SME Green IT SaaS Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

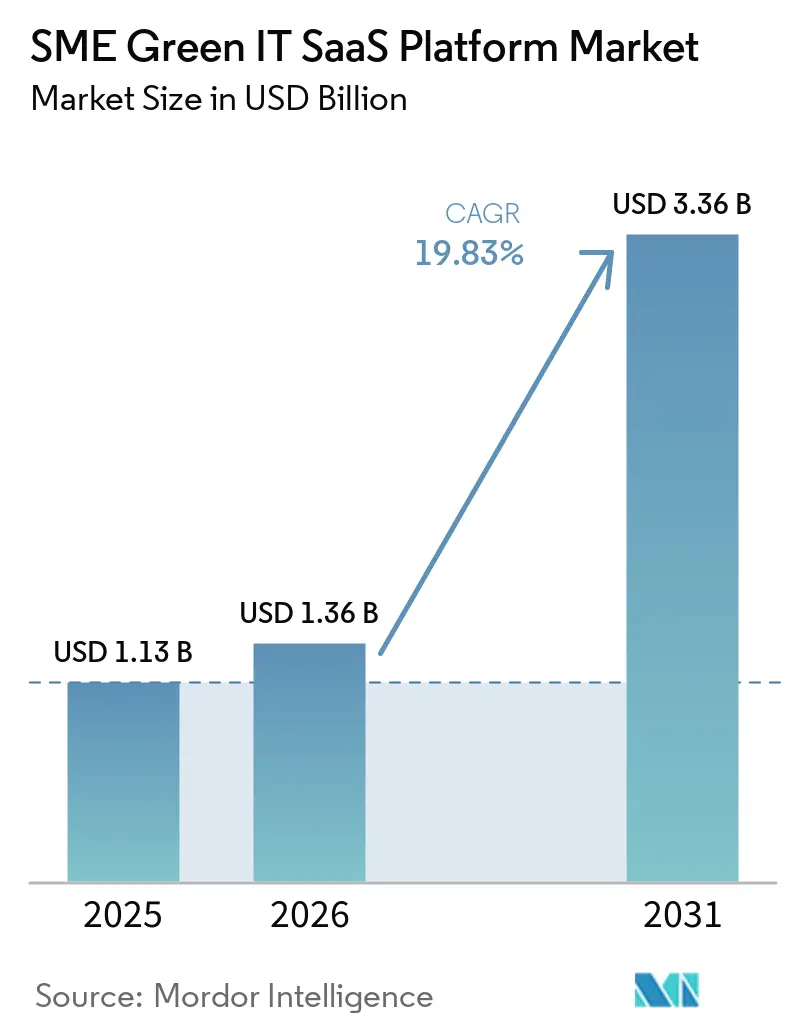

| Market Size (2026) | USD 1.36 Billion |

| Market Size (2031) | USD 3.36 Billion |

| Growth Rate (2026 - 2031) | 19.83% CAGR |

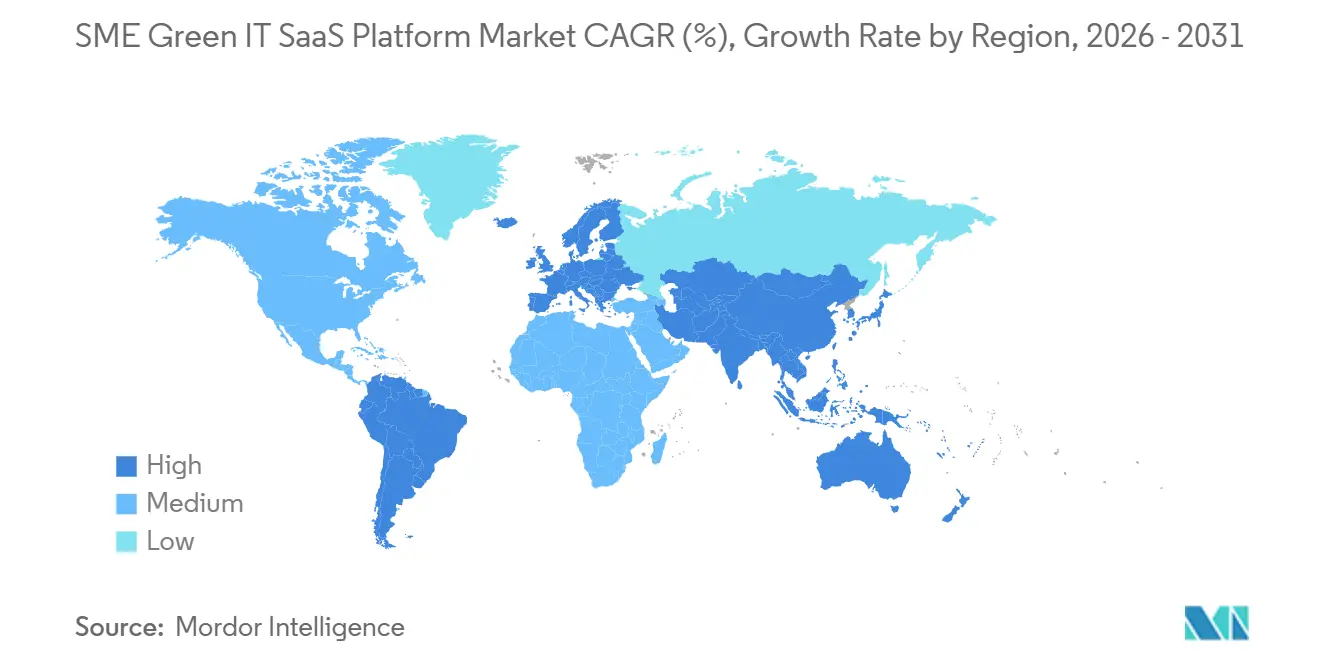

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

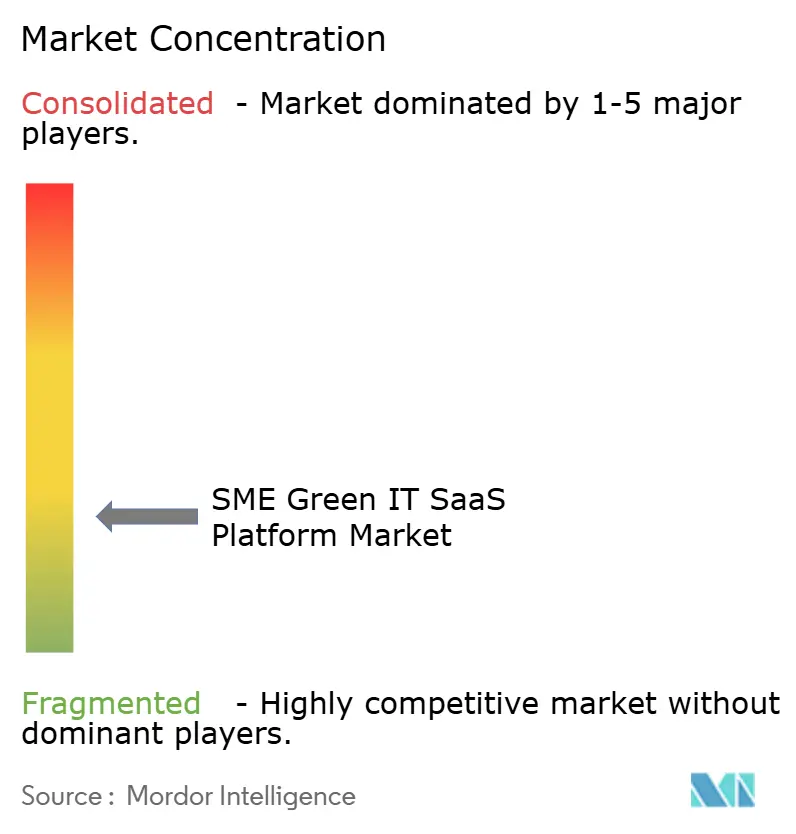

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

SME Green IT SaaS Platform Market Analysis by Mordor Intelligence

The SME green IT SaaS platform market size was valued at USD 1.13 billion in 2025 and estimated to grow from USD 1.36 billion in 2026 to reach USD 3.36 billion by 2031, at a CAGR of 19.83% during the forecast period (2026-2031). Adoption is moving away from optional disclosure tools and toward systems that handle supplier data requests, repeat reporting, and audit-ready records. Demand remains strong even after the EU narrowed the mandatory CSRD scope, because voluntary reporting under VSME and buyer requests from large enterprises continue to draw SMEs into structured disclosure workflows. Competition is shifting from stand-alone carbon-tracking products to broader platforms that combine reporting templates, integrations, and advisory support. Vendors with modular pricing, partner ecosystems, and service bundles are better placed because many SMEs need help with onboarding and data cleanup before software can be used consistently. The strongest near-term opportunity sits where regulatory timelines, procurement pressure, and established SaaS buying habits overlap, while the main risk remains fragmented source data that slows deployment and raises churn.

Key Report Takeaways

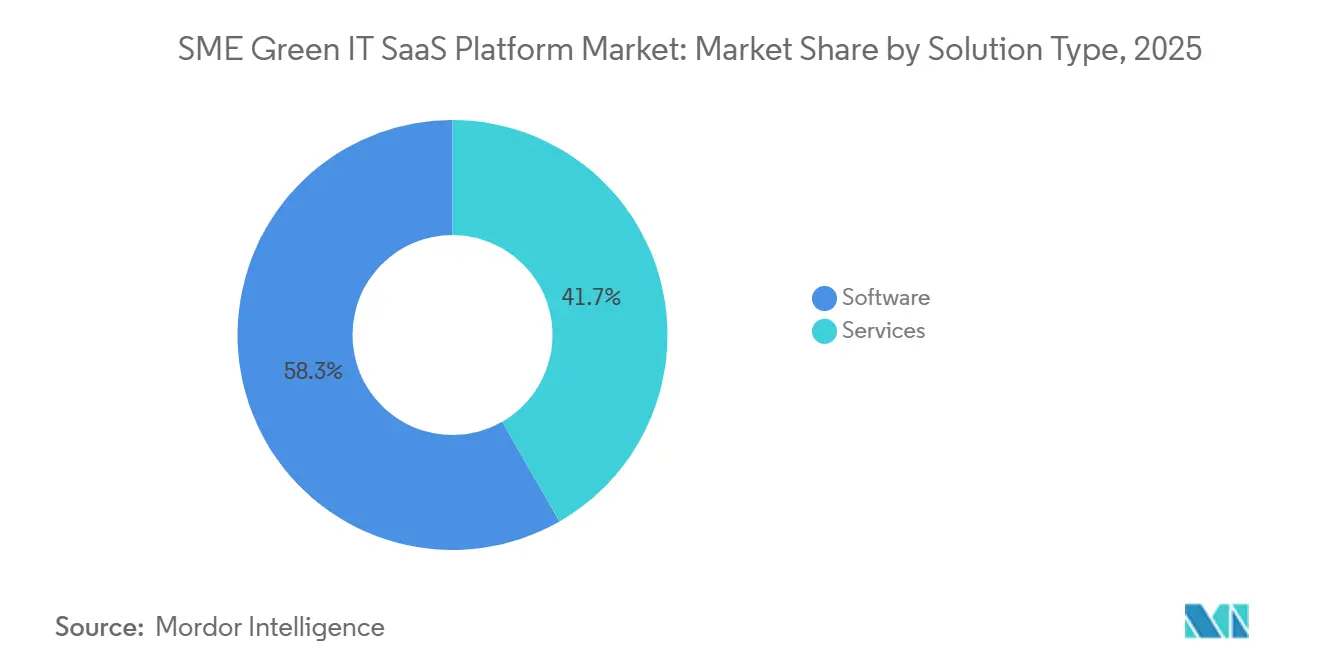

- By solution type, software accounted for 58.30% of the market in 2025, while services are projected to expand at 22.67% CAGR through 2031.

- By deployment model, cloud SaaS held 59.78% of the SME green IT SaaS platform market in 2025, while hybrid deployment is projected to expand at 20.42% CAGR through 2031.

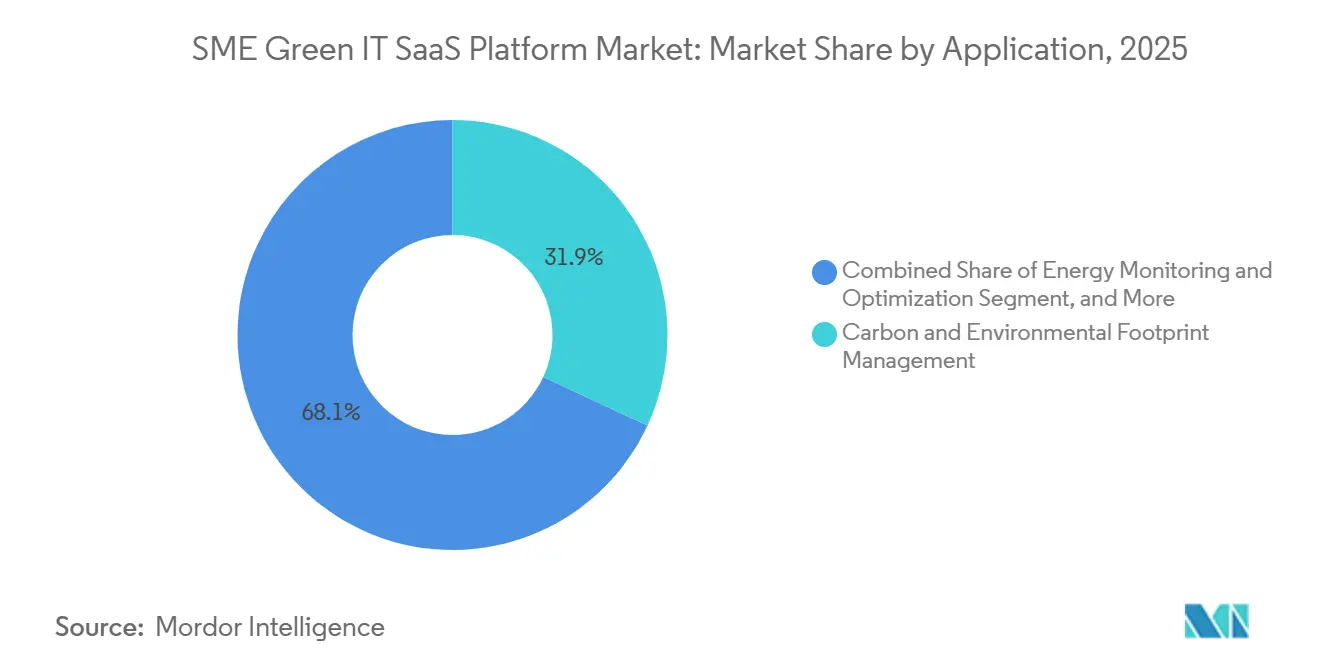

- By application, carbon and environmental footprint management accounted for 31.92% of the market in 2025, while ESG reporting and compliance management is projected to expand at 21.77% CAGR through 2031.

- By end-user industry, IT and telecom accounted for 28.64% of the market in 2025, while healthcare and life sciences are projected to expand at a 24.43% CAGR through 2031.

- By geography, North America held 37.64% of the SME green IT SaaS platform market in 2025, while Asia-Pacific is projected to expand at a 23.17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global SME Green IT SaaS Platform Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising Scope 3 Supplier Data Pressure on SME SaaS Adoption | +4.5% | Global, with highest intensity in EU, North America, and Japan | Short term (≤ 2 years) |

| Template-Driven Compliance for CSRD, ISSB, And Related Reporting | +3.8% | EU core, spill-over to Asia-Pacific and North America | Medium term (2-4 years) |

| AI-Assisted Carbon and Energy Workflows Reduce SME Admin Burden | +3.2% | Global | Medium term (2-4 years) |

| Lower Total Cost of Ownership Versus Legacy On-Premise Tools | +2.4% | North America, Western Europe, emerging Asia-Pacific | Short term (≤ 2 years) |

| Embedded Sustainability Requirements in B2B Procurement Portals | +2.0% | EU, North America, Australia | Medium term (2-4 years) |

| Margin Expansion Through Modular Cross-Sell of IT, Energy, and ESG Modules | +1.5% | North America, EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Scope 3 Supplier Data Pressure on SME SaaS Adoption

Large companies now ask smaller suppliers for primary emissions data more consistently, keeping the SME green IT SaaS platform market tied to procurement workflows rather than to formal reporting rules. The 2025 VSME recommendation provided non-listed SMEs with a defined disclosure format, making supplier questionnaires easier to align with a common template.[1]EFRAG, “Voluntary Sustainability Reporting Standard for Non-Listed SMEs,” EFRAG EcoVadis said in May 2026 that more than USD 2.5 trillion in procurement spend across its network is governed through sustainability risk insights, which shows how deeply buyer-led data requests now run through supply chains. This pressure is strongest in manufacturing, retail, and healthcare, where suppliers risk losing preferred status when they cannot respond quickly with usable carbon and ESG data. In the SME green IT SaaS platform market, that means adoption can remain firm even when public policy moves more slowly, because the immediate trigger often lies within commercial contracts.

Template-Driven Compliance for CSRD, ISSB, and Related Reporting

The SME green IT SaaS platform market is also benefiting from clearer disclosure templates that reduce the effort needed for first-time reporting. The EU Commission recommendation around the EFRAG VSME standard in July 2025 created a 46-point structure that vendors can build directly into onboarding and reporting workflows. IFRS issued targeted amendments to IFRS S2 in December 2025 to ease Scope 3 reporting burdens, which lowered the entry barrier for smaller preparers. When rules arrive in structured form, SMEs can start with guided data collection instead of designing their reporting process from scratch. This favors platforms that keep libraries updated across VSME, ESRS, and IFRS-based requirements, and it pushes the SME green IT SaaS platform market toward products with stronger compliance maintenance features.

AI-Assisted Carbon and Energy Workflows Reduce SME Admin Burden

AI features are becoming a practical adoption tool in the SME green IT SaaS platform market because they cut manual work for companies with small teams. SAP said in May 2026 that its Footprint Optimization Agent can reduce scenario simulation time from 1 day to 20 minutes, demonstrating how automation is moving from reporting to planning support. IBM made its Envizi Emissions Calculations Excel Add-in available on Microsoft AppSource in January 2026, helping non-technical users run GHG Protocol-aligned calculations within a familiar spreadsheet workflow.[2]IFRS Foundation, “Amendments to IFRS S2,” IFRS These tools matter because many SMEs still organize utility bills, invoices, and procurement records outside dedicated sustainability systems. As data ingestion, factor mapping, and audit-trail creation become more automated, the SME green IT SaaS platform market becomes more accessible to firms that would otherwise delay adoption.

Lower Total Cost of Ownership Versus Legacy On-Premise Tools

Lower upfront costs remain a direct growth lever for the SME green IT SaaS platform market, as subscription-based delivery reduces capital spending and spreads updates across the vendor base. SAP described in January 2025 how integrated cloud tools can bring Scope 3 reporting, due diligence support, and traceability into a single subscription environment. Microsoft added sustainability APIs to Dynamics 365 Business Central in its 2026 Wave 1 release, which supports lower-cost data flows between ERP records and external reporting systems. Modular pricing also helps smaller buyers start with carbon accounting and add energy or supplier modules later when their reporting needs expand. This pricing logic supports broader adoption in North America, Western Europe, and emerging Asia-Pacific, where SME buyers often want short deployment times and limited implementation risk.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Weak SME Data Discipline and Spreadsheet Dependence | -3.2% | Global, most acute in South and Southeast Asia, Southern Europe | Short term (≤ 2 years) |

| High Switch Friction From Fragmented Utility, ERP, and Asset Data | -2.6% | North America, EU, Asia-Pacific | Medium term (2-4 years) |

| Data Residency and Privacy Concerns in Regulated Verticals | -1.8% | EU, Middle East, Southeast Asia | Medium term (2-4 years) |

| Sustainability Budget Volatility in Price Sensitive Micro Enterprises | -1.4% | South America, Africa, South and Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Weak SME Data Discipline and Spreadsheet Dependence

Weak internal data discipline remains the most immediate brake on the SME green IT SaaS platform market, as many SMEs still store operational data in spreadsheets, PDFs, and disconnected systems. Sustainability platforms work best when utility, travel, procurement, and asset records are structured consistently, but many smaller firms lack that baseline. The VSME framework lowered the reporting burden for non-listed SMEs, but it did not solve the underlying problem of fragmented source data. This gap stretches onboarding timelines, reduces confidence in reported outputs, and can send users back to manual work after initial deployment. Vendors that can extract data from invoices, bills of lading, and meter readings with limited cleanup are better positioned to keep the SME green IT SaaS platform market moving in data-poor customer groups.

High Switch Friction From Fragmented Utility, ERP, and Asset Data

The SME green IT SaaS platform market also faces slower expansion when buyers must connect several utility portals, ERP systems, HR tools, and asset records before they can switch platforms. Integration work is costly for SMEs running older ERP systems or low-cost systems with limited API support. Sweep introduced an AWS Sustainability emissions connector in June 2026, demonstrating how vendor-built connectors can reduce some of this friction in cloud emissions reporting. Even so, each connector typically addresses only one data silo, so the full migration burden remains high for many customers. This raises customer acquisition costs for late entrants and can lock early buyers into their first usable platform, even when better functionality emerges later.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Services Growth Reflects Regulatory Complexity

Software accounted for 58.30% of the SME green IT SaaS platform market in 2025, maintaining the largest revenue pool through recurring SaaS subscriptions and scalable deployment. This part of the SME green IT SaaS platform market continues to win new projects because pre-built templates for VSME, CSRD, ISSB, and CDP reduce setup time for first-time users. Buyers also favor software-first rollouts when they want a clear operating system for data collection, emissions calculation, and recurring disclosure tasks. That pattern keeps core platforms at the center of vendor strategy even as surrounding service revenue expands.

Services are projected to expand at 22.67% CAGR through 2031, giving the segment the fastest pace in this part of the SME green IT SaaS platform market. The need for implementation support, managed reporting, and advisory services increases when SMEs must respond to multiple frameworks simultaneously. IFRS said its December 2025 amendments to IFRS S2 were intended to reduce the early Scope 3 burden, but companies still need support in translating the rules into operating practice. The SME sustainability software industry is shifting toward bundled offers that combine software access with domain expertise and partner delivery. Vendors that build certified service ecosystems can improve retention because customers are less willing to replace a platform once reporting processes and advisory support are integrated.

By Deployment Model: Hybrid Deployment Gains Ground in Regulated Settings

Cloud SaaS held 59.78% of the SME green IT SaaS platform market in 2025, showing that subscription delivery is now the default model for most new buyers. Its advantage rests on lower infrastructure burden, faster updates, and easier access for firms that do not maintain large internal IT teams. This position also reflects the way the SME green IT SaaS platform market aligns with broader SaaS buying habits in mid-market companies. For many SMEs, a cloud tool is the fastest route from spreadsheet-based tracking to repeatable reporting.

Hybrid deployment is forecast to grow at 20.42% CAGR through 2031, which makes it the fastest-growing model within the SME green IT SaaS platform market size for deployment choices. Growth is concentrated in healthcare, financial services, and public sector settings where privacy rules, internal control requirements, or data residency concerns limit full public cloud adoption. Microsoft expanded sustainability data connectivity in Dynamics 365 Business Central in 2026, and that kind of integration support makes mixed architecture more practical for smaller organizations.[3]Microsoft, “Dynamics 365 Business Central 2026 Wave 1 Sustainability APIs,” Microsoft On-premise systems keep a residual role where local storage remains the safer path for regulated operating data, including settings shaped by data localization rules in Saudi Arabia and Turkey. The SME sustainability software industry still favors vendors that can deliver one product stack across public cloud, private cloud, and local deployment without forcing customers into a full redesign.

By Application: Carbon Accounting Leads While Compliance Management Advances Fast

Carbon and environmental footprint management accounted for 31.92% of the market in 2025, making it the largest application block in the SME green IT SaaS platform market. This segment stays central because emissions measurement sits at the start of supplier reporting, investor disclosure, target setting, and internal tracking. Energy monitoring and optimization benefit from the same logic, as SMEs want operating data that supports both cost control and Scope 2 reporting. The SME green IT SaaS platform market keeps this application at the forefront because most customers still enter through carbon accounting before expanding usage.

ESG reporting and compliance management is projected to expand at a 21.77% CAGR through 2031, marking the fastest application growth in the SME green IT SaaS platform market for software use cases. The pace reflects the spread of overlapping frameworks that require a single database to serve multiple reporting outputs. ISO and IEC published ISO/IEC TS 19770-13:2026 to guide the link between IT asset management and ESG objectives, supporting the rise of lifecycle and circularity tools within broader reporting programs.[4]ISO/IEC, “ISO/IEC TS 19770-13:2026,” ISO EcoVadis also said in May 2026 that USD 2.5 trillion in spend is linked to sustainability risk intelligence, which strengthens the case for supplier sustainability and value-chain modules. As a result, vendors are extending beyond carbon ledgers into multi-framework disclosure, supplier engagement, and operational traceability.

By End-User Industry: IT and Telecom Leads While Healthcare Rises Fast

IT and telecom accounted for 28.64% of the 2025 market, giving it the largest vertical position in the SME green IT SaaS platform market. Large technology buyers often need supplier emissions data quickly, and that pulls smaller vendors into more formal reporting routines. The sector also has better software readiness than many other verticals, so deployment cycles are often shorter. This mix of reporting pressure and digital maturity helps keep IT and telecom at the top of the SME green IT SaaS platform market across verticals.

Healthcare and life sciences are projected to grow at a 24.43% CAGR through 2031, making it the fastest-growing vertical driven by end-user demand. Growth comes from pressure across pharmaceutical supply chains, medical device sourcing, reimbursement models, and investor scrutiny. Manufacturing, BFSI, and retail and e-commerce remain important adjacent users because traceability, financing of emissions, and supplier reporting create steady software demand. Public sector uptake is also widening, where tender rules require clearer sustainability disclosures from bidders. The SME sustainability software industry is broadening from digital-native adopters into regulated, documentation-heavy customer groups.

Geography Analysis

North America held 37.64% of the SME green IT SaaS platform market share in 2025, making it the largest regional market. The region maintains its lead in 2026 because mid-market firms are already accustomed to SaaS procurement, and climate disclosure pressure extends through state rules such as California SB 253 and Canadian disclosure requirements, as well as enterprise supply chains. A large installed base of SAP, Oracle, and Microsoft environments also gives the SME green IT SaaS platform market a ready path for embedded sustainability modules and faster cross-sell. That combination makes North America a demanding yet attractive proving ground for vendors seeking shorter implementation cycles and higher feature expectations.

Europe remained the second-largest regional position in the SME green IT SaaS platform market in 2025, supported by the strongest concentration of formal disclosure rules. The EU narrowed the mandatory CSRD scope in 2026, yet the SME green IT SaaS platform market still benefits, as large reporting companies continue to request supplier data, and the VSME framework provides a practical entry point for non-listed SMEs. Germany and France remain core demand centers, and the United Kingdom also contributes through broad corporate reporting and supply-chain compliance activity. European buyers continue to reward vendors that pre-configure ESRS and VSME workflows because faster time to first report matters more when internal sustainability teams are small.

Asia-Pacific is projected to grow at a 23.17% CAGR through 2031, making it the fastest-growing region in the SME green IT Saas platform market by geography. Growth comes from disclosure rollouts in Japan, China, and India, which are pushing listed companies and their suppliers toward more formal ESG data collection. The SME green IT Saas platform market in Japan also has a strong local layer of competition, as domestic vendors have added reporting features that meet local language and regulatory needs. South America is still at an earlier adoption stage, but Brazil stands out as the clearest regional opening as climate disclosure rules move forward for listed companies. The Middle East and Africa remain smaller in absolute terms, yet Saudi Arabia, the United Arab Emirates, and South Africa provide a base for longer-term expansion as national disclosure agendas and established reporting practices deepen.

Competitive Landscape

The SME green IT SaaS platform market was moderately fragmented in 2026, with no single vendor holding a decisive position across all customer groups. Purpose-built platforms such as Greenly, Normative, Sweep, Persefoni, and Watershed compete on carbon calculation, framework coverage, and automation depth, while larger vendors such as IBM, SAP, Microsoft, Oracle, Salesforce, Schneider Electric, and Siemens compete through installed software relationships. This split keeps the SME green IT SaaS platform market active at both the specialist layer and the enterprise integration layer. It also means smaller vendors must defend differentiation even when larger software companies package sustainability functions into broader business systems.

AI capability is now one of the clearest points of competition in the SME green IT SaaS platform market because buyers want fewer manual steps in data collection, mapping, and reporting. SAP said its Footprint Optimization Agent can reduce simulation time from 1 day to 20 minutes, which shows how enterprise vendors are using automation to compress work that once required specialist teams. Persefoni launched its Analytics Agent in May 2026 so finance, sustainability, and compliance teams can query emissions data in plain language, which pushes the SME green IT Saas platform market further toward self-service analysis. IBM also lowered adoption friction by bringing Envizi emissions calculations into Excel in January 2026, which matters in a customer base that still relies heavily on spreadsheets.[5]IBM, “Envizi Emissions Calculations Excel Add-In,” IBM These moves raise the feature floor for every vendor, and a clear gap still remains in lightweight tools for micro enterprises that need simple onboarding and lower price points.

Partnerships and acquisitions are also reshaping the SME green IT SaaS platform market as vendors try to add services, integrations, and specialized capability faster than they can build them internally. Sweep and Arcadis announced a global partnership in May 2026, and EcoVadis linked supplier carbon data with both Workiva and Watershed in 2026, which shows how the market is moving toward connected reporting ecosystems. Green Project Technologies absorbed the Emitwise platform in July 2025, so Emitwise no longer stands as an independent competitive line in the SME green IT SaaS platform market. The market rewards vendors that can combine software, advisory reach, and integration depth without making deployment too heavy for SMEs.

SME Green IT SaaS Platform Industry Leaders

Greenly SAS

Normative AB

Plan A Earth GmbH

Sweep SAS

Persefoni, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Sweep, an AWS ISV-Accelerate partner, launched a complete cloud emissions measurement solution based on the AWS Sustainability service, enabling enterprise customers to automatically consolidate cloud emissions data with their Scope 1, 2, and 3 reporting within Sweep's platform. The connector is available to all Sweep customers, removing a significant manual data-collection step from cloud-heavy SME operations.

- May 2026: SAP announced new sustainability AI agents, the Regulatory Readiness Agent and the Footprint Optimization Agent, to be made generally available by the end of 2026 through SAP Sustainability Control Tower. The Footprint Optimization Agent is projected to reduce scenario simulation time from approximately 1 day to approximately 20 minutes, making decarbonization planning accessible to sustainability teams without dedicated data-science resources.

- May 2026: Persefoni unveiled its Analytics Agent, an agentic AI tool allowing sustainability, finance, and compliance teams to query emissions data in plain language via Persefoni's CO2e Activity Ledger. Persefoni reports supporting more than 500 enterprise customers and 9,000+ organizations, having raised a cumulative USD 179 million in institutional investment.

- May 2026: EcoVadis and Workiva announced a strategic partnership to connect EcoVadis's primary supplier carbon data with Workiva's audit-ready reporting platform. The collaboration expands EcoVadis's Carbon Data Network, enabling mutual customers to replace industry averages with granular supplier emissions data in their Scope 3 disclosures.

Global SME Green IT SaaS Platform Market Report Scope

The SME Green IT SaaS Platform refers to cloud-based software solutions specifically designed for small and medium enterprises (SMEs) to streamline and enhance their IT sustainability initiatives. These platforms enable SMEs to minimize energy consumption, monitor carbon emissions, comply with ESG regulations, and seamlessly integrate sustainability data into routine business processes. Delivered as scalable, subscription-based SaaS tools, they reduce ownership costs and simplify implementation.

The SME Green IT SaaS Platform Market Report is Segmented by Solution Type (Software, and Services), Deployment Model (Cloud SaaS, Hybrid, and On-Premise), Application (Carbon and Environmental Footprint Management, Energy Monitoring and Optimization, ESG Reporting and Compliance Management, IT Asset Lifecycle and Circularity Management, and Supplier Sustainability and Value Chain Management), End-User Industry (IT and Telecom, BFSI, Manufacturing, Retail and E-Commerce, Healthcare and Life Sciences, Government and Public Sector, Energy and Utilities, Professional Services, and Other End-user Industries), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud SaaS |

| Hybrid |

| On-Premise |

| Carbon and Environmental Footprint Management |

| Energy Monitoring and Optimization |

| ESG Reporting and Compliance Management |

| IT Asset Lifecycle and Circularity Management |

| Supplier Sustainability and Value Chain Management |

| IT and Telecom |

| BFSI |

| Manufacturing |

| Retail and E-Commerce |

| Healthcare and Life Sciences |

| Government and Public Sector |

| Energy and Utilities |

| Professional Services |

| Other End-user Industries |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Turkey |

| Saudi Arabia | |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Solution Type | Software | |

| Services | ||

| By Deployment Model | Cloud SaaS | |

| Hybrid | ||

| On-Premise | ||

| By Application | Carbon and Environmental Footprint Management | |

| Energy Monitoring and Optimization | ||

| ESG Reporting and Compliance Management | ||

| IT Asset Lifecycle and Circularity Management | ||

| Supplier Sustainability and Value Chain Management | ||

| By End-User Industry | IT and Telecom | |

| BFSI | ||

| Manufacturing | ||

| Retail and E-Commerce | ||

| Healthcare and Life Sciences | ||

| Government and Public Sector | ||

| Energy and Utilities | ||

| Professional Services | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Turkey | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast size of the SME green IT SaaS platform market space?

The SME green IT Saas platform market size was USD 1.13 billion in 2025, reached USD 1.36 billion in 2026, and is forecast to reach USD 3.36 billion by 2031 at a 19.83% CAGR.

Which region leads adoption of SME green IT SaaS platform?

North America led with 37.64% share in 2025, supported by mature SaaS buying behavior, embedded ERP relationships, and climate disclosure pressure across supply chains.

Which region is expanding the fastest through 2031?

Asia-Pacific is projected to grow at 23.17% CAGR through 2031 as disclosure frameworks in Japan, China, and India push larger companies and suppliers toward structured ESG data collection.

Which application area is growing the fastest?

ESG reporting and compliance management is projected to grow at 21.77% CAGR, reflecting the need to serve several reporting frameworks from one data base.

Why are services growing faster than software licenses alone?

Services are forecast to grow at 22.67% CAGR because many SMEs need implementation help, managed reporting, and advisory support as rules and customer requests become more complex.

Which end-user group shows the strongest momentum?

Healthcare and life sciences is projected to grow at 24.43% CAGR as supply-chain reporting, sourcing scrutiny, and documentation-heavy compliance demands rise together.

Page last updated on: