South Africa Green IT Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

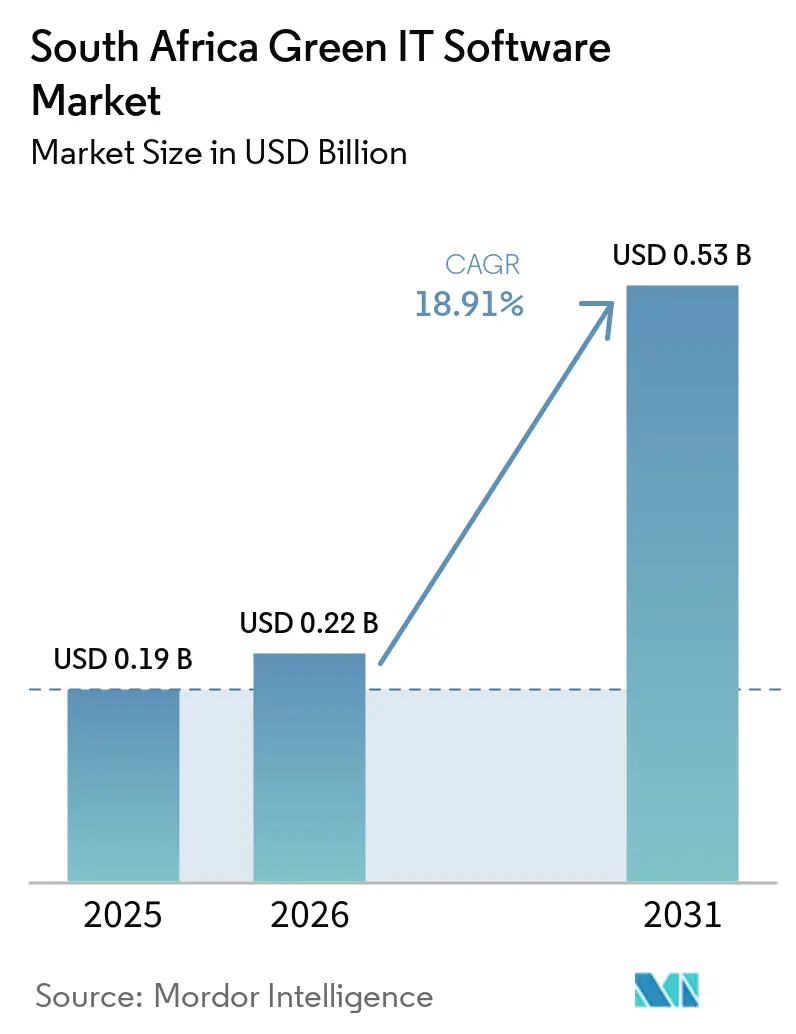

| Base Year Market Size (2025) | USD 0.19 Billion |

| Market Size (2026) | USD 0.22 Billion |

| Market Size (2031) | USD 0.53 Billion |

| Growth Rate (2026 - 2031) | 18.91% CAGR |

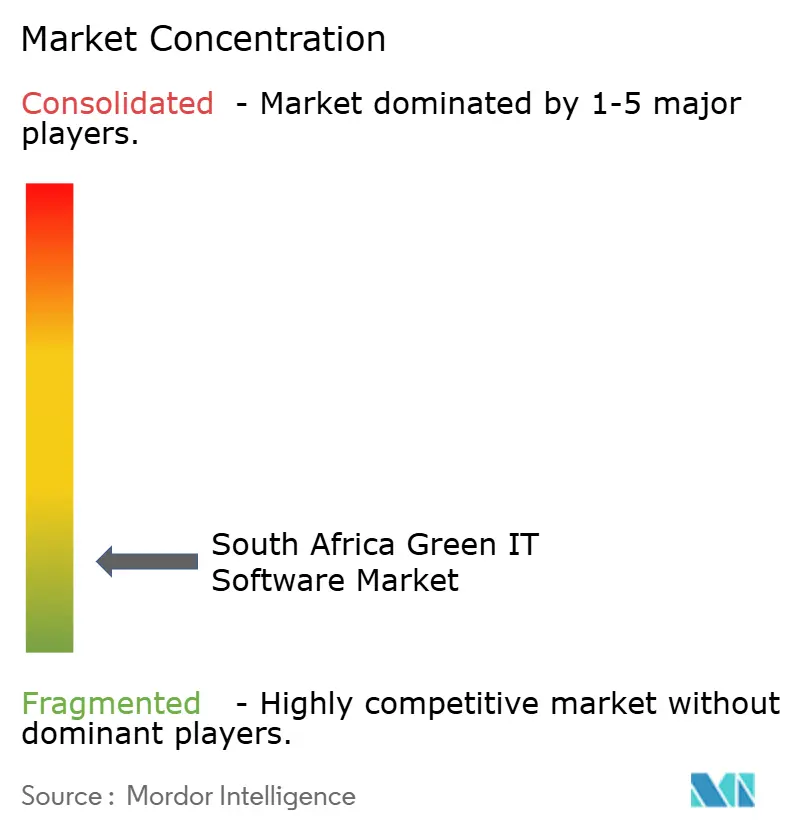

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Green IT Software Market Analysis by Mordor Intelligence

The South Africa green IT software market size was projected at USD 0.19 billion in 2025, reached USD 0.22 billion in 2026, and is forecast to reach USD 0.53 billion by 2031, growing at a CAGR of 18.91% from 2026 to 2031. Regulatory enforcement is shaping demand in a direct way because carbon budgets, climate disclosures, and stricter reporting practices are pushing companies to replace manual tracking with software-led workflows. The strongest demand is coming from organizations that need cleaner emissions data, faster reporting cycles, and systems that can stand up to internal review and outside verification. Higher electricity costs are also changing buying behavior because software that links energy use with cost control now supports both compliance and operating savings. Competition remains broad, with global EHS and ESG vendors, carbon accounting specialists, and local providers all active, while South Africa-based players still hold an advantage in mining and heavy industry where local operating conditions matter. The South Africa green IT software market is also benefiting from a longer demand cycle because cloud delivery, supplier emissions reporting, and decarbonization planning are expanding the role of software beyond a one-time compliance purchase.

Key Report Takeaways

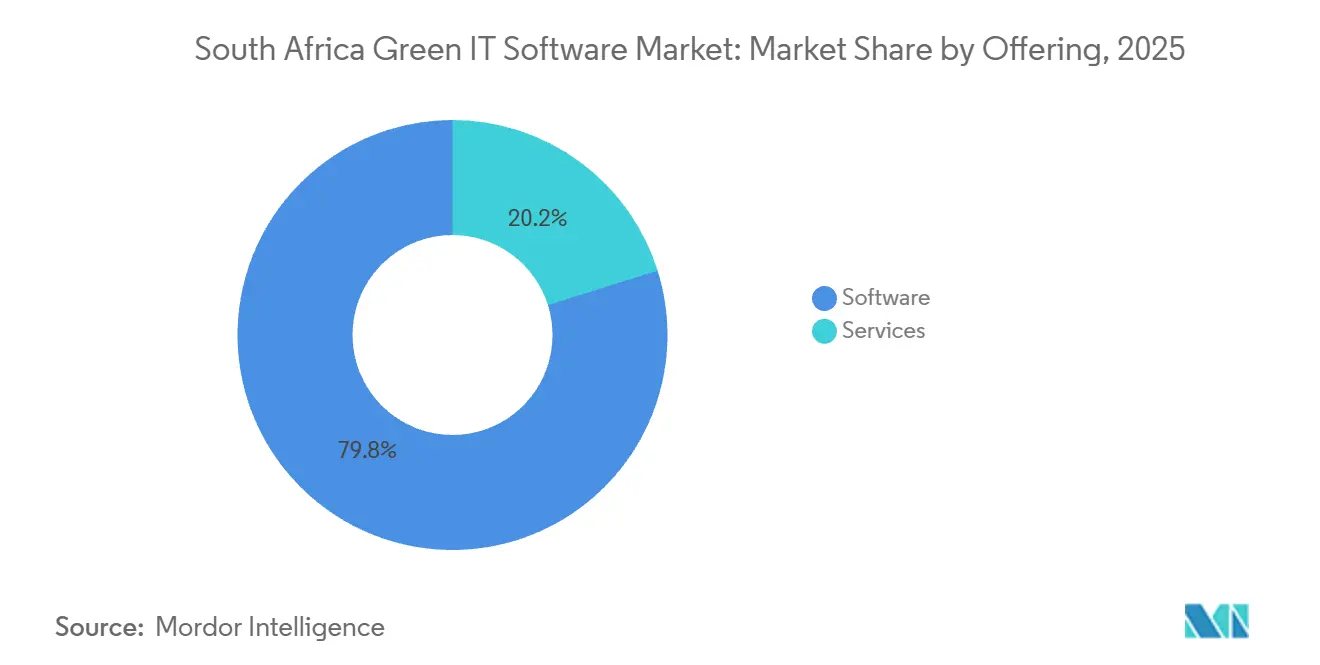

- By offering, software held 79.84% of the South Africa green IT software market share in 2025, while services are projected to expand at a 22.74% CAGR through 2031.

- By deployment mode, cloud accounted for 69.57% of the market in 2025, while hybrid is expected to record the fastest CAGR of 23.91% through 2031.

- By organization size, large enterprises captured 73.48% of the South Africa green IT software market share in 2025, while SMEs are forecast to grow at a 21.68% CAGR through 2031.

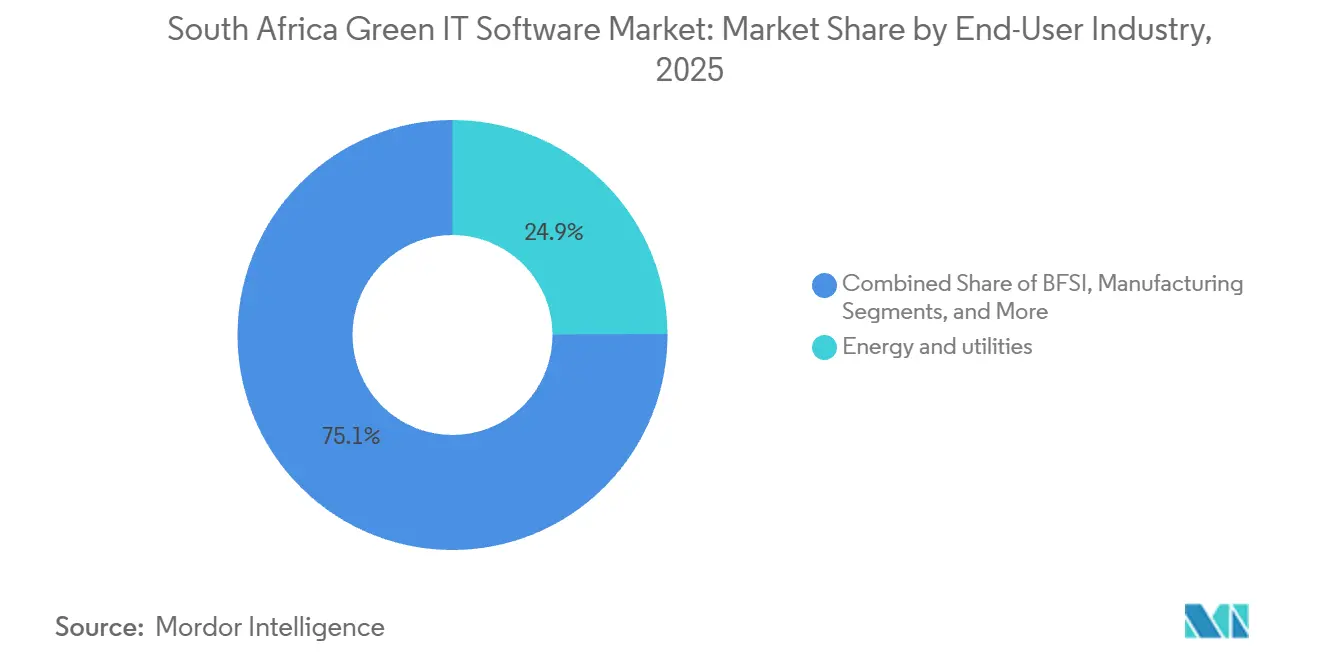

- By end-user industry, energy and utilities held 24.92% share in 2025, while IT and telecom is projected to expand at a 25.83% CAGR through 2031.

- By solution type, carbon management and accounting software accounted for 32.87% share in 2025, while decarbonization planning software is expected to advance at a 27.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Africa Green IT Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Pressure for Emissions and Energy Reporting | +3.5% | National, with alignment to ISSB standards across JSE-listed entities | Short term (≤ 2 years) |

| Rising Corporate Demand for Audit-Ready Sustainability Data | +3.0% | JSE-listed entities, banking, and insurance sectors nationwide | Medium term (2-4 years) |

| Energy Cost Volatility Increasing Optimization Software Spend | +2.5% | National, with acute pressure in Gauteng, Mpumalanga, and KwaZulu-Natal industrial corridors | Short term (≤ 2 years) |

| Growing Cloud Migration of Sustainability Workflows | +2.0% | National, driven by hyperscaler infrastructure investments in Cape Town and Johannesburg | Medium term (2-4 years) |

| Scope 3 Supplier Data Digitization Requirements | +1.5% | National, with spillover to SADC supplier networks | Medium term (2-4 years) |

| AI-Assisted Carbon and Energy Analytics Adoption | +1.2% | Global, with active local deployment among South African enterprises | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Pressure for Emissions and Energy Reporting

South Africa’s Climate Change Act 22 of 2024 entered into force on March 17, 2025, and established the country's first binding framework for carbon budgets and mitigation plans, underscoring the need for software that can track emissions at a far more detailed level.[1]Centre for Environmental Rights, “Climate Change Act 22 of 2024,” Centre for Environmental Rights, cer.org.za The fiscal side also became more demanding because the carbon tax rate was set at ZAR 190 (USD 10.40) per tonne of CO2 equivalent from January 1, 2024, which tied emissions data more closely to direct financial exposure. From January 2026, the compliance burden shifted further into operational decisions, as companies in the first commitment period had to manage against binding carbon budgets rather than broad policy direction alone. That shift favors platforms that support repeatable measurement, record retention, and verifiable reporting, rather than simple dashboarding. In the South Africa green IT software market, this means demand is being driven by legal and financial exposure, which gives enterprise software budgets stronger internal support. It also helps explain why the South Africa green IT software market is drawing buyers first toward core carbon and reporting tools before they widen spending into broader planning modules.

Rising Corporate Demand for Audit-Ready Sustainability Data

Large organizations now need sustainability data that can move through internal finance, risk, compliance, and disclosure processes without being rebuilt each reporting cycle. Telkom’s FY2025 sustainability reporting showed active progress toward automating real-time Scope 1, 2, and 3 data collection, which points to a clear shift from periodic manual reporting toward live enterprise data flows. Vodacom’s 2025 CDP disclosure also showed how mature reporting expectations are becoming because it reported that customer enablement helped avoid 2.7 million tCO2e, or 13 times its own Scope 1 and Scope 2 footprint.[2]Vodacom Group, “CDP Climate Report 2025,” Vodacom Group, vodacom.com Once companies begin publishing numbers at that level, they need stronger controls over source data, calculation methods, and version histories. That is one reason the South Africa green IT software market is rewarding platforms that support traceability and review workflows rather than tools that only present summary metrics. It also supports a broader move in the South Africa green IT software market toward systems that can serve finance teams, sustainability teams, and board reporting needs from the same data foundation.

Energy Cost Volatility Increasing Optimization Software Spend

Electricity tariffs remained a direct trigger for software investment because Eskom’s direct customer tariffs increased by 12.74% on April 1, 2025, and by a further 8.76% on April 1, 2026. That cost pressure matters because buyers do not need a long policy discussion to justify tools that can show lower consumption, reduced wastage, and tighter control across many facilities. Energy Partners reported a 34% reduction in energy consumption per hospital bed at Netcare through its Syntiro ESG platform, which shows that software can generate visible operating results inside a normal business cycle. For industrials, retailers, healthcare operators, and hospitality groups, the business case now joins cost control with emissions management in the same decision. This is helping the South Africa green IT software market expand beyond a reporting tool set and into daily operational management. It also creates room in the South Africa green IT software market for vendors that can connect meter data, facility performance, and carbon outputs inside one platform.

Growing Cloud Migration of Sustainability Workflows

Cloud adoption supports deployment speed because many buyers now prefer to add sustainability software on top of existing systems instead of replacing entire technology stacks. SAP Africa stated in April 2026 that staying on legacy ERP systems limits integration with modern cloud and AI tools and raises manual overheads, which supports the case for more modern deployment models. The practical result is not a full move away from internal systems but a layering model where analytics, reporting, and workflow tools sit in the cloud while operational data remains in place. That matches why cloud leads current revenue, while hybrid is rising fastest in the South Africa green IT software market. It also shows why the South Africa green IT software market is likely to keep favoring vendors with flexible deployment options rather than those tied to a single architecture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity with Legacy ERP and Metering Systems | -2.0% | National, concentrated in manufacturing, mining, and state-owned enterprises | Medium term (2-4 years) |

| Limited Availability of Sustainability Analytics Talent | -1.5% | National, with acute shortfalls in Limpopo, North West, and KwaZulu-Natal | Medium term (2-4 years) |

| Data Quality Gaps in Facility, Utility, and Supplier Inputs | -1.0% | National and SADC supply chain | Medium term (2-4 years) |

| Budget Sensitivity Among Mid-Market Buyers | -0.8% | National, concentrated in mid-market organizations outside Gauteng | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity with Legacy ERP and Metering Systems

Integration remains one of the main barriers because many large companies and state-linked entities still operate on older ERP environments that were not built around sustainability data fields. SAP Africa said in April 2026 that old ERP systems limit integration with cloud and AI tools and raise manual overheads, which fits the experience of companies trying to link utility meters, operating systems, spreadsheets, and enterprise reporting tools. In practice, this means the software decision is only one part of the job because buyers also need data mapping, connector work, validation rules, and operating ownership across departments. That raises implementation time and pushes many buyers toward vendors or partners that can deliver services as well as software. In the South Africa green IT software market, this slows adoption in sectors with complex site networks such as mining, manufacturing, and public infrastructure. It also explains why the South Africa green IT software market still shows strong services growth alongside a dominant software revenue base.

Limited Availability of Sustainability Analytics Talent

The skills constraint is real because software value depends on people who can configure systems, manage reporting logic, and translate rules into operating workflows. Research from the Mastercard Foundation highlighted strong demand across Africa for carbon accounting analysts, ESG reporting specialists, and sustainability managers, which points to a narrow talent pool for the roles many buyers now need. GSMA’s 2025 mobile ESG benchmarking also showed that data quality improves as reporting capability matures, which means software adoption is only part of the answer if internal expertise does not keep pace. Vendors are responding by embedding more automation, but companies still need staff who understand emissions boundaries, reporting standards, and approval paths. For the South Africa green IT software market, the result is a slower rollout curve in firms with lean sustainability teams and limited technology support. It also means the South Africa green IT software industry is likely to keep favoring tools with simpler setup, stronger templates, and lower day-to-day admin burdens.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Leads Revenue While Services Support the Next Stage of Adoption

Software accounted for 79.84% of revenue in 2025, indicating that the first spending priority in the South African green IT software market remained the purchase of core platforms rather than external support. Services are projected to grow at a 22.74% CAGR from 2026-2031, which points to a second phase where buyers need help with setup, integration, and ongoing changes in reporting requirements. This split fits a market where companies first secure a working system and then expand spending as internal data and workflows become more complex. It also shows that current revenue concentration does not reduce the longer-term role of implementation partners. In the South Africa green IT software market, that balance between platform purchase and service support is shaping how vendors package subscriptions, onboarding, and retention offers.

The software side remains dominant because companies want compliance-ready systems that can store, process, and report emissions and sustainability data in a structured way. The service side is rising faster because buyers often need outside support to connect legacy ERP records, facility data, and operational technology into one reporting environment. This is particularly relevant for the South Africa green IT software market where many organizations are still moving from spreadsheet tracking into formal platforms. As adoption broadens beyond large listed companies, services should remain important because smaller buyers usually lack internal teams that can manage complex configuration work on their own. That is why the South Africa green IT software market size for services is expanding quickly, even though software still accounts for the larger current revenue base.

By Deployment Mode: Cloud Holds the Lead While Hybrid Gains Ground

Cloud captured 69.57% of revenue in 2025, making it the largest deployment model in the South Africa green IT software market. Hybrid is projected to grow at a 23.91% CAGR through 2031, which shows that many companies prefer to combine cloud-based analytics and workflows with internal operational systems rather than shift everything at once. On-premises still matters for buyers with strict control needs, remote operations, or long-standing internal infrastructure. Even so, the center of new deployment activity is moving toward models that offer faster rollout and easier upgrades. That pattern keeps the South Africa green IT software market aligned with wider enterprise spending habits where flexibility often matters more than a single technology standard.

The growth of hybrid reflects business reality more than technology fashion because organizations often need to preserve internal systems while gaining better reporting and analysis tools. Mining groups, financial institutions, and state-linked organizations still have reasons to keep some data environments close to home, but they also want cloud layers that improve reporting speed and collaboration. This is why hybrid is the fastest-growing mode in the South Africa green IT software market, even while cloud remains the largest base.

By Organization Size: Large Enterprises Hold the Base While SMEs Lift Growth

Large enterprises captured 73.48% of 2025 revenue, which means the South Africa green IT software market still depends heavily on bigger organizations with stronger budgets and clearer disclosure pressure. SMEs are projected to grow at a 21.68% CAGR from 2026-2031, which shows that the next wave of adoption is moving into a broader set of buyers. Large companies were earlier adopters because they faced carbon budget exposure, listed-company reporting expectations, and stronger demands from investors, lenders, and multinational customers. SMEs are moving later, but the shift is still meaningful because cloud delivery lowers entry barriers and supplier reporting needs are spreading through value chains. The South Africa green IT software market is therefore becoming wider, even if the top revenue pool remains concentrated in large organizations.

SME demand is building for practical reasons rather than image reasons because smaller firms increasingly need structured data when they sell into larger corporate supply chains. That makes lower-cost SaaS tools, templates, and modular reporting functions more relevant than heavy enterprise buildouts. In this part of the South Africa green IT software market, ease of setup and lower support needs matter as much as advanced feature depth. Large enterprises will still shape vendor standards and product requirements, but SME growth should broaden the addressable base over the forecast period. This also means the South Africa green IT software market size tied to smaller buyers can rise without changing the fact that large firms still command the majority of current revenue.

By End-User Industry: Energy And Utilities Lead, While IT and Telecom Expand Fastest

Energy and utilities held 24.92% share in 2025, which made it the largest end-user group in the South Africa green IT software market. IT and telecom are projected to grow at a 25.83% CAGR through 2031, which sets the pace for future expansion across end users. Energy and utilities lead because emissions-intensive operations and direct reporting obligations make structured tracking a near-term need rather than a discretionary project. IT and telecom are growing faster because operators are automating data capture, improving reporting quality, and using digital infrastructure to support their own sustainability goals. This mix gives the South Africa green IT software market both a stable current base and a fast-moving next layer of adoption.

Telkom reported progress toward automating real-time Scope 1, 2, and 3 data collection, which shows how telecom operators are moving sustainability data into ongoing operating systems.[3]Vodacom Group, “CDP Climate Report 2025,” Vodacom Group, vodacom.com Vodacom’s 2025 CDP disclosure also showed large-scale reporting maturity through its avoided emissions reporting and broader climate data structure. At the same time, BFSI, manufacturing, healthcare, government, retail, construction, and other sectors continue to add demand at different speeds depending on energy costs, reporting pressure, and digital readiness. That makes end-user diversity an important support factor for the South Africa green IT software market because growth no longer depends on one sector alone.

By Solution Type: Carbon Management Leads While Decarbonization Planning Gains Speed

Carbon management and accounting software held the largest 2025 share at 32.87%, which kept it at the center of the South Africa green IT software market. Decarbonization planning software is projected to grow at a 27.46% CAGR from 2026 to 2031, which makes it the fastest-growing solution type. This progression is logical because many companies first need a reliable baseline before they can model reduction paths, capital options, and target scenarios. ESG reporting and compliance tools remain closely linked because companies often need reporting outputs built on the same governed data used for carbon accounting. The South Africa green IT software market, therefore, shows a clear sequence where measurement comes first and planning expands after baseline systems are in place.

Energy and resource optimization software also has a strong role because rising electricity tariffs make the cost side of energy use harder to ignore. Sustainability data management platforms remain relevant because buyers need a clean data layer before they can trust disclosure, planning, or energy tools. In the South Africa green IT software market, vendor success in solution type is increasingly tied to whether products can connect these functions without creating duplicate admin work. The South Africa green IT software industry is therefore moving toward platforms that can support accounting, reporting, optimization, and planning through a common structure rather than through disconnected modules. That supports the current lead for carbon management while leaving strong room for decarbonization planning to gain share as buyer maturity improves.

Geography Analysis

Gauteng is the main demand center in the South Africa green IT software market because it holds the Johannesburg Stock Exchange, many large corporate headquarters, major financial services activity, and a wide base of firms with formal reporting pressure. That concentration makes Gauteng the leading location for software sales, pilots, and enterprise deployments. The province also benefits from a strong mix of professional services, partner networks, and technology infrastructure, which makes implementation easier than in more dispersed operating regions. Because many companies manage national footprints from Gauteng offices, software procurement often begins there even when emissions sources sit in other provinces. This keeps Gauteng at the center of the South Africa green IT software market, even when the operational need is spread across mining, utilities, manufacturing, and logistics sites nationwide.

The Western Cape remains the second major cluster because Cape Town combines technology activity, renewable energy exposure, property development, and data center growth. KwaZulu-Natal also contributes meaningful demand through Durban’s port, logistics base, and industrial corridor, where transport, warehousing, and supply chain visibility are becoming more important. These provinces do not match Gauteng’s headquarters concentration, but they still add important use cases tied to facilities, power use, and supplier data. Their role shows that the South Africa green IT software market is not limited to listed-company reporting alone and is also linked to operational footprints.

Mining-focused provinces such as Mpumalanga, Limpopo, and North West create concentrated demand because heavy industry and site-level environmental management are already well established there. IsoMetrix’s position in mining and heavy industry reflects how software adoption often starts where reporting complexity, environmental controls, and operational risk are tightly linked. Sanlam’s FY2025 carbon footprint report showed that Scope 3 emissions represented 52% of the group’s total footprint, which indicates the level of maturity some South African organizations are reaching in broader emissions measurement. Taken together, these factors give the South Africa green IT software market a regional lead within Africa because the country has a stronger combination of disclosure culture, carbon pricing, and operating demand than many neighboring markets.

Competitive Landscape

The South Africa green IT software market is moderately fragmented overall, with large international platforms, pure-play carbon accounting vendors, and a smaller local group all competing for accounts. IsoMetrix remains the most established South Africa-headquartered provider in mining and heavy industry, which gives it a strong position where local deployment experience matters. Global vendors such as Schneider Electric, IBM, Wolters Kluwer, Cority, and Intelex remain active through direct presence, local partners, or broader enterprise relationships. This creates a competitive field where breadth of platform, local support depth, and implementation capacity often matter as much as product features. The result is a South Africa green IT software market where no single vendor defines the whole field, but some vendors hold stronger positions in specific buyer groups.

Strategic moves show how vendors are trying to widen their reach and lower adoption friction. IsoMetrix used its 2026 Customer Day in Johannesburg to preview a next-generation unified EHS and sustainability platform that combines AI, analytics, automation, and industry practices in one environment. Intelex announced its Q2 2026 product launch with AI-powered permit processing, field data capture automation, and new API endpoints, which point to a stronger focus on workflow speed and system connectivity. Cority also launched Cortex AI in December 2025, showing that vendors are using automation to reduce the staffing burden that many customers face.[4]Cority, “Cority Launches Cortex AI to Deliver Trusted Artificial Intelligence in EHS,” Cority, cority.com

Competition is also being shaped by relevance, not just visibility. South Pole does not operate as a core software competitor in this space because its main business centers on carbon projects, advisory work, and carbon credit activity rather than software licensing for the solution groups covered here. A closer reporting-platform peer is Workiva, which fits better where buyers need connected ESG and financial disclosure workflows. Wolters Kluwer reported 10% organic growth in EHS and ESG revenue in FY2025, supported by 19% growth in recurring cloud revenues, which shows how sticky enterprise sustainability contracts can become once systems are embedded. Overall, the South Africa green IT software market still has open space in mid-market reporting tools, supplier emissions data capture, and combined energy-plus-carbon platforms, which leaves room for both local specialists and international vendors with adaptable products.

South Africa Green IT Software Industry Leaders

Persefoni AI, Inc.

Plan A Earth GmbH

Sweep SAS

Sphera Solutions, Inc.

Wolters Kluwer N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: IsoMetrix previewed its next-generation unified EHS and sustainability platform, combining AI, analytics, automation, and industry best practices into a single environment, at its 2026 Customer Day held in Johannesburg, signaling a product architecture consolidation from its current Aurora and Lumina product lines.

- April 2026: Intelex Technologies announced its Q2 2026 product launch, featuring AI-powered permit processing and field data capture automation, new API endpoints enabling end-to-end permit data workflow synchronization, and SIF prevention classification tools, extending the platform's environmental compliance automation capabilities.

- February 2026: Normative launched an AI-powered Product Carbon Footprint capability, targeting CSRD Wave 2 companies required to collect Scope 3 Category 1 emissions data from suppliers at scale, and the platform is built to ISO 14067 standards with planned PACT conformance for supplier data sharing.

- December 2025: Cority launched Cortex AI, a first-of-its-kind suite of intelligent AI agents and a centralized AI Control Center embedded across EHS and sustainability workflows in the CorityOne platform, with voice-to-text, image interpretation, and document analysis capabilities spanning over 25 operational risk areas.

South Africa Green IT Software Market Report Scope

The South Africa Green IT Software Market refers to the market for software solutions and associated services that enable organizations to improve the environmental sustainability of their IT infrastructure, digital operations, and energy-intensive technology environments. These solutions help enterprises monitor and reduce carbon emissions, optimize energy consumption, automate ESG and sustainability reporting, manage sustainability data, and support decarbonization planning across data centers, cloud infrastructure, enterprise applications, and operational technology systems.

The South Africa Green IT Software Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and SMEs), End-User Industry (IT and Telecom, BFSI, Manufacturing, Energy and Utilities, Retail and E-Commerce, Government, Healthcare, Construction and Infrastructure, and Other End-user Industries), Solution Type (Carbon Management and Accounting Software, ESG Reporting and Compliance Software, Sustainability Data Management Platforms, Decarbonization Planning Software, and Energy and Resource Optimization Software). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| SMEs |

| IT and Telecom |

| BFSI |

| Manufacturing |

| Energy and Utilities |

| Retail and E-Commerce |

| Government |

| Healthcare |

| Construction and Infrastructure |

| Other End-User Industries |

| Carbon Management and Accounting Software |

| ESG Reporting and Compliance Software |

| Sustainability Data Management Platforms |

| Decarbonization Planning Software |

| Energy and Resource Optimization Software |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| SMEs | |

| By End-User Industry | IT and Telecom |

| BFSI | |

| Manufacturing | |

| Energy and Utilities | |

| Retail and E-Commerce | |

| Government | |

| Healthcare | |

| Construction and Infrastructure | |

| Other End-User Industries | |

| By Solution Type | Carbon Management and Accounting Software |

| ESG Reporting and Compliance Software | |

| Sustainability Data Management Platforms | |

| Decarbonization Planning Software | |

| Energy and Resource Optimization Software |

Key Questions Answered in the Report

How large is the South Africa green IT software market in 2026 and what is the 2031 outlook?

The South Africa green IT software market reached USD 0.22 billion in 2026 and is forecast to reach USD 0.53 billion by 2031 at a CAGR of 18.91%.

What is driving software demand in South Africa the most?

The strongest demand drivers are carbon budgets, tighter emissions reporting, rising electricity tariffs, and the push for cleaner audit-ready sustainability data across large organizations.

Which offering category leads current revenue?

Software led the market with 79.84% share in 2025 because companies first prioritized compliance-ready platforms before expanding into service-heavy implementation work.

Which deployment model is gaining traction fastest?

Hybrid is growing fastest at a 23.91% CAGR through 2031 because many companies want cloud analytics while keeping some operational systems on existing internal infrastructure.

Which end-user group matters most right now?

Energy and utilities led with 24.92% share in 2025 due to emissions-intensive operations and formal reporting needs, while IT and telecom is growing fastest at 25.83% CAGR.

What solution area is expanding fastest over the forecast period?

Decarbonization planning software is projected to grow at a 27.46% CAGR because more companies are moving from baseline emissions measurement into scenario modeling and reduction pathway planning.

Page last updated on: