Europe Gaming GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

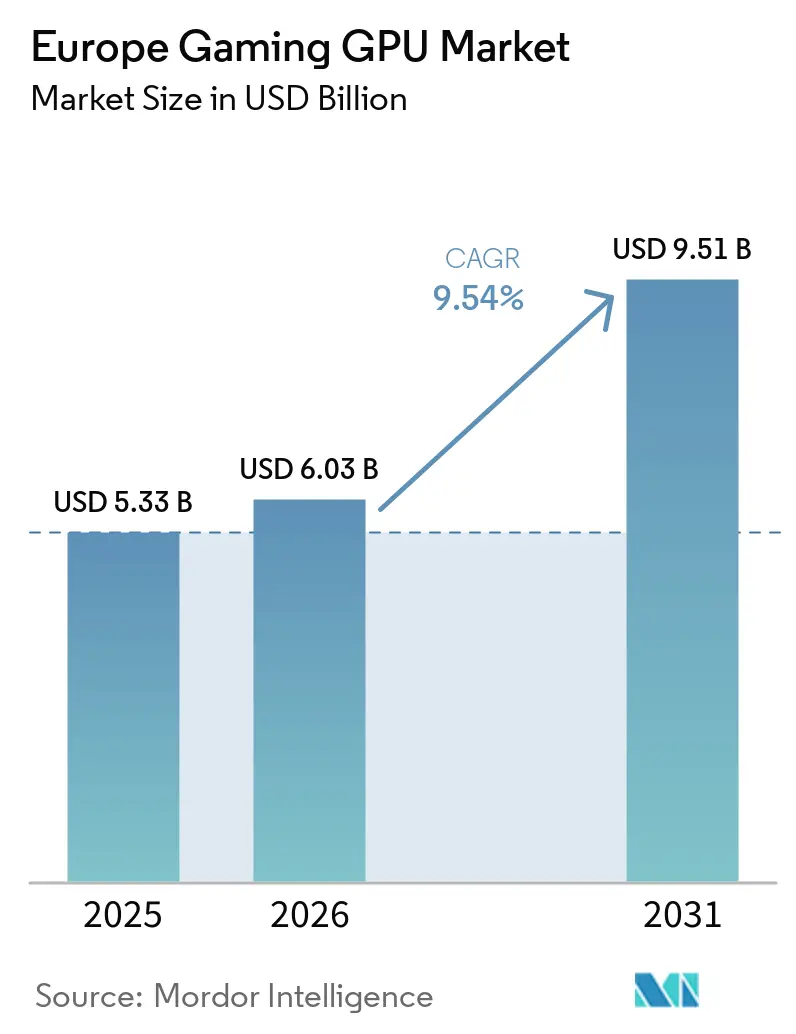

| Base Year Market Size (2025) | USD 5.33 Billion |

| Market Size (2026) | USD 6.03 Billion |

| Market Size (2031) | USD 9.51 Billion |

| Growth Rate (2026 - 2031) | 9.54% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Gaming GPU Market Analysis by Mordor Intelligence

The Europe gaming GPU market size is projected to be USD 5.33 billion in 2025, USD 6.03 billion in 2026, and reach USD 9.51 billion by 2031, growing at a CAGR of 9.54% from 2026 to 2031. Growth is being supported by broad gaming participation across Europe, which keeps hardware demand active across age groups and spending levels. The current cycle is also benefiting from the close timing of major new GPU launches in early 2025, which brought delayed upgrade demand back into the market after a long gap in flagship refreshes. Real-time ray tracing, AI-upscaling, and frame generation are raising the minimum performance level buyers now expect from new systems, especially in the discrete category. At the same time, high upfront hardware costs and a still-capable installed base are slowing replacement decisions for mainstream buyers and concentrating spending in the enthusiast tier. Cloud gaming expansion, portable high-performance systems, and tighter efficiency expectations in the EU are also shaping how vendors position products across the Europe gaming GPU market.

Key Report Takeaways

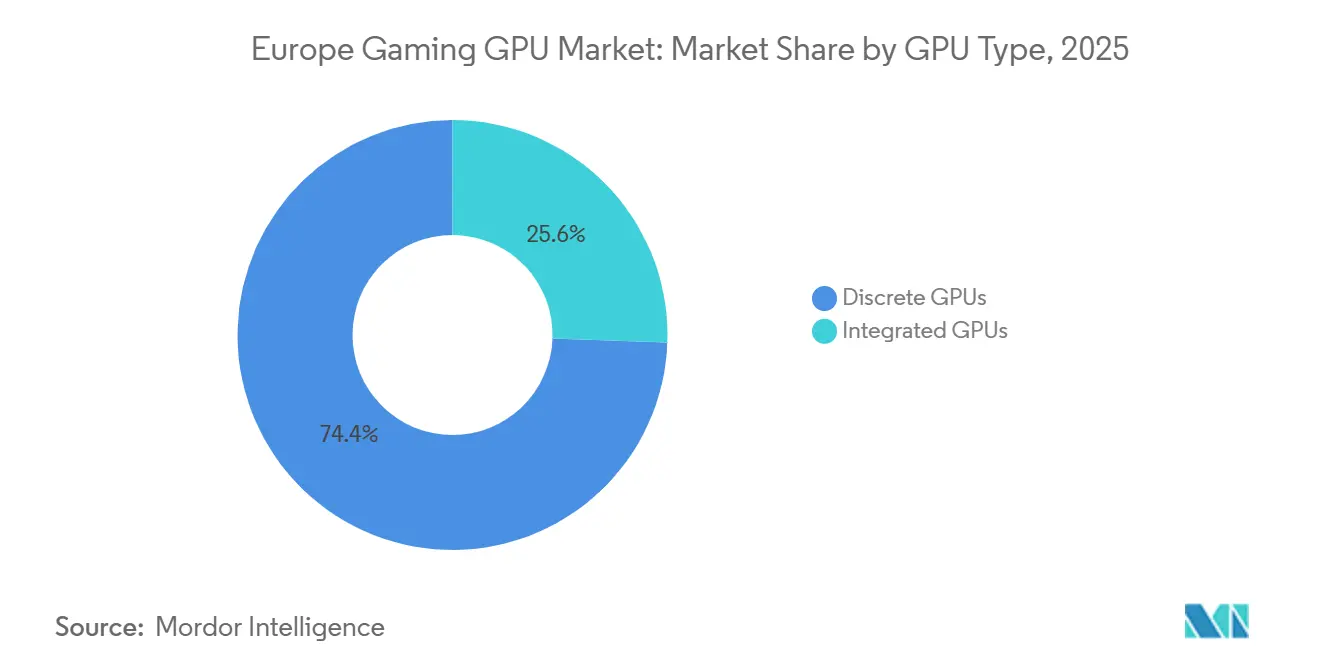

- By GPU type, discrete GPUs held 74.44% of the Europe gaming GPU market share in 2025 and are projected to expand at a 9.90% CAGR through 2031.

- By device type, gaming desktops accounted for 44.31% share of the Europe gaming GPU market size in 2025, while gaming laptops are projected to record the highest CAGR at 10.12% through 2031.

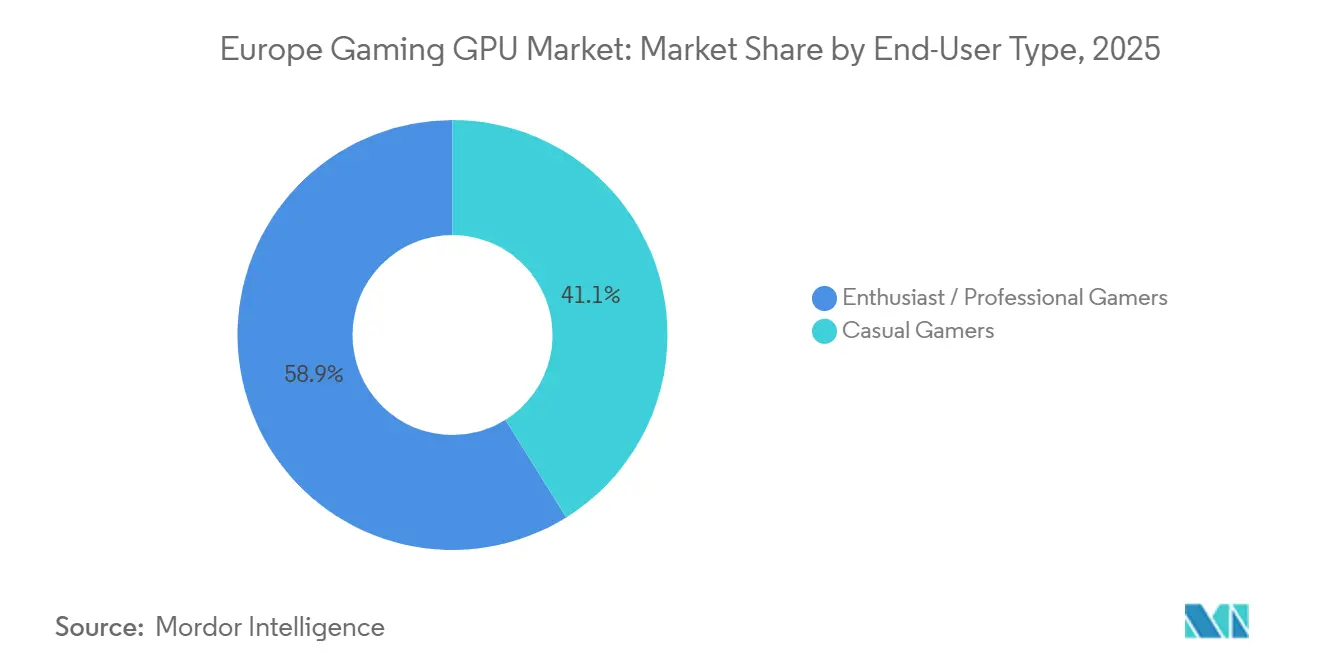

- By end-user type, enthusiast and professional gamers held 58.88% share in 2025 and are projected to grow at the fastest CAGR of 10.46% through 2031.

- By memory type, GDDR6X captured 53.16% share in 2025 and is projected to expand at the highest CAGR of 10.88% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Gaming GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Esports and Competitive PC Gaming Participation | +2.3% | UK, Spain, France, Germany, pan-European competitive circuits | Medium term (2-4 years) |

| Demand for Real-Time Ray Tracing And AI-Upscaling | +2.0% | Global, early-adoption concentration in Germany, UK, France | Short term (≤ 2 years) |

| Rising Adoption Of Gaming Laptops And Portable High-Performance PCs | +1.8% | Germany, UK, Italy, Nordic markets | Medium term (2-4 years) |

| Mobile Gaming Monetization Moving Toward Higher-Fidelity Titles | +1.5% | UK, Germany, France, smartphone-dominant urban markets | Medium term (2-4 years) |

| 5G Standalone Cloud Gaming Bundles Expanding Premium GPU Exposure | +1.1% | Germany, expanding to UK, France, Spain | Long term (≥ 4 years) |

| 16 GB VRAM Expectations Reshaping Upgrade Decisions | +0.9% | Pan-European, concentrated in enthusiast PC gamer communities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Esports And Competitive PC Gaming Participation

Competitive gaming demand in Europe rests on a very large player base that continues to feed more performance-focused hardware purchases over time. Video Games Europe and the European Games Developer Federation stated that 54% of Europeans aged 6-64 played video games in 2024, which kept the addressable hardware base broad across the region.[1]Video Games Europe, “All About Video Games - European Key Facts 2024,” Video Games Europe, videogameseurope.eu That broad participation supports a steady funnel from casual play into organized and performance-led gaming, where refresh rate, responsiveness, and visual stability matter more. Germany's games hardware and accessories segment grew 12% in 2025 to EUR 3.40 billion (USD 3.71 billion), showing that players were still willing to spend on gaming equipment even in a higher-cost environment.[2]Internal Revenue Service, “Yearly Average Currency Exchange Rates,” IRS, irs.gov Gaming PC accessories rose 13% to EUR 1.37 billion (USD 1.49 billion), which points to healthy component demand in one of the region's most important hardware markets. This keeps the Europe gaming GPU market tied to repeated performance-led upgrades rather than to a single purchase cycle.

Demand for Real-Time Ray Tracing and AI-Upscaling

AI-upscaling is now a standard purchase factor in the Europe gaming GPU market rather than an optional premium feature. NVIDIA said DLSS 4, introduced with the GeForce RTX 5000 generation, had reached more than 980 games and applications by May 2026.[3]NVIDIA Corporation, “NVIDIA DLSS And GeForce RTX: List Of All Games, Engines And Applications,” NVIDIA, nvidia.com AMD also positioned AI-assisted rendering as a core feature when it launched the Radeon RX 9000 series and RDNA 4 architecture with FSR 4 in February 2025.NVIDIA further stated that Multi Frame Generation on GeForce RTX 50 Series hardware can increase effective frame output by up to 8x in supported workloads. These technologies are pushing more buyers to look beyond basic 1080p performance and target cards that can sustain higher visual settings over a longer ownership period. That change is lifting the baseline specification that vendors must meet across the Europe gaming GPU market.

Rising Adoption of Gaming Laptops and Portable High-Performance PCs

Portable gaming systems are taking a larger role in the Europe gaming GPU market as laptop performance continues to move closer to desktop capability. ASUS ROG launched the 2026 Zephyrus G14 and G16 in Nordic markets with configurations up to NVIDIA GeForce RTX 5080 Laptop GPU and RTX 5090 Laptop GPU. ASUS also paired these systems with Nebula HDR OLED displays rated at 1,100 nits peak brightness, which shows that premium display and GPU features are now moving together in thinner portable systems. NVIDIA upgraded GeForce NOW to Blackwell RTX 5080-class infrastructure in September 2025 and enabled streaming at up to 5K and 120 FPS for Ultimate members. That upgrade improves the value of portable PCs because high-end gaming access no longer depends only on local thermal limits or onboard GPU class. The laptop category therefore gains from stronger local hardware and from wider access to cloud-rendered performance across the Europe gaming GPU market.

Mobile Gaming Monetization Moving Toward Higher-Fidelity Titles

Mobile gaming is broadening exposure to the Europe gaming GPU market because many players now encounter visually richer game experiences first on smartphones and tablets. Deutsche Telekom presented a 5G Standalone cloud gaming setup with NVIDIA at Gamescom 2025, using network slicing and low-latency delivery to bring premium rendering to mobile devices.[4]Deutsche Telekom, “Gamescom 2025, Telekom Presents The Ultimate Mobile Cloud Gaming Experience With 5G, Powered By NVIDIA,” Deutsche Telekom, telekom.com Deutsche Telekom also pointed to a German mobile gaming audience of 24.6 million players, which indicates how large the reachable base for streamed and GPU-intensive play already is. As streaming quality improves, more users can access visually demanding titles without carrying a discrete GPU inside the device itself. That does not remove GPU demand, but it shifts part of that demand toward server-side rendering and service infrastructure. The Europe gaming GPU market therefore, gains a broader entry point even as the form of hardware consumption becomes more mixed.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost Of Gaming GPUs And Systems | -1.5% | Pan-European, most acute in cost-sensitive markets such as Italy, Spain, Russia | Short term (≤ 2 years) |

| Mature Installed Base Lengthening Replacement Cycles | -1.2% | Pan-European, most pronounced in markets with strong historical discrete GPU penetration | Long term (≥ 4 years) |

| GDDR6 And GDDR6X Supply Tightness Inflating Midrange GPU Prices | -0.8% | Global supply issue, retail pricing impact concentrated in European midrange channel | Medium term (2-4 years) |

| EU Energy And Standby Compliance Pressure On High-TDP Hardware | -0.5% | EU member states, affects all hardware placed on the EU market from May 2025 | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Gaming GPUs and Systems

The current upgrade cycle still carries a high upfront cost burden for many buyers in the Europe gaming GPU market. AMD launched the Radeon RX 9070 at USD 549 and the RX 9070 XT at USD 599 in 2025, while Intel positioned the Arc B580 at USD 249 in late 2024. Even before taxes, partner premiums, and the cost of a full system are added, those levels keep current-generation hardware far from impulse-purchase territory for mainstream households. That pressure narrows the active buyer base for higher-VRAM and higher-ray-tracing tiers, even when long-term performance value is clear. It also pushes some users toward longer retention of existing systems or toward streamed gaming services instead of direct replacement. The result is a market where spending remains healthier than unit turnover because enthusiasts continue to buy sooner than mass-market users.

Mature Installed Base Lengthening Replacement Cycles

A mature installed base is slowing replacement demand in the Europe gaming GPU market because many relatively recent cards still handle mainstream game settings well enough. NVIDIA's wide DLSS software footprint helps extend the usable life of existing hardware by improving effective performance across a large installed library of supported titles. AMD's move to bring FSR 4 into the Radeon RX 9000 lineup also reinforces the role of software-based performance extension in current gaming hardware decisions. When software can stretch hardware life, mainstream players feel less urgency to replace a working card simply to remain playable. That extends replacement cycles and makes yearly demand more dependent on visible feature gains than on basic game compatibility loss. The Europe gaming GPU market therefore, leans more heavily on enthusiasts and professional users, who refresh for higher settings, creator workloads, or competitive targets rather than for simple continuity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By GPU Type: Discrete Silicon Retains Command Despite Integration Advances

Discrete GPUs commanded a 74.44% share of the Europe gaming GPU market in 2025 and are projected to expand at a 9.90% CAGR through 2031. Dedicated graphics hardware remains central because gaming performance still depends on sustained compute, stronger thermal headroom, and direct support for advanced visual workloads. NVIDIA's DLSS 4 footprint across more than 980 games and applications shows why feature-rich discrete cards continue to hold the strongest performance position. AMD reinforced that position in 2025 when it launched the Radeon RX 9000 series with RDNA 4, 16 GB GDDR6 configurations, and FSR 4 support for current-generation gaming. In practical terms, the largest slice of the Europe gaming GPU market continues to sit with cards designed for direct gaming load rather than for shared system use.

Integrated GPUs account for the remaining segment share and remain more relevant for casual play, thin devices, and cloud gaming access points. Intel's Arc B-series launch showed that the company still wants a role in value-oriented graphics, even though the strongest gaming demand remains concentrated in discrete categories. Cloud services from NVIDIA and Deutsche Telekom also reduce the need for a powerful local GPU in lighter gaming scenarios, which helps integrated and hybrid setups stay viable at the lower end. Even so, the Europe gaming GPU industry still draws most of its revenue and product attention from discrete silicon because premium gaming features are advancing fastest there.

By Device Type: Laptops Lead Growth While Desktops Hold Scale

Gaming desktops held 44.31% share of the Europe gaming GPU market size in 2025, which kept towers as the largest device category. Their lead reflects stronger upgrade flexibility, better cooling, and the ability to replace a graphics card without changing the full system. In enthusiast-led markets, desktops remain the clearest route to stepwise GPU upgrades rather than full hardware replacement. Germany's 2025 growth in gaming hardware and accessories supports that pattern because component spending remained active in one of the region's most important gaming hardware markets. That keeps the Europe gaming GPU market closely linked to desktop component demand, even as other device types expand.

Gaming laptops are projected to grow at a 10.12% CAGR through 2031, making them the fastest-growing device type in the Europe gaming GPU market. ASUS highlighted this shift in 2026 with Zephyrus G14 and G16 systems that carried up to RTX 5080 Laptop GPU and RTX 5090 Laptop GPU options in Nordic markets. NVIDIA's GeForce NOW Blackwell upgrade also increased the appeal of portable systems by enabling high-resolution streaming on devices that do not carry the same local GPU headroom. Smartphones and tablets add a third route because 5G cloud gaming services expose mobile users to premium GPU rendering without changing the device form factor.

By End-User Type: Enthusiast Spending Sets The Revenue Pace

Enthusiast and professional gamers held 58.88% of the Europe gaming GPU market in 2025 and are projected to grow at a 10.46% CAGR through 2031. This group shapes revenue more than any other because it upgrades earlier, values premium features sooner, and accepts higher pricing when visible performance gains are available. AMD's 2025 RDNA 4 launch and NVIDIA's ongoing expansion of DLSS-supported titles both aligned closely with this buyer logic through AI-assisted rendering and stronger frame generation support. The group also influences average selling prices because it is more willing to absorb premium system costs at launch. In the Europe gaming GPU industry, that makes the enthusiast cohort more important to revenue direction than its user count alone would imply.

Casual gamers account for the rest of the segment and are more likely to accept integrated graphics, entry discrete cards, or streamed play. Services such as Deutsche Telekom's 5G-focused cloud gaming setup and NVIDIA GeForce NOW widen those alternatives by moving part of the graphics workload to the network and server infrastructure. That reduces the urgency for direct hardware purchases among lighter users but does not remove their connection to GPU-led gaming experiences. As a result, spending in the Europe gaming GPU market stays concentrated in the performance-led cohort even while the regional player base remains broad.

By Memory Type: GDDR6X Holds The Premium Position

GDDR6X captured 53.16% of the Europe gaming GPU market in 2025 and is projected to post the fastest 10.88% CAGR through 2031. Its lead reflects the premium tier's focus on bandwidth-heavy workloads such as ray tracing, AI rendering, and higher-resolution gaming. NVIDIA's expanding DLSS feature set and Blackwell-era performance positioning keep high-end memory configurations central to flagship card appeal. This means the memory discussion in the Europe gaming GPU market now centers on both capacity and throughput. The premium segment, therefore, remains closely tied to higher-bandwidth memory choices.

GDDR6 holds an important secondary position because AMD's RX 9070 and RX 9070 XT both launched with 16 GB GDDR6 and targeted strong gaming performance at USD 549 and USD 599. Legacy graphics memory continues to fade as older hardware shifts into longer-life but lower-priority usage. Unified memory is gaining visibility in portable and compact devices, where efficiency and shared system design matter more than traditional board layouts. Even with those alternatives, the Europe gaming GPU industry still centers its premium value proposition on discrete cards that pair advanced rendering features with high-performance memory subsystems.

Geography Analysis

Germany remains the anchor country in the Europe gaming GPU market because it combines large-scale player demand, active hardware spending, and early infrastructure activity. The German games market grew 4% in 2025 to EUR 9.38 billion (USD 10.22 billion), while games hardware and accessories rose 12% to EUR 3.40 billion (USD 3.71 billion). Gaming PC accessories increased 13% to EUR 1.37 billion (USD 1.49 billion), showing sustained demand for GPU-adjacent spending and upgrade-led behavior. Deutsche Telekom also showcased a 5G Standalone cloud gaming model with NVIDIA in Germany in 2025, which strengthened the country's role in premium game delivery beyond direct device sales. With strong hardware demand and service-side experimentation, Germany remains the clearest national engine within the Europe gaming GPU market.

The United Kingdom and France form the next important demand layer in the Europe gaming GPU market, although their demand drivers are different. The UK benefits from the broad regional gaming base identified by Video Games Europe, which supports ongoing demand for both competitive PC setups and portable systems. France adds a stronger institutional compute angle because AMD and Eviden were selected in November 2025 to build the Alice Recoque exascale system at a project cost of EUR 554 million (USD 604 million). AMD and the French government deepened that relationship again in April 2026 as part of France's National AI Strategy, which strengthens France's place in the wider graphics and compute ecosystem. Together, the UK and France support the Europe gaming GPU market through consumer demand on one side and ecosystem relevance on the other.

Italy, Spain, Russia, and the Rest of Europe remain important because regional gaming participation is broad and demographically diverse. Italy and Spain continue to matter for mainstream gaming system demand, while Russia still retains relevance through competitive gaming communities even under more complex distribution conditions. Across the Rest of Europe, NVIDIA's Blackwell GeForce NOW expansion in Frankfurt and Paris improved access to high-end GPU rendering for nearby markets that depend more on streaming than on frequent local hardware upgrades. Nordic countries also showed healthy interest in premium portable gaming through ASUS's 2026 Zephyrus G14 and G16 rollout, which points to solid demand beyond the region's largest economies.

Competitive Landscape

The Europe gaming GPU market is concentrated at the core architecture layer because commercially relevant gaming designs still come from NVIDIA, AMD, and Intel. Competition becomes broader at the board and system level, where vendors differentiate through cooling, size, warranty support, and factory tuning rather than through new silicon design. NVIDIA strengthened its position in 2026 by extending DLSS support to more than 980 games and applications, which widened the software advantage tied to GeForce hardware. The company also upgraded GeForce NOW to Blackwell RTX 5080-class infrastructure in September 2025, giving European users access to premium rendering without a local flagship card. That two-layer strategy keeps NVIDIA visible in both direct hardware sales and subscription-led play.

AMD's clearest opening remains the value-focused performance tier, where the Radeon RX 9070 and RX 9070 XT launched with 16 GB GDDR6 memory and FSR 4 at USD 549 and USD 599. That pricing and feature position gave AMD a direct route to buyers who wanted current-generation capability without moving into the highest price brackets. AMD also expanded its European footprint through the Alice Recoque exascale project in France and through its April 2026 collaboration with the French government, which strengthens ecosystem depth beyond retail card sales. Intel remained relevant as the third silicon designer after launching the Arc B580 and Arc B570, which brought XeSS 2 and 12 GB GDDR6 into the budget discrete tier. Even where Intel has less influence in premium gaming, its presence still matters because it keeps entry-level competition from narrowing too far.

Another notable move came from the 2025 NVIDIA and Intel collaboration to develop consumer PC and data center products, including x86 SoCs integrating NVIDIA RTX GPU chiplets for compact PCs and gaming laptops. That arrangement adds a co-development route that could matter for smaller gaming form factors in Europe over time. For add-in-board makers and gaming system vendors, the main challenge is not inventing the next architecture, but packaging shared silicon in the most compelling way for local buyers. The Europe gaming GPU market therefore remains concentrated in technology control, while still showing wider variety in retail brands, system design, and route to end users.

Europe Gaming GPU Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc.

Intel Corporation

Qualcomm Incorporated

Apple Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: ASUS Republic of Gamers announced the ROG NUC 16, a compact gaming PC featuring up to an NVIDIA GeForce RTX 5080 Laptop GPU and an Intel Core ARL-HX processor, expanding the small-form-factor gaming segment in Europe with a platform designed for gaming, creative, and AI workloads.

- April 2026: AMD and the French government announced plans to deepen collaboration supporting France's National AI Strategy, with AMD contributing to the Alice Recoque exascale supercomputer ecosystem and expanding its European R&D footprint, deepening AMD's institutional presence in the European compute and gaming GPU supply chain.

- January 2026: AMD unveiled the Ryzen 7 9850X3D at CES 2026, positioned as the fastest gaming processor featuring Zen 5 architecture and AMD 3D V-Cache technology, reinforcing the company's integrated compute platform strategy for high-performance PC gaming.

- December 2025: Deutsche Telekom officially launched its 5G+ Gaming service with NVIDIA GeForce NOW, deploying 5G Standalone network slicing and L4S technology at national scale in Germany. The service was made available to eligible MagentaMobil customers with compatible Samsung Galaxy S24 and S25 series devices, establishing the first consumer-scale latency-optimized cloud gaming service in Europe on a 5G SA infrastructure.

Europe Gaming GPU Market Report Scope

The Europe Gaming GPU Market refers to the market for specialized graphics processing units used to accelerate image rendering and visual performance in gaming devices and systems across Europe. Gaming GPUs are designed to manipulate memory and process large amounts of data in parallel, enabling smoother gameplay, higher frame rates, and advanced graphics quality.

The Europe Gaming GPU Market Report is Segmented by GPU Type (Discrete GPUs, Integrated GPUs), Device Type (Gaming Desktops, Gaming Laptops, Smartphones, and Tablets), End-User Type (Casual Gamers, and Enthusiast and Professional Gamers), Memory Type (GDDR6, GDDR6X, Legacy Graphics Memory, and Unified Memory), and Country. Market Forecasts Are Provided In Terms Of Value (USD).

| Discrete GPUs |

| Integrated GPUs |

| Gaming Desktops |

| Gaming Laptops |

| Smartphones and Tablets (Mobile Gaming) |

| Casual Gamers |

| Enthusiast and Professional Gamers |

| GDDR6 |

| GDDR6X |

| Legacy Graphics Memory |

| Unified Memory |

| By GPU Type | Discrete GPUs |

| Integrated GPUs | |

| By Device Type | Gaming Desktops |

| Gaming Laptops | |

| Smartphones and Tablets (Mobile Gaming) | |

| By End-User Type | Casual Gamers |

| Enthusiast and Professional Gamers | |

| By Memory Type | GDDR6 |

| GDDR6X | |

| Legacy Graphics Memory | |

| Unified Memory |

Key Questions Answered in the Report

How large is the Europe gaming GPU market through 2031?

The Europe gaming GPU market was valued at USD 5.33 billion in 2025, is projected to reach USD 6.03 billion in 2026, and is forecast to reach USD 9.51 billion by 2031 at a 9.54% CAGR.

Which GPU type leads demand in Europe?

Discrete GPUs lead the category with 74.44% share in 2025 and are also the fastest-growing GPU type, with a projected 9.90% CAGR through 2031.

Why are gaming laptops growing faster than desktops in Europe?

Gaming laptops are projected to grow at 10.12% CAGR because portable systems now offer much stronger graphics performance, and cloud gaming upgrades are improving high-end access on thinner devices.

Which user group drives spending the most?

Enthusiast and professional gamers are the main revenue engine, holding 58.88% share in 2025 and recording the fastest projected CAGR at 10.46% through 2031.

How important are AI-upscaling and ray tracing in current buying decisions?

They are now central to purchase decisions because vendors are using them to define current-generation performance, and NVIDIA alone had DLSS support in more than 980 games and applications by May 2026.

Which countries matter most for gaming GPU demand in Europe?

Germany is the strongest anchor because it combines large gaming spend, rising hardware and accessories sales, and early cloud gaming infrastructure activity, while the UK, France, Italy, Spain, Russia, and Nordic markets remain important regional contributors.

Can cloud gaming reduce direct graphics card purchases?

Yes, especially for casual users, because services such as GeForce NOW and Deutsche Telekom's 5G-led setup allow premium rendering without a local flagship GPU, though they also expand overall exposure to GPU-powered gaming.

Page last updated on: