United Kingdom Green IT Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

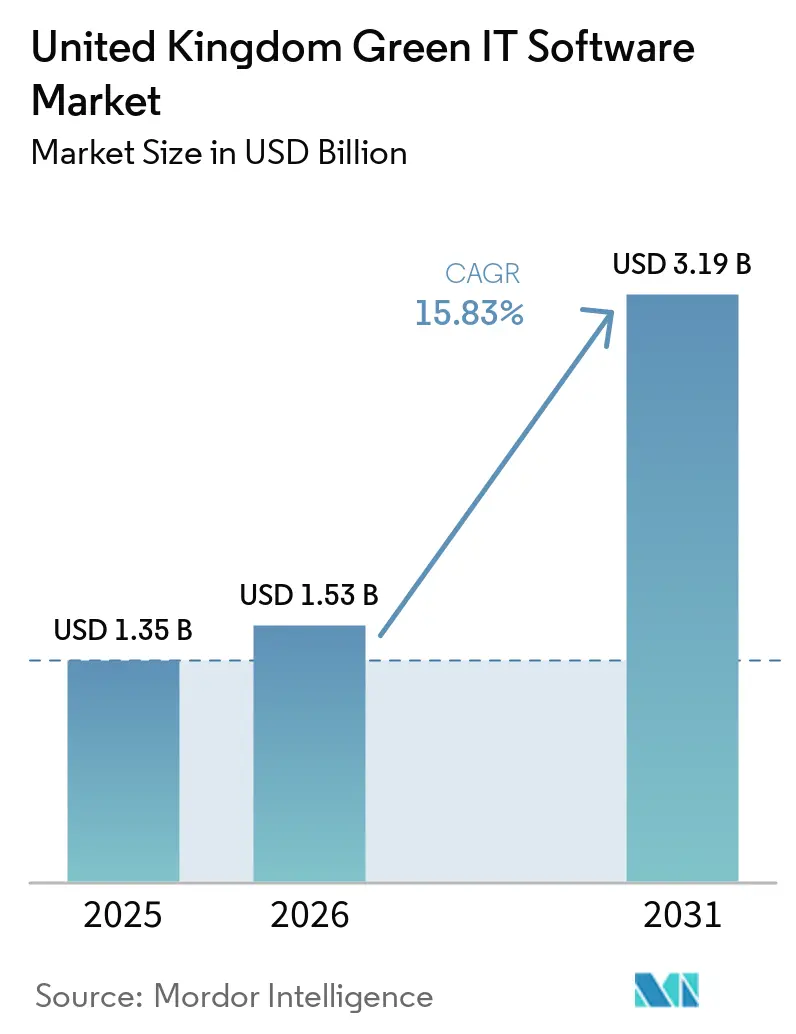

| Base Year Market Size (2025) | USD 1.35 Billion |

| Market Size (2026) | USD 1.53 Billion |

| Market Size (2031) | USD 3.19 Billion |

| Growth Rate (2026 - 2031) | 15.83% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Green IT Software Market Analysis by Mordor Intelligence

The United Kingdom green IT software market size was valued at USD 1.35 billion in 2025 and estimated to grow from USD 1.53 billion in 2026 to reach USD 3.19 billion by 2031, at a CAGR of 15.83% during the forecast period 2026-2031. The United Kingdom green IT software market is moving into a more urgent buying cycle because climate disclosure is shifting from a voluntary reporting exercise to a board-level compliance task. New UK sustainability reporting rules, stronger financed emissions expectations, and broader demand for audit-ready data are pushing software purchases into core risk and finance budgets rather than leaving them inside stand-alone sustainability teams. Enterprise buyers are also moving away from spreadsheet-led reporting because multi-framework disclosure now needs governed data, workflow controls, and easier access across finance, procurement, and operations teams. Cloud delivery is widening adoption because it supports faster rollout, simpler integration, and more practical collaboration across distributed business units and supplier networks. Competitive pressure is rising as large enterprise software vendors expand sustainability features inside existing platforms, while specialist vendors defend their positions with carbon accounting depth, financed emissions tools, and AI-led workflow automation.

Key Report Takeaways

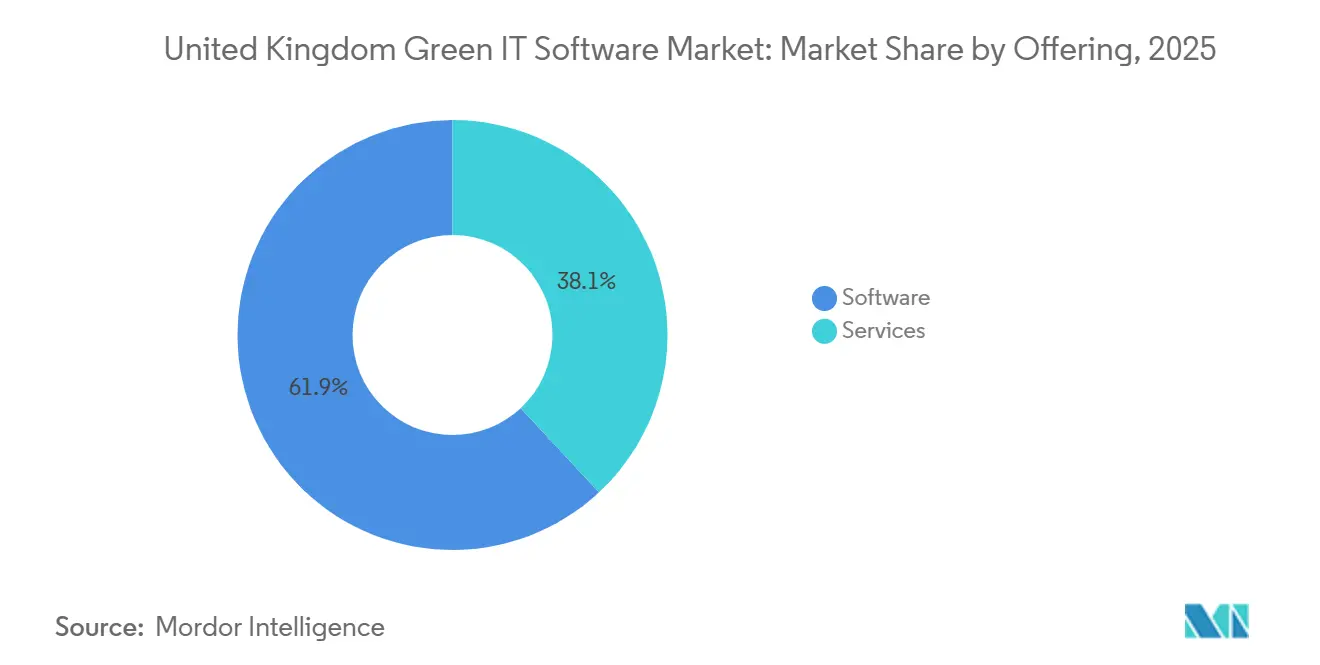

- By offering, software held 61.94% of the United Kingdom green IT software market in 2025, while services are projected to expand at a 17.26% CAGR through 2031.

- By deployment mode, cloud-based deployment accounted for 68.41% of the United Kingdom green IT software market size in 2025 and is projected to advance at an 18.67% CAGR through 2031.

- By solution type, carbon management and accounting software led with a 36.23% share in 2025, while sustainability data management platforms are projected to expand at a 21.77% CAGR through 2031.

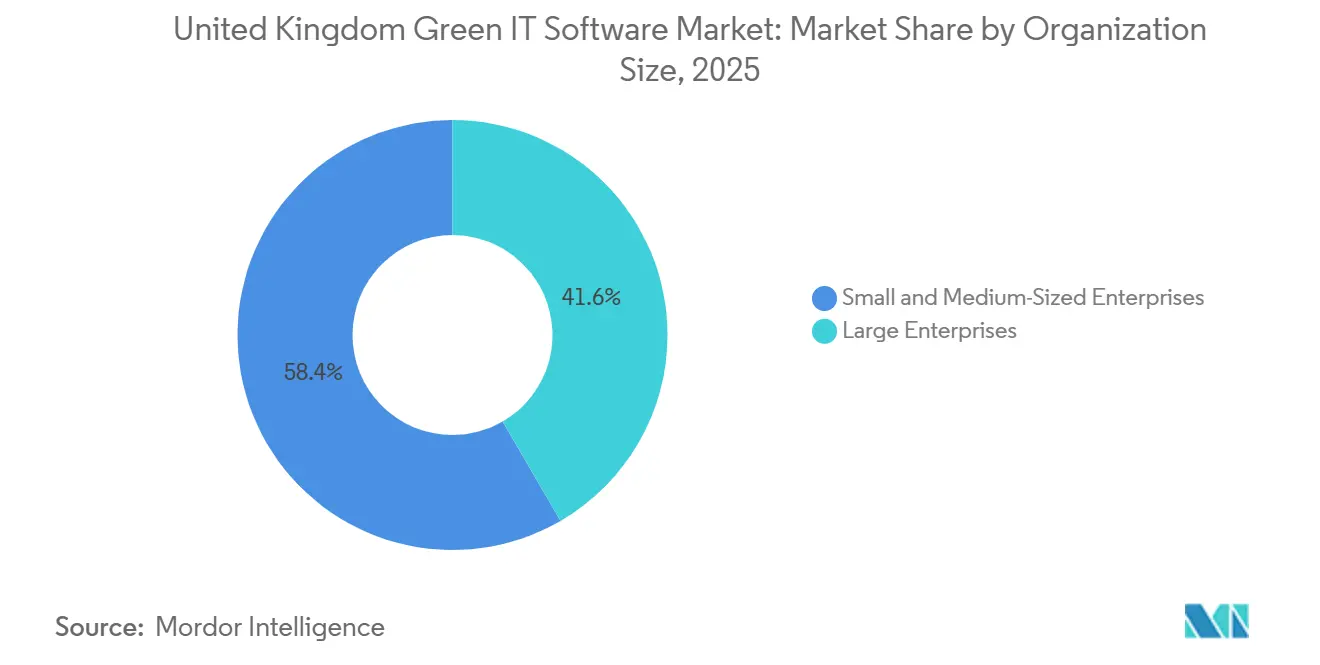

- By organization size, large enterprises captured 41.62% of the market in 2025, while SMEs are projected to grow at a 19.79% CAGR through 2031.

- By end user industry, BFSI held 31.62% of the United Kingdom green IT software market share in 2025, while the same segment is projected to record the highest CAGR at 21.19% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Green IT Software Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Mandatory ESG And Carbon Disclosure Compliance | +4.2% | United Kingdom-wide, concentrated impact in listed companies and FCA-regulated financial institutions | Short term (≤ 2 years) |

| Rising Enterprise Demand for Audit-Ready Emissions Data | +3.1% | United Kingdom-wide, strongest in large-cap corporates and FTSE-listed entities | Short term (≤ 2 years) |

| Cloud Migration of Sustainability Workflows | +2.8% | United Kingdom-wide, strongest in London financial hub and large enterprise IT centers | Medium term (2-4 years) |

| AI-Enabled Automation of Carbon Accounting Workloads | +2.4% | Global applicability, early adoption concentrated in United Kingdom technology and professional services sectors | Medium term (2-4 years) |

| Procurement Preference for Measurable Decarbonization Tools | +1.9% | United Kingdom-wide, spillover to SME supply chains nationwide | Medium term (2-4 years) |

| Tighter Scope 3 Visibility Requirements Across Supply Chains | +1.6% | United Kingdom-wide, highest impact in manufacturing and retail supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mandatory ESG and Carbon Disclosure Compliance

Mandatory disclosure is the strongest structural force behind growth in the United Kingdom green IT software market. The Department for Business and Trade published UK SRS S1 and UK SRS S2 on February 25, 2026, which moved UK reporting closer to the ISSB baseline and raised the need for controlled and audit-ready sustainability data. The FCA consultation paper CP26/5, issued in January 2026, proposed mandatory UK SRS S2 climate disclosures for listed issuers from accounting periods beginning on or after January 1, 2027, which gave enterprises a clear preparation window and turned software selection into a near-term compliance task.[1]Financial Conduct Authority, “CP26/5, Aligning Listed Issuers' Sustainability Disclosures With International Standards,” Financial Conduct Authority, fca.org.uk The United Kingdom green IT software market is also being lifted by the SECR baseline, because many companies already run documented greenhouse gas reporting processes and can now migrate those workflows into more structured platforms. The anti-greenwashing rule that has applied to all FCA-authorized firms since May 2024 adds another layer of pressure because firms need defensible data trails rather than narrative claims alone. This is why procurement in the United Kingdom green IT software market is increasingly tied to legal review, board oversight, and reporting timetables rather than to discretionary sustainability budgets.

Rising Enterprise Demand for Audit-Ready Emissions Data

The United Kingdom green IT software market is also benefiting from a clear shift toward assurance-compatible emissions reporting. Companies now need data that can stand up to scrutiny from auditors, investors, regulators, and internal finance teams at the same time. That change matters because climate reporting now extends beyond high-level narrative disclosure and reaches into source systems, calculation methods, governance logs, and supplier data collection. The transition from TCFD-based reporting toward the broader UK SRS framework widens the reporting surface, so enterprises need software that can manage climate, risk, and sustainability-related information in one controlled environment. The United Kingdom green IT software market, therefore, favors vendors that can support governed workflows, review steps, and evidence trails, because these features reduce the risk of reporting gaps late in the disclosure cycle. As a result, the market is gradually shifting away from stand-alone tools that measure emissions only and toward platforms that combine calculation, governance, and reporting functions.

Cloud Migration of Sustainability Workflows

Cloud adoption is reinforcing the expansion of the United Kingdom green IT software market because sustainability reporting now depends on broader access, easier integration, and faster system updates. Multi-framework reporting is difficult to manage in isolated on-premises tools because users across finance, operations, procurement, and sustainability teams need the same current data view. Defra’s Digital Sustainability Strategy for 2025-2030 supported this direction by promoting digital architectures where compute resources can scale more efficiently, which gave cloud-first sustainability infrastructure added policy support. Cloud delivery also fits the practical needs of the United Kingdom green IT software market because it is easier to connect APIs, supplier inputs, and shared workflows when organizations operate across many sites and business units. The change is not only technical, because cloud deployment is also being linked to supplier engagement, workflow speed, and easier collaboration with external assurance providers. That combination makes cloud adoption one of the clearest operating enablers for growth in the United Kingdom green IT software market.

AI-Enabled Automation of Carbon Accounting Workloads

AI is changing how work gets done inside the United Kingdom green IT software market because it reduces the amount of manual effort needed to prepare, classify, and review sustainability data. SAP announced in May 2026 that new sustainability AI agents would become generally available by the end of 2026, including tools that can cut manual compliance effort by up to 80% in selected workflows. IFS also launched IFS Zero in May 2026 as a unified emissions operating system for asset-intensive industries, which shows that AI-enabled sustainability management is spreading beyond reporting tools alone.[2]IFS, “IFS Launches IFS Zero,” IFS, ifs.com In the United Kingdom green IT software market, this matters because reporting teams are under time pressure, supplier data is inconsistent, and boards increasingly want faster visibility into both compliance status and decarbonization options. AI tools help vendors move from simple recordkeeping toward workflow orchestration, data cleaning, classification support, and scenario-led decision support. That shift raises the competitive standard in the United Kingdom green IT software market because buyers now expect speed and usability improvements, not just better emissions calculations.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented Enterprise Data Architectures | -1.8% | United Kingdom-wide, most acute in large multi-site enterprises and diversified conglomerates | Short term (≤ 2 years) |

| High Integration Effort With Legacy ERP and ESG Systems | -1.5% | United Kingdom-wide, concentrated in manufacturing, energy, and utilities sectors with aging IT infrastructure | Medium term (2-4 years) |

| Limited In-House Sustainability Analytics Skills in Mid-Market Firms | -0.9% | United Kingdom-wide, strongest constraint in regional and mid-market companies outside London | Medium term (2-4 years) |

| Budget Scrutiny for Non-Core Software Spending | -0.7% | United Kingdom-wide, disproportionately affecting SMEs and public sector entities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Enterprise Data Architectures

Fragmented internal data remains a major constraint on the United Kingdom green IT software market. Sustainability information often sits across finance systems, procurement tools, utility records, plant data sources, and supplier spreadsheets that were never designed to work together. When enterprises cannot create a reliable data layer, they also struggle to justify platform investment because the business case depends on the same visibility that is currently missing. The problem becomes more difficult when Scope 3 reporting expands, because outside suppliers add non-standard formats, uneven response quality, and different levels of reporting maturity. This slows implementation in the United Kingdom green IT software market and raises the importance of vendors that can combine software with advisory support. It also favors larger platform providers that can present a single-vendor consolidation path across multiple reporting workflows.

High Integration Effort With Legacy ERP and ESG Systems

Legacy system integration is another clear barrier in the United Kingdom green IT software market, especially in manufacturing, energy, utilities, and other sectors that operate aging enterprise infrastructure. A 2025 peer-reviewed study linked to Aston University found that integration with legacy databases often delayed emissions tracking rollouts by two or more quarters, which shows how often technical connection work becomes the real deployment bottleneck. SAP’s approach of embedding Green Ledger into S/4HANA addresses that problem for customers already inside its ecosystem, but it does not remove the challenge for organizations using other core systems. For the rest of the market, the cost is broader than software licensing because it includes API work, governance redesign, user training, and continuing maintenance. The British Business Bank also pointed to limited tailored support and uneven reporting requirements for SMEs, which suggests that simpler deployment models will matter even more as smaller buyers enter the United Kingdom green IT software market. As a result, integration simplicity is becoming a practical competitive factor rather than a secondary technical feature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Led Spending While Services Scaled Faster

Software held a 61.94% share of the United Kingdom green IT software market in 2025, which made it the dominant offering type during the present platform build-out phase. That lead reflected early enterprise spending patterns, because companies first prioritized carbon accounting, ESG reporting, and data management systems before building larger advisory and managed support layers. Buyers across the United Kingdom green IT software market needed tools that could replace spreadsheet-led reporting and support formal disclosure cycles, so licensing and configuration spending took the largest share first. This also matched the current maturity stage of the green IT software industry, where many buyers are still creating a structured data foundation rather than optimizing mature sustainability programs. The software category, therefore, benefited from immediate compliance pressure, a growing need for workflow controls, and a stronger push to centralize emissions and reporting activity.

Services are projected to grow at a 17.26% CAGR through 2031, which makes them the faster-scaling offering within the United Kingdom green IT software market. That pattern reflects a widening skills gap, because many companies can purchase software faster than they can build internal capacity to configure and operate it at audit-ready standards. The services mix is also shifting from one-time deployment work toward recurring support, including implementation consulting, managed reporting, carbon advisory, and audit assistance. This is especially important for mid-market buyers that need workable sustainability systems but do not have dedicated internal teams. Specialist vendors such as Normative AB are using software-plus-service models to match this need, which is helping services capture more value as software adoption broadens. Over time, services are likely to remain closely tied to software expansion in the United Kingdom green IT software market because regulatory updates and Scope 3 complexity create ongoing operational work after the first installation is complete.

By Deployment Mode: Cloud Consolidated Leadership Across Workflows

Cloud-based deployment commanded 68.41% of the market in 2025 and represented 68.41% of the United Kingdom green IT software market size, which confirmed its lead over hybrid and on-premises models. This position reflected enterprise demand for scalable systems that can support multi-site reporting, API connections, and frequent disclosure updates without heavy internal infrastructure work. The United Kingdom green IT software market has favored cloud deployment because reporting requirements are widening, and more users need secure access across finance, sustainability, procurement, and operations teams. Cloud platforms also make it easier to support supplier collaboration, centralized control, and faster system updates, which are increasingly necessary as reporting extends to Scope 3 and broader sustainability themes. As a result, cloud is not only a hosting option in the United Kingdom green IT software market, but also a practical operating model for faster, more coordinated reporting.

Cloud is also the fastest-growing deployment mode, with an expected CAGR of 18.67% through 2031. That dual lead on both size and growth suggests that migration is still in progress and that meaningful on-premises and hybrid workloads remain available for future conversion. On-premises tools remain relevant in some financial services and government settings where control and residency concerns have mattered, even though these constraints are easing over time. Hybrid models continue to work as transition architectures for organizations that need local handling of asset-heavy operational data while shifting reporting and analytics to the cloud. Defra’s digital sustainability strategy further supported cloud-centered approaches that use resources more efficiently, which strengthens the policy backdrop for this transition.[3]Department for Environment, Food and Rural Affairs, “Defra Digital Sustainability Strategy 2025 to 2030,” GOV.UK, gov.uk This means deployment decisions in the United Kingdom green IT software market are becoming closely tied to governance, collaboration speed, and the ability to scale future compliance demands.

By Solution Type: Data Management Became the Strategic Battleground

Carbon management and accounting software led the solution landscape with a 36.23% share in 2025, which shows where the first wave of buying concentrated. The category benefited from the statutory baseline already created by SECR, because many companies had to produce greenhouse gas inventories before newer reporting frameworks widened the disclosure task. For the United Kingdom green IT software market, that made carbon accounting the natural first purchase and the entry point into broader sustainability software adoption. Enterprises needed a system of record for emissions calculations before they could move into wider reporting, planning, and optimization functions. This leadership position therefore reflected the early maturity stage of the United Kingdom green IT software market rather than a permanent limit on where future value will sit.

Sustainability data management platforms are projected to grow at a 21.77% CAGR through 2031, which makes them the fastest-growing solution type. That rise points to a more advanced buyer need, because companies now see that point solutions cannot easily support UK SRS, CSRD, CDP, and TCFD requirements at the same time. A governed and centralized data layer is becoming more valuable because reporting now covers energy use, supply chain emissions, financial exposure, and governance inputs that need to connect across teams. ESG reporting and compliance software remains a major demand area because it turns raw data into framework-aligned outputs, while decarbonization planning and energy and resource optimization tools support the next stage of action after compliance baselines are built. The United Kingdom green IT software market is therefore shifting from isolated calculation tools toward more connected platforms that link measurement, governance, reporting, and planning in one environment. This is one of the clearest signs that the green IT software industry in the UK is moving from early adoption toward operational integration.

By Organization Size: Large Enterprises Led While SMEs Accelerated

Large enterprises captured 41.62% of the United Kingdom green IT software market in 2025, which reflected their earlier exposure to SECR, TCFD, CDP, and other reporting expectations. Their larger supplier bases, stronger internal reporting functions, and direct regulatory exposure made them the first major software buyers in this space. In the United Kingdom green IT software market, large organizations also had stronger budgets for platform integration, advisory support, and assurance-ready controls, which helped them move sooner than smaller firms. They effectively set the first standards for software functionality, governance depth, and vendor credibility. This early lead explains why large enterprises still anchor current revenue even as adoption broadens across the wider business base.

SMEs are projected to expand at a 19.79% CAGR through 2031, which makes them the fastest-growing organization size group. Their growth is being driven less by direct regulation and more by downstream pressure from large customers that need better supplier emissions data for Scope 3 reporting. That dynamic matters because many SMEs had limited prior exposure to formal sustainability reporting, yet they now need practical tools that can help them answer buyer requests without building large in-house teams. The British Business Bank highlighted financial limits, uneven support, and inconsistent reporting requirements as continuing obstacles, which means affordability and ease of use will shape success in this part of the market. The Aston University-linked research also pointed to gaps in digital maturity and integrated data infrastructure among SMEs, which raises the value of simple templates and pre-configured workflows. The United Kingdom green IT software market is therefore widening beyond large enterprises, but the winning products for SMEs will need to reduce complexity rather than just replicate enterprise-grade depth.

By End User Industry: BFSI Led on Both Scale and Growth

BFSI held 31.62% of the United Kingdom green IT software market share in 2025, which made it the largest end user industry. It is also expected to record the fastest CAGR at 21.19% through 2031, which gives it the rare position of leading on both current size and future growth. This reflects the unusually high reporting burden carried by financial institutions, which must address both operational emissions and financed emissions across portfolios. In the United Kingdom green IT software market, BFSI buyers need portfolio-level calculations, financed emissions methods, and scenario-ready analytics that general reporting tools cannot always provide without added configuration. That need has made financial services one of the most demanding and strategically important customer groups for platform vendors.

The FCA’s sustainability disclosure rules for asset managers, life insurers, and FCA-regulated pension providers increased the urgency of climate and sustainability reporting across financial institutions. SAP Fioneer’s ESG KPI Engine reflects this demand because it automates financed emissions calculations across loans and investments and aligns with PCAF and CSRD expectations.[4]SAP Fioneer, “Stay Audit-Ready With the ESG KPI Engine,” SAP Fioneer, sapfioneer.com Other sectors, such as IT and telecommunications, manufacturing, healthcare, retail and e-commerce, government and public sector, energy and utilities, and construction and infrastructure, continue to provide a broad demand base for the United Kingdom green IT software market. Each sector brings a different sustainability data challenge, from plant and energy intensity measurement to public procurement reporting and healthcare supply chain emissions tracking. That diversity reduces overdependence on a single customer group, even though BFSI remains the clearest driver of high-value use cases. The United Kingdom green IT software market is therefore led by financial services, but its long-run growth still rests on a wide spread of sector-specific adoption paths.

Geography Analysis

London and the South East lead the United Kingdom Green IT Software market, driven by a high concentration of listed companies, FCA-regulated financial institutions, and multinational headquarters. These organizations face early and complex disclosure requirements. The region benefits from a strong presence of technology firms, professional service providers, and systems integrators, which not only use these platforms for their reporting needs but also support client implementations. Businesses in this area are progressing from initial platform adoption to more advanced usage, transitioning from standalone carbon tools to integrated sustainability data management systems.

The Midlands and Northern England are emerging as the fastest-growing regions in the United Kingdom Green IT Software market. This growth is primarily fueled by Scope 3 reporting pressures cascading from large corporate buyers into manufacturing, logistics, and industrial supply chains. Key sectors driving this growth include the automotive industry in the West Midlands, steel production in South Yorkshire, textiles in Lancashire, and the industrial zone in the Humber, all of which face increasing supplier data requirements. Public initiatives, such as the Made Smarter East Midlands program, are further accelerating this growth. Launched in December 2025, the program provides energy efficiency grants ranging from GBP 15,000 to GBP 50,000 (USD 19,833 to USD 66,111) per facility for manufacturers. Additionally, cities like Manchester, Birmingham, Leeds, and Sheffield are experiencing a rise in digital services, enhancing software readiness among firms that previously relied on spreadsheets.

Scotland stands out due to significant budget allocations for its Net Zero and Energy programs, including offshore wind supply chain development. From 2026 onward, Scotland implemented a new budgeted carbon framework, increasing the relevance of reporting for public entities, health boards, and industrial operators. In contrast, Wales and Northern Ireland, characterized by a higher proportion of SMEs and public-sector focus, tend to lag behind the broader United Kingdom adoption cycle. However, growing supplier reporting pressures are gradually driving these regions toward structured carbon disclosures. The South West and East of England contribute demand from sectors such as aerospace, defense, life sciences, and agri-food, where product footprint tools and supply chain data systems are often prioritized over broader entity-level disclosure platforms.

Competitive Landscape

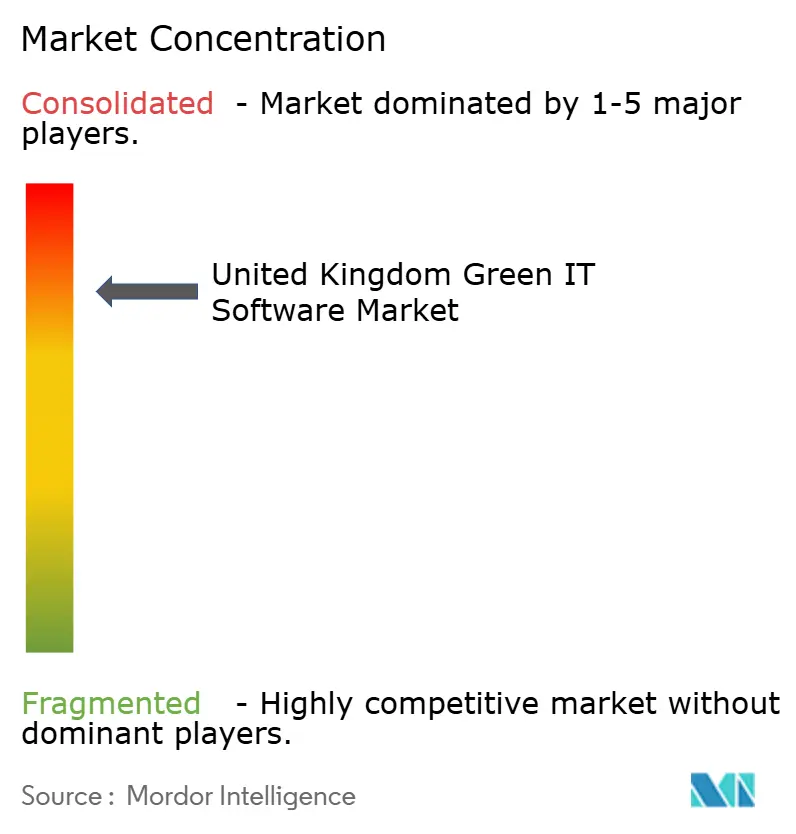

The United Kingdom green IT software market shows moderate-to-high consolidation, with large enterprise platform vendors competing against a broader group of specialist sustainability providers and newer AI-focused firms. SAP SE, Microsoft Corporation, IBM, Salesforce, Inc., and Workiva Inc. all benefit from established enterprise relationships in ERP, reporting, infrastructure, or CRM, which gives them a strong route into sustainability budgets once clients prefer expansion inside familiar platforms. In the United Kingdom green IT software market, this matters because buyers often want easier governance, fewer vendor relationships, and better integration with financial and operational systems. That gives platform incumbents an advantage in larger accounts where procurement teams value system fit and reporting control as much as feature depth.

SAP’s Green Ledger strategy is one clear example, because it places carbon accounting inside S/4HANA and ties sustainability data more closely to financial records and core business processes. Salesforce is using a similar expansion path by connecting sustainability workflows to its wider enterprise platform, which turns climate software into an extension of existing customer operations and data governance choices. Specialist firms still retain room to compete because many buyers need deeper expertise in financed emissions, supplier data engagement, or narrower sustainability workflows that large horizontal platforms do not fully cover. EcoVadis is building durability through network effects around supplier sustainability data, and in May 2026 it reported that more than USD 2.5 trillion in global spend was governed through its sustainability risk insights network.[5]EcoVadis SAS, “EcoVadis and Watershed Partner to Close the Scope 3 Data Gap,” EcoVadis, resources.ecovadis.com That kind of supplier network strength is hard to copy, which means competition in the United Kingdom green IT software market is not based on software features alone.

AI capability is becoming another important line of separation in the United Kingdom green IT software market. SAP SE’s new sustainability AI agents, IFS Zero, Watershed’s AI agents, and Persefoni’s analytics tools all point to a market where automation, workflow speed, and usability are becoming core buying criteria rather than optional extras. EcoVadis and Watershed also announced a partnership in March 2026 to connect supplier carbon data with platform workflows, which shows how competitive strategy is moving toward ecosystem building rather than stand-alone product launches. White-space opportunities remain in sector-specific financed emissions tools for BFSI, embedded sustainability workflows for mid-market ERP users, and AI-led supplier engagement systems. The United Kingdom green IT software market is therefore consolidating around platform breadth, integration strength, and data-network advantages, while specialists continue to compete where use cases are narrower and operational depth matters more.

United Kingdom Green IT Software Industry Leaders

Microsoft Corporation

SAP SE

Salesforce, Inc.

IBM Corporation

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: SAP SE announced that new sustainability AI agents, including those delivering up to 80% reduction in manual compliance efforts for packaging and product workflows, will be generally available by the end of 2026. This escalation of AI-embedded sustainability software strategy deepens integration between carbon intelligence and core enterprise business processes across SAP's global customer base.

- May 2026: IFS launched IFS Zero on 27 May 2026, an agentic emissions operating system designed for asset-intensive industries. The platform unifies Scope 1, 2, and 3 emissions measurement, disclosure, and optimization in a single system alongside IFS Cloud 26R1, materially expanding IFS's sustainability software portfolio beyond its traditional industrial ERP offering.

- May 2026: Persefoni AI Inc. unveiled its Analytics Agent, enabling users to analyze carbon footprint data through natural language prompts within the Persefoni platform. The launch reinforces Persefoni's specialist positioning for financial institutions managing multi-entity, PCAF-compliant financed emissions portfolios requiring audit-ready outputs.

- March 2026: EcoVadis SAS and Watershed Technology Inc. announced a strategic partnership integrating EcoVadis' primary supplier carbon data directly into Watershed's platform. The collaboration targets the Scope 3 data gap by connecting granular supplier-level primary data with Watershed's AI-powered carbon accounting and disclosure workflows.

United Kingdom Green IT Software Market Report Scope

The United Kingdom Green IT Software Market refers to software solutions and digital infrastructure designed to promote sustainable IT operations. These solutions focus on energy-efficient computing, carbon footprint tracking, and the responsible management of IT resources throughout their lifecycle. This software is critical for UK organizations, enabling compliance with net-zero carbon targets, ESG reporting requirements, and green finance regulations, while simultaneously reducing operational expenses and environmental impact.

The United Kingdom Green IT Software Market Report is Segmented by Offering (Software, and Services), Deployment (Cloud-Based, On-Premise, and Hybrid), Solution Type (Carbon Management and Accounting Software, ESG Reporting and Compliance Software, Sustainability Data Management Platforms, Decarbonization Planning Software, and Energy and Resource Optimization Software), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Information Technology and Telecommunications, Banking, Financial Services, and Insurance (BFSI), Manufacturing, Energy and Utilities, Retail and E-Commerce, Government, Healthcare, Construction and Infrastructure, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Carbon Management and Accounting Software |

| ESG Reporting and Compliance Software |

| Sustainability Data Management Platforms |

| Decarbonization Planning Software |

| Energy and Resource Optimization Software |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| IT and Telecommunications |

| Manufacturing |

| Banking, Financial Services, and Insurance (BFSI) |

| Government and Public Sector |

| Energy and Utilities |

| Healthcare |

| Retail and E-Commerce |

| Construction and Infrastructure |

| Other End User Industries |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud-Based |

| On-Premise | |

| Hybrid | |

| By Solution Type | Carbon Management and Accounting Software |

| ESG Reporting and Compliance Software | |

| Sustainability Data Management Platforms | |

| Decarbonization Planning Software | |

| Energy and Resource Optimization Software | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Banking, Financial Services, and Insurance (BFSI) | |

| Government and Public Sector | |

| Energy and Utilities | |

| Healthcare | |

| Retail and E-Commerce | |

| Construction and Infrastructure | |

| Other End User Industries |

Key Questions Answered in the Report

What is the 2026 size of the United Kingdom green IT software market?

The United Kingdom green IT software market size stood at USD 1.35 billion in 2025, reaches USD 1.53 billion in 2026 and is forecast to reach USD 3.19 billion by 2031 at a 15.83% CAGR.

Which deployment model leads adoption in the United Kingdom green IT software space?

Cloud-based deployment leads with a 68.41% revenue share in 2025 and is also projected to post the fastest growth at 18.67% through 2031.

Why is BFSI the strongest customer group for green IT software in the UK?

BFSI led with 31.62% share in 2025 and is expected to grow at 21.19% CAGR because banks, insurers, and asset managers must manage both operational and financed emissions reporting.

What is driving faster adoption among UK SMEs?

SMEs are projected to grow at 19.79% CAGR mainly because large corporate buyers are pushing supplier networks to provide better Scope 3 emissions data.

Which solution area is gaining the most momentum?

Sustainability data management platforms are projected to grow at 21.77% CAGR because companies need a centralized and governed data layer to support multiple disclosure frameworks.

Page last updated on: