South Korea Green IT Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

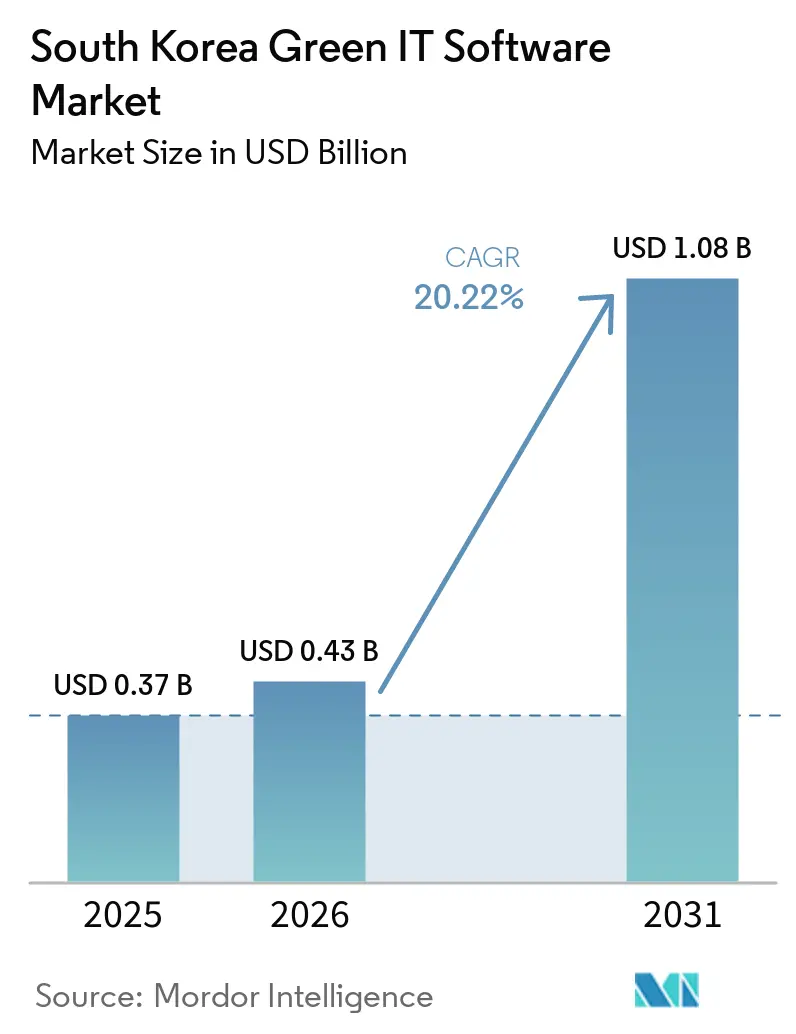

| Base Year Market Size (2025) | USD 0.37 Billion |

| Market Size (2026) | USD 0.43 Billion |

| Market Size (2031) | USD 1.08 Billion |

| Growth Rate (2026 - 2031) | 20.22% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Green IT Software Market Analysis by Mordor Intelligence

The South Korea green IT software market size is expected to increase from USD 0.37 billion in 2025 to USD 0.43 billion in 2026 and reach USD 1.08 billion by 2031, growing at a CAGR of 20.22% over 2026-2031. The South Korea green IT software market is moving into a more structured buying cycle because climate disclosure rules and carbon compliance are now closer to active implementation than they were in earlier planning rounds. Demand is also rising because large Korean business groups can extend one software decision across many affiliates, which shortens adoption timelines and concentrates spending into fewer procurement windows. Buyers are shifting toward platforms that combine carbon accounting, reporting, and data governance because disconnected tools make auditability and recurring reporting harder to manage. Competition is becoming more defined by local compliance depth, strong ERP connectivity, and automation features that reduce reporting effort across complex corporate structures. A clear expansion path remains in the supplier and mid-market base, where adoption is still uneven, but supply chain reporting requirements are starting to pull smaller companies into formal sustainability data systems.

Key Report Takeaways

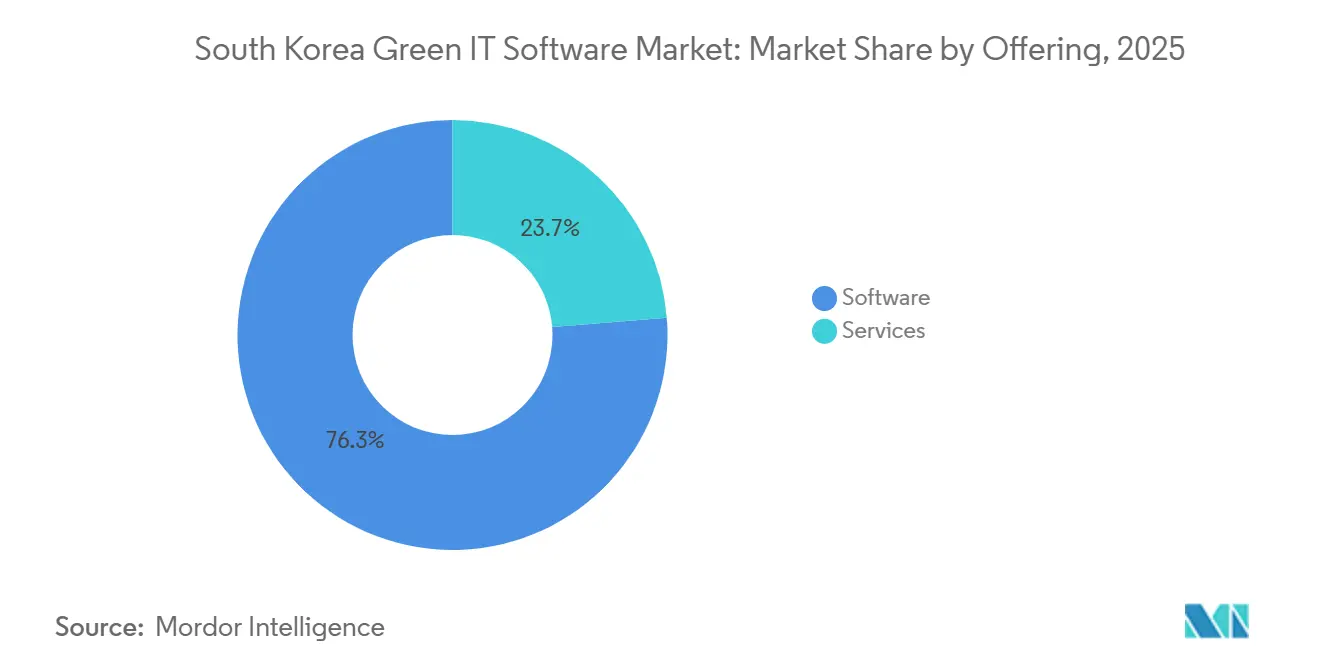

- By offering software with a 76.28% revenue share in South Korea green IT software market in 2025, highlighting a strategic shift toward platform deployment over traditional service-only models. The segment is further projected to grow at a robust CAGR of 24.11% through 2031.

- By deployment mode, cloud-based deployment accounted for a 62.71% revenue share in South Korea green IT software market and is projected to expand at a 23.23% CAGR through 2031.

- By organization size, large enterprises held 71.29% share in 2025, while SMEs are projected to expand at a 22.67% CAGR through 2031.

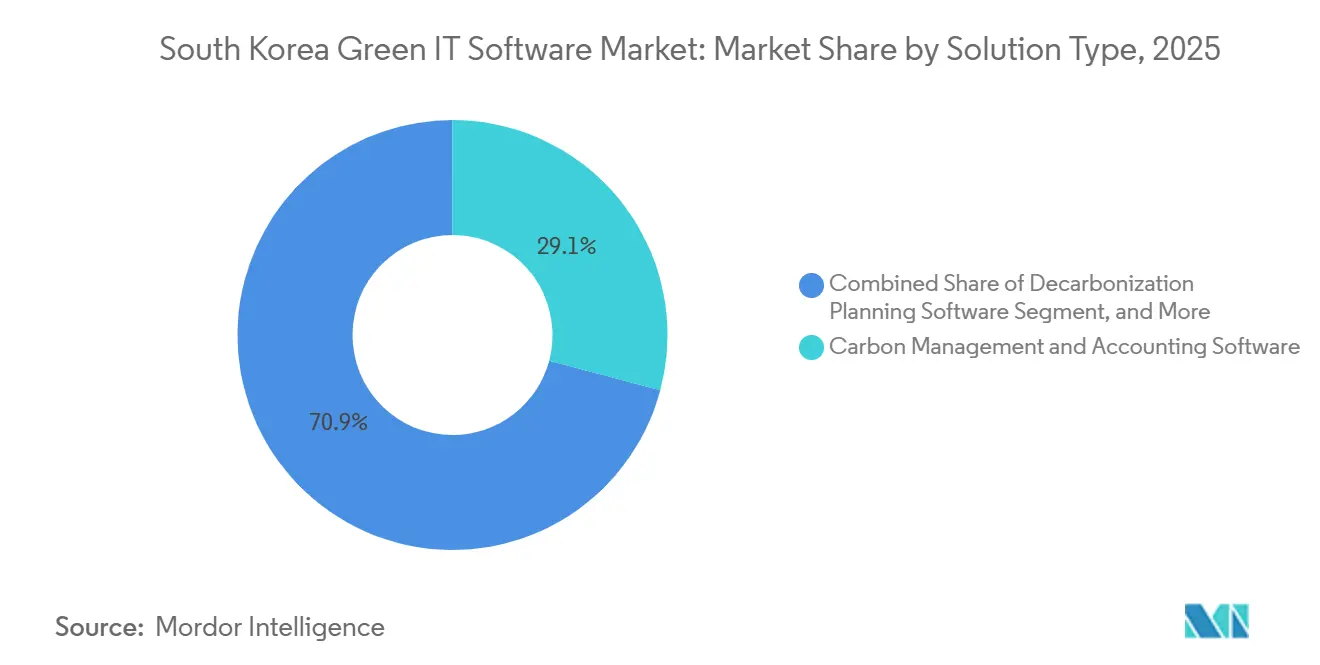

- By solution type, carbon management and accounting software accounted for 29.13% share in 2025, while sustainability data management platforms are projected to advance at a 22.14% CAGR through 2031.

- By end user industry, IT and telecommunications held 24.46% share in 2025, while manufacturing is projected to grow at a 22.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Green IT Software Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Mandatory Climate Disclosure Automation Across Listed Enterprises | +4.5% | National, with highest concentration among KOSPI-listed headquarters in the Seoul Capital Region | Short term (≤ 2 years) |

| K-ETS And K-Taxonomy Alignment Increasing Software Spend | +3.8% | Industrial clusters nationwide, with concentration in the Southern Industrial Belt | Medium term (2-4 years) |

| Energy Cost Reduction Pressure in Data Centers and Corporate IT | +3.1% | Seoul Capital Region and Gyeonggi corridor, with emerging relevance in Honam | Short term (≤ 2 years) |

| AI-Driven Optimization Of Workloads, Cooling, and Asset Utilization | +2.6% | National, with early gains in the Seoul Capital Region hyperscale corridor | Medium term (2-4 years) |

| Expansion of ESG Data Platforms Across Conglomerate Ecosystems | +2.1% | Seoul Capital Region and Southern Industrial Belt | Medium term (2-4 years) |

| Supplier-Level Carbon Data Requirements in Export-Oriented Value Chains | +1.8% | Southern Industrial Belt and semiconductor clusters in Gyeonggi | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory Climate Disclosure Automation Across Listed Enterprises

The South Korea green IT software market is gaining a firmer demand base because mandatory disclosure timelines are moving sustainability reporting into routine enterprise operations. The FSC published draft KSDS 1 and KSDS 2 on February 25, 2026, aligned with IFRS S1 and S2, for KOSPI-listed companies with consolidated assets above KRW 30 trillion, which is approximately USD 21 billion, from fiscal year 2027, with expansion to companies above KRW 10 trillion from fiscal year 2028.[1]Editorial Team, “Korean Regulator Consults on Sustainability Reporting Based on ISSB Standards,” IAS Plus, iasplus.com The ruling party also proposed accelerating the Scope 3 deadline to 2029, which would pull supplier data preparation forward and tighten implementation schedules across the broader corporate base. The draft structure also matters because the temporary safe harbor around smaller subsidiaries only applies at the start, so reporting perimeters are likely to widen after the first compliance cycle. That creates repeat platform work rather than one-time deployment, which supports recurring software demand in the South Korean green IT software market. It also explains why smaller suppliers are entering buying discussions earlier, because disclosure duties at large listed groups are already shaping data requirements across upstream vendor networks.

K-ETS And K-Taxonomy Alignment Increasing Software Spend

The South Korea green IT software market is also being pushed forward by a carbon compliance system that now requires tighter data quality and more consistent audit trails. Phase 4 of the K-ETS took effect from 2026 with a total emissions cap of 2.5373 billion tonnes CO2e, tighter industrial benchmarking, and expanded allocation rules across more sectors. The approved allocation plan also tightened the industrial benchmarking coefficient from the top 37% to the top 20% of performers, which makes approximated or manually reconciled reporting less practical than it was in Phase 3.[2]International Carbon Action Partnership, “Korea Approves Phase 4 K-ETS Allocation Plan for 2026-2030,” International Carbon Action Partnership, icapcarbonaction.com In parallel, the December 2024 K-Taxonomy revision expanded green activity coverage to 100 categories, and the Green Credit Management Guidelines linked that framework to lending classification decisions at financial institutions. Korea Credit Information Services then launched a K-Taxonomy Climate Finance Web Portal in May 2026, which gave banks a more structured workflow for climate finance review. These layers raise demand for carbon accounting and ESG reporting software because companies now need compatible records not only for regulators, but also for lenders, auditors, and financing counterparties.

Energy Cost Reduction Pressure In Data Centers And Corporate IT

Energy intensity in data centers and enterprise IT environments is creating a more operational reason to buy software, which broadens the South Korea green IT software market beyond compliance alone. The Ministry of Science and ICT issued the 2026 Sustainable Data Center Industry Development Support Program in April 2026, funding field testing and development of eco-friendly and high-efficiency equipment and software by Korean SMEs. Samsung SDS has already piloted immersion cooling at its Dongtan data center and projected energy savings of 30% to 50% relative to conventional air cooling, which shows that infrastructure efficiency is becoming measurable and software-linked rather than conceptual. As energy costs, uptime requirements, and carbon oversight converge, dashboards, optimization tools, and workload monitoring systems move closer to the center of normal IT operations. This matters because spending is easier to justify when software affects both compliance readiness and facility economics in the same reporting cycle. It also helps explain why the South Korea green IT software market is beginning to diffuse beyond headquarters-led purchasing into infrastructure-heavy sites that need continuous energy and cooling visibility.

AI-Driven Optimization of Workloads, Cooling, and Asset Utilization

AI is becoming a practical feature set inside the South Korea green IT software market because it improves both reporting speed and operational decision quality. Korean vendors are using AI to identify anomalies in energy use, detect reporting inconsistencies, and support faster review of sustainability disclosures. SK AX launched Xgentic Wire Compliance in May 2026, and the service was trained on more than 3,400 court rulings and regulatory decisions to detect greenwashing and legal risk in real time through the Click ESG platform. SAP also announced new sustainability AI agents in May 2026, with broader availability expected by the end of 2026, embedding carbon tracking and automation deeper into ERP and financial management workflows. This changes software buying behavior because the value case now reaches finance, sustainability, and operations teams at the same time. In the South Korea green IT software market, that shift can shorten internal approval cycles because AI-enabled systems are being treated less as optional reporting tools and more as infrastructure for recurring enterprise decisions.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented Emissions and Energy Data Across Legacy Systems | -3.2% | National, with greater severity among mid-tier manufacturers outside the Seoul Capital Region | Short term (≤ 2 years) |

| Weak Standardization of Scope 3 and Supplier Data Quality | -2.5% | Southern Industrial Belt and semiconductor and automotive supply chains in Gyeonggi | Medium term (2-4 years) |

| Integration Complexity With Existing ERP, EAM, and Cloud Stacks | -1.8% | National, concentrated among large enterprises with mixed IT estates | Short term (≤ 2 years) |

| Budget Prioritization Toward Compliance Over Full Sustainability Digitization | -1.3% | National, with highest severity in SMEs and mid-market KOSPI companies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Emissions and Energy Data Across Legacy Systems

The largest near-term barrier in the South Korea green IT software market is not weak demand, but the difficulty of assembling usable data from disconnected enterprise systems. Many Korean companies still manage utility records, factory-level readings, and ERP entries in separate environments that were not built for sustainability-grade auditability. Even large vendors have had to expand their systems in phases, and Samsung SDS reported that the second phase of its SGMS extended coverage to Scope 3 emissions and overseas subsidiaries in 2025, which shows that full reporting perimeter buildout takes time even at the top end of the market. For mid-tier manufacturers with fewer internal IT resources, that same problem can delay deployment, raise connector costs, and slow the move from pilot work to production reporting. This constraint is especially relevant outside the Seoul Capital Region, where many industrial sites carry older operational technology stacks and more limited standardization across plants. As a result, vendors that provide pre-built connectors into Korean ERP, manufacturing, and emissions workflows are likely to gain a practical edge during the current adoption cycle.

Weak Standardization of Scope 3 and Supplier Data Quality

Scope 3 reporting remains one of the harder commercial problems in the South Korea green IT software market because supplier data quality is still inconsistent across many export-linked industries. This matters most in sectors such as semiconductors, batteries, steel, petrochemicals, and automotive supply chains, where buyers need comparable upstream information before they can trust end-to-end platform outputs. The pressure is increasing because the proposal to accelerate Scope 3 timelines would shorten the window for suppliers to build structured carbon data processes. Operational examples are beginning to emerge, including blockchain-based product carbon data exchange in automotive supply chains and LRQA-verified CBAM MRV platforms for Korean manufacturers, but those examples still represent early-stage standardization rather than broad market readiness. Until collection methods and exchange standards become more consistent across supplier tiers, some buyers will continue limiting investment to the compliance modules they need first. That keeps full-suite adoption slower than the top-line demand conditions might otherwise suggest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Leads as Platforms Replace Point Solutions

Software held 76.28% of the segment in 2025, which confirms that the South Korea green IT software market is already centered on platforms rather than standalone advisory support. That share also shows that enterprise buyers now expect recurring functionality, audit trails, and system integration from their sustainability budgets instead of treating the category as a temporary compliance project. In the South Korea green IT software industry, this pattern reflects the practical limits of service-led delivery when reporting cycles become more frequent and standards keep evolving. Platform ownership matters because disclosures, emissions calculations, and review histories must stay available across reporting periods and across affiliates within large business groups. Software spending is also easier to scale across many subsidiaries, which makes it a better fit for chaebol procurement structures than high-touch service models.

Software platforms are anticipated to achieve a CAGR of 24.11% through 2031, representing the strongest growth trajectory within South Korea's green IT software market. The leading software cohort is being strengthened by vendors that combine carbon accounting, reporting, and workflow controls into a single environment. Samsung SDS expanded its SGMS in 2025 to include Scope 3 emissions and overseas subsidiaries, and it also obtained CPS certification for external reliability assurance, which supports the shift toward certified and auditable platform delivery. [3]Samsung SDS, “Sustainability Report 2025,” Samsung SDS, samsungsds.com This is important because buyers in the South Korea green IT software market are no longer comparing only features, they are also comparing whether systems can stand up to external review and repeat submissions. Services still retain strategic value because many deployments require ERP integration, plant-level data mapping, and internal workflow redesign before software can operate at full scale. That keeps implementation and advisory work relevant, especially in large industrial organizations with mixed legacy systems. Even so, services increasingly sit next to software rather than replacing it, because buyers need a permanent system of record after implementation work is completed.

By Deployment Mode: Cloud Gains Ground as Standards Change Faster

Cloud-based deployment is projected to expand at a 23.23% CAGR through 2031, making it the fastest-moving setup in the South Korea green IT software market. The input also indicates that cloud-based deployment was the leading mode, which suggests that the category is advancing on both scale and growth at the same time. In the South Korea green IT software industry, that combination is being supported by the need for frequent updates as compliance rules and reporting templates continue to evolve. Hosted systems let vendors push revisions faster, which matters when companies cannot afford delays between regulatory change and platform readiness. Cloud environments also help companies collect data from distributed offices, plants, and suppliers into a shared reporting structure without the same infrastructure burden as full on-premise builds.

In 2025, cloud-based deployment accounted for a substantial 62.71% share of South Korea's green IT software market. The model is especially attractive for SMEs because subscription pricing lowers the initial cost of entry and makes budgeting easier across shorter planning cycles. It also supports faster onboarding when companies need an initial compliance layer before expanding into optimization or decarbonization modules. On-premise deployment still matters in industries with strict data control preferences or heavy dependence on sensitive industrial systems, including semiconductor and defense-adjacent operations. Hybrid setups are therefore gaining relevance because many large Korean groups are trying to connect newer subsidiaries and older industrial assets within one reporting framework. This gradual shift helps the South Korea green IT software market because it widens the buyer pool without forcing every company into the same architecture at the same pace. Over time, the flexibility of cloud and hybrid models should support broader adoption as compliance expectations spread further down the corporate and supplier base.

By Organization Size: Large Enterprises Anchor Revenue While SMEs Drive Expansion

Large enterprises held 71.29% of the South Korea green IT software market share in 2025, which shows how strongly current spending is concentrated among major regulated corporations. The same figure means large enterprises accounted for 71.29% of the South Korea green IT software market size in 2025, reflecting the scale advantage that comes from enterprise-wide platform deployment. This concentration is structurally consistent with Korea's corporate landscape because a holding company decision at a major group can cascade across many subsidiaries and business units. Large companies also face the earliest reporting pressure, which gives them a stronger reason to commit budget before smaller firms do. Their internal systems are more complex, but they also have wider capacity to absorb multi-phase implementation work and longer procurement programs.

SMEs are projected to grow at a 22.67% CAGR through 2031, which makes them the most important forward-expansion group in the South Korea green IT software market. Their growth is being pulled by supply-chain reporting requirements rather than only by direct regulation, which means adoption starts before formal obligations fully reach them. SK AX stated that Click ESG has been deployed across approximately 3,400 domestic companies, which points to a subscription model that is already reaching a large smaller-enterprise base. SME demand should also benefit from green financing linkages and easier cloud deployment, both of which lower the threshold for first-time adoption. Even so, many smaller companies still prioritize only the minimum compliance layer because internal staffing and data maturity remain limited. That means vendor success in this part of the South Korea green IT software market will depend on simpler onboarding, modular pricing, and stronger connector libraries rather than only on broad product breadth.

By Solution Type: Carbon Accounting Holds the Core While Data Platforms Scale Faster

Carbon management and accounting software led with a 29.13% share in 2025, which places it at the center of current spending in the South Korea green IT software market. That lead reflects the immediate pressure created by K-ETS Phase 4, where emissions records now carry stronger financial and compliance consequences than in earlier periods. The Phase 4 allocation plan tightened industrial benchmarking and extended more demanding treatment across additional sectors, which makes verified data handling more important than approximate reporting. As a result, carbon accounting tools are often the first purchase because they connect the regulatory requirement to a measurable internal control problem. ESG reporting and compliance software follows closely because companies that must disclose also need workflow controls, review histories, and repeatable output formats.

Sustainability data management platforms are projected to advance at a 22.14% CAGR through 2031, making them the fastest-growing solution type in the South Korea green IT software market. That growth shows a clear move away from separate reporting and accounting tools toward a shared data layer that can support several frameworks at once. Buyers increasingly want a central environment that can feed KSDS, GRI, TCFD, CBAM, and internal management use cases without rebuilding the same information several times. The South Korea green IT software industry is therefore moving toward broader platform orchestration, where carbon accounting stays essential but no longer operates as an isolated function. Specialized tools for decarbonization planning and energy optimization remain at an earlier stage, yet they stand to benefit once companies complete their first compliance-focused buildout. Over the medium term, this sequence should expand average deal scope because firms that secure reliable data foundations are more likely to add reduction planning and performance modules later.

By End User Industry: IT and Telecom Leads Today While Manufacturing Builds Momentum

IT and telecommunications held 24.46% share in 2025, which made it the largest end user segment in the South Korea green IT software market. This lead reflects the heavy presence of data centers, cloud infrastructure, and digital service providers that have both direct energy exposure and strong reporting pressure. These buyers often see sustainability software as an operating tool as much as a disclosure tool because efficiency, cooling, and power visibility affect daily economics. The segment also benefits from stronger internal digital maturity, which makes deployment faster than in some older industrial settings. In practical terms, that means software vendors can often move beyond basic reporting sooner and position additional optimization functions within the same account.

Manufacturing is projected to grow at a 22.32% CAGR through 2031, which gives it the strongest forward momentum in the South Korea green IT software market. That acceleration comes from the overlap of domestic K-ETS obligations and export-facing carbon requirements in overseas value chains. Manufacturers need better plant-level emissions data, product-level records, and supplier coordination, which expands the use case from compliance reporting into production-linked traceability. This part of the South Korea green IT software industry is also important because it broadens demand beyond headquarters functions into industrial sites, procurement teams, and cross-border customer requirements. BFSI is gaining traction as taxonomy-linked lending and disclosure practices become more structured, while public sector demand adds stability through institution-led digitalization programs. Other sectors such as healthcare, retail, e-commerce, construction, and utilities remain smaller, but they are gradually moving into the addressable base as reporting expectations spread into a wider set of business activities.

Geography Analysis

The Seoul Capital Region is the largest hub in South Korea’s Green IT Software market. With Seoul, Incheon, and Gyeonggi hosting the headquarters of the country’s leading business conglomerates, the initial wave of compliance-driven procurement is naturally concentrated in this area. The region also accommodates key regulatory institutions and the Korean operations of major global enterprise software providers, reinforcing its position as the primary commercial center for significant deals. Buying decisions are often made at the group or headquarters level before being implemented across affiliates and operational sites, further strengthening the region's leadership.

The Seoul Capital Region also features a dense network of data centers and digital infrastructure operators, driving demand for reporting, energy visibility, and optimization software. This creates a dual demand dynamic: one focused on disclosure readiness and the other on infrastructure efficiency. Decisions by major enterprises such as Samsung, SK, LG, and Hyundai significantly influence their networks of subsidiaries and suppliers, making the region a concentrated hub for adoption. While growth is not limited to the capital area, its role as the decision-making center ensures it will remain the leading cluster even as adoption expands into more industrial and renewable-focused regions.

The Southern Industrial Belt, which includes Busan, Ulsan, and Gyeongnam, is emerging as a key growth area due to its large industrial complexes in petrochemicals, shipbuilding, steel, and automotive sectors. High emissions intensity and export-oriented operations drive demand for carbon accounting, CBAM-compliant workflows, and supplier data management across manufacturing-heavy industries. Other regions, such as Chungcheong and Honam, remain smaller at present but represent the next phase of geographic expansion as semiconductor, battery, and renewable-linked infrastructure activities increase. This shift reduces reliance on headquarters-driven demand and integrates more site-level operational users into the software ecosystem, diversifying adoption across South Korea.

Competitive Landscape

The South Korea green IT software market is moderately fragmented, with competition spread across domestic IT conglomerates, global software majors, and specialized climate technology providers. Domestic firms such as Samsung SDS Co., Ltd., LG CNS Co., Ltd., and SK Inc. C&C hold a natural advantage because they understand local reporting rules, legacy system requirements, and the procurement logic of major Korean business groups. Their position is strengthened by longstanding IT outsourcing and enterprise integration relationships, which make them difficult to displace once sustainability modules are attached to broader digital contracts. In the South Korea green IT software market, that local fit often matters as much as product breadth because compliance software must connect cleanly with Korean reporting practices and enterprise data environments. This is why domestic leaders continue to compete effectively even when global vendors bring larger international portfolios.

Samsung SDS Co., Ltd. strengthened its position by expanding SGMS in 2025 and obtaining CPS certification, which gave its offering a stronger third-party reliability signal. SK Inc. C&C also widened its strategic relevance through Click ESG adoption and AI-based compliance screening, which helped move its proposition beyond basic reporting support. LG CNS Co., Ltd. reinforced its cloud-led delivery posture through a high-profile Google Cloud partnership milestone in 2026, which supports more scalable enterprise deployment models. These moves show that domestic competition is not limited to local customization, it is also expanding through certification, AI capability, and ecosystem partnerships.

Global enterprise software suppliers such as SAP SE, Microsoft Corporation, IBM Corporation, Salesforce, and ServiceNow compete from a different angle in the South Korea green IT software market. Their value lies in internationally aligned compliance modules, broader workflow integration, and stronger support for multinationals that want one system across several jurisdictions. SAP’s sustainability AI agents and finance-linked carbon functionality are especially relevant because they connect emissions management to mainstream ERP and financial controls.[4]Editorial Team, “Autonomous Enterprise, New Sustainability AI Agents,” SAP News Center, news.sap.com Specialist players such as Glassdome and Thingspire are adding pressure at the focused-use-case end by offering export-compliance and disclosure tools that can be easier to adopt than full-suite platforms. That creates a competitive middle ground where buyers compare not only product depth, but also deployment speed, certification credibility, pricing flexibility, and supplier-network usability. The South Korea green IT software market should therefore remain competitive rather than consolidate quickly, especially as SME demand grows and buyers continue choosing between full platforms and narrower problem-solving tools.

South Korea Green IT Software Industry Leaders

Samsung SDS Co., Ltd.

LG CNS Co., Ltd.

SK Inc. C&C

Naver Cloud Corporation

Kakao Enterprise Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Samsung SDS announced a strategic AI, cloud, and security partnership with Google Cloud at Google Cloud Next 2026. At the same event, LG CNS was named Google Cloud Partner of the Year 2026 for Korea, the only Korean company to receive the designation, recognizing its Premier Partner status, AI capabilities, and data analytics contributions to enterprise customers.

- May 2026: SK AX launched "Xgentic Wire Compliance," an AI service trained on over 3,400 court rulings and regulatory decisions, capable of detecting greenwashing and legal risk in corporate sustainability disclosures in real time. The tool was integrated into the Click ESG platform, currently deployed across approximately 3,400 Korean companies, enabling AI-powered ESG compliance adherence within a single platform.

- May 2026: Korea Credit Information Services launched the K-Taxonomy Climate Finance Web Portal, providing financial institutions with step-by-step K-Taxonomy compliance assessment workflows for green lending decisions. The portal was initially extended to the banking sector, with planned expansion to insurance and securities firms as the system scales.

- April 2026: The Ministry of Science and ICT issued a consolidated call for the 2026 Sustainable Data Center Industry Development Support Program, funding development and field testing of eco-friendly, high-efficiency data center equipment and software by Korean SMEs, positioning sustainable data center technology as a nationally subsidized industrial competitiveness priority.

South Korea Green IT Software Market Report Scope

In South Korea, Green IT Software refers to environmentally sustainable computing solutions designed to minimize energy consumption, enhance the efficiency of IT resources, and contribute to the country's carbon neutrality objective by 2050. These solutions are closely aligned with South Korea's Green New Deal, a series of government-supported digital sustainability initiatives, as well as the rapid development of renewable energy-powered data centers and platforms for optimizing AI workloads.

The South Korea Green IT Software Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Solution Type (Carbon Management and Accounting Software, ESG Reporting and Compliance Software, Sustainability Data Management Platforms, Decarbonization Planning Software, and Energy and Resource Optimization Software), End-User Industry (IT and Telecommunications, Manufacturing, Banking, Financial Services, and Insurance (BFSI), Government and Public Sector, Energy and Utilities, Healthcare, Retail and E-Commerce, Construction and Infrastructure, and Other End User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Carbon Management and Accounting Software |

| ESG Reporting and Compliance Software |

| Sustainability Data Management Platforms |

| Decarbonization Planning Software |

| Energy and Resource Optimization Software |

| IT and Telecommunications |

| Manufacturing |

| Banking, Financial Services, and Insurance (BFSI) |

| Government and Public Sector |

| Energy and Utilities |

| Healthcare |

| Retail and E-Commerce |

| Construction and Infrastructure |

| Other End User Industries |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premise | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Solution Type | Carbon Management and Accounting Software |

| ESG Reporting and Compliance Software | |

| Sustainability Data Management Platforms | |

| Decarbonization Planning Software | |

| Energy and Resource Optimization Software | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Banking, Financial Services, and Insurance (BFSI) | |

| Government and Public Sector | |

| Energy and Utilities | |

| Healthcare | |

| Retail and E-Commerce | |

| Construction and Infrastructure | |

| Other End User Industries |

Key Questions Answered in the Report

What is the current and forecast value of the South Korea green IT software market?

The South Korea green IT software market was valued at USD 0.37 billion in 2025, reached at USD 0.43 billion in 2026, and is forecast to reach USD 1.08 billion by 2031 at a 20.22% CAGR from 2026 to 2031.

What is driving software spending in South Korea for green IT applications?

The strongest demand drivers are mandatory climate disclosure preparation, tighter K-ETS requirements, taxonomy-linked lending processes, and rising pressure to manage energy use in data centers and enterprise IT.

Which deployment model is growing the fastest in South Korea green IT software?

Cloud-based deployment is projected to grow at a 37.29% CAGR through 2031 because it supports faster updates, easier onboarding, and centralized reporting across distributed sites.

Which customer group contributes the most revenue and which one is expanding fastest?

Large enterprises held 71.29% share in 2025 because large listed groups face the earliest compliance pressure, while SMEs are growing fastest at a 22.67% CAGR as supply-chain data requirements spread downstream.

Which solution type leads spending and what is gaining momentum next?

Carbon management and accounting software led with 29.13% share in 2025 because emissions reporting sits at the core of current compliance needs, while sustainability data management platforms are rising quickly at a 22.14% CAGR.

Page last updated on: