Europe Green IT Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

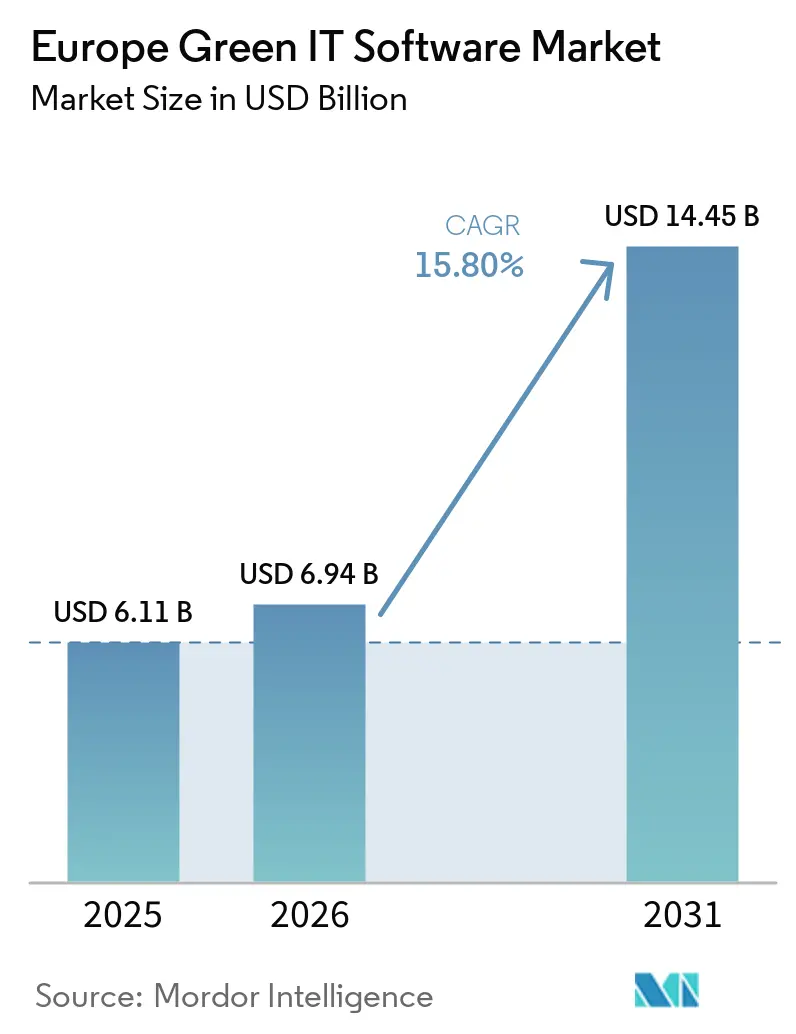

| Base Year Market Size (2025) | USD 6.11 Billion |

| Market Size (2026) | USD 6.94 Billion |

| Market Size (2031) | USD 14.45 Billion |

| Growth Rate (2026 - 2031) | 15.80% CAGR |

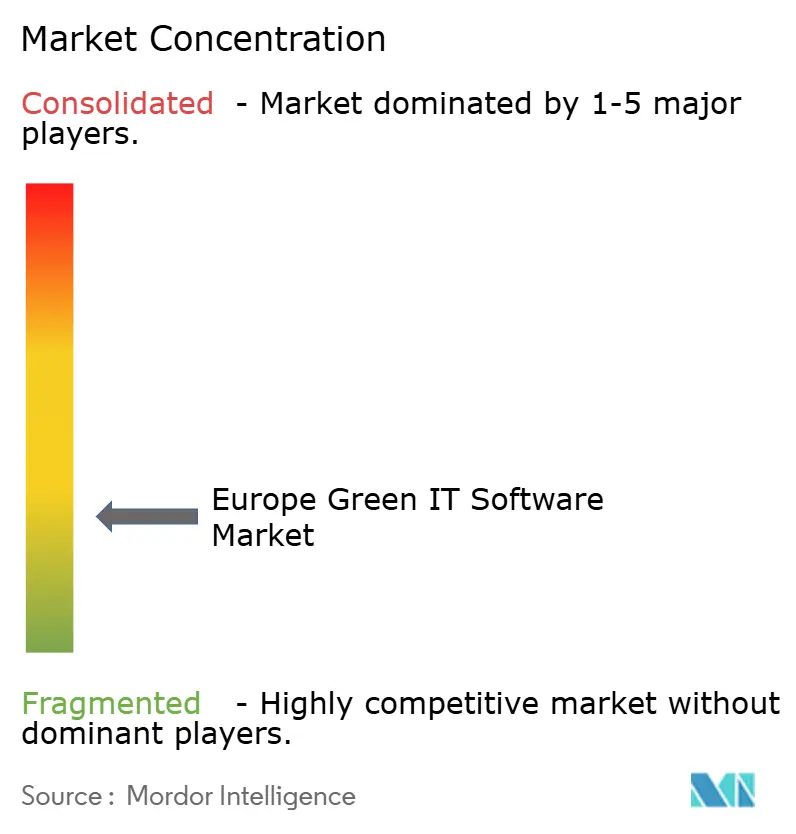

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Green IT Software Market Analysis by Mordor Intelligence

The Europe green IT software market size is projected to be USD 6.11 billion in 2025, USD 6.94 billion in 2026, and reach USD 14.45 billion by 2031, growing at a CAGR of 15.80% from 2026 to 2031. Growth in the Europe green IT software market is being shaped by the shift of sustainability disclosure from voluntary reporting into auditable enterprise compliance, which is pushing large organizations toward software that can manage entity-level data, reporting controls, and cross-framework workflows in one system. The March 2026 recalibration of reporting thresholds narrowed the pool of mandatory adopters, but it also concentrated spending among larger companies with more complex operations, stronger audit needs, and wider supplier networks, which supports higher-value deployments instead of low-touch compliance tools. Demand is also moving beyond disclosure into emissions management, energy optimization, and decarbonization planning as buyers look for platforms that can support decision-making after the first reporting cycle. AI-enabled automation is improving the speed of data collection and reconciliation, but buyers are still testing how far automation can go when disclosures must stand up to assurance reviews and regulator scrutiny. Competition is therefore developing around European regulatory depth, installed enterprise software relationships, data residency controls, and the ability to support both compliance and operational carbon reduction inside the same platform.

Key Report Takeaways

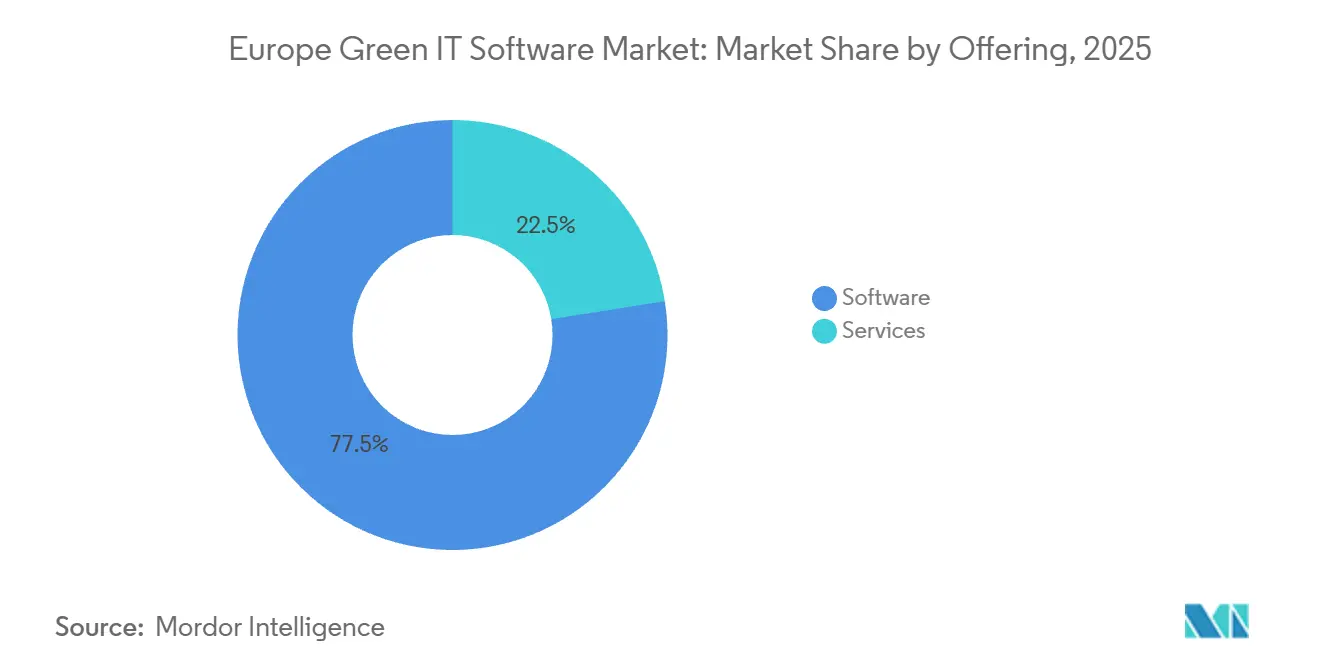

- By offering, software led with a 77.52% revenue share in 2025, while services are projected to expand at an 18.24% CAGR through 2031.

- By deployment mode, cloud held a 66.84% revenue share in 2025, while hybrid is projected to record the highest growth at a 19.18% CAGR between 2026 and 2031.

- By organization size, large enterprises accounted for 72.18% of revenue in 2025, while SMEs are projected to expand at a 17.95% CAGR through 2031.

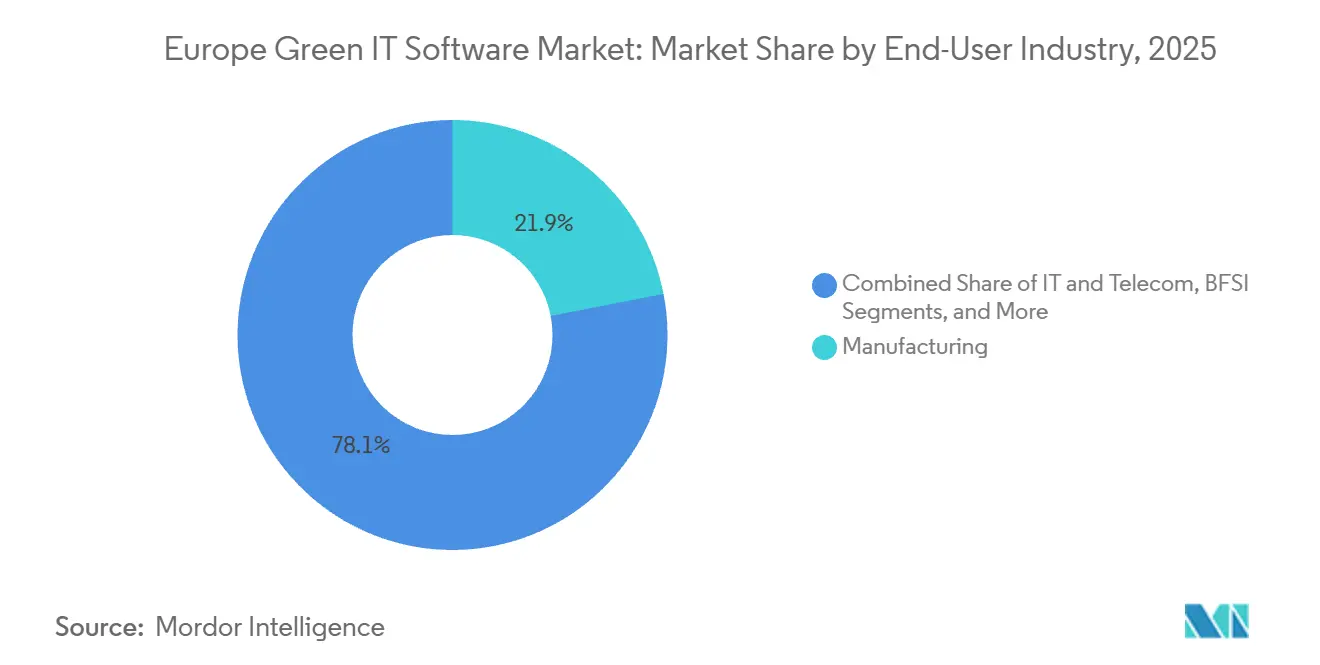

- By end-user industry, manufacturing held a 21.94% of the Europe green IT software market share in 2025, while healthcare is projected to advance at a 19.84% CAGR between 2026 and 2031.

- By solution type, ESG reporting and compliance software accounted for a 29.86% share in 2025, while decarbonization planning software is projected to grow at a 21.37% CAGR through 2031.

- By geography, Germany held 22.73% of the Europe green IT software market share in 2025, while Spain is projected to expand at an 18.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Green IT Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU Corporate Sustainability Reporting Directive Compliance Pressure | +3.8% | EU-wide, led by Germany, France, and the Nordics | Short term (≤ 2 years) |

| Rise in Audit-Ready Scope 1, 2, and 3 Reporting Workflows | +3.2% | EU-wide, with concentration in manufacturing and BFSI sectors | Medium term (2-4 years) |

| Expansion of Energy Optimization Use Cases in Data Centers and Digital Workplaces | +2.5% | Western Europe, led by the Nordics and Germany | Medium term (2-4 years) |

| AI-Enabled Automation of ESG Data Collection and Reconciliation | +2.1% | Europe-wide, early gains in the UK and Germany | Medium term (2-4 years) |

| Procurement Demand for Measurable Software Carbon Savings | +1.6% | Western Europe, with spillover to Nordics and Benelux | Medium term (2-4 years) |

| Cybersecurity and Data Residency Needs Favoring Enterprise-Grade Platforms | +1.0% | EU-wide, led by Germany, France, and Benelux | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Corporate Sustainability Reporting Directive Compliance Pressure

The CSRD remains the single largest structural catalyst for the Europe green IT software market because it turns sustainability reporting into a formal and reviewable enterprise obligation for large organizations across the region. ESMA reported 367 examinations of sustainability statements under CSRD and NFRD content review in 2025, and those reviews led to enforcement actions against 109 issuers, which showed that regulators were already acting during the first reporting cycle rather than allowing a long grace period.[1]European Securities and Markets Authority, “Report on 2025 Corporate Reporting Enforcement and Regulatory Activities,” ESMA, esma.europa.euThat enforcement posture matters for software demand because it pushes buyers toward systems with stronger controls, better audit trails, and clearer governance over entity-level disclosures and underlying source data. The 2026 threshold revision reduced the number of companies directly in scope, but it shifted mandatory spending toward larger enterprises whose multi-country structures and wider supplier bases usually require deeper deployments and broader implementation work. ESRS reporting also requires a level of structured information that is difficult to manage through spreadsheets once companies need consistency across subsidiaries, disclosure topics, and assurance processes, which keeps platform demand firm even when thresholds move. In practice, this driver gives the Europe green IT software market a compliance floor that is harder to reverse than a normal discretionary software budget cycle.

Rise In Audit-Ready Scope 1, 2, and 3 Reporting Workflows

Demand for audit-ready emissions workflows is rising because large companies need software that can move from raw operational inputs to disclosure-ready greenhouse gas reporting across Scope 1, Scope 2, and Scope 3 in a traceable format. Scope 3 has become the most difficult layer because enterprise buyers often need primary data from very large supplier and partner networks rather than simple averages or one-time estimates. EcoVadis and Watershed partnered in March 2026 to connect supplier-grade carbon information with enterprise reporting workflows, which showed how vendor strategy is moving toward shared data infrastructure rather than isolated carbon accounting tools. EcoVadis and Workiva extended that model in May 2026 by linking Carbon Data Network outputs into reporting workflows so customers could move toward more granular and audit-ready Scope 3 calculations.[2]EcoVadis, “EcoVadis Continues Expansion of Carbon Data Network With Workiva,” EcoVadis Resources, resources.ecovadis.comThese moves matter for the Europe green IT software market because they raise buyer expectations around interoperability, supplier engagement, and evidence quality rather than simple dashboard reporting. They also support the services layer because complex manufacturers, retailers, and financial groups still need ongoing help to collect, validate, and map supplier data into usable reporting structures.

Expansion of Energy Optimization Use Cases in Data Centers and Digital Workplaces

Data centers are becoming a larger demand center inside the European green IT software market because reporting obligations are now tied more directly to the energy performance of digital infrastructure. The European Commission published its first broad assessment of data center energy performance in July 2025 using 2024 reporting data, and that step moved energy efficiency from a technical facility issue into a structured compliance and disclosure topic. The same policy direction includes work on an EU-wide rating scheme and minimum performance standards, which suggests a longer runway for software that can monitor, optimize, and document energy use in data-heavy environments. This opportunity is widening as AI workloads raise power density and cooling complexity, which increases the value of software that can schedule workloads, manage resources, and reduce wasted energy inside digital operations. The SEANERGYS project under the EuroHPC Joint Undertaking further signals public support for AI-driven and scheduling-based energy optimization in advanced computing environments. As a result, the Europe green IT software market is expanding beyond reporting and into operating software that affects energy intensity, utilization patterns, and infrastructure efficiency in real time.

AI-Enabled Automation of ESG Data Collection and Reconciliation

AI-enabled automation is changing buying behavior in the Europe green IT software market because buyers now expect faster data collection, stronger reconciliation, and less manual processing across ESG workflows. Watershed launched purpose-built AI agents for ESG workflows in April 2026 and reported up to 93% lower data processing time, together with an average 80% reduction in time to actionable sustainability data across more than 100 customer collaborations. SAP also announced in May 2026 that its Sustainability Regulatory Readiness Agent within SAP Sustainability Control Tower could cut scenario simulation time from around 1 day to 20 minutes for CSRD materiality mapping, with general availability targeted by the end of 2026. These tools matter because they push the software category toward workflow automation and decision support rather than static data collection alone. Large enterprises are likely to benefit first because they already have deeper process maturity, larger data estates, and stronger budgets for integrating AI into reporting and planning systems. Smaller firms still face a slower adoption path, but the widening efficiency gap suggests that AI capability will become a practical differentiator for vendors that want to scale across the region.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Reporting Standards Across Jurisdictions and Frameworks | -1.8% | EU-wide, with additional divergence in the UK and Norway | Short term (≤ 2 years) |

| High Integration Burden With Legacy ERP, Cloud, and Data Stack Environments | -1.5% | EU-wide, with concentration in mid-market manufacturing and retail | Medium term (2-4 years) |

| Limited Internal Sustainability Analytics Skills in Mid-Market Firms | -0.9% | EU-wide, concentrated in Spain, Italy, and Central-Eastern Europe | Medium term (2-4 years) |

| Buyer Fatigue From Overlapping ESG, Carbon, and Energy Software Categories | -0.7% | EU-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Reporting Standards Across Jurisdictions and Frameworks

Fragmentation remains a real brake on adoption because multinational buyers still operate across multiple sustainability frameworks, disclosure expectations, and verification practices simultaneously. ESMA’s April 2026 compliance table showed that 5 of 30 EU and EEA national competent authorities declared non-compliance with the enforcement guidelines, while Germany and Spain were still listed as intending to comply, which means the supervisory baseline is not fully uniform across Europe. That uneven posture forces cross-border companies to maintain parallel reporting configurations and governance checks, especially when internal groups span several legal entities and reporting jurisdictions. The UK’s separate path around sustainability disclosure standards adds another layer for companies that must align EU reporting with non-EU requirements inside the same technology stack. This increases product development pressure for vendors because cross-framework mapping, terminology alignment, and disclosure logic must keep changing as standards evolve. It also makes buyers more cautious because a platform that works well in one reporting environment may still require extra configuration, services, or manual controls in another.

High Integration Burden with Legacy ERP, Cloud, and Data Stack Environments

Integration burden slows many deployments because sustainability software rarely works as a standalone layer and instead depends on data flowing from finance, operations, procurement, energy systems, supplier records, and legacy enterprise applications. The challenge is more severe when organizations have separate tools for carbon accounting, energy management, supply chain due diligence, and ESG reporting, since each tool often uses different schemas, identifiers, and refresh cycles. In the Europe green IT software market, that complexity keeps many mid-sized buyers tied to spreadsheets or phased rollouts even when the compliance case is already clear. Hybrid architectures can add another layer of work because data residency, privacy, and local hosting preferences often require custom connections between cloud workflows and locally controlled data environments. Vendors, therefore, need strong implementation and mapping capabilities, not just feature depth, if they want to convert interest into live deployments. The result is a slower near-term sales cycle, a larger role for services, and a higher risk that buyers postpone full rollouts until data ownership and integration responsibilities are clearer.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain Ground In A Software-Led Revenue Base

Software held 77.52% of revenue in 2025, which shows that recurring platform subscriptions remained the main commercial model in the Europe green IT software market. That position reflects the need for centralized systems that can manage reporting workflows, document controls, data lineage, and ongoing updates across several entities and use cases. The software layer is also where vendors build stickiness because customers depend on configuration, integrations, templates, dashboards, and audit-ready records that become harder to replace once reporting cycles are underway. In practical terms, the largest share stayed with platforms that could serve as the operational system of record for ESG reporting, carbon accounting, and sustainability data management rather than as one-time disclosure tools. This kept the revenue base anchored in licensing and subscriptions even as the scope of use widened across reporting, planning, and operational monitoring.

Services are projected to expand at an 18.24% CAGR between 2026 and 2031, which means the support layer is growing faster than the core platform layer inside the Europe green IT software market. Implementation work rises when buyers move from a basic reporting setup into double-materiality assessments, entity mapping, supplier onboarding, and control testing under formal governance requirements. Services also become more important when customers need support for assurance readiness, process design, and data collection across internal systems that were never built for sustainability reporting. This is why a software-led category still creates substantial room for integrators, managed data services, advisory teams, and specialist implementation partners. The balance of growth suggests that buyers are no longer only purchasing tools, but are also purchasing execution capacity that helps them make those tools usable inside real reporting calendars and operating structures.

By Deployment Mode: Cloud Leads While Hybrid Expands Fastest

Cloud deployment held 66.84% of revenue in 2025, which gave it the largest position in the Europe green IT software market size across deployment models. That share reflects the speed and scalability of SaaS delivery, especially when buyers must meet repeated reporting deadlines and coordinate users across business units and legal entities. Cloud platforms are also better placed for continuous updates, framework changes, supplier collaboration features, and AI-based workflow improvements that vendors now push into their products more frequently. For many organizations, this model shortened initial deployment time and reduced the burden of maintaining separate local installations across multiple sites. These factors kept Cloud as the default commercial and technical choice for much of the regional installed base.

Hybrid deployment is projected to grow at a 19.18% CAGR between 2026 and 2031, which makes it the fastest-moving setup even though cloud remained larger in absolute share. Growth is being supported by buyers who want cloud flexibility for analytics and workflow orchestration, but still prefer local or regional control over sensitive operational and reporting data. On-premises systems, therefore, remain relevant in regulated settings such as government, defense, and financial services, where internal policies can still restrict fully cloud-based handling of ESG-related records. ESG-X has positioned its architecture around EU-based and certified German data center infrastructure, which shows how data residency and governance are turning into visible buying criteria rather than background IT preferences.[3]ESG-X GmbH, “The Central ESG Software for CSRD, VSME, Carbon Accounting, and Double Materiality Analysis,” ESG-X, esg-x.com This shift gives hybrid models a stronger role in the Europe green IT software industry because the next phase of deployments will often depend on how well vendors can combine scale, privacy controls, and audit defensibility in one operating model.

By Organization Size: Large Enterprises Hold the Base as SMEs Move Up

Large enterprises accounted for 72.18% of revenue in 2025, giving them the largest role in the Europe green IT software market share by organization size. This outcome aligns with the first wave of formal reporting obligations, which focused on larger companies with broader disclosure duties, more subsidiaries, and more complex data needs. Large companies also tend to have wider supplier networks, more energy-intensive operations, and stronger internal audit requirements, which makes dedicated software more justifiable than manual or semi-manual approaches. Their early spending created the installed base that currently anchors platform revenue across the region. It also helped shape product direction because vendors first optimized for multi-entity governance, large user groups, and enterprise-grade reporting controls.

SMEs are projected to grow at a 17.95% CAGR through 2031, which points to a widening second wave of demand rather than a sudden shift away from large-enterprise dominance. Much of that demand is coming from supply chain pressure, since smaller companies are increasingly asked to provide primary emissions data and sustainability records to larger customers that must complete formal Scope 3 disclosures. The voluntary sustainability reporting standard for SMEs gives a more standardized entry point, which helps vendors build lighter products and simpler onboarding paths for this part of the market. This matters for the Europe green IT software industry because future growth will depend on how well vendors reduce friction for organizations that lack large internal sustainability teams or advanced data engineering capacity. The segment is therefore expanding less because SMEs suddenly mirror enterprise behavior, and more because reporting obligations are spreading through procurement relationships and supplier reporting requests.

By End-User Industry: Manufacturing Leads and Healthcare Climbs Quickly

Manufacturing held the largest end-user share at 21.94% in 2025, which positioned it at the center of Europe green IT software market size by industry use. The sector’s exposure to direct emissions, supply chain transparency demands, and reporting obligations makes carbon accounting and sustainability software part of core operating control rather than a side reporting task. Manufacturers also need broader data coverage because emissions and energy information often sit across plants, suppliers, logistics systems, procurement records, and product-level workflows. That complexity supports demand for platforms that can combine reporting with planning, operational monitoring, and supplier engagement. As a result, manufacturing remained the most established buying group across the regional demand base.

Healthcare is projected to record a 19.84% CAGR between 2026 and 2031, which makes it the fastest-growing end-user vertical in the Europe green IT software market. Large hospitals and healthcare organizations are facing stronger pressure to organize emissions reporting across buildings, procurement, travel, waste, and clinical support functions under formal governance expectations. Asklepios implemented a CSRD-specific software solution in 2025 to manage Scope 1, Scope 2, and Scope 3 emissions across its hospital network, which shows how the sector is embedding sustainability processes into broader operating and administrative systems. The sector’s procurement culture also gives sustainability data more weight, which makes software adoption relevant for both compliance and vendor evaluation. Healthcare, therefore, stands out not because it already has the largest installed base, but because its operational footprint and governance needs are creating a faster pace of platform adoption.

By Solution Type: Reporting Holds the Lead While Decarbonization Planning Surges

ESG reporting and compliance software held a 29.86% share in 2025, making it the largest solution layer inside the Europe green IT software market size by solution type. That leadership was expected because the first wave of spending centered on disclosure readiness, structured reporting workflows, and the need to turn sustainability information into a controlled enterprise process. Buyers initially prioritized systems that could gather data, document methodologies, support reviews, and produce reporting outputs that were easier to defend under scrutiny. This kept reporting and compliance software ahead of other categories during the first cycle of mandatory implementation. It also reinforced the link between regulatory change and near-term purchasing behavior across the region.

Decarbonization planning software is projected to grow at a 21.37% CAGR through 2031, which makes it the fastest-rising category in the Europe green IT software market. This shift suggests that organizations that completed early reporting work are now moving toward tools that model reduction pathways, assess tradeoffs, and link emissions targets to operational decisions. Normative introduced AI-powered Product Carbon Footprint software built to ISO 14067 specification, which points to rising demand for product-level carbon intelligence rather than company-level reporting alone. That direction matters because product-level data is becoming more relevant for supply chain transparency, customer disclosure needs, and future digital product information requirements. The result is a broader software mix in which compliance remains the entry point, but planning and product-level decarbonization are becoming the next high-growth layers.

Geography Analysis

Germany accounted for 22.73% of revenue in 2025, which gave it the leading position in the Europe green IT software market share by geography. Its lead reflects the overlap between EU disclosure obligations and Germany’s national supply chain due diligence environment, which creates a more demanding compliance setting than most peer markets. The country’s industrial base also increases implementation complexity, as automotive, chemical, and machinery sectors require broad coverage across direct operations and supplier networks. This pushes buyers toward multi-entity and enterprise-grade platforms that can handle both reporting depth and operational data integration. Germany also remains important because it attracts sophisticated buyers and several well-known regional vendors, reinforcing its position as the main anchor market.

The Nordics represent a smaller but more mature demand cluster inside the Europe green IT software market because many organizations in the region had already built stronger sustainability data practices before formal CSRD pressure intensified. That prior maturity helped create a local software ecosystem around carbon accounting and decarbonization, with Sweden standing out through vendors such as Normative and Position Green. The United Kingdom follows a different regulatory path, and that divergence creates demand for software that can support more than one reporting logic inside multinational groups rather than only EU-centered workflows. France also remains important because it has a developed ESG software base and large multinationals that often need supplier sustainability capabilities alongside core reporting functions. Spain, meanwhile, is projected to grow at an 18.91% CAGR between 2026 and 2031, which gives it the fastest expansion outlook among the named geographies.

Spain’s growth is supported by a compressed adoption cycle, together with public backing for AI-based sustainable digital technology through the Plan Nacional de Algoritmos Verdes.[4]Spanish Government, “Programa Nacional de Algoritmos Verdes,” Government of Spain, algoritmosverdes.gob.es Italy adds another steady demand layer because its manufacturing and infrastructure footprint creates a clear use case for structured emissions and sustainability software. The Rest of Europe group, which includes Central and Eastern EU members outside the named countries, broadens the addressable base as common obligations spread across the EU, even where local enforcement capacity is still developing. Russia remains structurally limited within the commercial opportunity because it does not participate in CSRD and because the wider geopolitical setting has constrained normal software relationships with European providers.

Competitive Landscape

The Europe green IT software market remains fragmented, but it is gradually consolidating around two broad competitive groups. One group consists of global enterprise software providers such as SAP, IBM, Salesforce, and Schneider Electric, which can embed sustainability capabilities into larger ERP, analytics, and energy management environments. The second group consists of European specialists such as Sweep, Plan A, Normative, Greenly, and osapiens, which compete more directly on regulatory depth, regional focus, and carbon accounting specialization. This split matters because buyers are not choosing only between products, but also between ecosystem integration and sustainability-specific functionality. The current structure leaves room for both types because enterprise incumbents bring installed relationships, while specialists often move faster on new reporting and decarbonization requirements.

A visible strategic pattern is the shift from standalone tools toward networked data models and automated workflows. EcoVadis expanded its Carbon Data Network through partnerships with Watershed in March 2026 and Workiva in May 2026, which strengthened the flow of primary supplier emissions data into enterprise reporting environments. SAP took a different route by adding sustainability AI agents inside its broader enterprise software stack, which supports faster materiality mapping and workflow automation for customers already operating in SAP environments. OSAPIENS raised USD 100 million in January 2026 and reached a valuation above USD 1.1 billion, which showed continuing investor confidence in large-account European compliance and sustainability platforms. These moves suggest that scale, data connectivity, and workflow automation are becoming as important as feature breadth in the Europe green IT software market.

White space remains strongest in the mid-market and among firms that sit outside the first wave of formal thresholds but still face reporting pressure through customer and supply chain relationships. Buyer hesitation also persists where companies worry that AI-generated outputs may move faster than internal assurance and governance teams are willing to accept. ESMA’s uneven enforcement alignment across jurisdictions keeps local regulatory interpretation important, which supports vendors that can combine product capability with country-level implementation support. Overall, no single company appears dominant enough in the input to define the category alone, so competition remains active across platform breadth, regional credibility, and the ability to convert compliance projects into longer-term carbon management relationships.

Europe Green IT Software Industry Leaders

SAP SE

IBM Corporation

Schneider Electric SE

Salesforce, Inc.

Workiva Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SAP announced new sustainability AI agents, including the Sustainability Regulatory Readiness Agent and Footprint Optimization Agent, at SAP Sapphire 2026, currently in beta with general availability planned by the end of 2026. Beta performance metrics include scenario simulation time reduced from approximately one day to 20 minutes and a greater than 50% reduction in packaging compliance review hours.

- May 2026: EcoVadis and Workiva announced a strategic partnership to connect EcoVadis' primary supplier carbon data from its Carbon Data Network directly into Workiva's AI-powered reporting platform, enabling mutual customers to advance from industry-average emission estimates to granular, audit-ready Scope 3 calculations suitable for ESRS disclosure.

- May 2026: UK-based Greenpixie closed a GBP 4.7 million (USD 5.97 million) pre-Series A round led by VERBUND X Ventures, the corporate venture arm of one of Europe's largest renewable electricity producers, to expand its FinOps and GreenOps software for Fortune 1000 firms targeting carbon and water reduction in cloud and AI infrastructure.

- April 2026: Watershed launched AI agents for ESG data management, reducing data processing time by up to 93% and average time to actionable sustainability data by 80%, developed with more than 100 enterprise customers, including Royal Mail and Smiths Group.

Europe Green IT Software Market Report Scope

The Europe Green IT software market encompasses software solutions and associated services designed to improve the environmental sustainability of IT operations while supporting regulatory compliance and corporate sustainability objectives. These solutions assist organizations in measuring greenhouse gas emissions, managing sustainability data, automating ESG disclosures, optimizing energy consumption, and planning decarbonization strategies across digital infrastructure, cloud environments, and enterprise technology ecosystems.

The Europe Green IT Software Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and SMEs), End-User Industry (IT and Telecom, BFSI, Manufacturing, Energy and Utilities, Retail and E-Commerce, Government, Healthcare, Construction and Infrastructure, and Other End-user Industries), Solution Type (Carbon Management and Accounting Software, ESG Reporting and Compliance Software, Sustainability Data Management Platforms, Decarbonization Planning Software, and Energy and Resource Optimization Software), and Geography (United Kingdom, Germany, France, Italy, Spain, Russia, Nordics, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| SMEs |

| IT and Telecom |

| BFSI |

| Manufacturing |

| Energy and Utilities |

| Retail and E-Commerce |

| Government |

| Healthcare |

| Construction and Infrastructure |

| Other End-User Industries |

| Carbon Management and Accounting Software |

| ESG Reporting and Compliance Software |

| Sustainability Data Management Platforms |

| Decarbonization Planning Software |

| Energy and Resource Optimization Software |

| United Kingdom |

| Germany |

| France |

| Italy |

| Spain |

| Russia |

| Nordics |

| Rest of Europe |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| SMEs | |

| By End-User Industry | IT and Telecom |

| BFSI | |

| Manufacturing | |

| Energy and Utilities | |

| Retail and E-Commerce | |

| Government | |

| Healthcare | |

| Construction and Infrastructure | |

| Other End-User Industries | |

| By Solution Type | Carbon Management and Accounting Software |

| ESG Reporting and Compliance Software | |

| Sustainability Data Management Platforms | |

| Decarbonization Planning Software | |

| Energy and Resource Optimization Software | |

| By Geography | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Nordics | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current and projected size of the Europe green IT software space?

The Europe green IT software market size stood at USD 6.11 Billion in 2025, reached USD 6.94 Billion in 2026, and is projected to reach USD 14.45 Billion by 2031 at a 15.80% CAGR.

What is driving adoption across Europe the most?

The strongest driver is the move from voluntary ESG activity to auditable reporting under EU sustainability rules, which has raised demand for software with stronger controls, data lineage, and multi-entity reporting workflows.

Which deployment model is expanding the fastest in Europe?

Cloud remained the largest model with a 66.84% share in 2025, while hybrid is projected to grow the fastest at a 19.18% CAGR through 2031 as buyers balance flexibility with data residency and governance needs.

Which customer group is creating the largest revenue base?

Large enterprises held 72.18% of revenue in 2025 because they were the first group facing the deepest reporting obligations and usually needed broader integrations across finance, operations, and supply chains.

Which end-user segment is growing the fastest?

Healthcare is projected to grow at a 19.84% CAGR through 2031, supported by rising reporting needs across large hospitals and health organizations and by the growing need to manage emissions across complex operating networks.

Which software category is seeing the fastest growth after reporting tools?

Decarbonization planning software is projected to grow at a 21.37% CAGR through 2031, showing that buyers are moving beyond disclosure into pathway modeling, product-level carbon tracking, and operational reduction planning.

Page last updated on: