Discrete GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 96.06 Billion |

| Market Size (2031) | USD 229.29 Billion |

| Growth Rate (2026 - 2031) | 19.01% CAGR |

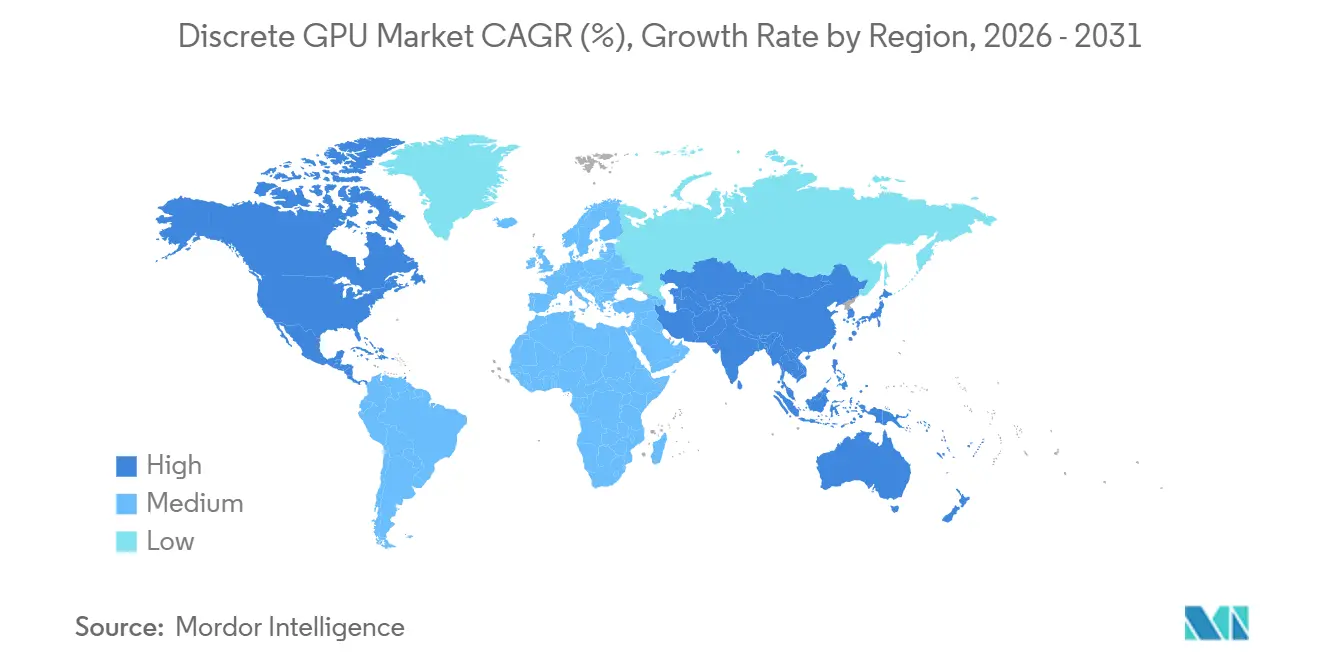

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

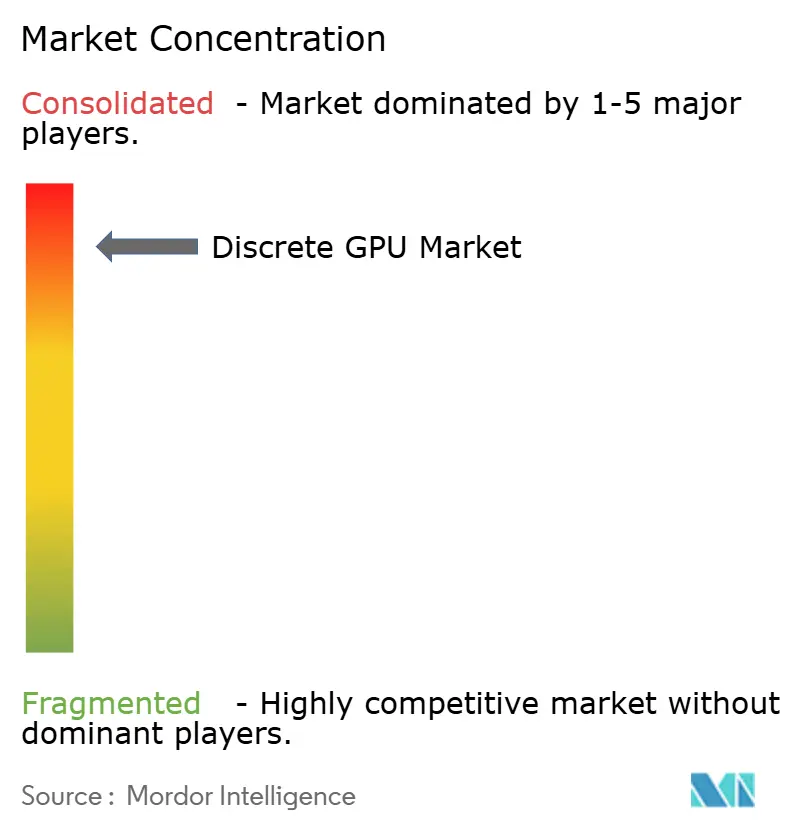

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Discrete GPU Market Analysis by Mordor Intelligence

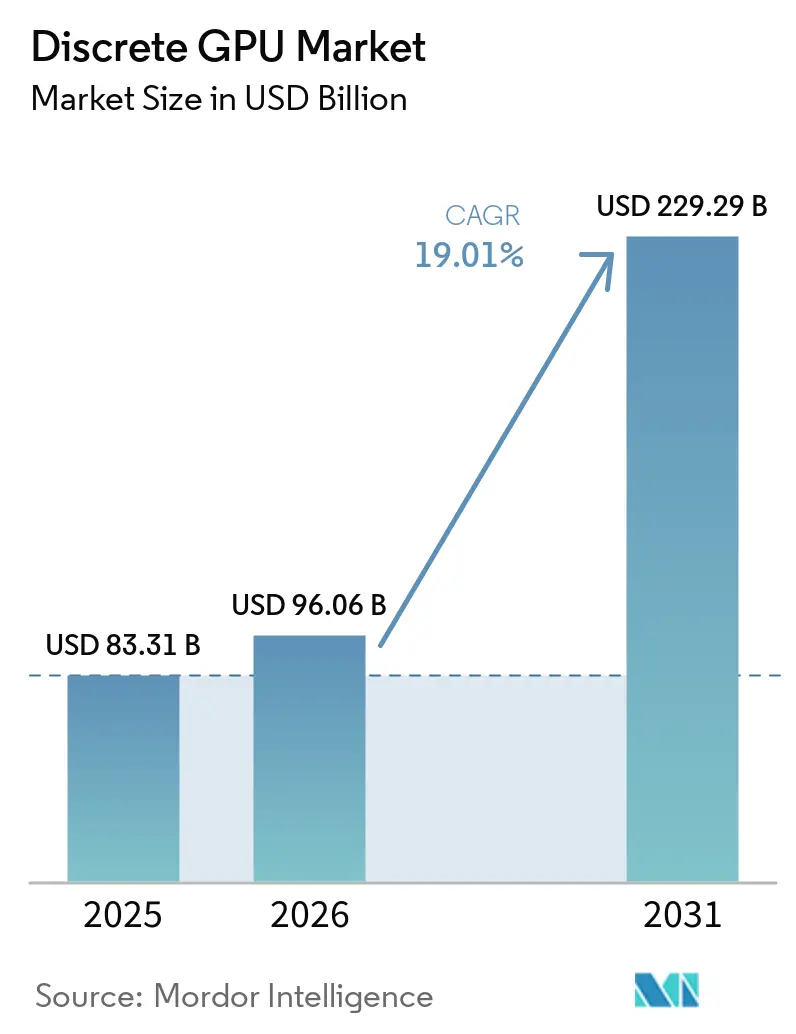

The discrete GPU market size is projected to be USD 83.31 billion in 2025, USD 96.06 billion in 2026, and reach USD 229.29 billion by 2031, growing at a CAGR of 19.01% from 2026 to 2031. Demand has shifted much faster than in earlier semiconductor cycles because AI training and, more importantly, AI inference have become the main drivers of demand in a short period. This has changed revenue priorities across the value chain, but gaming and professional visualization still remain important because they support architecture development, software tools, driver work, and long-term foundry relationships. The discrete GPU market is also being supported by rising cloud build-outs in Asia-Pacific and by continued demand for premium gaming and workstation systems. At the same time, memory tightness and export review complexity are limiting how quickly supply can respond, which is slowing upside rather than weakening the core demand picture. Competitive pressure remains strongest around NVIDIA, while AMD is pushing harder into data center accelerators, and Intel is using partnerships to stay relevant in future CPU-GPU system designs.

Key Report Takeaways

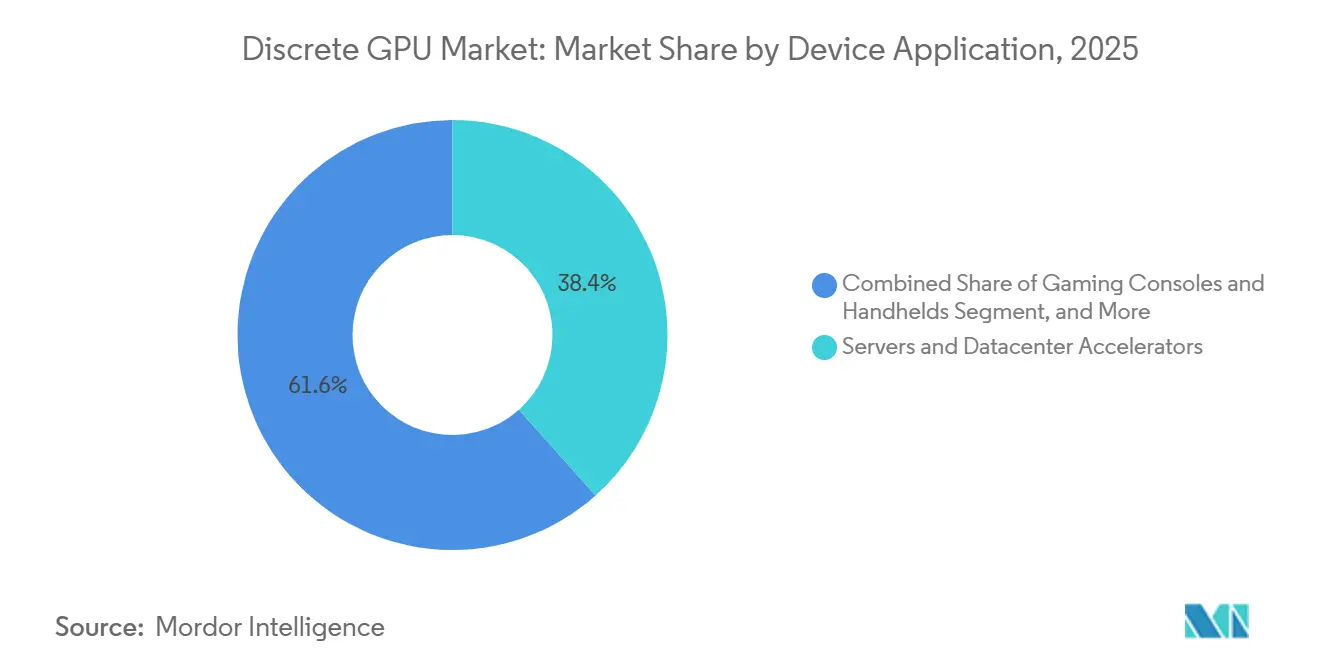

- By device application, servers and datacenter accelerators led with a 38.42% revenue share in 2025, and it is projected to expand at a 19.76% CAGR through 2031.

- By memory type, GDDR-based GPUs held 68.34% share in 2025, while HBM-based GPUs are projected to expand at a 20.18% CAGR through 2031.

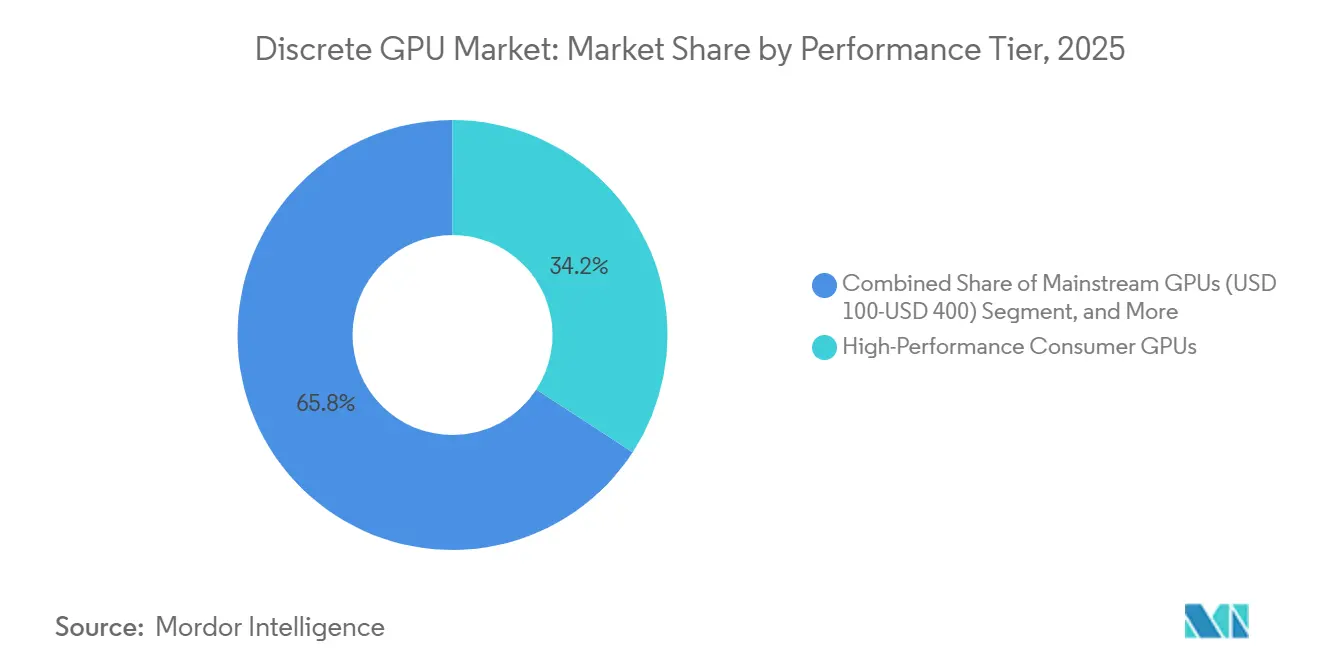

- By performance tier, High-Performance Consumer GPUs accounted for 34.18% of the discrete GPU market share in 2025, while Data Center and AI Accelerator GPUs are projected to expand at a 20.24% CAGR through 2031.

- By geography, Asia-Pacific held 42.57% of the discrete GPU market share in 2025 and is projected to expand at a 19.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Discrete GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI Training and Inference Demand for Discrete Accelerators | +7.2% | Global, with North America and Asia-Pacific as primary nodes | Short term (≤ 2 years) |

| Premium Gaming and Esports Visual Fidelity Upgrades | +4.3% | Asia-Pacific, North America, Europe | Medium term (2-4 years) |

| Creator and Professional Visualization Workstation Refresh | +2.8% | North America, Europe, Japan | Medium term (2-4 years) |

| Laptop GPU Adoption for Portable Gaming and AI-Creation Workloads | +2.1% | Asia-Pacific, North America | Medium term (2-4 years) |

| Local AI Inference on Deskside Workstations | +1.4% | North America, Europe, Japan | Medium term (2-4 years) |

| China Domestic GPU Substitution and Sovereign Stack Buildout | +1.0% | China, with spillover to broader Asia-Pacific sovereign AI programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI Training and Inference Demand for Discrete Accelerators

The discrete GPU market is being reshaped by AI infrastructure spending, and live inference demand is now rising fast enough to stand beside training as a core buying driver. NVIDIA reported USD 197.3 billion in fiscal 2026 data center revenue out of total revenue of USD 215.9 billion, underscoring how deeply AI workloads have reshaped the revenue mix of the leading supplier.[1]NVIDIA Corporation, “NVIDIA Reports Financial Results for Fourth Quarter and Fiscal 2026,” NVIDIA Newsroom, nvidianews.nvidia.com The same company indicated that inference accounted for a meaningful share of data center activity, suggesting that the spending base is shifting from model construction to production deployment. AMD is pursuing the same part of the market, as its data center segment reached USD 5.75 billion in Q1 2026, up 57% year over year, supported by Instinct shipments and hyperscaler demand, including Meta deployments. This matters for the discrete GPU market because inference creates broader, repeatable demand across clouds, enterprises, and sovereign compute programs, rather than relying on only a small number of training clusters. It also means competitive strength now depends on packaging, system design, interconnects, and software support as much as on the chip itself.

Premium Gaming and Esports Visual Fidelity Upgrades

Premium gaming remains a durable demand driver because higher-end buyers are paying for both visual quality and software features that extend the relevance of cards over time. NVIDIA launched the GeForce RTX 5090 at USD 1,999, the RTX 5080 at USD 999, the RTX 5070 Ti at USD 749, and the RTX 5070 at USD 549, which set the pricing anchor for the top end of the gaming stack. NVIDIA also stated that more than 800 games and applications use RTX and DLSS technologies, indicating that upgrade demand is supported by a deep software base rather than hardware specifications alone. In the discrete GPU market, this software tie-in matters because players tend to stay within platforms that preserve feature access and game optimization. Neural rendering, ray tracing, and higher fidelity requirements are therefore shortening the useful life of older cards in competitive and enthusiast gaming. This keeps gaming important to the discrete GPU market even while AI accelerators lead revenue growth, because gaming still supports developer tools, driver ecosystems, and product cadence across the wider stack.

Creator and Professional Visualization Workstation Refresh

Workstation demand is shifting from graphics-only use toward mixed workloads that include rendering, simulation, and local AI inference. Lenovo announced the ThinkStation P4 in May 2026 with AMD Ryzen PRO 9000 Series processors and the NVIDIA RTX PRO 6000 Blackwell Workstation Edition, demonstrating how OEMs are now positioning workstations as local AI systems rather than just CAD machines. The same launch highlighted 96 GB of GDDR7 ECC memory, suggesting rising memory requirements in advanced design, media, and model inference workflows. This supports higher selling prices in the discrete GPU market because enterprise buyers increasingly value a single machine that can handle visualization and secure local AI workloads within the same system. It also reduces the appeal of sending every workflow to cloud services when privacy, latency, or recurring API cost becomes a concern. As a result, workstation refresh demand is becoming more tied to long-run economics and internal control than to graphics performance alone.

Laptop GPU Adoption for Portable Gaming and AI-Creation Workloads

The discrete GPU market is also expanding, with laptops now supporting both high-end gaming and creator workloads in portable form factors. ASUS introduced the 2026 ROG Strix SCAR 18 with up to an NVIDIA GeForce RTX 5090 Laptop GPU at 175W TGP and a 4K 240Hz mini-LED panel, demonstrating how far mobile systems have come toward desktop-class performance. ASUS also launched the 2026 ROG Strix G16 and G18 with Intel Core Ultra 9 290HX Plus processors and up to the GeForce RTX 5080 Laptop GPU, reinforcing that premium mobile designs remain central to vendor road maps. Portable AI content creation and development work now matters alongside gaming, especially for buyers who care more about memory capacity, software compatibility, and mobility than about peak benchmark results. This widens the addressable customer base for notebook dGPU sales in the discrete GPU market. It also supports premium pricing in regions where users want one system for gaming, video work, design tasks, and local model experimentation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Memory Supply Tightness and Rising Board Costs | -2.8% | Global, with acute pricing pressure in the gaming GPU segment in North America and Europe | Short term (≤ 2 years) |

| Integrated Graphics and Powerful Notebooks Squeezing Entry-Level dGPU Demand | -1.9% | Global, with the greatest impact in the Asia-Pacific and Europe thin-and-light laptop markets | Medium term (2-4 years) |

| Export Controls and China-Specific Import Restrictions Distorting Product Mix | -1.5% | China, with spillover to the Asia-Pacific and the Middle East channel pricing | Long term (≥ 4 years) |

| Power, Thermals, and PSU Upgrade Burden at the High End | -0.8% | North America, Europe, Japan, and markets with high-end gaming and workstation concentrations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Memory Supply Tightness and Rising Board Costs

The discrete GPU market continues to face memory tightness because AI accelerators and gaming boards are drawing from overlapping advanced memory and packaging resources. NVIDIA’s GeForce RTX 50-series moved gaming cards further into GDDR7, which raised the baseline memory requirement for premium consumer products. Samsung began commercial HBM4 shipments in 2026 for AI computing, confirming that suppliers are expanding capacity but also showing how quickly advanced memory is being pulled into accelerator programs. When HBM and high-end graphics memory are in tight supply at the same time, board costs rise, and the lower end of the discrete GPU market loses pricing flexibility. That pressure is hardest on add-in-board partners that do not have the same purchasing scale as the largest brands. It also limits how quickly vendors can push supply beyond flagship products, even when end demand stays strong.

Integrated Graphics and Powerful Notebooks Squeezing Entry-Level GPU Demand

Entry-level discrete GPUs are under pressure because integrated graphics now cover a larger share of casual gaming and creator tasks than they did a few years ago. Thin-and-light notebooks are benefiting the most because buyers in that category often prefer lower power draw, lower system cost, and simpler thermal design over a separate entry card. This changes the mix of the discrete GPU market by pushing vendors toward the mainstream and premium price bands, where dedicated graphics still offer a clearer advantage. It also weakens the historical volume base that once came from low-cost add-in cards and entry notebook attach rates. The effect is structural rather than temporary because integrated solutions are improving across both consumer and professional use cases. As a result, the bottom tier of the discrete GPU market is likely to remain under pressure even if premium demand stays healthy.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Application: Servers and Datacenter Accelerators Lead Demand

Servers and datacenter accelerators accounted for 38.42% of the discrete GPU market in 2025, making them the largest device application segment. This position reflects demand that is no longer centered only on model training and is increasingly tied to production inference across cloud, enterprise, and sovereign compute environments. NVIDIA’s fiscal 2026 data center revenue reached USD 197.3 billion, indicating how much spending has already shifted toward accelerator systems. AMD also reported USD 5.775 billion in Q1 2026 data center segment revenue, supported by Instinct deployments at hyperscalers, including Meta.[2]AMD, “AMD Reports First Quarter 2026 Financial Results,” AMD Newsroom, amd.com The discrete GPU market is therefore being pulled by server platforms that combine silicon, packaging, networking, and software into full compute systems rather than by standalone chips alone.

PCs and workstations remained the second-largest revenue pool, as premium gaming cards and enterprise workstations continued to command high selling prices. Lenovo’s ThinkStation P4 launch in May 2026, built around AMD Ryzen PRO 9000 Series processors and the NVIDIA RTX PRO 6000 Blackwell Workstation Edition, shows how workstation demand is moving toward local AI inference and advanced visualization in a single machine. Gaming consoles and handhelds still shape visual expectations across the wider ecosystem, but they do not contribute directly to the add-in-board channel that defines most of the discrete GPU industry. Automotive and ADAS applications are expanding from a small base as in-vehicle compute needs rise, while mobile devices, tablets, and other embedded uses remain constrained by thermal and power limits. This keeps the discrete GPU market concentrated in segments where performance density and memory scale justify the extra hardware cost.

By Memory Type: HBM Expands Fast While GDDR Keeps Volume Leadership

HBM-based GPUs are projected to expand at a 20.18% CAGR from 2026 to 2031, making HBM the fastest-growing memory type in the discrete GPU market. That growth is tied to AI accelerators, where memory bandwidth and capacity have become core purchase criteria for hyperscalers and sovereign compute programs. Samsung stated in 2026 that it had begun commercial shipments of HBM4 for AI computing, indicating that memory suppliers are already advancing toward the next architecture cycle. Even so, HBM remains concentrated in the highest-value parts of the market because it has a tighter supply, more complex packaging requirements, and a higher system cost than consumer graphics memory. This means the discrete GPU market will continue to treat HBM as a strategic accelerator technology rather than as a broad-based standard across all product classes.

GDDR-based GPUs held 68.34% of the discrete GPU market share in 2025 because gaming, workstation, and mobile products still rely on a lower-cost, more thermally efficient memory approach. NVIDIA’s GeForce RTX 50-series products launched with GDDR7, indicating that the mainstream and premium gaming stack is still moving forward along the GDDR path rather than shifting to HBM. This keeps GDDR in volume leadership, since it remains the practical option for cards below the very top end of the pricing ladder. The split between HBM growth and GDDR volume leadership is central to the discrete GPU market because it shows that memory architecture is now dividing products by use case, price point, and deployment model more clearly than before.

By Performance Tier: Premium Demand Holds While the Low-End Faces Pressure

High-Performance Consumer GPUs accounted for 34.18% of 2026 revenue, which made them the largest performance-tier segment in the discrete GPU market. That share was supported by premium pricing across NVIDIA’s GeForce RTX 50-series lineup, with the RTX 5090 launching at USD 1,999 and the RTX 5080 at USD 999. The segment also benefited from buyers who wanted stronger ray tracing, neural rendering support, and more memory headroom for gaming and creator tasks. This part of the discrete GPU market remains resilient because it attracts users who upgrade for a better experience, not just for basic frame-rate gains. It also benefits from the fact that premium buyers are less sensitive to component inflation than entry buyers.

Data Center and AI Accelerator GPUs are projected to expand at a 20.24% CAGR through 2031, which makes them the fastest-growing performance tier in the market. That pace reflects a widening gap between consumer card economics and accelerator system economics, where enterprise buyers are willing to absorb far higher average selling prices when they are tied to productive AI workloads. Mainstream GPUs in the USD 100-USD 400 range are facing pressure from stronger integrated graphics and rising board costs, which are narrowing their value advantage. Low-cost GPUs below USD 100 face the deepest structural disruption, which means future growth in the discrete GPU market is likely to stay concentrated in premium consumer products and enterprise accelerators rather than in the bottom end of the stack.

Geography Analysis

China remains central to that position because it combines very large AI compute demand with policy support for domestic alternatives when access to the highest-end imported accelerators is restricted. The export review changes in early 2026 did not reduce complexity, and the documentary burden around advanced chip shipments continued to shape how vendors approached the China channel. Asia-Pacific also plays a critical role in supplying memory and advanced components, as Samsung’s commercial HBM4 shipments in 2026 underscored the region’s importance to accelerator readiness.[3]Samsung Electronics, “Samsung Ships Industry-First Commercial HBM4 With Ultimate Performance for AI Computing,” Samsung Global Newsroom, news.samsung.com Japan and South Korea remain important sources of premium gaming and professional visualization demand, while India and Southeast Asia are expanding through cloud GPU build-outs and a larger gaming user base.

North America remained the second-largest geography in the discrete GPU market because hyperscaler AI spending, premium gaming demand, and high-end workstation purchases all stayed concentrated in the region. NVIDIA and Intel announced a multi-generational collaboration in September 2025 to develop custom data center CPUs and x86 systems with NVIDIA RTX GPU chiplets, which reinforced North America’s role in future platform integration. NVIDIA and Corning also announced a multiyear partnership in May 2026 to expand US optical connectivity manufacturing capacity, linking GPU demand more directly to domestic AI infrastructure deployment. At the same time, export review rules continued to affect regional channel strategy because North American vendors still had to manage compliance for international shipments.

Europe’s discrete GPU market is split between a mature gaming and workstation base in major Western markets and a growing push toward sovereign AI compute capacity. The Middle East and Africa remain smaller in absolute size, but investment in AI infrastructure in the Gulf is improving the region’s relevance to future accelerator deployment. South America is centered on Brazil and Argentina, where demand is strongest in gaming and content creation but remains highly price sensitive. Across all 3 of these regions, the discrete GPU market is benefiting from the same long-run AI and premium graphics trends, but local growth still depends heavily on infrastructure funding, import conditions, and the availability of higher-end products.

Competitive Landscape

At the chip-design level, NVIDIA held around 94% of desktop add-in-board GPU revenue in Q4 2025, with AMD near 5% and Intel below 1%, leaving the competitive balance of the discrete GPU market heavily skewed toward one vendor. That lead is reinforced by software and platform depth, including a gaming ecosystem with more than 800 RTX-enabled games and applications. In the discrete GPU market, this software position matters because buyers often optimize around existing tools and deployed workflows rather than around raw hardware parity. AMD remains the main alternative in data center GPUs, with Q1 2026 data center segment revenue reaching USD 5.75 billion, indicating that hyperscalers are willing to qualify a second accelerator stack. Intel still has a small market presence, but it retains strategic value because it can link x86 platforms, packaging, and manufacturing to future GPU system designs.

NVIDIA has widened its moat through partnerships and supply-chain moves rather than solely through chip launches. In September 2025, NVIDIA and Intel announced a multi-generational collaboration on custom data center CPUs and x86 systems with NVIDIA RTX GPU chiplets, which reshaped the commercial path for tighter CPU-GPU integration across the PC stack. In May 2026, NVIDIA and Corning agreed on a multiyear partnership to expand US optical connectivity manufacturing, which extended NVIDIA’s position further into the infrastructure layer that supports AI factories.[4]Corning Incorporated, “NVIDIA and Corning Announce Long-Term Partnership To Strengthen U.S. Manufacturing for AI Infrastructure,” Corning News Release, corning.com AMD, meanwhile, tied its Instinct road map to larger hyperscaler programs and continued to present the data center segment as the center of its GPU growth strategy.

The add-in-board layer remains more fragmented than chip design, with ASUS, MSI, GIGABYTE, ZOTAC, SAPPHIRE, and Palit competing mostly through cooling, software, channel execution, and limited factory tuning. That part of the discrete GPU market has limited room for margin expansion unless vendors move into AI workstations, liquid-cooled systems, or enterprise integration. China’s domestic suppliers are becoming more strategically relevant because export restrictions have made local substitution a policy priority, even though their present global revenue footprint remains small. The result is a discrete GPU market that is likely to stay highly concentrated at the top while becoming more specialized at the system, product, and regional levels.

Discrete GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

ASUSTeK Computer Inc.

Micro-Star International Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: AMD announced more than USD 10 billion in investments across the Taiwan ecosystem, targeting advanced packaging capacity for the AMD Helios rack-scale platform featuring AMD Instinct MI450X GPUs and 6th Gen EPYC CPUs. The Helios platform is on track for multi-gigawatt customer deployments beginning in the second half of 2026.

- May 2026: Lenovo announced the ThinkStation P4, the first workstation combining AMD Ryzen PRO 9000 Series processors with NVIDIA RTX PRO 6000 Blackwell Workstation Edition GPUs featuring 96 GB GDDR7 ECC memory, designed for on-device AI inference, simulation, and large-scale rendering without cloud dependency.

- May 2026: NVIDIA and IREN Limited announced a strategic partnership to deploy up to 5 gigawatts of NVIDIA DSX-aligned AI infrastructure across IREN's global datacenter pipeline, as part of the agreement, IREN issued to NVIDIA a five-year right to purchase up to 30 million shares at USD 70 per share, representing a potential investment of up to USD 2.1 billion.

- May 2026: NVIDIA and Corning announced a multiyear commercial and technology partnership under which Corning will expand US-based optical connectivity manufacturing capacity by 10x and build 3 new advanced manufacturing facilities in North Carolina and Texas, creating more than 3,000 jobs, to support AI factory buildouts powered by NVIDIA accelerators.

Global Discrete GPU Market Report Scope

The scope of the report covers the analysis of the discrete GPU market, which includes standalone graphics processing units designed to handle complex graphical computations independently of the central processing unit. The study examines market trends, growth drivers, challenges, and opportunities, providing insights into the competitive landscape and technological advancements. The report focuses on the market dynamics during the forecast period, offering a comprehensive understanding of the discrete GPU market's current and future potential.

The Discrete GPU Market is Segmented by Device Application (Mobile Devices and Tablets, PCs and Workstations, Servers and Datacenter Accelerators, Gaming Consoles and Handhelds, Automotive / ADAS, and Other Embedded and Edge Devices), Memory Type (GDDR-based GPUs, and HBM-based GPUs), Performance Tier [Low-Cost GPUs (Less Than USD 100), Mainstream GPUs (USD 100-USD 400), High-Performance Consumer GPUs (USD 400-USD 1,200), Data Center / AI Accelerator GPUs (Greater than USD 1,200)], and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

| Mobile Devices and Tablets |

| PCs and Workstations |

| Servers and Datacenter Accelerators |

| Gaming Consoles and Handhelds |

| Automotive / ADAS |

| Other Embedded and Edge Devices |

| GDDR-based GPUs |

| HBM-based GPUs |

| Low-Cost GPUs (Less than USD 100) |

| Mainstream GPUs (USD 100-USD 400) |

| High-Performance Consumer GPUs (USD 400-USD 1,200) |

| Data Center / AI Accelerator GPUs (Greater than USD 1,200) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Device Application | Mobile Devices and Tablets | ||

| PCs and Workstations | |||

| Servers and Datacenter Accelerators | |||

| Gaming Consoles and Handhelds | |||

| Automotive / ADAS | |||

| Other Embedded and Edge Devices | |||

| By Memory Type | GDDR-based GPUs | ||

| HBM-based GPUs | |||

| By Performance Tier | Low-Cost GPUs (Less than USD 100) | ||

| Mainstream GPUs (USD 100-USD 400) | |||

| High-Performance Consumer GPUs (USD 400-USD 1,200) | |||

| Data Center / AI Accelerator GPUs (Greater than USD 1,200) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Southeast Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current and forecast size of the discrete GPU Market?

The discrete GPU market stood at USD 83.31 billion in 2025, reached USD 96.06 billion in 2026, and is projected to reach USD 229.29 billion by 2031 at a 19.01% CAGR.

Which application area leads to demand for discrete GPUs?

Servers and datacenter accelerators led demand with a 38.42% revenue share in 2025, driven by AI training and production inference deployments.

Why is HBM growing faster than other memory types in GPUs?

HBM is tied to AI accelerators, where bandwidth and capacity matter most, so it is projected to expand at a 20.18% CAGR through 2031 even though GDDR still leads in volume.

Why does Asia-Pacific lead regional growth?

Asia-Pacific held 42.57% share in 2025 and is projected to grow at a 19.89% CAGR because it combines strong AI infrastructure demand, gaming demand, and supply-chain depth.

What is the biggest risk to near-term expansion?

Memory tightness remains the main near-term constraint because advanced memory and packaging demand from AI accelerators raises costs and limits supply flexibility across gaming and workstation products.

Which companies shape competition the most?

NVIDIA remains the dominant player, AMD is the main challenger in data center accelerators, and Intel remains strategically important through platform and manufacturing partnerships.

Page last updated on: