Dairy Snack Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

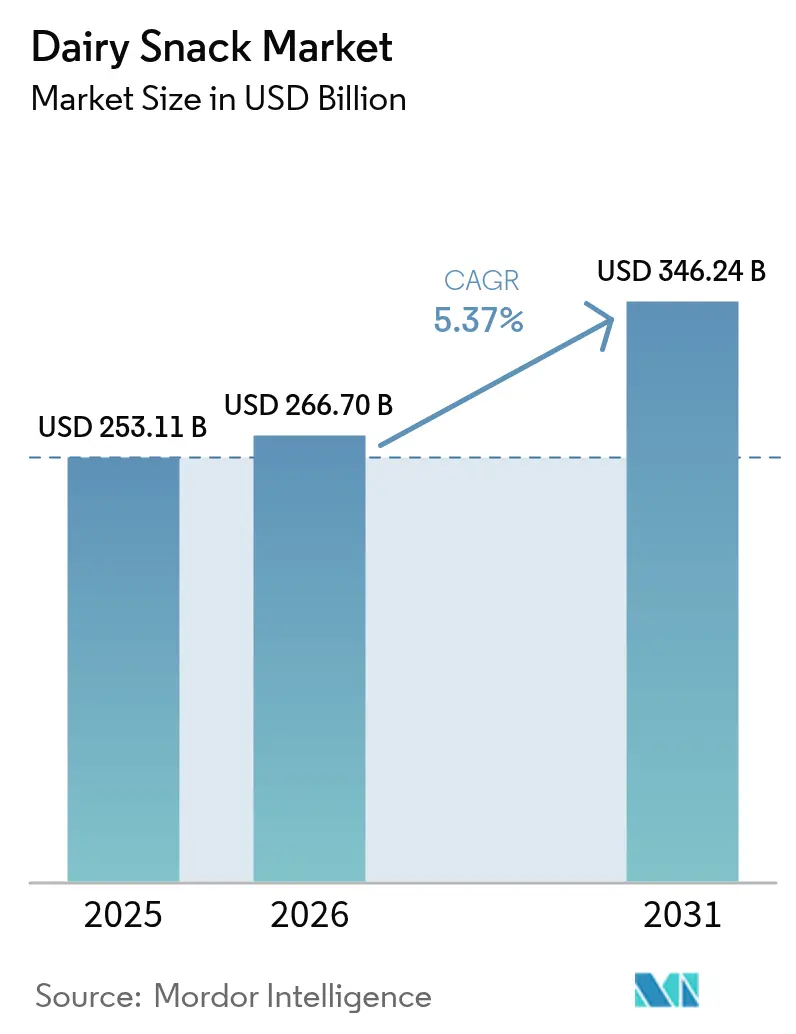

| Market Size (2026) | USD 266.7 Billion |

| Market Size (2031) | USD 346.24 Billion |

| Growth Rate (2026 - 2031) | 5.37% CAGR |

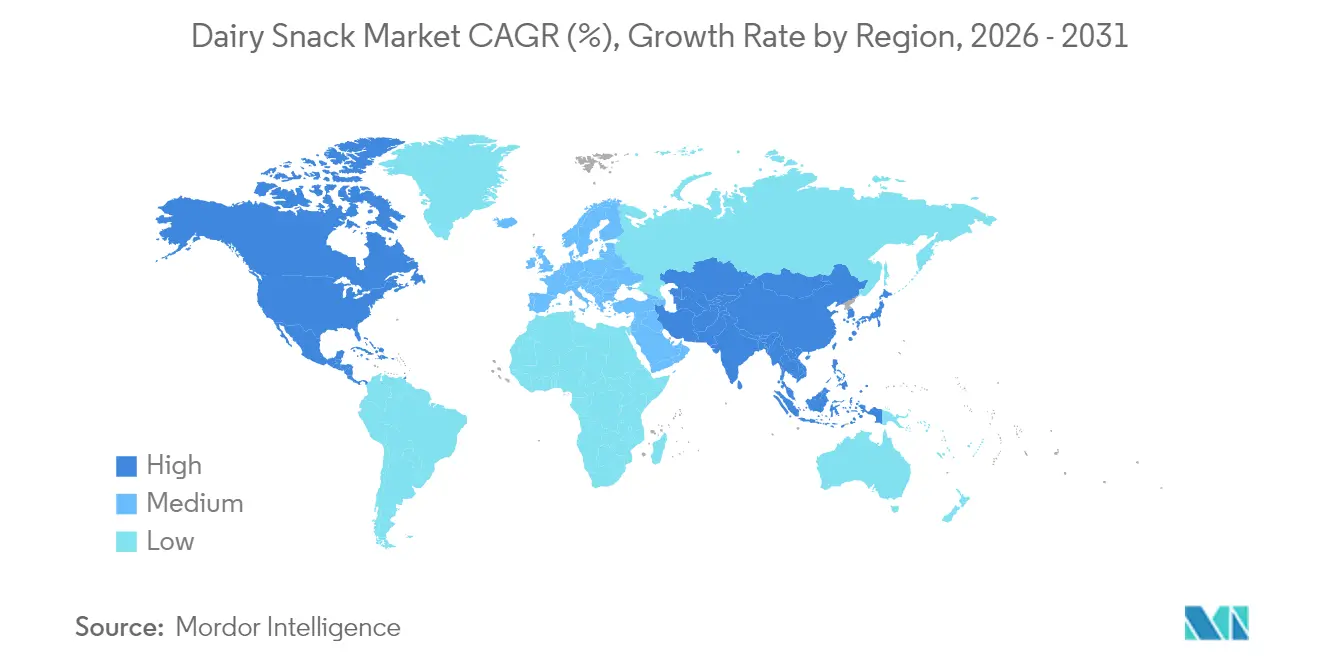

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

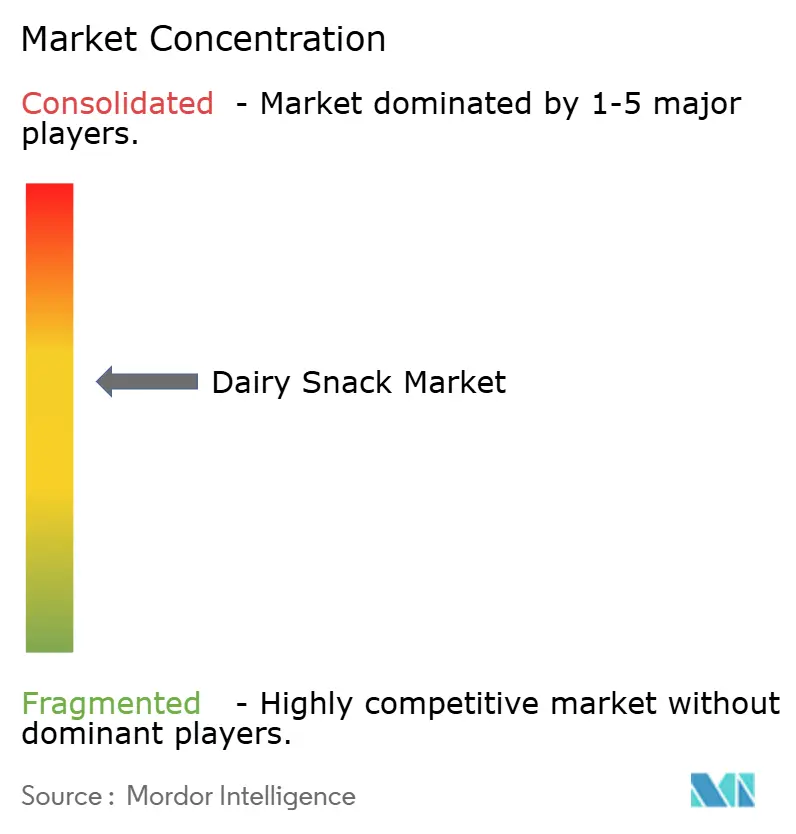

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Dairy Snack Market Analysis by Mordor Intelligence

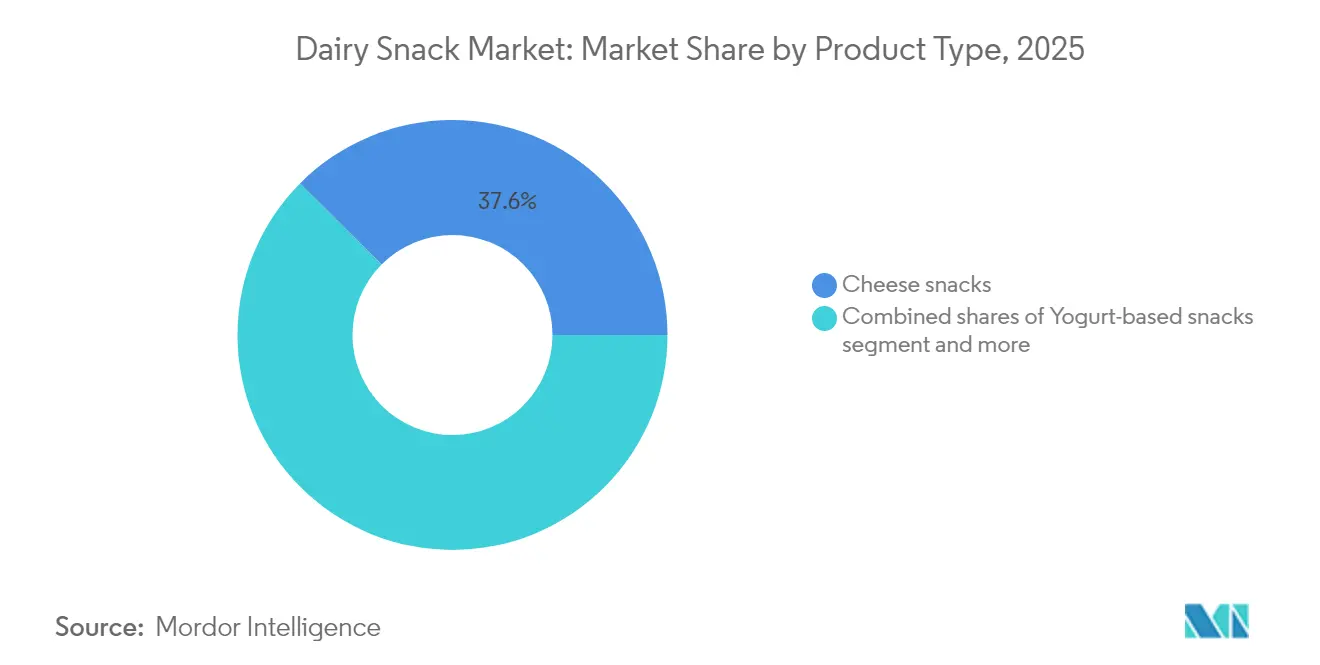

Dairy snack market size in 2026 is estimated at USD 266.7 billion, growing from 2025 value of USD 253.11 billion with 2031 projections showing USD 346.24 billion, growing at 5.37% CAGR over 2026-2031. Cheese snacks command the largest share at 38.12% in 2024, driven by protein-conscious consumers who prioritize convenient, nutrient-dense options that fit busy schedules. Yogurt-based snacks, meanwhile, are projected to grow fastest at 7.11% CAGR through 2030, propelled by probiotic fortification and on-the-go formats that appeal to health-focused buyers across urban centers. This bifurcation signals a market where traditional dairy staples retain volume leadership while functional innovations capture incremental growth. Demand strength rests on protein-seeking consumers who want convenient nutrition, sustained purchasing power in Asia-Pacific, and product upgrades that keep mature Western shoppers engaged. Cartons and tetra-packs continue to dominate unit volumes, yet flexible pouches are taking share as brands cut plastic and seek resealable portability. Online grocery penetration is reshaping route-to-market economics, pulling volume away from hypermarkets while rewarding manufacturers with direct-to-consumer capabilities. Premiumization is gathering pace, especially in North America, Europe, Japan, and selected tier-one Asian cities, where affluent buyers trade up to organic grass-fed or artisanal SKUs, supporting margin expansion even as mass segments keep volume leadership.

Key Report Takeaways

- By product type, yogurt-based snacks recorded the fastest expansion at a 6.89% CAGR through 2031, while cheese maintained the largest 37.55% revenue share of the cheese snacks market in 2025.

- By packaging format, cartons and tetra-packs held 59.68% of the cheese snacks market share in 2025; pouches are forecast to grow at a 6.58% CAGR between 2026-2031.

- By price tier, the premium segment is advancing at a 6.32% CAGR through 2031, whereas the mass tier controlled 78.10% of the cheese snacks market size in 2025.

- By distribution channel, supermarkets and hypermarkets captured 52.10% of 2025 sales; online retail shows the highest CAGR at 6.15% through 2031.

- By geography, Asia-Pacific contributed 25.30% of the cheese snacks market share in 2025 and is expanding at a 6.07% CAGR, the fastest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dairy Snack Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for protein-rich snacks fuels dairy-snack appeal | +1.2% | Global, with the strongest uptake in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Busy lifestyles and urban living boost demand for convenient, ready-to-eat dairy snacks | +1.0% | Global, concentrated in metropolitan areas of Asia-Pacific, North America, and Europe | Short term (≤ 2 years) |

| Product innovation in flavors, lactose-reduced, fortified, and portable formats expands appeal | +0.9% | Global, with rapid adoption in Asia-Pacific and North America | Medium term (2-4 years) |

| Increasing demand for functional/fortified dairy products (probiotics, vitamins) attracts health-focused buyers | +0.8% | Global, particularly strong in Japan, South Korea, and Western Europe | Long term (≥ 4 years) |

| Packaging and portion-control innovations expand consumer appeal | +0.6% | Global, with early gains in Europe and North America, spreading to the Asia-Pacific | Medium term (2-4 years) |

| Rising consumer interest in clean-label and natural-ingredient dairy snacks | +0.5% | North America and Europe lead, with emerging interest in urban Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Protein-Rich Snacks Fuels Dairy-Snack Appeal

Protein has become a non-negotiable attribute for snack buyers, with 71% of consumers prioritizing protein content in 2024, up from 59% in 2022, according to ingredient supplier IFF's trend analysis. This shift is redefining dairy snacks from indulgent treats into functional nutrition vehicles, particularly among fitness enthusiasts and time-pressed professionals who replace meals with high-protein options. Cheese snacks, cottage cheese cups, and Greek yogurt variants now compete directly with protein bars and shakes, capturing share from non-dairy alternatives that often rely on pea or soy isolates with less favorable amino-acid profiles. The trend is most pronounced in North America and Europe, where regulatory clarity around protein claims under FDA and EFSA guidelines enables aggressive marketing. In Asia-Pacific, protein messaging is gaining traction in urban centers like Shanghai and Mumbai, though price premiums remain a barrier in tier-two cities where per-capita income lags.

Busy Lifestyles and Urban Living Boost Demand for Convenient, Ready-to-Eat Dairy Snacks

Urbanization is compressing meal occasions into snacking windows, with majority of global consumers reporting they snack at least twice daily in 2024. Dairy snacks fit this pattern because they require no preparation, survive short periods outside refrigeration, and deliver satiety through fat and protein. Single-serve yogurt cups, cheese sticks, and drinkable smoothies are displacing traditional sit-down breakfasts in markets like Japan, where commuters purchase chilled snacks from convenience stores en route to work. In India, Amul's expansion into portion-controlled paneer cubes and flavored lassi pouches is capturing demand from college students and office workers who lack access to home-cooked meals during the day. The convenience driver is amplified by cold-chain improvements in Southeast Asia, where refrigerated vending machines and modern trade formats are proliferating in Jakarta and Manila, reducing reliance on ambient-stable snacks.

Product Innovation in Flavors, Lactose-Reduced, Fortified, and Portable Formats Expands Appeal

Innovation velocity is accelerating, with Danone launching its Remix yogurt line in 2024, featuring mix-in toppings that let consumers customize texture and flavor, addressing a key complaint about yogurt's monotony. Lactose-free variants now account for a growing share of launches, targeting the estimated 68% of the global population with some degree of lactose malabsorption[1]Source: NIH, "Know Your Blood Pressure Numbers", nih.gov. Arla's upcycled dairy initiative, which converts whey byproducts into high-protein snack ingredients, exemplifies how sustainability and nutrition are converging in product development. Portable formats such as squeezable yogurt tubes and resealable cheese pouches are expanding usage occasions beyond home consumption into schools, gyms, and outdoor activities. Fortification with probiotics, omega-3s, and vitamins is particularly strong in Japan, where Meiji's functional dairy snacks target elderly consumers seeking immune support and bone health.

Increasing Demand for Functional/Fortified Dairy Products Attracts Health-Focused Buyers

Functional ingredients are shifting dairy snacks from commodity to specialty, with probiotics, prebiotics, and milk fat globule membrane (MFGM) commanding price premiums of 20-40% over standard offerings. Chobani's probiotic yogurt drinks, launched in 2024, contain Lactobacillus strains clinically shown to support gut health, tapping into the USD 50 billion global probiotics market. In China, Yili's fortified milk snacks enriched with DHA and calcium are marketed to parents seeking cognitive and skeletal benefits for children, aligning with government nutrition guidelines that emphasize early-life development. Regulatory influence is significant here: FSSAI in India mandates specific fortification levels for products making health claims, raising barriers for smaller brands that lack R&D budgets [2]Source: FSSAI, "Regulatory Influence", fssai.gov.in. The functional trend is also creating white-space opportunities for dairy-probiotic hybrids that blur the line between food and supplements, a category where traditional dairy firms compete with pharmaceutical entrants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lactose intolerance and dairy allergies hinder growth | -0.8% | Global, with the highest prevalence in East Asia, Africa, and parts of Southern Europe | Long term (≥ 4 years) |

| Price sensitivity: Premium dairy snacks may be unaffordable for mass consumers | -0.6% | Emerging markets in Asia-Pacific, Africa, and Latin America | Short term (≤ 2 years) |

| Competition from plant-based and alternative snacks weakens dairy-snack demand | -0.7% | North America and Europe lead, with growing interest in urban Asia-Pacific | Medium term (2-4 years) |

| Shelf-life and cold-chain requirements complicate storage and distribution in some regions | -0.5% | Rural and semi-urban areas in Asia-Pacific, Africa, and Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lactose Intolerance and Dairy Allergies Hinder Growth

Lactose malabsorption affects approximately 68% of the global population, with prevalence exceeding 90% in East Asian countries like China and South Korea. This biological constraint caps addressable market size unless brands invest in lactose-free processing, which adds 15-20% to production costs due to enzyme treatment and separate production lines. Dairy allergies, though less common at 2-3% prevalence, trigger severe reactions that drive complete category avoidance, particularly among infants and young children. The restraint is most acute in Asia-Pacific, where traditional diets historically contained minimal dairy and populations lack the genetic adaptation seen in Northern European ancestry groups. Brands are responding with lactose-free cheese snacks and A2 milk-based yogurts, which some consumers find easier to digest, though clinical evidence remains mixed. Regulatory labeling requirements under Codex Alimentarius standards mandate clear allergen declarations, increasing compliance complexity for multinational firms operating across jurisdictions [3]Source: Codex Alimentarius, "Protecting health, facilitating trade", fao.org.

Competition from Plant-Based and Alternative Snacks Weakens Dairy-Snack Demand

Plant-based dairy alternatives are projected to grow, outpacing traditional dairy's expansion. Oat-based yogurts, almond-milk smoothies, and cashew cheese spreads are capturing share among flexitarian consumers who reduce but do not eliminate animal products, a cohort that represents 30-40% of Western markets. The competitive threat is most severe in premium segments, where plant-based brands leverage sustainability messaging and clean-label formulations to justify price parity with dairy. In North America and Europe, supermarket shelf space is shifting toward plant-based options, compressing visibility for traditional dairy snacks. However, dairy retains advantages in protein quality, calcium bioavailability, and taste familiarity that plant-based alternatives struggle to replicate without extensive fortification and flavoring. The restraint is less pronounced in Asia-Pacific, where soy-based products have coexisted with dairy for decades, and consumers view them as complementary rather than substitutional.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Functional Yogurts Outpace Traditional Cheese

Yogurt-based snacks are expanding at a 6.89% CAGR from 2026 to 2031, the fastest rate among product types, as brands layer in probiotics, protein fortification, and novel textures that differentiate them from commodity offerings. Cheese snacks, despite holding 37.55% market share in 2025, face maturity in Western markets where per-capita consumption has plateaued, though emerging-market adoption in Asia-Pacific is offsetting this drag. Spoonable yogurts dominate within the yogurt category, but drinkable variants are gaining as on-the-go formats proliferate; Danone's Remix line and Chobani's probiotic drinks exemplify this shift toward portability and functional claims. Ice cream and frozen dairy snacks, while traditionally indulgent, are being repositioned as protein-rich treats, with Unilever launching bite-sized formats in 2024 that deliver portion control without sacrificing taste. Smoothies occupy a niche but growing segment, appealing to health-conscious consumers who blend dairy with fruits and vegetables for nutrient density. Milk and cream-based snacks, including puddings and custards, remain popular in the Asia-Pacific, where sweet dairy desserts align with local palates, though growth is constrained by sugar-reduction trends. Other products, such as paneer cubes and dairy-based dips, are expanding in India and the Middle East, driven by regional culinary traditions that incorporate dairy into savory applications.

Innovation is the primary differentiator across product types. Cottage cheese ice cream, launched by several startups in 2024, combines the protein density of cheese with the indulgence of frozen desserts, targeting fitness enthusiasts who seek guilt-free treats. Lactose-free cheese snacks are proliferating in East Asia, where brands use enzyme treatment to broaden their addressable market beyond the lactose-tolerant minority. Regulatory compliance factors into product development, as FSSAI in India and FDA in the United States mandate specific labeling for fortified and functional claims, raising barriers for smaller entrants. The product-type segmentation underscores a market in transition, where traditional staples like cheese retain volume leadership but functional yogurts and hybrid formats capture the innovation premium.

By Packaging Format: Pouches Gain as Sustainability and Portability Converge

Cartons and tetra-packs commanded 59.68% of market share in 2025, reflecting their dominance in ambient-stable and refrigerated yogurt and milk-based snacks, yet pouches are projected to grow at 6.58% CAGR through 2031 as brands prioritize lighter, resealable options that reduce material use and improve on-the-go convenience. General Mills' Yoplait brand switched to cartons made from 78% plant-based materials in 2024, cutting packaging weight by 50% and signalling a broader industry shift toward renewable substrates. Pouches, particularly stand-up and spouted variants, are gaining traction in Asia-Pacific, where consumers value portion control and single-hand usability during commutes; Amul's flavored lassi pouches and Meiji's squeezable yogurt tubes exemplify this trend. Canned formats, while niche, persist in shelf-stable dairy desserts and sweetened condensed milk applications, though their share is eroding as consumers associate metal packaging with processed foods. Other formats, including glass jars for premium yogurts and biodegradable trays for cheese snacks, are emerging in Europe and North America, where sustainability credentials command price premiums.

The packaging shift is driven by both consumer preferences and regulatory pressures. Extended producer responsibility (EPR) schemes in the European Union mandate that brands finance end-of-life recycling for packaging, incentivizing lightweighting and mono-material designs that simplify waste sorting. In India, FSSAI's packaging standards require tamper-evident seals and clear date labeling, raising costs for smaller dairies that lack automated filling lines. Pouches offer a cost-effective solution because they use less material per unit and can be filled on flexible lines that accommodate multiple SKUs. However, cold-chain requirements remain a constraint for pouches in rural areas where refrigeration infrastructure is sparse, limiting their penetration outside urban centers. The packaging segmentation reveals a market where sustainability and convenience are no longer trade-offs but converging imperatives that reward brands capable of delivering both.

By Price Tier: Premium Segment Grows Faster Despite Mass Dominance

Mass-tier products held 78.10% of market share in 2025, reflecting dairy snacks' role as everyday staples in both developed and emerging markets, yet premium offerings are expanding at 6.32% CAGR through 2031 as affluent consumers trade up to organic, grass-fed, and artisanal variants that command 30-50% price premiums. The premium surge is most visible in North America and Europe, where brands like Chobani and Arla position their products around animal welfare, regenerative agriculture, and minimal processing. In Asia-Pacific, premium dairy snacks are gaining in tier-one cities like Tokyo, Seoul, and Singapore, where rising incomes and Western dietary influences are shifting consumption patterns toward quality over quantity. However, price sensitivity remains a binding constraint in India, Indonesia, and rural China, where per-capita dairy spending is a fraction of Western levels, and consumers prioritize volume over provenance. Mass-tier brands are responding by fortifying affordable products with vitamins and minerals, offering functional benefits without premium pricing; Amul's fortified milk snacks in India exemplify this strategy.

The premium-mass divide is also a strategic choice for multinationals. Nestlé and Danone operate dual portfolios, with mass brands capturing volume in emerging markets and premium lines defending margins in mature geographies. Private-label dairy snacks, which fall into the mass tier, are expanding in Europe as retailers like Aldi and Lidl leverage vertical integration to undercut branded competitors by 20-30%. This dynamic is compressing margins for mid-tier brands that lack either the scale of mass players or the differentiation of premium entrants. The price-tier segmentation highlights a bifurcating market where growth is concentrating at the extremes, ultra-affordable fortified products in emerging markets and high-margin artisanal offerings in developed economies, while the middle ground erodes.

By Distribution Channel: Online Retail Gains as Cold-Chain Logistics Mature

Supermarkets and hypermarkets captured 52.10% of the distribution share in 2025, leveraging their refrigerated footprint and one-stop shopping convenience, yet online retail is expanding at a 6.15% CAGR through 2031 as e-commerce platforms invest in last-mile cold-chain infrastructure that was rudimentary five years ago. In China, Alibaba's Hema Fresh stores integrate online ordering with in-store fulfillment, enabling 30-minute delivery of chilled dairy snacks in major cities. In India, BigBasket and Amazon Fresh are deploying refrigerated delivery vans and dark stores to extend their reach beyond ambient groceries into perishables. Convenience and grocery stores, while smaller in format, remain critical in Asia-Pacific, where high population density and frequent shopping trips favor neighborhood outlets over large-format retailers. Other distribution channels, including vending machines, food service, and direct-to-consumer subscriptions, are growing in niche segments; Japan's ubiquitous refrigerated vending machines dispense yogurt drinks and cheese snacks 24/7, capturing impulse purchases that brick-and-mortar stores miss.

The online shift is compressing margins for traditional retailers, who must invest in refrigeration upgrades and loyalty programs to retain foot traffic. Brands are responding by launching direct-to-consumer subscription models that bypass retail intermediaries; Chobani's online subscription service in the United States delivers weekly yogurt assortments at a 15% discount to retail prices, building customer lifetime value while capturing first-party data on consumption patterns. However, cold-chain constraints remain a barrier in rural areas and tier-two cities, where ambient temperatures exceed 30°C for much of the year, and refrigerated logistics add 25-35% to delivery costs. Regulatory compliance also varies by channel: online platforms in India must display FSSAI license numbers and expiration dates prominently, raising operational complexity for aggregators that source from multiple dairies. The distribution segmentation underscores a market in flux, where digital channels are gaining share, but physical retail retains structural advantages in impulse purchases and immediate availability.

Geography Analysis

Asia-Pacific held 25.30% of global market share in 2025 and is forecast to expand at 6.07% CAGR through 2031, outpacing North America and Europe, where per-capita dairy consumption has plateaued. China leads regional growth, driven by Yili and Mengniu's aggressive expansion into yogurt and cheese snacks that cater to urbanizing middle-class consumers seeking convenient, protein-rich options. Japan's market is characterized by functional dairy products targeting its aging population; Meiji's fortified yogurts and calcium-enriched cheese snacks address bone health and immune support, aligning with government initiatives to reduce elderly healthcare costs. India presents a contrasting dynamic, where Amul's cooperative model and extensive rural distribution network are democratizing access to dairy snacks in tier-two and tier-three cities, though cold-chain gaps in rural areas remain a binding constraint. Australia's market is mature, with stable consumption and a focus on premium, grass-fed dairy exports to Asia, while Indonesia, Malaysia, and Singapore are emerging hotspots where rising incomes and Westernizing diets are fueling demand for refrigerated snacks.

The Rest of Asia-Pacific, encompassing markets like Vietnam, Thailand, and the Philippines, is experiencing rapid urbanization and modern trade expansion that are unlocking latent demand for dairy snacks. In Vietnam, the proliferation of convenience stores operated by chains like Vinmart is improving access to chilled products in urban centers, though rural penetration lags due to inadequate cold-chain infrastructure. Regulatory frameworks vary significantly across the region: FSSAI in India mandates fortification levels and allergen labeling, while ASEAN's harmonization efforts under the ASEAN Food Safety Network are reducing cross-border trade barriers but remain incomplete. The geographic segmentation reveals a region where growth is concentrating in urban corridors with robust cold-chain logistics, while rural and semi-urban areas await infrastructure investments that can extend refrigerated distribution beyond tier-one cities. This bifurcation creates opportunities for brands that can tailor product formats, such as ambient-stable dairy snacks or ultra-high-temperature (UHT) processed options, to regions where refrigeration remains scarce.

Competitive dynamics in the Asia-Pacific differ markedly from Western markets. Local cooperatives and regional dairies command a significant share in India and China, leveraging cost advantages and cultural familiarity that multinational entrants struggle to replicate. Amul's brand equity in India, built over decades through its cooperative structure and rural outreach, insulates it from foreign competition, while Yili and Mengniu benefit from government support and scale economies that enable aggressive pricing. In contrast, Japan and Australia are dominated by established players like Meiji and Fonterra, whose innovation pipelines and premium positioning create high barriers for new entrants. The region's growth trajectory is also shaped by demographic trends: Southeast Asia's young, urbanizing population favors convenient, on-the-go formats, while Northeast Asia's aging societies prioritize functional benefits and health claims. This heterogeneity demands localized strategies that account for income levels, dietary traditions, and infrastructure maturity, making Asia-Pacific both the most promising and most complex geography for dairy snack expansion.

Regulatory Landscape

Regulation for dairy snacks is shaped by food safety standards, allergen declarations, and claim substantiation across major markets, with notable recent updates in China, the European Union, and the United States that affect formulations and cross-border supply. In China, the National Food Safety Standard for Fermented Milk (GB 19302-2025) entered into force on September 16, 2025, and the National Food Safety Standard for Cream, Butter, and Anhydrous Milk Fat (GB 19646-2025) entered into force on March 16, 2026, tightening microbial and compositional requirements that carry through yogurt-based snacks and dairy-fat inputs used in spreads, frozen dairy snacks, and inclusions.

Competitive Landscape

The dairy snacks market exhibits moderate concentration, as multinational giants like Nestlé, Danone, and Lactalis coexist with powerful regional cooperatives such as Amul, Fonterra, and FrieslandCampina that leverage local supply chains and cultural resonance. Strategy patterns cluster around three axes: scale players pursue cost leadership through vertical integration and procurement efficiencies, premium brands differentiate via organic certification and regenerative agriculture claims, and functional innovators layer in probiotics and protein fortification to justify price premiums.

Opportunities are emerging in hybrid formats, such as cottage cheese ice cream and dairy-probiotic beverages, that blur category boundaries and capture consumers seeking both indulgence and nutrition. Smaller entrants are disrupting incumbents by targeting niche segments: lactose-free cheese snacks in East Asia, A2 milk-based yogurts in Australia, and upcycled whey protein snacks in Europe exemplify how startups exploit underserved needs that large portfolios overlook.

Technology is becoming a competitive differentiator, particularly in precision fermentation and enzyme engineering that enable lactose-free processing at scale. Danone's investment in microbial strain libraries for probiotic yogurts and Nestlé's partnerships with ingredient suppliers to develop clean-label stabilizers illustrate how R&D intensity is separating leaders from laggards. The landscape is further complicated by private-label expansion in Europe, where retailers like Aldi and Lidl are vertically integrating into dairy production, compressing margins for branded suppliers. This dynamic is forcing multinationals to either premiumize their portfolios or exit low-margin categories, a strategic inflection point that will reshape market structure over the next five years.

Dairy Snack Industry Leaders

-

Nestlé S.A.

-

Danone S.A.

-

Lactalis Group

-

Fonterra Co‑operative Group

-

Unilever Plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

White space is concentrated in functional, portion-controlled dairy snacks that combine high protein and digestive-health positioning with portable packaging formats. Product moves in 2026 reflect active focus on protein and probiotic fortification, including Bel Brands USA launching Babybel PRO and Kraft Natural Cheese debuting Protein Cheese Sticks, which support a defensible shelf position versus protein bars and other better-for-you snack alternatives. Packaging and format innovation is also a near-term lever, particularly for yogurt pouches and ready-to-drink functional dairy beverages that fit on-the-go usage and omnichannel grocery as online cold-chain capability improves.

Recent Industry Developments

- July 2026: Land O'Lakes announced an investment to expand its Tulare, California dairy processing facility to increase production of ultra-filtered milk and high-value dairy proteins. The investment improves supply of protein-forward dairy bases used in fast-growing snack formats such as drinkable yogurts, smoothies, and fortified dairy beverages.

- October 2025: Frigo Cheese Heads expanded its snack cheese lineup with two new flavors and larger pack sizes, including Snack Sticks offered in 12-count packs. The update reinforces value-through-format strategies in cheese snacks, supporting household stocking and shareable occasions where mass-tier volumes are concentrated.

- November 2024: Nestle announced initial steps of its Dairy Plan to focus on lower-footprint dairy supply. The announcement signals a strategic pivot toward sustainable dairy procurement that supports premium and clean-label snack propositions in markets where packaging and sourcing scrutiny is rising.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the dairy snack market covers packaged, ready-to-eat dairy based products that are positioned and purchased for snacking occasions, across retail and online channels, and counted in value terms at selling prices in each country.

Scope exclusions: We exclude non-dairy snacks and dairy items mainly sold as meal ingredients (for example, plain cooking cream and bulk cheese blocks) when they are not marketed as snacks.

Segmentation Overview

-

Product Type

- Cheese snacks

-

Yogurt-based snacks

- Spoonable yogurts

- Drinkable yogurts

- Smoothies

- Ice Cream and Frozen Dairy Snacks

- Milk- and Cream-Based Snacks

- Others

-

Price Tier

- Mass

- Premium

-

Packaging Format

- Canned

- Pouches

- Cartons / Tetra‑packs

- Others

-

Distribution Channel

- Hypermarkets/Supermarkets

- Convenience/Grocery Stores

- Online Retail Stores

- Other Distribution Channels

-

Geography

-

North America

- United States

- Canada

- Mexico

- Rest of North America

-

Europe

- Germany

- United Kingdom

- Italy

- France

- Spain

- Thailand

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- Australia

- Rest of Asia-Pacific

-

South America

- Brazil

- Argentina

- Rest of South America

-

Middle East and Africa

- South Africa

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries, build the country list, and gather the baseline demand and supply signals that a dairy snack model needs. We referenced public sources such as USDA data for dairy categories, FAOSTAT for production and consumption context, UN Comtrade for trade flows of key dairy items, and food labeling and standards documents from bodies like the FDA and the European Commission.

To link those macro signals to snack products, we reviewed company filings, investor presentations, annual reports, and retailer and association websites for category language, channel mix, and pricing context. We also used paid subscriptions for company financials and for shipment-level trade records to reduce gaps on smaller brands and to cross-check import dependence in select markets. The sources listed here are illustrative only, and many other public and paid references were also used for data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary interviews and structured surveys were run with manufacturers, ingredient suppliers, packaging participants, distributors, and retail category managers to confirm what is actually bought as a snack and how it is priced across channels. Since this is a global market, inputs were validated across major demand centers in APAC, EMEA, and the Americas, and then assumptions were aligned to what respondents describe in yogurt, cheese, and other snackable dairy sub-categories.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 15% | APAC: 46% |

| Mid tier: 59% | Functional/Unit leaders: 33% | EMEA: 31% |

| Smaller Players: 15% | Managers: 52% | Americas: 23% |

Market-Sizing & Forecasting

The core model starts with a top-down build, where dairy consumption and trade indicators are translated into a snackable demand pool using penetration and packaging cues, and then value is reconstructed using country price levels. We then sanity-check totals using selective bottom-up approximations, such as sampled price-per-pack multiplied by estimated volumes in key channels, followed by supplier and distributor checks for directionally correct splits.

A few variables that materially move the result were tracked and updated, including the mix shift between cheese snacks and yogurt-based snacks, average pack sizes and multi-pack prevalence, retail price progression by format, online share of snack purchases, and cold-chain and shelf-life constraints that affect distribution reach. Where product boundaries were blurred, assumptions were tightened using interview feedback on what is marketed as a snack versus a staple dairy item, and gaps in smaller countries were handled through proxying from comparable markets with adjusted income and channel structure.

For forecasting, scenario analysis was applied so that growth reflects realistic changes in snacking frequency, premium versus mass mix, and channel expansion, and then the scenarios were aligned to expert consensus from primary research before finalizing the outlook.

Data Validation & Update Cycle

Outputs were triangulated across multiple signals, including macro dairy indicators, trade direction, pricing benchmarks, and respondent-confirmed channel dynamics, and then large variances were investigated before sign-off. When a country result looked out of line, the inputs were re-checked, and follow-up calls were triggered to revalidate the key driver, such as pack-price movement or the snack versus staple split.

A multi-step review is followed internally so assumptions, conversions, and growth paths stay consistent across regions and product formats. The report is refreshed annually, and interim updates are made when material events occur, such as major pricing shocks, regulatory labeling changes, or trade disruptions. Before delivery, we run a final refresh pass so clients receive the most current view available at the time of publication.

Mordor Intelligence's Dairy Snack Market Size Versus Other Published Estimates

Published dairy snack market values often look far apart because each publisher draws the line differently on what counts as a snack, which channels are counted, and which price points are used for valuation. Differences also show up when one estimate is anchored to a later base year, or when currency timing and inflation assumptions are applied unevenly.

Ice cream and other frozen dairy treats are the biggest swing item, and these are included in Mordor Intelligence's scope when they are positioned and sold as snack products rather than as a dessert or bulk take-home item, which changes the counted volume and the average price level used in the model.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 253.11 B (2025) | |

| Trade Statistics Outlet A | USD 63.21 B (2024) | This figure is framed as a sub-set within a broader snacks taxonomy and typically reflects a narrower product mapping for dairy snacks, which can undercount snackable dairy formats that do not sit cleanly in trade or snack category definitions. |

| Publisher-Led Survey B | USD 27.72 B (2024) | The estimate appears to use a tighter definition centered on a limited list of dairy snack types and consumer cohorts, and it can miss parts of the ready-to-eat dairy snack universe when products are counted only under select retail categories. |

The spread in published values is mainly explained by how wide the product list is, how snack occasions are interpreted, and whether pricing is built from country-level pack prices or broader category averages. By keeping the scope rules explicit and checking them with channel and category interviews, our total stays traceable to repeatable inputs and is easier to reconcile across regions.

Key Questions Answered in the Report

What is the current Dairy Snack Market size?

The Dairy Snack Market is projected to register a CAGR of 5.37% during the forecast period (2026-2031)

Which product sub-category is growing fastest within cheese-based snacks?

Yogurt-based snack formats lead growth at a 6.89% CAGR, propelled by probiotic fortification and on-the-go drinkable SKUs.

What region offers the highest growth outlook for cheese snacks?

Asia-Pacific shows the strongest trajectory with a 6.07% CAGR, led by China, India, and Southeast Asia.

How are online channels affecting cheese snack distribution?

Online grocery is expanding at a 6.15% CAGR due to investments in last-mile cold-chain delivery, raising direct-to-consumer volumes.

Page last updated on: