Graphic Processors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

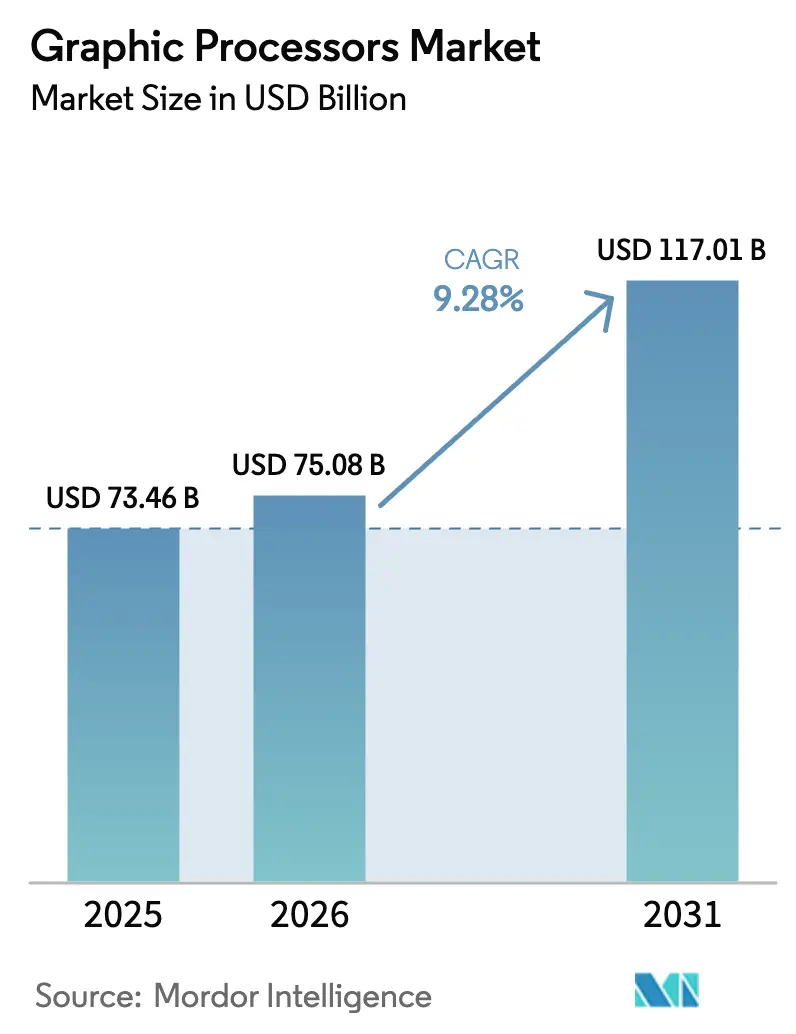

| Market Size (2026) | USD 75.08 Billion |

| Market Size (2031) | USD 117.01 Billion |

| Growth Rate (2026 - 2031) | 9.28% CAGR |

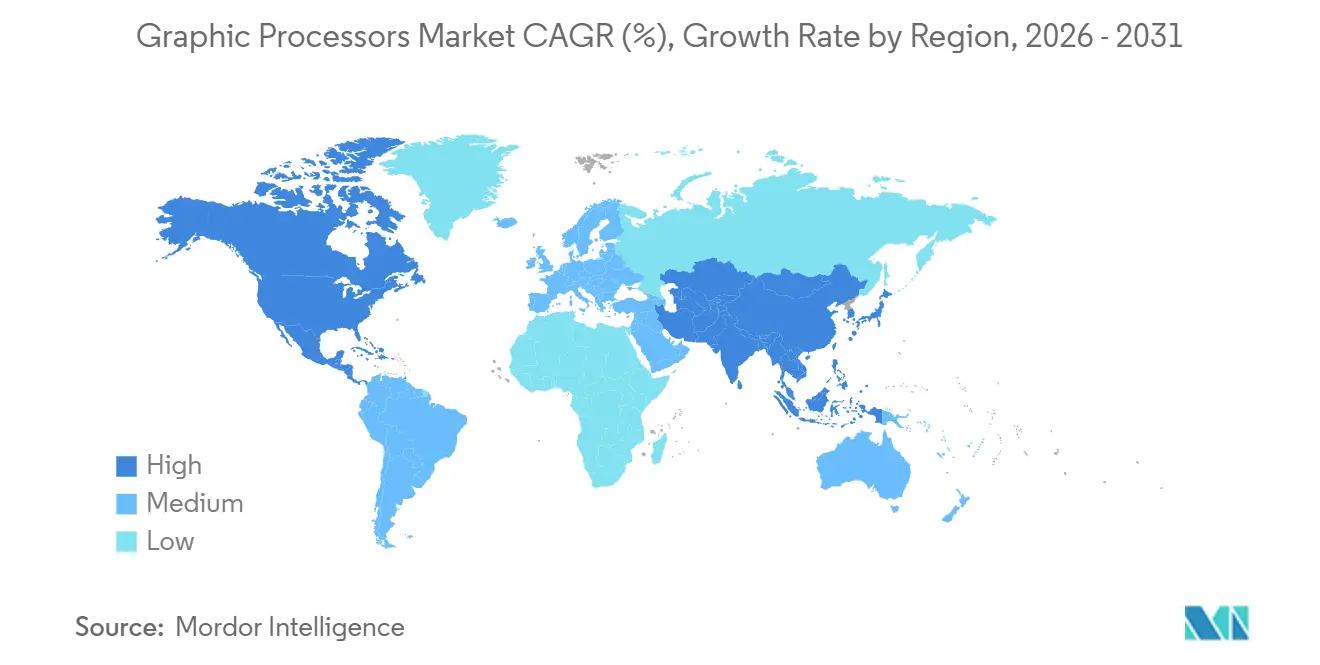

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

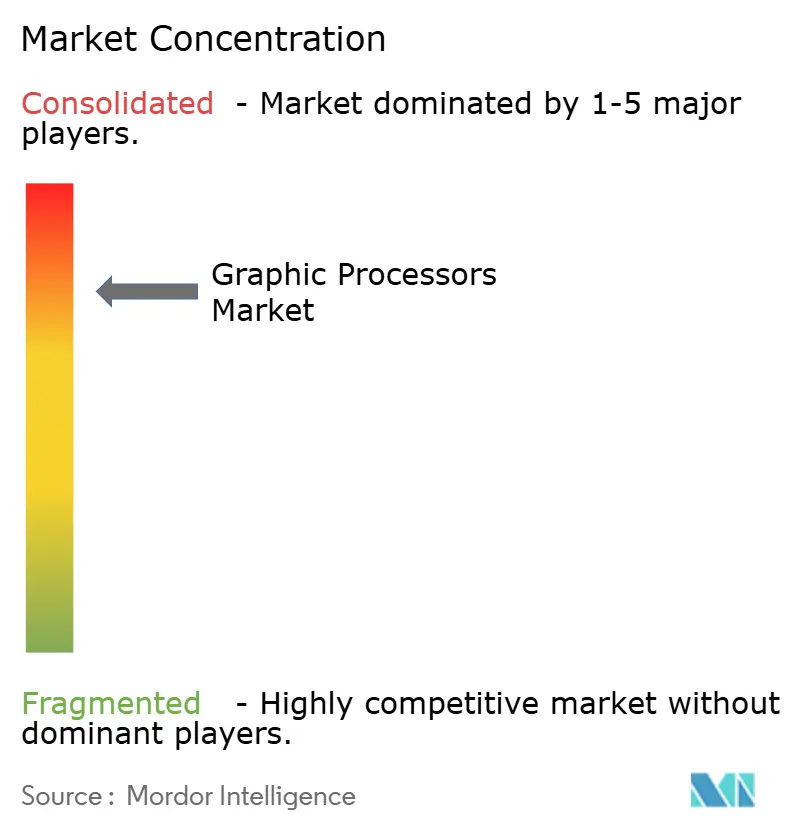

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Graphic Processors Market Analysis by Mordor Intelligence

The Graphic Processors Market size is projected to expand from USD 73.46 billion in 2025 and USD 75.08 billion in 2026 to USD 117.01 billion by 2031, registering a CAGR of 9.28% between 2026 to 2031. The increasing demand for accelerators powering large language model (LLM) training, real-time ray tracing in gaming, and on-device generative AI is reinforcing upgrade cycles despite component shortages and high average selling prices. Vendors are shifting roadmaps toward hybrid chiplet architectures that cut memory-transfer latency and improve throughput per watt, while hyperscalers are commercializing stranded capacity through second-based GPU-as-a-service offerings to diversify revenue. Thermal-envelope constraints, wafer-start scarcity at 5 nanometers and below, and export controls on high-end boards are tempering shipment velocity, yet underlying appetite for parallel compute keeps attach rates above 80% in data-center design wins. Alongside incumbent concentration in premium tiers, a wave of RISC-V and application-specific integrated circuit (ASIC) challengers is targeting inference workloads that demand lower power budgets and tighter cost envelopes.

Key Report Takeaways

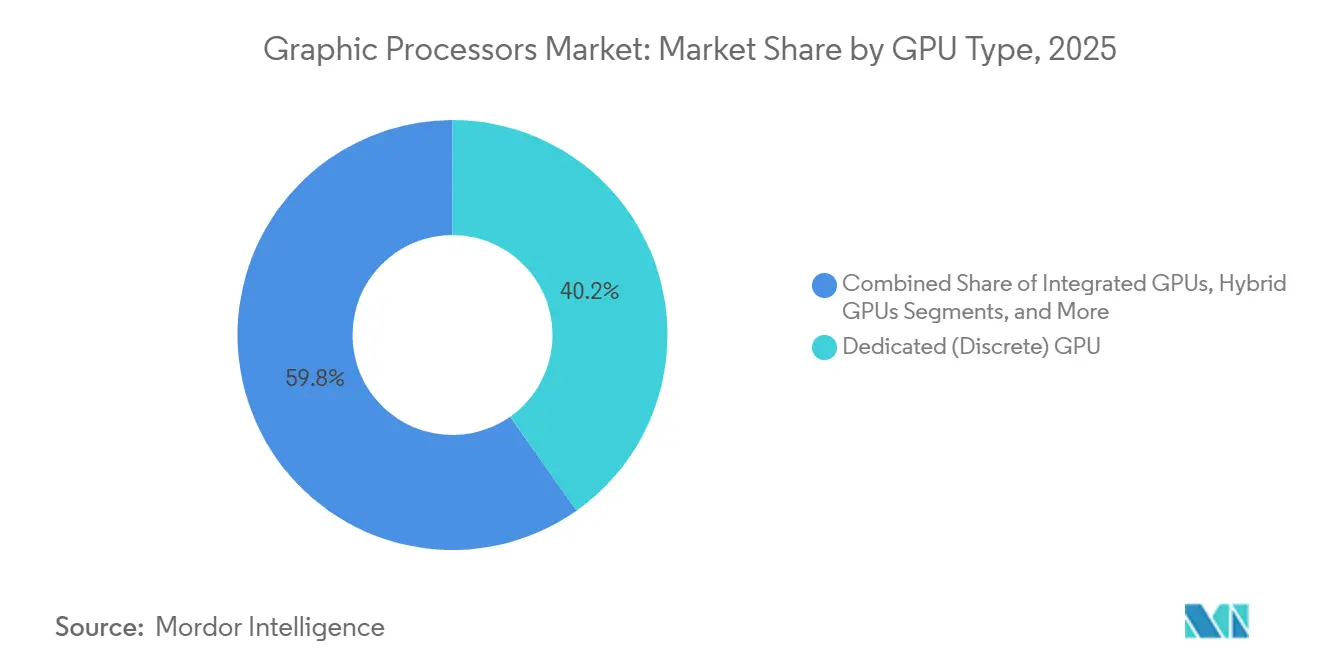

- By GPU type, dedicated discrete boards led with 40.22% of graphic processors market share in 2025. Hybrid GPUs are projected to advance at a 9.83% CAGR through 2031, the fastest among architectures.

- By deployment model, on-premise installations commanded a 72.91% revenue share in 2025. Cloud-as-a-service workloads are set to expand at a 10.02% CAGR during 2026–2031.

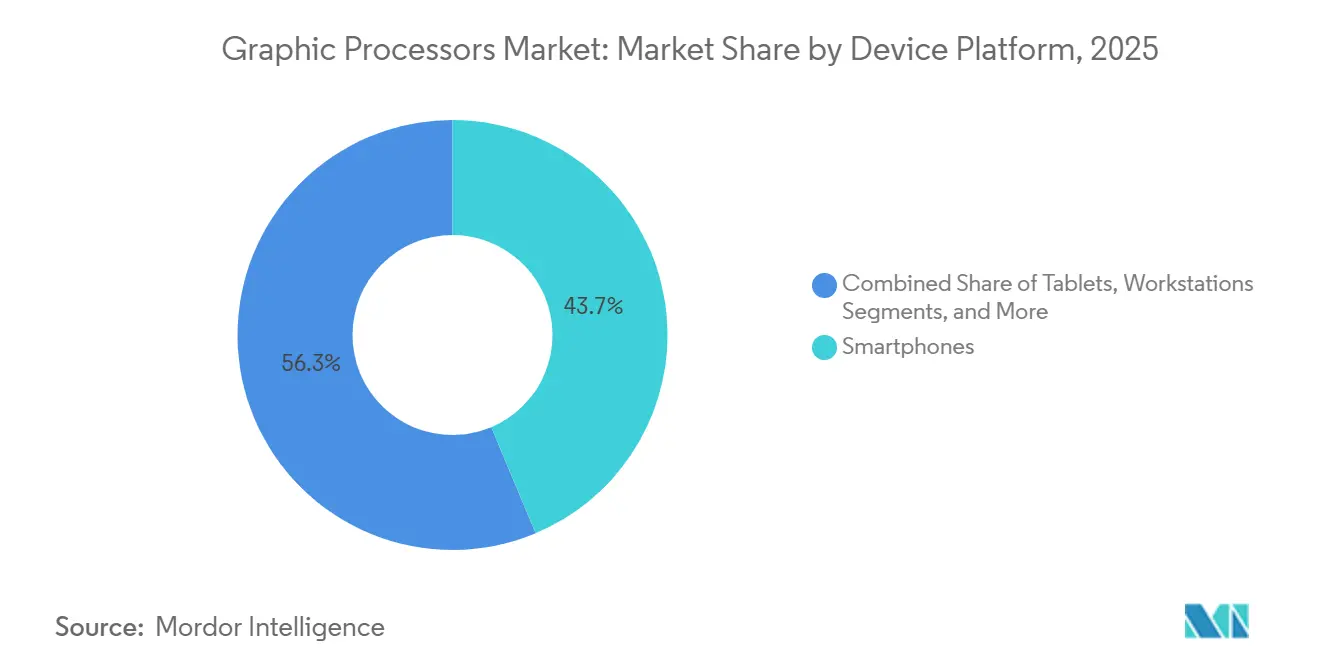

- By device platform, smartphones generated 43.67% of sales in 2025. Data-center servers are forecast to climb at a 9.64% CAGR through 2031.

- By end-user industry, consumer electronics held 33.03% of revenue in 2025. Healthcare and life sciences are the fastest-growing vertical, with a 10.93% CAGR through 2031.

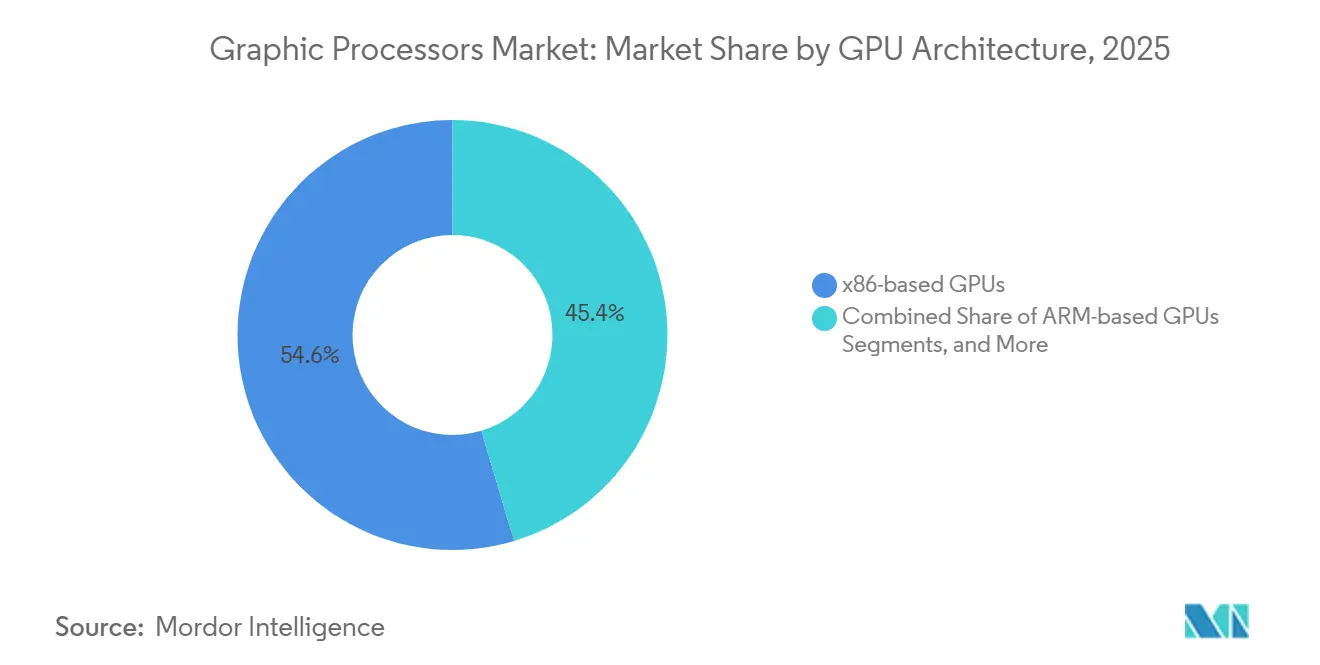

- By GPU architecture, x86 retained a 54.64% share in 2025. RISC-V GPUs are on track for a 9.51% CAGR, the highest among instruction-set options.

- By geography, North America led with 37.81% market share in 2025, while Asia-Pacific is projected to expand at an 11.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Graphic Processors Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand for AAA Gaming and Real-Time Ray Tracing | +1.8% | Global, with concentration in North America, Europe, and APAC gaming hubs | Medium term (2-4 years) |

| Proliferation of AI/Deep Learning Workloads | +2.5% | Global, led by North America and APAC data-center deployments | Long term (≥ 4 years) |

| Expansion of Cloud Gaming and GPU-as-a-Service | +1.5% | North America and Europe, early adoption in urban APAC markets | Medium term (2-4 years) |

| Chiplet and Advanced Packaging Breakthroughs | +1.2% | Global, with manufacturing concentrated in Taiwan and South Korea | Long term (≥ 4 years) |

| Government-Backed Exascale Supercomputing Programs | +0.8% | United States, European Union, China, Japan | Long term (≥ 4 years) |

| ARM/RISC-V Automotive-Grade Custom GPUs | +1.0% | Europe and APAC automotive corridors, spillover to North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for AAA Gaming and Real-Time Ray Tracing

Real-time ray tracing has become a baseline expectation, leading vendors to devote up to half of the die area to ray-triangle intersection units that sustain 60 frames-per-second output at 4K resolution. Console refreshes in 2025 injected second-generation ray-tracing cores, lifting the performance floor and pushing discrete GPU roadmaps toward native 8K rendering by 2027. Esports studios are adopting path-traced global illumination to curb artist workloads, tripling compute requirements over raster pipelines and expanding the mid-tier segment priced between USD 400 and USD 700. Subscription cloud gaming platforms now reserve 1.2 GPUs per concurrent user to preserve sub-50-millisecond latency, up from 0.8 in 2024, tightening high-end supply for hyperscale GPU pools. Premium smartphones integrated hybrid ray-tracing blocks in 2025, lifting flagship handset GPU attach rates by 18% year over year.

Proliferation of AI/Deep Learning Workloads

Frontier model training exceeded 10^25 floating-point operations in 2025, prompting clusters with 16,384 accelerators linked via 400 Gb/s fabrics to complete runs within 90 days. Inference is moving from batch to real-time streams, favoring tensor cores optimized for INT8 and FP16 over generic vector units. Hospitals deployed federated learning frameworks across 50-100 sites, raising per-site GPU needs from 2 to 8 units for privacy-preserving diagnostics. Automakers fitted on-vehicle modules with 200-tera-operations-per-second throughput to support over-the-air updates, adding USD 800-USD 1,200 to bill-of-materials and reinforcing premium-trim segmentation. Quantitative trading desks cut strategy development cycles from 6 months to 3 weeks through GPU-based reinforcement learning, triggering 22% deployment growth in 2025 in the graphic processors market.

Expansion of Cloud Gaming and GPU-as-a-Service

Hyperscalers introduced second-billed accelerator offerings in 2025, lowering the entry point for indie developers who previously avoided reserved-instance lock-ins.[1]Amazon Web Services, “Per-Second GPU Pricing Launch,” aws.amazon.com Global cloud-gaming subscriptions climbed to 45 million, yet 30% annual churn prompted providers to co-locate GPU pods within 10 milliseconds of metropolitan exchanges to mitigate latency spikes. Remote-work demand for workstation-class experiences lifted virtual desktop infrastructure with GPU pass-through by 35% year over year. Emerging spot markets for idle capacity allowed brokers to aggregate fractional compute and resell at 40% discounts, pressuring hyperscaler margins and hastening moves toward internal silicon. Data-sovereignty mandates in the European Union and India kept personal-data workloads inside national borders, inflating per-instance costs by up to 25%.

Chiplet and Advanced Packaging Breakthroughs

Chiplet designs decoupled compute, memory, and I/O in 2025, enabling 3 nanometer logic stacked beside 5 nanometer SRAM and trimming wafer costs by up to 30%.[2]TSMC, “Chiplet Architecture Advances,” tsmc.com The Universal Chiplet Interconnect Express (UCIe) standard opened doors for third-party tensor tiles that integrate via 2.5D interposers, cutting time-to-market from 24 months to 14 months. Eight-high HBM stacks delivered 1.2 TB/s bandwidth inside a 55 mm square, eliminating the need for off-package buffers in training rigs. Multi-die packages incorporated microfluidic channels circulating dielectric coolant at 2 L/min, sustaining 15% higher boost clocks relative to air-cooled boards despite a USD 50-USD 80 added unit cost. Machine-learning-based binning raised known-good-die yields from 88% to 94% by mid-2025, offsetting complexity penalties.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advanced-Node Supply Bottlenecks (≤5 Nm) | -1.3% | Global, acute in North America and Europe GPU supply chains | Short term (≤ 2 years) |

| High ASPs Limiting Mainstream Adoption | -0.9% | Global, pronounced in price-sensitive APAC and South America markets | Medium term (2-4 years) |

| Export Controls on High-End GPUs | -0.7% | China, Russia, spillover to Middle East and select APAC markets | Medium term (2-4 years) |

| Thermal Envelope (>600 W) Deployment Limits | -0.5% | Global data centers, concentrated in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Advanced-Node Supply Bottlenecks (≤5 nm)

Foundry capacity at 5 nm and below remained tight in 2025, as TSMC allocated 60% of N3 wafer starts to smartphone processors, pushing GPU lead times to 26 weeks for volume orders. Samsung’s 3 nm yields hovered near 70%, below cost-competitive thresholds, forcing fallback to 5 nm nodes at 20% lower performance per watt. Intel’s Arizona ramp slipped six months, delaying domestic capacity for U.S. designers and prolonging reliance on Taiwan fabrication. Dual-sourcing expansions require 12–18 months of process-co-development, limiting near-term diversification. Wafer price inflation of 8% compounded margin compression and curbed aggressive expansion in the graphic processors market.

High ASPs Limiting Mainstream Adoption

Flagship data-center boards cleared USD 30,000 per unit in 2025, confining uptake to hyperscalers and enterprises with USD 50 million-plus budgets.[3]The Information, “GPU Pricing Dynamics at Hyperscalers,” theinformation.com Enthusiast consumer GPUs crossed USD 1,800, restricting sales to the top income quintile in developed markets. Automotive-grade accelerators priced at USD 800-USD 1,200, equating to 2–3% of vehicle cost, relegated GPU-enabled ADAS functions to premium trims. Leasing and GPU-as-a-service mitigated capex but resulted in a 10-15% higher total cost of ownership over three years due to financing premiums. Elasticity analysis showed that a 10% ASP cut could lift unit demand by up to 22%, underscoring the latent opportunity if chiplet economies of scale materialize.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By GPU Type: Hybrid Designs Gain Enterprise Traction

Dedicated discrete boards retained a 40.22% stake in 2025 in the graphic processors market, driven by hot-swappable data center cards that simplify maintenance windows. Hybrid accelerators are forecast to grow at a 9.83% CAGR amid demand for unified memory that eliminates PCIe bottlenecks and cuts system power by 25-30%. Integrated GPUs continue to dominate thermally constrained laptops, whereas external enclosures target mobile creatives seeking episodic boosts but are hampered by Thunderbolt bandwidth ceilings that cap utilization at 70-80%.

Chiplet-based hybrids combine 3 nm CPU cores with 5 nm GPU tiles, balancing yield and cost while sustaining competitive throughput. Discrete inference boards introduced sparsity engines that raise effective throughput by up to 60% on transformer models without area penalties. External GPU ecosystems are exploring proprietary connectors to overcome Thunderbolt 5 constraints.

By Deployment Model: Clouds Monetize Idle Capacity

The on-premise segment captured 72.91% of 2025 revenue in the graphic processors market, as latency-sensitive or sovereign workloads remained tethered to local clusters. Cloud-as-a-service is projected to grow 10.02% annually, driven by second-based billing that attracts deep learning experimentation and burst capacity. Financial and healthcare operators keep primary training on site for compliance but burst peak loads to co-located regions, creating hybrid orchestration demand.

Spot GPU prices have varied by 50-80% across zones, prompting workload schedulers to migrate jobs to optimize costs. Lengthening hardware refresh cycles from 3.2 to 4.5 years reflects cautious capital expenditure and software-side efficiency gains. Reserved-capacity contracts offer 35-45% discounts but expose clients to generation-lock-in risk as new silicon lands.

By Device Platform: Data Centers Absorb LLM Training

Smartphones led with 43.67% revenue in 2025 in the graphic processors market, propelled by sub-100-millisecond on-device generative AI that circumvents cloud round-trips. Data-center servers are projected to advance at a 9.64% CAGR, absorbing frontier model training rigs of 8,192-16,384 GPUs. Gaming PCs and consoles kept steady volumes, but upgrade intervals lengthened to 3.8 years as generational gains narrowed.

Workstations adopted hardware video encoding that slashed 8K timeline scrub lag by 40% and boosted creative productivity. Tablets remain thermally constrained, limiting sustained graphics to one-fifth of discrete levels. Automotive infotainment demanded ISO 26262-certified GPUs, extending design cycles by up to 18 months and concentrating share among established suppliers.

By End-User Industry: Healthcare Accelerates Diagnostics

Consumer electronics commanded 33.03% of 2025 demand, reflecting smartphones, consoles, and PCs where GPU capability influences buyer decisions. Healthcare is set for a 10.93% CAGR on the back of MRI reconstruction that cuts scan times to 12 minutes and drug-discovery screens that process 10 million compounds weekly. IT and telecom providers offloaded packet processing to GPUs, tripling network throughput.

Media studios embraced neural rendering to replace physical sets, trimming shoot days by up to 30%. Automakers deployed fleet-wide perception updates using on-vehicle accelerators, tightening feedback loops for autonomous algorithms. Defense agencies achieved near-real-time synthetic-aperture radar processing, shortening decision cycles from hours to minutes in the graphic processors market.

By GPU Architecture: RISC-V Secures Automotive Beachhead

x86 architectures held 54.64% in 2025 as mature ecosystems and legacy compatibility deter costly refactoring. RISC-V is forecast to expand at a 9.51% CAGR, led by automotive tier-1s eyeing royalty-free designs that pare per-vehicle license costs by up to USD 10. ARM continues to dominate sub-10-watt envelopes with 2-3x performance-per-watt advantages, especially in mobile.

Open-source toolchain maturation cut RISC-V porting effort from 18 to 6 months, lowering entry thresholds for startups. x86 vendors introduced expanded vector extensions that doubled inference throughput, narrowing efficiency gaps with ARM. Fragmented ARM memory-coherency protocols posed software hurdles for unified CPU-GPU address spaces.

Geography Analysis

North America contributed 37.81% of 2025 revenue, driven by hyperscale build-outs in Virginia, Oregon, and Texas, which accounted for over half of global high-end shipments. Asia-Pacific is projected to expand at an 11.52% CAGR, underpinned by sovereign-AI programs in China and India that prioritize domestic silicon and localized model training.[4]Wall Street Journal, “China, India Sovereign AI GPU Initiatives,” wsj.com Europe registered moderate growth, as energy tariffs inflated operating expenses by 18-22%, prompting delays in refreshes in the graphic processors market.

Middle East investments established AI-free zones, where the United Arab Emirates and Saudi Arabia commissioned clusters of more than 10,000 accelerators to build Arabic LLMs. Africa and South America contributed under 5% combined, though smartphone GPU attachment in Brazil, Nigeria, and South Africa rose 25-30% with carrier financing expansion.

China’s imports fell 12% after high-bandwidth interconnect restrictions, prompting domestic efforts at Alibaba’s T-Head and Biren to achieve 70-80% of NVIDIA A100 performance by late-2025. Japan allocated USD 2.3 billion to national AI clusters totaling 15,000 GPUs to train language models without relying on U.S. cloud services. India’s semiconductor incentive attracted USD 1.8 billion commitments, though front-end fabs remain three years out. Germany and France co-funded GPU R&D projects but trailed commercial offerings by 18-24 months in power efficiency.

Competitive Landscape

The graphics processor market is highly concentrated; the top three vendors captured a high share of 2025 data-center sales. Incumbents defend attach rates above 80% by tethering accelerators to proprietary fabrics and software stacks, elevating switching costs to up to USD 10 million for mid-tier clouds. Challenger ASIC makers tout 3-5x performance-per-watt advantages for inference, exploiting the gulf between training-centric GPUs and production needs.

Edge AI represents white space where sub-15-watt budgets and sub-10-millisecond latency invite bespoke silicon; startups raised USD 800 million in 2025 to chase this slice. Patent filings for greater than 1 Tb/s chiplet interconnects jumped 40%, signaling a strategic race to own next-gen packaging standards. Hyperscalers accelerated vertical integration, unveiling internal GPUs that could shrink the external addressable market by 8-12% over five years.

RISC-V vendors sacrifice 5-8 points of gross margin to avoid royalties while accelerating automotive and industrial time-to-market, where software customization outweighs peak flops. Meanwhile, incumbent mobile suppliers continue to refine power-efficiency curves, defending share as ARM-based laptop pushes blur device boundaries.

Graphic Processors Industry Leaders

NVIDIA Corporation

Advanced Micro Devices Inc.

Intel Corporation

Samsung Electronics Co. Ltd.

Qualcomm Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: NVIDIA expanded its Israel R&D hub with a USD 3.2 billion investment focused on next-generation GPU architectures.

- November 2025: AMD purchased Silo AI for USD 665 million to deepen large language model software expertise.

- October 2025: Intel debuted Gaudi 3 accelerators targeting 50% lower TCO for inference and secured 12,000-unit hyperscale orders.

- September 2025: TSMC initiated 3 nm GPU mass production for a leading U.S. client, achieving 80% yield.

- August 2025: Qualcomm and Mercedes-Benz partnered on a custom RISC-V GPU delivering 300 TOPS for 2027 vehicles.

Global Graphic Processors Market Report Scope

The Graphic Processors Market Report is Segmented by GPU Type (Dedicated, Integrated, Hybrid, External), Deployment Model (On-Premise, Cloud-as-a-Service), Device Platform (Smartphones, Tablets, Gaming PCs and Consoles, Workstations, Data-Center Servers, Automotive), End-User Industry (Consumer Electronics, IT and Telecom, Media and Entertainment, Automotive, Defense, Healthcare), GPU Architecture (x86, ARM, RISC-V, Proprietary), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Dedicated (Discrete) GPUs |

| Integrated GPUs |

| Hybrid GPUs (APUs) |

| External GPUs (eGPU Enclosures) |

| On-Premise |

| Cloud-as-a-service |

| Smartphones |

| Tablets |

| Gaming PCs and Consoles |

| Workstations |

| Data-center Servers |

| Automotive Infotainment and ADAS |

| Consumer Electronics |

| IT and Telecom |

| Media and Entertainment |

| Automotive |

| Defense and Intelligence |

| Healthcare and Life Sciences |

| x86-based GPUs |

| ARM-based GPUs |

| RISC-V-based GPUs |

| Proprietary/Other ISAs |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By GPU Type | Dedicated (Discrete) GPUs | |

| Integrated GPUs | ||

| Hybrid GPUs (APUs) | ||

| External GPUs (eGPU Enclosures) | ||

| By Deployment Model | On-Premise | |

| Cloud-as-a-service | ||

| By Device Platform | Smartphones | |

| Tablets | ||

| Gaming PCs and Consoles | ||

| Workstations | ||

| Data-center Servers | ||

| Automotive Infotainment and ADAS | ||

| By End-User Industry | Consumer Electronics | |

| IT and Telecom | ||

| Media and Entertainment | ||

| Automotive | ||

| Defense and Intelligence | ||

| Healthcare and Life Sciences | ||

| By GPU Architecture | x86-based GPUs | |

| ARM-based GPUs | ||

| RISC-V-based GPUs | ||

| Proprietary/Other ISAs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the graphic processors market in 2026 and what CAGR is expected through 2031?

The graphic processors market size reached USD 75.08 billion in 2026 and is projected to grow at a 9.28% CAGR to USD 117.01 billion by 2031.

Which GPU type is expanding the fastest?

Hybrid GPUs that merge CPU and GPU cores on one die are forecast to post the quickest growth at 9.83% CAGR through 2031.

Why are cloud GPU services gaining traction?

Second-based billing, stranded-capacity monetization, and burst scalability are driving 10.02% CAGR for cloud-as-a-service deployments.

What is the main geographic growth engine?

Asia-Pacific leads with an 11.52% CAGR as China and India pursue sovereign-AI programs and domestic silicon strategies.

Which vertical shows the highest future demand for GPUs?

Healthcare and life sciences stand out with a 10.93% CAGR, driven by accelerated medical imaging and drug-discovery workloads.

How concentrated is supplier power in data-center GPUs?

The top three vendors commanded roughly 75–80% of 2025 data-center revenue, signaling a high concentrated supplier landscape.

Page last updated on: