Europe Integrated GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

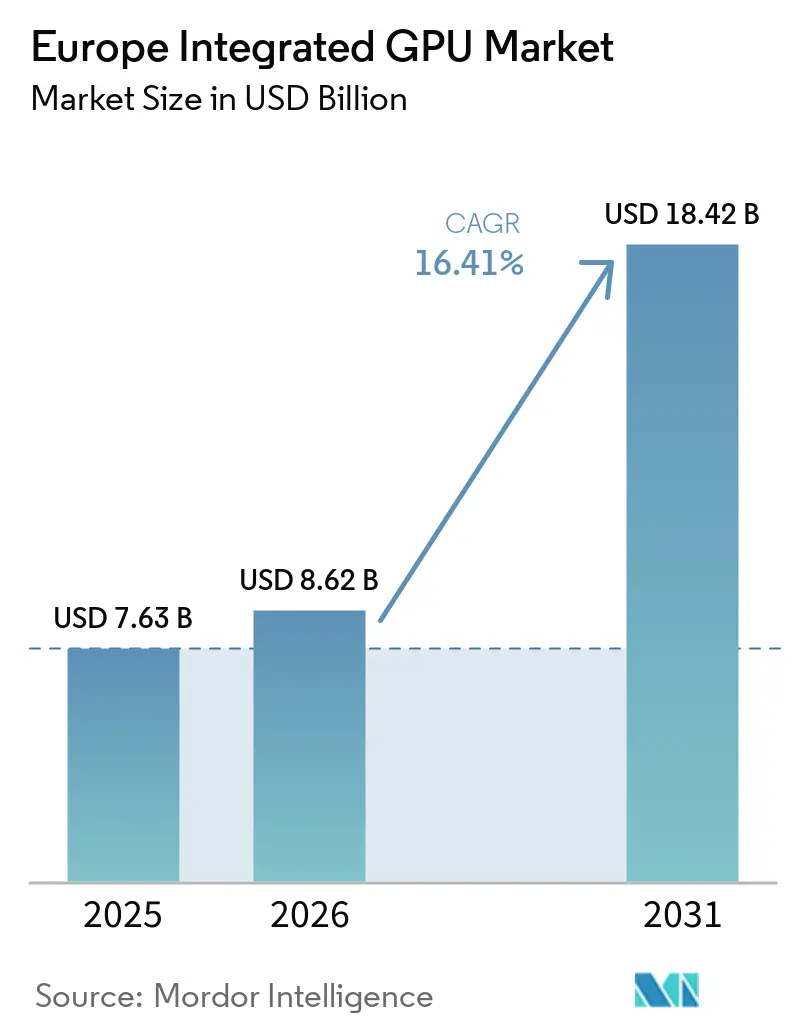

| Base Year Market Size (2025) | USD 7.63 Billion |

| Market Size (2026) | USD 8.62 Billion |

| Market Size (2031) | USD 18.42 Billion |

| Growth Rate (2025 - 2031) | 16.41% CAGR |

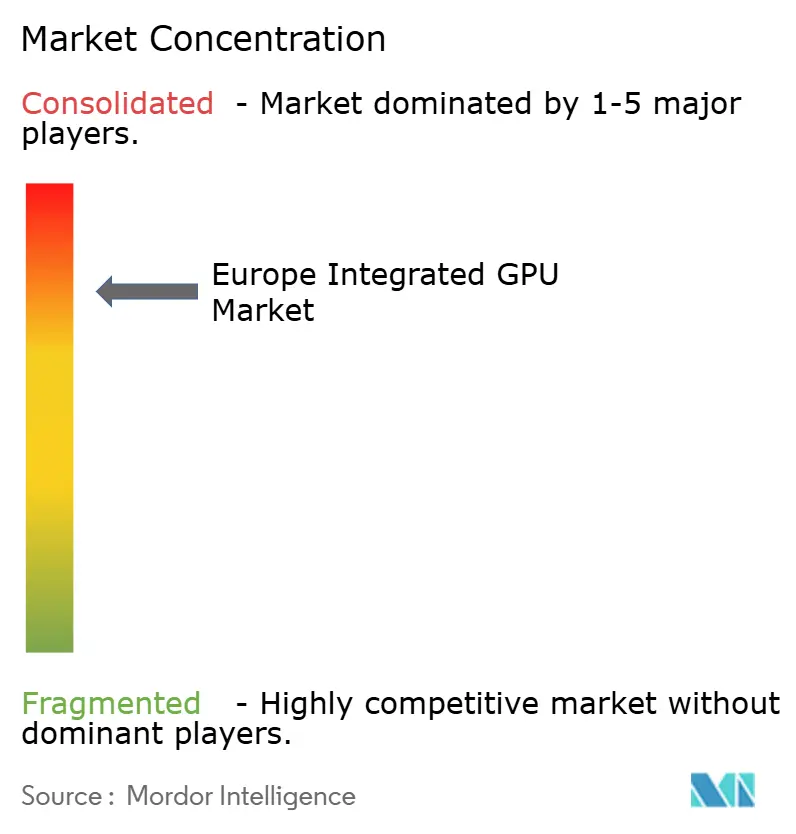

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Integrated GPU Market Analysis by Mordor Intelligence

The Europe integrated GPU market size is projected to be USD 7.63 billion in 2025, USD 8.62 billion in 2026, and reach USD 18.42 billion by 2031, growing at a CAGR of 16.41% from 2026 to 2031. The Europe integrated GPU market is moving upward as AI-native processor designs bring graphics, media, and AI acceleration onto the same package while staying within strict power limits. Device refresh activity is also rising across business and consumer channels as multiple replacement cycles now overlap in notebooks, smartphones, tablets, and embedded systems. The Europe integrated GPU market is also being supported by Europe’s large enterprise IT base, its strong industrial automation footprint in countries such as Germany and Italy, and a policy setting that favors lower-power electronics design. Competitive activity remains intense as Intel and AMD push PC graphics performance higher, while Qualcomm, MediaTek, and Samsung increase mobile GPU capability through advanced-node system-on-chip development. Near-term cost pressure from memory inflation and advanced-node capacity competition may slow some unit growth, but the Europe integrated GPU market continues to gain value as buyers shift toward richer integrated graphics platforms instead of basic replacement systems.

Key Report Takeaways

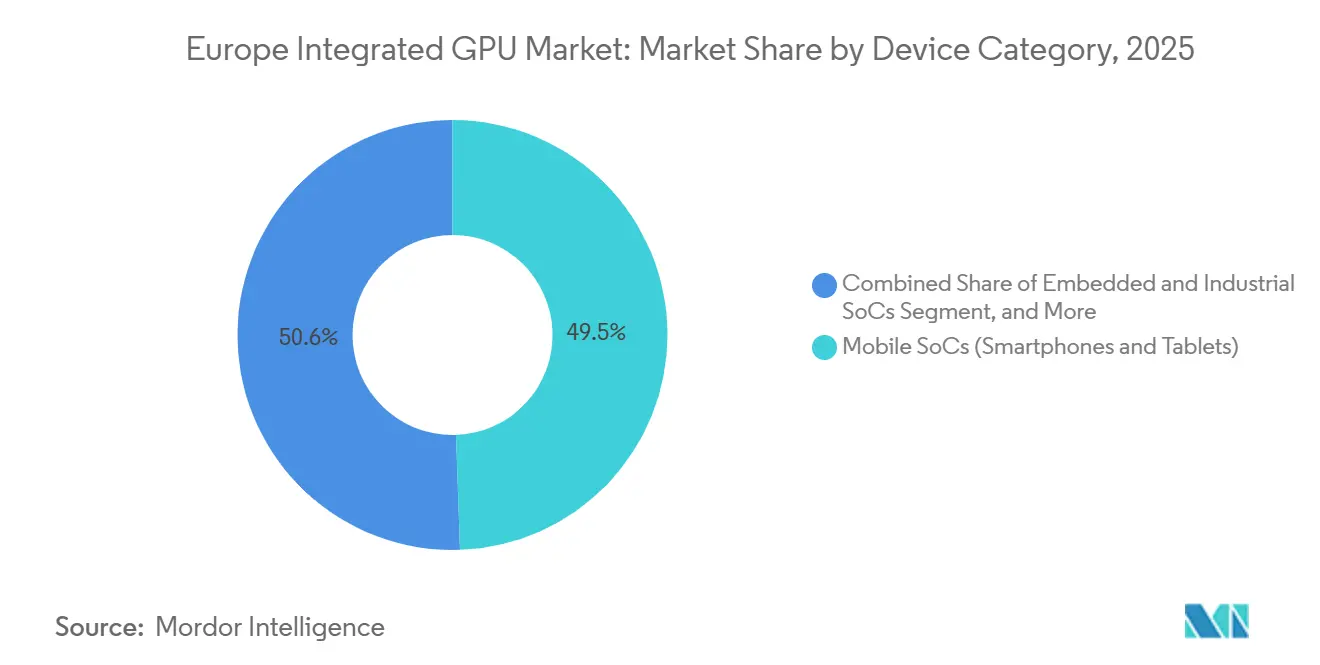

- By device category, Mobile SoCs held the largest share at 49.45% in 2025, while Server and Data Center Processors with Integrated Graphics is projected to expand at a CAGR of 16.97% during 2026-2031 as European data center operators adopt unified processor platforms for compute, video, and lightweight inference workloads.

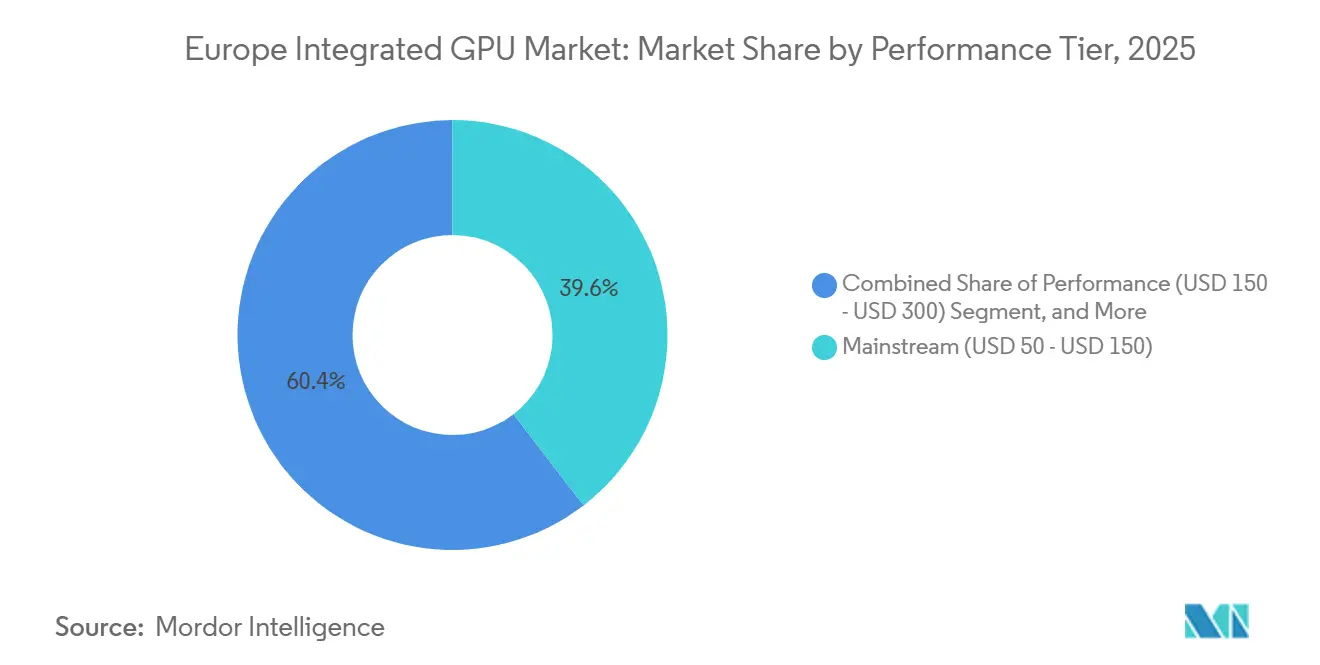

- By performance tier, the Mainstream segment held the largest share at 39.56% in 2025, while the Performance segment is projected to expand at a CAGR of 17.34% over 2026-2031 as AI-capable notebook configurations move into broader enterprise procurement.

- By geography, Germany accounted for the largest share at 28.22% in 2025 in the Europe integrated GPU market, while France is projected to grow at a CAGR of 17.54% through 2031 as government-backed AI investment programs and commercial AI PC adoption accelerate.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Integrated GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Windows 11 Refresh and Windows 10 Retirement | +2.8% | Germany, United Kingdom, Rest of Europe, SME-concentrated enterprise installed base | Short term (≤ 2 years) |

| Rising AI-Capable Notebook Penetration | +3.5% | Pan-European, commercial channels leading with higher AI PC adoption rates versus consumer | Medium term (2-4 years) |

| Demand for Power-Efficient Graphics in Thin-and-Light Devices | +2.2% | European Union-wide, premium notebook OEM design concentration in Germany, United Kingdom, France | Medium term (2-4 years) |

| Premium Smartphone SoC Migration to Richer Graphics and Advanced Nodes | +2.5% | France, Germany, United Kingdom, premium smartphone density markets | Medium term (2-4 years) |

| Europen Union Ecodesign and Energy Labeling Pressure Favoring Lower-Power Designs | +1.6% | European Union-wide, compliance factors under Commission Regulation (EU) 2023/1670 and its December 2025 amendment | Long term (≥ 4 years) |

| Industrial Edge AI Rollouts Expanding Embedded SoC Demand | +2.1% | Germany, France, Italy, spillover to Benelux and Nordics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising AI-Capable Notebook Penetration Reshapes Integrated GPU Demand Mix

AI-capable notebooks have become a defined buying category across the Europe integrated GPU market as enterprises look for systems that can support local AI features over a full replacement cycle. Intel launched Panther Lake Core Ultra Series 3 at CES 2026 with up to 12 Xe3 GPU cores and a 50 TOPS NPU, making the platform a clear signal that graphics and AI now sit together in the same client computing conversation.[2]Intel, “CES 2026, Intel Core Ultra Series 3 Debut as First Built on Intel 18A,” Intel Newsroom, newsroom.intel.com The practical change is that the NPU and iGPU now share mixed workloads such as video enhancement, background segmentation, and document processing in everyday business use. That raises the graphics specification floor even in notebooks that were once treated as standard office machines. The Europe integrated GPU market is therefore benefiting not only from more units, but also from a stronger mix as AI-ready notebooks move from a niche class into mainstream enterprise demand.

Windows 11 Refresh and Windows 10 Retirement Drive Structural PC Hardware Replacement

Windows 10 reached its official end of support on October 14, 2025, and that created direct hardware replacement pressure across European device fleets that did not meet Windows 11 security minimums such as TPM 2.0 and Secure Boot.[1]Microsoft, “Windows 10 Support Has Ended on October 14, 2025,” Microsoft Support, microsoft.com This matters for the Europe integrated GPU market because the refresh is hardware-led rather than software-led, which lifts processor shipments more strongly than a normal operating system transition. Many small and medium enterprises delayed upgrades through 2024, so a meaningful share of installed devices could not move forward without full replacement. Buyers are also tending to choose AI-capable platforms instead of minimum-spec compliant systems, and that supports stronger value across the Mainstream and Performance tiers. The Europe integrated GPU market is therefore seeing a larger uplift than earlier Windows sunsets would have suggested.

Premium Smartphone SoC Migration to Richer Graphics and Advanced Nodes Expands Mobile iGPU Value

Mobile SoCs remain the largest value pool in the Europe integrated GPU market, and richer smartphone graphics are lifting revenue per unit even though handset volumes are not surging. Samsung unveiled the Exynos 1680 in March 2026 on a 4nm process with the Xclipse 550 GPU based on AMD RDNA 3 architecture, and the company stated that GPU performance improved by 16% over the prior generation. MediaTek announced the Dimensity 9500 in September 2025 with 33% higher peak GPU performance and 42% better power efficiency than its predecessor, while also bringing 120fps hardware ray tracing into flagship Android devices. MediaTek then followed in January 2026 with the Dimensity 9500s and Dimensity 8500, confirming that richer graphics blocks are moving from flagship products into premium mid-range devices. In practical terms, the Europe integrated GPU market is gaining from a wider smartphone replacement band that now sits around EUR 300-EUR 500 (USD 339-USD 565) and carries stronger graphics content than earlier mid-range generations.

Demand for Power-Efficient Graphics in Thin-and-Light Devices Elevates Advanced-Node iGPU Design Spend

Thin-and-light notebooks define much of the commercial computing base in the Europe integrated GPU market, so power efficiency remains central to graphics design. Intel stated that Panther Lake was built on Intel 18A and paired its Arc B390 integrated graphics with performance levels that move much closer to entry discrete notebook GPUs within thin system power envelopes. Qualcomm also positioned the Snapdragon X2 Elite around strong graphics capability per watt, with support for DirectX 12.2 Ultimate and Vulkan 1.4 for performance-tier notebooks.[3]Qualcomm, “Snapdragon X2 Elite Product Brief,” Qualcomm, qualcomm.com EU regulation adds another layer because Commission Regulation (EU) 2023/1670 created energy efficiency requirements and labeling rules for smartphones and tablets placed on the regional market. The Europe integrated GPU market is therefore being pushed by both buyer demand and compliance logic toward designs that deliver more graphics capability per milliwatt.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advanced-Node Supply Competition from AI Accelerators and Premium Mobile SoCs | -2.0% | Global, most acute for TSMC 3nm-2nm and Samsung foundry allocations, European OEM procurement affected | Short term (≤ 2 years) |

| Memory and Storage Cost Inflation Limiting Replacement Budgets | -1.3% | Pan-European consumer and SME segments with constrained hardware budgets | Short term (≤ 2 years) |

| Cyber Resilience Act Compliance Burden for Connected Embedded Platforms | -1.0% | EU-wide, Regulation (EU) 2024/2847 entered into force on December 10, 2024, reporting obligations from September 11, 2026, main obligations from December 11, 2027 | Medium term (2-4 years) |

| High-End Creator and Gaming Workloads Still Pulling Demand Toward Discrete GPUs | -1.5% | Germany, United Kingdom, France, dense gaming and content-creation user bases | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advanced-Node Supply Competition From AI Accelerators and Premium Mobile SoCs Constrains Supply

The Europe integrated GPU market depends on advanced foundry capacity because premium notebooks and smartphones now need leading-edge nodes to deliver higher graphics capability within lower power limits. This creates a structural supply problem because AI accelerators and premium mobile processors are chasing the same 3nm-4nm class capacity. The issue is important for vendors such as AMD, MediaTek, and Qualcomm because they are effectively competing against their own higher-margin product lines for wafer starts. That can delay next-generation launches, raise pricing, or limit supply at the volume tier for European OEM customers. The Europe integrated GPU market therefore faces a real near-term brake even when end-user demand remains healthy.

High-End Creator and Gaming Workloads Sustain Discrete GPU Demand at the Top End

The Europe integrated GPU market has moved much closer to entry discrete performance, but it still does not displace dedicated graphics in the highest creator and gaming workloads. Intel’s Panther Lake Arc B390 showed that integrated graphics can now approach entry discrete benchmarks in some notebook use cases, but demanding users still need more sustained headroom for high-fidelity gaming and creative rendering. This leaves Germany, the United Kingdom, and France with a durable installed base that still prefers discrete configurations for enthusiast and professional work. AMD’s roadmap choice to extend RDNA 3.5 for volume notebook integrated graphics while holding back broader RDNA 4 iGPU adoption also reflects that practical ceiling in the high end. The Europe integrated GPU market therefore keeps growing, but its addressable space at the premium extreme remains capped by discrete GPU demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Category: Mobile SoCs Hold the Volume Base While Server Processors Add New Value Growth

Mobile SoCs held 49.45% of the Europe integrated GPU market share in 2025, making them the largest device category across the region’s revenue mix. Their lead reflects Europe’s dense premium smartphone base and the ongoing move of upper-mid and flagship Android devices toward richer integrated graphics blocks with hardware ray tracing, faster media engines, and stronger on-device AI support. Samsung’s Exynos 1680 and MediaTek’s Dimensity 9500 family show how the mobile layer of the Europe integrated GPU industry is moving toward higher graphics value at advanced nodes rather than relying only on unit growth. Desktop and Laptop Processors remained the second-largest category because the Windows 11 refresh cycle sustained replacement demand across enterprise notebooks and desktops in 2025 and into 2026.

Server and Data Center Processors with Integrated Graphics are projected to expand at a CAGR of 16.97% through 2031, which makes them the fastest-growing device category in the Europe integrated GPU market size outlook. European cloud operators and enterprise data centers are increasingly looking at unified processors that can handle compute, video transcoding, lightweight inference, and visualization without a dedicated add-in accelerator in every use case. Intel’s preview of Xeon 6+ Clearwater Forest, expected in the first half of 2026, illustrates how advanced-node integrated graphics capability is moving into server-grade platforms at a speed that supports this shift. Embedded and Industrial SoCs are smaller in absolute value, but they are gaining strategic importance as edge AI expands in factories and industrial equipment across Germany, France, and Italy. NXP’s i.MX 93W and Renesas’ acquisition of Irida Labs show that the Europe integrated GPU industry is also shifting toward embedded platforms where graphics, AI, connectivity, and software differentiation now matter together in customer decisions.

By Performance Tier: Mainstream Keeps the Broad Base While Performance Tier Drives Faster Value Expansion

The Mainstream segment accounted for 39.56% of the Europe integrated GPU market size in 2025, which reflects the region’s large installed base of enterprise PCs and replacement notebooks that need balanced cost, power, and graphics capability. This part of the market continues to benefit from corporate fleet procurement, consumer notebook replacement, and a broader shift toward AI-ready systems that still need to stay within common budget limits. Entry-Level products remain present in low-cost consumer devices, education systems, and simple industrial human-machine interfaces, but they face pressure as older-node cost advantages become less decisive. The Performance segment is projected to expand at a CAGR of 17.34% through 2031, and that pace shows how much of the Europe integrated GPU market is now moving toward higher-capability client systems during the current replacement cycle. Buyers are increasingly selecting notebooks with stronger integrated graphics to support AI-assisted workflows, richer media handling, and longer platform life instead of buying the least expensive Windows 11-compatible option.

The High-Performance tier remains narrower than the volume bands, but it is becoming more relevant as premium thin-and-light devices push integrated graphics much closer to entry discrete territory. Intel’s Panther Lake Arc B390, with 12 Xe3 Battlemage cores and XeSS 3 multi-frame generation support, directly expands the ceiling of what integrated graphics can handle in compact notebooks. The September 2025 Intel-NVIDIA collaboration added a new strategic angle because future x86 SoCs with NVIDIA RTX GPU chiplets could create a premium sub-category within the upper end of the Europe integrated GPU market. That potential realignment matters because it suggests that the Europe integrated GPU industry is not only moving up through Mainstream and Performance systems, but is also testing how far integrated graphics can reach before the discrete boundary becomes less rigid.

Geography Analysis

Germany accounted for 28.22% of the Europe integrated GPU market share in 2025, giving it the largest national position in the region. The country’s lead is tied to a large enterprise IT installed base, a strong concentration of Industry 4.0-oriented manufacturers, and public and private procurement cycles aligned with the end of Windows 10 support. Intel and the German federal government finalized a revised letter of intent for a leading-edge wafer fabrication site in Magdeburg with investment exceeding EUR 30 billion (USD 33.9 billion), reinforcing Germany’s strategic role in the regional semiconductor ecosystem. Even though commercial benefits from that investment will take time to flow through, Germany remains the strongest anchor point for the Europe integrated GPU market in both demand and long-term supply positioning. The United Kingdom ranked as the second-largest national market because of its deep commercial PC base and growing cloud infrastructure footprint, even though post-Brexit divergence from EU product rules creates some extra certification complexity for suppliers.

France is projected to expand at a CAGR of 17.54% through 2031, making it the fastest-growing major geography in the Europe integrated GPU market. Its growth is supported by an active government AI agenda and by faster deployment of AI-capable commercial systems across financial services, healthcare, and public administration. AMD and the French government announced plans in April 2026 to deepen collaboration under France’s National Strategy for AI, including the planned Alice Recoque exascale supercomputer and a Center of Excellence for AI Factory France. Italy is also becoming more important because machine vision, robotics, and industrial automation deployments continue to raise demand for embedded processors with integrated graphics for local visual AI tasks.

The Rest of Europe segment is heterogeneous, but it gives the Europe integrated GPU market a broad base rather than a single-country growth profile. Nordic markets contribute an above-average mix of Performance and High-Performance systems because enterprise AI adoption and premium notebook penetration are already high. Poland and other Central and Eastern European countries are earlier in the commercial AI PC transition, which leaves more room for replacement-led volume growth through 2028. Benelux markets are influenced by clustered European Commission and NATO procurement cycles, while Spain has also shown meaningful notebook demand as replacement activity continues to work through the installed base.

Competitive Landscape

The Europe integrated GPU market is moderately concentrated at the platform level, but it is not dominated by one vendor across every major product group. Intel and AMD hold the strongest positions in desktop and laptop CPU integrated graphics, while Qualcomm, MediaTek, and Samsung lead mobile SoC competition. STMicroelectronics, NXP Semiconductors, and Renesas play a more strategic role in embedded and industrial designs where graphics, AI, security, and connectivity have to be integrated within a tighter system requirement. This split structure means the Europe integrated GPU market is competitive in a different way across PCs, smartphones, and industrial systems. It also means no single supplier carries leadership across the full regional demand base.

The premium client computing tier is where competitive pressure is rising most visibly in the Europe integrated GPU market. Intel’s Panther Lake Arc B390 brought a major jump in client iGPU capability, while Qualcomm’s Snapdragon X2 Elite pushed the performance-per-watt case for Arm-based commercial notebooks with support for DirectX 12.2 Ultimate and Vulkan 1.4. The September 2025 Intel-NVIDIA collaboration to develop x86 SoCs integrating NVIDIA RTX GPU chiplets, backed by a USD 5 billion NVIDIA investment in Intel, is the most consequential strategic move in the current competitive set. If those products reach the market at scale, they could create a new premium class that further narrows the distance between integrated and discrete graphics in high-end notebooks. That possibility raises the stakes for both Intel and AMD in the upper client tiers of the Europe integrated GPU market.

Mobile and embedded strategies are also evolving fast as suppliers try to hold margin and relevance within the Europe integrated GPU market. Samsung’s Exynos 1680 kept AMD-derived graphics IP at the center of its mid-range smartphone differentiation, while MediaTek used richer Arm-based GPU blocks in the Dimensity 9500 and 8500 family to strengthen both flagship and premium mid-range positions. NXP’s i.MX 93W showed another competitive route by building AI, secure wireless connectivity, and Cyber Resilience Act-ready security features into a single embedded processor package. Imagination Technologies remains relevant through its E-Series GPU IP for customers that want programmable graphics and AI capability in mobile, embedded, and edge designs rather than a finished chip from a branded processor vendor.

Europe Integrated GPU Industry Leaders

Intel Corporation

Qualcomm Incorporated

Apple Inc.

MediaTek Inc.

Advanced Micro Devices, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Renesas Electronics completed the acquisition of Irida Labs, a Greece-based company specializing in embedded software for AI-powered visual perception systems. The acquisition strengthens Renesas' edge AI embedded processing offerings and enables system-level solutions that integrate hardware and software for camera and machine vision systems across industrial, robotics, smart city, and healthcare markets.

- May 2026: Semidynamics and SiPearl announced a strategic partnership to develop a European rack-scale AI compute platform for large-scale AI inference, combining SiPearl's high-performance EU-sovereign CPU with Semidynamics' RISC-V-based GPU and AI inference technology, marking a significant step toward European-controlled rack-scale compute infrastructure.

- May 2026: Imagination Technologies released GPU Driver 26.1, introducing Vulkan advancements and Android 17 preview support within its 2026 Long Term Support driver branch, providing SoC vendors early readiness for the next Android graphics baseline and accelerating platform bring-up for PowerVR-based embedded designs.

- May 2025: Broadcom signed FuriosaAI as a new custom AI chip partner, adapting FuriosaAI's Tensor Contraction Processor technology into a multi-die system-on-package using Broadcom's XDSiP technology, targeting high-volume AI inference workloads that may intersect with integrated graphics compute pipelines in future data center configurations.

Europe Integrated GPU Market Report Scope

The Integrated GPU Market encompasses the global industry involved in the design, development, and deployment of graphics processing units integrated into a system-on-chip (SoC) or processor architecture rather than as standalone discrete components. These integrated GPUs share system memory and are widely used to deliver efficient graphics processing across cost-sensitive, power-efficient computing devices.

The Europe Integrated GPU Market is Segmented by Device Category (Desktop and Laptop Processors, Mobile SoCs (Smartphones and Tablets), Embedded and Industrial SoCs, Server and Data Center Processors with Integrated Graphics), Performance Tier (Entry-Level (less than USD 50), Mainstream (USD 50 - USD 150), Performance (USD 150 - USD 300), and High-Performance (greater than USD 300)), and Geography (Germany, United Kingdom, France, Italy, Spain, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Desktop and Laptop Processors |

| Mobile SoCs (Smartphones and Tablets) |

| Embedded and Industrial SoCs |

| Server and Data Center Processors with Integrated Graphics |

| Entry-Level (Less than USD 50) |

| Mainstream (USD 50 - USD 150) |

| Performance (USD 150 - USD 300) |

| High-Performance (Greater than USD 300) |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Device Category | Desktop and Laptop Processors |

| Mobile SoCs (Smartphones and Tablets) | |

| Embedded and Industrial SoCs | |

| Server and Data Center Processors with Integrated Graphics | |

| By Performance Tier | Entry-Level (Less than USD 50) |

| Mainstream (USD 50 - USD 150) | |

| Performance (USD 150 - USD 300) | |

| High-Performance (Greater than USD 300) | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size and forecast of the Europe integrated GPU market?

The Europe integrated GPU market was valued at USD 7.63 billion in 2025, stood at USD 8.62 billion in 2026, and is projected to reach USD 18.42 billion by 2031 at a CAGR of 16.41%.

Which device category held the largest share in Europe?

Mobile SoCs led with 49.45% share in 2025 because Europe has a dense premium smartphone base and a strong shift toward richer integrated graphics in advanced-node mobile processors.

Which segment is expected to grow the fastest through 2031?

Server and Data Center Processors with Integrated Graphics is projected to be the fastest-growing device category at a CAGR of 16.97%, while the Performance tier is projected to grow at 17.34%.

Why is the Windows 11 transition important for integrated GPU demand?

Windows 10 support ended in October 2025, and many existing enterprise PCs could not meet Windows 11 hardware minimums, which pushed buyers toward full device replacement and stronger AI-capable integrated platforms.

Which country leads regional revenue, and which one is growing the fastest?

Germany held the largest share at 28.22% in 2025, while France is projected to record the fastest growth at a CAGR of 17.54% through 2031.

What is shaping competition among suppliers in this space?

Competition is being driven by stronger PC iGPU architectures from Intel and AMD, richer mobile SoCs from Qualcomm, MediaTek, and Samsung, and rising embedded relevance for NXP, STMicroelectronics, and Renesas.

Page last updated on: