Asia-Pacific Vehicle-Embedded Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

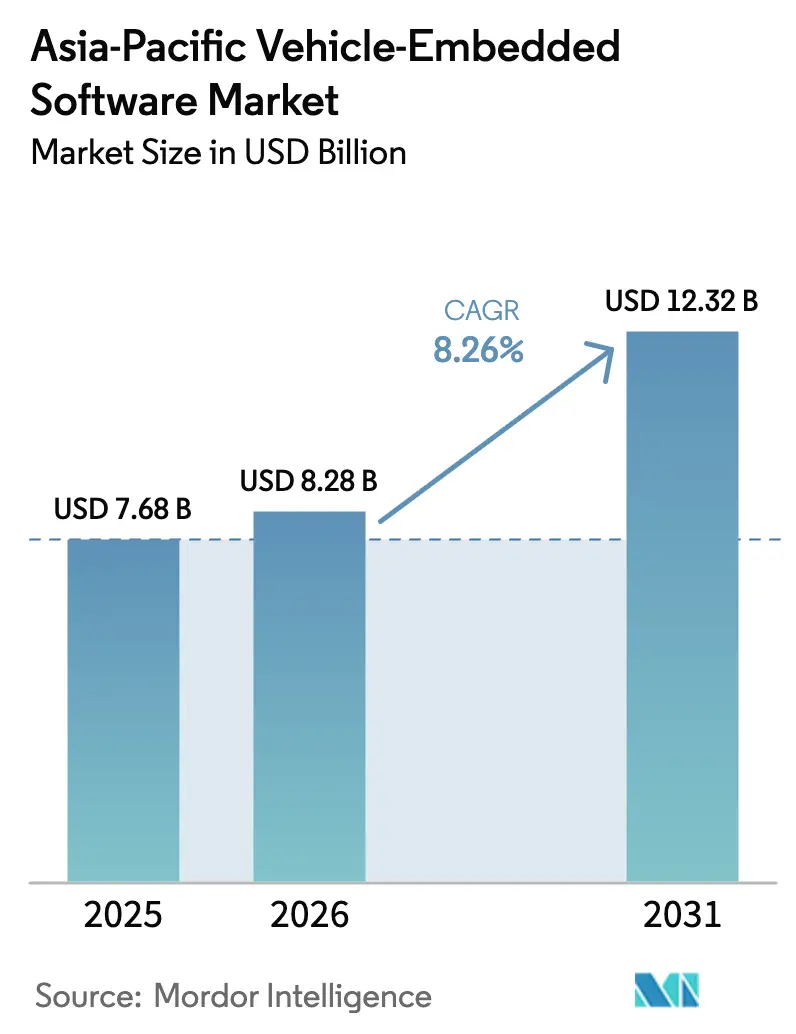

| Base Year Market Size (2025) | USD 7.68 Billion |

| Market Size (2026) | USD 8.28 Billion |

| Market Size (2031) | USD 12.32 Billion |

| Growth Rate (2026 - 2031) | 8.26% CAGR |

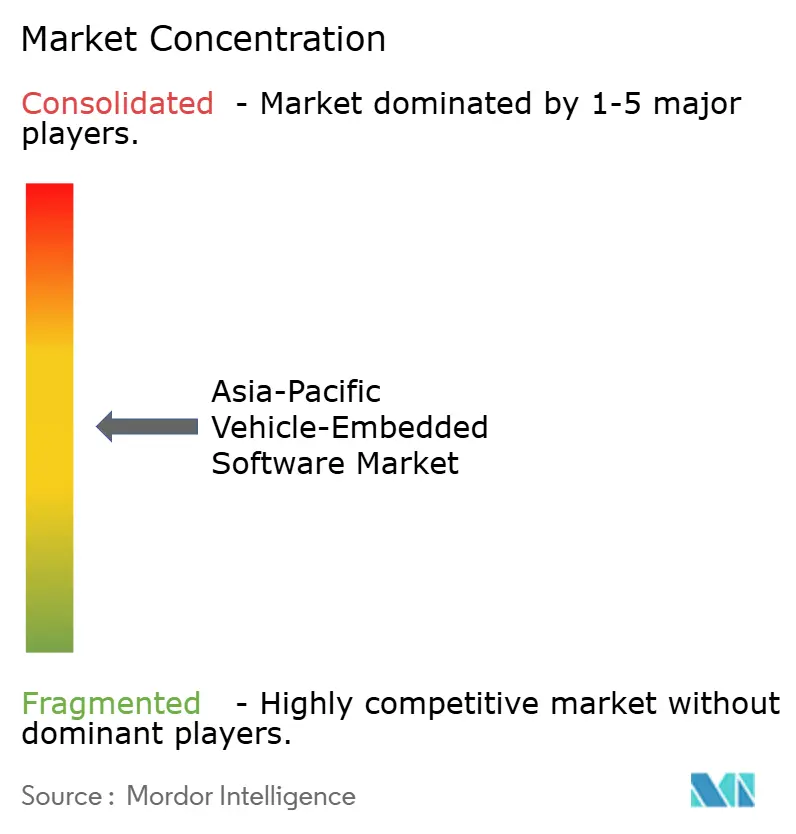

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Vehicle-Embedded Software Market Analysis by Mordor Intelligence

The Asia-Pacific vehicle-embedded software market size is expected to grow from USD 7.68 billion in 2025 to USD 8.28 billion in 2026 and is forecast to reach USD 12.32 billion by 2031 at 8.26% CAGR over 2026-2031. Pervasive electrification, mandatory advanced driver assistance functions, and the rapid pivot toward centralized compute platforms are expanding software spend per vehicle far faster than hardware costs. New cybersecurity mandates such as China’s GB 44495-2024 and Japan’s revised Road Transport Vehicle Act are accelerating the migration from distributed electronic control units to zonal and domain architectures that rely on scalable middleware. Open-source AUTOSAR Adaptive stacks and Linux-based operating systems are lowering entry barriers for regional suppliers, while over-the-air update ecosystems are unlocking post-sale revenue streams for original equipment manufacturers. Competitive intensity is rising as Chinese software houses, Indian engineering service providers, and global tier-1s race to deliver validated code bases that can pass ISO 26262 audits on compressed timelines within the Asia-Pacific vehicle-embedded software market.

Key Report Takeaways

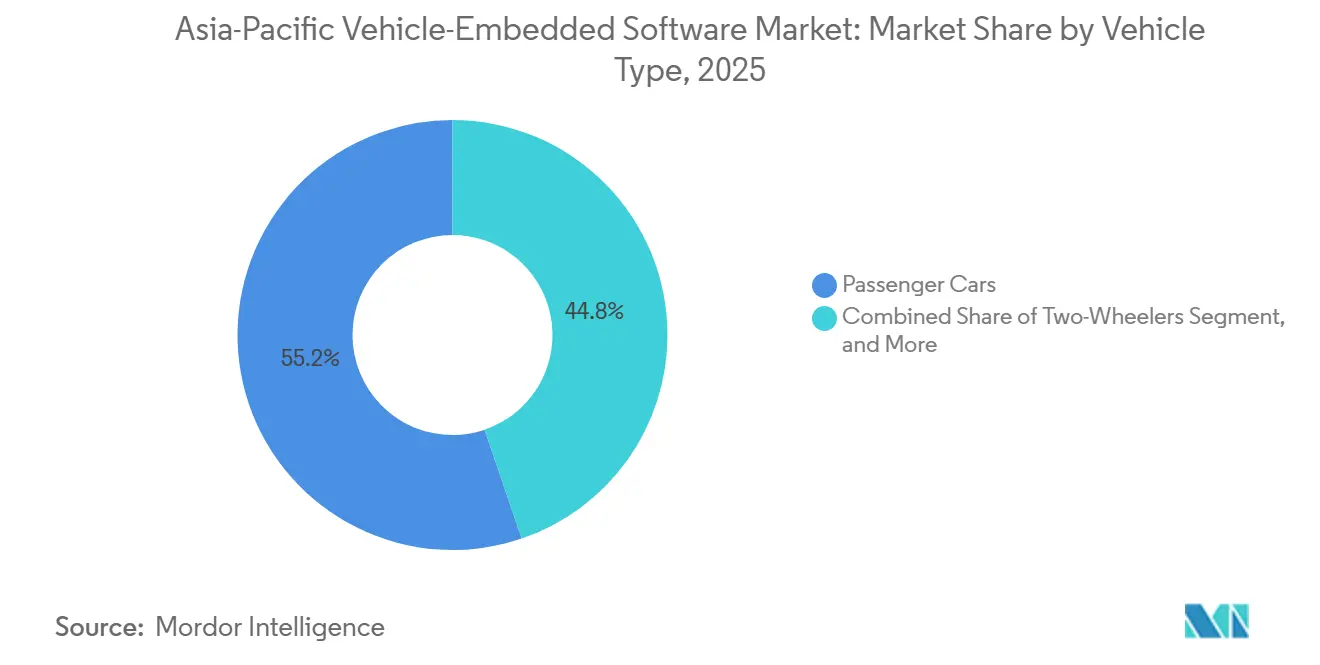

- By vehicle type, passenger cars accounted for 55.21% of the Asia-Pacific vehicle-embedded software market in 2025, whereas two-wheelers are advancing at a 9.23% CAGR over 2026-2031.

- By software type, application software accounted for 38.43% of the Asia-Pacific vehicle-embedded software market in 2025, but middleware is set to grow at a 9.56% CAGR through 2031.

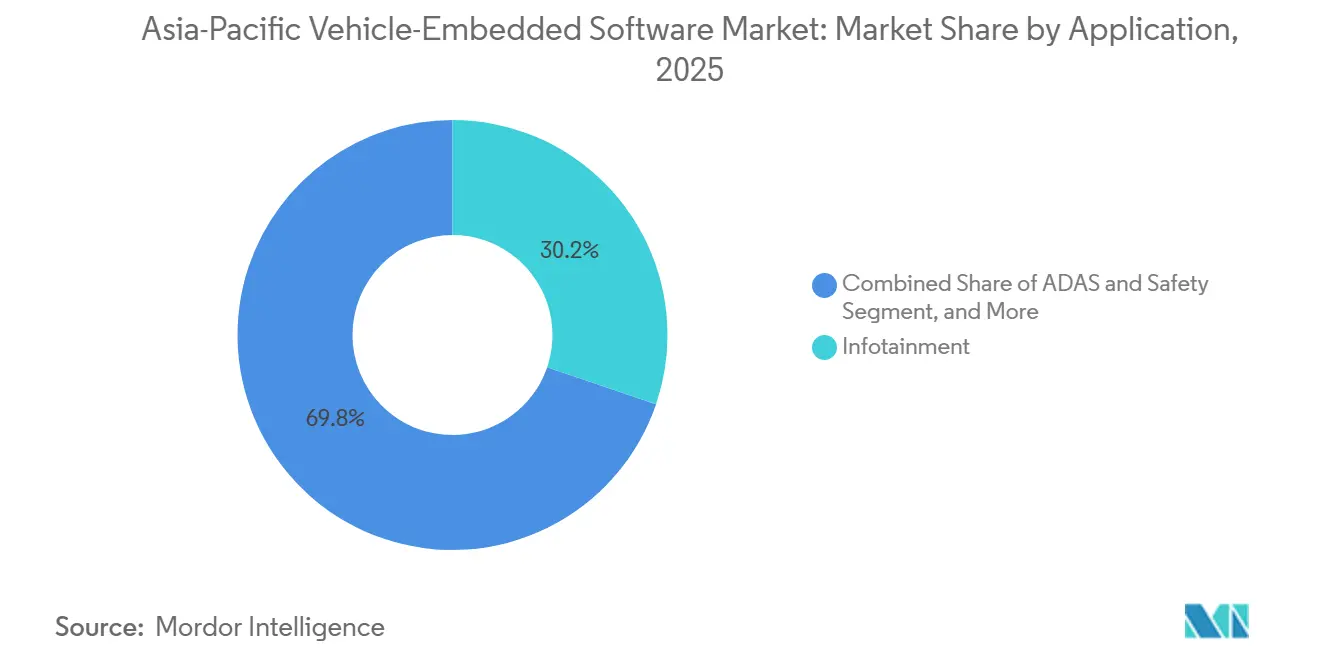

- By application, infotainment accounted for 30.21% of the Asia-Pacific vehicle-embedded software market in 2025, and ADAS and safety software are growing at a 9.78% CAGR between 2026 and 2031.

- By propulsion type, battery electric vehicles led with 43.56% of the Asia-Pacific vehicle-embedded software market share in 2025, while fuel cell electric vehicles are projected to expand at a 9.46% CAGR through 2031.

- By country, China represented 31.64% share of the Asia-Pacific vehicle-embedded software market size in 2025, whereas India is on track to record a 9.87% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Vehicle-Embedded Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Electrification of Passenger Cars | +2.1% | China, India, Japan, South Korea | Medium term (2-4 years) |

| Mandatory Advanced Driver Assistance Systems in China and Japan | +1.8% | China, Japan, with spillover to South Korea and ASEAN | Short term (≤ 2 years) |

| Over-the-Air Update Ecosystems Scaling Across OEMs | +1.5% | Global, with early adoption in China, Japan, South Korea | Medium term (2-4 years) |

| Open-Source AUTOSAR Adoption by Tier-1s | +1.2% | Global, concentrated in Japan, India, China | Long term (≥ 4 years) |

| Emerging Software-Defined Vehicle Architectures | +1.4% | China, Japan, South Korea, India | Medium term (2-4 years) |

| AI-Centric Embedded Platforms for Autonomous Shuttles | +0.9% | China, Japan, Singapore, with pilots in Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Electrification of Passenger Cars

Battery electric vehicle deliveries in China surpassed 9.5 million units in 2025, accounting for 38% of passenger-car sales and driving demand for software-managed battery management systems.[1]China Association of Automobile Manufacturers, “2025 Annual Production And Sales Statistics,” caam.org.cn Indian manufacturers embed real-time operating systems in sub-USD 1,500 scooters to regulate lithium iron phosphate packs and deliver predictive range functions. Japan’s April 2025 efficiency rules require software-validated power-train optimization during type approval, pulling tier-1s into joint algorithm development with semiconductor partners.[2]Ministry of Land, Infrastructure, Transport and Tourism, “Road Transport Vehicle Act Amendments For ADAS,” mlit.go.jp Each premium electric sedan now ships with more than 300 million lines of code, triple the load of a conventional model, magnifying middleware revenue opportunities.[3]Society of Automotive Engineers, “Software Content In Modern Vehicles,” sae.org

Mandatory Advanced Driver Assistance Systems in China and Japan

China’s automatic emergency braking and lane-keeping mandate effective January 2026 covers roughly 25 million new vehicles a year. Japan amended its Road Transport Vehicle Act in March 2025 to extend adaptive cruise control to trucks over 3.5 tons, widening ADAS reach into commercial fleets. Renesas shipped over 2 million R-Car V4H chips to Toyota in 2025, supporting consolidation of ADAS and infotainment loads on one compute domain. Continental’s CAEdge platform reaches 15-millisecond detection latency by offloading neural-net preprocessing to dedicated accelerators. Functional-safety validation at ASIL-D continues to add up to 18 months to release cycles, driving tighter OEM-supplier collaboration across the region.

Over-The-Air Update Ecosystems Scaling Across OEMs

Volkswagen China’s centralized electrical architecture pushed delta-compressed updates under 50 megabytes to 1.2 million connected cars within 72 hours in January 2026. Hyundai convened 47 suppliers in Seoul to harmonize OTA protocols and cut platform fragmentation. NIO’s Banyan 2.0 platform pairs redundant 5G telematics units with blockchain-based audit trails mandated by Japan’s seven-year retention rule. BYD disclosed that software-enabled upgrades provided 8% of its after-sales revenue in 2025, validating OTA monetization at scale.

Emerging Software-Defined Vehicle Architectures

Zonal controllers replace dozens of legacy ECUs, trimming harness mass by 12-18 kilograms per vehicle and routing all functions through service-oriented middleware. Early Chinese and Japanese pilots deploy containerized applications on multi-core SoCs that host AUTOSAR Adaptive and Linux side-by-side. Semiconductor vendors' roadmap higher memory bandwidth and integrated hardware security modules aligned with these workloads. Pilot fleets in Tokyo demonstrate robotaxi operations controlled entirely through Toyota’s Arene operating system, confirming software-centric business models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cybersecurity Vulnerabilities in Vehicle ECUs | -1.3% | Global, acute in China, Japan, India | Short term (≤ 2 years) |

| Scarcity of Functional Safety-Certified Developers | -1.1% | India, ASEAN, with spillover to China | Medium term (2-4 years) |

| Rising BOM Cost Pressure on Low-End Two-Wheeler Makers | -0.7% | India, Indonesia, Vietnam, Thailand | Short term (≤ 2 years) |

| Fragmented Asia-Pacific Regulatory Compliance Landscape | -0.6% | ASEAN, Australia, New Zealand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cybersecurity Vulnerabilities in Vehicle ECUs

UN R155 compliance audits show 23% of legacy architectures lack hardware cryptography, forcing OEM retrofits costing more than USD 40 per unit.[4]United Nations Economic Commission for Europe, “UN Regulation No. 155 Cyber Security And Cyber Security Management System,” unece.org Hong Kong will align with R155 and R156 by December 2026, adding fresh retrofit demand across gray-market imports. China’s GB 44495-2024 mandates full-lifecycle cybersecurity management, spurring cloud-based security operation centers that watch CAN-bus traffic for anomalies. Semiconductor shortages slow the rollout of security-enhanced microcontrollers, extending exposure windows for known vulnerabilities.

Scarcity of Functional Safety-Certified Developers

The ASEAN Automotive Federation recorded an 18,000-engineer shortfall in ISO 26262 skills during 2025, delaying ADAS localization in Thailand, Indonesia, and Vietnam. India’s engineering firms certify about 3,000 developers a year, yet attrition eclipses 20%, eroding gains. Japan’s subsidy of JPY 500,000 (USD 3,300) per certification aims for 5,000 specialists by 2027. Despite captive academies and university ties, the three-to-four-year lag between enrollment and field-ready expertise constrains overall project throughput.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Two-Wheelers Lead Growth Momentum

Two-wheelers are projected to expand at 9.23% CAGR, propelled by Indian and Southeast Asian start-ups that bundle Linux dashboards, Bluetooth, and remote diagnostics into scooters below USD 1,500. Passenger cars retained 55.21% of Asia-Pacific vehicle-embedded software market share in 2025, buoyed by China’s 21 million-unit output and Japan’s electronics heritage. Light commercial vehicles integrate fleet telematics to comply with real-time tracking mandates in South Korea and Australia. Heavy trucks adopt predictive maintenance that analyzes vibration and oil quality data, reducing unplanned downtime by 15%.

While two-wheelers drive unit growth, passenger cars remain the largest revenue engine for the Asia-Pacific vehicle-embedded software market size, yet cost-sensitive sedans in Indonesia and the Philippines often strip advanced middleware to hit target price points. Light-duty vans benefit from mandated electronic logging devices, fostering incremental software sales per vehicle. Heavy commercial vehicles pay higher average selling prices for prognostics platforms that schedule service visits only when sensors flag abnormal patterns, further widening embedded software margins.

By Software Type: Middleware Captures Incremental Value

Middleware is forecast to rise at 9.56% CAGR as zonal controllers need service-oriented frameworks that broker data among heterogeneous processors. Application software held 38.43% of Asia-Pacific vehicle-embedded software market size in 2025, yet is shifting to containerized deployment for faster updates. Operating systems converge around Linux for infotainment and QNX or similar microkernels for safety, enabling common toolchains. Firmware revenue declines proportionally as value migrates upward.

Tier-1s increasingly offer proprietary middleware bundles tuned to specific system-on-chips, raising switching costs for automakers. Consortia such as COVESA publish open interface definitions to preserve interoperability. The resulting blend of closed performance-optimized stacks and open community code forces OEMs to balance time-to-market against long-term vendor lock-in across the Asia-Pacific vehicle-embedded software industry.

By Application: ADAS Surges On Regulatory Pull

ADAS and safety software is projected to climb at 9.78% CAGR, accelerated by China’s and Japan’s compulsory fitment rules. Infotainment still commanded 30.21% of the market share in 2025, but Android Automotive commoditizes basic functions and prompts OEMs to invest in augmented-reality navigation and AI assistants for differentiation. Power-train controllers in electric vehicles optimize battery discharge and motor torque with millisecond accuracy, deepening code complexity. Body and comfort functions migrate to zonal ECUs that simplify wiring layouts.

Telematics is growing due to usage-based insurance and compliance requirements, as it integrates high-frequency data streams into insurer rating models. The convergence of ADAS and infotainment on shared compute platforms is ongoing, which reinforces middleware demand. This trend is driving fresh architectural experiments across the Asia-Pacific vehicle-embedded software market.

By Propulsion Type: Fuel Cell Vehicles Amplify Software Content

Fuel cell electric vehicles are rising at a 9.46% CAGR as Japan and South Korea subsidize hydrogen refueling corridors and stack development. Battery electric vehicles held 43.56% of the market share in 2025, and shifted toward 800-volt systems that require precise charge-rate control. Hybrids embed algorithms that optimize gasoline-to-electric transitions based on route topology. Internal combustion engines remain the largest installed base but cede investment priority to electrified power-trains.

Toyota’s Arene operating system in the Mirai manages hydrogen pressure, stack cooling, and regenerative braking from over 200 sensor inputs. Hyundai’s HTWO toolkit allows third-party developers to fine-tune hydrogen consumption for specific duty cycles. Japan plans 800,000 FCEVs by 2030 under its revised hydrogen roadmap, sustaining long-run software demand in this niche yet code-intensive segment.

Geography Analysis

China accounted for 31.64% of regional revenue in 2025, anchored by HarmonyOS Cockpit integrations exceeding 1.5 million vehicles and Apollo’s 10 million kilometers of autonomous testing data. The January 2026 ADAS mandate applies to roughly 25 million units annually and forces rapid deployment of sensor-fusion middleware, while domestic chip-design programs pour investment into RISC-V cores for future safety controllers. ZEEKR’s 001 FR sedan adopted NVIDIA DRIVE Orin for Level 2+ autonomy, illustrating selective sourcing of foreign compute when performance dictates. Validation bottlenecks for safety-critical code remain a drag, but China’s scale secures its leadership in the Asia-Pacific vehicle-embedded software market.

India is the fastest-growing geography at 9.87% CAGR, fueled by Tata Elxsi’s and KPIT’s multi-year global tier-1 contracts and the rollout of AIS-189 and AIS-190 cybersecurity norms in October 2025. Renesas partnered with Tata Elxsi to localize ADAS middleware for chaotic traffic, while KPIT’s QuantumLeap cloud environment trims integration cycles 25% for European suppliers. Mahindra’s Snapdragon Ride-powered XUV.e8 enters production in late 2026, confirming that domestic OEMs will pay for advanced compute to future-proof electric SUVs. India’s two-wheeler ecosystem embeds connected stacks at scale, reinforcing its role as a growth pole for the Asia-Pacific vehicle-embedded software market.

Japan and South Korea marshal deep semiconductor capacity and aggressive 5G rollouts to pilot AI-centric shuttles and cloud-native OTA workflows. Toyota’s Arene controls robotaxi fleets in Tokyo and Osaka, while Hyundai AutoEver’s new 1,200-engineer software factory targets 50 million validated lines of code annually for Kia’s electric crossovers. Nissan will migrate to five domain controllers by 2028, trimming wiring mass 18 kilograms in the next-generation Leaf. Australia and New Zealand align with UN R155, pushing importers to retrofit secure telematics, and Southeast Asian incentives for electric two-wheelers seed regional demand for middleware governing battery-swap networks.

Competitive Landscape

The Asia-Pacific vehicle-embedded software market is moderately fragmented, with Bosch, Denso, and Continental competing against Huawei, Baidu, and multiple OEM captive units. Legacy tier-1s are acquiring niche middleware firms and partnering with chip makers. These collaborations enable them to ship pre-validated stacks on system-on-chips, reducing OEM integration times while protecting license revenue.

Chinese OEMs deepen vertical integration; BYD’s 3,000-engineer Shenzhen software center handles cockpit, power-train, and ADAS code, and NIO purchased autonomous-driving start-up Momenta for USD 300 million to internalize perception algorithms. Indian validation specialists position as low-cost integrators, delivering ISO 26262 verification at rates 40% below European peers and winning global contracts. NVIDIA’s DRIVE and Qualcomm’s Snapdragon Digital Chassis expand their regional footprints as automakers seek single-vendor solutions that combine silicon, software, and toolchains.

Patent filings grew 32% in 2025, led by Huawei in vehicle-to-everything communication and Toyota in fuel-cell optimization, underscoring an escalating race for defensible intellectual property. The chronic shortage of ASIL-D-certified engineers remains a competitive moat for incumbents, yet it simultaneously caps their ability to scale large-scale software programs rapidly, leaving openings for new entrants willing to invest in functional-safety training at speed. Heightened regulatory scrutiny compounds resource strain, making strategic alliances, joint validation centers, and open-source collaboration indispensable for sustaining momentum across the Asia-Pacific vehicle-embedded software market.

Asia-Pacific Vehicle-Embedded Software Industry Leaders

Robert Bosch GmbH

Denso Corporation

Continental AG

Panasonic Holdings Corporation

NXP Semiconductors N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Continental introduced CAEdge, a sensor-fusion platform that achieves 15-millisecond object detection latency and meets ASIL-D targets for highway pilot.

- January 2026: Denso became a Core Partner of AUTOSAR, pledging open-source Adaptive Platform modules that can cut middleware license fees by 30% for high-volume OEMs.

- January 2026: HARMAN International released a software-defined vehicle toolchain that lets engineers simulate zonal networks in the cloud, reducing physical prototypes 40%.

- January 2026: Volkswagen China launched a centralized electrical architecture capable of pushing delta-compressed OTA packages under 50 megabytes to 1.2 million vehicles in 72 hours.

Asia-Pacific Vehicle-Embedded Software Market Report Scope

The Asia-Pacific Vehicle-Embedded Software Market is the market for software integrated into vehicles to control various functions, enhance performance, and improve the user experience. This includes software for applications such as ADAS and safety, infotainment, powertrain, body control and comfort, and telematics.

The Asia-Pacific Vehicle-Embedded Software Market Report is Segmented by Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, and Two-Wheelers), Software Type (Operating System, Middleware, Application Software, and Firmware), Application (ADAS and Safety, Infotainment, Powertrain, Body Control and Comfort, and Telematics), Propulsion Type (Internal Combustion Engine, Battery Electric Vehicle, Hybrid Electric Vehicle, and Fuel Cell Electric Vehicle), and Country (China, Japan, South Korea, India, Australia and New Zealand, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Two-Wheelers |

| Operating System |

| Middleware |

| Application Software |

| Firmware |

| ADAS and Safety |

| Infotainment |

| Powertrain |

| Body Control and Comfort |

| Telematics |

| Internal Combustion Engine |

| Battery Electric Vehicle |

| Hybrid Electric Vehicle |

| Fuel Cell Electric Vehicle |

| China |

| Japan |

| South Korea |

| India |

| Australia and New Zealand |

| Rest of Asia-Pacific |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Heavy Commercial Vehicles | |

| Two-Wheelers | |

| By Software Type | Operating System |

| Middleware | |

| Application Software | |

| Firmware | |

| By Application | ADAS and Safety |

| Infotainment | |

| Powertrain | |

| Body Control and Comfort | |

| Telematics | |

| By Propulsion Type | Internal Combustion Engine |

| Battery Electric Vehicle | |

| Hybrid Electric Vehicle | |

| Fuel Cell Electric Vehicle | |

| By Country | China |

| Japan | |

| South Korea | |

| India | |

| Australia and New Zealand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What value will the Asia-Pacific vehicle-embedded software market reach by 2031?

The market is forecast to reach USD 12.32 billion by 2031 on an 8.26% CAGR.

Which propulsion type shows the fastest software spending growth?

Fuel cell electric vehicles are set to expand at 9.46% CAGR between 2026 and 2031.

Why is middleware growing faster than other software layers?

Zonal and domain architectures need service-oriented middleware, driving a 9.56% CAGR for this layer.

How do ADAS mandates affect software demand?

China’s and Japan’s rules make emergency braking and lane-keeping compulsory, lifting ADAS software orders across high-volume vehicles.

Where are the best regional growth opportunities?

India leads with a projected 9.87% CAGR thanks to new cybersecurity standards and a thriving engineering-services ecosystem.

Page last updated on: