Singapore Green IT Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

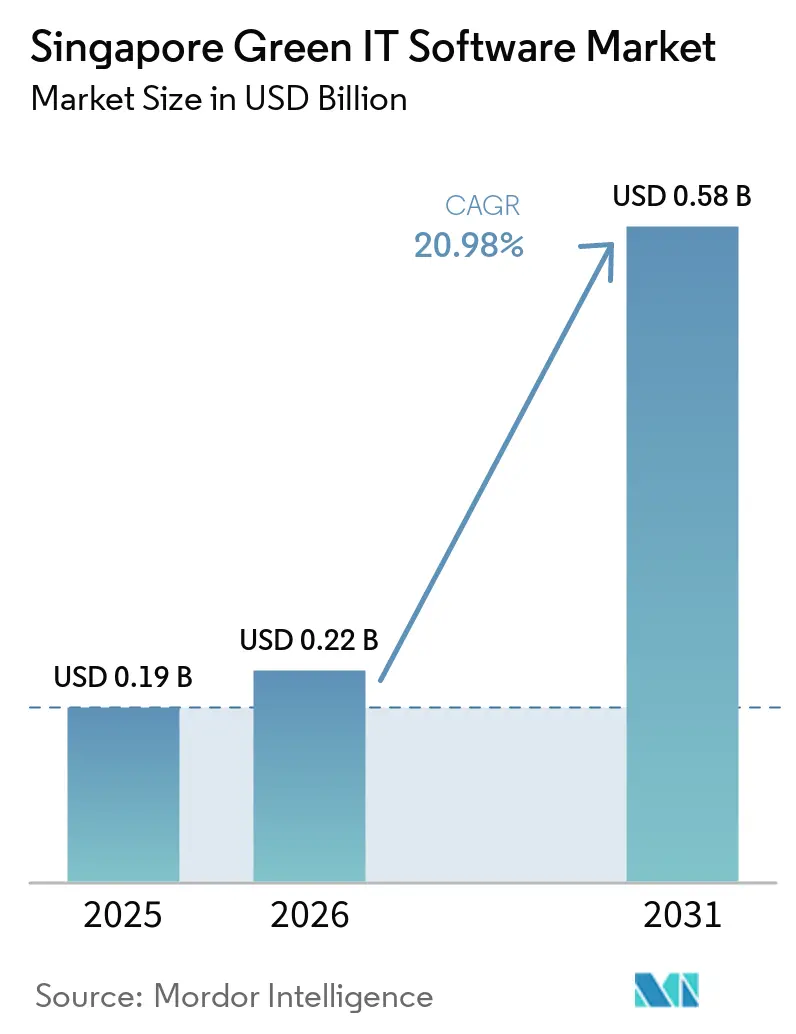

| Base Year Market Size (2025) | USD 0.19 Billion |

| Market Size (2026) | USD 0.22 Billion |

| Market Size (2031) | USD 0.58 Billion |

| Growth Rate (2026 - 2031) | 20.98% CAGR |

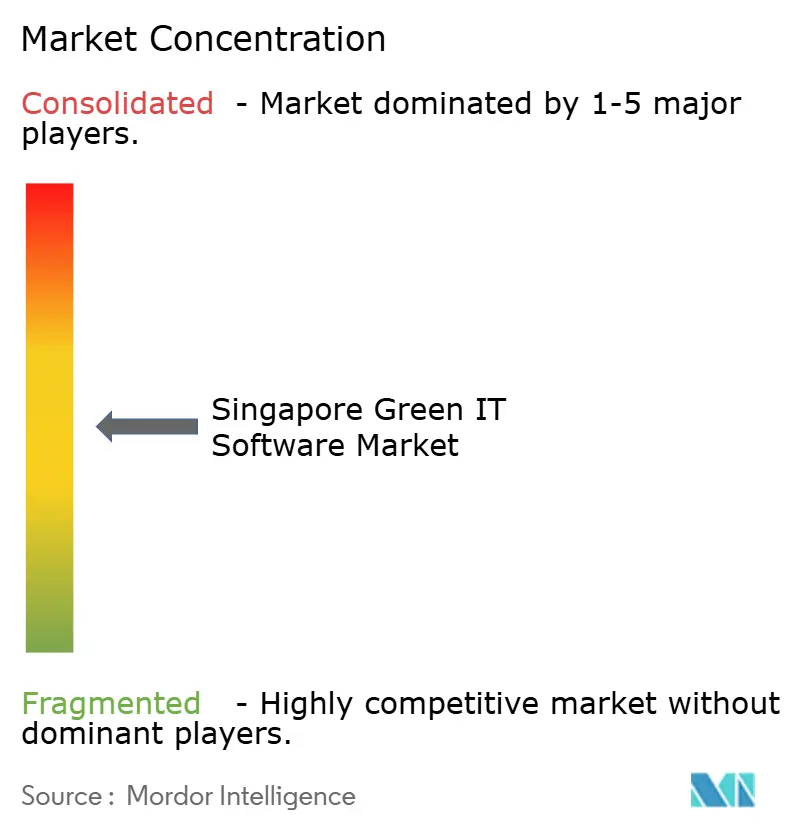

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Green IT Software Market Analysis by Mordor Intelligence

The Singapore green IT software market size was valued at USD 0.19 billion in 2025 and is forecast to reach USD 0.58 billion by 2031, growing at a CAGR of 20.98% during 2026-2031. Growth is being shaped first by Singapore’s phased climate disclosure rules, which have turned carbon reporting tools from a discretionary purchase into a required operating system for many listed companies and their supply chains. The market is also benefiting from public digital infrastructure, including practical green software guidance, cloud carbon calculators, and Singapore-specific emission factors that make deployment easier and reporting more consistent. Demand remains concentrated in larger regulated buyers because they face tighter audit, governance, and framework mapping needs, while smaller firms are still earlier in adoption despite targeted enablement efforts. Hybrid technology strategies are becoming more important as enterprises try to balance data control, compliance, and scalable analytics across business units and jurisdictions. The main limits on adoption continue to be legacy integration challenges, measurement inconsistency across frameworks, and a shortage of specialized implementation talent, all of which extend deployment timelines even when software demand is strong.

Key Report Takeaways

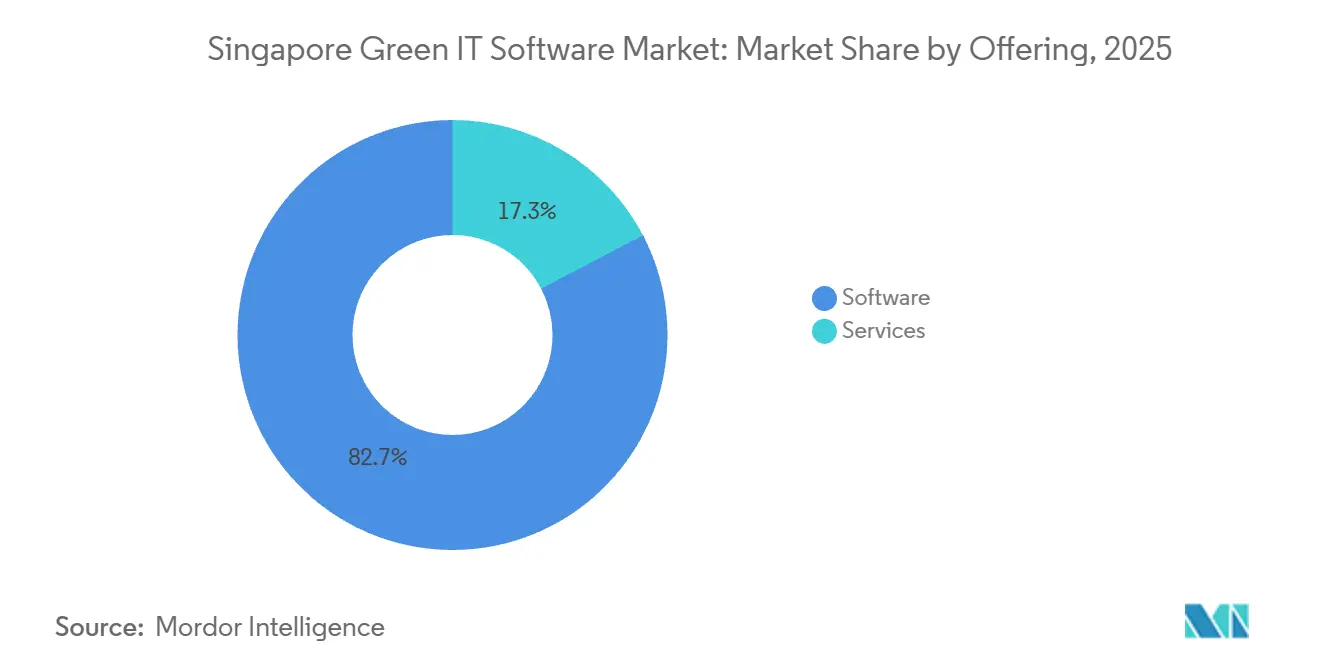

- By offering, software held 82.67% of the Singapore green IT software market share in 2025, while services are projected to expand at a 24.86% CAGR through 2031.

- By deployment mode, cloud accounted for 72.94% of the market in 2025, while hybrid is expected to record the highest CAGR at 26.18% through 2031.

- By organization size, large enterprises represented 76.28% of the Singapore green IT software market share in 2025, while SMEs are projected to grow at a 23.74% CAGR through 2031.

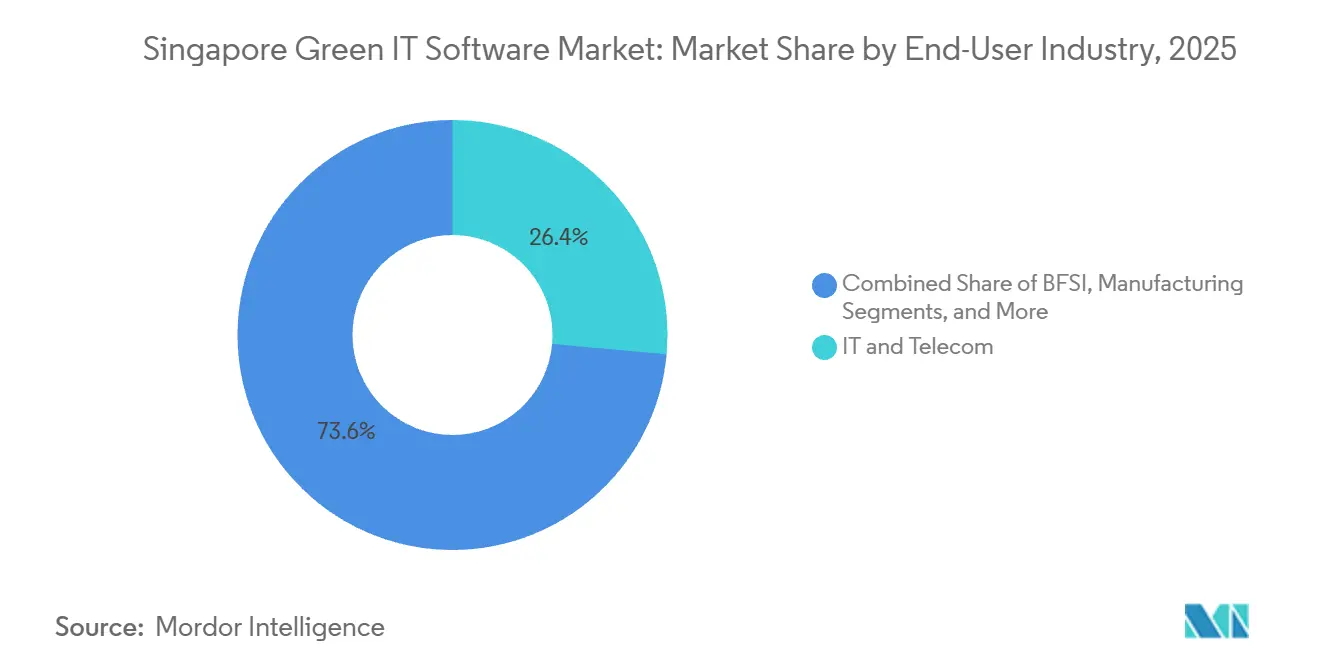

- By end-user industry, IT and Telecom led with a 26.43% share in 2025, while healthcare is projected to advance at a 24.92% CAGR through 2031.

- By solution type, carbon management and accounting software accounted for 34.72% of the market in 2025, while decarbonization planning software is projected to expand at a 26.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Green IT Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Corporate Sustainability Reporting Requirements | +4.8% | National, with early demand concentrated in Singapore’s central business district and MNC-heavy industrial clusters | Short term (≤ 2 years) |

| Public-Private Demand for Carbon-Aware IT Operations | +3.9% | National, with spill-over to Asia-Pacific regional headquarters using Singapore as proof-of-concept for multi-country rollouts | Short term (≤ 2 years) |

| Cloud Migration and Virtualization Efficiency Gains | +3.2% | National, driven by Singapore’s data center ecosystem, with spill-over to Malaysia and Indonesia via regional hyperscaler nodes | Medium term (2-4 years) |

| AI-Driven Energy Optimization for Software and Infrastructure | +2.8% | National, with secondary impact across Asia-Pacific through Singapore-based R&D pilots and vendor headquarters | Medium term (2-4 years) |

| Green Procurement Standards in Enterprise and Public Sector Buying | +2.1% | National, concentrated in government-linked companies and publicly listed enterprises | Medium term (2-4 years) |

| Singapore as a Regional Compliance Hub for Asia-Pacific Headquarters | +1.6% | National, with multiplied effect across Asia-Pacific as MNC regional offices use Singapore deployments to standardize regional reporting | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Corporate Sustainability Reporting Requirements

The Singapore green IT software market is being pushed forward by a reporting framework that has removed optionality for many enterprise buyers. From FY2025, all SGX-listed companies had to report Scope 1 and Scope 2 emissions in line with IFRS S2, and STI constituents must report Scope 3 emissions from FY2026, which widened software demand into supplier data collection and verification workflows.[1]Accounting and Corporate Regulatory Authority, “Sustainability Reporting and Assurance Requirements,” ACRA, acra.gov.sg The same roadmap extends ISSB-aligned obligations to large non-listed companies from FY2030, which creates a rolling compliance pipeline rather than a one-time buying cycle. This structure matters because it shifts green reporting tools from periodic reporting aids into core systems for continuous data capture, control, and audit readiness. It also expands procurement beyond directly regulated entities, since larger companies increasingly need suppliers to submit comparable carbon information in formats that can feed enterprise reporting systems. The result is a demand pattern in which the Singapore green IT software market grows not only from listed issuers, but also from the wider commercial network that supports them.

Public-Private Demand for Carbon-Aware IT Operations

The Singapore green IT software market is also benefiting from an unusual alignment between public guidance and enterprise operating needs. IMDA stated that Singapore became the first government organization to join the Green Software Foundation, and that the Software Carbon Intensity specification it contributed to has been published as an ISO standard, which gives buyers a more neutral basis for discussing software-related emissions. IMDA’s green software trials, run with 13 companies since May 2024, showed that participating enterprises achieved at least 20% reductions in carbon emissions, energy usage, and costs, which gave enterprises a clearer business case for operational software changes. A 2025 pulse survey cited by Singapore’s Ministry of Digital Development and Information found that 81% of non-SMEs had adopted at least 1 digital sustainability solution, which indicates that realized demand has already moved beyond pilot use cases in the regulated enterprise base. These signals matter because they connect software adoption to energy savings, cost discipline, and governance rather than to disclosure alone. That combination gives the Singapore green IT software market a broader operating rationale than many other sustainability software categories.

Cloud Migration and Virtualization Efficiency Gains

The Singapore green IT software market is drawing support from cloud migration because shared infrastructure and centralized telemetry make energy and emissions monitoring easier to scale. IMDA and the National University of Singapore Energy Studies Institute developed Singapore-specific cloud emission factors and released a cloud carbon calculator, which gave enterprise teams a more localized way to compare cloud and on-premises configurations. IMDA also launched SS715:2025, a Singapore standard that targets at least 30% lower energy use for data center IT equipment, which strengthens the case for software that can track, benchmark, and report equipment efficiency. Under IMDA’s second Data Center Call for Application, new capacity must be at least 50% powered by eligible green energy pathways, which means cloud environments in Singapore are moving toward structurally lower emissions intensity over time. As a result, cloud deployment is not only a technical architecture decision; it also becomes part of the emissions reporting logic that enterprises need their software to capture. This has reinforced demand for platforms that can absorb operational data at scale and translate it into reporting-ready sustainability outputs.

AI-Driven Energy Optimization for Software and Infrastructure

The Singapore green IT software market is increasingly shaped by AI, as the same technologies that raise compute intensity are also used to manage it more precisely. SAP announced in May 2026 that its Footprint Optimization Agent would reduce emissions scenario simulation time from 1 day to 20 minutes and cut the variance between industry-average ESG estimates and actual values by 30 to 40 percentage points. Watershed launched AI agents in April 2026 that reduced the time to actionable sustainability data by 80%, with 1 enterprise completing a data-cleaning project in 20 minutes that had previously taken 5 hours. IMDA’s Practical Green Software Guide identified right-sizing AI models as 1 of 3 core practices that helped enterprises achieve early carbon and cost reductions, thereby placing model governance directly within software purchasing criteria. This matters because vendors are no longer competing only on dashboard breadth or framework libraries; they are increasingly competing on the speed and efficiency with which their systems can produce reliable decision support. That shift gives the Singapore green IT software market an additional performance layer that goes beyond compliance functionality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity With Legacy Enterprise Systems | -2.1% | National, concentrated in BFSI, manufacturing, and government-linked enterprises with multi-decade ERP architectures | Short term (≤ 2 years) |

| Limited Standardization in Green Software Measurement Methodologies | -1.6% | National, with compounding effect for Singapore MNC regional offices that must reconcile multiple national disclosure frameworks | Medium term (2-4 years) |

| High Cost of Data Collection, Auditability, and Continuous Reporting | -1.3% | National, with disproportionate impact on SMEs and mid-market enterprises without dedicated sustainability IT budgets | Medium term (2-4 years) |

| Shortage of Specialized Green Software and Sustainability Analytics Talent | -1.0% | National, with secondary impact across APAC as Singapore-based talent pools are competed for by regional MNC offices | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity with Legacy Enterprise Systems

The Singapore green IT software market faces a persistent execution barrier in enterprises that still operate older ERP, database, and reporting architectures. The draft’s cited 2025 IMDA survey found that 38% of non-adopting enterprises pointed to limited knowledge, while practical implementation friction also continued to raise project cost and extend deployment schedules. This challenge is especially relevant where emissions data must be extracted from finance, operations, procurement, and facility systems that were not originally designed for sustainability reporting. IMDA’s Digital Technologies for Sustainability Playbook tried to reduce this burden by mapping digital tools to enterprise sustainability use cases, which should help buyers frame integration steps more clearly. Even so, buyers still face a significant change-management task because live operating data, framework logic, and assurance expectations all have to be connected before the software can deliver full value. That keeps implementation risk high even when the enterprise's intent to buy is already established.

Limited Standardization in Green Software Measurement Methodologies

The Singapore green IT software market also faces a methodological constraint because enterprises often need to reconcile multiple sustainability frameworks simultaneously. The draft highlighted differences across the GHG Protocol, ISSB standards, the EU framework, and SGX-related reporting needs, which forces many multi-framework buyers to maintain more than 1 calculation logic inside their reporting stack. Singapore has started to narrow this problem in ICT-related reporting through the IMDA and NUS ESI emission factors released in 2026, which created a more localized basis for cloud and ICT emissions calculations. IMDA also noted Singapore’s role in the Green Software Foundation and the Software Carbon Intensity framework, but adoption still remains uneven because the specification is not applied uniformly across vendors. This inconsistency makes product comparison harder for enterprise buyers who want a clear and defensible way to evaluate software-related emissions performance. It also lengthens evaluation cycles because buyers often need additional validation before committing to a platform standard.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Anchors Revenue While Services Rise with Compliance Complexity

Software held 82.67% of the Singapore green IT software market share in 2025, indicating that buyers strongly preferred platforms that could support recurring data collection, calculation, and disclosure workflows. In the Singapore green IT software market, the weight at the software layer reflected the practical need for systems that can map data across IFRS S1, IFRS S2, SGX-related requirements, and supplier engagement processes without relying on disconnected manual tools. The segment’s position also reflects buying behavior in regulated enterprises, where version control, audit trails, and repeatable reporting logic carry more weight than one-time advisory work. Software demand has therefore been tied closely to the need for structured outputs, operating discipline, and continuous reporting readiness, especially after mandatory disclosures began to move through the listed company base. This made platform capability the first decision point in many enterprise buying cycles, with service support added around the software rather than replacing it.

Services are projected to grow at a 24.86% CAGR through 2031, which shows that implementation work is expanding as enterprise reporting moves into more complex areas such as Scope 3 and internal controls. The Singapore green IT software industry is seeing services growth because many buyers still need configuration support, training, regulatory interpretation, and workflow redesign before platforms can function as intended. Salesforce stated in May 2026 that it was establishing Data and AI Centers of Excellence with Accenture, PwC Singapore, and Huron in Singapore, which reflects the bundled delivery model increasingly used around enterprise platforms. In practice, service demand is also renewed by framework changes, data expansion, and assurance preparation, which means the service layer has recurring value even after the first deployment. That dynamic should keep the offering mix centered on software revenue while steadily increasing the role of attached service work across large-account implementations.

By Deployment Mode: Cloud Leads the Installed Base While Hybrid Expands Fastest

Cloud accounted for 72.94% of the market in 2025, and that position reflected the ease with which centralized cloud environments can support multi-entity reporting, scalable data ingestion, and ongoing software updates. The Singapore green IT software market size for cloud-linked deployment remained strongest because IMDA’s carbon calculator and localized emission factors gave procurement teams a clearer way to compare cloud architectures with on-premises setups using Singapore-specific assumptions. The strength of Singapore’s data center ecosystem also supported cloud adoption, because software buyers could align operational flexibility with a more maturing sustainability infrastructure around energy sourcing and equipment efficiency. These conditions reduced friction for enterprises that wanted sustainability reporting tools to work across subsidiaries, business units, and regional operations from a shared technology base. As a result, cloud was not only the default deployment choice for many buyers, it also became the easiest format for vendors to standardize and scale.

Hybrid is projected to expand at a 26.18% CAGR through 2031, which reflects the need to balance scalability with tighter internal controls over sensitive data. The Singapore green IT software market is seeing stronger hybrid demand in regulated accounts because some enterprises want analytics and collaboration in the cloud while keeping selected datasets or governance layers within controlled environments. This pattern is consistent with Singapore’s broader compliance posture, where data architecture decisions often need to satisfy both operational and risk management concerns rather than cost alone. On-premises systems, therefore, remain relevant in agencies and highly controlled institutions, but they are increasingly being supplemented instead of serving as complete standalone environments. Hybrid deployment has gained ground because it offers a practical transition path for organizations that cannot move reporting operations fully into the cloud in a single step.

By Organization Size: Large Enterprises Set the Baseline While SME Adoption Builds from a Lower Base

Large enterprises represented 76.28% of the market in 2025, which reflected their stronger exposure to mandatory disclosures, higher audit expectations, and broader supply-chain reporting responsibilities. In the Singapore green IT software market, these buyers set the early compliance baseline because they had to build systems that could capture emissions data at scale and produce repeatable outputs suitable for internal review and external assurance. Their position was reinforced by the fact that they act as anchor companies in supply chains, which means their software choices often influence the tools, templates, and data expectations imposed on smaller vendors. This gave large enterprises a central role in shaping actual demand realization, not only through direct buying power but also through their influence over downstream reporting practices. That pattern helps explain why market adoption has been strongest in organizations with more complex governance structures and stronger regulatory exposure.

SMEs are projected to grow at a 23.74% CAGR through 2031, although they started from a much lower adoption base than large enterprises. The Singapore green IT software market still showed under-penetration in this group, with SME adoption at only 27% in 2025, which left meaningful room for lower-cost and easier-to-deploy solutions. Gprnt announced in May 2025 what it described as the world’s first nationwide utility for automated sustainability metric generation, backed by USD 4.62 million in seed funding from Ant International and MUFG Bank, and aimed at simplifying disclosure for smaller firms.[2]Gprnt, “Gprnt Announces World’s First Nationwide Utility for Sustainability Reporting,” Gprnt, gprnt.ai The same launch was closely linked to the Green 100 structure described in the draft, where large enterprises were expected to activate suppliers through simplified metric disclosure, which should make SME participation more structured over time. This combination of lower starting penetration and more practical enablement tools explains why growth is likely to remain strong even though SMEs still trail larger companies in actual installed software depth.

By End-User Industry: IT and Telecom Leads Current Spending, While Healthcare Records the Fastest Growth

IT and Telecom accounted for 26.43% of the market in 2025, making it the largest end-user industry in current spending terms. The Singapore green IT software market size within this user base remained elevated because the sector combines heavy operational energy use with a relatively mature internal understanding of digital measurement, cloud operations, and software-led optimization. IMDA’s green software trials and practical guidance were closely tied to this ecosystem, which helped position ICT participants as both users of sustainability software and contributors to the standards and practices shaping it. That dual role gave IT and Telecom a natural lead in adoption because it had both the technical capacity and the business incentive to operationalize green software earlier than many other industries. The installed base built in this segment also supports adjacent market growth, since practices tested in ICT environments often inform broader enterprise deployment strategies.

Healthcare is projected to grow at a 24.92% CAGR through 2031, which places it as the fastest-growing end-user segment in the Singapore green IT software market. The rise of this segment reflects the growing relevance of formal sustainability metrics in financing, operations, and enterprise governance, which requires software that can capture more than basic emissions figures alone. The segment also benefits from the wider expansion of sustainability-linked performance management, where reporting systems must connect environmental data to commercial and compliance processes. BFSI remains an important buyer group because financial institutions and portfolio-linked reporting needs continue to support demand for more advanced calculation and control features. Manufacturing, energy and utilities, government, construction and infrastructure, and retail and e-commerce also remain active demand pools, especially where enterprise buyers need to track operational intensity and supplier-linked disclosures more consistently over time.

By Solution Type: Carbon Accounting Leads Current Demand, While Planning Tools Gain Speed

Carbon Management and Accounting Software accounted for 34.72% of the market in 2025, and that leadership reflected the immediate need to quantify Scope 1, Scope 2, and Scope 3 emissions before enterprises could do anything more advanced. The Singapore green IT software market share at this solution layer stayed the highest because measurement is the starting point for disclosure, assurance preparation, target setting, and procurement-led supplier engagement. IMDA stated in 2026 that new ICT-specific factors were added to the Singapore Emission Factors Registry, which widened the empirical basis available for software-generated carbon calculations. That mattered because enterprises need more localized and more defensible inputs when emissions outputs will be reviewed by management, investors, and assurance providers. Carbon accounting, therefore, remained the entry point for most deployments, even when buyers expected their platforms to expand later into planning, optimization, or supplier collaboration.

Decarbonization Planning Software is projected to grow at a 26.85% CAGR through 2031, which shows that enterprises are moving from baseline measurement into action sequencing and investment prioritization. The Singapore green IT software industry is starting to place more value on scenario modeling tools because buyers that already built initial emissions baselines now need to compare pathways, assess tradeoffs, and identify the most practical reduction steps. EcoVadis stated in May 2026 that its partnership with Workiva would connect supplier carbon data directly into disclosure workflows, while its March 2026 partnership with Watershed focused on closing the Scope 3 data gap through better links between supplier data and decarbonization planning. Energy and Resource Optimization Software is also benefiting from SS715:2025, because clearer efficiency benchmarks improve the commercial case for tools that connect compliance, energy monitoring, and cost reduction. Together, these shifts show a market moving beyond simple carbon counting toward software that can support operational and capital decisions with greater precision.

Geography Analysis

The Singapore green IT software market is a single-country study, so the geography analysis centers on Singapore’s position relative to other APAC and ASEAN markets rather than on domestic subregional splits. The Singapore green IT software market was valued at USD 0.19 billion in 2025 and is forecast to reach USD 0.58 billion by 2031 at a 20.98% CAGR, which reflects a stronger adoption trajectory than many nearby markets that are still earlier in structured climate disclosure rollout. Singapore’s regulatory base remains a major differentiator because mandatory Scope 1 and Scope 2 reporting for all SGX-listed companies started from FY2025, and Scope 3 reporting for STI constituents follows from FY2026. That timing gives Singapore a more immediate compliance trigger for enterprise software deployment than several Southeast Asian peers. It also creates a stronger demand for tools that can handle supplier data, framework mapping, and audit-ready workflows from the outset.

The Singapore green IT software market also benefits from the city-state’s role as a regional operating center. Singapore Economic Development Board stated that the country hosts around 4,600 multinational corporation regional offices, which creates a channel through which software deployed for local compliance can also become a template for broader Asia-Pacific reporting programs.[3]Singapore Economic Development Board, “Latest in Singapore’s Sustainability Scene, Round-Up From January to March 2026,” EDB, edb.gov.sg Public infrastructure adds to this advantage because the Singapore Emission Factors Registry, localized ICT emission factors, SS715:2025, and the Green Data Center Roadmap reduce the setup burden for both buyers and vendors. These assets lower the practical cost of deployment because companies do not need to build every reporting input from scratch. In effect, geography is supporting demand through policy, data infrastructure, and regional business concentration at the same time.

The Singapore green IT software market is also positioned to benefit from wider regional alignment with mandatory sustainability reporting after 2026. IMDA’s Digital Technologies for Sustainability Playbook noted that Japan’s standards take effect in 2027, China requires sustainability reports from more than 300 listed entities by 2026, and Australia implements mandatory Scope 3 reporting in 2026, which raises the value of platforms that can support multi-jurisdiction reporting from a Singapore base. This matters because it reinforces software development and enterprise deployment from both the demand side and the innovation side. As regional frameworks become stricter, Singapore is likely to remain the reference point from which many Asia-Pacific green software rollouts are designed and managed.

Competitive Landscape

The Singapore green IT software market remains moderately concentrated in its top tier, with global platform vendors such as SAP, Microsoft, IBM, and Salesforce benefiting from existing enterprise relationships, while specialist providers compete through product depth and faster workflow design. The Singapore green IT software market still supports a meaningful specialist tail because buyers do not all want the same balance of ERP integration, supplier collaboration, AI automation, and decarbonization planning. This creates a split between broad enterprise suites that can cross-sell into established accounts and focused vendors that gain traction through narrower problem-solving. Large accounts often favor vendors that can integrate with finance, procurement, and cloud environments already in place, while smaller or newer adopters may prefer simpler, more targeted tools. That structure supports competition on both breadth and usability rather than on price alone.

SAP strengthened its position in May 2026 by announcing sustainability AI agents, including the Footprint Optimization Agent, which reduces scenario simulation time from 1 day to 20 minutes and narrows variance between estimates and actual values.[4]SAP SE, “Autonomous Enterprise, New Sustainability AI Agents,” SAP News Center, sap.com Salesforce had already committed USD 1 billion to Singapore over 5 years in March 2025, which reinforced its local infrastructure and delivery capacity for data-intensive enterprise applications that can also support sustainability workflows. EcoVadis expanded its ecosystem role in March and May 2026 through partnerships with Watershed and Workiva, both designed to connect supplier carbon data more directly into reporting and planning environments. These moves show that competition is increasingly about workflow connectivity and speed rather than only about the number of metrics a platform can display. Vendors that shorten data preparation, improve traceability, and support clearer decisions are likely to gain the strongest traction in enterprise accounts.

The Singapore green IT software market also has room for newer challengers, especially where incumbents are less flexible on cost, implementation complexity, or local process design. Gprnt’s May 2025 launch showed how SME-focused automation can open a lower-cost route to sustainability reporting that large enterprise platforms had not fully addressed. Persefoni added to this competitive pressure in May 2026 when it launched the Persefoni Analytics Agent, and its October 2025 partnership with Diligent strengthened its reach into institutional reporting environments. Watershed’s April 2026 AI launch added another example of how workflow speed is becoming a competitive differentiator in the Singapore green IT software market. Taken together, the field remains competitive, but the vendors best placed in Singapore are those that combine enterprise trust, localized reporting logic, and demonstrable efficiency gains inside day-to-day operating workflows.

Singapore Green IT Software Industry Leaders

SAP SE

Microsoft Corporation

Salesforce, Inc.

IBM Corporation

Workiva Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SAP announced that new sustainability AI agents, including the Footprint Optimization Agent, Sustainability Regulatory Readiness Agent, and Packaging Compliance Agent, would be generally available by the end of 2026. The Footprint Optimization Agent reduces the time required to simulate Scope 1, 2, and 3 emissions scenarios from approximately 1 day to 20 minutes and addresses a 30-to-40 percentage-point variance typically observed between industry-average ESG estimates and actual values.

- May 2026: EcoVadis announced a strategic partnership with Workiva to connect primary supplier carbon data directly into Workiva's disclosure platform, enabling mutual customers to move from spend-based Scope 3 estimation to granular, audit-ready primary supplier data. The partnership expanded EcoVadis's Carbon Data Network, which also includes Sweep, Normative, Watershed, and Carbmee, creating an interconnected Scope 3 data ecosystem that positions EcoVadis as the supplier-facing data layer feeding multiple accounting and reporting platforms simultaneously.

- May 2026: Persefoni AI launched the Persefoni Analytics Agent, an agentic AI tool enabling enterprises to interrogate emissions data through natural language queries without exiting the Persefoni platform. The launch followed the October 2025 strategic partnership with Diligent and accelerated Persefoni's positioning as an AI-first carbon management platform for complex institutional reporting requirements.

- April 2026: Watershed launched new AI agents, including data cleaning and analysis agents that reduced time to actionable sustainability data by 80%. The launch also included a new Sustainability AI Fellowship program to expand the pipeline of practitioners trained on AI-driven sustainability workflows.

Singapore Green IT Software Market Report Scope

The Singapore Green IT Software Market comprises software platforms and related services that help organizations measure, manage, optimize, and reduce the environmental impact of their information technology operations and digital infrastructure. These solutions enable enterprises to track carbon emissions, monitor energy consumption, automate ESG and sustainability reporting, manage sustainability data, optimize cloud and data center efficiency, and support decarbonization initiatives across IT environments. The market includes carbon management and accounting software, ESG reporting and compliance solutions, sustainability data management platforms, decarbonization planning tools, and energy and resource optimization software deployed by enterprises, financial institutions, government agencies, telecommunications providers, and data center operators across Singapore.

The Singapore Green IT Software Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and SMEs), End-User Industry (IT and Telecom, BFSI, Manufacturing, Energy and Utilities, Retail and E-Commerce, Government, Healthcare, Construction and Infrastructure, and Other End-user Industries), Solution Type (Carbon Management and Accounting Software, ESG Reporting and Compliance Software, Sustainability Data Management Platforms, Decarbonization Planning Software, and Energy and Resource Optimization Software). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| SMEs |

| IT and Telecom |

| BFSI |

| Manufacturing |

| Energy and Utilities |

| Retail and E-Commerce |

| Government |

| Healthcare |

| Construction and Infrastructure |

| Other End-User Industries |

| Carbon Management and Accounting Software |

| ESG Reporting and Compliance Software |

| Sustainability Data Management Platforms |

| Decarbonization Planning Software |

| Energy and Resource Optimization Software |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| SMEs | |

| By End-User Industry | IT and Telecom |

| BFSI | |

| Manufacturing | |

| Energy and Utilities | |

| Retail and E-Commerce | |

| Government | |

| Healthcare | |

| Construction and Infrastructure | |

| Other End-User Industries | |

| By Solution Type | Carbon Management and Accounting Software |

| ESG Reporting and Compliance Software | |

| Sustainability Data Management Platforms | |

| Decarbonization Planning Software | |

| Energy and Resource Optimization Software |

Key Questions Answered in the Report

What is the current and forecast value of the Singapore green IT software space?

It was valued at USD 0.19 billion in 2025 and is forecast to reach USD 0.58 billion by 2031 at a CAGR of 20.98% during 2026-2031.

What is driving software demand in Singapore most strongly?

Mandatory climate disclosure rules, supplier data requirements, and practical public tools such as ICT emission factors and cloud carbon calculators are driving adoption.

Which deployment model is leading adoption in Singapore?

Cloud led with 72.94% of the market in 2025 because it supports scalable data ingestion, easier updates, and wider enterprise reporting coverage.

Which customer group is generating the most demand today?

Large enterprises accounted for 76.28% of the market in 2025 because they face the highest compliance, audit, and supply-chain reporting obligations.

Which end-user segment is growing the fastest?

Healthcare is projected to grow at a 24.92% CAGR through 2031, reflecting stronger use of sustainability-linked metrics and wider reporting expectations.

Which software category is expanding the fastest?

Decarbonization Planning Software is expected to grow at a 26.85% CAGR through 2031 as enterprises move from emissions measurement into pathway modeling and investment planning.

Page last updated on: