Microalgae-Based Aquafeed Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 320.08 Billion |

| Market Size (2031) | USD 481.29 Billion |

| Growth Rate (2026 - 2031) | 8.50% CAGR |

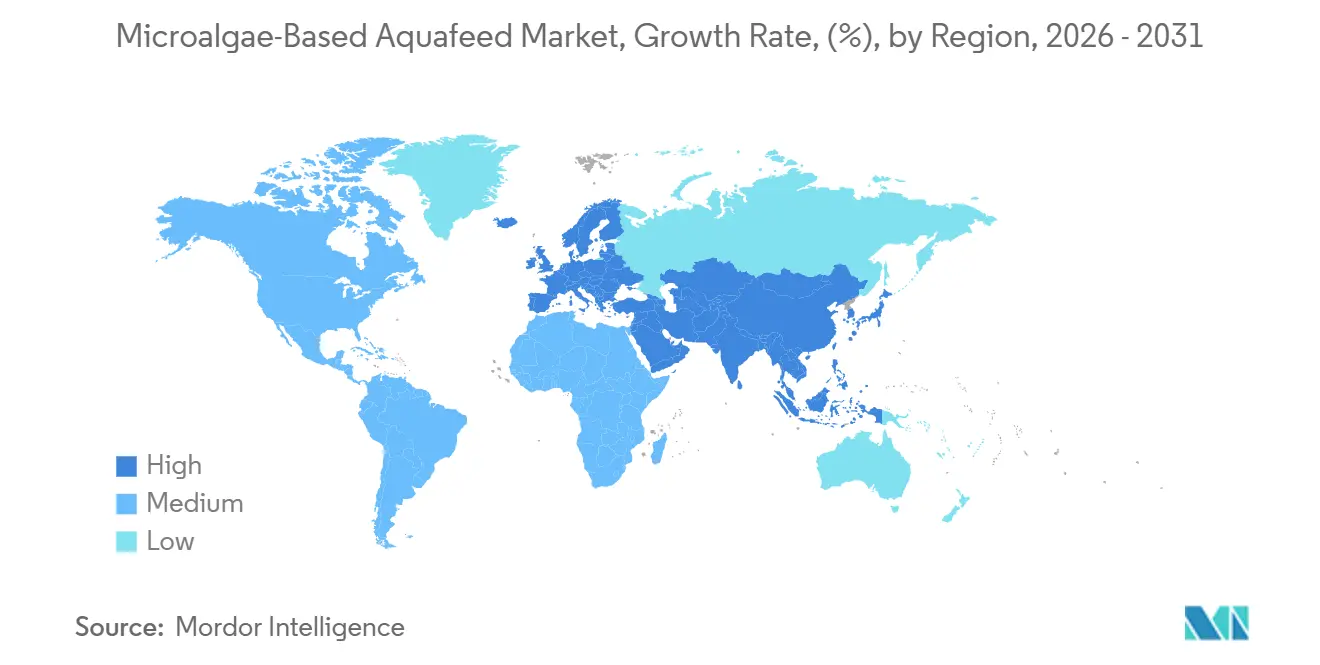

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

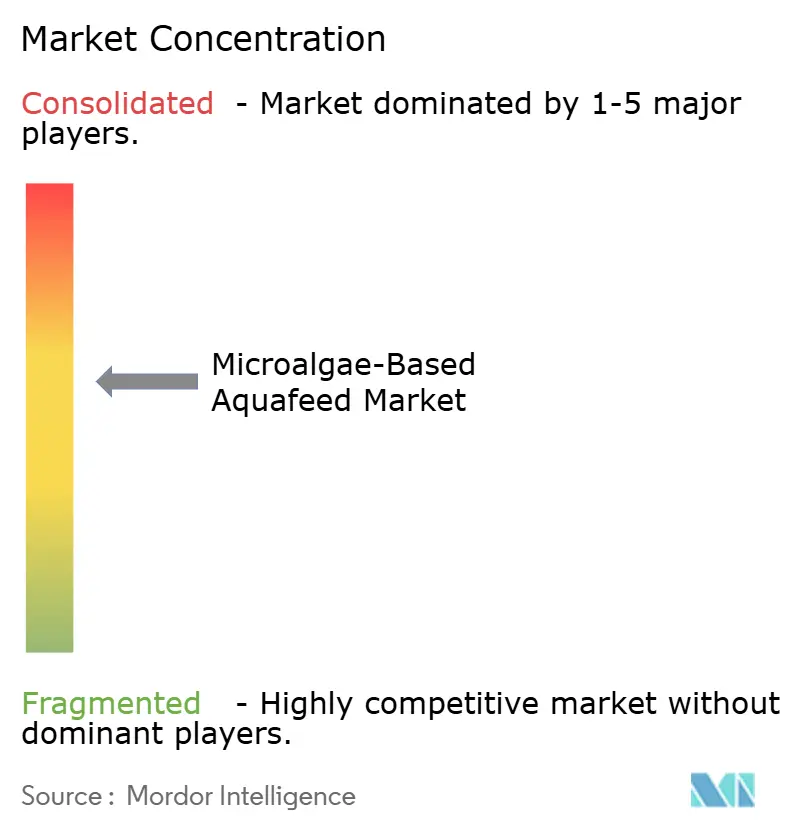

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Microalgae-Based Aquafeed Market Analysis by Mordor Intelligence

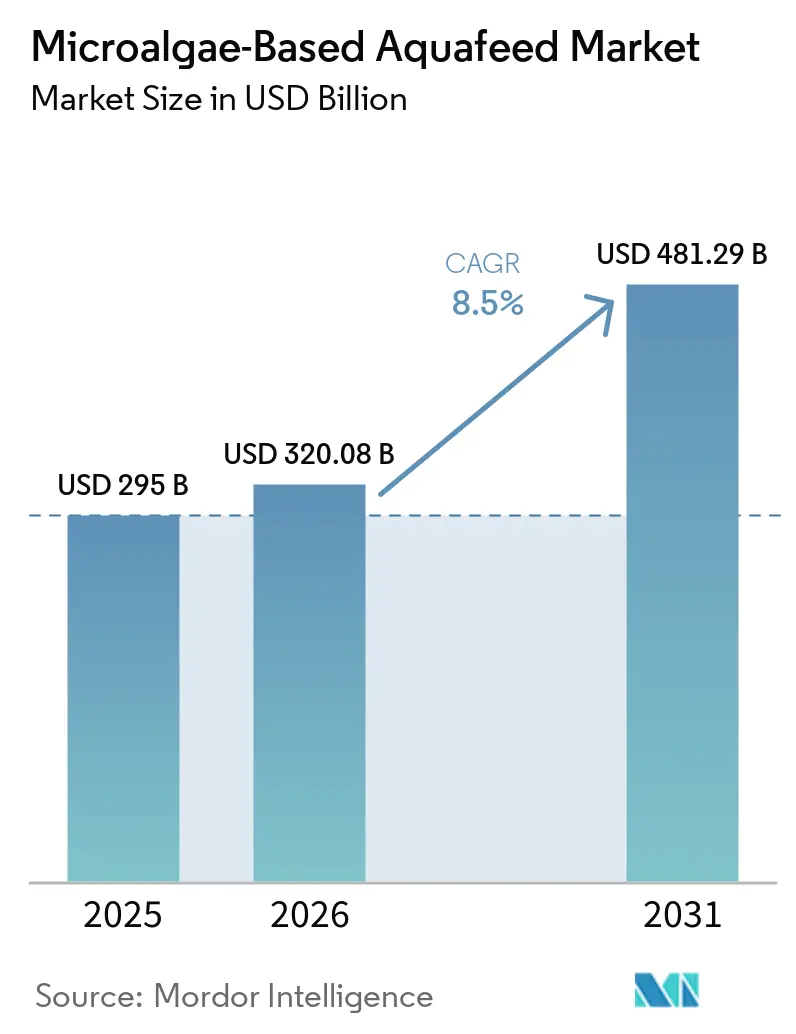

The microalgae-based aquafeed market size is anticipated to expand from USD 295 million in 2025 and USD 320.08 million in 2026 to USD 481.29 million by 2031, registering a 8.5% CAGR between 2026 to 2031. Growing pressure on fishmeal quotas, retailer sustainability mandates, and traceability standards is steering feed formulators toward algal ingredients that deliver consistent omega-3 profiles and immune-modulating bioactives without drawing on wild forage stocks. Europe led 2025 revenue as Norwegian and Danish salmon producers replaced fish oil with algal oils to comply with Marine Stewardship Council requirements and capture antibiotic-free price premiums. Asia-Pacific is set for the fastest regional expansion as India’s 2024-25 zero-tariff policy on algal oil and China’s five-year alternative-protein incentives lower landed costs and encourage large shrimp and carp farms to trial algae-rich diets. Product innovation is accelerating, resulting in a larger share of demand for algal oil, yet protein isolates segment is growing fast as shrimp hatcheries adopt high-protein concentrates that improve larval survival and growth. Meanwhile, photobioreactor efficiencies and higher fishmeal’s higher prices are narrowing the historical cost gap and strengthening the commercial case for microalgae inclusion.

Key Report Takeaways

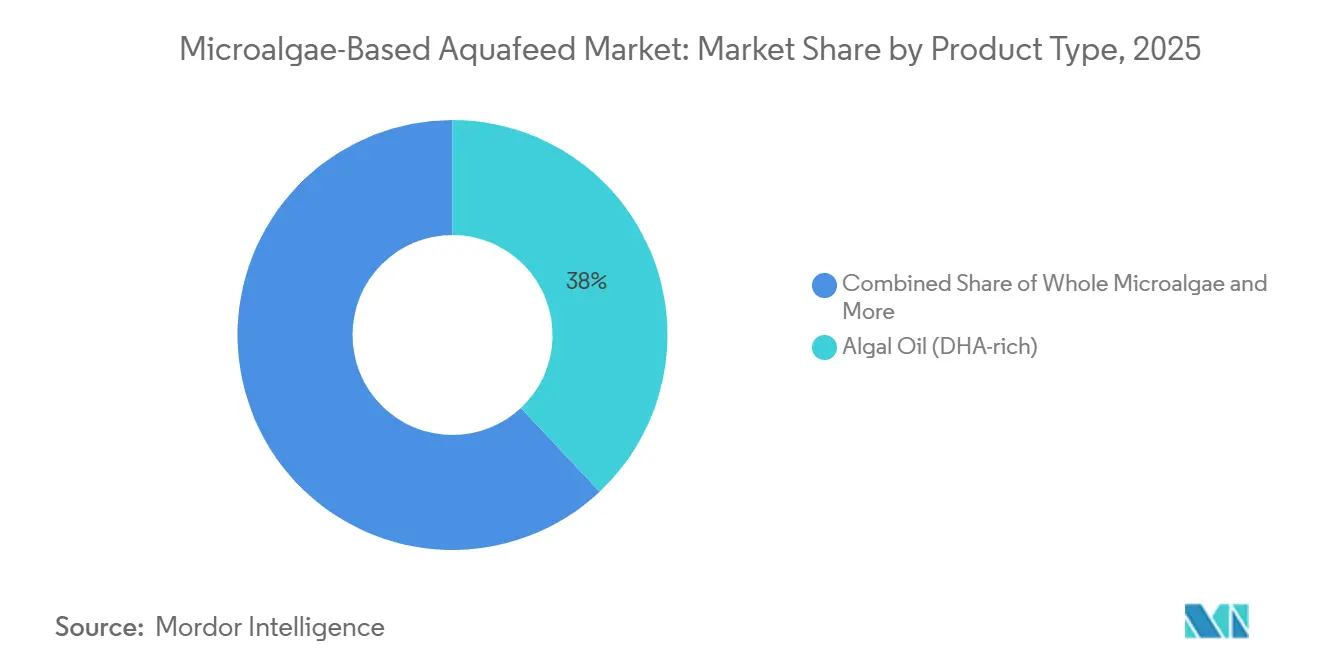

- By product type, algal oil held the largest share with 38.0% of the microalgae-based aquafeed market share in 2025, while protein isolates are projected to expand at fastest 13.5% CAGR during 2026-2031.

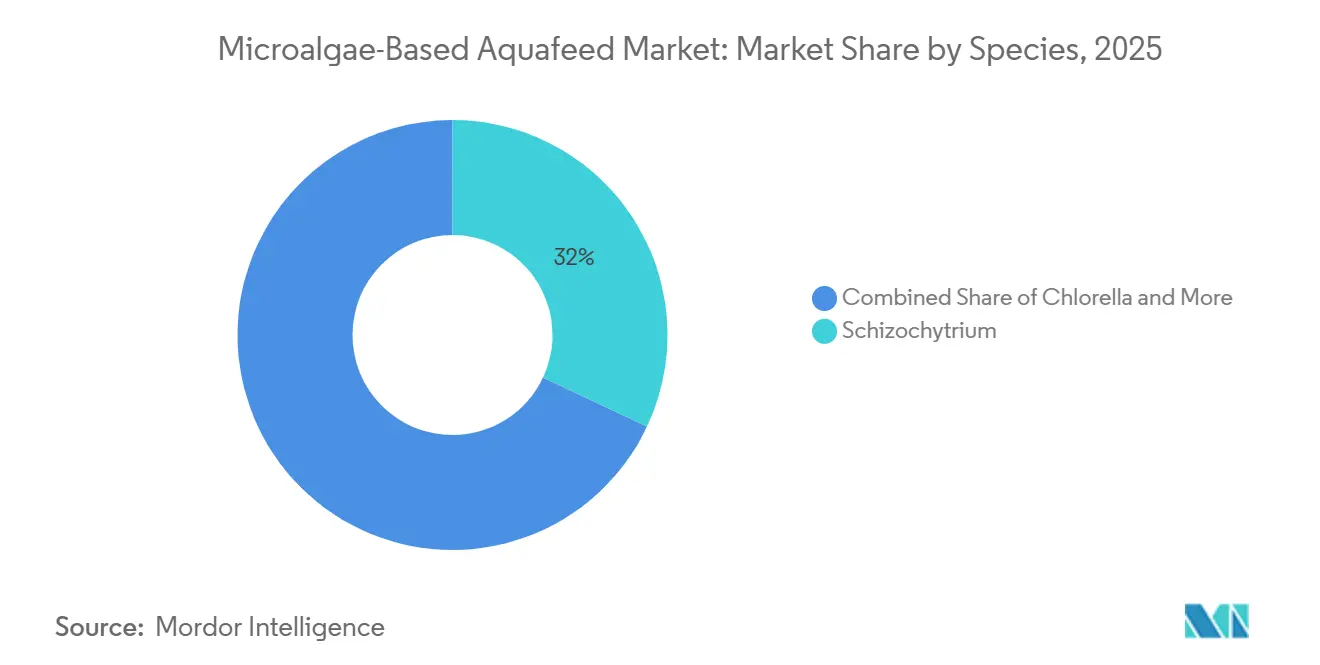

- By species, Schizochytrium occupied the largest 32.0% share of the microalgae-based aquafeed market size in 2025, whereas Nannochloropsis is forecast to post the fastest 14.0% CAGR through 2026-2031.

- By geography, Europe dominated with the largest 35.5% share of the microalgae-based aquafeed market share in 2025, while Asia-Pacific is anticipated to record a fastest 10.7% CAGR through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Microalgae-Based Aquafeed Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid cost decline in closed-photobioreactor farming | +4.2% | Global, with early adoption in Europe and North America | Medium term (2-4 years) |

| Premium pricing opportunity for antibiotic-free seafood | +3.8% | Europe, North America, Japan | Short term (≤2 years) |

| Corporate net-zero pledges are accelerating algae inclusion | +3.5% | Global, led by Europe and North America | Medium term (2-4 years) |

| Regenerative aquaculture certifications are emerging | +2.1% | Europe, North America, Australia, and New Zealand | Long term (≥4 years) |

| Carbon-credit monetization for algae feed plants | +1.9% | Europe, the Middle East, and North America | Long term (≥4 years) |

| Marine ingredient supply volatility post-2025 El Niño events | +3.2% | Global, with an acute impact in South America and the Asia-Pacific | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rapid Cost Decline in Closed-Photobioreactor Farming

Closed photobioreactors are cutting operating expenses below USD 3 per kilogram of dry biomass, closing the historical gap with fishmeal and spurring wider use of algae in premium salmon and shrimp feeds. Algiecel secured DKK 50 million (USD 6.7 million) in 2024 to deploy modular units at industrial emission points, demonstrating the scalability of mobile systems that capture waste carbon dioxide at source. Lifecycle analyses indicate Spirulina production costs could fall to USD 1.30 per kilogram at full scale, positioning algae near price parity with fishmeal as long as spot prices stay above USD 1,700 per metric ton. The closed-system design also eliminates contamination from mycotoxins and heavy metals, a key requirement for premium formulations in the microalgae-based aquafeed market. Regulators such as the United States Food and Drug Administration and the European Food Safety Authority favor photobioreactor-grown strains for their traceability, shortening approval times versus open-pond alternatives.

Premium Pricing Opportunity for Antibiotic-Free Seafood

Retailers in Europe and North America pay double-digit premiums for antibiotic-free salmon and shrimp, giving farmers a direct economic incentive to adopt immune-boosting algal ingredients. The Veramaris Big Data Chile study 2026 study covering 143 million Chilean salmon showed diets containing at least 7.2% combined eicosapentaenoic acid and docosahexaenoic acid improved feed conversion ratios and cut quality downgrades by up to 100%, reinforcing the cost–benefit case for algae inclusion. Trials with Microchloropsis gaditana increased fillet omega-3 content by 23% and reduced bacterial infections by 85.68%, demonstrably lowering antibiotic use. Similar effects were observed in shrimp, where Spirulina at 10% inclusion increased final weight to 10.82 grams and halved Vibrio mortality, demonstrating that microalgae-based aquafeed market solutions can drive both health and financial gains. As consumer awareness continues to rise, antibiotic-free labeling is moving from a differentiator to a prerequisite in premium channels, cementing algae’s role in high-value aquaculture.

Corporate Net-Zero Pledges are Accelerating Algae Inclusion

Feed buyers face mounting scrutiny over Scope 3 emissions, encouraging the switch from fishmeal to microalgae that cuts 1.5-2.0 metric tons of carbon dioxide equivalents per metric ton replaced. BioMar Group purchased the LetSea research center in 2025 to develop net-zero diets and aims to phase out marine ingredients in European seabass and gilthead seabream feeds by 2028. Industrial carbon-capture projects in Norway sequester 300,000 metric tons of carbon dioxide annually to cultivate algae for salmon feed, and associated carbon-credit revenue offsets 10-15% of biomass production costs. Lenders and investors are beginning to price carbon exposure into capital costs, so adopters of algae-rich feeds gain preferential financing, reinforcing demand within the microalgae-based aquafeed market.

Regenerative Aquaculture Certifications are Emerging

New labels that require nutrient circularity and ecosystem restoration, such as Seaforest, demand verifiable algae inputs to demonstrate closed-loop nutrient management. The European Union-funded ALLIANCE project (2025-2029) is building integrated microalgae biorefineries that treat aquaculture wastewater while producing feed-grade biomass, directly linking compliance with effluent limits to algae adoption. King Abdullah University of Science and Technology operates a 42,000-square-meter facility cultivating seawater-adapted Spirulina and Chlorella, capturing 1.8 kilograms of carbon dioxide per kilogram of biomass, and illustrating the regenerative model’s scalability[1]Source: King Abdullah University of Science and Technology, “KAUST Biotechnology Solution Could Be Key to Unlocking Saudi Food Security,” KAUST, kaust.edu.sa. Early adopters in Australia and New Zealand leverage regenerative certification to access premium markets in Japan and South Korea, where consumers reward restorative farming. Because no single global standard exists, producers investing now in traceability systems and lifecycle data build first-mover credibility in the evolving microalgae-based aquafeed market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price gap versus fishmeal persists in developing nations | -2.8% | Asia-Pacific (excluding Japan), South America, Africa | Short term (≤2 years) |

| Regulatory approval lag for novel algae strains | -1.6% | Global, with acute impact in Europe and North America | Medium term (2-4 years) |

| Mycotoxin and heavy-metal contamination risk | -1.2% | Asia-Pacific, Africa, South America | Medium term (2-4 years) |

| Public perception of "genetically edited" algal feeds | -0.9% | Europe, Japan, South Korea | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Regulatory Approval Lag for Novel Algae Strains

The United States Food and Drug Administration's Generally Recognized as Safe pathway and the European Union's Novel Food regulation can add 2-3 years and significant documentation costs before the commercial launch of new strains[2]Source: European Food Safety Authority, “Homepage,” European Food Safety Authority, efsa.europa.eu . This delay is acute for CRISPR-edited high-EPA algae that offer superior lipid profiles yet face stricter scrutiny, especially in Europe and Japan, where public skepticism toward gene editing persists. Companies such as KnipBio secured United States and Canadian approvals for bacterial biomass in 2025 but still await European clearance, limiting scale-up across the microalgae-based aquafeed market. Regulatory fragmentation forces producers to maintain separate production lines, duplicating costs and slowing global rollouts. Lack of harmonization under Codex Alimentarius keeps the approval lag a structural restraint in the medium term.

Public Perception of Genetically Edited Algal Feeds

European Commission’s consumer surveys in 2024 showed that 42% of Europeans would avoid seafood fed with gene-edited ingredients, signaling a reputational risk for farmers using CRISPR-modified algae[3]Source: European Commission, “Homepage,” European Commission, ec.europa.eu . Japan enforces labeling requirements for gene-edited feed components, complicating supply chains and potentially stigmatizing end products. In contrast, the United States market is more accepting, but global brands must harmonize labeling and cannot ignore perception hotspots. Large producers such as Veramaris deliberately avoid gene editing to sidestep controversy, but that strategy caps performance potential relative to engineered strains. Unless transparent communication campaigns shift public opinion, consumer resistance will remain an overhang on the microalgae-based aquafeed market, especially in premium retail channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Protein Isolates Emerging as Fastest Segment

Algal oil held the largest 38.0% share of the microalgae-based aquafeed market in 2025, as salmon producers rely on its stable docosahexaenoic acid profile to secure premium fillet pricing. In contrast, protein isolates are the fastest segment and are projected to grow at a 13.5% CAGR during 2026-2031 as shrimp hatcheries in Thailand, Ecuador, and India replace fishmeal with high-protein concentrates that lift larval survival. The microalgae-based aquafeed market size for isolates is expanding further as the United States Food and Drug Administration's Generally Recognized as Safe rules and the European Union's Novel Food reviews favor standardized compositions that streamline safety checks. Cost declines in closed photobioreactors and the ability to monetize carbon credits narrow the price gap with fishmeal, reinforcing the adoption of the fastest segment.

Whole microalgae and algal meal occupy niche positions that deliver pigmentation and immune benefits to tilapia and ornamental fish at 5-15% inclusion, even when cell wall barriers reduce digestibility. Algal oil is still forecast to grow at a solid CAGR through 2031 as multi-year supply contracts ensure steady demand in premium salmon and marine finfish feeds. Multi-functional oils, such as the Omega Origins launched by Fermentalg in 2026, contain 40% eicosapentaenoic acid and 20% docosahexaenoic acid. These oils reduce post-processing steps and lower finished-feed costs. Producers that can co-cultivate multiple strains inside modular systems gain flexibility to supply blended ingredients that meet diverse nutrient targets across the remaining segments.

By Species: Schizochytrium Retains Largest Share While Nannochloropsis Is Fastest Rising

Schizochytrium delivered the largest 32.0% microalgae-based aquafeed market share in 2025 because its high docosahexaenoic acid content and fermentation consistency meet premium salmon specifications. Nannochloropsis is the fastest-growing species segment and is projected to expand at a 14.0% CAGR over 2026-2031, following rainbow trout trials that confirmed full fishmeal replacement with equal growth and up to 40% lower phosphorus discharge. Declining photobioreactor costs and the environmental bonus of displacing as much as 2 metric tons of carbon dioxide equivalents per metric ton of fishmeal reinforce demand for Nannochloropsis. Feed formulators increasingly combine the largest and fastest strains to balance docosahexaenoic acid and eicosapentaenoic acid in a single pellet, streamlining logistics in a tightening sustainability landscape.

Spirulina is experiencing steady growth, valued for its pigmentation properties and immune support benefits in shrimp and tilapia, even when inclusion levels reach their maximum without pre-treatment. Chlorella remains niche because high fiber content lowers digestibility for carnivorous fish, unless costly cell-wall disruption is added, limiting its current market size. Competitive pressure is rising from bacterial single-cell proteins, so algae producers now market multi-strain blends that pair Spirulina for color with Schizochytrium for docosahexaenoic acid and Nannochloropsis for eicosapentaenoic acid in one feed solution.

Geography Analysis

Europe delivered the largest 35.5% share of the microalgae-based aquafeed market in 2025, as Norwegian and Danish salmon farmers adopted algal oils to meet Marine Stewardship Council traceability and antibiotic-free standards. Asia-Pacific is the fastest region, forecast to expand at a 10.7% CAGR from 2026-2031 on the back of India’s zero-tariff algal oil policy and China’s alternative-protein incentives. Europe continues to channel public funding into microalgae biorefineries that clean aquaculture effluent, while Asia-Pacific leverages import duty cuts to narrow the cost gap with fishmeal. These contrasting yet complementary policy drivers underpin divergent growth paths in the largest and fastest regional markets.

North America is growing steadily as Food and Drug Administration approvals open the door for novel strains and as salmon producers integrate algae to curb Scope 3 emissions. South America benefits from Chilean data showing improved feed conversion ratios and fewer downgrades when algal oils exceed 7.2% combined long-chain omega-3 content. The Middle East scales seawater-adapted Spirulina and Chlorella facilities that link carbon capture with inland aquaculture expansion. Africa remains early-stage, with pilot projects in Egypt and South Africa awaiting further cost declines before commercial rollouts.

Regional investment patterns signal accelerating capacity additions. European photobioreactor hubs in Scotland and France target multi-fold capacity jumps by 2027, while Japanese and South Korean pilots validate technology ahead of full commercialization. New carbon-credit programs in Norway and California offset up to 15% of production cost, making algae more competitive and fuelling cross-continental interest. As fishmeal volatility persists and sustainability labels harden, every major aquaculture zone is projected to widen algae usage, collectively expanding the global microalgae-based aquafeed market.

Competitive Landscape

The five largest suppliers collectively commanded a dominant share of the microalgae-based aquaculture feed market in 2025, underscoring a moderately concentrated market structure. Cargill, Incorporated and Corbion N.V. anchor this leadership by running multi-thousand-metric-ton AlgaPrime DHA lines that satisfy Western Europe’s traceability requirements while locking in multi-year salmon contracts. Both firms leverage vertical integration to control strain selection, fermentation, and downstream distribution, giving them scale efficiencies that smaller rivals struggle to match. Their early investments in carbon-accounting tools also position them to capture feed buyers that must report Scope 3 emissions to retailers and lenders.

BioMar Group A/S, Nutreco N.V., and Alltech, Inc. reinforce the leadership tier through portfolio breadth and research depth. BioMar Group A/S acquired the LetSea research center in 2025 to accelerate the development of net-zero diet prototypes that phase out marine ingredients by 2028. Nutreco N.V. employs its global Skretting network to co-develop algal formulations with shrimp and trout integrators, tightening customer lock-in across multiple continents. Alltech, Inc. blends its traditional feed expertise with in-house algae cultivation, signaling that a broad ingredient basket remains a key lever for negotiating long-term offtake agreements.

Emerging disruptors such as KnipBio, Algiecel, and MiAlgae are chipping away at incumbent dominance by pairing circular feedstocks and carbon-credit revenue, a model that improves margin resilience amid volatile fishmeal prices. Strategic consolidation is also reshaping the field, whereas the PhytoSmart–Cellana merger in 2024 and the Archer-Daniels-Midland Company–Alltech joint venture declared for 2026 broaden strain libraries and extend distribution footprints. Investment momentum remains strong, as illustrated by Unibio’s 50,000-metric-ton single-cell protein project in Saudi Arabia, which intensifies competitive pressure on algal proteins. As carbon pricing tightens and certification schemes harden, both incumbents and disruptors are projected to scale fermentation and photobioreactor assets, collectively expanding the addressable market for microalgae-based aquafeed.

Microalgae-Based Aquafeed Industry Leaders

Cargill, Incorporated

Corbion N.V.

BioMar Group A/S

Nutreco N.V.

Alltech, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Fermentalg introduced Omega Origins, a high-EPA algal oil comprising 40% eicosapentaenoic acid and 20% docosahexaenoic acid. This product is developed using proprietary Schizochytrium through patented fermentation processes, which ensure high purity and quality. The production method eliminates the need for post-production concentration steps, making it a more efficient and sustainable solution for obtaining essential omega-3 fatty acids.

- March 2026: Unibio and Saudi Industrial Investment Group have revealed plans for a 50,000 metric ton single-cell protein plant in Al Jubail. The facility aims to address the growing demand for sustainable protein sources and will utilize advanced fermentation technology. Construction is scheduled to begin in the second half of 2026, with potential scalability to 300,000 metric tons to meet future market needs.

- July 2025: Mara Renewables received USD 9.1 million from S2G Investments to expand fermentation capacity for DHA-rich algal oils. This funding aims to support the production of sustainable and high-quality ingredients for the aquafeed and pet nutrition markets, addressing the growing demand for alternative and eco-friendly nutritional solutions.

Global Microalgae-Based Aquafeed Market Report Scope

Microalgae-based aquafeed is a sustainable, nutrient-rich feed source for farmed aquatic animals, serving as a highly digestible alternative to traditional fishmeal and fish oil. It delivers essential proteins, lipids, and vitamins while reducing the environmental impact of aquaculture and easing pressure on wild fish stocks.

The microalgae-based aquafeed market report is segmented by product type (whole microalgae, algae meal or flour, algal oil dha-rich, algae protein isolate, and others), by species (spirulina, chlorella, nannochloropsis, schizochytrium, and others), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD) for all segments and sub-segments.

| Whole Microalgae |

| Algae Meal/Flour |

| Algal Oil (DHA-rich) |

| Algae Protein Isolate |

| Others |

| Spirulina |

| Chlorella |

| Nannochloropsis |

| Schizochytrium |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Whole Microalgae | |

| Algae Meal/Flour | ||

| Algal Oil (DHA-rich) | ||

| Algae Protein Isolate | ||

| Others | ||

| By Species | Spirulina | |

| Chlorella | ||

| Nannochloropsis | ||

| Schizochytrium | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the microalgae-based aquafeed market be by 2031?

The microalgae-based aquafeed market size is projected to reach USD 481.29 million by 2031.

Which product delivers the largest revenue contribution today?

Algal oil commanded the largest 38.0% market share in 2025 because salmon producers prize its stable docosahexaenoic acid profile.

What is the fastest-growing product category between 2026-2031?

Protein isolates are forecast to post the fastest 13.5% CAGR as shrimp hatcheries adopt high-protein concentrates that replace fishmeal without hurting survival.

Which region leads global demand for algae-based feeds?

Europe held the largest 35.5% share of global revenue in 2025 due to stringent traceability and antibiotic-free standards in its salmon sector.

Where is regional growth accelerating most quickly through 2031?

Asia-Pacific is projected to log the fastest 10.7% CAGR due to India's zero-tariff algal-oil policy and China's incentives for alternative proteins.

How concentrated is supplier power in this space?

The top five companies including Cargill, Incorporated, Corbion N.V., BioMar Group A/S, Nutreco N.V., and Alltech, Inc. controlled dominant share of microalgae-based aquaculture feed market size in 2025, signalling a moderately concentrated supplier base.

Page last updated on: