North America Green IT Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

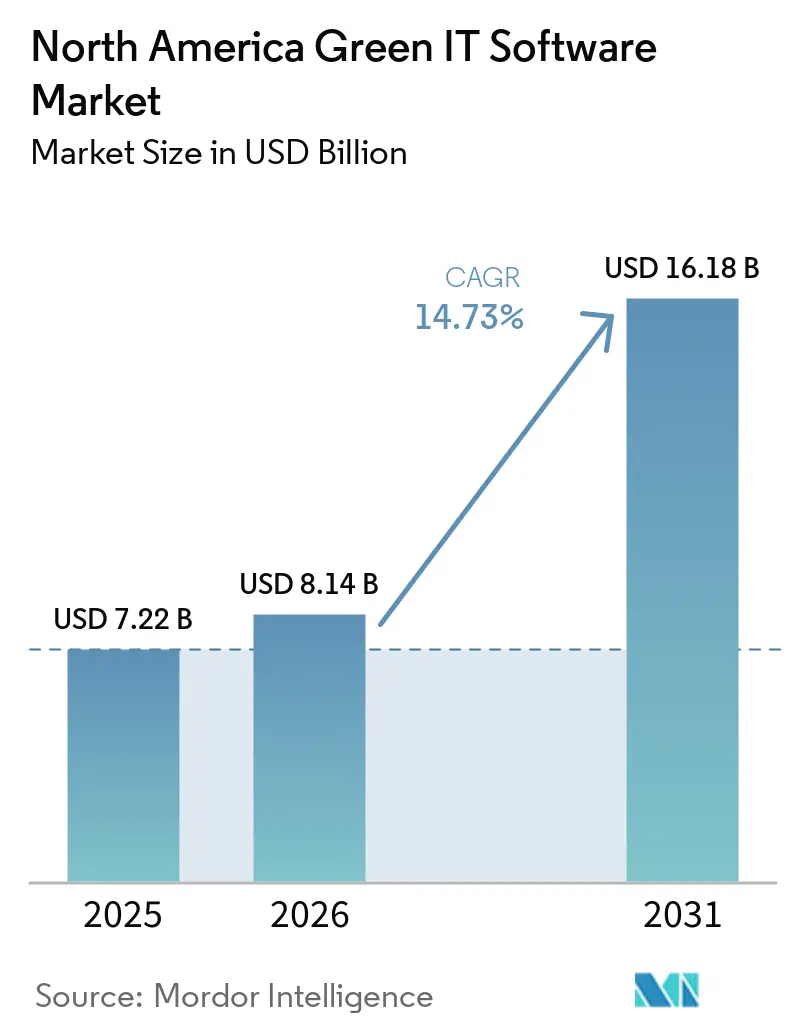

| Base Year Market Size (2025) | USD 7.22 Billion |

| Market Size (2026) | USD 8.14 Billion |

| Market Size (2031) | USD 16.18 Billion |

| Growth Rate (2026 - 2031) | 14.73% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Green IT Software Market Analysis by Mordor Intelligence

The North America green IT software market size is projected to expand from USD 7.22 billion in 2025 and USD 8.14 billion in 2026 to USD 16.18 billion by 2031, registering a CAGR of 14.73% between 2026 and 2031. The North America green IT software market is growing because enterprises now treat sustainability data as an operating requirement that must stand up to audit, procurement review, and board oversight. Demand is also strengthening because state mandates in the United States, disclosure reforms in Mexico, and carbon pricing in Canada are pushing companies to standardize carbon data across business units instead of relying on isolated reporting tools. The North America green IT software market is also moving beyond basic footprint measurement, as buyers want systems that connect emissions data with procurement, capital allocation, and financial close processes. Competition is becoming more layered because ERP vendors are embedding carbon functions inside core business systems, while specialist providers are focusing on disclosure quality, supplier data depth, and workflow precision. The strongest opportunities now sit with platforms that can combine traceable data collection, flexible deployment, and decision support without creating another fragmented software stack for already stretched enterprise teams.

Key Report Takeaways

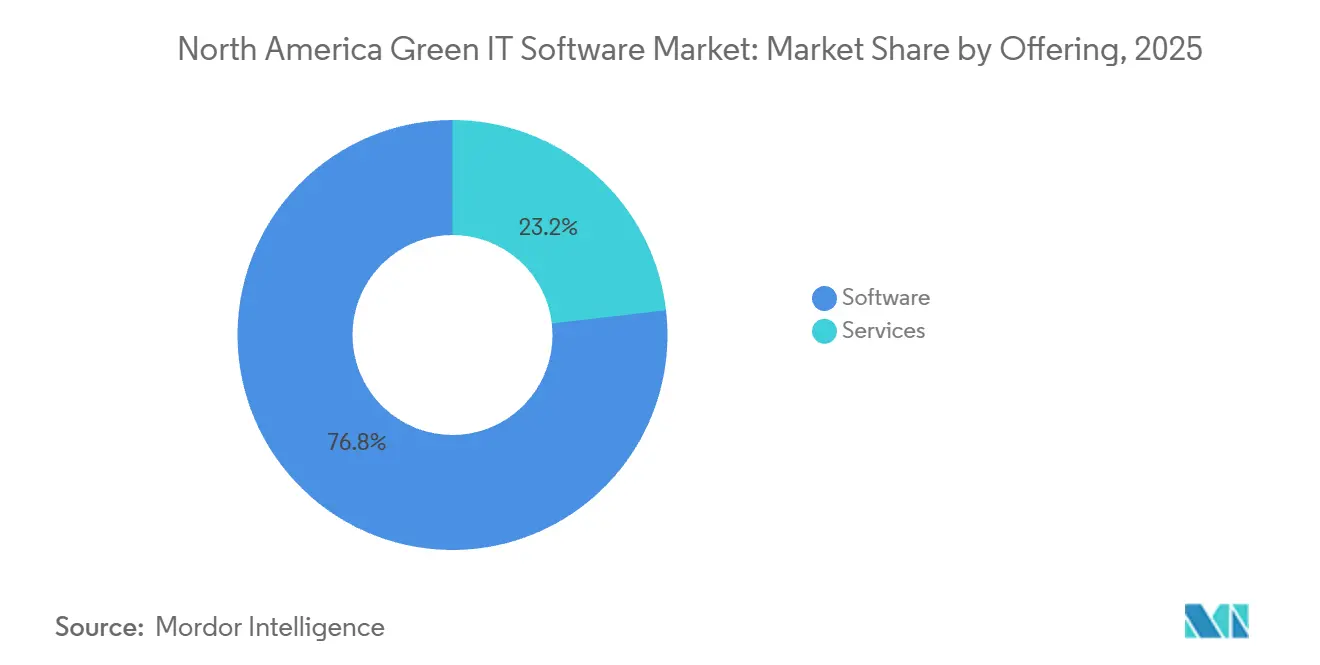

- By offering, software accounted for 76.84% of the 2025 revenue of the North America green IT software market, while services are projected to expand at a 17.12% CAGR through 2031.

- By deployment mode, cloud captured 68.92% of revenue in 2025, while hybrid is projected to record the highest CAGR of 18.46% through 2031.

- By organization size, large enterprises accounted for 71.36% of revenue share in 2025, while SMEs are projected to expand at a 16.89% CAGR through 2031.

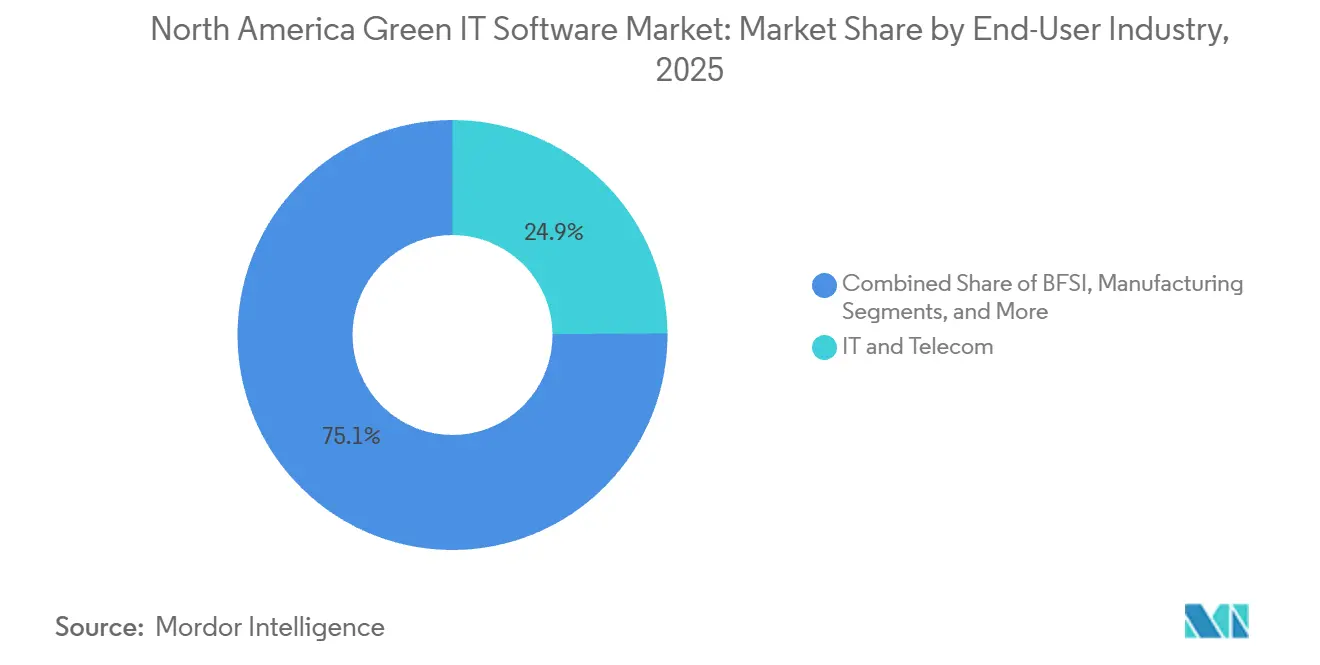

- By end-user industry, IT and telecom accounted for 24.87% of the revenue of the North America green IT software market in 2025, while healthcare is projected to grow at an 18.72% CAGR through 2031.

- By solution type, carbon management and accounting software held 31.74% share in 2025, while decarbonization planning software is projected to grow at a 20.15% CAGR through 2031.

- By geography, the United States held 81.16% of the North America green IT software market share in 2025, while Mexico is projected to expand at a 17.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Green IT Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Enterprise Demand for Carbon-Ready IT Workflows | +2.8% | North America, United States primary, Canada secondary | Short term (≤ 2 years) |

| Regulatory Push for Audit-Ready Sustainability Reporting | +2.5% | North America, California SB 253 and SB 261, Mexico CNBV IFRS S1 and S2, Canada OBPS | Short term (≤ 2 years) |

| Data Center Energy Cost Optimization Initiatives | +1.5% | North America, United States hyperscalers primary | Medium term (2-4 years) |

| AI-Enabled Scope 3 Data Collection and Exception Handling | +1.2% | Global, North America core markets | Medium term (2-4 years) |

| Green Cloud Migration and Virtualization Programs | +0.9% | North America and EU | Medium term (2-4 years) |

| Board-Level ESG Accountability and Disclosure Controls | +0.7% | North America and EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Enterprise Demand for Carbon-Ready IT Workflows

The North America green IT software market is being pushed by a clear shift in enterprise behavior, as sustainability programs are moving from periodic disclosure exercises into continuous data workflows inside finance, procurement, and operations. Buyers increasingly want systems that can trace emissions data back to operational records, because internal review teams and external stakeholders now expect a clearer chain of evidence than spreadsheet-based processes can provide. This change is also increasing demand for workflow tools that can connect business activity, carbon factors, approval steps, and audit logs in the same environment. Vendors are responding by adding automation and scenario tools that help users work with carbon data in a more operational way, instead of as a reporting afterthought. The North America green IT software market benefits from this transition because enterprise buyers are no longer selecting tools only for disclosure; they are selecting platforms that can support repeatable decisions across business functions.

Regulatory Push for Audit-Ready Sustainability Reporting

The North America green IT software market is also advancing as regional regulations are becoming more layered, even though the federal climate disclosure approach in the United States remains unsettled. The U.S. Securities and Exchange Commission proposed rescinding its climate-related disclosure rules in May 2026, yet enterprises still face strong pressure from state rules, customer requirements, and cross-border reporting expectations.[1]U.S. Securities and Exchange Commission, “SEC Proposes Rescission of Climate-Related Disclosure Rules,” SEC Newsroom, sec.gov Mexico strengthened this regional compliance cycle through tools linked to IFRS-based sustainability reporting, giving issuers a more defined path for structuring their first mandatory reports. Canada is reinforcing the same direction through a carbon pricing framework that makes accurate emissions measurement more material for business planning and compliance cost control. As these obligations accumulate, the North America green IT software market is becoming less dependent on any single rule and more tied to the broader need for auditable, multi-jurisdiction data management.

Data Center Energy Cost Optimization Initiatives

The North America green IT software market is gaining additional support from data center operators, which now treat energy performance as both a cost and a reporting issue. Large facilities are under pressure to manage energy intensity more carefully because power use now affects operating margins, capacity planning, and carbon performance at the same time. The World Economic Forum noted in December 2025 that data centers can cut overhead energy use sharply when power usage effectiveness improves from older levels toward best-in-class operation. That operating context supports software that links facility data, energy use, and emissions records in one workflow, especially where cloud growth and AI workloads are adding more strain to infrastructure planning. The North America green IT software market is therefore seeing stronger interest in platforms that can turn building and equipment data into actions that matter for both sustainability and budget decisions.

AI-Enabled Scope 3 Data Collection and Exception Handling

The North America green IT software market is also being shaped by AI tools that reduce the time and effort needed to work with complex supplier and activity data. Scope 3 processes have been difficult for many companies because supplier records arrive in different formats, with varying levels of detail and weak traceability across approval cycles. Vendors are responding by adding agents, guided workflows, and scenario tools that shorten the time needed to clean data, test assumptions, and prepare reporting outputs. SAP stated that its Footprint Optimization Agent is expected to reduce carbon scenario simulation time from one full workday to around 20 minutes per analysis cycle by the end of 2026.[2]SAP SE, “New Sustainability AI Agents,” SAP News Center, news.sap.com The North America green IT software market is benefiting because buyers now see AI not only as a reporting aid, but also as a way to reduce manual effort in data preparation, review, and exception handling.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Sustainability Data and ESG Systems Talent | -1.8% | Global, with acute pressure in North America | Short term (≤ 2 years) |

| High Implementation Complexity Across Legacy IT Stacks | -1.3% | North America, United States and Canada | Medium term (2-4 years) |

| Data Sovereignty and Cross-Border Hosting Constraints | -0.8% | North America, spillover to Mexico and Canada | Medium term (2-4 years) |

| Buyer Fatigue From Fragmented ESG Toolchains | -0.6% | North America, United States primary | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shortage Of Sustainability Data and ESG Systems Talent

The North America green IT software market still faces a practical execution problem, because many companies do not have enough staff who can manage sustainability data, enterprise systems, and assurance needs together. The gap is not limited to specialist sustainability teams, since procurement, finance, and operations staff also need to work with these platforms in day-to-day processes. When companies lack those skills, implementation slows, workflow adoption weakens, and software value is realized later than buyers expected. This pressure is one reason vendors are adding more guided automation and natural-language support to reduce the skill burden on internal teams. The North America green IT software market remains attractive, but this talent constraint continues to limit how quickly organizations can move from purchase to full operational use.

High Implementation Complexity Across Legacy IT Stacks

The North America green IT software market also encounters friction because most large enterprises still run a mix of ERP modules, spreadsheets, utility data feeds, custom databases, and operational systems that were never built for audit-grade carbon workflows. Integrating those environments takes time because buyers need consistent data structures, clear ownership rules, and reliable links between operational records and disclosure outputs. This is why product strategy in the market is moving toward connectors, APIs, and embedded calculation tools instead of standalone interfaces. IBM highlighted this need in 2026 by launching the Envizi Emissions API and Envizi Emissions Calculations in Excel, both designed to embed greenhouse gas calculations into existing business workflows. The North America green IT software market will continue to expand, but legacy complexity still favors vendors that can simplify integration rather than those that only add more reporting functionality.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Leads as Audit Needs Intensify

Software accounted for 76.84% of the North America green IT software market share in 2025, showing that buyers preferred platform-based systems over service-heavy delivery models when traceability and control became more important. That result reflects a structural buyer preference for systems that keep carbon records, workflow history, and reporting logic inside the enterprise technology environment. In the North America green IT software market, software is often chosen first because companies want repeatable controls instead of project-based reporting exercises. Audit readiness also matters more now because sustainability data increasingly needs the same level of review discipline that financial data receives. This keeps core platforms at the center of purchasing decisions, especially in larger organizations with multiple reporting entities and approval layers.

The software segment also benefits because it supports ongoing use across procurement, finance, operations, and corporate sustainability teams without forcing those functions into separate data environments. SAP has continued to position this embedded model around a common data foundation, which aligns well with enterprise demand for less fragmented sustainability workflows. Services, while smaller in 2025, are projected to grow at a 17.12% CAGR through 2031 because many first-time buyers still need implementation support, data setup, methodology guidance, and assurance preparation. That growth is especially important where reporting requirements are new and internal teams have not yet built stable operating routines. As a result, the North America green IT software market is not moving away from services, but it is making services more complementary to software rather than the main source of value.

By Deployment Mode: Hybrid Gains as Governance Splits Deployments

Cloud held 68.92% of revenue in 2025, which shows how strongly enterprises favored scalable deployment, easier global data aggregation, and lower upfront infrastructure requirements. Cloud also fits the operating model of companies that need to gather emissions, utility, supplier, and compliance data from many sites and legal entities. In the North America green IT software market, cloud remains the default choice for many new deployments because it supports faster rollout and easier product updates. Buyers also value the way cloud architecture can support centralized governance while still allowing business units to contribute data from different systems. These advantages explain why cloud remained the leading deployment mode even as governance requirements became more demanding.

Hybrid is projected to post the fastest CAGR of 18.46% through 2031 because some organizations now want cloud flexibility without placing every sensitive record outside their internal environment. This matters most in regulated settings where personal, financial, or contractual information can sit next to carbon and supplier data. The hybrid shift also shows that the North America green IT software market is maturing, because buyers are refining early deployment choices after working through initial assurance cycles. Vendors that can support both centralized reporting and selective on-premises data handling are in a stronger position as enterprise architecture decisions become more nuanced. On-premises systems will remain relevant for legacy-heavy operators, but the demand center is clearly moving toward architectures that balance scale with governance.

By Organization Size: Large Enterprises Anchor Demand While SMEs Gain Pace

Large enterprises held 71.36% of 2025 revenue, reflecting their broader regulatory exposure, larger implementation budgets, and stronger need for multi-entity data control. Many of these buyers operate across several jurisdictions, which makes a fragmented approach to carbon accounting increasingly impractical. In the North America green IT software industry, large enterprises also benefit from installed ERP environments that can be extended rather than replaced when sustainability functions are added. That installed base helps larger buyers move faster once strategic alignment is in place, even if implementation work remains complex. It also reinforces the advantage of vendors that can link carbon processes directly with procurement, finance, and operational systems already in use.

SMEs are projected to grow at a 16.89% CAGR through 2031 because supply chain pressure is moving sustainability expectations downstream from large buyers to smaller suppliers. This means many SMEs are not adopting platforms only for internal goals, but to preserve commercial access and meet customer disclosure requests. The North America green IT software market is therefore widening beyond top-tier corporations and creating a more distributed customer base over time. EcoVadis has supported this shift by expanding Carbon Data Network partnerships that are designed to improve supplier-level primary data exchange across enterprise ecosystems.[3]EcoVadis, “EcoVadis Accelerates Scope 3 Transparency, Adding Carbmee to Rapidly Expanding Carbon Data Network,” EcoVadis Press Release, resources.ecovadis.com As this supplier-led adoption expands, current revenue concentration in large enterprises is likely to ease, even though they will remain the largest spending group.

By End-User Industry: Healthcare Scales Fastest Across End Users

IT and telecom led with 24.87% share in 2025 because the sector is both a large software buyer and a core enabler of the cloud and digital infrastructure behind many sustainability platforms. Companies in this segment face pressure from enterprise customers, investors, and data center operations at the same time, which makes carbon data management more central to business planning. In the North America green IT software market, that combination supports sustained demand for measurement, supplier engagement, and reporting tools. The sector also tends to adopt digital process tools earlier than more traditional industries, which helps software vendors scale product enhancements faster. This keeps IT and telecom at the center of market demand even as other verticals deepen their own programs.

Healthcare is projected to expand at an 18.72% CAGR through 2031 because hospitals, life sciences companies, and healthcare supply networks are under increasing pressure to understand the carbon impact of distributed purchasing and product use. These organizations often manage complex supply chains and strict operating standards, which makes emissions data more difficult to gather and verify. The North America green IT software market is seeing a stronger opening here because generic reporting workflows do not always capture the operational detail that healthcare buyers need. That is why sector-specific data support and more precise workflow design are becoming more relevant in this vertical, even though the space is still developing. BFSI and manufacturing remain important middle-tier demand centers, while energy and utilities, retail and e-commerce, government, construction and infrastructure, and other industries collectively keep the end-user mix broad enough to limit overdependence on one vertical.

By Solution Type: Decarbonization Planning Moves to the Forefront

Carbon management and accounting software held 31.74% of revenue in 2025, confirming that emissions measurement still serves as the core entry point for enterprise adoption. Companies typically need a reliable baseline before they can move into reduction planning, board reporting, or resource optimization. In the North America green IT software industry, that makes accounting systems are the foundation on which adjacent solution categories are built. ESG reporting and compliance software, along with sustainability data management platforms, sit close to this base because they help translate activity records into usable disclosure outputs. Together, these categories create the core workflow stack that many enterprises adopt before they spend more on optimization or scenario planning.

Decarbonization planning software is projected to grow at a 20.15% CAGR through 2031, which shows that buyers increasingly want tools that support action, not only measurement. This part of the North America green IT software market is gaining relevance because procurement teams, finance teams, and operations leaders now need to test carbon pathways before making investment or sourcing decisions. SAP has reinforced this shift through its Footprint Optimization Agent, which is designed to shorten the time needed for carbon scenario analysis and make planning more usable inside business workflows. Energy and resource optimization software also remains important because it connects sustainability goals with measurable cost outcomes in facilities, infrastructure, and data center settings. That combination means the market is broadening from disclosure-led demand into a more operational mix where planning and performance management carry greater strategic weight.

Geography Analysis

The United States accounted for 81.16% of revenue in 2025, which gave it the clear lead across the region and established it as the core revenue base for the North America green IT software market. The country benefits from the scale of its enterprise sector, its early adoption of digital business systems, and its concentration of software vendors that continue to expand product capability. The North America green IT software market size remains heavily tied to the United States because many of the region’s largest buyers, technology providers, and implementation partners are headquartered there. Even with the federal climate disclosure approach shifting in 2026, investment did not lose momentum because large enterprises still face state rules, customer requirements, and cross-border expectations. Large U.S. corporations in technology, manufacturing, and retail also devote between USD 2 million and USD 5 million annually to their carbon IT stacks, which supports a high-value enterprise buyer base inside the region.

Canada held the second-largest position in regional demand and continues to create structured software need through a stable carbon pricing framework. That price path gives industrial emitters a stronger reason to measure emissions accurately and manage data quality with greater discipline. The North America green IT software market also benefits from Canadian vendor depth, with companies such as Cority Software Inc. and Novisto strengthening the country’s role as both a buyer base and a development center. Canada’s reporting infrastructure and active provincial carbon policy environment make it one of the more systematic demand centers in the region.

Mexico is projected to record the fastest CAGR at 17.94% through 2031, making it the most dynamic country opportunity in the North America green IT software market over the forecast period. The current growth cycle is being supported by a phased compliance schedule tied to IFRS S1 and S2 aligned reporting requirements for issuers, which creates a multi-year implementation path instead of a one-time adjustment. This structure matters because many organizations in Mexico are still in the gap assessment and implementation stage, not the optimization stage. As a result, the country is likely to generate strong demand for core platforms, setup support, and workflow standardization before buyers move more heavily into advanced planning tools.

Competitive Landscape

The North America green IT software market remains moderately fragmented at the overall level, but competition is tightening as leading vendors try to own larger portions of the enterprise workflow. SAP SE and IBM Corporation sit at the center of this push because both companies are embedding carbon management more directly into business systems that buyers already use. That matters in the North America green IT software market because existing data relationships can be as important as standalone functionality when enterprises choose long-term platforms. IBM strengthened this position in April 2026 by launching the Envizi Emissions API and Envizi Emissions Calculations in Excel, both designed to place emissions logic inside familiar enterprise processes. SAP has followed a similar path by expanding its sustainability roadmap around ERP-linked data control and AI-enabled workflow support.

Specialist vendors are responding by focusing on data quality, supplier intelligence, and use-case depth rather than trying to match ERP incumbents across every feature. This is visible in the way EcoVadis has expanded its Carbon Data Network through direct ecosystem partnerships intended to improve primary supplier data flow and reduce dependence on generalized estimates. That network model could reshape competition in the North America green IT software market because strong data exchange utilities can become difficult for buyers to replace once procurement and disclosure workflows depend on them. Workiva is also using product updates to deepen its role in disclosure workflows, including new sustainability support tied to simplified ESRS intelligence in 2026.[4]Workiva Inc., “Sustainability Release Notes for May 2026,” Workiva Support Center, support.workiva.comThese moves show that the market is not dividing only between large and small vendors, but between platforms that control underlying data flows and those that offer narrower application layers.

White-space opportunities remain strongest in SME onboarding, sector-specific workflow design, and operational integration with existing enterprise systems. Mid-market buyers still need faster deployment, lower process burden, and cleaner user experience than many large-enterprise tools were originally built to deliver. Cority’s recognition in 2026 for enterprise carbon management software, supported by a library of more than 1 million time-stamped emissions factors, shows that mid-tier specialists can still compete well when they offer deeper functional precision.[5]Cority Software Inc., “Cority Named as a Leader in Carbon Management Software,” Cority News and Media, cority.comThe North America green IT software market is therefore likely to stay competitive across several layers, with incumbents winning on breadth, specialists winning on workflow depth, and emerging providers targeting speed and simplicity where enterprise stacks remain too heavy.

North America Green IT Software Industry Leaders

Workiva Inc.

Persefoni AI Inc.

IBM Corporation

SAP SE

Salesforce, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SAP SE announced new sustainability AI agents, including the Sustainability Regulatory Readiness Agent, Footprint Optimization Agent, and Packaging Compliance Agent, for general availability by the end of 2026. The Footprint Optimization Agent reduces carbon scenario simulation time from a full workday to approximately 20 minutes, while the Regulatory Readiness Agent automates the translation of materiality to reporting scope for CSRD and other frameworks.

- April 2026: IBM Corporation announced the general availability of the Envizi Emissions API and, separately, Envizi Emissions Calculations in Excel, enabling organizations and third-party developers to embed GHG Protocol-aligned emissions calculations into existing enterprise systems and spreadsheet workflows at scale.

- April 2026: EcoVadis added Carbmee GmbH to its Carbon Data Network, following the March 2026 addition of Watershed to the ecosystem. The expanding network of CDN partners, now including Sweep, Normative, Watershed, and Carbmee, aims to replace spend-based Scope 3 estimates with verified primary data at scale.

- March 2026: EcoVadis and Watershed partnered to close the Scope 3 data gap by expanding supplier-specific primary data exchange through the Carbon Data Network.

North America Green IT Software Market Report Scope

The North America green IT Software market refers to the market for software platforms and related services that help organizations measure, manage, optimize, and reduce the environmental impact of their information technology operations. These solutions enable enterprises to monitor carbon emissions, track energy consumption, automate ESG and sustainability reporting, manage sustainability data, optimize data center efficiency, and support decarbonization initiatives across IT infrastructure, cloud environments, and digital operations.

The North America Green IT Software Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and SMEs), End-User Industry (IT and Telecom, BFSI, Manufacturing, Energy and Utilities, Retail and E-Commerce, Government, Healthcare, Construction and Infrastructure, and Other End-user Industries), Solution Type (Carbon Management and Accounting Software, ESG Reporting and Compliance Software, Sustainability Data Management Platforms, Decarbonization Planning Software, and Energy and Resource Optimization Software), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| SMEs |

| IT and Telecom |

| BFSI |

| Manufacturing |

| Energy and Utilities |

| Retail and E-Commerce |

| Government |

| Healthcare |

| Construction and Infrastructure |

| Other End-User Industries |

| Carbon Management and Accounting Software |

| ESG Reporting and Compliance Software |

| Sustainability Data Management Platforms |

| Decarbonization Planning Software |

| Energy and Resource Optimization Software |

| United States |

| Canada |

| Mexico |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| SMEs | |

| By End-User Industry | IT and Telecom |

| BFSI | |

| Manufacturing | |

| Energy and Utilities | |

| Retail and E-Commerce | |

| Government | |

| Healthcare | |

| Construction and Infrastructure | |

| Other End-User Industries | |

| By Solution Type | Carbon Management and Accounting Software |

| ESG Reporting and Compliance Software | |

| Sustainability Data Management Platforms | |

| Decarbonization Planning Software | |

| Energy and Resource Optimization Software | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the North America green IT software market size in 2026 and how fast will it grow through 2031?

The North America green IT software market was valued at USD 7.22 billion in 2025, is forecast at USD 8.14 billion in 2026, and is expected to reach USD 16.18 billion by 2031 at a 14.73% CAGR.

Which segment leads by offering in North America green IT software?

Software led by offering with 76.84% of 2025 revenue because buyers favored platform-based systems that support traceable and audit-ready carbon workflows.

Why is hybrid deployment growing faster than cloud-only models?

Hybrid is projected to grow at an 18.46% CAGR because buyers increasingly want cloud scale while keeping sensitive financial, operational, or contractual records under tighter governance.

Which customer group drives the largest share of spending?

Large enterprises held 71.36% of 2025 revenue, supported by wider regulatory exposure, larger budgets, and stronger need for multi-entity data control.

Which end-user vertical is expanding the fastest?

Healthcare is projected to grow at an 18.72% CAGR through 2031 as hospitals, life sciences companies, and healthcare supply networks face more pressure to improve supply chain emissions visibility.

Which country offers the strongest growth opportunity through 2031?

Mexico is expected to post the fastest growth at a 17.94% CAGR, supported by its phased IFRS S1 and S2 aligned sustainability reporting requirements for issuers.

Page last updated on: