North America Integrated GPU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2025 - 2031 |

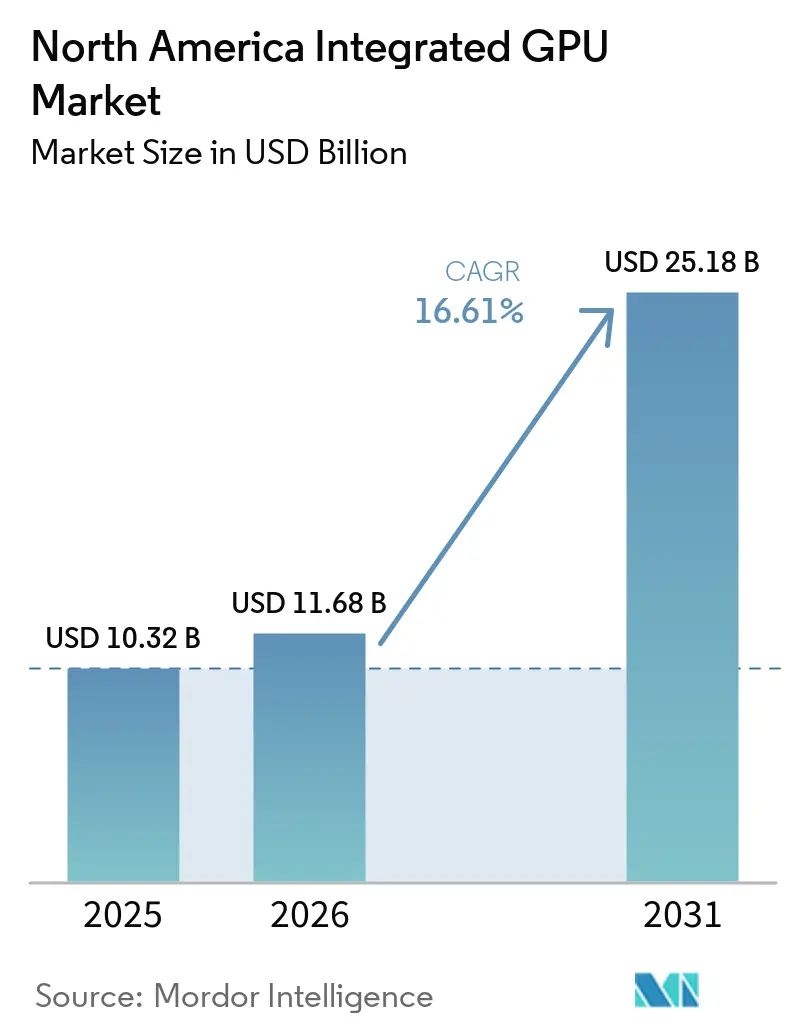

| Base Year Market Size (2025) | USD 10.32 Billion |

| Market Size (2026) | USD 11.68 Billion |

| Market Size (2031) | USD 25.18 Billion |

| Growth Rate (2025 - 2031) | 16.61% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Integrated GPU Market Analysis by Mordor Intelligence

The North America integrated GPU market size was USD 10.32 billion in 2025 and is projected to reach USD 25.18 billion by 2031 at a CAGR of 16.61% during 2026-2031. Growth is being driven by a shift in computing design, where AI-capable iGPUs, unified memory, and dedicated NPUs increasingly sit on a single SoC. That combination is reducing the need for discrete graphics in a broad set of consumer and professional workloads across the region. The upgrade cycle has also moved forward because Windows 10 end of support and Copilot+ PC hardware thresholds turned many purchase decisions into both a compliance issue and a capability upgrade. Premium smartphones, tablets, and AI-ready PCs are supporting stronger selling prices because buyers are paying for local AI performance rather than basic graphics alone. Edge AI programs, industrial HMI deployments, and sovereign compute initiatives are also widening the North America integrated GPU market beyond traditional PCs and mobile devices.

Key Report Takeaways

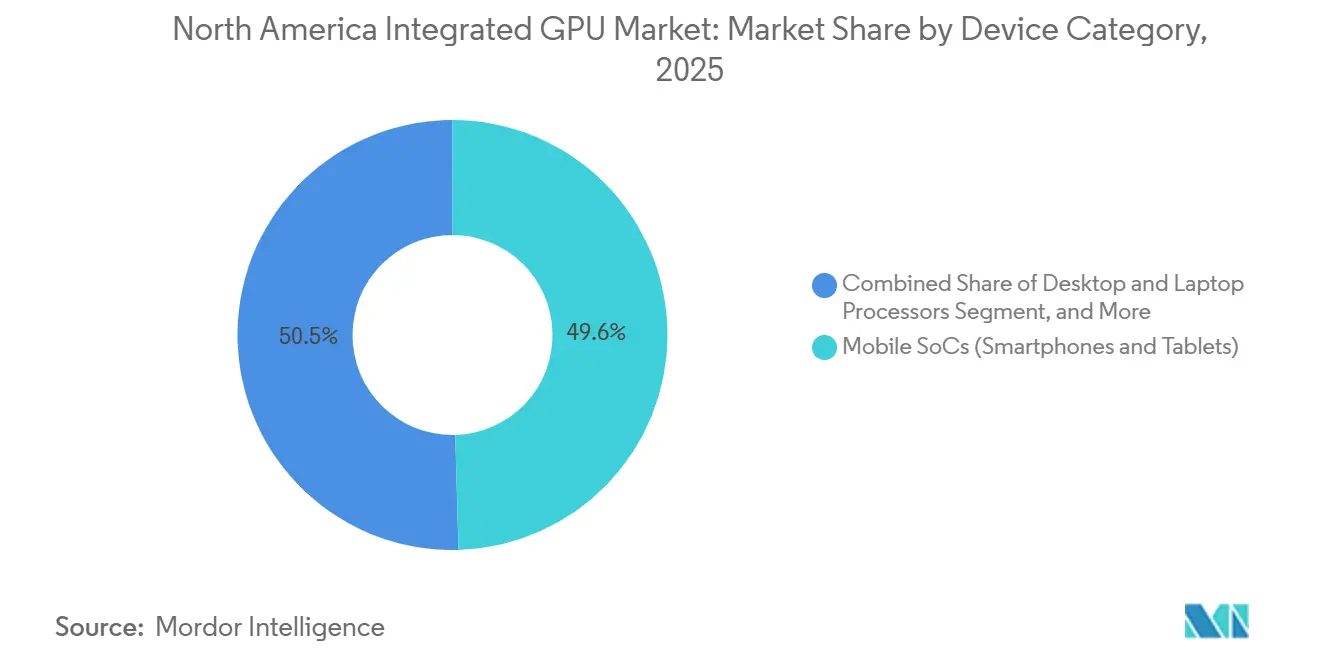

- By device category, Mobile SoCs held 49.55% of revenue in 2025, while Server and Data Center Processors with Integrated Graphics are projected to expand at a 16.98% CAGR through 2031.

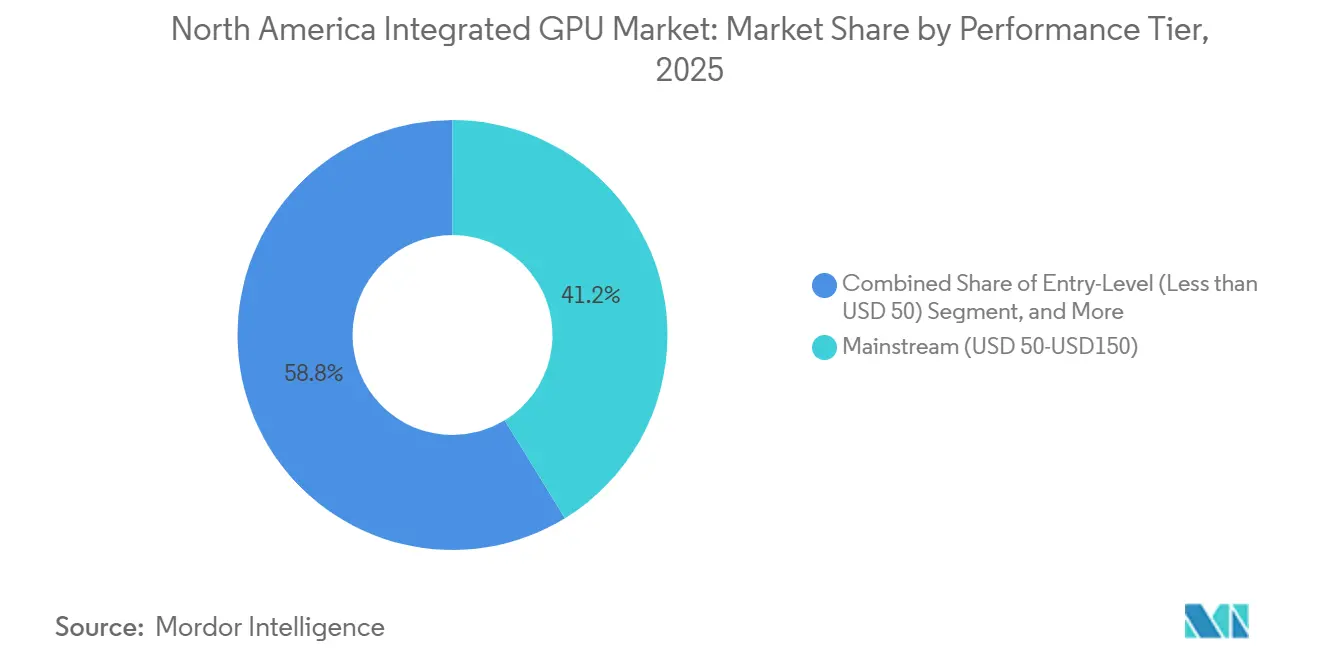

- By performance tier, Mainstream accounted for 41.23% of revenue in 2025, while the Performance tier is projected to grow at a 17.25% CAGR through 2031.

- By geography, the United States held 84.54% of the North America integrated GPU market in 2025, while Canada is projected to expand at a 17.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Integrated GPU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI PC Refresh Cycle After Windows 10 End Of Support | +5.2% | United States and Canada, enterprise and SMB PC fleets | Short term (≤ 2 years) |

| Rising GenAI Workloads On Premium Smartphone And Tablet SoCs | +3.8% | United States and Canada, premium mobile and tablet segment | Medium term (2-4 years) |

| Cost And Power Advantage Versus Discrete Graphics In Mainstream Systems | +2.5% | North America-wide, mainstream OEM laptop and desktop ecosystems | Medium term (2-4 years) |

| Growth In Edge AI And Industrial HMI SoCs | +1.8% | United States, manufacturing and energy, Canada, edge compute, Mexico, nearshore industrial | Long term (≥ 4 years) |

| LPDDR5X And Unified Memory Bandwidth Lifting iGPU Usability | +1.4% | North America-wide, laptop and mobile device segments | Short term (≤ 2 years) |

| Single-Chip Platform Optimization Under Tariff Pressure | +0.9% | United States and Canada, OEM supply chains targeting BOM cost certainty | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI PC Refresh Cycle After Windows 10 End of Support

Windows 10 reached end of support on October 14, 2025, which removed regular security and feature updates for systems that were still widely used across enterprise and SMB fleets. In North America, that change turned PC replacement into a more urgent decision for IT teams working under security and compliance requirements. Intel’s Core Ultra Series 3 Panther Lake processors entered commercial availability at CES in January 2026 as the first client chips built on Intel 18A, with up to 180 Platform TOPS and an Xe3 Arc GPU that moved performance well above the prior generation.[1]Intel Corporation, “Intel Unveils Panther Lake Architecture, First AI PC Platform Built on 18A,” Intel Newsroom, newsroom.intel.com Microsoft’s Copilot+ PC threshold of 40 dedicated NPU TOPS also placed many older systems outside the preferred hardware pool for on-device AI work. This pairing of a firm support deadline and a clear hardware step-up is pulling refresh budgets forward instead of letting companies delay purchases. It is also supporting near-term expansion in the North America integrated GPU market because buyers are paying for AI readiness rather than only replacing aging PCs.

Rising GenAI Workloads on Premium Smartphone and Tablet SoCs

Apple’s M5, released on October 15, 2025, used third-generation 3-nanometer technology, a 10-core GPU, dedicated Neural Accelerators in each GPU core, and 153 GB/s of unified memory bandwidth. Apple said the chip delivered more than 4x peak GPU AI compute versus M4, which raised the performance standard for premium notebooks, tablets, and spatial devices sold in the region. Qualcomm’s heterogeneous design pairs the Adreno GPU with the Hexagon NPU on the same die, which improves on-device token generation by avoiding off-chip data movement and reducing memory latency.[2]Qualcomm Incorporated, “Unlocking On-Device Generative AI with an NPU and Heterogeneous Computing,” Qualcomm, qualcomm.com This matters in the North America integrated GPU market because premium users increasingly expect voice, vision, translation, and assistant features to run locally with better responsiveness and privacy. Micron’s 1-gamma LPDDR5X, shipped in June 2025 at 10.7 Gbps, cut power use by 20% and improved AI voice-translation response times by more than 50% in the company’s Llama 2 testing. Higher memory throughput is therefore improving sustained iGPU usability in flagship smartphones and tablets rather than only lifting headline benchmark scores.

Cost and Power Advantage Versus Discrete Graphics in Mainstream Systems

Integrated graphics remove the need for separate VRAM, dedicated board power delivery, and extra PCIe overhead, which lowers system cost and system power draw in high-volume PCs. That cost structure matters in the North America integrated GPU market because OEMs can shift savings into storage, battery size, or thinner system designs instead of paying for an add-in card. AMD’s Ryzen AI MAX+ 395 combined 40 RDNA 3.5 compute units, a 256-bit LPDDR5X memory interface, and 32 MB of Infinity Cache in a thin-and-light platform detailed in March 2025. AMD also positioned the chip as capable of discrete workstation GPU performance in selected creative workloads without an external GPU cost premium. As iGPU platforms improve, the practical market for entry and mid-tier discrete GPUs in productivity systems narrows first, even before gaming and workstation demand changes. That is why mainstream buyers are starting to judge value on total device capability and battery life, not only on the presence of standalone graphics.

Growth in Edge AI and Industrial HMI SoCs

Demand is rising for embedded SoCs that can handle machine vision, control logic, and display output from one low-power chip in factories, utilities, medical systems, and retail terminals across North America. Renesas introduced the RZ/G3E MPU with 4 Cortex-A55 cores, full HD graphics output, and an Ethos-U55 NPU rated at 512 GOPS for high-performance HMI and edge computing uses. NXP’s i.MX 95 family combines an Arm Mali-G310 integrated GPU with an onboard NPU for industrial HMI, automotive infotainment, and building automation platforms. In Canada, the FABrIC initiative announced CAD 10.7 million (USD 7.8 million), for 11 Edge AI semiconductor projects in May 2026, which supports a wider base for embedded iGPU adoption. The same pull is visible in Mexico, where nearshore assembly and industrial automation are expanding the need for display-capable SoCs that can stay within regional supply chains. This gives the North America integrated GPU market a longer runway beyond PCs and handsets because industrial demand follows equipment cycles that are less tied to consumer replacement patterns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Performance Ceiling Versus Discrete GPUs In Gaming And Workstations | -2.1% | United States, gaming OEMs and professional workstation segment | Long term (≥ 4 years) |

| Shared Memory Bandwidth and Capacity Constraints | -1.4% | North America-wide, laptop and creative professional segments | Medium term (2-4 years) |

| Tariffs and Memory Inflation Raising System Prices | -1.0% | United States and Canada, entry and mainstream price bands | Short term (≤ 2 years) |

| Limited Fit for Integrated Graphics In Server and Data Center Deployments | -0.6% | United States, hyperscale and enterprise data centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Performance Ceiling Versus Discrete GPUs in Gaming and Workstations

Integrated graphics still share system memory with the CPU, which keeps available bandwidth well below discrete cards that use GDDR6X or HBM. Intel said Panther Lake with Xe3 graphics moved closer to entry-level discrete mobile performance, but that still leaves a large gap to higher-end gaming and workstation cards. In North America, that gap matters because gaming, 3D content creation, architectural visualization, and simulation remain concentrated in professional segments that pay the highest per-unit prices. These workloads also require sustained memory bandwidth and VRAM pools that can exceed 24 GB, which current iGPU platforms do not match in multi-user or multi-model settings. The issue for vendors is less about total shipment volumes and more about revenue density, because the premium end of graphics spending still sits in discrete hardware. As a result, the North America integrated GPU market can grow rapidly without fully displacing the most profitable workstation and enthusiast categories.

Shared Memory Bandwidth and Capacity Constraints

Unified memory helps simplify system design, but it forces the CPU, NPU, and iGPU to compete for the same DRAM pool during mixed workloads. AMD’s Strix Halo platform offered up to 276 GB/s through LPDDR5X-8533, which is strong for many single-model AI tasks but still below the highest bandwidth levels now seen in premium unified-memory systems.[3]Advanced Micro Devices, Inc., “AMD Ryzen AI MAX+ 395 Processor, Breakthrough AI Performance in Thin and Light,” AMD, amd.com In creative workstations and advanced on-device AI use, that gap becomes visible during sustained media processing, multi-model inference, and large-parameter model execution. Mainstream systems in the USD 50-USD 300 bands also tend to share 16 GB to 32 GB of total system memory, which limits how much can be treated as effective graphics memory for heavier AI and media workloads. Micron’s 1-gamma LPDDR5X narrows part of this gap with faster speeds and better power efficiency, but the initial wave is concentrated in premium mobile designs rather than high-volume laptop price bands. That means bandwidth progress will help first at the top end while the volume base of the North America integrated GPU market will take longer to benefit.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Category: Mobile SoCs Dominate While Server Segment Surges

Mobile SoCs held 49.55% of device-category revenue in 2025, the largest slice of the North America integrated GPU market share within this segmentation. Apple’s strength in premium smartphones and tablets helped sustain that lead, while Qualcomm continued to build its role in higher-value Windows-on-ARM systems and premium mobile computing. Desktop and laptop processors remain central to the North America integrated GPU market because enterprise refresh demand is now tied to AI-ready client hardware rather than only routine replacement. AMD said its mobile processor unit share rose to 26.0% in Q4 2025, reflecting stronger Ryzen AI uptake in enterprise and premium consumer systems. Embedded and industrial SoCs stayed smaller in revenue terms, but they remained widely distributed across factory automation, energy, and retail equipment deployments.

Server and Data Center Processors with Integrated Graphics are projected to expand at a 16.98% CAGR through 2031, making them the fastest-growing device category. That growth reflects a practical need at the rack edge, where inference, visualization, media handling, and local display output often need to run together without the cost of a discrete add-in card. Intel highlighted this direction with Crescent Island, an Xe3P-based data center GPU announced with 160 GB of LPDDR5X memory for air-cooled enterprise inference workloads. AMD also said in November 2025 that it expected very rapid expansion in data center AI revenue, which supports wider use of embedded graphics IP across edge-oriented server platforms. Across the North America integrated GPU industry, this category is gaining from lower idle power, simpler deployment, and branch and factory use cases that do not justify a separate accelerator card.

By Performance Tier: Mainstream Rules While the Performance Band Accelerates

The Mainstream tier held 41.23% of revenue in 2025, giving it the largest position in the North America integrated GPU market size by pricing band. The Performance tier is projected to expand at a 17.25% CAGR through 2031, which makes it the fastest-growing bracket as enterprises and premium consumers move toward AI-capable devices. This band now benefits from PC refresh demand, Copilot+ PC eligibility, and smartphone replacement cycles that reward stronger on-device inference capability rather than only higher clock speeds. Intel’s Panther Lake platform pushed this range upward with up to 180 Platform TOPS and a major GPU step on Intel 18A. The result is a mix shift toward better-equipped systems while the high-volume center of demand still remains in mainstream laptops and mobile SoCs.

Entry-level silicon below USD 50 still served embedded HMI, industrial IoT, and simple display use cases where long product cycles matter more than peak graphics. At the top end, platforms above USD 300 held pricing power because buyers in creative work and local AI development valued higher memory ceilings and broader graphics capability. AMD’s Ryzen AI MAX+ 395 supported up to 128 GB of LPDDR5X-8533 unified memory and enabled large on-device model work that previously depended more heavily on discrete hardware. That shift matters for the North America integrated GPU industry because some developer and workstation tasks are moving onto portable systems that can keep data local and power use contained. Even so, premium tiers will grow alongside mainstream volumes, not in place of them, because the installed base still spans cost-sensitive enterprise fleets, consumer notebooks, and industrial systems.

Geography Analysis

The United States accounted for 84.54% of regional revenue in 2025, the clear largest share of the North America integrated GPU market share by geography. The country combines the region’s largest enterprise PC fleet with the deepest premium smartphone, tablet, and commercial device spending base. Windows 10 end of support on October 14, 2025 pushed many organizations toward faster replacement cycles, especially where security and support status mattered. That demand has tilted toward Performance and High-Performance platforms that can meet Copilot+ PC requirements and support on-device AI tasks. The CHIPS and Science Act is also improving supply resilience, with more than USD 100 billion in announced U.S. semiconductor investments from Intel, TSMC, and Samsung.

Canada is projected to record a 17.43% CAGR through 2031, making it the fastest-growing geography and an important part of the North America integrated GPU market size outlook. The Government of Canada committed CAD 662 million (USD 485 million), with IBM Canada and C2MI in November 2025 to expand semiconductor manufacturing and packaging capacity in Bromont, Quebec. Bell Canada’s 300 MW AI Fabric data center in Saskatchewan, announced in March 2026 with Cerebras and CoreWeave as anchor tenants, showed that AI infrastructure buildout is moving beyond pilot stage. FABrIC added CAD 10.7 million (USD 7.8 million), for 11 Edge AI semiconductor projects in May 2026, aimed at edge computing, connectivity, and sensing uses that support embedded iGPU demand. This mix of public funding, packaging capacity, and AI facility investment is giving Canada outsized momentum in server and embedded deployments relative to its current size.

Mexico remained the smallest national market, but its role in back-end electronics assembly and industrial automation gives it strategic weight in regional supply chains. OECD analysis said Mexico is targeting semiconductor exports of USD 9.8 billion by 2030 through stronger back-end assembly and mature-node packaging capabilities. The same analysis noted GDP growth of 0.4% in 2025, which constrained near-term domestic consumer electronics demand even as nearshoring supported industrial equipment purchases. The 2026 USMCA review adds policy uncertainty, yet preserving tariff-free semiconductor trade remains important for OEMs sourcing iGPU-equipped industrial modules through Mexico.

Competitive Landscape

The North America integrated GPU market remained moderately concentrated in premium computing tiers and more fragmented in embedded and industrial categories. Intel and AMD continued to dominate x86 integrated graphics revenue in laptops and desktops, while Apple controlled a large share of premium notebook and tablet value through its closed silicon model. AMD said its mobile processor unit share reached 26.0% in Q4 2025 and mobile revenue share reached 24.9%, which reflected growing Ryzen AI adoption in enterprise and premium consumer systems. Apple’s M5 family raised performance expectations with more than 4x peak GPU AI compute versus M4 and 153 GB/s of unified memory bandwidth, which reinforced its premium positioning. Qualcomm added a third scaled architecture in PCs by pairing Snapdragon X chips with local AI features and tighter connectivity integration.

Competitive strategy in the North America integrated GPU market is increasingly defined by platform control rather than raw graphics alone. Intel’s Panther Lake combined Intel 18A, RibbonFET transistors, PowerVia backside power delivery, and Xe3 graphics, giving Intel a manufacturing-led differentiation path that rivals cannot copy directly. Qualcomm strengthened its long-term position when it completed the Alphawave Semi acquisition in December 2025, adding PCIe 7.0, CXL, and UCIe connectivity IP that supports tighter SoC data fabric integration. AMD used its November 2025 strategy update to highlight a 2.5x expansion in AI PC platform coverage since 2024 and to preview next-generation processors aimed at much higher AI performance. These moves show that vendors are competing across process technology, memory architecture, interconnect, software readiness, and product breadth at the same time.

A notable opening remains in industrial and automotive edge systems where buyers increasingly want stronger integrated graphics together with long-life supply, safety certification, and AI capability. NXP and Renesas already serve this embedded base well, but their current offerings still prioritize reliability and control over the compute density seen in mainstream PC-class platforms. That leaves room for suppliers that can combine industrial certification with performance-tier graphics for advanced HMI, machine vision, and local inference in North American facilities. The North America integrated GPU market is therefore likely to stay multi-polar, with leadership split by architecture, device class, and end-use requirements rather than concentrated around one universal supplier.

North America Integrated GPU Industry Leaders

Intel Corporation

Apple Inc.

Advanced Micro Devices, Inc.

Qualcomm Incorporated

MediaTek Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The Government of Canada's FABrIC initiative announced CAD 10.7 million (USD 7.8 million) in federal funding for 11 Edge AI semiconductor projects across Canada, with an estimated total project value of CAD 44.3 million (USD 32.4 million), targeting edge computing, AI connectivity, and low-power sensing applications that directly support embedded iGPU demand.

- May 2026: NXP announced the i.MX 937 applications processor for automotive, industrial, and commercial IoT applications, featuring an integrated eIQ Neutron NPU and 1080p60-capable GPU, development board access is planned for late 2026 with full silicon in early 2027, extending NXP's edge AI iGPU roadmap for North American industrial customers.

- May 2026: Qualcomm introduced the Snapdragon 8 Gen 5, delivering an NPU rated 46% faster than the Snapdragon 8 Gen 3 with support for INT2 precision quantization enabling higher compression of large language models at mobile power envelopes, the chip targets premium Android smartphone OEMs expanding on-device AI capabilities for 2026 flagship devices.

- March 2026: Bell Canada and the Government of Saskatchewan announced the 300 MW Bell AI Fabric data center in Regina with Cerebras and CoreWeave as anchor tenants, representing a major expansion of Canada's national AI compute infrastructure and driving new demand for server-class SoCs with integrated graphics for inference visualization tasks.

North America Integrated GPU Market Report Scope

The North America Integrated GPU Market encompasses the global industry involved in the design, development, and deployment of graphics processing units integrated into a system-on-chip (SoC) or processor architecture rather than as standalone discrete components. These integrated GPUs share system memory and are widely used to deliver efficient graphics processing across cost-sensitive, power-efficient computing devices.

The North America Integrated GPU Market is Segmented by Device Category (Desktop and Laptop Processors, Mobile SoCs (Smartphones and Tablets), Embedded and Industrial SoCs, and Server and Data Center Processors with Integrated Graphics), Performance Tier (Entry-Level (Less than USD 50), Mainstream (USD 50 - USD 150), Performance (USD 150 - USD 300), and High-Performance (Greater than USD 300)), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Desktop and Laptop Processors |

| Mobile SoCs (Smartphones and Tablets) |

| Embedded and Industrial SoCs |

| Server and Data Center Processors with Integrated Graphics |

| Entry-Level (Less than USD 50) |

| Mainstream (USD 50 - USD 150) |

| Performance (USD 150 - USD 300) |

| High-Performance (Greater than USD 300) |

| United States |

| Canada |

| Mexico |

| By Device Category | Desktop and Laptop Processors |

| Mobile SoCs (Smartphones and Tablets) | |

| Embedded and Industrial SoCs | |

| Server and Data Center Processors with Integrated Graphics | |

| By Performance Tier | Entry-Level (Less than USD 50) |

| Mainstream (USD 50 - USD 150) | |

| Performance (USD 150 - USD 300) | |

| High-Performance (Greater than USD 300) | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the size outlook for the North America integrated GPU space?

It was valued at USD 10.32 billion in 2025 and is projected to reach USD 25.18 billion by 2031, growing at a 16.61% CAGR during 2026-2031.

What is driving faster replacement demand for integrated GPU platforms in North America?

Windows 10 end of support, Copilot+ PC hardware thresholds, and rising demand for on-device AI are pushing enterprises and consumers toward newer AI-capable systems.

Which device category leads revenue in the region?

Mobile SoCs led with 49.55% of device-category revenue in 2025, supported by strong premium smartphone and tablet demand.

Which pricing band is expanding the fastest?

The Performance tier is projected to grow at a 17.25% CAGR through 2031 as buyers move toward AI-ready laptops, premium mobile SoCs, and higher-value computing platforms.

Which country is growing the fastest in North America?

Canada is projected to post the highest CAGR at 17.43% through 2031, supported by sovereign AI programs, packaging investment, and new data center capacity.

What is the main limit on broader integrated GPU adoption in premium workloads?

Integrated graphics still face memory bandwidth and capacity limits versus discrete GPUs, which keeps high-end gaming and workstation workloads more dependent on standalone graphics hardware.

Page last updated on: