Microwavable Foods Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

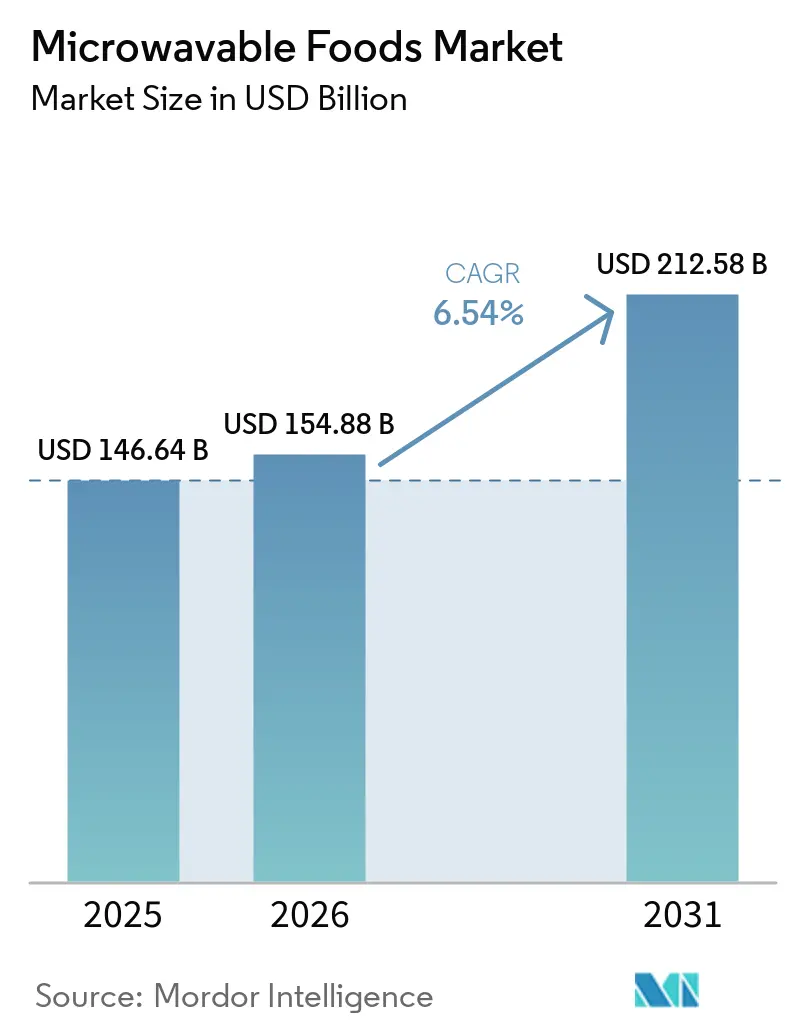

| Market Size (2026) | USD 154.88 Billion |

| Market Size (2031) | USD 212.58 Billion |

| Growth Rate (2026 - 2031) | 6.54% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Microwavable Foods Market Analysis by Mordor Intelligence

The microwavable foods market size is expected to grow from USD 146.64 billion in 2025 to USD 154.88 billion in 2026 and is forecast to reach USD 212.58 billion by 2031 at 6.54% CAGR over 2026-2031. The global microwavable foods market is experiencing significant growth, fueled by consumer preferences for convenience, health-conscious options, and diverse offerings, alongside continuous innovation from manufacturers. Time-strapped households are increasingly opting for quick-preparation solutions. Leading companies, such as Nestlé (known for Stouffer’s and Lean Cuisine) and Conagra Brands (offering Healthy Choice and Banquet), are revamping their product lines to prioritize nutrition and balanced meal options. Regional players like MTR Foods and Gits are expanding the market by introducing authentic Indian ready-to-eat meals, while Daawat offer microwavable rice cups aimed at attracting younger, urban consumers. Packaging advancements, including microwave-safe bowls, are redefining consumer expectations around usability and portion control, further enhancing the appeal of these products. However, rising costs in cold chain logistics and stricter regulations on single-use plastics are driving manufacturers to innovate with sustainable packaging solutions. These developments illustrate how microwavable foods are evolving from being merely convenient to becoming a strategic combination of speed, health, and innovation, establishing their role as a cornerstone of modern food consumption.

Key Report Takeaways

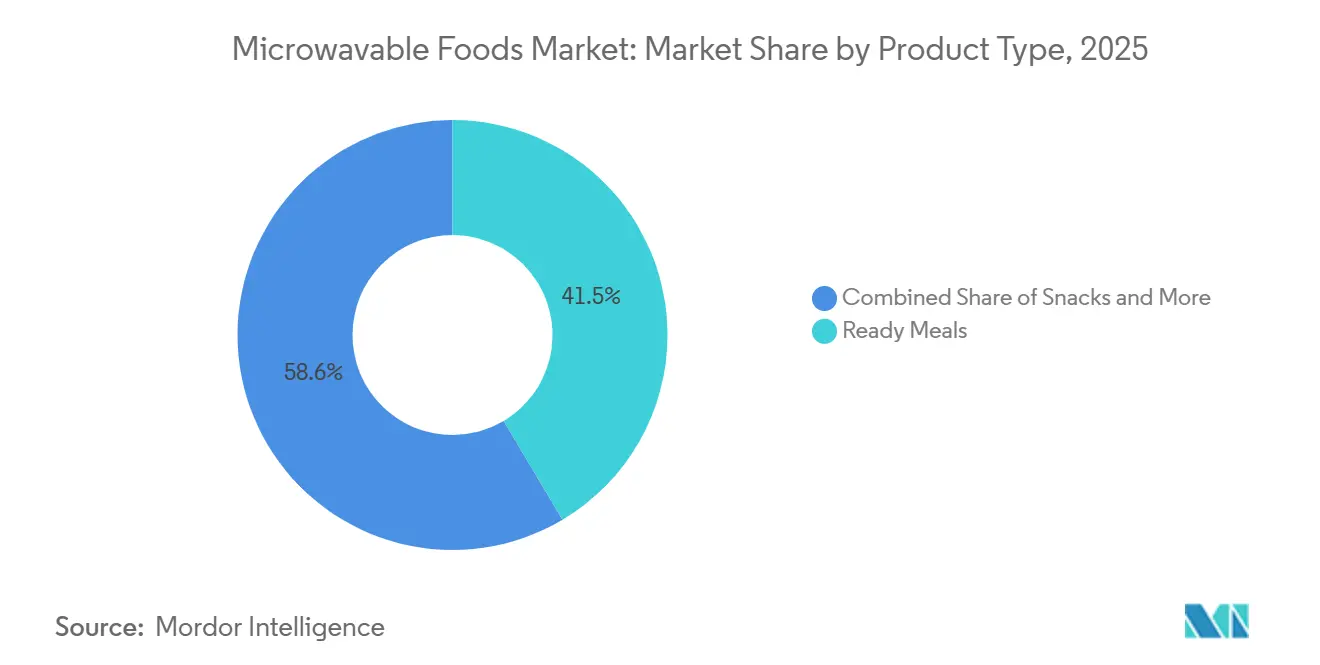

- By product type, ready meals led the microwavable foods market with a share of 41.45% in 2025, and are anticipated to register the fastest CAGR of 7.44% during 2026-2031.

- By type, frozen retained 54.79% share in 2025, whereas chilled is forecast to expand at a 7.68% CAGR through 2031.

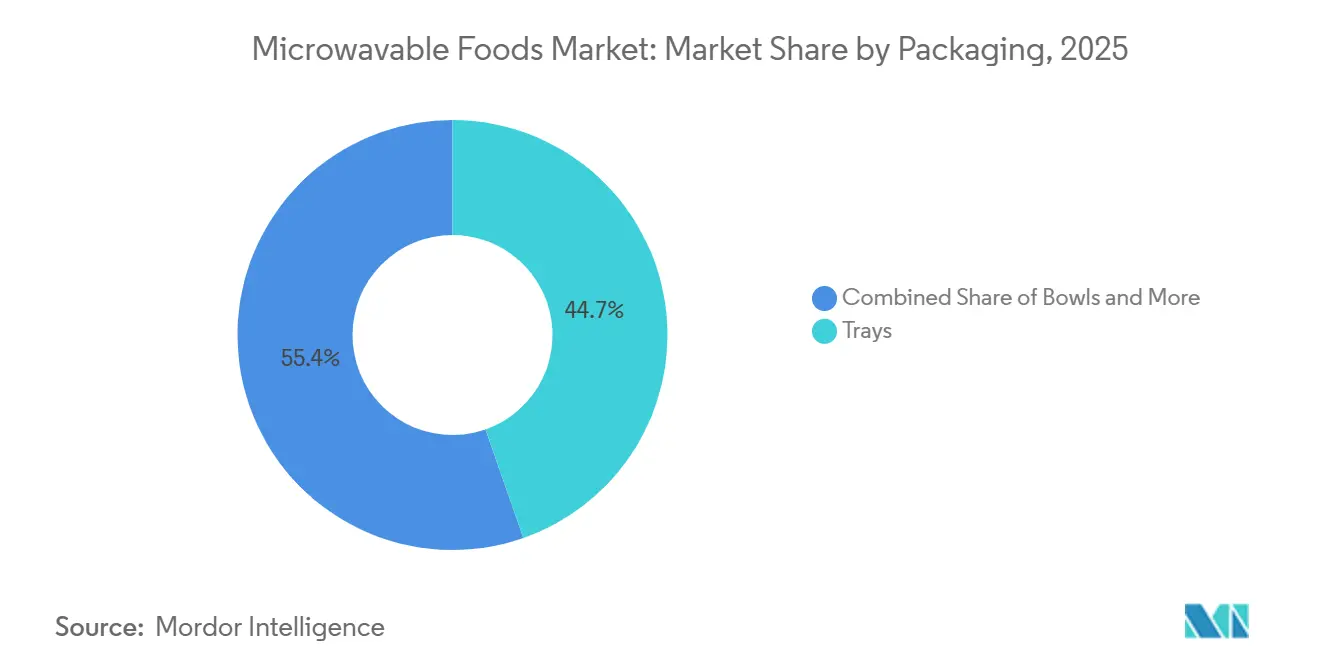

- By packaging, trays held 44.65% of 2025 revenue, but bowls are expected to grow fastest at 8.01% through 2031.

- By distribution channel, retail led the microwavable foods market with a share of 81.13% in 2025, while foodservice is anticipated to register the fastest CAGR of 7.47% during 2026-2031.

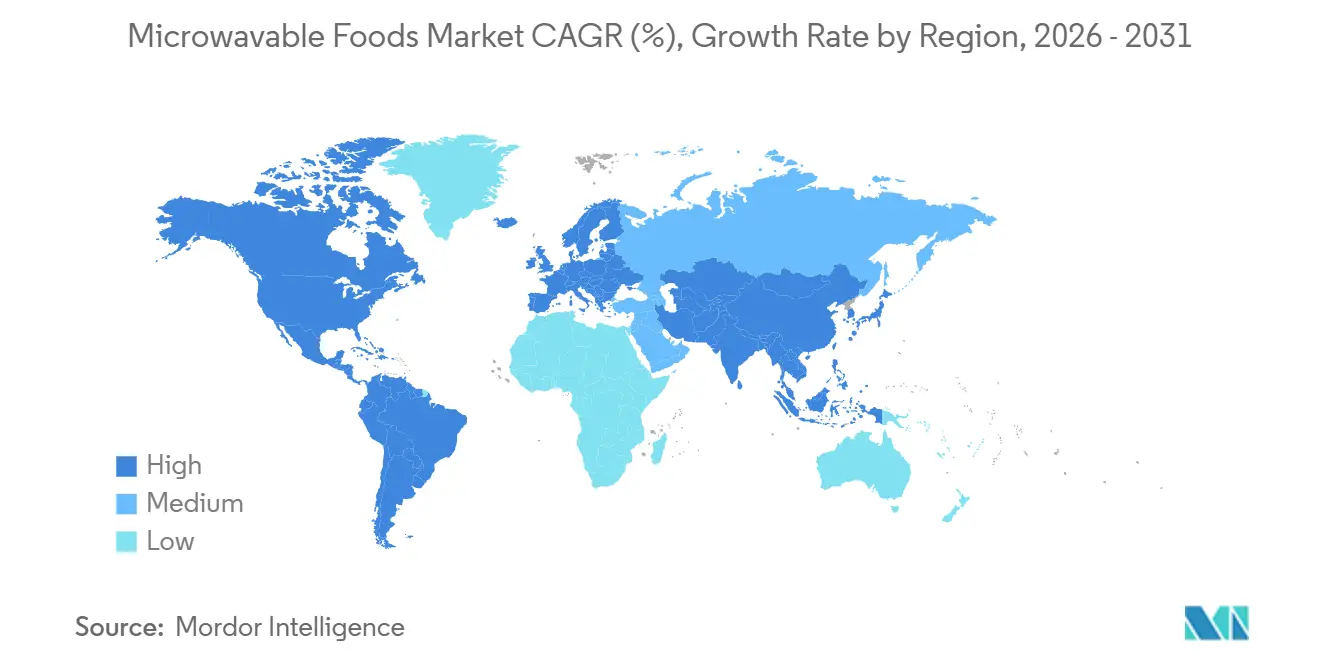

- By geography, North America led the microwavable foods market with a share of 36.88% in 2025, while Asia-Pacific is anticipated to register the fastest CAGR of 7.99% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Microwavable Foods Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Time-starved consumers driving demand for heat-and-eat meals | +1.7% | Global | Short-term (≤ 2 years) |

| Expansion of ethnic and international cuisine in microwavable formats | +0.9% | Global, Asia-Pacific and North America lead | Medium-term (2–4 years) |

| Rising popularity of high-protein and functional ready meals | +1.1% | Global, North America and Europe lead | Short-term (≤ 2 years) |

| Premiumization of frozen and chilled ready meal offerings | +0.8% | North America and European Union | Medium-term (2–4 years) |

| Rising adoption of labor-saving meal solutions in foodservice operations | +0.7% | Global, Asia-Pacific and European Union primary markets | Medium-term (2–4 years) |

| Technological advancements in microwave-compatible packaging | +0.5% | European Union lead, global spill-over | Long-term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Time-starved consumers driving demand for heat-and-eat meals

Time-pressed consumers are increasingly viewing microwavable foods as intentional choices in their meal planning, rather than as last-minute solutions. This shift reflects changing lifestyles, particularly in dual-income households, where convenience is essential but must also align with expectations for nutrition and variety. The American Frozen Food Institute (AFFI) and Food Marketing Institute’s (FMI) 2026 Power of Frozen in Retail report highlights this trend. Based on a survey of 1,560 United States shoppers, the report reveals that 77% now purchase frozen foods with a specific meal or day in mind, up from 71% in 2023[1]Source: American Frozen Food Institute, "America’s Rethinking Meal Planning: New Report Finds Frozen Foods Becoming a Kitchen Essential," affi.org. This data indicates a clear shift toward planned consumption over impulse buying. Additionally, microwavable foods are becoming more relevant by complementing scratch cooking, as many consumers now combine fresh and frozen ingredients in their meals. This trend expands usage occasions beyond the traditional “no time to cook” scenario, positioning microwavable foods as a practical solution that balances speed, health, and flexibility, making them a key part of modern eating habits.

Expansion of ethnic and international cuisine in microwavable formats

The global microwavable foods market is experiencing significant growth, driven by the increasing demand for ethnic and international cuisines that offer authentic, restaurant-quality flavors with unmatched convenience and affordability. Consumers, influenced by the variety offered by food delivery platforms, are now seeking microwavable options that deliver similar diverse taste experiences in a more convenient format. For example, in October 2025, Maple Leaf Foods introduced its 'Musafir' brand, a South Asian-inspired product line featuring protein-rich options such as masala paneer bites and butter chicken bites, both microwaveable in just 90 seconds. Similarly, AB World Foods expanded its presence in the single-serve ambient aisle by launching Patak’s and Blue Dragon product ranges, offering Indian and pan-Asian flavors, also ready in 90 seconds. These product launches highlight how authentic, diaspora-inspired flavors are becoming mainstream in retail, raising consumer expectations in the frozen food aisle. As a result, microwavable foods are evolving beyond convenience to become a gateway for consumers to explore global culinary experiences.

Rising popularity of high-protein and functional ready meals

The global microwavable foods market is experiencing a significant transformation, driven by the increasing demand for high-protein and functional ready-to-eat meals. Previously considered a niche offering, high-protein and functional meals have now become a mainstream consumer expectation. Today’s consumers view protein-rich options as a baseline requirement in their meals. To address this shift, manufacturers are redesigning their products to deliver higher protein-to-calorie ratios, improved textures, and portion sizes that cater to consumer needs for satiety and overall wellness. Conagra Brands’ Future of Frozen report, in 2025, emphasized this trend, revealing that protein accounted for USD 12 billion in consumer spending within the frozen food market. The report also highlighted strong consumer interest, with hundreds of millions of online searches for protein-related terms. Nestlé responded to this demand through its Vital Pursuit brand, specifically targeting users of Glucagon-Like Peptide-1 receptor agonists (GLP-1 receptor agonists) who are seeking functional frozen meal options. Similarly, Conagra reinforced its market presence with the introduction of MEGA Breakfast Bowls in February 2026, offering protein-centric solutions in the breakfast category. These advancements demonstrate how functional nutrition is becoming a core driver in the microwavable foods sector, positioning it as a reliable choice for health-conscious and wellness-focused consumers.

Rising adoption of labor-saving meal solutions in foodservice operations

Foodservice operations are becoming a significant growth driver in the microwavable foods market, as businesses increasingly adopt labor-saving meal solutions to address rising costs and operational pressures. This shift is not solely dictated by consumer demand but is also shaped by supply-chain dynamics. Kitchens are replacing traditional back-of-house labor with pre-configured microwavable components that ensure consistency, reduce dependency on fuel, and streamline preparation processes. In Germany, the growing demand for “Fix and Fertig” (ready-to-eat) products demonstrates how operators are rapidly embracing this trend. Similarly, in India, increasing labor costs and challenges with liquefied petroleum gas (LPG) supply have driven foodservice providers toward distributed reheating models. From a strategic perspective, foodservice operators are now influencing product specifications at the supply-chain level. They are seeking precise portioning, dependable microwave reheating capabilities, and extended shelf-life formats that exceed traditional retail requirements. For manufacturers, this shift presents a valuable opportunity. By investing in foodservice-grade product reformulations, they can position microwavable foods as essential tools for improving efficiency and ensuring consistency in professional kitchens, rather than merely as consumer convenience products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer perception of microwavable foods as highly processed | -0.8% | Global, North America and European Union primary | Short-term (≤ 2 years) |

| Volatility in cold chain, energy, and frozen logistics costs | -0.7% | Global | Short-term (≤ 2 years) |

| Environmental concerns related to single-use plastic packaging | -0.5% | European Union lead, North America secondary | Medium-term (2–4 years) |

| Food delivery apps intensifying competition for ready meals | -0.4% | Global, urban Asia-Pacific and North America | Medium-term (2–4 years) |

| Source: Mordor Intelligence | |||

Consumer perception of microwavable foods as highly processed

Consumer perception presents a significant challenge for the global microwavable foods market. Many consumers associate these products with being overly processed, placing them under scrutiny alongside other ultra-processed food categories. This perception has created a clear divide: some brands are strategically reformulating their products to offer cleaner labels and functional benefits, while others face persistent image challenges that cannot be resolved through marketing efforts alone. The rise in wellness-focused consumption further compounds this issue. This trend, driven in part by users of glucagon-like peptide-1 receptor agonist (GLP-1 RA) medications who demand precise nutritional ratios and ingredient transparency, has made undifferentiated microwavable meals increasingly uncompetitive. The strategic implication is clear: brands must innovate to remain relevant. While reformulation, such as reducing sodium, increasing fiber content, and eliminating certain oils, is technically achievable, it requires substantial research and development investments. Smaller producers often lack the financial resources to undertake such initiatives. As a result, the category faces structural pressures that could accelerate market consolidation. Only well-capitalized companies are positioned to adapt quickly and meet evolving consumer expectations effectively.

Volatility in cold chain, energy, and frozen logistics costs

The global microwavable foods market is facing significant challenges due to rising costs in cold chain logistics, energy, and frozen transportation. These cost increases are not only compressing profit margins but also hindering innovation across the value chain. A survey conducted by Lineage in March 2026, which included 1,000 supply chain decision-makers from the United States, Canada, and Mexico, highlighted that 73% of respondents expect tariffs to continue negatively impacting their financial performance through 2026. Additionally, 57% reported that the financial burden of tariffs in 2025 exceeded their initial expectations, emphasizing the persistent cost pressures. On the energy front, industrial electricity prices in the United States reached approximately 13.27 cents per kilowatt-hour in 2025, marking the highest level since 2022. This increase was primarily driven by geopolitical tensions disrupting natural gas supplies and heightened demand from digitalization and artificial intelligence infrastructure competing for energy resources on the same grid. Furthermore, disruptions in shipping have exacerbated costs for frozen goods beyond standard freight rates. These disruptions have also introduced additional challenges, such as higher inventory carrying costs and stricter compliance requirements related to temperature-chain documentation. These combined pressures are disproportionately affecting mid-sized manufacturers, limiting their ability to allocate resources toward product development and premiumization efforts. This comes at a time when consumer expectations for quality and innovation are steadily rising, further intensifying the challenges faced by these manufacturers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ready Meals Define Category Economics

Ready Meals lead the global microwavable foods market, contributing 41.45% of revenues in 2025 and are expected to grow at a CAGR of 7.44% from 2026 to 2031. This dominance highlights their ability to provide complete, nutritionally balanced solutions that align with consumer preferences for convenience, protein-rich options, and wellness-focused products. Ready Meals have become the cornerstone of the category's financial performance, offering not only time-saving benefits but also a reliable reputation for health and nutrition. This makes them a critical focus area for manufacturers and retailers aiming to meet evolving consumer demands.

Other product categories, such as snacks, soups and broths, bakery and desserts, and vegetables and side dishes, bring variety and innovation to the market. Snacks are gaining popularity through globally inspired, single-serve formats. Soups and broths are leveraging their premium and functional positioning to attract health-conscious consumers. Vegetables and side dishes benefit from clean-label claims, while bakery and desserts continue to grow their niche appeal. Despite these developments, the market's growth remains firmly anchored in ready meals, which not only drive current category performance but also set the direction for future expansion.

By Type: Chilled Formats Outpace Frozen on Value Credentials

In 2025, frozen formats maintained their leadership in the global microwavable foods market, capturing a 54.79% share. This dominance is driven by long-standing consumer preferences and the widespread availability of cold-chain infrastructure, particularly in North America and Europe. These regions play a critical role in shaping the market's economic foundation. As consumers increasingly view convenience and quality as complementary attributes, frozen formats continue to serve as the cornerstone of global microwavable food consumption.

Chilled formats, on the other hand, are experiencing rapid growth, with a projected CAGR of 7.68% from 2026 to 2031. This growth reflects their rising status as the preferred choice for premium, fresh-like ready meals. The trend is particularly evident in markets where advancements in cold-chain infrastructure have extended into grocery and convenience retail. European supermarkets have significantly increased the shelf space allocated to chilled ready meals, recognizing that profit margins for chilled products outperform those of ambient options and are approaching the levels of premium frozen products. While ambient formats remain essential in regions with underdeveloped cold infrastructure, chilled formats are increasingly seen as the forefront of innovation. They are meeting consumer demand for freshness and premium quality while reshaping the competitive dynamics within the microwavable foods sector.

By Packaging: Bowls Challenge Tray Dominance on Ergonomic Logic

In 2025, trays remain the leading packaging format in the global microwavable foods market, accounting for a significant 44.65% share of revenues. Their popularity is driven by their operational efficiency, as trays are a critical component of automated retail packing lines and are fully compatible with the standardized microwave cooking profiles used in most ready-meal formulations. Trays provide manufacturers and retailers with a reliable solution for mass-market distribution by ensuring consistency, scalability, and seamless integration with existing infrastructure.

On the other hand, bowls are emerging as the fastest-growing packaging format, with a projected CAGR of 8.01% during the forecast period of 2026 to 2031. This growth is fueled by their ergonomic design, ability to support portion control, and potential for brand differentiation, advantages that trays cannot easily replicate. Bowls convey a sense of single-serve authenticity, align with the growing popularity of protein bowls in the foodservice industry, and optimize material usage by reducing waste relative to their fill volume. As regulatory requirements increasingly emphasize material substitution and recyclability, bowls are positioned as a key area of innovation in packaging. They offer a compelling combination of consumer appeal and compliance benefits. While trays currently define the scale and stability of the market, bowls are setting the stage for future growth and premiumization.

By Distribution Channel: Foodservice Operators Accelerate Frozen Adoption

In 2025, retail remained the dominant distribution channel in the global microwavable foods market, accounting for a significant 81.13% of revenues. This leadership was driven by the widespread availability of frozen-aisle infrastructure in supermarkets and hypermarkets, which continued to serve as the primary shopping destinations for consumers. At the same time, online retail steadily gained traction, particularly in regions where quick-commerce platforms enabled the delivery of chilled ready meals within minutes. Convenience and grocery stores also played a vital role in this growth by offering single-serve formats designed for impulse purchases, thereby integrating microwavable foods into consumers' everyday eating habits.

Conversely, the foodservice sector is anticipated to be the fastest-growing distribution channel, with a CAGR of 7.47% forecasted for the period 2026–2031. This growth extends beyond volume, as foodservice operators increasingly adopt microwavable frozen components to streamline operations and reduce labor costs. This adoption validates these product formats and often leads to their acceptance in retail markets. The convergence of foodservice and retail is transforming stock-keeping unit (SKU) economics, benefiting manufacturers who can develop product designs that cater to both channels. The rapid growth of foodservice highlights its role as a driver of innovation and a builder of consumer trust, positioning it as a critical growth avenue in the evolving microwavable foods market.

Geography Analysis

In 2025, North America holds a dominant 36.88% share of the global microwavable foods market. This leadership is attributed to a well-developed frozen-aisle infrastructure in supermarkets and hypermarkets, coupled with the rapid expansion of online retail and convenience store formats. The region's growth is being shaped by evolving consumer preferences, such as the increasing demand for protein-rich products influenced by Glucagon-Like Peptide-1 (GLP-1) trends, and the premiumization of offerings, particularly through the introduction of diverse ethnic cuisines. Canada and Mexico significantly contribute to this growth by launching products tailored to their diaspora communities and enhancing infrastructure. Additionally, regulatory measures like California’s Senate Bill 54 (SB54), which mandates reductions in single-use plastics, are driving changes in packaging strategies. These factors position North America as a leader in both consumption and regulatory compliance.

Asia-Pacific is the fastest-growing region, with a projected compound annual growth rate (CAGR) of 7.99% from 2026 to 2031. This growth is driven by demographic and economic shifts, as urban households in countries like China, India, and Southeast Asia increasingly adopt microwavable food formats. Factors such as compressed work schedules and the expansion of quick-commerce platforms are making these products more accessible. According to the Japan Frozen Food Association, Japan's frozen food consumption exceeded 3 million tons in 2025[3]Source: Japan Frozen Food Association, "Frozen Food Production and Consumption in 2025," reishokukyo.or.jp. In China, the adoption of frozen products suitable for microwaving has surged, now accounting for approximately 60% of the country's frozen food consumption. The region is also a hub for innovation, particularly in ready meals, which are experiencing a significant increase in new product launches. This positions Asia-Pacific as a key driver of growth in the global microwavable foods market.

Europe, led by Germany, is the second-largest regional market. Data from the German Frozen Food Institute (dti) indicates that total sales of frozen food products in Germany grew by 2.5% in 2025, reaching a volume of 4.238 million tons[2]Source: German Frozen Food Institute, "Frozen Food Continues on Record Course," tiefkuehlkost.de. This growth is driven by strong demand across both retail and out-of-home segments, influenced by time constraints and rising labor costs. The United Kingdom is leading innovation in chilled food formats, while France and Italy are focusing on premiumizing ambient and chilled ready meals by emphasizing regional authenticity. Central and Eastern Europe are benefiting from increased investments that are expanding product diversity. Meanwhile, South America and the Middle East and Africa, though smaller contributors, are steadily growing due to the development of cold-chain infrastructure in countries like Brazil, the United Arab Emirates (UAE), Argentina, and South Africa. Together, these regions highlight a global market where North America provides scale, Asia-Pacific drives momentum, and Europe balances tradition with innovation.

Competitive Landscape

The global microwavable foods market presents a highly fragmented competitive landscape. In North America, companies such as Conagra Brands and Nestlé USA leverage their extensive branded product portfolios to maintain a strong market presence. In Europe, the merger of Greencore and Bakkavor in 2026 positioned the combined entity as a leader, particularly in private-label offerings and chilled convenience food formats. Recent consolidations in Europe have set new industry standards for scale, while advancements in microwave packaging technologies, supported by increased patent activity, are creating technical barriers. These barriers enhance brand differentiation and premiumization, especially for companies with significant research and development capabilities.

Strategic priorities within the industry highlight diverse approaches. Companies like CJ CheilJedang are focusing on geographic expansion by investing in localized production facilities in Hungary and South Korea to meet both regional and global demand. Meanwhile, niche players such as Amy's Kitchen, Saffron Road, and NISSIN are carving out premium positions in the market. By combining clean-label attributes with globally inspired flavors, these companies are challenging established brands that often struggle to match their agility and authenticity.

The fragmented nature of the market is further emphasized by private-label retailers and regional specialists stepping in to fill gaps left by multinational corporations exiting or deprioritizing frozen food categories. This has created a dynamic competitive environment where scale, innovation, and niche positioning coexist. The market rewards both large-scale consolidation at the top and the emergence of smaller, agile players at the margins. The interplay of regional strengths, technical innovation, and consumer-driven demand for premium products ensures that competition remains fluid. This evolving landscape provides opportunities for new challengers to capture market share, even as established players work to defend their positions.

Microwavable Foods Industry Leaders

-

Nestlé S.A.

-

Conagra Brands, Inc.

-

The Kraft Heinz Company

-

General Mills, Inc.

-

CJ CheilJedang Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Amy's Kitchen, a family-owned leader in organic prepared food, announced its expansion into more than 150 Costco warehouses. This initiative brought its popular Cheese Enchiladas and Bean and Cheese Burritos to Costco members across key regions in the United States. The rollout began in Los Angeles, followed by the Bay Area and Texas. This represented one of Amy's Kitchen's most significant retail expansions, introducing the brand to millions of new households through Costco, one of the country's most trusted retail chains.

- March 2026: South Korean food conglomerate CJ CheilJedang opened its first fully automated production line for frozen gimbap. This strategic move aimed to address the growing global demand for the Korean dish, which consists of rice, vegetables, and cooked meat rolled in dried seaweed and served in bite-sized slices. The facility, located on the company’s campus in Jincheon, North Chungcheong province, was the result of an 18-month effort to develop proprietary equipment. This technology automated every stage of production, from loading fillings into rice to slicing and tray-packing the finished rolls.

- February 2026: Conagra Brands, Incorporated, launched a protein-rich addition to its breakfast offerings with the introduction of Banquet MEGA Breakfast Bowls. Each bowl contained 30 grams of protein, and the four new varieties provided a hearty and flavorful breakfast option. Staying true to the Banquet MEGA promise of delivering big flavor, high protein, and great value, these bowls featured a tray-in-tray steaming technology. This innovation kept the sauce, and ingredients separate while frozen, ensuring that when microwaved, the eggs remained fluffy, the potatoes stayed tender, and the proteins retained their juiciness.

Global Microwavable Foods Market Report Scope

Microwavable food refers to food products that are specifically designed to be safely cooked, reheated, or prepared using a microwave oven, offering convenience and speed without compromising safety or quality.

The microwavable foods market is segmented by product type, type, packaging, distribution channel, and geography. By product type, the market is segmented into ready meals, snacks, soups and broths, bakery and dessert products, vegetables and side dishes, and others. By type, the market is segmented into frozen, chilled, and ambient/shelf stable. By packaging, the market is segmented into trays, bowls, cups and tubs, and others. By distribution channel, the market is segmented into Foodservice and Retail. By geograohy, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Ready Meals |

| Snacks |

| Soups and Broths |

| Bakery and Dessert Products |

| Vegetables and Side Dishes |

| Others |

| Frozen |

| Chilled |

| Ambient/Shelf Stable |

| Trays |

| Bowls |

| Cups and Tubs |

| Others |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| United Arab Emirates | |

| Rest of Middle East and Africa |

| By Product Type | Ready Meals | |

| Snacks | ||

| Soups and Broths | ||

| Bakery and Dessert Products | ||

| Vegetables and Side Dishes | ||

| Others | ||

| By Type | Frozen | |

| Chilled | ||

| Ambient/Shelf Stable | ||

| By Packaging | Trays | |

| Bowls | ||

| Cups and Tubs | ||

| Others | ||

| By Distribution Channel | Foodservice | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the size of the global microwavable foods market?

The global microwavable foods market was valued at USD 146.64 billion in 2025 and is forecast to reach USD 212.58 billion by 2031, expanding at a CAGR of 6.54% between 2026 and 2031.

Which product type dominates the market?

Ready Meals are the largest product type, accounting for 41.45% of revenues in 2025. They are also the fastest-growing product category, projected to expand at a CAGR of 7.44% from 2026–2031.

Which format leads the market?

Frozen formats held the largest share at 54.79% in 2025, supported by strong infrastructure and consumer habits. However, Chilled formats are the fastest-growing, expected to rise at a CAGR of 7.68% over 2026–2031.

What packaging format is most widely used?

Trays dominate packaging with a 44.65% share in 2025 due to their compatibility with automated packing lines. Bowls, however, are the fastest-growing format, forecasted to expand at 8.01% CAGR, driven by ergonomic and single-serve appeal.

Which distribution channel is largest?

Retail channels accounted for 81.13% of market revenues in 2025, led by supermarkets, hypermarkets, and online platforms. Foodservice is the fastest-growing channel, projected at a CAGR of 7.47% from 2026–2031, as operators adopt microwavable frozen components for efficiency.

Which region leads the global market?

North America is the largest regional market, holding 36.88% of global revenues in 2025. Asia-Pacific is the fastest-growing region, forecasted to expand at a CAGR of 7.99% between 2026 and 2031, driven by demographic shifts, urbanization, and quick-commerce adoption.

Page last updated on: