosure and assurance requirements.

Which deployment model is used the most?

Cloud is the leading deployment model with 61.78% share in 2025 because buyers want faster regulatory updates, lower version fragmentation, and easier links with finance, risk, and procurement systems.

Which software category is expanding the fastest?

Supply Chain Sustainability Software is projected to grow at a 23.28% CAGR through 2031 as Scope 3 reporting obligations spread from large enterprises to supplier networks.

Why are large enterprises still the main buyers?

Large enterprises held 69.85% share in 2025 because they manage more jurisdictions, more reporting frameworks, and larger supplier networks, which raises the need for integrated and assurance-ready platforms.

Page last updated on: