North America Gaming GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

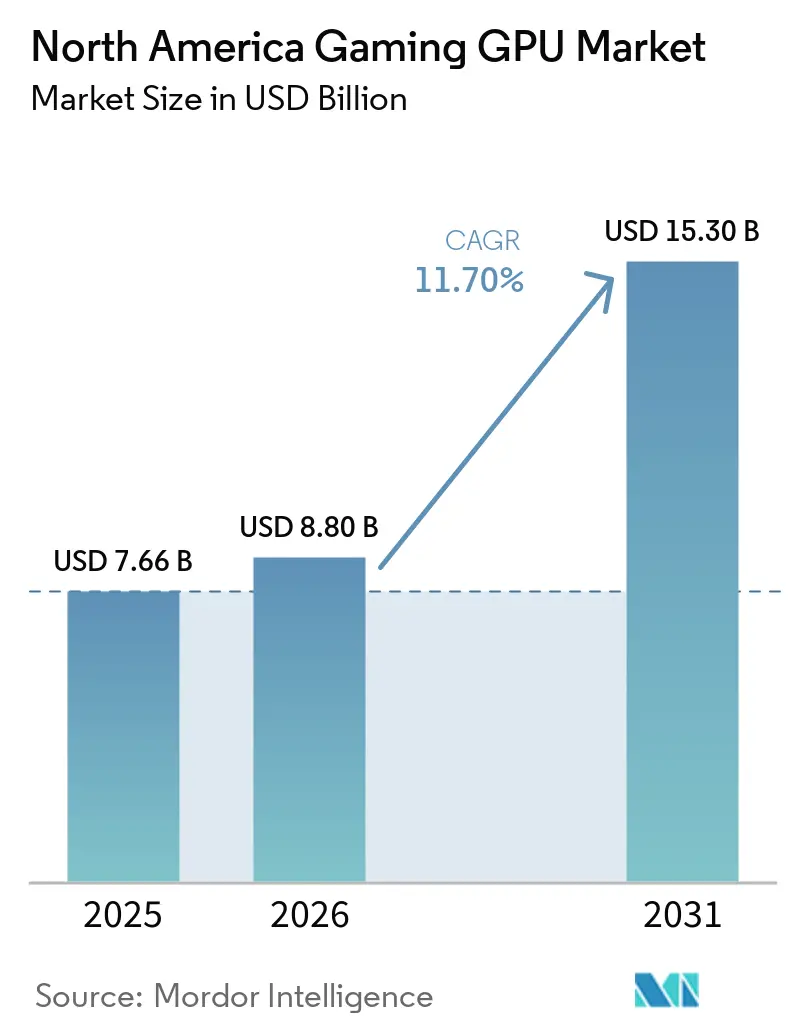

| Base Year Market Size (2025) | USD 7.66 Billion |

| Market Size (2026) | USD 8.80 Billion |

| Market Size (2031) | USD 15.30 Billion |

| Growth Rate (2026 - 2031) | 11.70% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Gaming GPU Market Analysis by Mordor Intelligence

The North America gaming GPU market size is projected to expand from USD 7.66 billion in 2025 and USD 8.80 billion in 2026 to USD 15.30 billion by 2031, registering a CAGR of 11.70% between 2026 to 2031. The North America gaming GPU market is being supported by a faster replacement cycle, as AI upscaling, neural rendering, and ray-traced content are making older hardware feel less capable even before pure raster performance becomes unusable. Consumer spending on video games, hardware, and accessories in the United States reached USD 60.7 billion in 2025 and is projected to rise to USD 62.8 billion in 2026, which keeps the broader demand base healthy for new graphics launches. Unlike the earlier period shaped by crypto swings, the current demand pattern in the North America gaming GPU market is tied more closely to AI-enhanced gaming, premium image reconstruction, and a wider refresh cycle across desktops and laptops. Tariffs, supply constraints in memory, and uneven game release timing may slow near-term unit growth, but they also keep average selling prices firm and preserve value growth. Competitive activity in the North America gaming GPU market is therefore centered on software-led differentiation, tighter product segmentation, and wider access to advanced features across more price tiers.

Key Report Takeaways

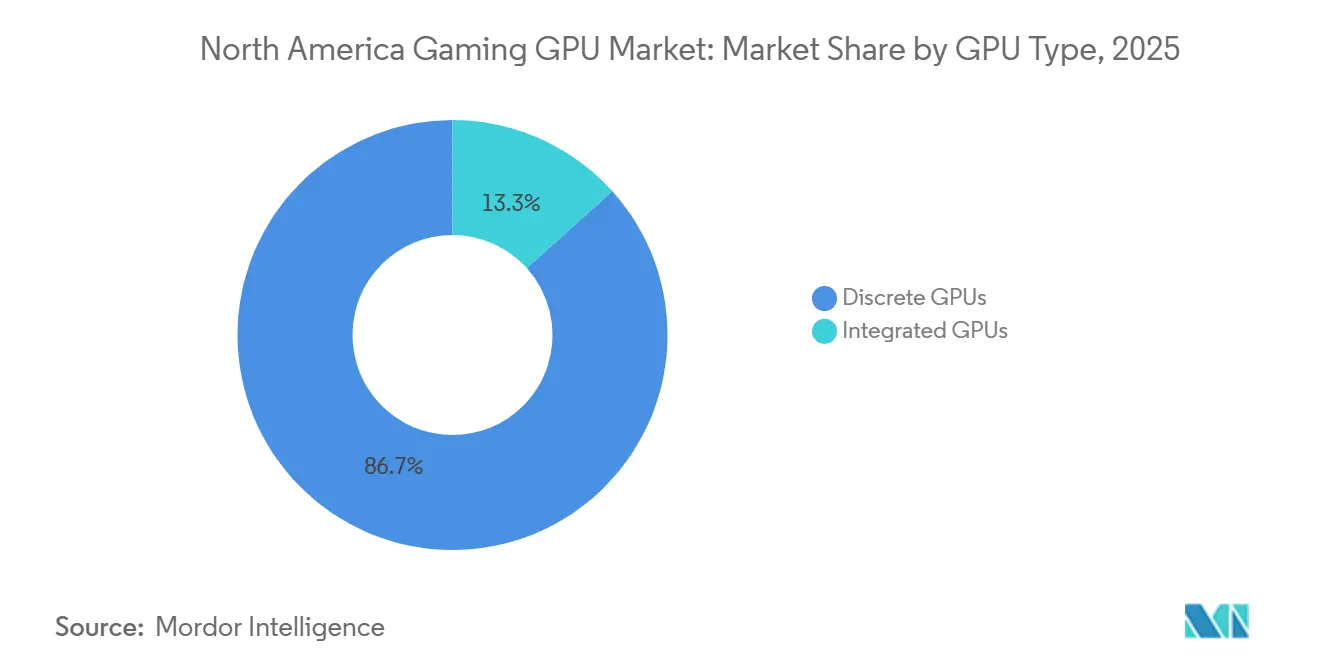

- By GPU type, discrete GPUs held 86.67% revenue share of the North America gaming GPU market in 2025, and the same segment is projected to expand at a 12.12% CAGR through 2031.

- By device type, gaming desktops accounted for a 54.31% share of the North America gaming GPU market size in 2025, while gaming laptops are projected to expand at a 12.67% CAGR through 2031.

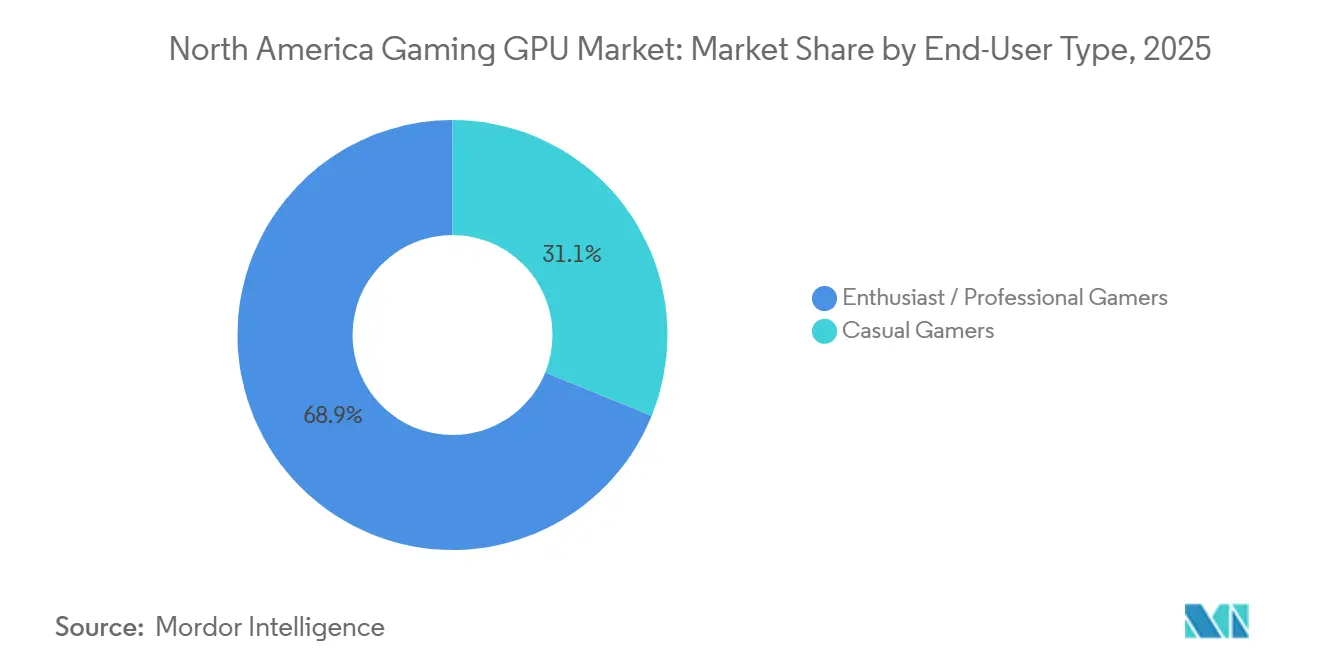

- By end-user type, enthusiast and professional gamers represented 68.88% of the North America gaming GPU market size in 2025, and this segment is projected to grow fastest at a 13.01% CAGR through 2031.

- By memory type, GDDR6X captured 63.16% share of the North America gaming GPU market in 2025, and this segment is projected to expand at a 12.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Gaming GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI Upscaling and Neural Rendering Refresh the Upgrade Cycle | +2.8% | United States dominant, spill-over to Canada | Medium term (2-4 years) |

| AAA Titles and Ray Tracing Raise Baseline GPU Requirements | +2.3% | United States, Canada | Medium term (2-4 years) |

| Esports, Streaming, and Creator Demand Sustain Premium GPU Spend | +1.8% | United States, Canada, with growing esports infrastructure in Mexico | Long term (≥ 4 years) |

| Mobile AAA Pipelines Expand Gaming GPU Demand | +1.3% | North America, United States dominant, Mexico fast-growing mobile base | Long term (≥ 4 years) |

| Vapor-Chamber Designs Unlock Thinner High-Performance Gaming Laptops | +1.0% | United States, Canada | Short term (≤ 2 years) |

| Unreal Engine 5 Mobile Toolchains Improve Premium Phone GPU Monetization | +0.7% | Global, with North America as lead monetization region | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI Upscaling And Neural Rendering Refresh The Upgrade Cycle

In the North America gaming GPU market, AI frame generation is now as important as raw rendering power because the newest visual gains are tied to the latest hardware platforms. NVIDIA introduced DLSS 4.5 at CES 2026 with a second-generation transformer model for super resolution and a new Dynamic Multi Frame Generation capability, and those features were limited to RTX 50-series Blackwell GPUs.[1]NVIDIA Developer Blog, “NVIDIA DLSS 4.5 Delivers Super Resolution Upgrades and New Dynamic Multi Frame Generation,” NVIDIA Developer Blog, developer.nvidia.com That hardware gating changes buyer behavior because an older card can still run a game, yet it cannot deliver the same image reconstruction, latency handling, or frame delivery experience as a newer model. AMD is also pushing further into ML-assisted rendering, with the FSR SDK 2.2 adding ML-powered FSR Upscaling 4.1 and Ray Regeneration 1.1 for RDNA 4 while still keeping analytical fallback modes for older hardware. As more major titles are optimized around these techniques, the North America gaming GPU market is shifting toward shorter upgrade windows and stronger demand for cards that can unlock the full visual stack. This gives an advantage to vendors that can pair hardware launches with a strong software ecosystem and clear feature separation across each product tier.

AAA Titles And Ray Tracing Raise Baseline GPU Requirements

The North America gaming GPU market is also moving upward because current high-end games treat ray tracing and AI-assisted rendering as baseline expectations rather than as optional extras. NVIDIA built the Blackwell GeForce RTX 50 family around fifth-generation Tensor Cores, fourth-generation RT Cores, PCIe Gen 5, and GDDR7 support, which shows how premium gaming workloads are evolving. The company then extended that feature set into the mainstream tier with the RTX 5060 launch in April 2026, which brought DLSS 4 and Multi Frame Generation to a USD 299 product level. AMD responded at Computex 2025 with the Radeon RX 9060 XT and FSR 4 support, confirming that mainstream competition now depends on neural rendering capability as much as on conventional graphics throughput.[2]AMD Investor Relations, “AMD Introduces New Radeon Graphics Cards and Ryzen Threadripper Processors at COMPUTEX 2025,” AMD Investor Relations, ir.amd.com This pushes more buyers toward upper mid-range and enthusiast configurations, because smooth play on high refresh displays increasingly depends on dedicated AI and ray-tracing blocks instead of only raw shader count. As a result, major game releases now have a stronger ability to move spending toward higher performance cards in the North America gaming GPU market.

Esports, Streaming, And Creator Demand Sustain Premium GPU Spend

Competitive gaming remains a durable support for premium graphics demand because serious players buy for low latency, stable frame pacing, and multitasking headroom rather than only for headline frame rates. North America accounted for 42.49% of global esports value in 2025, confirming the region's position as the main commercial center for competitive gaming infrastructure. Circana reported that U.S. consumer spending on video games, hardware, and accessories reached USD 60.7 billion in 2025 and is projected to rise to USD 62.8 billion in 2026, which shows that the wider spending base continues to support premium hardware purchases. That matters in the North America gaming GPU market because streamers, creators, and professional players tend to treat the graphics card as a work-linked purchase instead of a discretionary accessory. Their demand also gives OEMs and board partners a steadier source of revenue when casual spending softens, which helps support premium product launches across the cycle. This pattern keeps the high-performance end of the North America gaming GPU market more resilient than lower-priced tiers.

Mobile AAA Pipelines Expand Gaming GPU Demand

Mobile graphics progress is widening the addressable performance base around the North America gaming GPU market, even though smartphones and tablets still contribute a smaller share of revenue than desktops and laptops. Qualcomm launched the Snapdragon 8 Elite Gen 5 in September 2025 with the Adreno 840 GPU, a 23% performance gain, 20% lower power use, 18 MB of dedicated on-chip cache, and full Unreal Engine 5 support.[3]Qualcomm Technologies, “Snapdragon 8 Elite Gen 5 Product Brief,” Qualcomm Technologies, qualcomm.com MediaTek also launched the Dimensity 9500 in September 2025 with the Arm Mali G1-Ultra GPU, second-generation hardware ray tracing, a 33% peak performance gain, and support for 120 FPS ray-traced mobile gaming through Unreal Engine 5.6 features. These advances matter because they raise consumer expectations for portable gaming quality, and they create a clearer bridge from mobile play into higher-value graphics hardware purchases later on. The effect is strongest in markets where smartphone gaming is the first step into premium gaming ecosystems, which gives the North America gaming GPU market an additional long-range demand path. It also means GPU-related R&D is no longer driven by PCs alone, as mobile silicon makers continue to lift the performance floor for gaming visuals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tariff and Trade Actions Raise Import Costs | -1.6% | United States primary, Canada and Mexico via cascading price effects | Short term (≤ 2 years) |

| Elevated GDDR Pricing Pressures GPU Affordability | -1.3% | Global, with North America retail bearing outsized burden | Medium term (2-4 years) |

| Stronger Integrated Graphics Erode Entry-Level Discrete Demand | -0.9% | United States, Canada | Long term (≥ 4 years) |

| Notebook Thermal Limits Constrain Real-World Performance Gains | -0.5% | United States, Canada | Medium term (2-4 years |

| Source: Mordor Intelligence | |||

Tariff And Trade Actions Raise Import Costs

Section 232 changed pricing conditions in the North America gaming GPU market by imposing a 25% duty on certain imported semiconductors and derivative products from January 15, 2026. Because a large share of add-in-board supply is assembled outside the United States, the added duty lifts landed cost before retail margin, logistics cost, and channel markup are applied. That is hardest to absorb at entry price points, where buyers are more sensitive to price changes and board partners have less flexibility to offset the increase elsewhere. The policy also pushes supply chains to review regional assembly choices more closely, which may support longer-term manufacturing shifts even while near-term shelf prices remain elevated. Canada and Mexico still feel part of that pressure because pricing decisions for the region often start in the U.S. channel and then spread across neighboring markets. The result is a slower unit recovery path for the North America gaming GPU market, even when interest in new launches remains solid.

Elevated GDDR Pricing Pressures GPU Affordability

Memory availability has become a clear affordability constraint in the North America gaming GPU market, especially when flagship products need the newest standards and mainstream cards still depend on premium memory configurations. NVIDIA introduced GDDR7 on the RTX 5090 and RTX 5080 in January 2025, while later products such as the RTX 5060 stayed on GDDR6X, which shows how memory choice is now central to both pricing and product segmentation. AMD kept the Radeon RX 9060 XT in the USD 299 to USD 349 range with GDDR6, highlighting how vendors are balancing bandwidth targets against bill-of-material pressure in the mid-range. Even with those adjustments, retail pricing stayed under pressure in early 2026, and high-end cards continued to trade well above MSRP in key channels. When memory conditions remain tight, board partners lose room for promotions, value-focused buyers delay purchases, and the used market becomes more attractive. That combination makes affordability a persistent drag on the North America gaming GPU market even when product interest remains strong.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By GPU Type: Discrete GPUs Sustain an Unchallenged Hardware Tier

Discrete GPUs held 86.67% of the North America Gaming Graphics Processing Unit (GPU) market share in 2025, and the segment is projected to expand at a 12.12% CAGR through 2031. This combination of scale and speed shows that the North America gaming GPU industry is still being defined by dedicated graphics hardware rather than by shared silicon solutions. NVIDIA's RTX 50-series Blackwell architecture raised the performance floor with fifth-generation Tensor Cores and fourth-generation RT Cores, which reinforced the appeal of discrete gaming products across 2025 and 2026 launches. The RTX 5060 and related Blackwell products also widened access to those features at lower price points, which helped extend the addressable buyer base beyond only the top end.

Integrated GPUs remained the smaller tier in the North America gaming GPU market, even as their performance improved enough to become a credible option for lighter play and value-focused systems. Intel's Panther Lake Arc B390 was benchmarked above the earlier AMD 890M iGPU and near RTX 4050 laptop-class results in entry-level titles, which shows how quickly the baseline is rising for integrated graphics. Even so, shared memory bandwidth, tighter power limits, and weaker performance under heavier ray-traced loads still keep integrated options below discrete cards in demanding play scenarios. That is why dedicated graphics should continue to anchor revenue, profitability, and product differentiation across the forecast period in the North America gaming GPU market.

By Device Type: Desktops Anchor Revenue While Laptops Lead Growth

Gaming desktops accounted for a 54.31% share of the North America Gaming Graphics Processing Unit (GPU) market size in 2025. That lead reflects the strength of enthusiast builders who still prefer full-power discrete cards, larger power budgets, broader upgrade flexibility, and custom cooling that is not available in thinner mobile systems. The Blackwell generation also encouraged fresh desktop builds because it was the first consumer GPU line built around PCIe Gen 5, which added a compatibility reason for platform refresh beyond raw performance gains. In the North America gaming GPU market, desktops therefore remain the core revenue base where premium specifications and add-in-board variety are easiest to monetize.

Gaming laptops are projected to grow at a 12.67% CAGR through 2031, making them the fastest-expanding device type in the North America gaming GPU market. That growth reflects better thermal design, broader OEM support, and stronger consumer acceptance of portable systems that can deliver advanced AI-assisted rendering without giving up premium gaming performance. NVIDIA's laptop rollout for the RTX 50 family, including broad OEM availability and pre-orders across ASUS, Lenovo, HP, MSI, and other brands, helped normalize premium notebook gaming across the region. Smartphones and tablets remain the smallest device segment through 2031, but their graphics capability is rising quickly as Qualcomm and MediaTek bring console-like rendering features into flagship mobile chips.

By End-User Type: Enthusiast And Professional Buyers Define Margin And Growth

Enthusiast and professional gamers represented 68.88% of the North America Gaming Graphics Processing Unit (GPU) market size in 2025, and this segment is projected to grow at a 13.01% CAGR through 2031. That structure is significant because the largest buyer group is also the fastest-growing one, which places premium performance at the center of the North America gaming GPU industry rather than at its edge. This group includes competitive players, streamers, and digital creators who value rendering headroom, strong encoding support, and stable performance under heavy multitasking. Premium demand also held up despite higher street prices, as high-end cards continued to sell above MSRP in early 2026 across major retail channels.

Casual gamers remained the smaller end-user tier, and they faced the greatest pressure from tariffs, higher memory-linked costs, and a softer willingness to absorb premium pricing. Circana said that more than one-third of U.S. gamers planned to buy fewer full-price games or wait longer for discounts in 2026, which points to broader caution in discretionary spending that can spill over into hardware purchases. AMD still reported gaming segment revenue of USD 720 million in Q1 2026, up 11% year over year, which shows that premium gaming hardware spending continued to expand even in a tougher affordability environment.[4]AMD, “AMD Reports First Quarter 2026 Financial Results,” AMD, amd.com The split between performance-focused buyers and price-sensitive buyers is therefore becoming more visible across the North America gaming GPU market, with premium tiers carrying a growing share of value.

By Memory Type: GDDR6X Sets The Performance Benchmark While Unified Memory Gains Ground

GDDR6X held 63.16% of the North America Gaming Graphics Processing Unit (GPU) market size in 2025, and the segment is projected to expand at a 12.44% CAGR through 2031. Its lead reflects the large installed base tied to NVIDIA's recent gaming generations and the continued relevance of high-bandwidth memory for AI-assisted rendering and ray-traced workloads. NVIDIA's RTX 5060 launch confirmed that GDDR6X remains part of the current cycle even as the company moved GDDR7 into the very top end of the stack. That keeps GDDR6X important in the North America gaming GPU market because it sits at the point where performance demand and cost discipline still meet.

GDDR6 remained the second-largest memory tier and continued to support value-oriented products, especially AMD's RX 9000-series mainstream cards. AMD's RX 9060 XT launch at Computex 2025 showed that GDDR6 still has a strong role in the mid-range, where price sensitivity is higher, but buyers still expect modern upscaling and competitive frame rates. Unified memory and other memory types remain smaller in revenue terms, but they are gaining relevance as mobile and tightly integrated platforms improve their gaming performance and developer support. The practical effect is a more layered memory landscape, where the North America gaming GPU market continues to reward bandwidth-heavy dedicated cards while gradually opening more use cases for integrated and mobile architectures.

Geography Analysis

The United States held the largest country-level revenue share in the North America gaming GPU market in 2025. Its lead comes from a deep gaming PC base, strong retail availability, a large creator economy, and spending levels that can support premium GPU configurations. Circana reported that U.S. consumer spending on video games, hardware, and accessories reached USD 60.7 billion in 2025 and is projected to reach USD 62.8 billion in 2026, which keeps the surrounding demand environment favorable for successive GPU launches. U.S.-bound inventory is also the first to feel the full effect of Section 232 tariff compliance, which means the country will remain the main pricing reference point for the region through 2026 and 2027.

Canada is the second-largest geography in the North America gaming GPU market, and it is also the fastest-growing country in the wider regional gaming hardware ecosystem at a 15.05% CAGR through 2031. That growth reflects a smaller installed base catching up, a larger premium laptop audience, and a stronger esports presence around Toronto, Vancouver, and Montreal. OEM support has closely tracked the United States, with GeForce RTX 50-series laptops reaching Canadian channels alongside the broader North American rollout. Canada still remains linked to U.S. pricing behavior because much of the import and channel structure flows through the same regional supply path. That means tariff-driven price floors in the United States usually appear in Canada with a lag rather than staying isolated in one market.

Mexico is the fastest-emerging demand center in the North America gaming GPU market, even though it remains smaller than the United States and Canada in total value. A growing middle class, a mobile-first gamer base, and rising interest in streaming and higher-quality play are widening the addressable audience for more capable graphics hardware. That dynamic is helped by flagship mobile platforms from Qualcomm and MediaTek, which are bringing stronger graphics performance and Unreal Engine 5 support into premium smartphones sold across North America. The Rest of North America remains a smaller contributor and usually follows U.S. product timing and price trends with limited delay.

Competitive Landscape

The North America gaming GPU market remained highly concentrated at the chip design layer in 2025, even though the final board and system ecosystem was broader. NVIDIA controlled 94% of discrete add-in-board GPU shipments in Q4 2025, while AMD fell to near 5%, leaving very little room for a scaled third player in consumer gaming graphics. That lead is reinforced by software advantages, AI rendering exclusivity, and the ability to separate gaming products from compute-oriented products across the Blackwell stack. The result is a North America gaming GPU market where one supplier sets much of the pricing tone, feature cadence, and competitive benchmark.

AMD remained relevant by pushing the Radeon RX 9060 XT into the USD 299 to USD 349 range with RDNA 4 and FSR 4 support, which preserved a viable mainstream alternative for value-focused buyers. NVIDIA answered across a broader spread of price points with the RTX 5060 in April 2026 and the RTX 5050 in May 2026, extending DLSS 4 and Blackwell features deeper into the volume market. At the partner level, ASUS, MSI, GIGABYTE, PNY, and ZOTAC remained important because cooling design, board size, power delivery, and local availability still shape final purchase decisions after the chip vendor is chosen. CES 2026 also showed how aggressively board makers are differentiating through compact cards, hybrid cooling, display integration, and thinner notebook platforms. GIGABYTE further deepened its collaboration with AMD in January 2026 to advance on-device AI across gaming laptops, motherboards, and monitors, which shows that partners are trying to build platform positioning beyond stand-alone GPU hardware.

Intel has become more of a boundary condition than a full-scale challenger in the North America gaming GPU market, because its strongest current influence comes from integrated graphics gains at the low end. Panther Lake results indicate that integrated graphics are improving enough to pressure entry-level discrete demand in lighter gaming scenarios. White-space opportunity remains stronger in mobile gaming GPUs and handheld-oriented graphics, where Qualcomm, MediaTek, and Intel are all trying to turn stronger graphics blocks into more sustained gaming use and better content support. Even with that emerging pressure at the edge, the competitive center of gravity in the North America gaming GPU market still sits with NVIDIA and a narrow group of large board partners.

North America Gaming GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Qualcomm Incorporated

Apple Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: NVIDIA announced the GeForce RTX 5050 desktop and laptop GPU lineup, bringing the Blackwell RTX architecture to the entry-tier at USD 249 for desktop and USD 999 for laptops. This launch filled the last price gap in the RTX 50 series and extended DLSS 4 Multi Frame Generation access to budget-conscious gamers, broadening the total addressable market for NVIDIA-exclusive AI rendering features.

- April 2026: NVIDIA launched the GeForce RTX 5060 desktop GPU family at USD 299, delivering DLSS 4 with Multi Frame Generation and Blackwell neural rendering capabilities at a mainstream price point for the first time. Stock-clocked and overclocked models became available from ASUS, GIGABYTE, MSI, PNY, and ZOTAC, accelerating board-partner manufacturing activity across the RTX 50 ecosystem.

- March 2026: NVIDIA announced multiyear strategic agreements with Lumentum Holdings, including a USD 2 billion investment in Lumentum to support RandD and U.S.-based manufacturing of advanced laser components. This positions NVIDIA to secure next-generation optical interconnect technology critical to GPU cluster infrastructure as AI workloads scale beyond standalone chip configurations.

- February 2026: NVIDIA reported record fourth-quarter fiscal 2026 revenue of USD 68.1 billion, up 73% year-over-year. Gaming GPU momentum came from the RTX 50 series laptop ramp, with pre-orders from ASUS, Gigabyte, HP, Lenovo, and MSI opening February 25, 2026 ahead of March retail availability, with RTX 5090 laptops starting at USD 4,299 and RTX 5080 laptops at USD 2,499.

North America Gaming GPU Market Report Scope

The North America Gaming GPU Market refers to the market for graphics processing units used in gaming devices and systems across the United States, Canada, and Mexico. It includes discrete and integrated gaming GPUs that improve frame rendering, visual quality, and real-time gaming performance by processing large amounts of data in parallel.

The North America Gaming GPU Market Report is Segmented by GPU Type (Discrete GPUs, and Integrated GPUs), Device Type (Gaming Desktops, Gaming Laptops, and Smartphones and Tablets (Mobile Gaming)), End-User Type (Casual Gamers, and Enthusiast and Professional Gamers), Memory Type (GDDR6, GDDR6X, Legacy Graphics Memory, and Unified Memory), and Country. The Market Forecasts are Provided in Terms of Value (USD).

| Discrete GPUs |

| Integrated GPUs |

| Gaming Desktops |

| Gaming Laptops |

| Smartphones and Tablets |

| Casual Gamers |

| Enthusiast and Professional Gamers |

| GDDR6 |

| GDDR6X |

| Legacy Graphics Memory |

| Unified Memory |

| United States |

| Canada |

| Mexico |

| By GPU Type | Discrete GPUs |

| Integrated GPUs | |

| By Device Type | Gaming Desktops |

| Gaming Laptops | |

| Smartphones and Tablets | |

| By End-User Type | Casual Gamers |

| Enthusiast and Professional Gamers | |

| By Memory Type | GDDR6 |

| GDDR6X | |

| Legacy Graphics Memory | |

| Unified Memory | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America gaming GPU market?

The North America gaming GPU market was valued at USD 7.66 billion in 2025, is projected at USD 8.80 billion in 2026, and is forecast to reach USD 15.30 billion by 2031 at an 11.70% CAGR.

Which GPU type leads demand in North America gaming systems?

Discrete GPUs lead by a wide margin, holding 86.67% of revenue in 2025, and they are also the fastest-growing GPU type through 2031.

Why are gamers upgrading graphics cards more quickly now?

AI upscaling, neural rendering, and ray-traced gaming are making newer GPUs more valuable because many advanced features are tied to the latest hardware generations.

Which device category is growing fastest for gaming graphics demand?

Gaming laptops are the fastest-growing device segment, projected to expand at a 12.67% CAGR through 2031, while desktops still lead current revenue.

Which buyer group drives the most value in this space?

Enthusiast and professional gamers are the largest and fastest-growing end-user group, holding 68.88% share in 2025 and expanding at a 13.01% CAGR.

How are tariffs affecting GPU pricing in North America?

U.S. Section 232 tariffs have raised imported semiconductor costs from January 2026, which increases landed prices and makes entry-level cards harder to price competitively.

Page last updated on: