Gaming GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 38.72 Billion |

| Market Size (2031) | USD 66.24 Billion |

| Growth Rate (2026 - 2031) | 11.34% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

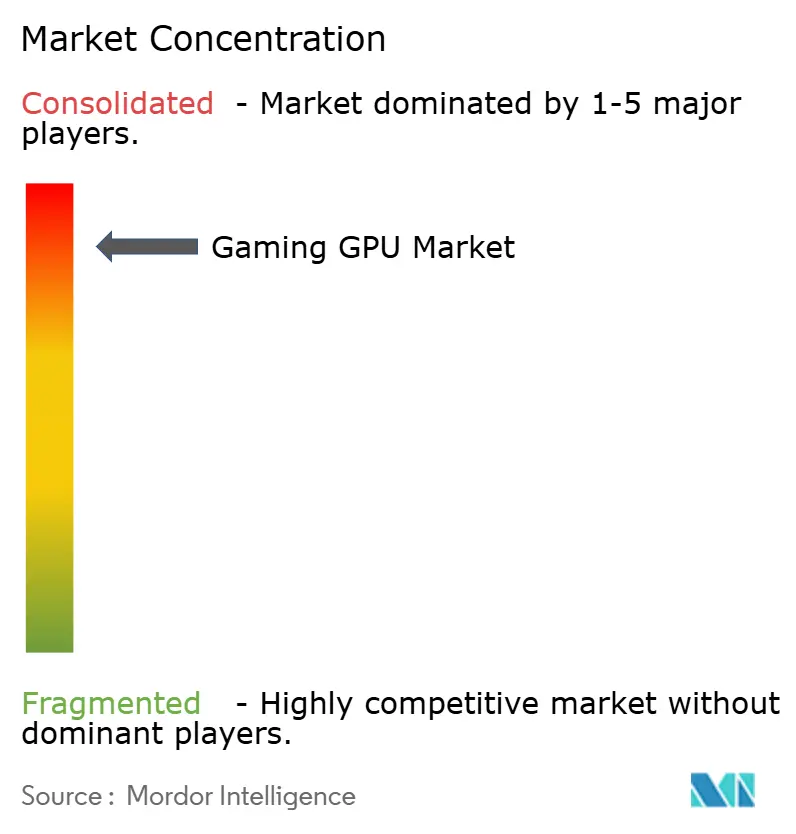

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gaming GPU Market Analysis by Mordor Intelligence

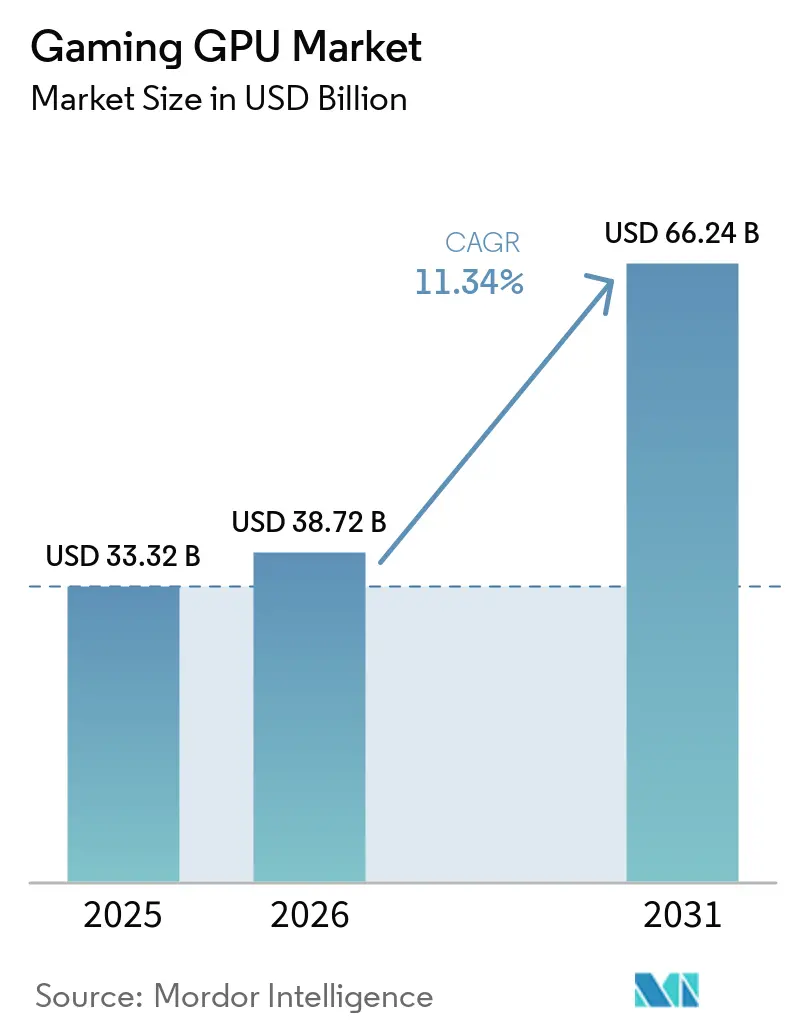

The gaming GPU market size is expected to increase from USD 33.32 billion in 2025 to USD 38.72 billion in 2026 and reach USD 66.24 billion by 2031, growing at a CAGR of 11.34% over 2026-2031. The market is being reshaped by a clear move away from raw raster performance toward AI-based rendering, frame generation, and ray tracing features that now influence buying decisions much more directly than before. New product cycles from NVIDIA and AMD have shortened replacement windows for serious players, as key performance gains are now tied to architecture-level AI capabilities rather than driver updates alone. The market also continues to benefit from strong premium demand, especially among enthusiast buyers who remain active even when selling prices rise. Regional momentum remains strongest in Asia-Pacific, where esports culture, premium PC demand, and mobile gaming scale support both higher volume and faster growth. Competitive pressure is intense, but it is concentrated among a small number of silicon vendors, while memory tightness, export controls, and the emergence of alternatives, such as integrated graphics and cloud delivery, continue to shape the pace and mix of demand.

Key Report Takeaways

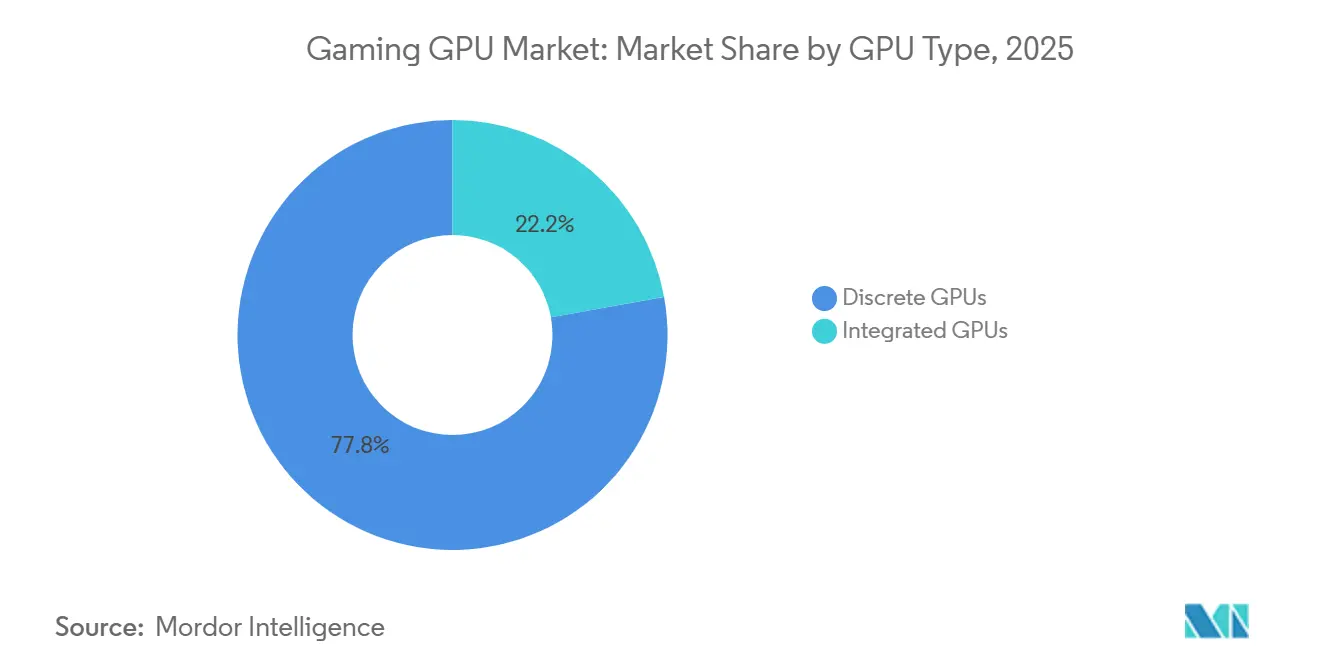

- By GPU type, discrete GPUs held 77.83% share in 2025, and are expected to register the fastest CAGR of 11.71% over the forecast period in the gaming GPU market.

- By device type, gaming desktops accounted for 48.37% of the market in 2025, while gaming laptops are projected to expand at a 11.94% CAGR through 2031.

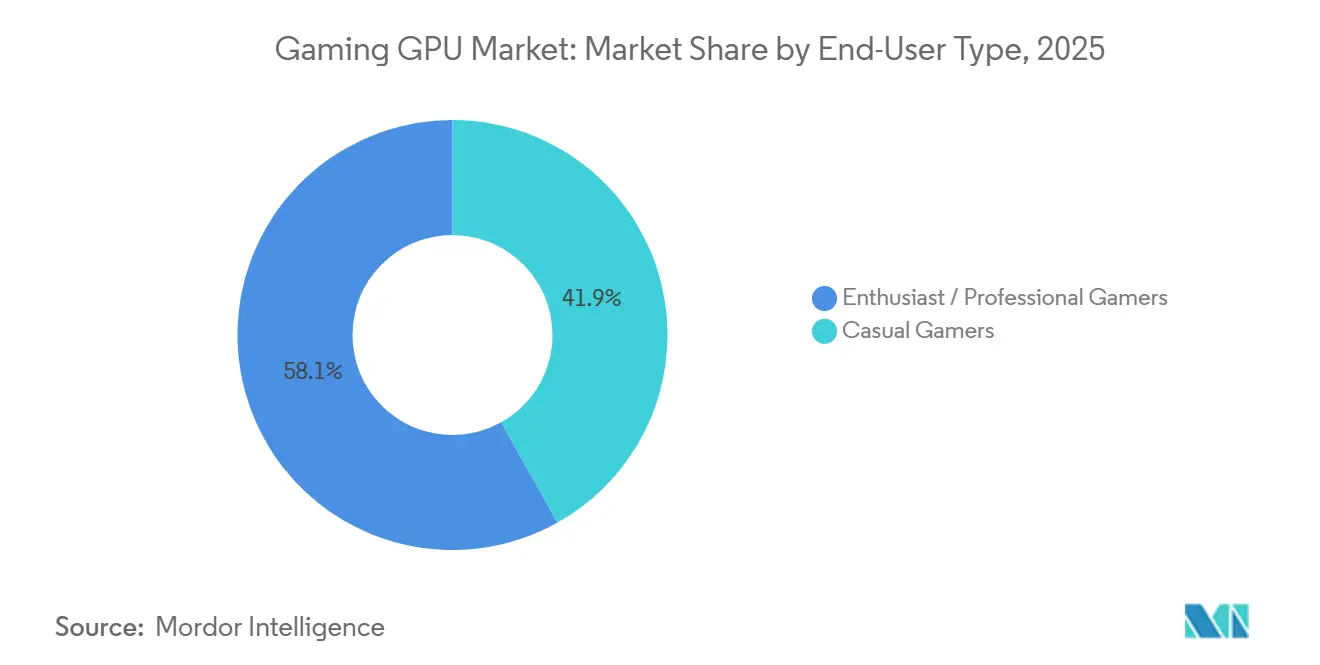

- By end-user type, enthusiast and professional gamers accounted for 58.12% of the market in 2025 and are projected to expand at a 11.64% CAGR through 2031.

- By memory type, GDDR6X accounted for 54.92% of the market size in 2025 and is projected to grow at a 12.14% CAGR through 2031.

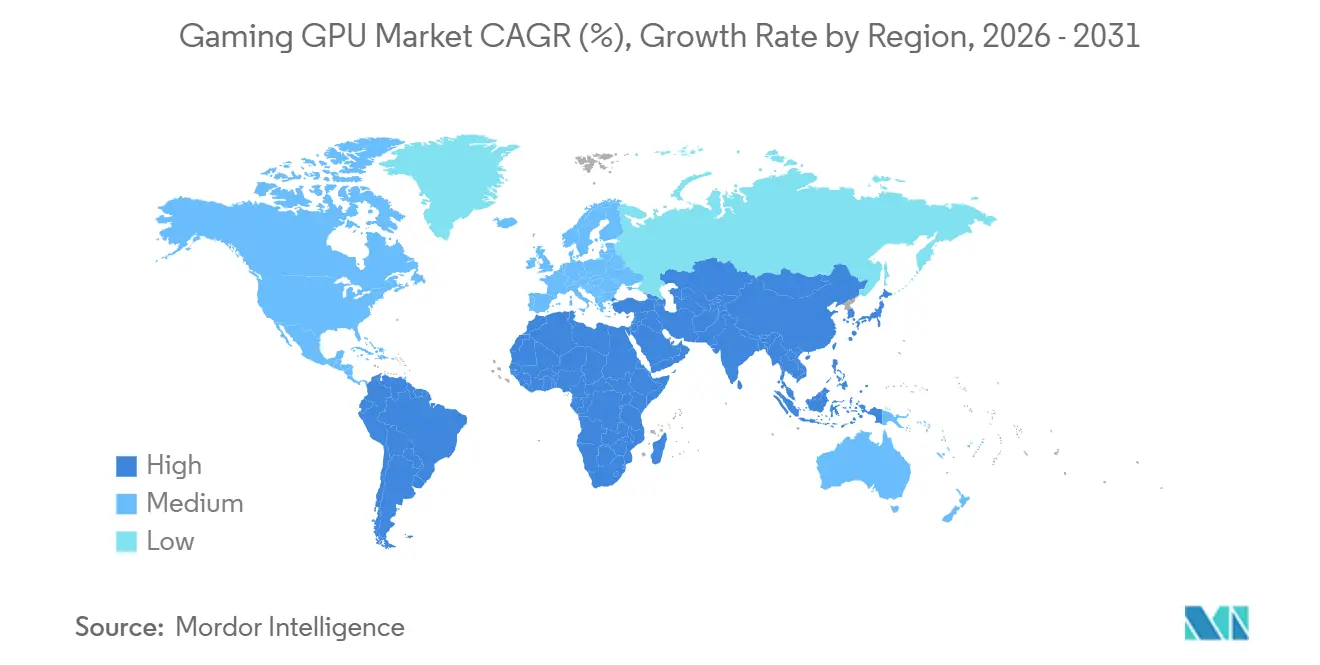

- By geography, Asia-Pacific held 52.88% of the gaming graphics processing unit (GPU) market share in 2025 and is projected to expand at a 12.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gaming GPU Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI Upscaling and Ray Tracing Refresh Cycle | +3.2% | Global, strongest in North America and Asia-Pacific | Short term (≤ 2 years) |

| Esports and Competitive FPS Upgrade Demand | +2.0% | Global, strongest in South Korea, North America, and Europe | Medium term (2-4 years) |

| Gaming Laptop and Handheld PC Proliferation | +1.8% | Asia-Pacific core, spill-over to North America and Europe | Medium term (2-4 years) |

| Mobile Ray Tracing and Premium Smartphone GPU Adoption | +1.4% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| PC Development Focus and Steam Deck Optimization | +0.9% | North America and Europe | Medium term (2-4 years) |

| Creator-Centric UGC and Real-Time Modding Workloads | +0.7% | North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI Upscaling and Ray Tracing Refresh Cycle

The gaming GPU market is seeing one of its strongest demand triggers from AI upscaling and neural rendering. NVIDIA introduced DLSS 4 with a transformer-based rendering pipeline and Multi Frame Generation, and stated that the feature set would be available across more than 125 titles by May 2025. That change matters because gamers who had stretched older cards through software tuning could no longer reach the same performance threshold without moving to Blackwell-based hardware. AMD reinforced the same direction when it launched RDNA 4, positioning higher ray tracing throughput and AI-ready graphics capabilities as standard expectations rather than premium extras. This creates a wider performance gap between new and older hardware, making each major architecture launch more commercially meaningful than a routine refresh.

Esports and Competitive FPS Upgrade Demand

The market continues to be driven by competitive gaming, where frame consistency and low latency matter as much as visual quality. NVIDIA placed strong emphasis on Reflex 2, saying the technology can reduce input latency by up to 75%, which directly aligns with the needs of esports and fast-response game genres. In practice, that shifts upgrade logic away from resolution alone and toward motion response and control precision. The gaming graphics processing unit (GPU) market benefits because serious players are more willing to replace still-functional cards when new hardware offers a measurable latency advantage that older platforms cannot replicate through simple updates. This also keeps premium products relevant even when the broader consumer electronics environment becomes more cautious.

Gaming Laptop and Handheld Pc Proliferation

The steady improvement of mobile graphics platforms is also supporting the gaming GPU market. NVIDIA launched Blackwell Max-Q with the RTX 50 Laptop GPU line and said the design extended battery life by up to 40% versus the prior generation while improving mobile gaming efficiency.[1]NVIDIA, “NVIDIA Blackwell GeForce RTX 50 Series Opens New World of AI Computer Graphics,” NVIDIA, nvidianews.nvidia.com That matters because gaming laptops are now much closer to serving as primary gaming machines instead of backup systems for travel. This supports growth by bringing more premium spending into mobile devices without fully sacrificing advanced features such as AI rendering and high-end visual performance. The effect is strongest in regions where portability, shared living spaces, and multi-use device buying patterns already favor laptops over fixed desktops.

Mobile Ray Tracing and Premium Smartphone GPU Adoption

The gaming GPU market is increasingly influenced by progress in premium smartphones as mobile graphics capabilities become more advanced. MediaTek launched the Dimensity 9500s in January 2026 with the Arm Immortalis-G925 GPU and positioned the platform around sustained ray-traced gaming at up to 120 frames per second. Arm also introduced the Mali G1 Ultra, featuring a second-generation ray tracing unit and stronger AI acceleration for mobile devices. This does not replace PC demand, but it raises gamer expectations around lighting, responsiveness, and AI-assisted graphics across device categories. Over time, the market benefits from that shift, as users who become familiar with richer mobile graphics are more likely to expect similar features when they move to laptops and desktops.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Foreccast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium GPU Pricing and Long Replacement Cycles | -2.4% | Global | Medium term (2-4 years) |

| Cloud Gaming and Good-Enough Integrated Graphics Substitution | -1.5% | North America and Europe | Medium term (2-4 years) |

| GDDR7 and Advanced Memory Tightness | -1.2% | Global | Short term (≤ 2 years) |

| Export Controls and China-Specific Gaming SKU Fragmentation | -0.9% | China, with spill-over to Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premium GPU Pricing and Long Replacement Cycles

The gaming GPU market still faces a clear demand limit from high selling prices at the premium end. NVIDIA launched the GeForce RTX 5090 at USD 1,999, while the rest of the Blackwell stack also established a higher price ladder across top performance tiers. AMD responded with more aggressive pricing in the mid-range, but its positioning also showed that affordability has become a central part of competitive strategy in the market. Many buyers still find that recent GDDR6X-based cards remain sufficient for a large share of current titles, especially when feature support is already broad across the installed base. That keeps revenue healthy at the high end but slows unit replacement in more price-sensitive parts of the market.

GDDR7 and Advanced Memory Tightness

The gaming graphics processing unit (GPU) market is also constrained by limited memory supply, which affects pricing and availability. NVIDIA’s RTX 50 series brought GDDR7 to flagship gaming cards, but broader adoption has not been smooth because next-generation memory has remained more expensive than earlier standards. AMD took a different path with the Radeon RX 9000 series, sticking with GDDR6, giving the company a way to avoid supply risks and maintain competitive pricing.[2]AMD, “Quick Reference Guide, AMD Radeon RX 9000 Series Desktop Graphics,” AMD, amd.com That decision has helped keep viable alternatives in the channel, but it also shows that supply planning is shaping product design more directly than in past cycles. For the market, this means faster innovation does not always translate into immediate mass adoption when the memory system behind it remains difficult to scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By GPU Type: Discrete Cards Anchor Revenue and Refresh Cycles

Discrete GPUs held 77.83% of the gaming GPU market in 2025, which shows how strongly dedicated graphics hardware still shapes revenue and performance expectations. The market continues to rely on discrete cards for 4K gaming, advanced ray tracing, and AI-assisted rendering workloads, while integrated solutions still struggle to match them at the top end. NVIDIA expanded the pricing range for its Blackwell lineup in 2025, stretching from the RTX 5090 down to the RTX 5050 desktop product. AMD added pressure in the value-oriented part of the segment with RDNA 4, emphasizing higher ray tracing throughput per compute unit and greater memory capacity at comparable price points.

The market also remains favorable to discrete cards, as software support continues to expand for advanced rendering features. NVIDIA stated that more than 800 games and applications support RTX technologies, which helps extend the commercial life of dedicated cards across a wide installed base. Integrated graphics are becoming more capable and more relevant in mainstream gaming, but they are influencing the lower end of the market more than the premium end. That means the industry is not seeing discrete leadership collapse, but it is seeing the entry tier become more contested. In practical terms, discrete GPUs still anchor the highest-value portion of spending because serious players, creators, and premium laptop buyers continue to look for a performance margin that integrated solutions rarely deliver consistently. The result is that the market keeps its core revenue base in dedicated hardware even as the lower tiers become more fluid.

By Device Type: Laptops Lead The Next Growth Wave

Gaming desktops held 48.37% of revenue in 2025, while gaming laptops are projected to expand at an 11.94% CAGR from 2026 to 2031. That pattern shows that the gaming graphics processing unit (GPU) market still depends on desktops for its largest revenue pool, but current growth is shifting toward portable systems. NVIDIA supported that transition when it rolled out RTX 50 Laptop GPUs with Blackwell Max-Q, tying higher mobile efficiency to longer battery life and broader premium OEM coverage. The market benefits because this narrows the historical performance gap that once kept many serious players tied to desktop towers.

Laptop growth also reflects a change in purchase logic rather than only a change in hardware design. Buyers increasingly want a single device that can handle gaming, work, study, and travel without sacrificing access to newer AI rendering features. NVIDIA’s extension of DLSS 4 and Blackwell capabilities into laptop systems supports that shift by making advanced graphics features available beyond fixed desktop setups. Mobile gaming devices add another layer to the market, as premium tablets and smartphones now feature graphics capabilities once limited to larger platforms. MediaTek’s 2026 flagship launch showed how mobile devices are moving toward higher frame rates and ray tracing support, which keeps the overall device boundary more fluid than before.

By End-User Type: Enthusiast Demand Anchors Revenue Structure

Enthusiast and professional gamers accounted for 58.12% of revenue in 2025 and are projected to expand at an 11.64% CAGR through 2031. That makes this group both the largest and the fastest-growing demand base in the gaming GPU market, confirming that revenue is highly concentrated among buyers who prioritize performance and feature access. The segment is especially responsive to each new capability jump in AI upscaling, ray tracing quality, and latency reduction. The gaming GPU market, therefore, remains more insulated from soft consumer demand than many other hardware categories because its leading customers tend to value performance consistency over pure affordability. This premium skew also explains why top-tier launches continue to shape the category's narrative, even when unit affordability remains a challenge for casual players.

The replacement cycle for this cohort is getting shorter because key performance gains are increasingly tied to architecture-level features that older products cannot fully emulate. NVIDIA’s Blackwell generation introduced fifth-generation Tensor Cores, fourth-generation RT Cores, and DLSS 4 Multi Frame Generation, which together raised the performance ceiling for the enthusiast tier. AMD’s RDNA 4 launch reinforced the same buying logic by emphasizing stronger ray tracing output and AI-ready graphics capability for gamers seeking new value at the upper mid-range and enthusiast levels. Casual gamers still matter to the gaming GPU market, but their purchases are more price-sensitive, influenced by integrated alternatives, and the used hardware channel. That keeps future revenue growth tilted toward enthusiast and professional users, even if broader ownership expands at a slower pace.

By Memory Type: GDDR6X Leads Through A Supply Dislocation

GDDR6X held 54.92% share in 2025 and is projected to expand at a 12.14% CAGR through 2031. This means the gaming GPU market size remains anchored in a memory standard that is already well established, even though GDDR7 entered the spotlight with the latest flagship launches. NVIDIA introduced GDDR7 in the RTX 50 series, but the installed base and broader commercial reach of GDDR6X-class products still matter because support across games and applications remains deep. The gaming GPU market is therefore not moving in a straight line from one memory generation to the next.

Supply conditions help explain why this segment remains strong. AMD deliberately used GDDR6 in the Radeon RX 9070 XT and RX 9070, reducing supply exposure and enabling more competitive pricing against newer GDDR7-equipped rivals. That decision helped preserve multiple viable memory tiers in the gaming GPU market, rather than forcing a rapid, more expensive jump to next-generation memory across the board. GDDR6 remains important in laptops and value-oriented systems, while legacy memory types continue to fade as older hardware is retired from active use. Unified memory is also gaining a niche role in compact and mobile gaming devices, but the center of revenue still lies with established discrete memory card standards. For that reason, the gaming GPU market continues to reward supply stability and software longevity just as much as pure specification novelty.

Geography Analysis

Asia-Pacific held 52.88% of the gaming GPU market share in 2025 and is projected to grow at a 12.31% CAGR through 2031. The market is strongest in this region because it combines deep esports engagement, large gamer populations, and rising demand for premium PCs, laptops, and mobile gaming devices. South Korea and Japan remain important for high-end hardware spending, while India and Southeast Asia add scale through broader adoption of gaming smartphones and mid-range laptops. The gaming GPU market also draws support in Asia-Pacific from a younger gaming base that is comfortable moving across device types rather than staying within a single platform. At the same time, export controls have made it more difficult for China to obtain premium GPUs, potentially reshaping product positioning and vendor opportunities across the region.

North America remains the second-largest regional revenue base, supported by high average selling prices, a mature PC gaming culture, and strong demand from enthusiasts who replace hardware more often than casual players. The United States market is especially important for premium discrete cards, where top-tier performance products still find buyers at scale. NVIDIA’s Blackwell product rollouts and broad OEM support show how central North America remains for premium launches and early adoption. Europe follows a similar demand pattern, with interest in competitive gaming and PC hardware supporting a steady market for higher-end products.

South America, the Middle East, and Africa are smaller in terms of revenue, but all three regions continue to grow in practical gaming relevance. In South America, demand is more concentrated in mid-range systems and mobile gaming because affordability remains a major factor in hardware choice. In the Middle East and Africa, premium gaming setups are gaining visibility through esports venue investment and higher-end consumer demand in selected markets. Arm’s continued expansion of mobile GPU IP also supports market in these regions, as premium smartphones remain a more accessible path to advanced graphics features than top-tier PCs for many users.[3]Arm, “Mali G1-Ultra, Next-Generation Flagship GPU for Mobile Gaming,” Arm, arm.com

Competitive Landscape

The gaming GPU market is highly concentrated, especially in discrete graphics, where product direction, software standards, and pricing signals are set by a very small number of chip designers. NVIDIA remains the strongest force in the market because it combines premium hardware, broad OEM reach, and a software stack that has become deeply tied to how many new games are optimized. The company’s January 2025 Blackwell launch brought fifth-generation Tensor Cores, fourth-generation RT Cores, and DLSS 4 into a full family of gaming products, which gave it both a feature lead and a marketing advantage at the top end. NVIDIA then widened its addressable base through the RTX 5060 and RTX 5050 launches, extending the same architecture and AI across a broad OEM reach, and a software stack that has become deeply tied to the number of new games and rendering messages in lower price bands. This gives the market a leader that is not only strong in flagship products but also active in shaping mainstream upgrade behavior.

AMD remains the main competitive counterweight and has focused its strategy on value, memory capacity, and more balanced pricing in the upper mid-range. Its March 2025 RDNA 4 launch positioned the Radeon RX 9070 XT and RX 9070 around stronger ray tracing performance and 16 GB configurations that stood out against comparable rivals.[4]AMD, “AMD Unveils Next-Generation AMD RDNA 4 Architecture with the Launch of AMD Radeon RX 9000 Series Graphics Cards,” AMD, amd.com AMD’s Q1 2026 results also showed gaming revenue of USD 720 million, indicating that the company continued to see demand, even in a category with high competitive intensity. In the gaming GPU market, that matters because credible pressure from AMD helps prevent the high end from becoming the only source of product energy and buying interest.

A different layer of competition comes from mobile and integrated graphics, where Apple, Qualcomm, MediaTek, Samsung, and Arm influence gamer expectations even if they are not all direct competitors in add-in cards. ARM’s licensing model keeps it central to premium mobile graphics because its GPU designs flow into several smartphone chip programs with a wide geographic reach. MediaTek’s January 2026 flagship chipset launch is a good example of that direction because it pushed ray tracing and high frame rate gaming further into mainstream premium mobile hardware. The market, therefore, remains concentrated in discrete silicon, but the broader graphics ecosystem is becoming more layered as mobile and integrated platforms raise the baseline for what gamers expect from visual performance and AI features.

Gaming GPU Industry Leaders

Intel Corporation

Apple Inc.

NVIDIA Corporation

Advanced Micro Devices, Inc.

Qualcomm Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: AMD announced more than USD 10 billion in investments in the Taiwan ecosystem to expand advanced packaging manufacturing for next-generation AI infrastructure, securing capacity alongside its gaming GPU roadmap partners.

- May 2026: AMD reported Q1 2026 gaming revenue of USD 720 million, up 11% year-over-year, driven by strong Radeon GPU demand, partially offset by lower semi-custom revenue. Client and gaming combined revenue reached USD 3.6 billion, up 23% year over year, indicating renewed momentum in the discrete gaming GPU segment.

- January 2026: MediaTek launched the Dimensity 9500s chipset featuring the Arm Immortalis-G925 GPU with Adaptive Game Technology 3.0 and Frame Rate Converter 3.0, enabling sustained 120 FPS ray-traced gaming in flagship Android devices.

- July 2025: NVIDIA launched GeForce RTX 5050 desktop graphics cards starting at USD 249 and RTX 5050 Laptop GPUs starting at USD 999 from board partners including ASUS, GIGABYTE, MSI, ZOTAC, and others. The launch extended Blackwell architecture, including DLSS 4 Multi Frame Generation, to the entry-tier gaming segment.

Global Gaming GPU Market Report Scope

The Gaming GPU Market encompasses the global industry that develops, produces, and sells graphics processing units (GPUs) specifically optimized for gaming applications. These GPUs are designed to deliver high-performance graphics rendering, real-time processing, and advanced visual effects such as ray tracing, AI-based upscaling, and high frame-rate rendering across gaming devices.

The Gaming GPU Market Report is Segmented by GPU Type (Discrete GPUs, and Integrated GPUs), Device Type (Gaming Desktops, Gaming Laptops, and Smartphones and Tablets), End-User Type (Casual Gamers, and Enthusiast/Professional Gamers), Memory Type (GDDR6, GDDR6X, Unified Memory, and Other Memory Types), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Discrete GPUs |

| Integrated GPUs |

| Gaming Desktops |

| Gaming Laptops |

| Smartphones and Tablets (Mobile Gaming) |

| Casual Gamers |

| Enthusiast / Professional Gamers |

| GDDR6 |

| GDDR6X |

| Unified Memory |

| Other Memory Types (GDDR5, Legacy) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By GPU Type | Discrete GPUs | |

| Integrated GPUs | ||

| By Device Type | Gaming Desktops | |

| Gaming Laptops | ||

| Smartphones and Tablets (Mobile Gaming) | ||

| By End-User Type | Casual Gamers | |

| Enthusiast / Professional Gamers | ||

| By Memory Type | GDDR6 | |

| GDDR6X | ||

| Unified Memory | ||

| Other Memory Types (GDDR5, Legacy) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the gaming GPU market size in 2026 and how large will it be by 2031?

The gaming GPU market stands at USD 38.72 billion in 2026 and is projected to reach USD 66.24 billion by 2031, growing at an 11.34% CAGR over 2026-2031.

Which region leads demand for gaming GPUs?

Asia-Pacific led with 52.88% share in 2025 and is also projected to post the fastest regional CAGR of 12.31% through 2031.

Why are gaming laptops growing faster than desktops?

Gaming laptops are projected to expand at 11.94% CAGR because newer mobile GPU designs have narrowed the performance gap with desktops while improving battery life and portability.

Why does GDDR6X still lead even after GDDR7 launched?

GDDR6X held 54.92% share in 2025 and remains important because it has a large installed base, broad software support, and fewer supply constraints than newer memory standards.

Who are the main competitors in this space?

NVIDIA and AMD remain the central competitors in discrete gaming GPUs, while Arm, MediaTek, Apple, Qualcomm, and Samsung shape demand and expectations in mobile and integrated graphics.

What are the biggest risks affecting future GPU demand?

High premium pricing, longer replacement cycles, tight next-generation memory supply, export controls, and improving integrated graphics can all slow unit expansion even when revenue keeps rising.

Page last updated on: