India Green IT Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

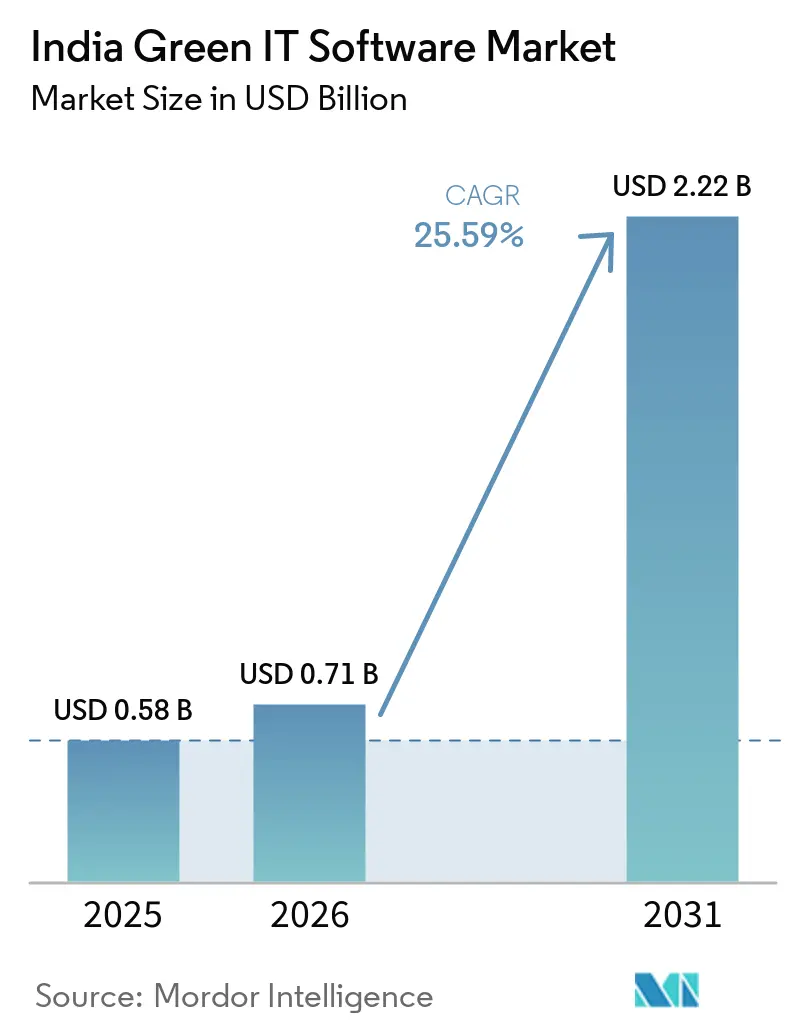

| Base Year Market Size (2025) | USD 0.58 Billion |

| Market Size (2026) | USD 0.71 Billion |

| Market Size (2031) | USD 2.22 Billion |

| Growth Rate (2026 - 2031) | 25.59% CAGR |

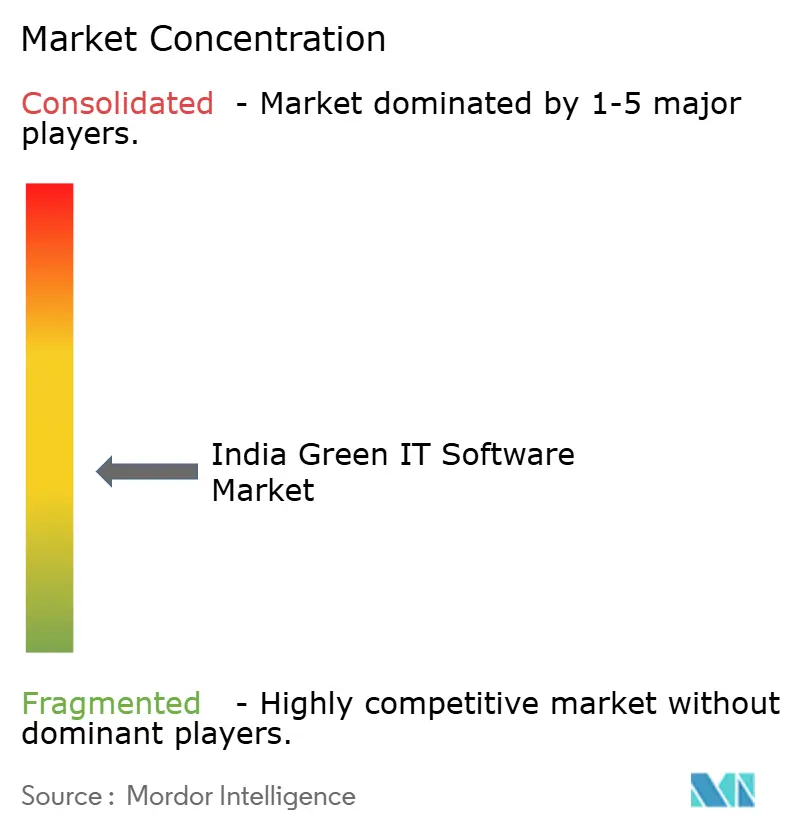

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Green IT Software Market Analysis by Mordor Intelligence

The India green IT software market size is expected to increase from USD 0.58 billion in 2025 to USD 0.71 billion in 2026 and reach USD 2.22 billion by 2031, growing at a CAGR of 25.59% over 2026-2031. Growth in the India green IT software market is being shaped by stronger corporate sustainability commitments, rising power costs in data-intensive operations, and a more formal reporting environment for listed companies. Enterprises are moving away from spreadsheets and isolated tracking tools because these methods do not support audit-ready reporting or steady cross-functional use. Demand is also widening from large listed companies toward suppliers, service firms, and energy-intensive operators that now need cleaner emissions data and better workflow control. Competition is centered on platform depth, system integration, and the ability to support multiple reporting frameworks in one operating environment. The India green IT software market is also gaining from the buildout of hyperscale and colocation infrastructure, which is raising the value of software that can connect energy use, emissions accounting, and compliance reporting in one system.

Key Report Takeaways

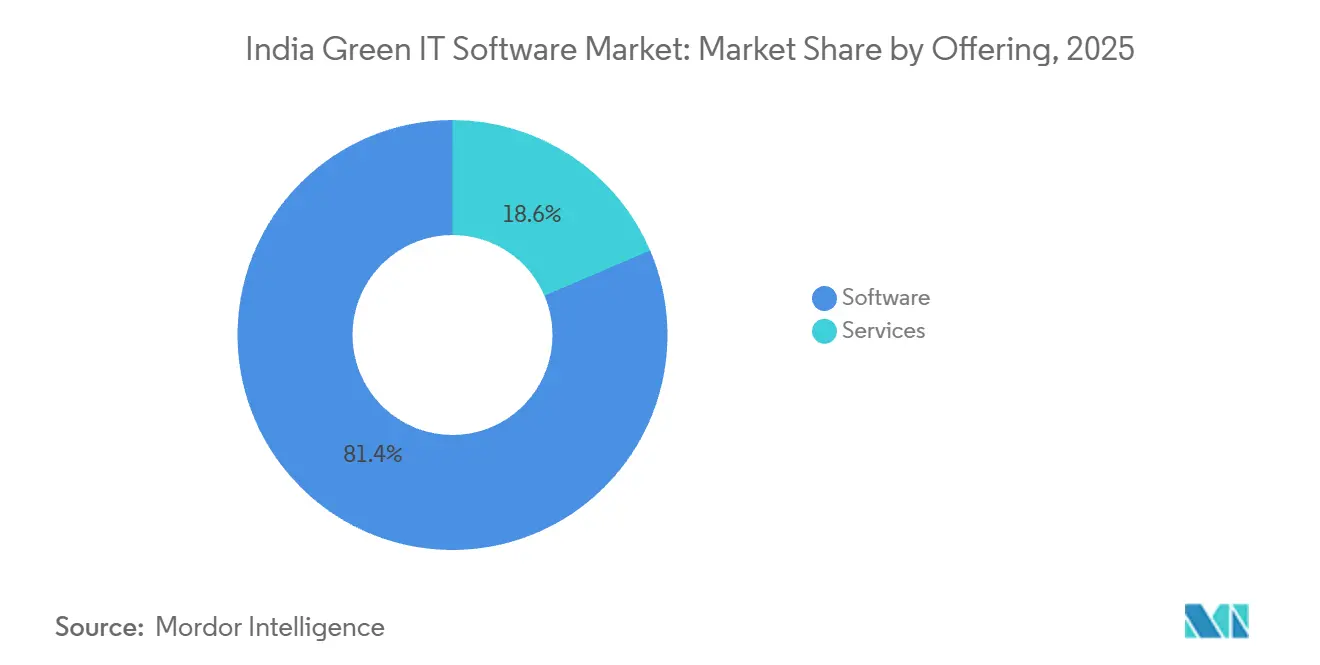

- By offering, software held 81.43% share in 2025, while services are projected to expand at a 29.74% CAGR through 2031.

- By deployment mode, cloud held 73.86% of the India green IT software market share in 2025, while hybrid is projected to record the fastest CAGR of 31.28% through 2031.

- By organization size, large enterprises accounted for 74.91% share in 2025, while SMEs are projected to grow at a 28.96% CAGR through 2031.

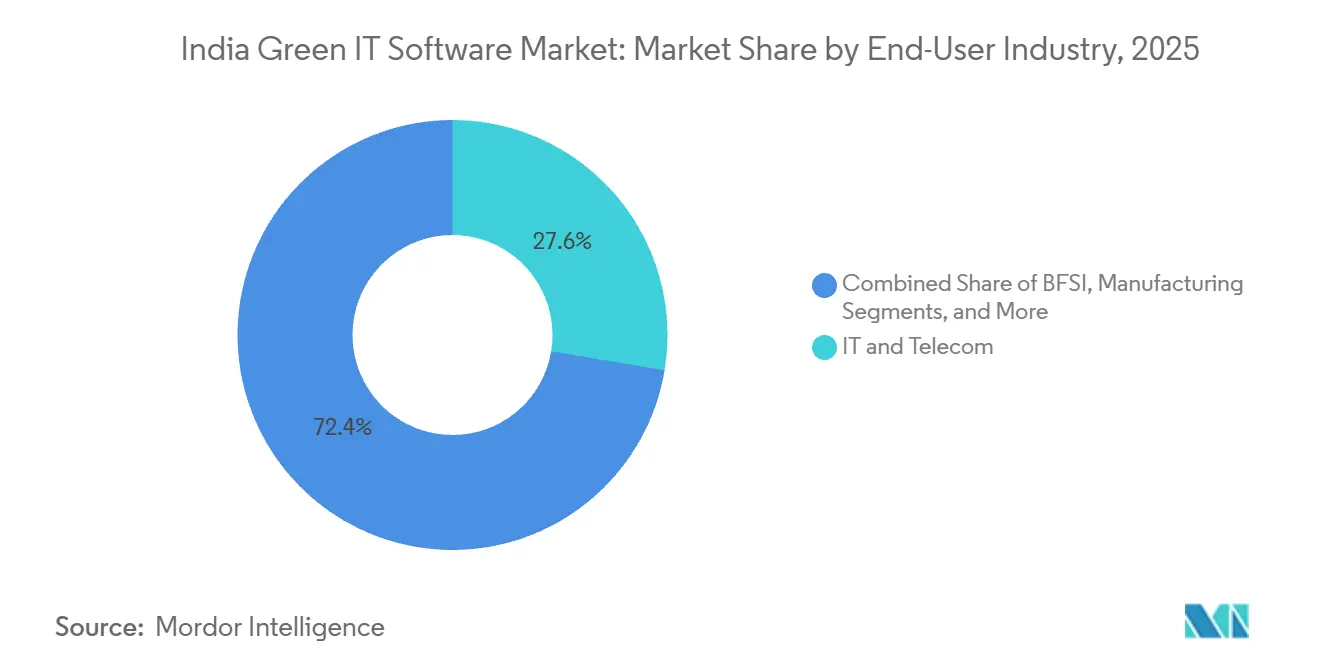

- By end-user industry, IT and Telecom accounted for 27.62% of the India green IT software market size in 2025, while healthcare is projected to expand at a 30.15% CAGR through 2031.

- By solution type, Carbon Management and Accounting Software held 33.48% share in 2025, while Decarbonization Planning Software is projected to grow at a 31.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Green IT Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Corporate Net-Zero Commitments | +5.2% | National, with early gains in Mumbai, Bengaluru, Delhi NCR | Medium term (2-4 years) |

| Escalating Data Center Energy Costs | +4.8% | National, concentrated in Mumbai, Chennai, Hyderabad, Visakhapatnam | Short term (≤ 2 years) |

| Regulatory Push for Emissions Disclosure | +4.5% | National, with high intensity in NSE and BSE listed company hubs | Medium term (2-4 years) |

| Expansion of Hyperscale and Colocation Data Centers in India | +3.8% | Andhra Pradesh, Gujarat, Maharashtra, Tamil Nadu | Medium term (2-4 years) |

| AI-Based Energy Optimization in IT Workloads | +3.2% | National, with early adoption in Bengaluru, Hyderabad, Pune | Long term (≥ 4 years) |

| Green Software Procurement by Large Indian Enterprises | +2.8% | National, with early gains in IT and ITES hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Corporate Net-Zero Commitments

India’s corporate net-zero target base increased from 29 to 34 companies between 2024 and 2025, showing a stronger governance posture among large enterprises.[1]Net Zero Tracker, “Net Zero Stocktake 2025,” Net Zero Climate, zerotracker.net This matters for the India green IT software market because each target requires a more formal process for emissions measurement, internal controls, and repeatable disclosure. Companies that move from target setting to assured reporting cannot rely on spreadsheet-led processes for long because they need version control, audit trails, and better supplier data handling. The buying decision is also becoming less voluntary because external stakeholders increasingly expect comparable and credible climate data from Indian companies with public commitments. As a result, the India green IT software market is benefiting from sustainability programs that now sit closer to finance, compliance, procurement, and board-level oversight.

Escalating Data Center Energy Costs

India’s hyperscale data center pipeline is making electricity management a central operating issue rather than a secondary facility concern. AirTrunk committed USD 30 billion to build 5 GW of data center capacity in India by 2030, which highlights the scale at which power use and efficiency now shape infrastructure economics. Google’s direct electricity management move for its planned Visakhapatnam facility showed that energy procurement and usage monitoring are becoming strategic capabilities for operators in the country. This directly supports the India green IT software market because buyers need tools that can track energy intensity, compare facility performance, and connect usage data with reporting obligations. As more large computing capacity comes online, software demand extends beyond traditional enterprise users to hyperscalers, colocation providers, and large property operators linked to digital infrastructure.

Regulatory Push for Emissions Disclosure

India’s listed company disclosure environment is tightening through a structure that expects more formal climate reporting from large enterprises and their value chains. This creates demand in the India green IT software market because companies need systems that can gather activity data, maintain control frameworks, and produce repeatable outputs across entities and sites. The pressure is stronger for firms with complex operating footprints because manual processes create duplication, inconsistent boundaries, and weak audit support. Companies that serve export markets also face a practical need to align Indian disclosures with wider reporting expectations from customers and investors outside India. This is pushing buyers toward integrated sustainability platforms rather than narrow tools that solve only one reporting task at a time.

Expansion of Hyperscale and Colocation Data Centers in India

The expansion of hyperscale and colocation facilities is creating a wider demand base for the India green IT software market beyond board-led ESG programs. A CEEW study noted that hyperscalers and colocation operators dominate India’s data center landscape, with the top 5 operators holding 66% of operational capacity. Meta’s June 2026 decision to lease a 168 MW AI-enabled data center in Jamnagar, along with renewable energy tie-ups exceeding 900 MW, showed how quickly sustainability-linked infrastructure commitments are scaling in India.[2]CNBC, “Meta Agrees to Indian AI Data Center Deal with Reliance Industries,” CNBC, cnbc.com Operators in this environment need software that can connect renewable energy use, cooling efficiency, workload intensity, and audit-ready disclosures in one operating model. This changes the demand mix because energy monitoring and carbon accounting are becoming part of the base digital stack for data center growth in India rather than optional add-ons.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity with Legacy Enterprise Systems | -3.2% | National, with high intensity in manufacturing and BFSI hubs | Medium term (2-4 years) |

| Limited Availability of Skilled Green IT and Carbon Accounting Talent | -2.8% | National, most acute in tier-2 and tier-3 cities | Long term (≥ 4 years) |

| Data Quality Gaps in Scope 3 and Embedded Emissions Tracking | -2.1% | National, with high intensity in manufacturing supply chains | Medium term (2-4 years) |

| Buyer Hesitation Around Near-Term ROI in Mid-Market Firms | -1.6% | National, most acute in non-BRSR-mandated mid-market segments | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity with Legacy Enterprise Systems

Many Indian enterprises still run on ERP landscapes that were not designed to produce carbon accounting outputs from site-level operating data. This slows the India green IT software market because software deployment often needs middleware work, custom APIs, and master data cleanup before reporting can stabilize. The problem is most visible in manufacturing, energy, and BFSI environments where operating systems, utility data, and supplier records sit across several disconnected platforms. Buyers in these sectors often face longer implementation cycles because sustainability reporting cannot be separated from broader data architecture issues. Vendors are responding with connectors for major enterprise systems, but deployments still stretch when emissions capture needs plant-level or facility-level granularity. That keeps sales cycles longer and raises the total cost of ownership for buyers who are also funding core modernization projects.

Limited Availability of Skilled Green IT and Carbon Accounting Talent

India also faces a practical skills gap at the point where sustainability methods, enterprise data, and software administration meet. This limits the India green IT software market because a purchased platform still needs people who can structure emissions boundaries, clean source data, and manage recurring disclosure workflows. The issue is sharper outside major metro clusters, where buyers may have budget approval but do not yet have stable operating teams for sustainability software. The result is a slower time to value, weaker internal adoption, and a greater risk that software remains underused after implementation. It also affects service-led expansion because system integrators and consulting teams need trained staff who can translate reporting rules into working data models. Until this talent base becomes broader, software growth will remain strongest in organizations that already have larger digital and compliance teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Platform Supremacy Persists as Services Scale Up

Software commanded 81.43% of the market in 2025, which shows how strongly buyers favored scalable platforms over project-led support in the early phase of adoption. The India green IT software market developed this way because listed enterprises needed systems that could be audited, updated, and reused across multiple reporting cycles. Software demand was also supported by the need for centralized workflows, permission controls, and consistent methods for emissions measurement across large organizations. Buyers in regulated or disclosure-heavy settings usually preferred subscription tools because they created a more durable operating layer than one-time advisory work. This helped software remain the base category for adoption even as companies continued to rely on outside experts during implementation.

Services are still gaining ground quickly and are projected to expand at a 29.74% CAGR through 2031, which reflects a wider need for configuration, integration, and managed reporting support. Many mid-sized companies are entering the India green IT software industry without internal sustainability technology teams, so they are turning to implementation partners to shorten deployment time. That raises the value of managed services because buyers want help with supplier data requests, workflow setup, and recurring report preparation after the platform goes live. Indian IT service firms are well-positioned in this layer because they already manage ERP, cloud, and compliance environments for many large enterprises. The services opportunity also helps smaller software vendors because they can reach enterprise customers through partner-led delivery models instead of building large direct service teams. Over time, the balance between software and services is likely to become more complementary, with platform revenue anchoring the account and service revenue driving adoption depth and renewal stability.

By Deployment Mode: Cloud Leads, Hybrid Closes the Distance Fast

Cloud deployment accounted for 73.86% in 2025, which confirms that most buyers wanted lower setup friction and faster access to updated reporting logic. Cloud-first adoption suited the India green IT software market because companies could avoid heavy local infrastructure builds and rely on regular product updates. It also matched the broader shift toward SaaS business systems across Indian enterprises, especially where sustainability teams are lean and depend on shared IT support. Centralized access and easier upgrades made cloud systems attractive for companies handling recurring disclosure cycles across many internal stakeholders. This kept cloud in the lead even where buyers still depended on several older operating systems in the background.

Hybrid deployment is the fastest-growing mode and is projected to advance at a 31.28% CAGR through 2031 because many large enterprises need to connect on-premises operational data with cloud-based calculation and reporting engines. In that context, hybrid captured the most practical middle ground for the India green IT software market because it respects data sensitivity while still allowing modern analytics and workflow orchestration. Large companies in manufacturing, financial services, and complex multi-site operations often cannot shift every dataset into a pure cloud setup at the same pace. Hybrid models, therefore, allow them to keep certain records and source systems local while using the cloud for emissions logic, dashboards, and disclosure preparation. On-premises deployments still retain some presence in environments with stronger localization preferences, but their relative role is narrowing as cloud security and domestic hosting choices improve. The real product advantage now sits with vendors that can support mixed architectures without making buyers redesign the rest of their enterprise stack.

By Organization Size: Large Enterprises Anchor Revenues While SMEs Represent Structural Upside

Large enterprises held 74.91% share in 2025, which reflected the concentration of early spending among companies with the highest disclosure obligations and the broadest internal reporting structures. This concentration defined the India green IT software market in its current phase, as large listed organizations had stronger budgets, stronger governance requirements, and greater pressure to formalize climate data. They also faced a wider Scope 3 challenge because supplier networks, business units, and operating sites had to be brought into one reporting model. That favored enterprise-grade platforms over lighter tools with limited control features or weak integration depth. In many cases, adoption by large enterprises also had a signaling effect inside supply chains because suppliers started to receive more structured requests for emissions and activity data.

SMEs are projected to grow at a 28.96% CAGR through 2031, making them the most important structural expansion layer for the next phase of the India green IT software market. This shift is happening because value-chain reporting requests are moving downstream from large enterprises to suppliers that were not previously inside formal disclosure systems. The SME opportunity in the India green IT software industry is also being widened by lower-cost platforms that are designed around Indian reporting needs and simpler workflow setup. Buyers in this segment tend to prefer tools that reduce manual template work and fit into existing accounting and compliance routines with limited customization. Adoption is also spreading outside the largest metro centers as industrial towns in Gujarat, Maharashtra, and Tamil Nadu face stronger customer-led sustainability data expectations. That creates a broader demand map where future growth comes less from the first wave of large buyers and more from second-wave suppliers and mid-market adoption.

By End-User Industry: IT and Telecom Sets Benchmarks, Healthcare Emerges as a Fast Mover

IT and Telecom led all end-user industries with a 27.62% share in 2025, showing that the sector remained the earliest and most organized adopter of green IT software. This lead fit the India green IT software market because IT companies already had stronger digital operating models, central data teams, and visible sustainability commitments. The sector also benefits from using its own internal environment as a testing ground for reporting workflows, automation, and cross-site emissions tracking. That tends to shorten adoption cycles because internal software familiarity is already high and governance teams are used to regular disclosures. As a result, IT and Telecom continue to set the pace for platform depth, reporting maturity, and enterprise-wide rollout models.

Healthcare is projected to expand at a 30.15% CAGR through 2031, which makes it the fastest-growing end-user segment even without the same direct compliance pressure seen in some industrial sectors. The growth signal matters for the India green IT software market because it shows that buying decisions are no longer driven only by mandatory reporting, they are also shaped by financing, accreditation, and operational management needs. Hospitals and healthcare providers are placing more weight on environmental performance metrics, which creates demand for software that can connect facility data with broader sustainability reporting. BFSI is also moving forward because climate-risk reporting and investor scrutiny are increasing the need for portfolio-level emissions visibility. Manufacturing and utilities remain important demand centers where facility-level accounting is tied more directly to energy intensity and compliance readiness. Government, retail, and construction are still earlier in the adoption curve, but procurement reform and greener commercial assets are creating new entry points for software vendors.

By Solution Type: Carbon Accounting Anchors Budgets, Decarbonization Planning Builds Momentum

Carbon Management and Accounting Software held 33.48% in 2025, making it the largest solution category because most buyers still begin with measurement before they move into strategy and optimization. That pattern is central to the India green IT software market because companies first need verified emissions data before they can set targets, test pathways, or track operational improvements with confidence. Early budgets, therefore, flowed to tools that support boundary setting, emissions calculation, audit readiness, and recurring disclosures. This made carbon accounting the entry point for many enterprise programs, especially where reporting quality mattered more than advanced planning features in the first phase. It also gave integrated platform vendors an advantage because accounting functions often become the system of record for later modules.

Decarbonization Planning Software is projected to grow at a 31.82% CAGR through 2031, which shows that buyers are starting to shift from measurement alone toward action sequencing and reduction planning. In the India green IT software market size mix, this category is expanding because enterprises with 2 to 3 years of baseline data now want tools that can model pathways and connect targets with operating decisions. ESG Reporting and Compliance Software and Sustainability Data Management Platforms also continue to grow because buyers must handle several overlapping disclosure formats with more control and less manual rework. Energy and Resource Optimization Software is gaining traction in data center and manufacturing settings, where software can link environmental goals with direct cost savings. The overall direction suggests that spending is broadening from single-purpose deployment toward multi-module platform adoption. Vendors that cover accounting, reporting, planning, and optimization in one environment are therefore in a stronger position as buyer maturity rises.

Geography Analysis

The India green IT software market remains concentrated in Bengaluru, Mumbai, Delhi NCR, Hyderabad, Chennai, and Pune because these cities host a high share of large enterprises, IT services firms, and disclosure-led corporate activity. Bengaluru continues to lead adoption through its dense base of IT services majors and global capability centers that have moved carbon accounting closer to core governance processes. Mumbai remains a strong demand center because BFSI institutions face growing pressure around climate disclosure and portfolio transparency. Delhi NCR is also important because many listed companies, national business groups, and regulatory-facing corporate functions are concentrated there. This metro concentration gave India's green IT software market an early growth base built on enterprise density rather than national diffusion alone.

The coastal infrastructure story is widening the map. CEEW identified advantages for cities such as Mumbai, Chennai, and Visakhapatnam because of cable landing access and location features that support large data center development.[3]Council on Energy, Environment and Water, “Data Centre Study, Market and Energy Outlook,” CEEW, ceew.in Google’s energy management step in Visakhapatnam and Reliance-linked data center expansion in Andhra Pradesh are reinforcing that shift toward new digital infrastructure corridors. In Gujarat, Meta’s Jamnagar project is adding another location where renewable power, compute infrastructure, and software-led sustainability monitoring are becoming tightly linked.

Tier-2 cities such as Ahmedabad, Coimbatore, Nagpur, and Bhubaneswar are also seeing early adoption as supply-chain digitization pushes sustainability data requests deeper into industrial networks. The India green IT software market share of future demand is therefore likely to widen geographically as suppliers and exporters respond to customer-led data expectations. Pune is gaining in manufacturing-led demand, while Hyderabad is strengthening in pharmaceuticals and technology-linked sustainability workflows. Smaller cities are still at an earlier stage, but they are no longer outside the commercial scope of the India green IT software market because compliance reach, export pressure, and infrastructure investment are moving together.

Competitive Landscape

The India green IT software market is fragmented across solution types, but enterprise buying is showing clearer consolidation around vendors that can support scale, controls, and integration depth. Global pure-play carbon software providers compete with large enterprise platform vendors that already sit inside Indian finance, ERP, and reporting environments. This creates a market where buyers often choose between methodological specialization and broader enterprise system fit. The difference matters because some companies want purpose-built carbon tools, while others prefer sustainability modules that extend software already used across the organization. That tension is likely to remain a defining feature of the India green IT software market as adoption moves from first purchase to multi-year platform standardization.

Product strategy is increasingly centered on automation. Persefoni launched its Analytics Agent in May 2026 to help users work with emissions data through natural language prompts, showing how workflow speed is becoming a point of competition. Watershed launched AI agents in April 2026, including a data cleaning tool that reduced time to actionable sustainability data by 80% across test customers, which directly addresses one of the hardest adoption bottlenecks in carbon reporting. SAP also announced sustainability AI agents in May 2026 that extend regulatory readiness and disclosure support inside its broader enterprise stack, which strengthens the case for embedded platform models.[4]SAP News Center, “New Sustainability AI Agents,” SAP, sap.com

Another area of competition is the link between cloud infrastructure data and carbon accounting workflows. Sweep announced in June 2026 that it had built a measurement solution using AWS Sustainability Service so enterprise users could pull audit-ready cloud emissions data into one reporting environment. That matters for the India green IT software market because data center growth and cloud use are raising the value of direct, machine-readable emissions inputs. White space remains strongest in the SME and mid-market layer, where buyers want lower-cost tools built around Indian reporting needs and simpler accounting integrations. Indian service firms also remain important market makers because they influence platform selection during enterprise transformation and managed reporting engagements.

India Green IT Software Industry Leaders

Persefoni AI, Inc.

Wipro Limited

SAP SE

IBM Corporation

Watershed Technology Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Meta Platforms announced it would lease a 168 MW AI-enabled data center from Reliance Industries in Jamnagar, Gujarat, marking Meta's first built-to-suit data center in India. Simultaneously, Meta partnered with CleanMax and Fourth Partner Energy for nearly 1 GW of renewable energy across northern and southern India, substantially expanding the clean energy infrastructure that underpins green-certified IT operations in the country.

- June 2026: Tata Power Trading Company, Keppel Limited, and Tata Realty launched a cooling-as-a-service deployment at Intellion Park in Chennai using AI and machine learning optimization, targeting energy consumption reductions of over 20%. The initiative signals a new commercial model for IT infrastructure sustainability in India, where AI-driven energy management is packaged as a service to reduce both operational costs and Scope

- May 2026: SAP announced at SAP Sapphire that its new sustainability AI agents, including a Sustainability Regulatory Readiness Agent for automated materiality assessment and disclosure preparation, would be generally available by the end of 2026. The announcement extended SAP Green Ledger's carbon accounting capabilities into AI-driven compliance automation, directly relevant to Indian enterprises managing both BRSR and CSRD reporting obligations.

- May 2026: Persefoni AI launched the Persefoni Analytics Agent, an agentic AI tool embedded within its carbon accounting and sustainability reporting platform. The agent enables users to query emissions data via natural language prompts, replacing static dashboards and accelerating the path from data to disclosure-ready insights. Persefoni serves over 500 enterprise customers globally and has raised cumulative institutional funding of USD 179 million.

India Green IT Software Market Report Scope

The India green IT software market comprises software applications and services that enable organizations to reduce the environmental footprint of their IT infrastructure and digital operations while supporting sustainability and net-zero goals. These solutions provide capabilities such as carbon emissions tracking, ESG reporting, sustainability data aggregation, energy consumption monitoring, resource optimization, and decarbonization planning across enterprise IT environments, cloud infrastructure, and data centers.

The India Green IT Software Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and SMEs), End-User Industry (IT and Telecom, BFSI, Manufacturing, Energy and Utilities, Retail and E-Commerce, Government, Healthcare, Construction and Infrastructure, and Other End-user Industries), and Solution Type (Carbon Management and Accounting Software, ESG Reporting and Compliance Software, Sustainability Data Management Platforms, Decarbonization Planning Software, and Energy and Resource Optimization Software). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| SMEs |

| IT and Telecom |

| BFSI |

| Manufacturing |

| Energy and Utilities |

| Retail and E-Commerce |

| Government |

| Healthcare |

| Construction and Infrastructure |

| Other End-User Industries |

| Carbon Management and Accounting Software |

| ESG Reporting and Compliance Software |

| Sustainability Data Management Platforms |

| Decarbonization Planning Software |

| Energy and Resource Optimization Software |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| SMEs | |

| By End-User Industry | IT and Telecom |

| BFSI | |

| Manufacturing | |

| Energy and Utilities | |

| Retail and E-Commerce | |

| Government | |

| Healthcare | |

| Construction and Infrastructure | |

| Other End-User Industries | |

| By Solution Type | Carbon Management and Accounting Software |

| ESG Reporting and Compliance Software | |

| Sustainability Data Management Platforms | |

| Decarbonization Planning Software | |

| Energy and Resource Optimization Software |

Key Questions Answered in the Report

What is the size of the India green IT software market in 2026 and what is the outlook to 2031?

The India green IT software market stood at USD 0.71 billion in 2026 and is forecast to reach USD 2.22 billion by 2031 at a CAGR of 25.59% over 2026-2031.

Which offering category leads software demand in India?

Software led with 81.43% share in 2025 because enterprises preferred scalable platforms with stronger audit trails, repeatable workflows, and easier version control than one-time services.

Why is hybrid deployment gaining traction so quickly?

Hybrid is projected to grow at a 31.28% CAGR through 2031 because many large companies need to connect on-premises ERP and operating data with cloud-based emissions engines and reporting tools.

Which buyer group contributes the most revenue today?

Large enterprises held 74.91% share in 2025 because they faced stronger disclosure obligations, had broader supplier ecosystems, and had the budget to invest in enterprise-grade platforms.

Which end-user group is expanding the fastest?

Healthcare is projected to grow at a 30.15% CAGR through 2031 as hospitals and providers place greater weight on environmental performance, financing expectations, and structured reporting needs.

Which solution type remains the main entry point for buyers?

Carbon Management and Accounting Software held 33.48% share in 2025 because most companies still start with measurement, audit support, and disclosure readiness before moving into pathway planning and optimization.

Page last updated on: