GPU Memory Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.40 Billion |

| Market Size (2031) | USD 32.15 Billion |

| Growth Rate (2026 - 2031) | 20.90% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

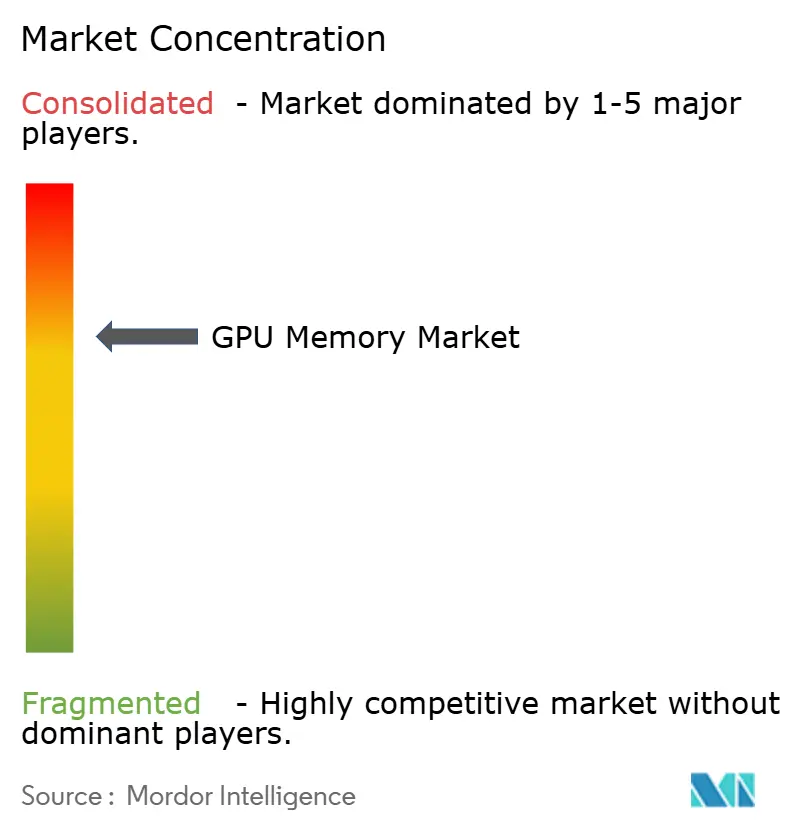

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GPU Memory Market Analysis by Mordor Intelligence

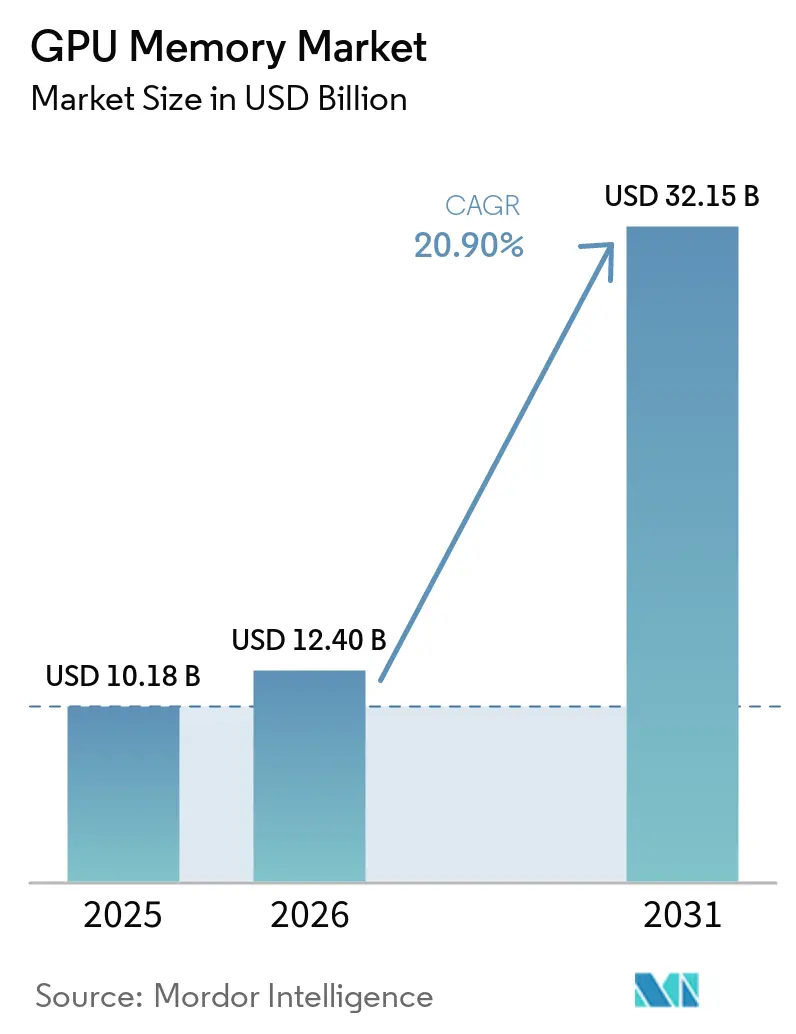

The GPU memory market size is expected to increase from USD 10.18 billion in 2025 to USD 12.40 billion in 2026 and reach USD 32.15 billion by 2031, growing at a CAGR of 20.90% over 2026-2031. The GPU memory market is moving on a structural demand base because each new GPU generation requires more memory capacity and more bandwidth per chip than the one before it. That pattern means the GPU memory market is expanding faster than GPU unit shipments alone, since memory content per accelerator keeps rising at the board and rack level. AI infrastructure spending is also changing buying behavior, as customers now secure memory for entire server racks and clusters instead of only for individual processors. Packaging capacity, supplier qualification timing, and 3D stacking yields now influence the GPU memory market almost as much as end demand, which keeps supply tight even while manufacturers add new lines. GDDR7 is also widening the addressable scope of the GPU memory market because it supports inference, visualization, gaming, and edge deployments where HBM is not the preferred cost or system fit.

Key Report Takeaways

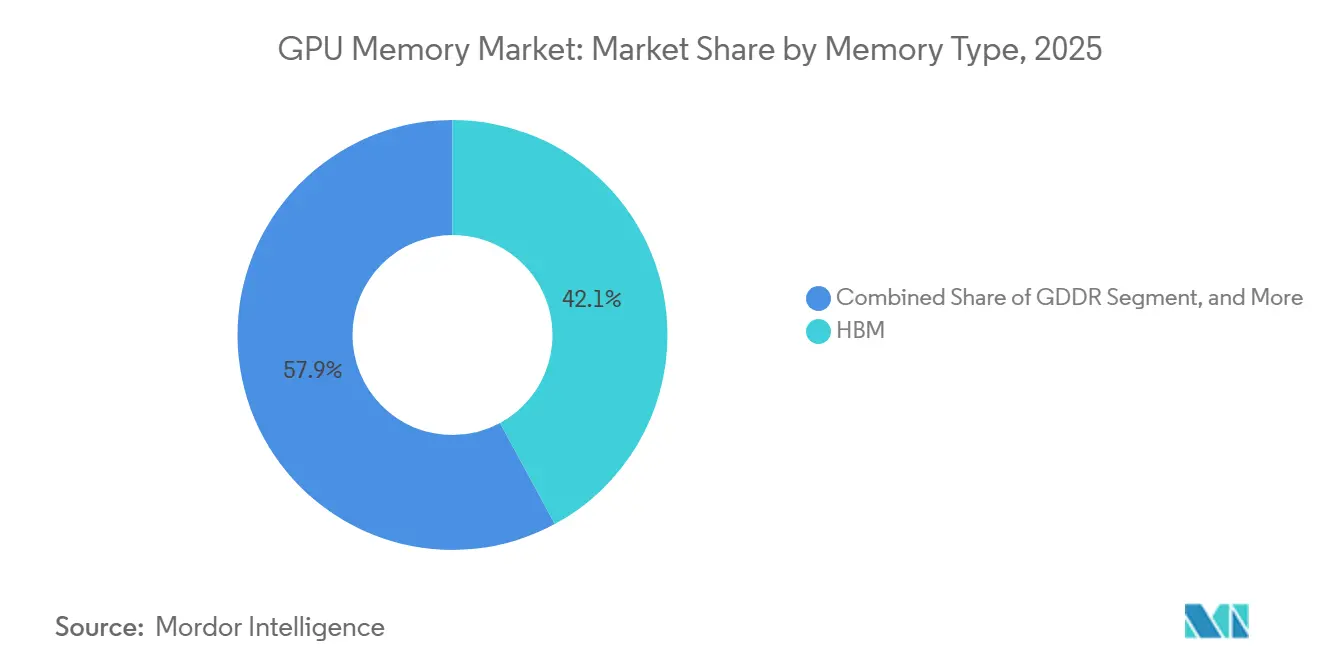

- By memory type, HBM led with 42.11% revenue share in 2025 and is also projected to expand at a 21.52% CAGR through 2031.

- By memory capacity, the 16 GB to 32 GB band held 30.55% share in 2025, while the Above 64 GB band is expected to record the highest CAGR of 21.46% through 2031.

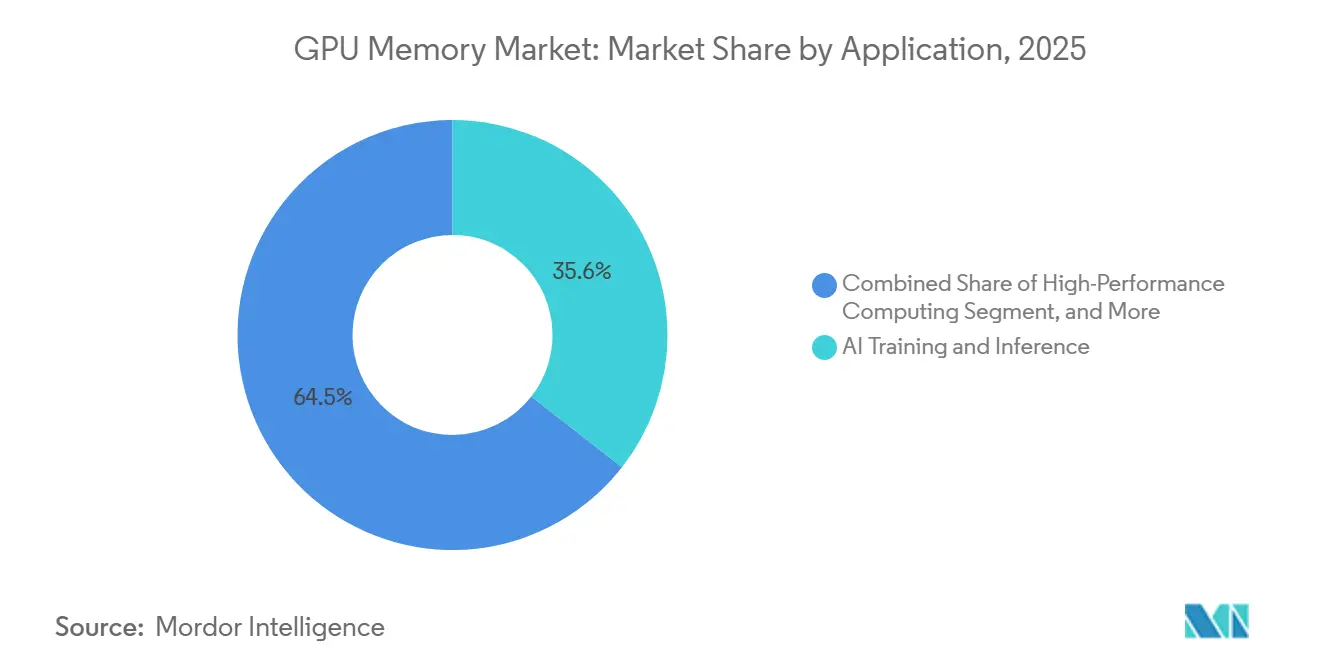

- By application, AI training and inference accounted for 35.55% share of the GPU memory market in 2025, while edge AI and embedded acceleration is projected to grow at a 21.35% CAGR through 2031.

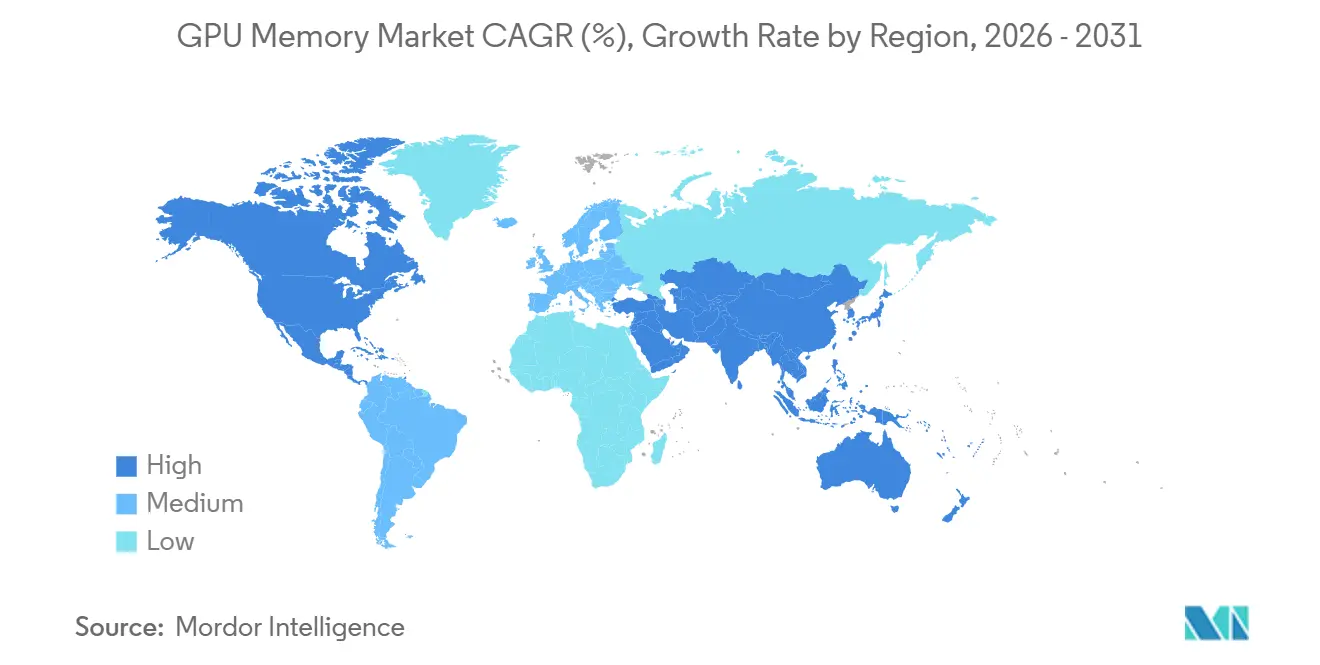

- By geography, Asia-Pacific held 48.34% share in 2025, making it the leading regional revenue base for the GPU memory market, while the same segment grew at 21.56% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global GPU Memory Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI Training Cluster Expansion Increasing HBM Consumption | +7.5% | Global, concentration in North America and Asia-Pacific | Short term (≤ 2 years) |

| NVIDIA Blackwell and Successor Platform Rollouts Increasing Qualification Demand | +4.5% | Global, with early concentration in North America | Short term (≤ 2 years) |

| Cloud Gaming and AI Workstation Upgrades Increasing GDDR7 Adoption | +2.8% | North America, Asia-Pacific, Europe | Short term (≤ 2 years) |

| Advanced Packaging Capacity Buildout Unlocking New GPU Memory Supply | +2.2% | Asia-Pacific, Taiwan and South Korea | Medium term (2-4 years) |

| OEM Preference for Higher Bandwidth Per Watt in Data Center GPUs | +1.5% | Global | Medium term (2-4 years) |

| Rising Demand for High-Capacity Modules in Inference Accelerators | +1.2% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI Training Cluster Expansion Increasing HBM Consumption

AI infrastructure buildouts have turned HBM from a premium memory option into one of the main supply gates for the GPU memory market. NVIDIA specified 192 GB of HBM3E for each Blackwell B200 GPU, and the GB300 Blackwell Ultra raises that requirement to 288 GB per GPU, which sharply lifts memory content per accelerator generation.[1]NVIDIA Corporation, “NVIDIA Blackwell RTX PRO Comes to Workstations and Servers for Designers, Developers, Data Scientists and Creatives to Build and Collaborate With Agentic AI,” NVIDIA Newsroom, nvidianews.nvidia.com NVIDIA also stated that a single GB200 NVL72 rack carries more than 13.4 TB of HBM3E, which shows why procurement has shifted from chip-level decisions to rack-level commitments. This change means the GPU memory market grows not only because more accelerators are shipped, but also because each deployment now absorbs far more memory than earlier system designs. The near-term effect is tighter supply utilization, since additional wafer starts alone do not solve limits in stacking, packaging, and qualification across the GPU memory market.

NVIDIA Blackwell and Successor Platform Rollouts Increasing Qualification Demand

Platform transitions are now one of the strongest timing factors in the GPU memory market because memory suppliers need to qualify each new generation before large customer volumes begin. Bloomberg reported in June 2026 that Samsung, SK hynix, and Micron all cleared HBM4 certification for NVIDIA Vera Rubin, making qualification the gateway to the next supply cycle. SK hynix then deepened that position with a multi-year technology partnership with NVIDIA covering HBM4, Vera Rubin systems, RTX Spark-powered PCs, and Jetson Thor robotics platforms.[2]SK hynix Inc., “SK hynix and NVIDIA Announce Multi-year Technology Partnership to Advance Memory for AI Factories,” SK hynix Newsroom, news.skhynix.com These platform rollouts force suppliers to support overlapping roadmaps for HBM3E, HBM4, and next-generation derivatives at the same time, which raises development pressure across the GPU memory market. The practical result is that early certification often matters as much as manufacturing scale, because qualified volume is what customers can deploy without delay.

Cloud Gaming and AI Workstation Upgrades Increasing GDDR7 Adoption

GDDR7 is widening the reach of the GPU memory market by serving deployments where HBM is not necessary or not economical. Rambus noted that JEDEC finalized the GDDR7 standard in early 2024, and by 2025 the three major memory suppliers had moved into mass production paths around the new standard. NVIDIA stated that its RTX PRO 6000 Blackwell Server Edition uses 96 GB of GDDR7 and delivers up to 1.6 TB/s, which shows that workstation and server use cases now form a real demand base beyond gaming. This broadens the GPU memory market across inference, visualization, digital twins, and cloud-based graphics services where memory cost and deployment density matter more than peak bandwidth alone. It also gives manufacturers a second high-value growth track while HBM capacity remains under pressure, which helps balance product mix across the GPU memory market.

Advanced Packaging Capacity Buildout Unlocking New GPU Memory Supply

Advanced packaging expansion is a supply driver for the GPU memory market because HBM cannot be used in AI accelerators without 2.5D integration and interposer-based assembly. Epoch AI found that advanced packaging and HBM, not logic die production, were the main bottlenecks in AI chip output during 2025. That makes packaging capacity a direct lever for GPU memory availability, since more packaged accelerators can only ship when memory stacks and interposer assembly scale together. Korea JoongAng Daily reported that Samsung and SK hynix are both expanding HBM-related production and packaging infrastructure, which strengthens the supply base centered in South Korea. As a result, capacity additions in Taiwan and South Korea do not just support chip output, they also unlock more usable volume for the GPU memory market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Qualified Supplier Concentration Limiting Volume Flexibility | -2.8% | Global | Medium term (2-4 years) |

| Yield Sensitivity in 3D Stacking and TSV Processing | -2.0% | Global, Asia-Pacific core | Medium term (2-4 years) |

| Allocation Tension Between HBM and GDDR Wafer Starts | -1.5% | Global | Short term (≤ 2 years) |

| Thermal And Power-Delivery Limits in Compact GPU Platforms | -0.8% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Qualified Supplier Concentration Limiting Volume Flexibility

Supplier concentration remains one of the clearest constraints on the GPU memory market because only a very small group of manufacturers can deliver qualified HBM at scale. Bloomberg confirmed in 2026 that Samsung, SK hynix, and Micron were the three memory makers certified for NVIDIA’s HBM4 cycle, which underlines how limited the qualified supplier base remains. Seoul Economic Daily reported that global large technology companies even proposed direct funding for SK hynix production lines and equipment, which shows how difficult it is to secure incremental supply through normal purchasing channels. This concentration reduces volume flexibility across the GPU memory market because new customers cannot quickly diversify to alternative sources when demand rises faster than planned capacity. It also means procurement timing is increasingly set by allocation agreements and qualification access, not only by end demand or GPU wafer availability.

Yield Sensitivity In 3D Stacking and TSV Processing

Yield sensitivity in 3D stacking continues to restrain the GPU memory market because HBM manufacturing depends on fine TSV structures, thin dies, and stable bonding results across many layers. Semiconductor Engineering reported that TSV processing operates in a narrow dimensional regime, where manufacturing tolerances differ sharply from conventional planar DRAM production.[3]Semiconductor Engineering, “TSV Complexity Leads to Manufacturing Bottleneck,” Semiconductor Engineering, semiengineering.com FSM Wafer explained that HBM4 stack development pushes dies toward 30-micron thickness, which raises wafer warpage risk and makes stress control a major yield variable. KED Global reported that Samsung’s 12-layer HBM3E qualification for NVIDIA took an extended development period before clearance, showing how yield issues can delay commercial entry into a platform cycle. In the GPU memory market, these technical setbacks matter because a defect in any die within a deep stack can affect the value of the full assembly and delay customer deployment plans.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Memory Type: HBM Leads Across Revenue Share and Growth

HBM held 42.11% of the GPU memory market share in 2025, making it the largest memory type, and this part of the GPU memory market size is projected to rise at a 21.52% CAGR through 2031. HBM keeps that lead because large AI training and inference systems now depend on high bandwidth, dense packaging, and rising memory-per-GPU specifications across each platform cycle. NVIDIA’s current data center roadmap already shows how fast requirements are increasing, with Blackwell and successor systems moving to much higher HBM loads per accelerator and per rack. Bloomberg also confirmed that Samsung, SK hynix, and Micron all qualified for NVIDIA’s HBM4 cycle in 2026, which supports the next phase of HBM revenue expansion.

The growth profile of HBM is also reinforced by active supplier roadmaps in 2026, with Samsung and SK hynix moving 12-layer HBM4E and related next-generation products toward customer deployment. SK hynix stated that its June 2026 HBM4E sample shipments reached 48 GB per stack, which supports the move toward much larger memory footprints in future AI accelerators. GDDR remains the main complement to HBM in the GPU memory market because it supports lower-cost inference, gaming, visualization, and workstation deployments where system economics matter more than maximum bandwidth. Rambus and NVIDIA both showed that GDDR7 is now moving into mainstream product lines, which gives the market a broad second growth base outside HBM-heavy server clusters. Other memory types still matter, but their role remains more selective and is tied to architectures that trade peak bandwidth for lower cost or higher capacity per dollar.

By Memory Capacity: The 64 GB And Above Tier Defines Next-Generation Platform Requirements

The 16 GB to 32 GB band held 30.55% share in 2025, which reflects the large installed base of gaming, workstation, and enterprise GPUs already deployed across the GPU memory market. The Above 64 GB band is the fastest-growing capacity tier, and this portion of the GPU memory market size is forecast to expand at a 21.46% CAGR from 2026 to 2031. That shift is closely tied to AI accelerator designs that now require 192 GB to 288 GB of memory per GPU, which moves demand well beyond the capacity bands that defined earlier product cycles. SK hynix stated in June 2026 that its 12-layer HBM4E sample reached 48 GB per stack, and the same release linked the product to future systems that will need very large aggregate memory per processor.

The 8 GB to 16 GB range still supports meaningful unit demand in consumer and mid-range workstation products, but its revenue role is becoming less central as larger cards move into the mainstream. The Up to 8 GB band continues to fade because even entry-level graphics and AI-assisted rendering workloads now require more headroom than earlier gaming generations. The 32 GB to 64 GB tier is gaining ground in professional use cases, and NVIDIA’s RTX PRO 6000 Blackwell Server Edition with 96 GB of GDDR7 shows how workstation-class products are moving into higher-capacity configurations. Across the GPU memory market, the key mix change is no longer just a move to faster memory, it is a move to materially larger memory pools per accelerator.

By Application: Edge AI Fastest-Growing As AI Inference Decentralizes

AI training and inference accounted for 35.55% of revenue in 2025, which made it the largest application in the GPU memory market. Edge AI and embedded acceleration is projected to grow at a 21.35% CAGR through 2031, as inference workloads move closer to industrial, medical, automotive, and robotics end points. This pattern expands the GPU memory market beyond hyperscaler campuses, because more memory-enabled compute is being placed in distributed systems that need local processing and low latency. It also supports a wider product mix, since edge deployments often prefer compact GDDR-based designs while centralized training systems continue to favor HBM-heavy architectures.

Cloud GPU and data center acceleration remains the second major demand block because large service providers keep scaling training clusters and inference services around the latest GPU platforms. High-performance computing continues to provide a stable base for the GPU memory market, especially in simulation, weather modeling, and research workloads that value both memory bandwidth and capacity. Gaming and consumer graphics still contribute high unit volumes, but average memory content per card is far below what data center accelerators consume, which keeps revenue intensity lower for this application mix. Professional visualization and content creation are also expanding as workstation products combine larger GDDR7 pools with AI acceleration features, which lets one hardware class serve rendering, design, and inference use cases.

Geography Analysis

Asia-Pacific accounted for 48.34% of the GPU memory market share in 2025, which made it the largest regional base for both supply and revenue. The region holds that position because South Korea anchors HBM manufacturing through Samsung and SK hynix, while Taiwan remains central to advanced packaging that is required for HBM deployment in AI accelerators. Korea JoongAng Daily reported that Samsung and SK hynix are scaling HBM-related production, which reinforces Asia-Pacific’s role as the core production center for the GPU memory market. Japan adds depth through semiconductor equipment, testing systems, and memory research support, which strengthens the regional ecosystem around manufacturing continuity. India and Southeast Asia are also becoming more relevant to the GPU memory market as cloud operators expand data center footprints in Singapore, Malaysia, and Indonesia.

North America remains the main demand center in the GPU memory market because the largest AI infrastructure programs are still concentrated among U.S. cloud and platform companies. Mordor Intelligence stated that large-scale training and data center GPU deployments in North America continue to shape hardware procurement patterns, which directly supports memory demand across HBM and GDDR categories. The region also benefits from supply-chain diversification efforts, since U.S.-linked memory capacity is increasingly valued by customers that want a broader geographic sourcing base. This keeps North America important to the GPU memory market even though the heaviest manufacturing concentration remains in Asia-Pacific.

Europe is becoming a more meaningful consumption geography for the GPU memory market as hyperscalers and enterprises add AI-ready capacity under stricter governance and compliance needs. AWS committed EUR 33.7 billion (USD 35.7 billion), to expand GPU capacity in Spain through 2033, and Google announced EUR 5.5 billion (USD 5.83 billion), for GPU and TPU buildout in Hanau and Frankfurt in December 2025. The EU AI Act is also supporting demand for private cloud and on-premise AI infrastructure, which lifts enterprise hardware demand that depends on advanced memory content. South America and Middle East and Africa remain smaller in current scale, but the GPU memory market has room to deepen there as sovereign AI projects and digital infrastructure programs advance through the forecast period.

Competitive Landscape

The GPU memory market remains concentrated at the memory supply layer, where Samsung, SK hynix, and Micron control the qualified HBM pool that supports leading AI accelerators. Bloomberg’s June 2026 report that all three major suppliers cleared HBM4 certification for NVIDIA Vera Rubin shows how platform access is limited to a very small set of approved vendors. This makes competition in the GPU memory market less about broad commodity volume and more about qualification timing, execution quality, and the ability to align roadmaps with major GPU platforms. SK hynix strengthened its position in June 2026 by signing a multi-year technology partnership with NVIDIA that covers HBM4, future AI systems, PCs, and robotics products. That move matters because it ties a leading memory supplier more closely to one of the largest downstream demand engines in the GPU memory market.

Samsung is using a different strategy in the GPU memory market by pairing memory development with broader platform integration and high-volume ramp execution. Seoul Economic Daily and Dong-A Ilbo both showed that Samsung moved early in HBM4 mass production and quickly built commercial momentum in 2026, which supports its attempt to regain ground in advanced memory supply. Digital Today Korea also reported that Samsung signed a memorandum of understanding with AMD for HBM4 supply tied to the Instinct MI455X program, which gives Samsung a strategic socket in the current accelerator cycle. These steps show that competitive positioning in the GPU memory market now depends on customer-specific wins as much as on raw fabrication scale.

A second layer of competition sits around packaging, interfaces, and outsourced assembly because the GPU memory market cannot expand smoothly without those capabilities. Epoch AI showed that advanced packaging was one of the main bottlenecks in AI chip production during 2025, which elevates the strategic role of firms connected to CoWoS and related integration flows. Rambus also has ecosystem influence because standards and signaling requirements affect how quickly next-generation memory can move from design to production. As a result, the GPU memory market is not shaped only by chipmakers, it is also shaped by packaging specialists, interface technology providers, and test and assembly partners that can support deep-stack production at scale. The overall structure still favors a concentrated leadership group, because qualification, packaging, and system integration remain hard to replicate quickly.

GPU Memory Industry Leaders

SK hynix Inc.

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

NVIDIA Corporation

Advanced Micro Devices, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: SK hynix shipped 12-layer HBM4E samples to major AI customers, achieving 48 GB capacity, 16 Gbps per pin, and power efficiency improvements exceeding 20% over the prior generation, advancing toward NVIDIA Vera Rubin Ultra deployments expected in 2027. SK hynix applied its Advanced MR-MUF technology to achieve structural stability and a 17% improvement in heat resistance compared with HBM4.

- June 2026: SK hynix and NVIDIA announced a multi-year technology partnership to co-develop next-generation AI memory, covering HBM4 for NVIDIA Vera Rubin, Vera CPUs, RTX Spark-powered PCs, and Jetson Thor robotics platforms. The agreement also applies NVIDIA CUDA-X libraries and NVIDIA PhysicsNeMo to accelerate SK hynix's semiconductor design and fab operations.

- June 2026: NVIDIA CEO Jensen Huang confirmed at Computex Taipei that Samsung, SK hynix, and Micron all cleared HBM4 certification for NVIDIA Vera Rubin, the first qualification cycle in which all 3 major HBM suppliers passed simultaneously.

- June 2026: Samsung's HBM4 cumulative revenue surpassed USD 1 billion within 4 months of mass production launch in February 2026, with full-year 2026 revenue projected to approach USD 10 billion as GPU and ASIC-based hyperscaler customers expand procurement. HBM4 shipment volume is expected to increase more than 200% year over year in 2026.

Global GPU Memory Market Report Scope

The Global GPU Memory Market refers to the worldwide industry focused on the design, production, and deployment of memory solutions specifically optimized for Graphics Processing Units (GPUs), which are critical for handling high-performance computing tasks such as gaming, artificial intelligence, machine learning, data analytics, and scientific simulations.

The GPU Memory Market Report is Segmented by Memory Type (HBM, GDDR, and Other GPU Memory Types), Memory Capacity (Up to 8 GB, 8 GB to 16 GB, 16 GB to 32 GB, 32 GB to 64 GB, and Above 64 GB), Application (Professional Visualization and Content Creation, AI Training and Inference, High-Performance Computing, Cloud GPU and Data Center Acceleration, Gaming and Consumer Graphics, and Edge AI and Embedded Acceleration), and Geography (North America, Europe, Asia Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| HBM |

| GDDR |

| Other GPU Memory Types |

| Up to 8 GB |

| 8 GB to 16 GB |

| 16 GB to 32 GB |

| 32 GB to 64 GB |

| Above 64 GB |

| Professional Visualization and Content Creation |

| AI Training and Inference |

| High-Performance Computing |

| Cloud GPU and Data Center Acceleration |

| Gaming and Consumer Graphics |

| Edge AI and Embedded Acceleration |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Memory Type | HBM | |

| GDDR | ||

| Other GPU Memory Types | ||

| By Memory Capacity | Up to 8 GB | |

| 8 GB to 16 GB | ||

| 16 GB to 32 GB | ||

| 32 GB to 64 GB | ||

| Above 64 GB | ||

| By Application | Professional Visualization and Content Creation | |

| AI Training and Inference | ||

| High-Performance Computing | ||

| Cloud GPU and Data Center Acceleration | ||

| Gaming and Consumer Graphics | ||

| Edge AI and Embedded Acceleration | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the GPU memory market?

The GPU memory market size is valued at USD 12.40 billion in 2026 and is forecast to reach USD 32.15 billion by 2031, at a CAGR of 20.90% over 2026-2031.

Which memory type leads revenue in GPU memory?

HBM leads the GPU memory market with a 42.11% share in 2025 and is also the fastest-growing memory type with a 21.52% CAGR through 2031.

Why is demand rising so quickly for high-capacity GPU memory?

New AI accelerator platforms are using much larger memory pools per GPU, which is why the Above 64 GB band is expected to grow at a 21.46% CAGR through 2031.

Which application drives the largest share of demand?

AI training and inference held 35.55% of revenue in 2025, making it the largest application area for the GPU memory market.

Why does Asia-Pacific dominate this space?

Asia-Pacific held 48.34% share in 2025 because South Korea concentrates HBM production and Taiwan remains critical to advanced packaging for AI accelerators.

How is GDDR7 affecting the business outlook?

GDDR7 is expanding the GPU memory market into workstations, inference servers, gaming, and edge systems, which gives suppliers a broader demand base beyond HBM-heavy training clusters.

Page last updated on: