Air-Dried Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 22.54 Billion |

| Market Size (2031) | USD 28.09 Billion |

| Growth Rate (2026 - 2031) | 4.87% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Air-Dried Food Market Analysis by Mordor Intelligence

The air-dried food market size is expected to grow from USD 21.6 billion in 2025 to USD 22.5 billion in 2026, and is forecast to reach USD 28.1 billion by 2031, at a 4.9% CAGR over 2026-2031. Manufacturers are increasingly replacing preservative-heavy formulations with simpler, shelf-stable, and minimally processed ingredients in snacks, soups, sauces, and meal kits. Natural Resources Institute Finland reports that in 2024, each person consumed an average of 0.6 kilograms of smoked, salted, or dried fish[1]Source: Natural Resources Institute Finland, "Consumption of Food Commodities per Capita (Kg/year)", statdb.luke.fi. This shift is largely driven by consumer demand for clean labels and stricter retailer standards on artificial additives. As a result, industrial buyers are raising ingredient specifications, driving a surge in demand for air-dried formats. The air-dried food market enjoys widespread demand across various categories and regions, making its expansion less reliant on any single product and helping to mitigate pressures from rising energy costs and trade tariffs. However, cross-border input cost pressures and a general consumer confusion between air-dried, freeze-dried, and dehydrated products are currently constraining pricing and margin performance. In response, companies are prioritizing sourcing diversification, stringent quality compliance, and clearer product positioning. This strategy not only addresses current challenges but also paves the way for growth in premium, organic, and functional formats, where supply is notably tighter.

Key Report Takeaways

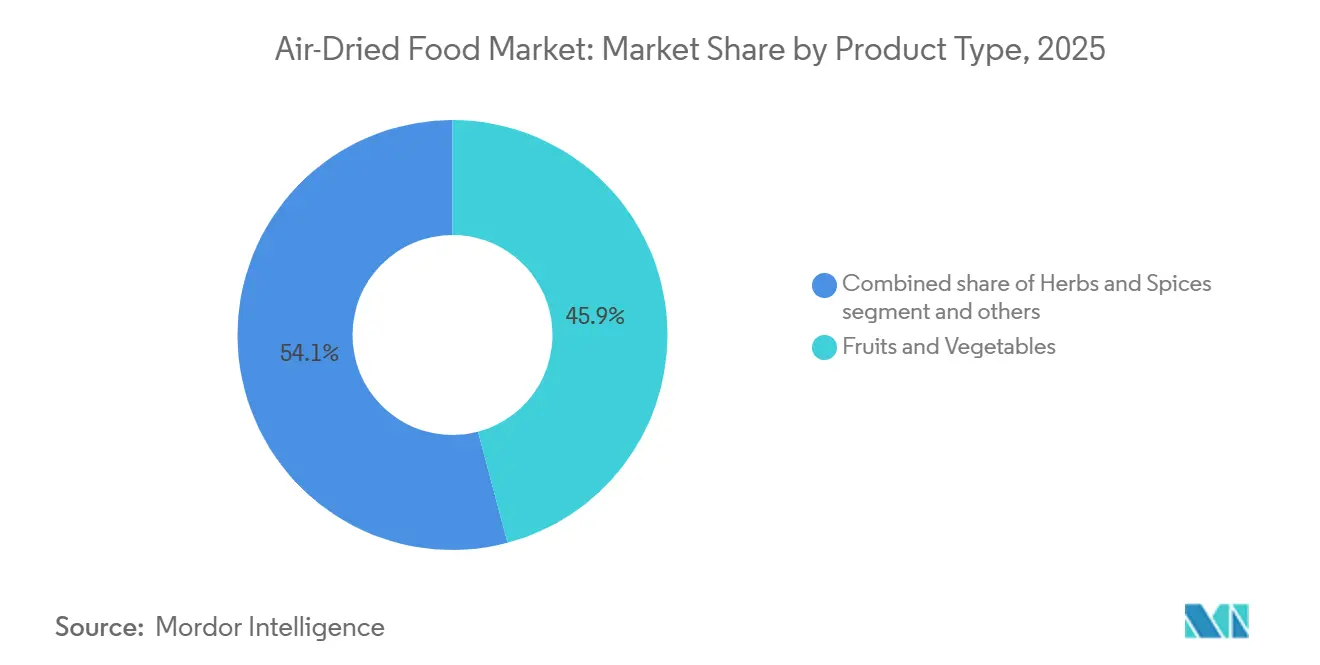

- By product type, fruits and vegetables accounted for the largest share of the air-dried food market, at 45.9% in 2025, and are projected to grow at the fastest CAGR of 5.2% during 2026-2031.

- By nature, conventional accounted for the largest share of the air-dried food market, at 86.2% in 2025, while organic is projected to grow at the fastest CAGR of 5.4% during 2026-2031.

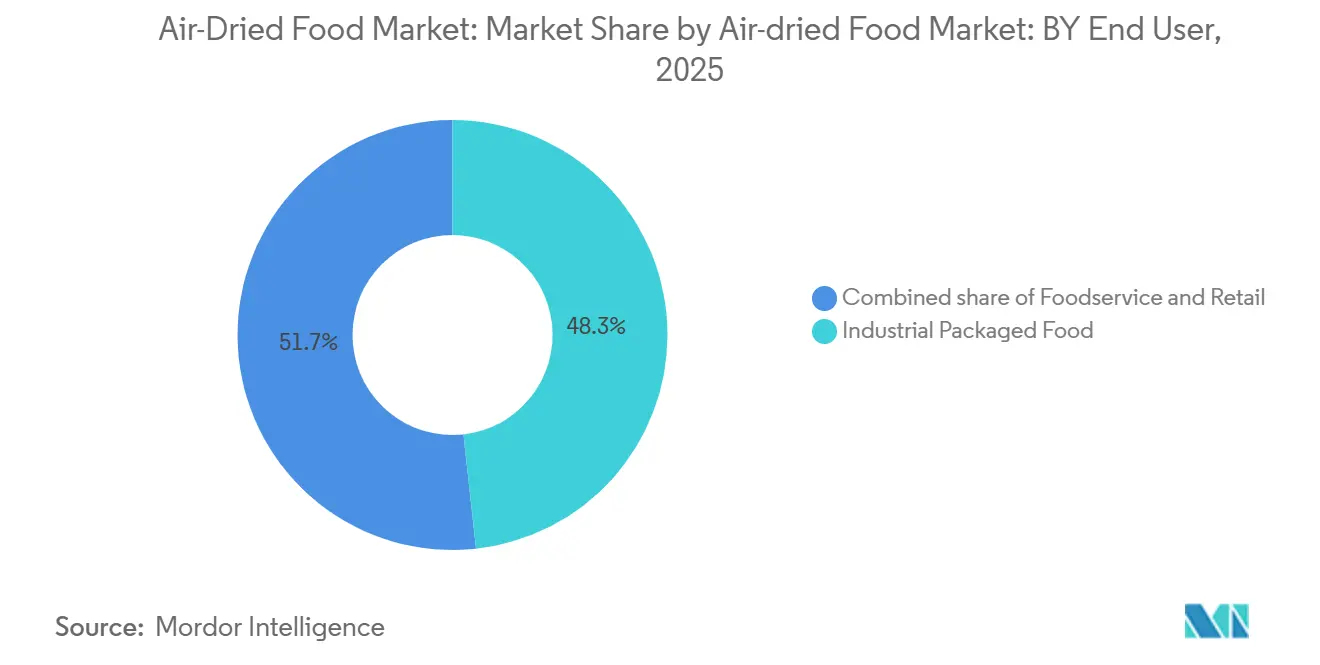

- By end user, industrial packaged food accounted for the largest share of the air-dried food market, at 48.3% in 2025, while retail is projected to grow at the fastest CAGR of 5.6% during 2026-2031.

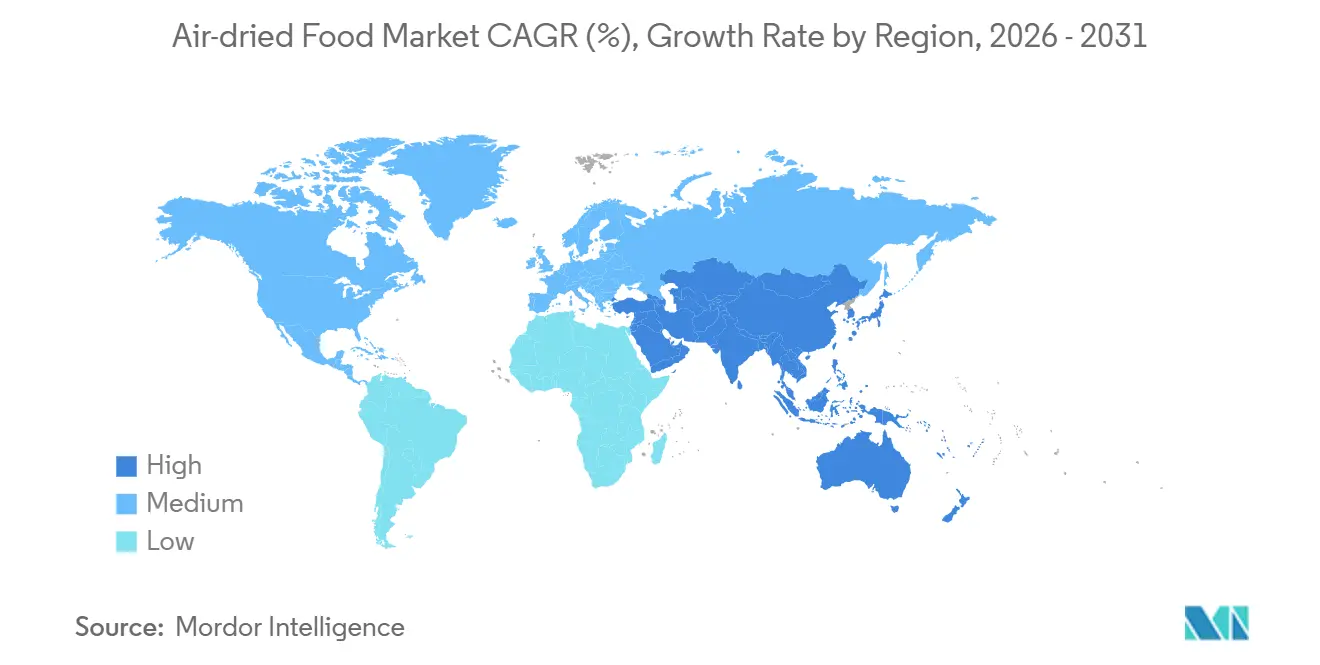

- By geography, Asia-Pacific led the market with a share of 39.7% in 2025, and is anticipated to register the fastest CAGR of 6.2% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Air-Dried Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for shelf-stable clean-label foods | +1.1% | Global, with strongest relevance in North America and Europe | Short-term (≤ 2 years) |

| Expansion of premium snack and meal kit formats | +0.8% | North America, Europe, and Asia-Pacific urban centers | Medium term (2-4 years) |

| Growth of direct-to-consumer and e-commerce food channels | +0.6% | Global, with the strongest relevance in Asia-Pacific and North America | Medium term (2-4 years) |

| Ai-enabled moisture control and quality consistency gains | +0.4% | Global, with early adoption in North America, Europe, and Japan | Long-term (≥ 4 years) |

| Solar-thermal and low-carbon drying adoption in emerging plants | +0.3% | Sub-Saharan Africa, South Asia, Southeast Asia, and South America | Long-term (≥ 4 years) |

| Air-dried pet food premiumization and humanization spillover | +0.4% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising demand for shelf-stable clean-label foods

Snacks, soups, and meal kit manufacturers are increasingly shunning artificial preservatives, turning instead to air-dried ingredients. These ingredients bolster shelf life without the stigma of heavy processing. According to the 2025 Food and Health Survey by the International Food Information Council, over 24% of U.S. shoppers are on the hunt for natural ingredients[2]Source: International Trade Center, "Value of fired vegetables imported to the United Kingdom", trademap.org. This growing preference is influencing retailer listing mandates. Industrial procurement is reflecting this trend, with major food corporations embedding preservative-free stipulations in their supplier specifications, moving beyond viewing clean labels as mere branding. Furthermore, the value of low-moisture foods is underscored in areas with inconsistent cold-chain access[3]Source: Food and Agriculture Organization, “Sustainable Food Cold Chains”, fao.org. These foods cater to both premium consumer products and supply chains prioritizing shelf stability. Given the rising emphasis on traceability and preventive controls, well-documented air-dried ingredients are gaining traction. Their documentation not only positions them as compliance assets but also bolsters product claims.

AI-enabled moisture control and quality consistency gains

Moisture variability has long posed challenges in the air-dried food market, impacting reject rates, rehydration quality, and contract adherence. A study published in Foods in January 2026 highlighted the efficacy of a CNN-LSTM-MHA model, which achieved moisture prediction variance of under 2% during the convective drying of yuba. This model outperformed traditional control methods, especially under delayed and nonlinear drying conditions. For suppliers, such precision translates to reduced defect rates, minimized energy waste from over-drying, and enhanced alignment with buyer specifications. Supporting this trend, a 2025 review in Applied Food Research underscored the industrial viability of modular AI retrofits. These retrofits enable online monitoring, dynamic prediction, and intelligent control on pre-existing dryer infrastructures. Such advancements offer smaller specialist suppliers a tangible edge, allowing them to safeguard supply agreements in the air-dried food market, even as they focus on a narrow yet premium product range.

Air-dried pet food premiumization and humanization spillover

Expanding its drying capacity, the air-dried pet food segment is now also catering to human food applications. This dual focus not only enhances the air-dried food market's equipment and ingredient sourcing but also enriches its process expertise. According to APPA, in 2024, 94 million U.S. households had pets, underscoring the momentum behind premium pet feeding trends and their influence on new product investments. This shift in format is prompting companies to adopt shared production lines and dual-purpose sourcing for both pet and human-grade formulations, sidestepping the need for entirely separate systems. At the 2026 Global Pet Expo, brands like Open Farm, Winnie Lou, and Earth Animal unveiled new air-dried complete diets, toppers, and novel protein formats. Their offerings indicate a significant shift: air-dried formats are transitioning from mere treats to staples in daily feeding. This evolution not only broadens the buyer base for processors in the air-dried food market but also diminishes reliance on a singular customer group or end use.

Growth of direct-to-consumer and e-commerce food channels

Direct-to-consumer channels are steering the air-dried food market away from commodity pricing and towards premium branded sales. Subscription-based e-commerce thrives with ambient products, as consumers find it easier to make repeat purchases without the need for cold storage or urgent replenishment. In the Asia-Pacific region, this advantage is pronounced. Urban consumers in Japan and South Korea are already leveraging direct-order channels for premium snacks and ingredients, bolstered by ongoing urban growth. This shift is also granting shelf access to brands that initially cultivated demand online and are now transitioning to physical retail with a pronounced premium stance. As the channel mix evolves, air-dried food suppliers without a brand presence may face greater pricing pressures than their brand-recognized counterparts.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High energy intensity in thermal drying operations | -0.8% | Global, with strongest effect in energy-import-dependent markets in South Asia and MEA | Short term (≤ 2 years) |

| Quality variability from raw material moisture and size differences | -0.6% | Global, with strongest effect in emerging sourcing hubs in Sub-Saharan Africa and South Asia | Medium term (2-4 years) |

| Trade tariffs and cross-border input cost pressure | -0.5% | North America and Europe, with spillover into Asia-Pacific export corridors | Short term (≤ 2 years) |

| Consumer confusion between air-dried, freeze-dried, and dehydrated foods | -0.3% | North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High energy intensity in thermal drying operations

Energy is the predominant controllable expense in the air-dried food market, influencing both profit margins and the pace of new capacity investments. Research published in Food Engineering Reviews reveals that conventional hot-air drying dominates, accounting for over 75% of global industrial food drying processes. Furthermore, they linked the drying process to 15% of the sector's total CO2-equivalent emissions. In regions grappling with unstable power grids and reliance on imported fuels, the cost of producing a kilogram of dried output surges beyond initial projections, placing smaller processors at a competitive disadvantage. A 2026 Horizon-backed EDDY project, showcased on Zenodo, highlighted the potential of advanced sensing and modeling in slashing drying energy demands by up to 60%. However, it also underscored the significant gap for many mid-scale operators, who, tethered to traditional methods, lag far behind this energy-efficient benchmark.

Trade tariffs and cross-border input cost pressure

Trade policies are creating cost uncertainties in the air-dried food market, particularly for manufacturers reliant on dried vegetables, herbs, and spices sourced from Asia. A draft analysis indicated that tariff collections on food items, later exempted, surged to USD 1.5 billion in the first four months of 2025, a significant increase from 2024. This underscores the swift impact of policy changes on landed costs. In October 2025, McCormick’s management noted that while they had taken mitigation actions, these were not permanent solutions. They emphasized that 2026 would necessitate further sourcing adjustments, productivity enhancements, and pricing strategies to counteract lingering tariff impacts. Processors relying on Chinese-sourced garlic, onions, bell peppers, and specialty fruits face continued pressure on gross margins. This is largely due to the 6 to 12-month qualification period for alternative suppliers. Consequently, air-dried food companies are diversifying their supply chains by establishing parallel corridors in India, Mexico, and Eastern Europe, rather than relying on a single source.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fruits and Vegetables Lead the Category and Also Set the Growth Pace

In 2025, Fruits and Vegetables commanded a dominant 45.9% share of the air-dried food market, establishing themselves as the primary volume base for both industrial ingredients and consumer snacks. This prominence stems from robust demand by manufacturers of soups, meal kits, and sauces, all seeking shelf-stable ingredients with simplified label profiles. Additionally, the segment reaps benefits from branded snack launches centered on single-ingredient fruit and vegetable products, catering to both bulk procurement and premium retail markets. A 2026 review in Food Control highlighted that AI-integrated drying systems enhance the retention of bioactive compounds, like anthocyanins and ascorbic acid, in blueberries, bolstering their nutritional appeal in specialty channels.

Forecasted to expand at a brisk 5.2% CAGR through 2031, Fruits and Vegetables not only dominate the current air-dried food market but also lead its future growth trajectory. This expansion is bolstered by AI-driven moisture control, especially crucial as fresh produce enters the drying phase with moisture levels that are often higher and more variable than those of herbs or processed meats. Processors with diverse supply networks spanning India, Turkey, Eastern Europe, and China can better navigate disruptions—be it from tariffs or weather—ensuring consistent throughput and pricing. Thus, the segment stands out as the primary growth engine and the largest revenue source in the air-dried food industry.

By Nature: Conventional Holds Scale While Organic Expands Faster

In 2025, Conventional dominated the air-dried food market with an 86.2% share, underscoring the market's reliance on large industrial buyers. These buyers prioritize supply continuity and cost stability over certification premiums. This dominance is bolstered by procurement models in packaged food manufacturing, where consistent availability often trumps premium claims for many high-volume SKUs. The segment's structural stability stems from its alignment with long-term ingredient contracts, allowing it to absorb large order volumes without the certification bottlenecks that challenge smaller supply pools. However, this dominance doesn't preclude a shift in the product mix. Many brand owners are now adopting dual sourcing strategies, incorporating certified inputs for select premium lines.

Organic is set to grow at a 5.4% CAGR through 2031, marking it as the fastest-growing segment in the air-dried food market. This surge is driven by cleaner portfolio extensions, retailer demands for additive-free ranges, and a push for premium shelf positioning in Japan and other organized grocery markets. Stringent regulations, like USDA organic rules and the updated EU organic regulation, mandate chain-wide certification from farm to processing. This not only limits the pool of qualified suppliers but also elevates prices for compliant producers. Consequently, while Organic emerges as a rapidly growing niche in the air-dried food industry, its ascent is tempered by supply constraints and certification lead times, which slow its race to close the gap with Conventional.

By End User Application: Industrial Packaged Food Drives Scale While Retail Delivers Faster Growth

In 2025, Industrial Packaged Food claimed a dominant 48.3% share, establishing itself as the leading end-user in the air-dried food market. This dominance stems from long-term agreements with producers of soups, sauces, instant noodles, and meal kits, all of whom prioritize shelf-stable components of consistent quality. Following closely is the foodservice sector, which values concentrated dried herbs and vegetables for their ability to streamline preparation and ensure menu consistency. This diverse application base provides the market with a stable demand foundation, even amidst pricing pressures on premium consumer formats.

Retail is projected to grow the fastest, with a 5.6% CAGR through 2031. This surge is buoyed by the expansion of specialty retail and increased online access to air-dried products. While supermarkets and hypermarkets dominate in volume due to the cost advantages of ambient storage over fresh alternatives, specialty and convenience stores are carving out a niche. They're elevating air-dried products through a focus on premium nutrition and protein-centric snack launches. A testament to this trend is Jack Link’s March 2026 debut of a 3-ingredient air-dried beef slice line, strategically rolled out across U.S. convenience and grocery channels. This move underscores how industry giants are leveraging air-drying to penetrate the lucrative transparent-label retail market, commanding a higher value per serving.

Geography Analysis

In 2025, Asia-Pacific commanded a dominant 39.7% share of the air-dried food market, solidifying its status as the largest regional segment. China stands as the primary processing hub, with its dehydrated ingredients bolstering both regional trade and extensive export activities. Meanwhile, Vietnam is amplifying this momentum, driven by heightened intra-Asia-Pacific demand. This shift is deepening the region's internal trade, moving it away from a sole reliance on Western demand cycles. The region's vast population, coupled with an increasing preference for shelf-stable convenience foods, continues to fuel robust demand for air-dried foods.

Looking ahead, Asia-Pacific is projected to lead with a robust 6.2% CAGR through 2031, underscoring its accelerated growth compared to other regions. Within the Asia-Pacific region, India emerges as the fastest-growing market. The urban middle class's rising spending power and the accessibility of online grocery platforms are broadening the reach of premium air-dried products, extending their appeal beyond just major metropolitan areas. Countries like Japan, South Korea, and Singapore are becoming pivotal demand centers, with direct-order e-commerce playing a crucial role in promoting premium snacks and ingredients. Furthermore, the United Nations anticipates a significant urban expansion in Asia, projecting an increase of 1.2 billion in the region's urban population by 2050, further bolstering this trend.

North America and Europe, being mature markets for air-dried foods, set stringent quality benchmarks. Here, clean-label standards, stringent food safety controls, and ingredient transparency are paramount. In North America, the emphasis on high specifications means that traceability and validated food safety systems are crucial for suppliers aiming for long-term contracts. Europe’s focus is concentrated in countries like Germany, the UK, Italy, France, and the Netherlands, where there's a well-established demand for premium snacks, soup mixes, and foodservice ingredients. South America, with nations such as Brazil, Argentina, Colombia, and Peru, is entering an earlier growth phase, driven by urban dietary shifts and an expanding modern retail landscape. In the Middle East and Africa, while the GCC stands out as the premier demand center, production capabilities are being bolstered. Initiatives like AfricaRice’s solar-gas hybrid dryer workshop, set to span 8 African countries in November 2025, highlight the continent's push to strengthen its production capacity.

Competitive Landscape

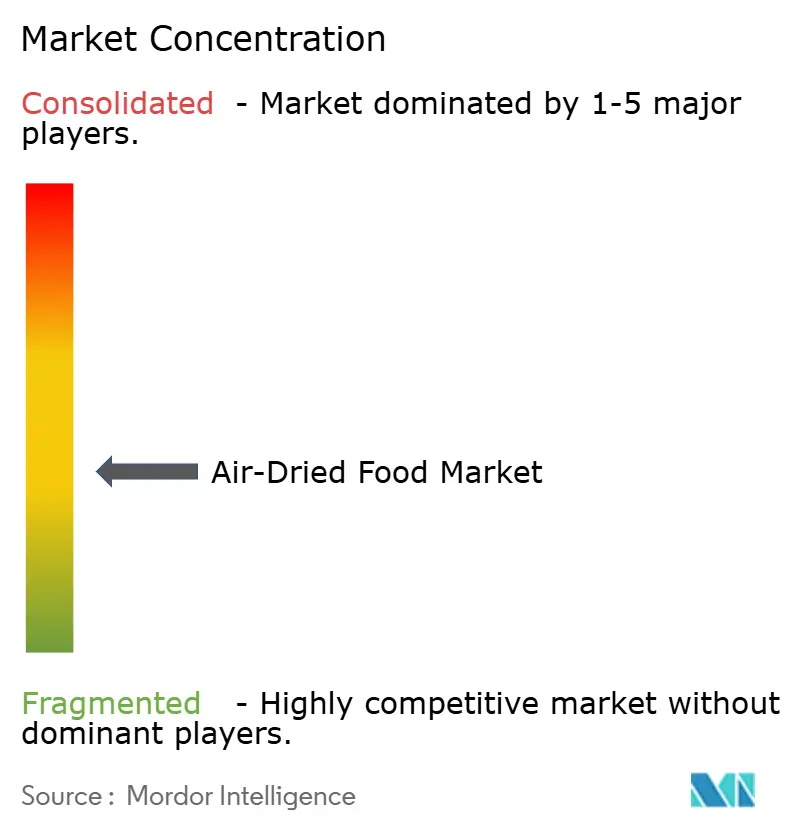

The air-dried food market remains fragmented, so competition is shaped by a mix of scale-driven sourcing strength and specialist-quality positioning rather than by a single dominant supplier. Major players like Nestlé, PepsiCo, Conagra Brands, and General Mills leverage their expansive portfolios and established channel relationships to dominate the industrial packaged food and mass retail sectors. Meanwhile, specialist suppliers such as Van Drunen Farms, BCFoods, and Silva International carve out their niche by emphasizing traceability, food safety validation, and ingredient consistency. In 2025, BCFoods bolstered its standing by integrating Culinary Farms and achieving a 5-log microbial reduction validation at its Linxi garlic plant, aligning more closely with the sourcing standards of major U.S. retailers and consumer packaged goods (CPG) companies.

There's a notable emphasis on organic certification, process transparency, and small-batch customization, especially for premium foodservice and specialty retail buyers. Technology is emerging as a significant differentiator; for instance, AI-driven moisture control is enhancing quality consistency and minimizing waste for early adopters. Research in 2026 highlighted that hybrid ultrasonic-convective dryer systems could boost energy efficiency by 35% and cut drying time by 41% compared to traditional hot-air systems. If these findings hold in commercial applications, they could significantly enhance unit economics. Such advancements are crucial in the air-dried food market, where smaller operators seek process advantages to compete with larger firms that benefit from lower procurement costs.

As a result, competitive strategies in the air-dried food market are evolving in three interconnected ways: broadening ingredient scopes, enhancing compliance documentation, and sharpening premium positioning. Companies diversifying their sourcing from regions such as India, Mexico, Eastern Europe, and China are better equipped to navigate tariff disruptions and maintain supply continuity. Retail-oriented players are gaining traction, as branded snack and protein products often yield higher margins than bulk ingredient contracts. In 2026, Jack Link’s capitalized on this trend with the launch of a clean-label air-dried beef product, while BCFoods deepened its industrial supply credibility through strategic portfolio integration and plant validation. This dynamic landscape allows both large incumbents and specialized processors to thrive, provided they balance cost control with dependable documentation and superior product quality.

Air-Dried Food Industry Leaders

-

Nestlé S.A.

-

PepsiCo, Inc.

-

Unilever PLC

-

General Mills, Inc.

-

Kerry Group plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Jack Link's, under its clean-label initiative, debuted a new line of air-dried beef slices made with just three ingredients. These 2-ounce bags are now available in convenience stores, grocery outlets, and various retail channels across the U.S. Each serving boasts 31 grams of protein and is free from artificial preservatives. The company has plans to introduce multipacks, sticks, and steaks, all featuring similarly minimal ingredient profiles, in late 2026.

- September 2025: BCFoods' Linxi manufacturing plant has validated a 5-log microbial reduction for its garlic operations. This achievement underscores the plant's FSMA-compatible pathogen reduction capability, making it eligible for key supplier programs of several major US retailers and CPG manufacturers. As a result, BCFoods bolsters its competitive stance in North America's ingredient supply market.

- May 2025: Silva International is ramping up its focus on air-dried vegetables. The company is enhancing consistency and shelf stability in its green bean and related ingredient lines. This move is in response to the rising demand from plant-based food manufacturers seeking dependable, specification-stable dried ingredients.

- February 2025: BCFoods has fully integrated its subsidiary, Culinary Farms, into its brand. This move not only expands BCFoods' portfolio to encompass premium dried tomatoes, chiles, seasonings, spice blends, and smoked ingredients but also streamlines operational and supply chain resources. As a result, BCFoods aims to enhance service reliability and diversify its offerings to the industrial packaged food and premium foodservice segments on a global scale.

Global Air-Dried Food Market Report Scope

| Fruits and Vegetables |

| Herbs and Spices |

| Meat and Seafood |

| Other Products |

| Conventional |

| Organic |

| Industrial Packaged Food | |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Specialty Stores | |

| Convenience Stores | |

| Online Retail Stores | |

| Other Retail Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Belgium | |

| Sweden | |

| Poland | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Morocco | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa |

| By Product Type | Fruits and Vegetables | |

| Herbs and Spices | ||

| Meat and Seafood | ||

| Other Products | ||

| By Nature | Conventional | |

| Organic | ||

| By End User Application | Industrial Packaged Food | |

| Foodservice | ||

| Retail | Supermarkets/Hypermarkets | |

| Specialty Stores | ||

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Retail Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Belgium | ||

| Sweden | ||

| Poland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Morocco | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and outlook for air dried food demand?

The air-dried food market was valued at USD 21.6 billion in 2025, stands at USD 22.5 billion in 2026, and is forecast to reach USD 28.1 billion by 2031 at a 4.9% CAGR.

Which product segment leads this space?

Fruits and Vegetables led with 45.9% share in 2025 and are also projected to grow at the fastest 5.2% CAGR through 2031.

Why are clean-label products supporting growth?

Manufacturers and retailers are pushing for fewer artificial additives, and this is improving demand for shelf-stable ingredients that can support cleaner labels without losing functionality.

Which end-user channel is expanding the fastest?

Asia-Pacific is the largest region with 39.7% share in 2025 and also the fastest-growing one at 6.2% CAGR through 2031.

Page last updated on: