Green IT Asset Management (ITAM) Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

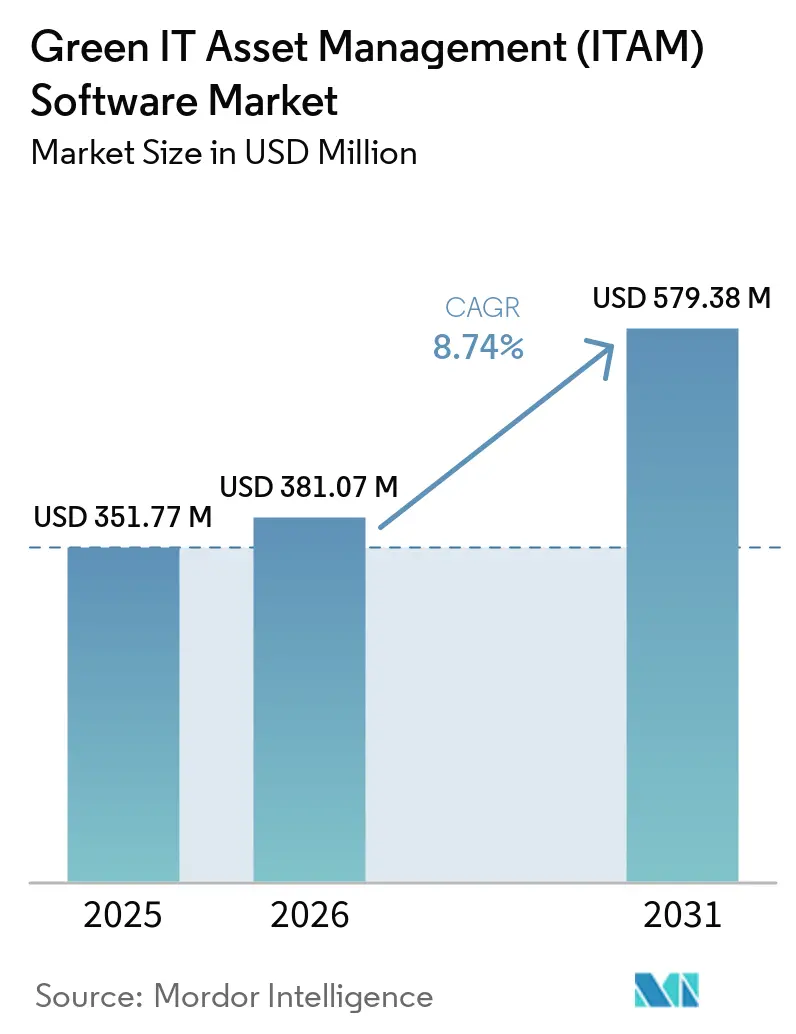

| Market Size (2026) | USD 381.07 Million |

| Market Size (2031) | USD 579.38 Million |

| Growth Rate (2026 - 2031) | 8.74% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Green IT Asset Management (ITAM) Software Market Analysis by Mordor Intelligence

The Green IT Asset Management (ITAM) Software Market size is expected to increase from USD 351.77 million in 2025 to USD 381.07 million in 2026 and reach USD 579.38 million by 2031, growing at a CAGR of 8.74% over 2026-2031. Growth is being shaped by the combination of sustainability disclosure pressure and the steady rise of hybrid cloud and SaaS environments, which have made static asset inventories less useful for enterprise control. Enterprises now want a broader governance layer that can connect software visibility, asset lifecycle records, carbon tracking, and audit readiness into a single operating model. This shift is lifting contract values and extending deal cycles because buyers are evaluating these platforms across finance, compliance, and sustainability workflows rather than only IT operations. Competitive positioning is also changing, as vendors that cannot unify SaaS, cloud, and on-premises data are facing greater pressure from buyers who want fewer overlapping tools. A large part of the remaining opportunity sits in first-time adoption, carbon-aware lifecycle management, and mid-market deployments, where automated discovery is removing earlier infrastructure and staffing barriers.

Key Report Takeaways

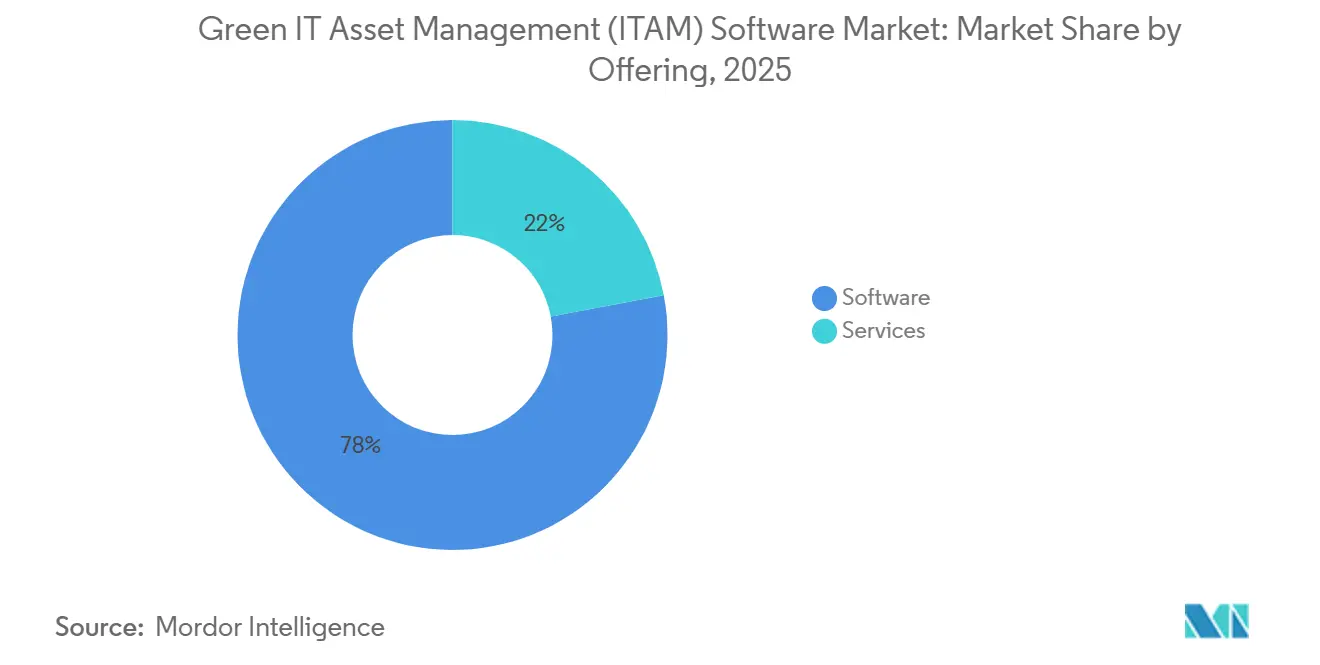

- By offering, software accounted for 77.96% of Green IT Asset Management (ITAM) Software Market revenue in 2025, while services are projected to expand at a 11.19% CAGR through 2031.

- By deployment mode, cloud accounted for 62.03% of the market share in 2025, while hybrid is expected to record the fastest CAGR of 12.13% through 2031.

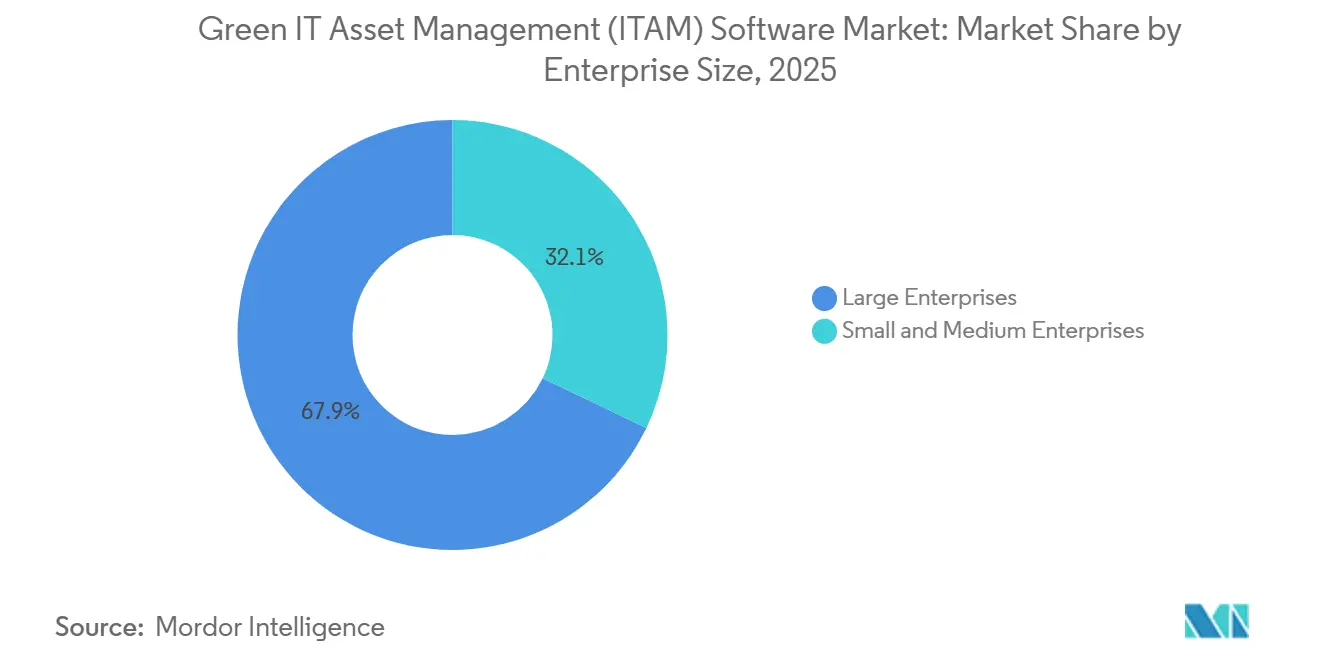

- By enterprise size, large enterprises held 67.89% share in 2025, while SMEs are projected to grow at an 11.78% CAGR through 2031.

- By end-use industry, IT and Telecom accounted for 24.12% share in 2025, while Energy and Utilities are projected to expand at a 13.81% CAGR through 2031.

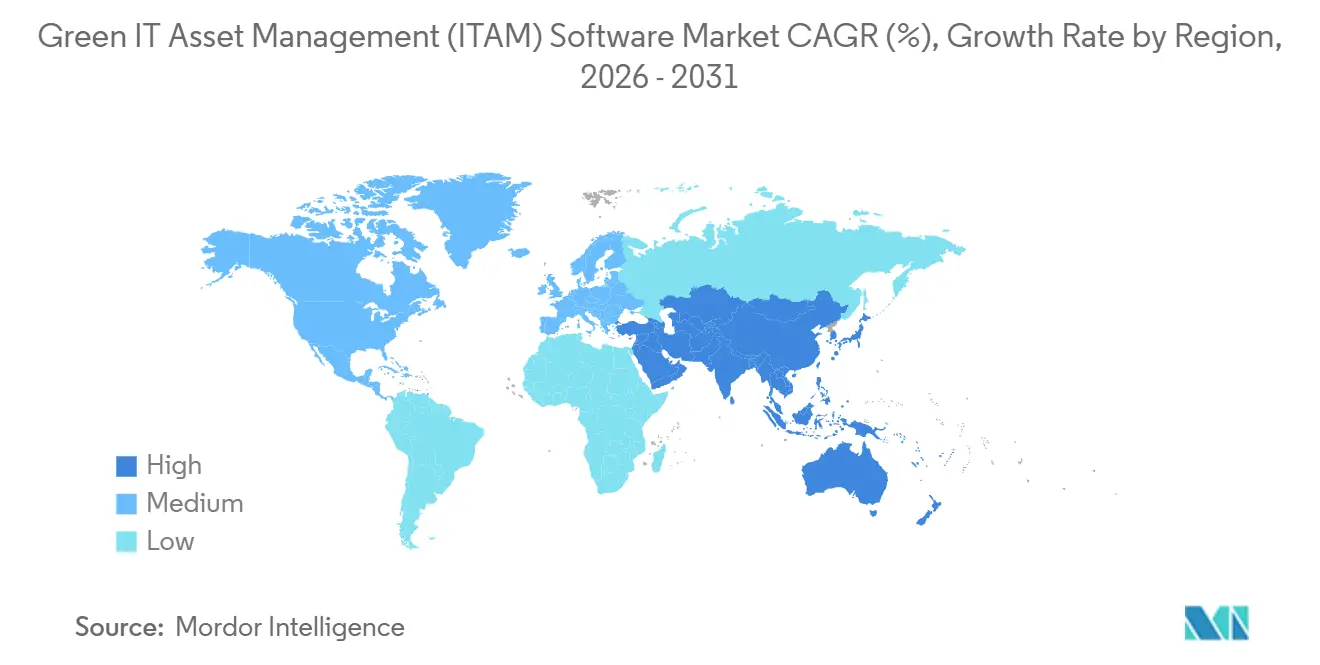

- By geography, North America held 37.02% of the Green IT Asset Management (ITAM) Software Market share in 2025, while Asia-Pacific is projected to advance at a 12.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Green IT Asset Management (ITAM) Software Market Trends and Insights

Drivers Impact Analys*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ESG-Linked IT Carbon Accounting Requirements | +2.0% | Global, with highest compliance intensity in Europe, expanding to North America and Asia-Pacific | Medium term (2-4 years) |

| AI-Driven Asset Discovery and License Optimization | +1.7% | Global, with highest early adoption in North America and Western Europe | Short term (≤ 2 years) |

| Rising Software and SaaS Waste Reduction Mandates | +1.4% | Global, with budget pressure strongest in North America, the United Kingdom, and Germany | Short term (≤ 2 years) |

| Hybrid Cloud and Multi-Environment Visibility Needs | +1.1% | Global, strongest in North America and Asia-Pacific, with spillover to the Middle East and Africa | Short term (≤ 2 years) |

| FinOps and SAM Convergence for Technology Spend Governance | +0.9% | North America and Europe, with emerging adoption in Asia-Pacific | Medium term (2-4 years) |

| Software Audit Exposure and True-Up Avoidance Pressure | +0.6% | North America and Western Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

ESG-Linked IT Carbon Accounting Requirements

Mandatory sustainability reporting has moved the Green IT Asset Management (ITAM) Software Market closer to compliance infrastructure than simple cost control. Enterprises are being asked to maintain clearer records on hardware fleets, SaaS subscriptions, utilization patterns, refresh cycles, and reuse activity when they support broader environmental reporting. Static spreadsheets are no longer enough for that task because they cannot provide the asset-level continuity that regulated organizations now expect from internal reporting systems. Alliance Green IT reported in 2025 that 47% of organizations already used ITAM processes to support ecological objectives, indicating that environmental use cases were becoming mainstream before adoption widened further.[1]Alliance Green IT, “Baromètre Green IT 2025,” Alliance Green IT, alliancegreenit.org GLPI also highlighted the growing role of carbon-focused asset lifecycle management in 2025, which supports the direction toward platforms that combine inventory control with environmental measurement. This is pushing the Green IT Asset Management (ITAM) Software Market toward vendors that can demonstrate reliable device-level records and credible lifecycle workflows, rather than just license reconciliation.

AI-Driven Asset Discovery and License Optimization

AI is changing the operating model of the Green IT Asset Management (ITAM) Software Market because manual asset governance can no longer keep pace with modern software estates. Flexera stated in its 2025 State of ITAM Report that its Technopedia catalog covered more than 2.1 million software use rights, underscoring the scale of the recognition burden for enterprise discovery and normalization.[2]Flexera, “Flexera 2025 State of ITAM Report,” Flexera, info.flexera.com Xensam reported in December 2024 that its application library had reached 500,000 titles, including a 50% year-over-year increase in recognized SaaS applications, reflecting how quickly software visibility needs are expanding. Flexera also found that only 43% of enterprises felt confident in complete IT estate visibility in 2025, down from 47% the prior year, indicating that complexity is still growing faster than many teams can monitor with traditional methods. As a result, the Green IT Asset Management (ITAM) Software Market is placing greater emphasis on AI-led discovery, as it can surface unauthorized applications, idle licenses, and shadow AI activity with less manual effort. That shift is helping AI-native vendors justify higher pricing because buyers now see automated discovery as a basic operating requirement rather than a premium feature.

Rising Software and SaaS Waste Reduction Mandates

Waste reduction has become a stronger purchase trigger in the Green IT Asset Management (ITAM) Software Market because software and SaaS spending is now reviewed more closely at the finance level. Organizations want clearer visibility into unused entitlements, overlapping tools, renewal timing, and application sprawl so they can connect technology budgets to measurable governance outcomes. The FinOps Foundation reported in 2026 that 90% of FinOps practitioners managed SaaS as part of their operational remit, indicating that SaaS oversight has become part of standard spend management practice rather than a separate niche activity.[3]FinOps Foundation, “State of FinOps 2026 Report,” FinOps Foundation, data.finops.org Flexera reinforced this direction in July 2025, launching Flexera One SaaS Management with a focus on SaaS discovery, optimization, and shadow AI visibility in enterprise environments. This is positioning the Green IT Asset Management (ITAM) Software Market as a governance layer that can translate software waste into recovered spend and better renewal decisions. It also raises procurement priority because CFO-led accountability programs increasingly treat software waste as a continuing control issue rather than a one-time clean-up project.

Hybrid Cloud and Multi-Environment Visibility Needs

Hybrid estates have become one of the clearest demand drivers in the Green IT Asset Management (ITAM) Software Market because large organizations rarely operate in a single environment anymore. Buyers need a single view across on-premises infrastructure, public clouds, and expanding SaaS portfolios to maintain dependable asset, entitlement, and usage records. Flexera reported in 2025 that 76% of organizations had visibility into on-premises hardware, while only 50% felt confident in SaaS coverage, and only 27% could track bring-your-own-license positions in cloud environments. Lansweeper also emphasized broader asset visibility across network and cloud environments in its 2025 platform update, highlighting how the discovery architecture is being redesigned for hybrid operating conditions. The Green IT Asset Management (ITAM) Software Market is therefore moving toward platforms that connect cloud intelligence with on-premises entitlement records instead of treating those layers separately. This trend is also narrowing the gap between ITAM and FinOps, as both teams now rely on improved hybrid licensing and usage visibility to support spending decisions.[4]

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Poor IT Asset Data Quality and Normalization Gaps | -1.3% | Global, with highest severity in South America, the Middle East and Africa, and South and Southeast Asia | Long term (≥ 4 years) |

| Integration Complexity Across Legacy, Cloud, and SaaS Tools | -1.0% | Global, especially in North America and Europe with large incumbent installations | Medium term (2-4 years) |

| Shortage of Skilled ITAM and Software Licensing Specialists | -0.7% | Global, with highest severity in Asia-Pacific and South America | Long term (≥ 4 years) |

| Privacy Concerns Around Continuous Endpoint and Telemetry Collection | -0.4% | Europe and other markets with personal data protection frameworks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Poor Asset Data Quality Limits Reporting Accuracy

The largest operating challenge in the Green IT Asset Management (ITAM) Software Market is still poor asset data quality. Lansweeper noted in 2025 that automated inventory is important because manual records quickly lose reliability in dynamic environments, weakening lifecycle, utilization, and compliance records over time. Naming gaps across procurement systems, CMDB tools, and endpoint records still result in duplicate records and inconsistent manufacturer identities, which in turn weaken carbon attribution and license positions. That problem becomes more serious when firms try to connect energy, device, and cloud data to formal sustainability reporting. The Green IT Asset Management (ITAM) Software Market, therefore, still depends on strong normalization engines, because without them, even good discovery coverage does not produce reporting-grade output.[4]Lansweeper, “Automating IT Asset Inventory for Large Networks,” Lansweeper, lansweeper.com

Complex Integrations Delay Value Realization

The Green IT Asset Management (ITAM) Software Market also faces slower adoption when integration work becomes too large. A typical enterprise may keep procurement data in ERP software, endpoint inventory in device management tools, cloud spend in hyperscaler dashboards, and SaaS activity in identity or application systems, and those records rarely line up cleanly. The FinOps Foundation said in its 2026 framework that ITAM, IT financial management, sustainability, and security are converging disciplines, which means fragmented tool stacks now create broader control gaps than before. Green IT programs add another layer, as cloud carbon data often arrives in provider-specific formats that still need translation into usable reporting categories. That leaves the Green IT Asset Management (ITAM) Software Market with a long implementation cycle in many large accounts, which is one reason services and managed delivery continue to grow.[4]Xensam, “Xensam Launches DataBridge,” Xensam, xensam.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Scale Dominates, But Services Complexity Is Rising

Services are projected to expand at a 11.19% CAGR from 2026 to 2031, making it the fastest-growing segment within the Green IT Asset Management (ITAM) Software Market. That growth reflects the rising workload tied to data normalization, discovery design, workflow configuration, and ongoing optimization across multi-environment estates. Enterprises are finding that stronger AI capabilities do not, by themselves, reduce deployment effort, because AI still depends on clean integrations, rule tuning, and policy design. Service demand is also rising as more buyers seek to combine ITAM, SaaS management, and spend governance into a single operating framework. This is giving implementation partners and vendor-led service teams a larger role in enterprise rollouts.

Software held a 77.96% revenue share in 2025, making it the commercial anchor of the Green IT Asset Management (ITAM) Software Market. Buyers still prefer continuous, real-time discovery platforms over periodic review engagements because the platform model closes visibility gaps between formal assessments. The FinOps Foundation and ITAM Forum announced a strategic partnership in June 2025 that included working groups, shared event tracks, and a FinOps for SaaS training course, which supports the rise of a broader service ecosystem around converged deployments. Vendors that bundle software with structured onboarding and managed optimization are likely to win more mid-market business because procurement teams want clearer ownership over implementation outcomes. The Green IT Asset Management (ITAM) Software Industry is therefore keeping software as the base revenue layer while services expand account value and reduce execution risk.

By Deployment Mode: Hybrid Redefines Visibility Architecture

Hybrid deployment is projected to grow at a 12.13% CAGR from 2026 to 2031, making it the fastest-growing deployment model in the Green IT Asset Management (ITAM) Software Market. This pattern shows that enterprise architecture is being shaped by coexistence rather than standardization, as organizations still need different operating models across varying security, sovereignty, and infrastructure conditions. Hybrid designs let companies keep on-premises discovery in controlled environments while extending analytics and reporting through cloud services for broader governance. That structure fits global organizations that cannot shift every workload or asset category into a single environment. It also enhances the value of asset intelligence by enabling the interpretation of cloud and on-premises records together.

Cloud accounted for 62.03% of the Green IT Asset Management (ITAM) Software Market in 2025, underscoring buyers' preference for SaaS-delivered discovery and faster feature updates. Cloud scale also reflects the appeal of lower infrastructure overhead and easier administration for distributed teams. On-premises deployments continue to matter in banking, government, and defense, where data sovereignty or air-gapped environments limit the use of external telemetry models. Flexera reported in 2025 that only 27% of enterprises had meaningful visibility into bring-your-own-license positions in cloud environments, which helps explain why hybrid governance remains a central buying requirement. The Green IT Asset Management (ITAM) Software Industry is therefore moving toward deployment models that integrate cloud usage, entitlement records, and endpoint data within a single governance layer rather than across isolated tools.

By Enterprise Size: Large Enterprises Lead, SMEs Narrow The Gap

SMEs are projected to grow at a 11.78% CAGR from 2026 to 2031, making them the fastest-growing segment in the Green IT Asset Management (ITAM) Software Market. Cloud-native delivery has lowered the infrastructure and staffing barriers that once kept advanced ITAM tools out of reach for smaller organizations. Many SMEs are now adopting these platforms first as spend intelligence systems that can identify unused subscriptions and improve renewal discipline. That purchase logic is practical because smaller teams often feel the effect of software waste more quickly in annual budget cycles. It is also broadening adoption beyond the older model, where ITAM was justified mainly by exposure to publisher audits.

Large enterprises held a 67.89% share in 2025, making them the largest customer group in the Green IT Asset Management (ITAM) Software Market. Their broader publisher mix, deeper cloud footprints, and larger software estates create much higher financial exposure when records are incomplete or poorly reconciled. Flexera reported in 2025 that 45% of enterprises paid more than USD 1 million in audit fines over the prior 3 years, underscoring how material that exposure can be in large and complex environments. Entry-level options from vendors such as Freshworks and InvGate are helping lean teams enter the category with less setup burden, while AI-based recommendations are shortening time-to-value for smaller deployments. The Green IT Asset Management (ITAM) Software Market is therefore expanding beyond its traditional enterprise base, even though large organizations still generate most of the current revenue.

By End-Use Industry: Energy And Utilities Drives Fastest Expansion

Energy and Utilities is projected to expand at a 13.81% CAGR from 2026 to 2031, which makes it the fastest-growing end-use segment in the Green IT Asset Management (ITAM) Software Market. Utilities are digitizing grid operations, deploying more connected field assets, and bringing operational technology into broader governance programs. That creates demand for stronger lifecycle control because software entitlements, device usage, cyber exposure, and environmental reporting can no longer be managed in separate workflows. The segment is also gaining momentum because critical infrastructure operators increasingly need clearer visibility across IT, OT, and IoT environments. This makes Energy and Utilities one of the clearest long-run expansion paths for vendors that can support both operational complexity and compliance depth.

IT and Telecom accounted for 24.12% of the Green IT Asset Management (ITAM) Software Market share in 2025, making it the largest end-use segment. The segment stayed ahead because licensing complexity, multi-cloud architecture scale, and software vendor diversity remain especially high in technology-intensive organizations. BFSI and the Government and Public Sector followed as meaningful adoption groups because regulatory scrutiny and public-sector modernization continue to support asset governance spending. Industrial Manufacturing, Oil and Gas, Retail and E-Commerce, and Construction and Infrastructure are also growing demand centers as ERP compliance, connected asset tracking, and SaaS sprawl become harder to manage through manual controls. The Green IT Asset Management (ITAM) Software Market is therefore broadening across verticals, even while IT and Telecom remain the largest revenue base, and Energy and Utilities post the strongest forward growth.

Geography Analysis

North America held 37.02% of the Green IT Asset Management (ITAM) Software Market share in 2025, making it the largest regional contributor. The United States remains the center of demand because enterprise digitization is deep, FinOps practices are mature, and software audit activity remains high enough to support a clear return on investment. Flexera reported in 2025 that Microsoft, IBM, and SAP led audit programs reaching 50%, 37%, and 32% of surveyed organizations, which helps explain why proactive asset governance remains commercially attractive in the region. Canada is adding demand through public-sector digital modernization, while Mexico is benefiting from nearshoring-led enterprise IT expansion. These conditions keep North America the most mature region in the Green IT Asset Management (ITAM) Software Market.

Europe remains a core region for the Green IT Asset Management (ITAM) Software Market because sustainability reporting needs are pulling IT governance and environmental accountability closer together. Large enterprises increasingly need asset records that can support Scope 3 measurement, lifecycle evidence, and more disciplined hardware management inside broader disclosure frameworks. Alliance Green IT found in 2025 that 47% of organizations already used ITAM processes to support ecological objectives, which reflects a stronger environmental use case than in many other regions. This is making Europe one of the most important regions for carbon-aware lifecycle management and the adoption of related workflows.

The Asia-Pacific Green IT Asset Management (ITAM) Software Market is projected to expand at a 12.92% CAGR from 2026 to 2031, making it the fastest-growing regional segment. Organizations across China, India, Japan, South Korea, and Australia are managing more complex hybrid estates after rapid cloud migration and broader software portfolio growth. India is becoming especially active because large IT services firms and global capability centers need better control over cloud-native workloads and significant SAP and Oracle footprints. Japan is also opening more first-time deployment opportunities as enterprise cloud adoption expands under digital transformation programs. ServiceNow and Lenovo announced an expanded strategic agreement in May 2026 across Australia, New Zealand, Hong Kong, Singapore, and Ireland, which shows how vendors are building more region-specific operating models for international enterprise buyers. South America is led by Brazil, where sustainability alignment and SaaS adoption are supporting demand. The Middle East and Africa are expanding from a smaller base, with Saudi Arabia and the United Arab Emirates leading through national digitization programs and stronger investment in enterprise technology governance.

Competitive Landscape

The Green IT Asset Management (ITAM) Software Market remains fragmented, with a visible first tier of global platform vendors and a second tier of focused specialists competing on discovery depth, software intelligence, and lifecycle visibility. ServiceNow, Flexera, IBM, and Ivanti form the broad platform layer, while Xensam, Lansweeper, USU Software, and Certero compete through narrower product focus and faster feature specialization. The main dividing line is now the ability to normalize data across SaaS, cloud, and on-premises environments because buyers want one operating view instead of several partial records. Vendors that cannot unify those layers face a higher risk of displacement as procurement teams consolidate around broader technology spend governance platforms.

The Green IT Asset Management (ITAM) Software Market is also showing a strong pattern of expansion through acquisition and adjacent capability build-out. Flexera acquired ProsperOps and Chaos Genius in January 2026 to extend its FinOps position into agentic AI-enabled cost optimization for cloud and data workloads. ServiceNow completed its Armis acquisition in 2026 to link AI-powered cyber asset intelligence with ITAM and security workflows across IT, OT, and IoT environments. These moves show that competition is no longer limited to license reconciliation because visibility, operational risk, and AI spend governance are becoming part of the same buying conversation. They also raise the strategic value of platforms that can connect asset data to remediation, security, and financial controls.

Specialist vendors are responding through product-led differentiation inside the Green IT Asset Management (ITAM) Software Market. Xensam launched DataBridge in May 2025 to synchronize software intelligence with ServiceNow CMDBs via standardized connectors, reducing the integration burden for shared enterprise accounts. Lansweeper introduced Lens AI in 2025 to let users query asset inventories in plain language, which lowers the analysis burden for teams without strong data engineering support. Flexera also launched AI Cost Management and Data Explorer in 2026, which pushed the Green IT Asset Management (ITAM) Software Market further into AI spend governance and natural-language access to asset intelligence. White-space opportunities remain strongest in carbon-aware device retirement guidance and in SME-focused subscription bundles tied to software portfolio size rather than rigid seat-based pricing.

Green IT Asset Management (ITAM) Software Industry Leaders

ServiceNow, Inc.

Flexera Software LLC

IBM Corporation

BMC Software, Inc.

Ivanti, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: ManageEngine, a division of Zoho Corporation, announced the rollout of Zia Agents across its digital enterprise management suite on May 21, 2026, enabling autonomous AI execution across IT service management and ITAM workflows without human intervention. The launch marked a shift from AI-assisted to fully autonomous IT operations and extended cross-product asset intelligence without requiring custom integration overhead.

- April 2026: ISO and IEC published ISO/IEC TS 19770-13:2026 on April 12, 2026, providing the first dedicated international guidance for incorporating sustainability aspects into IT asset management systems. The specification aligned ITAM with ISO 14001, ISO 26000, ISO 50001, and the GHG Protocol, establishing a shared compliance target that enterprises can use to structure vendor evaluations and vendors can align product roadmaps to.

- April 2026: The Green Software Foundation published a white paper on March 31, 2026, mapping the Software Carbon Intensity standard under ISO/IEC 21031:2024 to EU CSRD ESRS E1 reporting requirements. The paper provided European organizations with a four-phase framework for integrating software emissions data into auditable disclosures, with Accenture, Cisco, Google, Microsoft, NTT DATA, Siemens, and UBS as steering members.

- January 2026: Flexera released carbon emissions forecasting as part of Flexera One Cloud Sustainability, introducing predictive carbon budgeting, a Google Cloud Carbon Emissions dashboard, Azure subscription-level carbon context, and Power BI custom sustainability reports. The release enabled cloud sustainability teams to forecast and manage emissions with the same analytical rigor applied to cloud spend, a capability directly aligned with ESRS E1 auditable reporting requirements.

Global Green IT Asset Management (ITAM) Software Market Report Scope

The Green IT Asset Management (ITAM) Software market refers to platforms and services that enable organizations to manage IT assets including hardware, software, and SaaS application through a sustainability-focused lens. These solutions provide capabilities such as hardware lifecycle management, software license optimization, SaaS usage monitoring, and sustainability modules that track energy consumption, carbon footprint, and end-of-life recycling or disposal. By embedding environmental intelligence into IT asset management, these platforms help enterprises reduce costs, extend asset lifecycles, minimize e-waste, and align IT operations with ESG and decarbonization goals.

The Green IT Asset Management (ITAM) Software market report is segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), End-Use Industry (IT and Telecom, BFSI, Industrial Manufacturing, Energy and Utilities, Oil and Gas, Retail and E-Commerce, Construction and Infrastructure, Government and Public Sector), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| IT and Telecom |

| BFSI |

| Industrial Manufacturing |

| Energy and Utilities |

| Oil and Gas |

| Retail and E-Commerce |

| Construction and Infrastructure |

| Government and Public Sector |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By offering | Software | ||

| Services | |||

| By Deployment Mode | Cloud | ||

| On-Premises | |||

| Hybrid | |||

| By Enterprise Size | Large Enterprises | ||

| Small and Medium Enterprises | |||

| By End-Use Industry | IT and Telecom | ||

| BFSI | |||

| Industrial Manufacturing | |||

| Energy and Utilities | |||

| Oil and Gas | |||

| Retail and E-Commerce | |||

| Construction and Infrastructure | |||

| Government and Public Sector | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the size of the Green IT Asset Management (ITAM) Software Market in 2026?

The Green IT Asset Management (ITAM) Software Market stands at USD 381.07 million in 2026 and is forecast to reach USD 579.38 million by 2031 at a CAGR of 8.74%.

What is driving demand for Green IT Asset Management (ITAM) Software solutions?

Demand is being supported by sustainability disclosure pressure, software and SaaS waste control, AI-led discovery, and the need for clearer visibility across hybrid environments.

Which region currently leads adoption of Green IT Asset Management (ITAM) Software?

North America led with 37.02% share in 2025 because of deep enterprise digitization, stronger FinOps maturity, and high software audit exposure.

Which region is growing the fastest through 2031?

Asia-Pacific is projected to grow at a 12.92% CAGR from 2026 to 2031 as enterprises manage more complex hybrid estates after rapid cloud migration.

Which deployment model is most widely used in this space?

Cloud led with 62.03% share in 2025, while hybrid is projected to grow faster because buyers want one governance layer across cloud, SaaS, and on-premises assets.

Which end-use segment offers the strongest growth outlook?

Energy and Utilities is projected to expand at a 13.81% CAGR through 2031 because grid digitization, connected assets, and converging compliance needs are lifting lifecycle governance demand.

Page last updated on: