Government and Public Sector Green IT Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

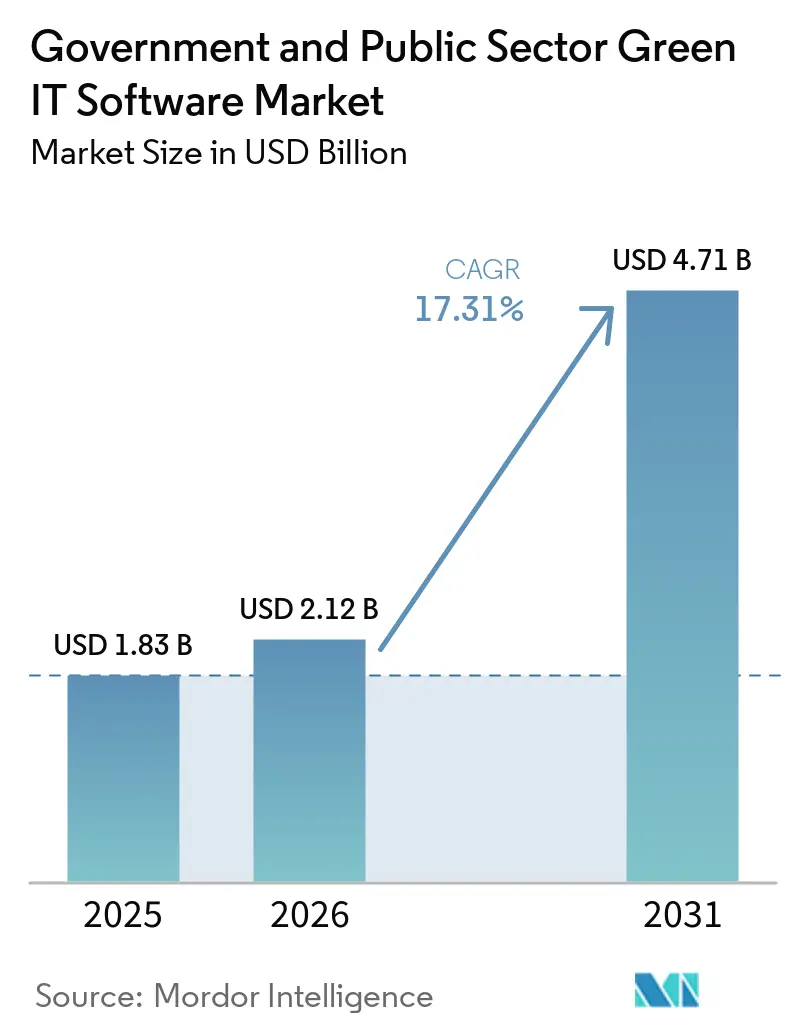

| Market Size (2026) | USD 2.12 Billion |

| Market Size (2031) | USD 4.71 Billion |

| Growth Rate (2026 - 2031) | 17.31% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Government and Public Sector Green IT Software Market Analysis by Mordor Intelligence

The government and public sector green IT software market size is expected to increase from USD 1.83 billion in 2025 to USD 2.12 billion in 2026 and reach USD 4.71 billion by 2031, growing at a CAGR of 17.31% over 2026-2031. This growth reflects a clear shift in how public agencies manage sustainability records, as many bodies that once relied on manual annual filings now need verified, audit-ready carbon data throughout the year. Policy deadlines that went into effect across 2025 and 2026 are shortening decision cycles, which is pushing software procurement into a tighter time window than agencies usually follow. The government and public sector green IT software market is also being shaped by the fact that agencies prefer vendors already connected to approved procurement channels and core enterprise systems. That pattern supports broader platform expansion, especially when software can absorb rule changes through managed updates instead of agency-led reconfiguration. Even so, budget fragmentation, data sovereignty demands, and limited internal carbon accounting capacity are prolonging deployment cycles in the government and public sector green IT software market compared to commercial environments.

Key Report Takeaways

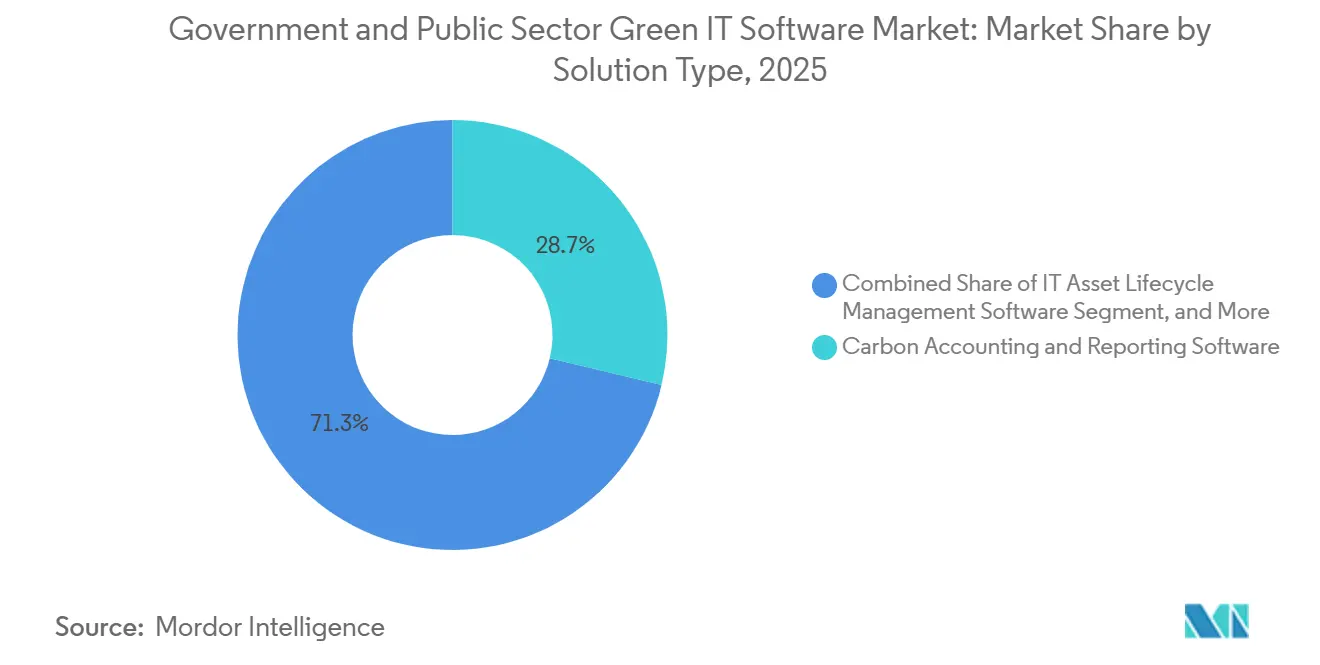

- By solution type, carbon accounting and reporting software held 28.74% of the government and public sector green IT software market share in 2025, while green procurement and supplier sustainability software is projected to expand at 18.12% CAGR through 2031.

- By deployment, cloud accounted for 65.41% of revenues in 2025, while hybrid deployment is expected to record the highest CAGR of 17.95% during 2026-2031.

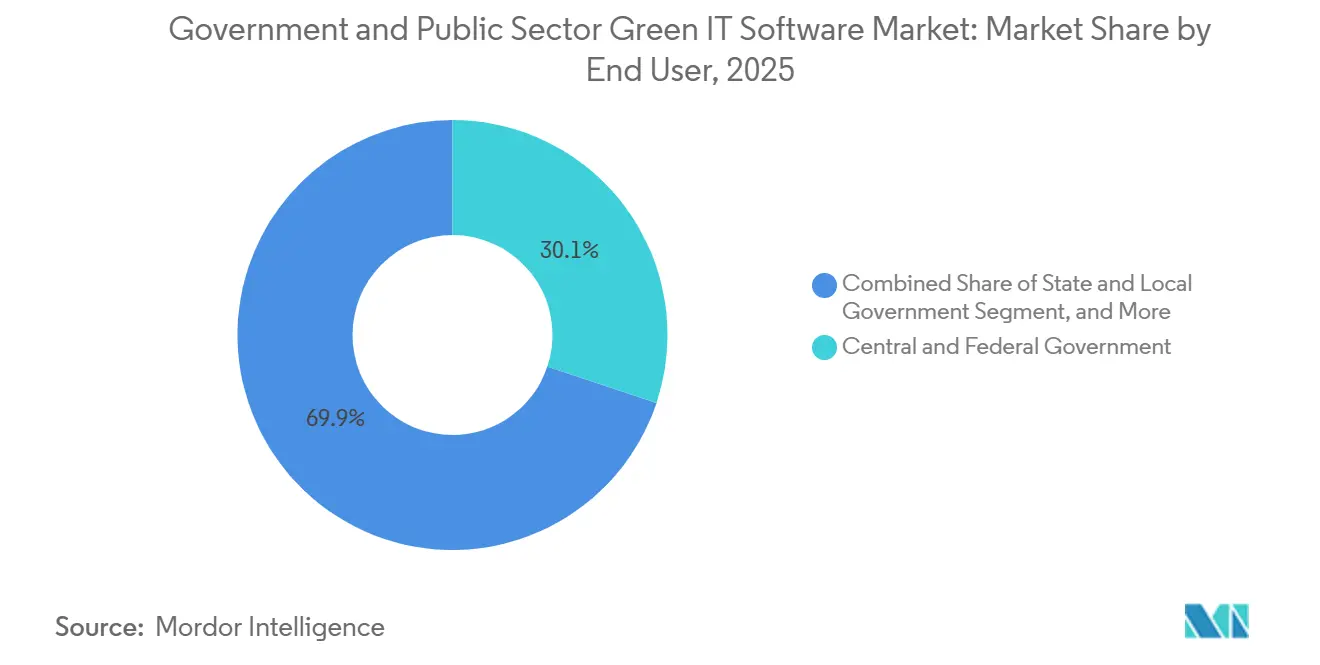

- By end user, central and federal government agencies accounted for 30.12% of spending in 2025, while public education and public healthcare institutions are projected to grow at a 18.25% CAGR through 2031.

- By application, compliance, audit, and ESG workflow automation accounted for 29.63% of revenue in 2025, while public procurement and supplier emissions tracking are projected to grow at a 18.34% CAGR through 2031.

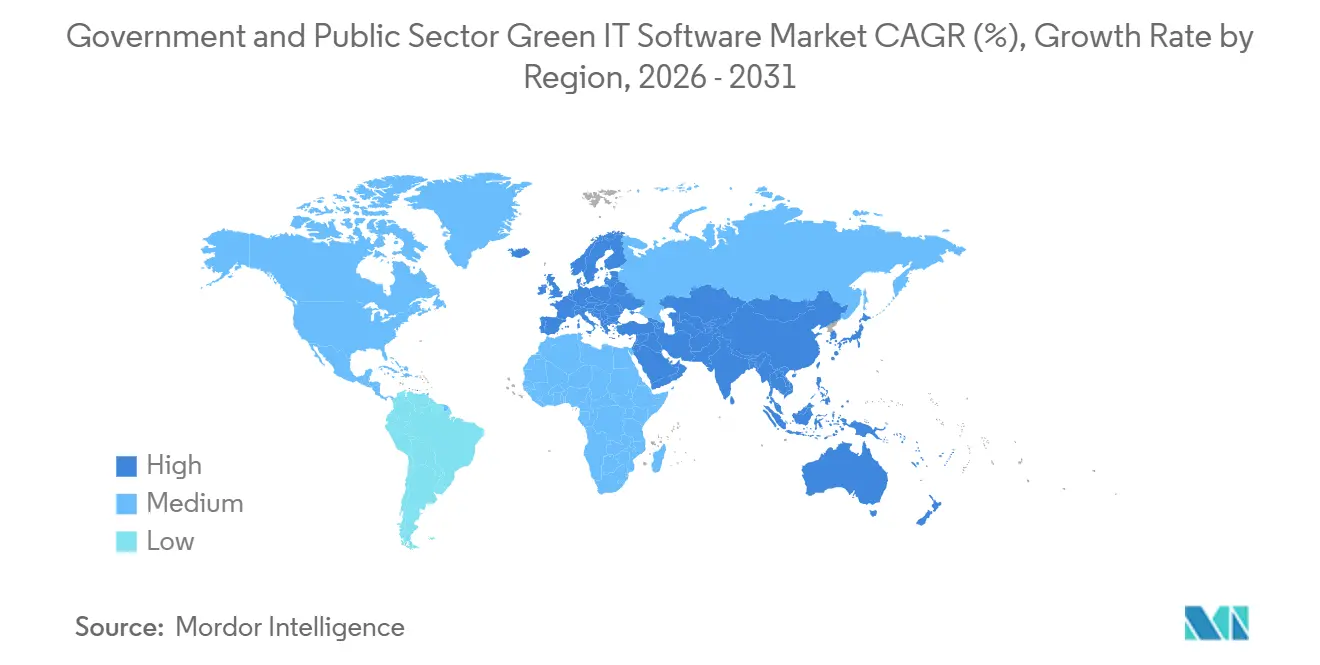

- By geography, Europe led with 34.56% of revenue in 2025, while Asia-Pacific is projected to expand at 18.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Government and Public Sector Green IT Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Public Sector Net-Zero Procurement Requirements | +4.2% | EU core, spill-over to North America, APAC, and Middle East and Africa | Short term (≤ 2 years) |

| Government Digital Modernization Mandates | +3.5% | Global, concentrated gains in North America, EU, and APAC | Short term (≤ 2 years) |

| Rising Utility and Data Center Energy Cost Pressure | +2.8% | Global, highest intensity in North America and Western Europe | Medium term (2-4 years) |

| Shift Toward Sustainability Reporting Automation in Agencies | +2.6% | Global, with early adoption gains in EU and APAC | Medium term (2-4 years) |

| Legacy IT Carbon Visibility Gaps Across Public Institutions | +2.0% | North America, EU, and advanced APAC markets | Medium term (2-4 years) |

| Demand for Audit-Ready Carbon Data in Grant-Funded Programs | +1.5% | North America, EU, South America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Public Sector Net-Zero Procurement Requirements Reshape Contract Standards

Public procurement rules are pushing the government and public sector green IT software market away from voluntary reporting and toward contract-bound emissions documentation. The United Kingdom applied PPN 006 to major government contracts advertised from February 24, 2025, and the rule requires suppliers on contracts above GBP 5 million (USD 6.59 million) to submit carbon reduction plans as a condition of participation. That requirement changes software demand because agencies need systems that can collect, retain, and present supplier and operational emissions data in a form procurement teams can verify. It also brings together procurement, legal, finance, and sustainability teams on a single workflow, underscoring the value of centralized reporting and audit trails in the government and public sector green IT software market. Vendors that already fit formal public buying processes therefore gain an access advantage that can matter as much as feature depth when agencies evaluate bids.[1]UK Government, “PPN 006: Taking Account of Carbon Reduction Plans in the Procurement of Major Government Contracts,” UK Government, gov.uk

Government Digital Modernization Mandates Accelerate Platform Consolidation

Digital modernization programs are widening the budgetary path for the government and public sector green IT software markets, as sustainability requirements are being built into broader technology renewal agendas. The United Kingdom's Defra Digital Sustainability Strategy 2025-2030 set a target to reduce IT carbon emissions by 16% by 2030 and required digital service suppliers with an annual contract value above GBP 1 million (USD 1.32 million) to hold externally verified carbon footprints and net-zero plans. The same strategy stated that Defra group IT operations generated 10,000 tonnes of CO2 equivalent in 2024, equal to 13% of the department's total emissions, which shows why software-backed tracking is moving closer to core IT governance. In the United States, the GSA's OneGov agreement with SAP in December 2025 offered federal agencies discounts of up to 80% across database, integration, analytics, and cloud tools, with projected savings of USD 165 million. These moves favor vendors that already sit within approved procurement and enterprise technology stacks, which support platform consolidation across the government and public-sector green IT software markets.[2]UK Government, “Defra Digital Sustainability Strategy 2025 to 2030,” UK Government, gov.uk

Rising Data Center Energy Costs Shift the Software ROI Case

Energy and infrastructure costs are changing the buying logic in the government and public sector green IT software market, as agencies can now tie sustainability software to operating savings rather than just compliance. Defra's digital sustainability plan set a target to keep power usage effectiveness at no higher than 1.3 across operated data centers, providing agencies with a clear technical benchmark for energy management tools. In February 2026, the UAE Ministry of Energy and Infrastructure, Khazna Data Centers, and Agility announced a pilot deployment of Phaidra's AI-driven energy management technology across government data centers to improve cooling efficiency. That kind of deployment supports the case for software that integrates emissions control, facility performance, and cost discipline within a single operating environment. As agencies face tighter budgets, solutions that demonstrate both carbon visibility and efficiency gains are likely to gain faster approval in the government and public-sector green IT software markets.[3]Khazna Data Centers, “UAE Ministry of Energy and Infrastructure, Khazna, and Agility Announce Pilot to Implement Phaidra AI,” Khazna Data Centers, khaznadatacenters.com

Sustainability Reporting Automation Replaces Spreadsheet Workflows

Reporting automation is becoming increasingly important in the government and public sector green IT software market, as agencies increasingly need connected data that can flow from suppliers and operations into formal disclosures without manual rework. In May 2026, EcoVadis and Workiva announced a partnership that linked primary supplier carbon data directly into audit-ready sustainability reporting workflows, which shows how procurement and reporting are being connected in a more structured way. In March 2026, NTT Group released a cradle-to-grave lifecycle CO2 calculation standard for software, aligned with Japan's Ministry of Economy, Trade and Industry carbon footprint guidance, which adds a more formal basis for software-related emissions accounting. Together, these moves show that agencies and vendors are building workflows around standardized data models instead of isolated spreadsheets and one-off templates. Vendors that can reuse a single data set across supplier review, internal accounting, and disclosure tasks are therefore better positioned as documentation demands expand in the government and public-sector green IT software market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Legacy Procurement and Budget Cycles | -1.8% | Global, most acute in North America and EU member states with decentralized procurement | Short term (≤ 2 years) |

| Data Sovereignty and Public Cloud Approval Constraints | -1.4% | EU, Asia-Pacific, and Middle East and Africa with strict data localization rules | Medium term (2-4 years) |

| Long Software Validation and Change-Management Timelines | -1.2% | North America and EU where government IT approval cycles are longest | Medium term (2-4 years) |

| Limited Internal ESG and Carbon Accounting Skill Depth | -0.9% | Global, most acute in smaller municipalities and developing-market public agencies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Budget and Procurement Cycles Slow Discretionary Uptake

Annual budgeting structures continue to slow the government and public sector green IT software market, as sustainability tools often compete with higher-priority IT projects within the same funding cycle. In many agencies, cybersecurity, workforce systems, and legacy modernization still rank ahead of carbon management platforms in appropriations reviews, which delays rollouts even when mandates are clear. The GSA's OneGov agreement with SAP lowered entry costs through deep discounts and projected USD 165 million in savings, but the arrangement also showed that short-term procurement windows can shape adoption timing and renewal risk. The same challenge arises at the subnational level, where city, county, and state budget calendars often do not align with national reporting expectations so that the policy requirement can arrive before the budget authority. Vendors that offer phased deployment, pilot scopes, and modular pricing are better suited to move through this constraint in the government and public sector green IT software market.

Data Sovereignty Requirements Create Competing Architecture Demands

Data sovereignty rules are slowing down parts of the government and public sector green IT software market because agencies are being asked to decarbonize their digital operations while maintaining tighter control over where public data resides. The European Commission's Sovereign Cloud Framework made environmental sustainability one of 8 scored criteria, but it also required that data sovereignty conditions be satisfied before public workloads move into compliant cloud environments. France's Interministerial Digital Directorate told ministries in April 2026 to formalize plans to reduce extra-European digital dependencies by autumn 2026, which shows how strongly localization concerns are shaping public technology choices. These conditions push many agencies toward hybrid models and longer validation cycles instead of direct migration to broad public cloud deployments. Vendors with sovereign-ready, government-authorized, or locally controlled architecture, therefore, gain a durable access advantage across the government and public-sector green IT software markets.[4]European Commission, “Sovereign Cloud Framework Explained,” European Commission, commission.europa.eu

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Carbon Accounting Leads While Procurement Intelligence Gains Speed

Carbon accounting and reporting software held 28.74% of the government and public sector green IT software market share in 2025, which made it the largest solution type at the start of the forecast period. That lead reflects the practical order of agency work, because public bodies first need a measured and auditable emissions baseline before they can set reduction targets, compare suppliers, or defend grant-linked disclosures. The category also benefits from how government buyers evaluate systems, since audit traceability and structured records matter as much as user features as compliance obligations expand. SAP's May 2026 announcement that its carbon accounting offering was recognized again in the IDC MarketScape reinforces the appeal of ERP-native architectures that align emissions records more closely with financial control practices.

Energy and power management software is gaining traction alongside the leading category, as agencies now face a stronger need to tie sustainability actions to operating efficiency and data center performance targets. Green procurement and supplier sustainability software is projected to expand at 18.12% CAGR through 2031, the fastest pace within the solution mix. EcoVadis and Workiva's May 2026 partnership shows why this category is moving quickly: supplier carbon data is being linked more directly into audit-ready reporting rather than staying in separate procurement systems. Sustainability data management platforms are also becoming increasingly important because agencies need a single environment to bring together accounting, procurement, and operational information without the need for repeated manual consolidation.

By Deployment: Cloud Remains Dominant While Hybrid Adoption Builds Through Compliance Needs

Cloud deployment accounted for 65.41% of revenue in 2025, which kept it well ahead of other deployment models in the government and public sector green IT software market. Agencies favor the cloud where possible because subscription delivery can shorten time to compliance and shift rule updates, maintenance, and release management toward the vendor. That matters in public settings, where internal IT teams often face limited capacity and need software that can stay current without extensive reconfiguration. Cloud also fits the wider pattern of government modernization programs that use negotiated procurement channels and approved platforms to accelerate adoption.

Hybrid deployment is projected to grow at 17.95% CAGR during 2026-2031, making it the fastest-rising model as buyers balance compliance speed with control over sensitive data. The European Commission's Sovereign Cloud Framework and France's 2026 directive on reducing extra-European dependencies both support this middle path by raising the bar for where and how public-sector data can be stored and processed. On-premises deployment, therefore, remains relevant for defense, national security, and agencies with strict operational data rules, even if it no longer sets the pace of growth. Vendors that can move data cleanly between local environments and compliant cloud layers are likely to capture a larger share of the government and public sector green IT software market as sovereignty requirements remain in place.

By End User: Federal Demand Leads While Education and Healthcare Expand Faster

Central and federal government agencies commanded 30.12% of spending in 2025, which made them the largest end-user group in the government and public sector green IT software market. Their lead reflects direct exposure to national net-zero commitments, formal oversight, and larger procurement budgets than most other public entities. These agencies also tend to run more complex estates, which increases the need for systems that can connect carbon accounting, procurement records, and audit documentation under one governance structure. Public-sector modernization programs in the United Kingdom and United States further reinforce this pattern by linking sustainability expectations with large-scale public procurement channels and core IT renewal.

Public education and public healthcare institutions are projected to grow at 18.25% CAGR through 2031, which places them ahead of other end-user groups on expansion pace. That rise reflects a tighter need for audit-ready environmental records in institutions that manage large facilities, broad supplier networks, and public funding oversight. Public utilities and related agencies form another important demand pool because energy and infrastructure operations create a clearer cost-saving case for monitoring and optimization software. Across end users, vendors with simple implementation, tiered product depth, and limited setup burden are better placed to reach smaller public bodies that do not have enterprise-scale internal sustainability teams.

By Application: Compliance Automation Anchors Spend While Supplier Tracking Drives New Demand

Compliance, audit, and ESG workflow automation accounted for 29.63% of the government and public sector green IT software market in 2025, making it the leading application area. Agencies usually direct their first software budgets toward meeting existing disclosure and review requirements before expanding into broader optimization and supplier intelligence use cases. The category stays important because the same records often need to serve internal review, external reporting, and grant or procurement evidence requests without conflicting versions. That provides workflow automation with durable value in the government and public sector green IT software market, especially where documentation quality is closely examined.

Public procurement and supplier emissions tracking are projected to expand at 18.34% CAGR through 2031, the fastest growth among applications. NTT Group's March 2026 lifecycle CO2 calculation standard for software shows that procurement-related emissions records are becoming more formal and detailed, especially when software assets themselves are subject to carbon review. EcoVadis and Workiva's connected workflow adds another signal, because supplier-level carbon data is now moving straight into reporting environments built for audit and disclosure. As agencies extend accountability from their own operations into supplier networks, application categories that connect contracts, vendors, and disclosures are likely to hold stronger renewal value over time in the government and public sector green IT software market.

Geography Analysis

Europe accounted for a 34.56% share of the government and public sector green IT software market in 2025, maintaining its lead among regional markets. The region's position is supported by a dense policy landscape in which environmental compliance, procurement controls, and digital governance are advancing together rather than as separate agendas. The European Commission's Sovereign Cloud Framework made environmental sustainability one of the scored dimensions for public cloud procurement while also keeping sovereignty assurance central to adoption decisions. The United Kingdom added further momentum through public procurement and digital sustainability rules that place formal expectations on suppliers and departmental IT operations. As a result, Europe combines broad compliance pressure with procurement systems that can channel spending toward vendors already prepared for public-sector review.

North America was the second-largest regional market for government and public sector green IT software in 2025. In the United States, adoption is being shaped heavily by centralized procurement vehicles, which give large software vendors a faster route into federal estates than one-by-one agency sales. The GSA's OneGov agreement with SAP showed how federal bodies can scale access to analytics, integration, and cloud capabilities through negotiated discounts and common procurement terms. This structure supports volume deployment but also leaves room for specialist tools that provide deeper supplier, asset, or disclosure functionality alongside the main platform.

Asia-Pacific is projected to expand at a 18.45% CAGR during 2026-2031, making it the fastest-growing regional segment in the government and public sector green IT software market. The region is moving from policy planning to implementation, which is broadening demand for carbon accounting, lifecycle tracking, and procurement-oriented reporting tools. NTT Group's March 2026 release of a lifecycle CO2 calculation standard for software reflects a more formal treatment of software-related emissions in advanced Asia-Pacific markets. South America, the Middle East, and Africa are smaller bases today, yet the UAE pilot announced with Khazna, Agility, and the Ministry of Energy and Infrastructure shows that government energy management deployments are moving into active execution outside the two largest regions. This means future expansion outside Europe and North America is likely to begin with targeted public projects and then widen as agencies build internal capacity and procurement familiarity.

Competitive Landscape

The government and public sector green IT software market is moderately concentrated, with enterprise software vendors holding the strongest positions where procurement access and system integration matter most. Competition is less focused on price and more on platform breadth, regulatory coverage, and the ability to integrate with existing ERP, IT service management, and reporting estates. Large vendors such as SAP, ServiceNow, IBM, Microsoft, and Workiva benefit from installed relationships, while specialists such as Sphera, Cority, Dakota Software, Enablon, and Wolters Kluwer retain focused positions in compliance-heavy workflows. The balance of the government and public sector green IT software market, therefore, still reflects both scale advantages and niche expertise rather than winner-take-all concentration.

SAP strengthened its government position when the U.S. GSA signed a OneGov agreement in December 2025 that offered federal agencies up to 80% discounts across major software categories and projected USD 165 million in savings. That move mattered because it turned procurement access into a strategic edge before technical comparison even began across many federal buying processes. EcoVadis and Workiva then expanded the competitive focus in May 2026 by linking supplier carbon records with audit-ready sustainability reporting workflows. Makersite added another signal in June 2026 when it acquired Siemens's SiGREEN platform, strengthening its product carbon footprint and Scope 3 capabilities around supplier data exchange. These actions show that competition in the government and public sector green IT software market is increasingly moving toward connected data networks and broader procurement reach, rather than stand-alone reporting features.

AI-supported automation and supplier data connectivity are becoming key differentiators as agencies seek fewer manual steps and higher documentation quality across complex review chains. SAP's continued push around Green Ledger also supports the view that vendors are trying to tie emissions records more directly to financial-grade control structures rather than treating sustainability data as an isolated reporting layer. The next major opening remains below the federal tier, where state, county, and municipal agencies still present a wide field for vendors that can offer lighter implementation and lower administrative burden. Honeywell and Johnson Controls also remain relevant adjacency players because facility energy management and IT sustainability workflows are converging in public environments. Overall, the government and public sector green IT software market should remain competitively mixed, with large platforms winning where procurement and integration dominate, and specialists holding ground where depth in disclosure, supplier data, or operational emissions is harder to replace.

Government and Public Sector Green IT Software Industry Leaders

SAP SE

Microsoft Corporation

IBM Corporation

Schneider Electric SE

ServiceNow, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Makersite announced the acquisition of SiGREEN, Siemens AG's product carbon footprint and supply chain data exchange platform, effective June 1, 2026. The deal strengthens Makersite's Scope 3 supplier emissions tracking capabilities and removes a standalone product carbon footprint module from Siemens's portfolio, directly reshaping competition for supply-chain decarbonization tools used in government procurement workflows.

- May 2026: EcoVadis and Workiva Inc. announced a strategic partnership to connect EcoVadis's primary supplier carbon data directly into Workiva's audit-ready sustainability reporting platform. The integration targets mutual customers' Scope 3 report accuracy and addresses the gap between industry-average emissions estimates and verified supplier-level data, a requirement now embedded in multiple government procurement frameworks.

- May 2026: SAP SE was named a Leader in the IDC MarketScape, Worldwide Carbon Accounting and Management Applications 2026 Vendor Assessment, for the second consecutive time. The recognition cited SAP Green Ledger's ERP-native double-entry carbon accounting architecture and its integration with SAP Business Technology Platform for government-grade audit traceability, capabilities directly aligned with public-sector procurement criteria.

- April 2026: The European Commission awarded a contract to 4 providers for sovereign cloud services covering all EU institutions, bodies, offices, and agencies. The Sovereign Cloud Framework applied to this procurement explicitly scores environmental sustainability as 1 of 8 criteria dimensions, creating a landmark procurement reference for green IT software expectations in EU public-sector technology buying.

Global Government and Public Sector Green IT Software Market Report Scope

The Government and Public Sector Green IT Software market comprises platforms and services that enable public institutions to manage, monitor, and optimize IT operations, with a focus on sustainability, energy efficiency, and carbon reduction. These solutions provide functionalities such as carbon accounting and disclosure, energy and workload optimization, IT asset lifecycle management, sustainability data integration, and green procurement with supplier emissions tracking. They also support compliance, audit, and ESG workflow automation tailored to government and public sector requirements.

The Government and Public Sector Green IT Software market report is segmented by Offering (Software [Carbon Accounting and Reporting Software, Energy and Power Management Software, IT Asset Lifecycle Management Software, Sustainability Data Management Platforms, Green Procurement and Supplier Sustainability Software], and Services), Deployment (Cloud, On-Premises, and Hybrid), End User (Central and Federal Government, State and Local Government, Public Utilities and Public Agencies, Public Education and Public Healthcare Institutions), Application (Carbon Data Collection and Disclosure, Energy Optimization and Workload Scheduling, IT Asset Utilization and Lifecycle Optimization, Public Procurement and Supplier Emissions Tracking, Compliance, Audit, and ESG Workflow Automation), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Carbon Accounting and Reporting Software |

| Energy and Power Management Software |

| IT Asset Lifecycle Management Software |

| Sustainability Data Management Platforms |

| Green Procurement and Supplier Sustainability Software |

| Cloud |

| On-Premises |

| Hybrid |

| Central and Federal Government |

| State and Local Government |

| Public Utilities and Public Agencies |

| Public Education and Public Healthcare Institutions |

| Carbon Data Collection and Disclosure |

| Energy Optimization and Workload Scheduling |

| IT Asset Utilization and Lifecycle Optimization |

| Public Procurement and Supplier Emissions Tracking |

| Compliance, Audit, and ESG Workflow Automation |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Solution Type | Carbon Accounting and Reporting Software | ||

| Energy and Power Management Software | |||

| IT Asset Lifecycle Management Software | |||

| Sustainability Data Management Platforms | |||

| Green Procurement and Supplier Sustainability Software | |||

| By Deployment | Cloud | ||

| On-Premises | |||

| Hybrid | |||

| By End User | Central and Federal Government | ||

| State and Local Government | |||

| Public Utilities and Public Agencies | |||

| Public Education and Public Healthcare Institutions | |||

| By Application | Carbon Data Collection and Disclosure | ||

| Energy Optimization and Workload Scheduling | |||

| IT Asset Utilization and Lifecycle Optimization | |||

| Public Procurement and Supplier Emissions Tracking | |||

| Compliance, Audit, and ESG Workflow Automation | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the size of the government and public sector green IT software market?

The government and public sector green IT software market size is projected to increase from USD 1.83 billion in 2025 to USD 2.12 billion in 2026 and reach USD 4.71 billion by 2031, at a CAGR of 17.31%.

Which solution category leads spending in green IT software for government agencies?

Carbon accounting and reporting software led with 28.74% of revenue in 2025 because agencies need an auditable emissions baseline before they expand into broader sustainability workflows.

Which deployment model is growing fastest in public-sector green IT software?

Hybrid deployment is projected to grow at 17.95% CAGR through 2031 as agencies try to balance cloud flexibility with sovereignty and localization requirements.

Why are procurement rules becoming so important for public-sector sustainability software?

Procurement rules now increasingly require carbon data, supplier transparency, and audit-ready records, which turns sustainability capability into a formal buying requirement instead of an optional feature.

Which region is expanding fastest for government green IT software adoption?

Asia-Pacific is projected to grow at 18.45% CAGR through 2031, making it the fastest-growing regional segment in the government and public sector green IT software market.

What application area is driving the next wave of demand?

Public procurement and supplier emissions tracking is projected to expand at 18.34% CAGR through 2031 as agencies extend accountability from their own operations into supplier networks and Scope 3 workflows.

Page last updated on: