Canned Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 143.96 Billion |

| Market Size (2031) | USD 177.98 Billion |

| Growth Rate (2026 - 2031) | 4.34% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Canned Food Market Analysis by Mordor Intelligence

Canned food market size in 2026 is estimated at USD 143.96 billion, growing from 2025 value of USD 137.97 billion with 2031 projections showing USD 177.98 billion, growing at 4.34% CAGR over 2026-2031. Urbanization is fueling the demand for convenient meal options, especially among working professionals and students. Government mandates on emergency preparedness are bolstering the stockpiling of canned foods. Meanwhile, manufacturers are innovating, enhancing flavors, nutritional content, and embracing sustainable packaging. Regulatory shifts, like China's stringent clean-label mandates and Europe's push for sustainability, are nudging manufacturers towards natural ingredients, reduced artificial preservatives, and eco-friendly packaging. The market's fragmented landscape is a boon for regional players and niche producers, allowing them to carve out a niche with unique products, ethnic flavors, and locally-sourced ingredients. With economic recovery in South America boosting consumer spending, retail growth in emerging Asia-Pacific markets, and a rising appetite for premium, organic, and gourmet canned products in North America and Europe, the market is poised for robust growth.

Key Report Takeaways

- By product type, canned fish and seafood held 33.10% of the canned food market share in 2025; canned fish and seafood are projected to register the fastest 5.50% CAGR to 2031.

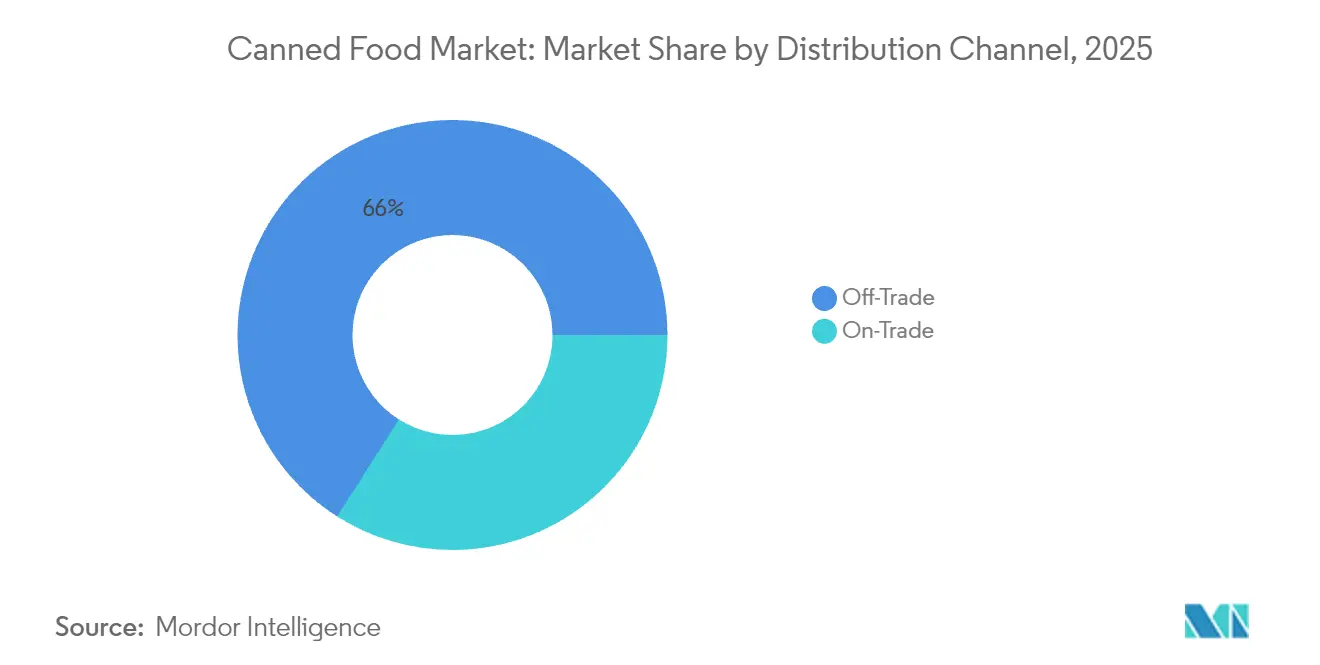

- By distribution channel, off-trade formats dominated with 65.98% revenue share in 2025; the off-trade is forecast to expand at a 5.05% CAGR through 2031.

- By form, chunks and pieces commanded a 54.35% share of the canned food market size in 2025; chunks and pieces are set to grow at a 5.18% CAGR to 2031.

- By geography, Europe accounted for 38.70% of the 2025 market, while South America is the fastest-growing region with a 7.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Canned Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience and health drive surge in canned food | +0.8% | Global, with concentration in North America and Asia-Pacific urban centers | Medium term (2-4 years) |

| Extended shelf life and storage capabilities aligned with modern consumer requirements | +0.7% | Global, particularly strong in emerging markets with limited cold chain infrastructure | Long term (≥ 4 years) |

| Canned seafood consumption increased by protein diversification | +0.6% | North America and Europe core, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Strategic government stockpiling for military and emergency response | +0.4% | Global, with emphasis on developed nations and conflict-prone regions | Long term (≥ 4 years) |

| Consumer purchase decisions influenced by sustainability certifications and product traceability | +0.5% | Europe and North America leading, spillover to developed Asia-Pacific markets | Medium term (2-4 years) |

| Expansion of canned food offerings in the foodservice sectors | +0.9% | Global, with strongest growth in North America restaurant-to-retail transitions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Convenience and health drive surge in canned food

As urban living spaces shrink, the demand for convenience and health has propelled a notable rise in canned food consumption. Statistics Korea highlights a rise in South Korea's one-person households, increasing from 7.5 million in 2022 to 7.83 million in 2023[1]Source: Statistics Korea, "Number of one-person households in South Korea from", kosis.kr. This trend has intensified the appetite for compact, portion-controlled canned meals, perfectly suited for today's time-constrained lifestyles. Premium brands, such as Fishwife, are not just selling canned food; they're curating an aspirational lifestyle, especially resonating with millennials and Gen Z through vibrant online communities. Social media has become a pivotal platform, with consumers actively discovering and promoting new canned offerings, amplifying their market presence. Moreover, single-serve packaging not only aligns with health and convenience trends but also mitigates concerns about food waste and budget constraints, making canned foods a go-to for urban shoppers prioritizing both affordability and sustainability.

Extended shelf life and storage capabilities aligned with modern consumer requirements

During times of supply chain disruptions and high inflation, households increasingly rely on canned foods, thanks to their extended shelf life. Metal cans can preserve food quality and nutritional value for 2-5 years without refrigeration. This not only cuts down on food waste but also results in carbon dioxide savings, akin to taking millions of vehicles off the road. Such preservation is especially advantageous for consumers who buy in bulk, helping them counter rising food prices and secure their household's food supply. Beyond homes, institutional buyers and foodservice operators leverage canned products to manage inventory costs, ensure a steady supply, and reduce food spoilage. This shift has led to a surge in demand for shelf-stable foods, which promise long-term food security without the need for specialized storage or constant power. Canned foods, with their minimal storage requirements, play a pivotal role in sustainable food distribution, cutting down energy consumption while ensuring product quality. Moreover, the sturdy design of metal cans shields contents from external threats, guaranteeing safety and quality, whether in tough storage conditions or during lengthy transport.

Canned seafood consumption increased by protein diversification

As consumers pivot towards sardines, mackerel, and premium conservas, the canned seafood market is diversifying beyond its traditional staples of tuna and salmon. Canned seafood, often seen as a cost-effective alternative to its fresh counterpart, boasts essential omega-3 fatty acids, high-quality protein, and vital nutrients. The preservation process not only safeguards the seafood's nutritional value but also extends its shelf life, appealing to consumers eyeing long-term storage. Busy households and food service establishments are drawn to the convenience of canned seafood, further bolstering its market presence. Highlighting the intersection of health and environmental awareness, the Marine Stewardship Council (MSC) notes that consumers are actively pursuing products with verified sustainability claims, often at a premium. The MSC Fisheries Standard, a benchmark for sustainability, emphasizes three core principles: fishing from healthy stocks, adopting long-term management practices, and minimizing ecosystem impact. Over 400 wild-capture fisheries globally proudly uphold this certification[2]Source: Marine Stewardship Council, "What does the MSC label mean", msc.org. By focusing on local production, the industry is tackling sustainability concerns, cutting down transportation distances, and championing responsible fishing in domestic waters. Beyond just seafood, these canneries are pivotal for coastal communities, driving job creation, economic development, and upholding stringent quality control standards.

Strategic government stockpiling for military and emergency response

Amid geopolitical tensions and climate disruptions, governments worldwide are stockpiling canned foods, underscoring a heightened focus on food security. Switzerland's emergency reserves boast tens of thousands of tonnes of non-perishables, ensuring 2,300 daily calories for individuals over a span of three to four months. Through a system of import surcharges, Switzerland's program not only guarantees food availability during emergencies but also establishes predictable demand patterns for suppliers. This extensive procurement strategy shapes global trends, with military and emergency response entities enforcing stringent packaging and shelf-life standards, favoring established canned food producers. Such standards often mandate moisture-resistant packaging, temperature stability, and an extended shelf life of 2-5 years. As climate change amplifies the frequency of natural disasters, the strategic importance of food stockpiling grows. Additionally, the expanding military forces are propelling market growth. In 2023, the United States, as reported by the Stockholm International Peace Research Institute, allocated a staggering USD 916 billion to military spending, accounting for over 40% of the global military expenditure, which stands at USD 2.4 trillion.[3]Source: Stockholm International Peace Research Institute, "Trends in World Military Expenditure 2023", www.sipri.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer purchasing behavior influenced by sodium content and preservative levels in products | -0.6% | Global, with strongest impact in health-conscious North America and Europe markets | Medium term (2-4 years) |

| Environmental impact of metal can disposal raises sustainability concerns | -0.4% | Europe and North America leading, expanding to developed Asia-Pacific markets | Long term (≥ 4 years) |

| Quality Issues and Product Recalls Raising Trust Issues | -0.7% | Global, with acute impact in manufacturing-heavy regions and emerging markets | Short term (≤ 2 years) |

| Growing consumer preference for fresh and unprocessed food products | -0.5% | Developed markets primarily, with North America and Europe showing strongest trends | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer purchasing behavior influenced by sodium content and preservative levels in products

As health consciousness rises, consumers are scrutinizing sodium and preservative levels in their food choices, driving growth in the canned food market. Alarmingly, Americans consume too much sodium, largely from processed foods, including canned goods. This trend has sparked concerns from health organizations and regulatory bodies alike. Responding to these concerns, the FDA has rolled out comprehensive sodium reduction guidelines, exerting significant pressure on the canned food industry to reformulate its products. Simultaneously, there's a growing consumer demand for preservative-free options. In China, the National Health Commission (NHC) and the State Administration for Market Regulation (SAMR) have introduced the National Food Safety Standard for Canned Foods (GB 7098-2025)[4]Source: USDA, "National Food Safety Standard Canned Foods Finalized", apps.fas.usda.gov. This rigorous standard governs all canned products in China, detailing requirements for ingredients, physical and chemical indicators, contaminants, and microbial limits.

Environmental Impact of Metal Can Disposal Raises Sustainability Concerns

From regulators to consumers, stakeholders are increasingly scrutinizing the sustainability of metal packaging. The environmental impact of metal can disposal has emerged as a significant constraint on the global canned food market. While aluminum and steel cans tout their recyclability and contribution to a "circular economy," evidence and regulatory actions from 2024 onward spotlight challenges in waste generation, recycling, carbon footprints, and the sustainability of alternative packaging materials.Metal cans present a unique challenge for landfills: they corrode over time yet can persist for decades. Additionally, sourcing raw materials like aluminum, steel, and tinplate for new cans comes with environmental costs, including energy consumption, greenhouse gas emissions, and disruption to ecosystems. Despite the assertion that these materials are "infinitely recyclable," the reality is different. In 2023, the U.S. recorded a 43% post-consumer recycling rate for aluminum beverage cans, down from the historical average of 52%. Meanwhile, the Aluminum Association noted a 57% industry recycling rate, factoring in both imported and exported scrap.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Seafood Leads Premium Transformation

In 2025, canned fish and seafood command a 33.10% market share, buoyed by a surge in consumer preference for nutrient-rich, high-protein foods. This segment's expansion is bolstered by its widespread availability, extended shelf life, and a strong sustainability image, especially for products like tuna, salmon, and sardines. In developed markets, brands are capitalizing on premium positioning, rolling out offerings like wild-caught, traceable, and low-sodium seafood to cater to health-savvy consumers. Additionally, the growing focus on transparency in sourcing and labeling has further strengthened consumer trust in these products. Moreover, the adaptability of seafood in diverse cuisines has cemented its popularity among retail shoppers and foodservice providers alike, solidifying its top market status.

With a projected CAGR of 5.50% through 2031, this segment stands out as the fastest-growing in the canned food realm. The uptick in demand is fueled by rising seafood consumption in emerging markets, fresh innovations in packaging and flavors, and a heightened consumer awareness of the benefits of omega-3s and proteins. Companies are also tapping into sustainability certifications and ethical sourcing narratives to draw in new clientele. Furthermore, advancements in packaging technology, such as easy-open cans and recyclable materials, are enhancing convenience and aligning with eco-conscious consumer preferences. The growth of online platforms and convenience stores as sales channels further broadens market access, driving consistent expansion in both mass-market and premium segments.

By Form: Whole Products Gain Momentum

In 2025, chunks and pieces formats command a dominant 54.35% market share, largely due to their prevalent use in processed foods, ready-to-eat meals, and foodservice applications. Their adaptability in various cooking processes, combined with cost-effective production and distribution, has made them a favorite among manufacturers and retailers alike. This segment's versatility across different cuisines and product types ensures a steady demand in global markets. Additionally, their ability to cater to diverse consumer preferences, ranging from traditional dishes to modern fusion cuisines, further enhances their appeal. Furthermore, efficient processing techniques and scalability empower companies to offer competitive pricing, solidifying the segment's leading position in both retail and foodservice sectors.

Projecting forward, the chunks and pieces segment is set to experience the most rapid growth, with an anticipated CAGR of 5.18% extending through 2031. This surge is largely attributed to a rising consumer preference for convenient, high-quality ingredients that seamlessly blend into prepared meals, snacks, and salads. The segment is also reaping the benefits of technological advancements in preservation and packaging, which bolster shelf life and texture. These innovations not only improve product quality but also reduce food waste, aligning with sustainability goals and consumer expectations. In response to these trends, manufacturers are innovating, rolling out versatile flake-based products tailored for health-conscious consumers and those seeking quick meal preparations, further fueling market growth.

By Distribution Channel: Foodservice Accelerates Growth

In 2025, off-trade channels command a dominant 65.98% market share, bolstered by robust retail penetration and easy consumer access. Supermarkets and hypermarkets lead the distribution landscape, showcasing a vast product range, running promotional campaigns, and employing competitive pricing. These expansive stores adeptly cater to bulk buyers and family-oriented shoppers, driving steady volume sales. Their ability to offer a one-stop shopping experience, combined with frequent discounts and loyalty programs, further strengthens their position in the market. Meanwhile, convenience and grocery stores amplify the segment's success, tapping into both urban and regional markets. They cater to time-sensitive shoppers with single-serve and easily storable products, ensuring accessibility and quick purchase options for consumers with busy lifestyles.

Among off-trade channels, online retail emerges as the quickest-growing avenue, projected to surge at a 7.45% CAGR through 2031, outpacing the overall off-trade growth rate of 5.05%. This surge is driven by heightened digital engagement, a preference for home deliveries, and mobile app subscriptions that promote repeat buying. E-commerce platforms enhance consumer experience with personalized offerings, bundled deals, and effortless order tracking. Additionally, the convenience of shopping from home, coupled with the availability of diverse payment options and flexible delivery schedules, has significantly contributed to the growth of online retail. The growing trend of online grocery shopping, especially for shelf-stable and ready-to-eat items, is reshaping traditional retail and broadening brand visibility across diverse demographics. This shift is further supported by advancements in logistics and supply chain efficiency, enabling faster and more reliable deliveries.

Geography Analysis

Europe contributed 38.70% of 2025 revenue, maintaining its position as the largest regional market. This dominance stems from established consumption patterns, robust supply chains, and strict sustainability regulations. The region's emphasis on Marine Stewardship Council certification and high-recycled-content metal cans generates additional value that supports environmental innovations. Germany, France, the United Kingdom, the Netherlands, Belgium, and Spain represent the primary importing and consuming markets of canned food.

Germany, as Europe's largest food market, presents significant export opportunities, particularly in the organic segment. While the UK and France show strong demand due to lower domestic production compared to Spain and Italy, the Netherlands serves as both a major consumer and re-export hub. South America demonstrates the highest growth trajectory with a 7.12% CAGR. Economic recovery in Argentina and Colombia improves consumer purchasing power, while government initiatives support domestic seafood processing to enhance export value.

In Asia-Pacific, market conditions vary by country. Indian consumers increase spending on essential items, with canned legumes and fruits gaining popularity during monsoon-related supply disruptions. China's implementation of the National Food Safety Standard (GB 7098-2025) introduces tighter controls on contaminants and microbiological parameters, potentially increasing operational costs while improving consumer confidence. Chinese manufacturers are adapting to Beijing's February 2025 preservative restrictions by implementing enhanced thermal processing technology to maintain product quality. North America sustains market volume through product innovation, established brand preferences, and new fish-canning facilities in Oregon and Massachusetts, reducing import dependence.

Competitive Landscape

The global canned market remains fragmented, with established companies like Conagra Brands Inc. and Kraft Heinz maintaining strong retail presence while competing against emerging artisanal brands that use social media platforms effectively. Traditional seafood processors face competition from local and regional players who have built strong consumer trust through sustainable fishing practices and transparent supply chains.

The industry is consolidating its packaging operations, with a specific focus on seafood-specific preservation techniques and eco-friendly packaging solutions. Companies are increasing research and development investments in product development while implementing sustainable practices to address consumer environmental concerns. Strategic acquisitions continue to reshape the canned seafood market, particularly in regions with high fish consumption and established fishing industries.

Established companies improve operations through technology adoption, including advanced fish processing equipment and quality control systems. New market entrants build consumer relationships through direct-to-consumer sales, distinctive packaging, and QR code technology that provides producer information, particularly attracting younger consumers who seek sustainably sourced seafood products. These emerging players differentiate themselves through specialty offerings like wild-caught fish and premium seafood varieties.

Canned Food Industry Leaders

-

Kraft Heinz Company

-

Bolton Group (Rio Mare, Saupiquet)

-

The Campbell's Company

-

Hormel Foods Corporation

-

Del Monte Pacific Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Simak, a state-backed company owned by Fisheries Development Oman, has launched its commercial canned tuna product line in the domestic market. The facility, situated in the Duqm Special Economic Zone, has the capacity to produce over 100 million cans annually, processing more than 30,000 metric tons of raw seafood.

- March 2024: The Bull Brand launched three new ready-to-eat canned mince meals: Bolognaise Mince, Chilli Mince, and Savoury Mince. These new variants offer great value for money and are highly versatile.

- March 2024: Conagra Brands expanded its tomato processing capabilities in Canada. The enhancements at its Dresden plant in Ontario include software updates, the installation of a new evaporator to increase tomato paste production, and the introduction a dedicated production line for the Ro-Tel brand, which offers canned tomato.

- March 2024: Bisto launched a new gravy specifically crafted for sausages. This thicker gravy is designed to offer a savory, slightly sweet flavor that complements and enhances the meaty taste of sausages, making sausage-based dishes more flavorful.

Global Canned Food Market Report Scope

Canned food is defined as commercially sterile, shelf-stable products that are sealed hermetically in containers. This process guarantees their safety for consumption over extended periods, even without refrigeration.

The global canned food market is segmented by type into canned meat products, canned fish/seafood, canned vegetables, canned fruits, and others. Based on distribution channels, the market is segmented into supermarkets/hypermarkets, convenience/grocery stores, online retail stores, and other distribution channels. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East & Africa.

The report offers the market size and forecast of the market in value (USD) for all the above segments.

| Canned Meat and Poultry |

| Canned Fish and Seafood |

| Canned Fruits |

| Canned Vegetables |

| Other Types |

| Whole |

| Chunks/Pieces |

| Others |

| Off-Trade | Supermarkets and Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retailers | |

| Other Distribution Channels | |

| On-Trade (Food-Service/Catering) |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Russia | |

| Norway | |

| Sweden | |

| Denmark | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Malaysia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Canned Meat and Poultry | |

| Canned Fish and Seafood | ||

| Canned Fruits | ||

| Canned Vegetables | ||

| Other Types | ||

| By Form | Whole | |

| Chunks/Pieces | ||

| Others | ||

| By Distribution Channel | Off-Trade | Supermarkets and Hypermarkets |

| Convenience/Grocery Stores | ||

| Online Retailers | ||

| Other Distribution Channels | ||

| On-Trade (Food-Service/Catering) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Norway | ||

| Sweden | ||

| Denmark | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Malaysia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current canned food market size and how fast is it growing?

The canned food market size reached USD 143.96 billion in 2026 and is projected to grow at a 4.34% CAGR to USD 177.98 billion by 2031.

Which product category leads the canned food market?

Canned fish and seafood led with 33.10% canned food market share in 2025, supported by rising demand for diversified protein and premium tinned fish offerings.

Why is South America the fastest-growing region?

Economic recovery and an expanding retail base, especially in Brazil where packaged-food sales increased, underpins South America’s 7.12% CAGR outlook to 2031.

How are clean-label trends influencing the canned food industry?

Regulations such as China’s 2025 preservative ban and European consumer preference for traceable ingredients are pushing manufacturers toward lower-sodium, additive-free recipes and sustainable packaging.

Page last updated on: