Frozen-Cooked Ready Meals Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 43.10 Billion |

| Market Size (2030) | USD 54.88 Billion |

| Growth Rate (2025 - 2030) | 4.95% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Frozen-Cooked Ready Meals Market Analysis by Mordor Intelligence

The global frozen-cooked ready meals market reached USD 43.10 billion in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 4.95% through 2030, reaching USD 54.88 billion by the forecast period's end. This steady expansion reflects fundamental shifts in consumer behavior driven by urbanization, dual-income households, and the rising adoption of GLP-1 medications that prioritize portion-controlled, single-serve meal solutions. The market's resilience stems from manufacturers' ability to balance convenience with evolving health expectations.

Key Report Takeaways

- By product type, non-vegetarian meals held 76.44% of the frozen-cooked ready meals market share in 2024, while vegetarian meals are projected to grow at a 6.19% CAGR from 2025-2030.

- By category, conventional products accounted for 92.36% of the frozen-cooked ready meals market size in 2024; organic lines are forecast to register a 7.11% CAGR through 2030.

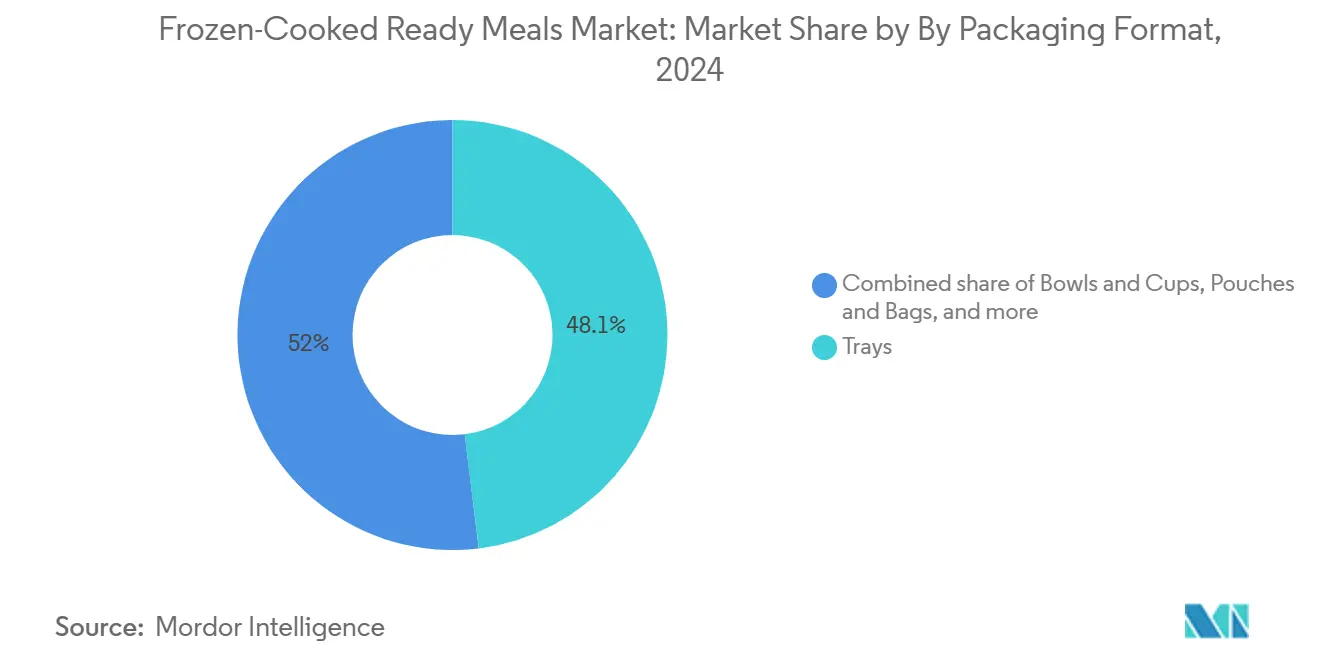

- By packaging format, trays led with 48.05% revenue share in 2024, but pouches and bags are expected to post a 5.79% CAGR to 2030.

- By distribution channel, supermarkets/hypermarkets captured 43.32% share of the frozen-cooked ready meals market size in 2024, whereas online retail is poised for a 6.36% CAGR over the same period.

- By geography, Europe held 31.46% of frozen-cooked ready meals market share in 2024, yet Asia-Pacific is projected to expand at a 6.28% CAGR to 2030.

Global Frozen-Cooked Ready Meals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Innovation in Product Variety | +0.8% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Preference for Specialty and Health-focused Meals | +1.2% | Global, led by North America and Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Growth in Organic and Natural Product Offerings | +0.6% | North America and Europe core, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Rising E-commerce and Direct-to-Consumer Sales | +1.0% | Global, with Asia-Pacific leading adoption rates | Medium term (2-4 years) |

| Advances in Cold Chain Logistics | +0.7% | Asia-Pacific core, spill-over to Middle East and Africa and Latin America | Medium term (2-4 years) |

| Busy Lifestyles and Time Pressure Leading to Demand for Convenient Meal Solutions | +1.3% | Global, with urbanized regions showing highest impact | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Innovation in Product Variety

Product diversification has become the cornerstone of competitive differentiation in the frozen-cooked ready meals sector, with manufacturers leveraging artificial intelligence and consumer analytics to accelerate new product development cycles. Companies like Campbell's are utilizing AI-driven platforms to curate consumer data and enable agile product development, reducing time-to-market for reformulated and plant-based ready meals. Global flavor profiles are becoming increasingly integrated into everyday dining, with a noticeable rise in the popularity of Indian and Japanese cuisines. This shift reflects a growing consumer desire for authentic international experiences enjoyed from the comfort of home. Street-food-inspired frozen products are gaining traction, especially those featuring Asian dumplings, which dominate this category. Additionally, bite-sized and mini meal formats are resonating strongly with younger generations like Gen Z and millennials, who tend to favor snackable, flexible eating options over traditional meals. This innovation velocity is supported by advances in isochoric freezing technology and packaging engineering that preserve texture and flavor integrity across diverse product categories.

Preference for Specialty and Health-focused Meals

The convergence of health consciousness and convenience has fundamentally reshaped product development priorities, with GLP-1 medication adoption creating unprecedented demand for portion-controlled, high-protein frozen meals. Nestlé's launch of Vital Pursuit, specifically targeting GLP-1 users with single-serve, high-protein options, exemplifies how pharmaceutical trends are driving food innovation. Gut health claims in frozen foods surged significantly over the past years, reflecting consumer understanding of the microbiome's role in overall wellness. The "modern health" trend encompasses not just nutritional enhancement but also functional benefits, with manufacturers incorporating prebiotics, probiotics, and adaptogens into frozen meal formulations. Single-serve, high-protein, high-fiber meals are experiencing particularly strong growth as consumers seek maintenance options post-GLP-1 treatment. This health-forward positioning extends beyond ingredients to packaging transparency, with clean-label reformulation becoming a competitive necessity despite technical challenges in maintaining taste and texture in frozen applications.

Growth in Organic and Natural Product Offerings

Organic frozen meals are experiencing accelerated growth at 7.11% CAGR, significantly outpacing conventional alternatives, driven by consumer willingness to pay premiums for perceived health and environmental benefits. The USDA organic certification process has become increasingly rigorous, with supply chain integrity and traceability requirements creating barriers to entry that favor established players with robust sourcing networks.[1]Source: United States Department of Agriculture, “Organic Certification and Accreditation,” ams.usda.gov Consumer trust in organic labeling remains high despite supply chain complexities, with 73% of consumers viewing organic certification as a reliable indicator of product quality. Natural ingredient sourcing challenges have intensified due to climate variability and geopolitical tensions affecting key agricultural regions, creating cost pressures that manufacturers are absorbing to maintain market position. The clean-label movement extends beyond organic certification to encompass minimal processing, recognizable ingredients, and transparent sourcing practices. Regulatory frameworks like the EU's Farm to Fork strategy are reinforcing organic growth trajectories by establishing sustainability targets that favor organic production methods over conventional alternatives.

Advances in Cold Chain Logistics

Cold chain infrastructure development, particularly in the Asia-Pacific regions, is unlocking previously inaccessible markets and enabling geographic expansion of frozen-cooked ready meals. China's cold storage capacity reached 237 million cubic meters in June 2024, with government investments in refrigerated transport networks reducing spoilage rates and expanding distribution reach to tier-2 and tier-3 cities[2]Source: International Institute of Refrigeration, “China’s cold chain growth: increased capacity and sustainable practices in 2024,” iifiir.org. Advanced Transportation Management Systems (TMS) are optimizing frozen food distribution efficiency, with Thailand-Japan trade routes demonstrating 15% cost reductions through route optimization and predictive maintenance. Isochoric freezing technology is revolutionizing product quality by minimizing cellular damage during the freezing process, enabling manufacturers to offer premium texture and nutritional retention. Internet of Things (IoT) sensors and blockchain technology are providing end-to-end cold chain visibility, reducing insurance costs and enabling quality guarantees that support premium positioning. The development of sustainable refrigerants and energy-efficient cold storage facilities is addressing environmental concerns while reducing operational costs, particularly important as natural gas price volatility affects traditional blast-freezing economics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile cold-chain logistics costs | -0.9% | Global, with highest impact in emerging markets | Short term (≤ 2 years) |

| Clean-label reformulation barriers | -0.6% | North America and Europe, expanding globally | Medium term (2-4 years) |

| Natural-gas price shocks hurting blast-freezing economics | -0.7% | Europe and North America, with supply chain dependencies | Short term (≤ 2 years) |

| Rising bans on single-use plastic trays in EU states | -0.4% | Europe core, potential expansion to other regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Cold-Chain Logistics Costs

Energy price volatility and supply chain disruptions continue creating unpredictable cost structures for frozen-cooked ready meals manufacturers, with natural gas price fluctuations directly impacting blast-freezing operations and cold storage facilities. European natural gas prices experienced high volatility in 2024, forcing manufacturers to implement dynamic pricing strategies and hedge against energy cost spikes. Transportation fuel costs and refrigerated trucking capacity constraints have created regional supply chain bottlenecks, particularly affecting distribution to rural markets where infrastructure investments lag urban centers. The shortage of qualified cold-chain logistics personnel has intensified wage inflation, with specialized drivers commanding 25% premium wages compared to standard freight operators. Insurance costs for temperature-sensitive cargo have increased due to climate-related disruptions and equipment failures, adding 0.3-0.5% to total product costs. Manufacturers are responding through vertical integration of cold-chain assets and strategic partnerships with logistics providers, though these investments require significant capital commitments that may constrain short-term profitability.

Clean-Label Reformulation Barriers

Technical challenges in reformulating frozen meals to meet clean-label standards while maintaining taste, texture, and shelf-life present ongoing obstacles for manufacturers seeking to capitalize on natural ingredient trends. The removal of traditional preservatives and stabilizers requires sophisticated food science expertise and often results in shorter shelf-life or compromised sensory attributes that consumers reject. FDA guidance on natural flavoring definitions and FSIS regulations on processed meat products create regulatory complexity that varies by product category and geographic market. Ingredient sourcing for clean-label formulations faces supply chain constraints, with organic and non-GMO ingredients commanding premium prices and limited availability during peak demand periods. Consumer education remains challenging, as clean-label expectations often conflict with food safety requirements and preservation needs inherent in frozen food manufacturing. The cost of reformulation, including R&D investments, regulatory approvals, and production line modifications, can exceed USD 2 million per product line, creating barriers for smaller manufacturers and limiting innovation velocity across the industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vegetarian Growth Outpaces Traditional Dominance

Non-vegetarian meals maintain commanding market leadership with 76.44% share in 2024, reflecting established consumer preferences and protein-centric meal expectations, yet vegetarian alternatives demonstrate superior growth momentum at 6.19% CAGR (2025-2030). This growth acceleration stems from expanding flexitarian demographics, environmental consciousness, and improved plant-based protein technologies that deliver satisfying texture and flavor profiles previously unattainable in frozen applications. Poultry-based meals dominate the non-vegetarian segment due to cost efficiency and broad consumer acceptance, while beef-based options face headwinds from sustainability concerns and premium pricing. Seafood meals occupy a premium niche with higher margins but limited volume growth due to supply chain volatility and sustainability certification requirements.

The plant-based protein revolution has enabled vegetarian frozen meals to transcend traditional limitations through innovations in texture and umami flavor development, with companies leveraging fermentation technology and protein isolates to create meat-like experiences. Pork-based meals remain regionally concentrated in Asian and European markets, while other meat categories, including lamb and game proteins serve specialized consumer segments.

By Category: Organic Acceleration Challenges Conventional Dominance

Conventional frozen meals retain overwhelming market dominance at 92.36% share in 2024, supported by cost efficiency, established supply chains, and broad consumer accessibility, while organic alternatives surge at 7.11% CAGR (2025-2030). This organic acceleration reflects consumer willingness to pay premiums for perceived health benefits, environmental sustainability, and supply chain transparency, despite higher retail prices that can exceed conventional alternatives by 40-60%. The USDA organic certification framework provides consumer confidence and regulatory clarity, though compliance costs and supply chain complexity create barriers for smaller manufacturers seeking organic market entry.

Organic growth drivers include expanding retail distribution, improved taste profiles through advanced organic ingredient processing, and demographic shifts toward health-conscious younger consumers with higher disposable incomes. Conventional products continue evolving through clean-label initiatives, non-GMO sourcing, and reduced-sodium formulations that bridge the gap between traditional and organic positioning. The regulatory landscape supporting organic agriculture, including government subsidies and certification streamlining, reinforces long-term growth trajectories while conventional manufacturers explore hybrid approaches combining organic ingredients with conventional processing methods.

By Packaging Format: Flexible Solutions Gain Traction Against Traditional Trays

Traditional trays command 48.05% market share in 2024, leveraging established manufacturing infrastructure, consumer familiarity, and retail merchandising advantages, yet face mounting pressure from pouches and bags packaging formats growing at 5.79% CAGR (2025-2030). This shift toward pouches and bags reflects EU Packaging and Packaging Waste Regulation (PPWR) requirements, driving recyclability mandates and sustainability concerns about single-use plastic trays. Bowls and cups maintain a steady market position through portion control benefits and microwave convenience, while other packaging formats, including compostable materials and hybrid solutions, gain experimental adoption.

The packaging evolution encompasses both environmental and functional improvements, with flexible formats offering superior freezer space efficiency, reduced transportation costs, and enhanced barrier properties that extend shelf life. Manufacturers are investing in monomaterial polyethylene films and paper-based alternatives that meet recycling infrastructure requirements while maintaining cold-chain integrity. Tray manufacturers are responding through bio-based materials, industrial compostability certifications, and reduced plastic content formulations that address regulatory requirements without compromising functionality.

By Distribution Channel: Digital Commerce Transforms Traditional Retail

Supermarkets/hypermarkets maintain market leadership with 43.32% share in 2024, benefiting from established cold-chain infrastructure, consumer shopping habits, and promotional capabilities, while online retail channels accelerate at 6.36% CAGR (2025-2030), reflecting fundamental shifts in consumer purchasing behavior. This digital transformation extends beyond pandemic-driven adoption to encompass subscription services, personalized nutrition platforms, and direct-to-consumer models that bypass traditional retail intermediaries. Convenience stores serve targeted urban demographics with limited selection but premium positioning.

The e-commerce evolution requires sophisticated last-mile cold-chain solutions, with companies investing in temperature-controlled fulfillment centers and partnerships with specialized delivery providers to maintain product integrity. Online platforms leverage artificial intelligence for personalized recommendations, predictive ordering, and inventory optimization that traditional retail channels cannot match. Traditional retailers are responding through omnichannel strategies, click-and-collect services, and digital integration that combines online convenience with in-store experience.

Geography Analysis

Europe's market leadership position at 31.46% share in 2024 stems from sophisticated cold-chain infrastructure, established consumer acceptance of frozen convenience foods, and regulatory frameworks that balance food safety with innovation support. The region's growth trajectory faces headwinds from EU Packaging and Packaging Waste Regulation (PPWR) requirements that mandate recyclability and restrict single-use plastics, creating compliance costs estimated at EUR 2-4 billion annually across the food packaging sector.

Asia-Pacific emerges as the highest-growth region at 6.28% CAGR (2025-2030), driven by rapid urbanization, expanding middle-class populations, and government investments in cold-chain infrastructure that unlock previously inaccessible markets. India's frozen food market benefits from changing dietary patterns, dual-income household growth, and e-commerce penetration. Japan and South Korea represent mature sub-markets with premium positioning and technological innovation focus, while Southeast Asian countries, including Thailand, Indonesia, and Singapore, show emerging potential constrained by infrastructure development needs. The region's growth momentum reflects demographic dividends, with younger populations more receptive to convenient meal solutions and international flavor profiles that drive product innovation and market expansion.

North America maintains stable market positioning through established supply chains, consumer acceptance, and innovation leadership in health-focused product development, though mature market dynamics limit volume growth compared to emerging regions. The United States drives regional consumption through premium positioning, clean-label initiatives, and specialized dietary requirements including gluten-free, keto-friendly, and plant-based alternatives that command higher margins. Canada's market development follows similar patterns with additional emphasis on bilingual labeling requirements and provincial food safety regulations that create compliance complexity. Mexico represents emerging growth potential within the North American framework, driven by urbanization and expanding retail infrastructure that supports frozen food distribution.

Competitive Landscape

Top Companies in Frozen-Cooked Ready Meals Market

The frozen-cooked ready meals market exhibits moderate concentration, reflecting balanced competition between established multinational corporations and emerging regional players pursuing differentiated positioning strategies. Strategic patterns emphasize vertical integration of cold-chain assets, artificial intelligence adoption for product development acceleration, and geographic expansion into high-growth Asia-Pacific markets where infrastructure investments create competitive moats.

Technology deployment focuses on isochoric freezing innovations, sustainable packaging solutions, and e-commerce platform optimization that enables direct-to-consumer relationships and personalized nutrition positioning. White-space opportunities emerge in specialized dietary segments, including GLP-1-compatible portion-controlled meals, gut health-focused formulations, and premium international cuisine offerings that command higher margins while serving underserved consumer needs.

Emerging disruptors leverage subscription models, clean-label positioning, and direct-to-consumer distribution to bypass traditional retail intermediaries and capture health-conscious demographics willing to pay premiums for transparency and convenience. Established players respond through acquisition strategies, innovation partnerships, and omnichannel distribution expansion that combines retail presence with digital capabilities.

Frozen-Cooked Ready Meals Industry Leaders

Nestlé SA

Conagra Brands Inc.

Campbell Soup Company

Ajinomoto Co. Inc.

The Kraft Heinz Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: GRUBBY is reintroducing Allplants recipes through a new frozen ready meal range, marking its first venture into this category. The range features nine recreated Allplants recipes, including the Miso and Tamari Buddha Bowl, Nduja Rigatoni, and Creamy Mac and Greens with Herb Crumb.

- August 2025: Chopstix, the U.K. noodle bar chain, has launched its first frozen ready meal range exclusively at The Food Warehouse. The range includes seven of the restaurant's popular dishes: Sweet & Sour Chicken, KPOP BBQ Chicken, Chinese Chicken Curry, Salt & Pepper Chicken, Beef Teriyaki, Signature Caramel Drizzle Chicken, and Firecracker Chicken.

- May 2025: Dolly Parton partnered with Conagra Brands to launch single-serve frozen meals based on Southern cuisine. The product line includes traditional dishes such as country fried steak and chicken and dumplings, focusing on delivering authentic Southern flavors.

Global Frozen-Cooked Ready Meals Market Report Scope

A frozen-cooked meal refers to any complete meals or portions of meals that are precooked, assembled into a package, and frozen for retail sale. Frozen meals are popular as they offer a diverse menu and are convenient to prepare. In the food industry, freezing usually refers to deep freezing or lowering the temperature of the product below -18°C.

The scope of the frozen-cooked ready meals market includes segmentation of the market based on type, application, and geography. By product type, the market is segmented into vegetarian meals and non-vegetarian meals. Non-vegetarian meals are further segmented into chicken meals, beef meals, and other non-vegetarian meals. By distribution channel, the market is segmented into supermarkets/ hypermarkets, convenience stores, online retailers, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| Vegetarian Meals | |

| Non-Vegetarian Meals | Poultry-Based Meals |

| Beef-Based Meals | |

| Seafood Meals | |

| Pork-Based Meals | |

| Other Meats |

| Conventional |

| Organic |

| Trays |

| Bowls and Cups |

| Pouches and Bags |

| Others |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Channels |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Vegetarian Meals | |

| Non-Vegetarian Meals | Poultry-Based Meals | |

| Beef-Based Meals | ||

| Seafood Meals | ||

| Pork-Based Meals | ||

| Other Meats | ||

| By Category | Conventional | |

| Organic | ||

| By Packaging Format | Trays | |

| Bowls and Cups | ||

| Pouches and Bags | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Channels | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global frozen-cooked ready meals demand be in 2030?

The category is forecast to reach USD 54.88 billion by 2030, growing at a 4.95% CAGR from the 2025 base.

Which region is expanding fastest in frozen-cooked ready meals?

Asia-Pacific is projected at a 6.28% CAGR owing to urbanization, e-commerce uptake, and cold-chain investments.

What packaging change is most influential for frozen meals?

Flexible pouches and bags, advancing at a 5.79% CAGR, are displacing rigid trays as recyclability rules tighten.

How is e-commerce altering frozen meal sales?

Online channels, expanding at 6.36% CAGR, use insulated logistics and subscription models to deliver convenient, personalized options.

Page last updated on: