Market Overview

| Study Period | 2021 - 2031 |

|---|---|

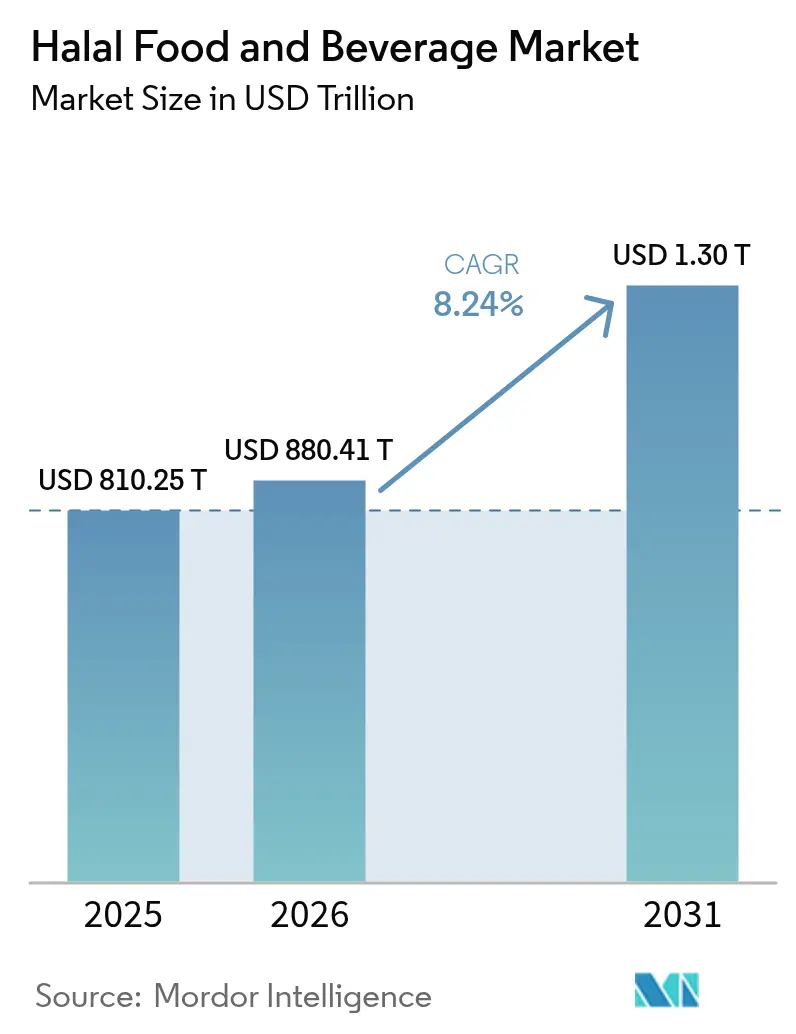

| Market Size (2026) | USD 880.41 Trillion |

| Market Size (2031) | USD 1.30 Trillion |

| Growth Rate (2026 - 2031) | 8.24% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Halal Food And Beverage Market Analysis by Mordor Intelligence

The halal food and beverages market size is expected to increase from USD 810.25 billion in 2025 to USD 880.41 billion in 2026 and reach USD 1,304.21 billion by 2031, growing at a CAGR of 8.55% over 2026-2031. Steady population growth in Muslim-majority economies, rising disposable income among diaspora communities, and the strategic repositioning of certification as a live data layer are together redefining how brands compete. Mandatory regimes such as Indonesia’s Law No. 33/2014, live-scanned QR codes from Singapore’s MUIS, and blockchain pilots by Malaysia’s JAKIM have compressed audit cycles, elevated transparency, and forced multinationals to re-engineer supply-chain visibility. Mergers between sovereign capital and Brazilian protein giants, coupled with widening retail access via e-commerce subscription models, are lifting the addressable base for premium certified products. Fraud incidents still appear, but regulators' appetite for traceability technology is closing those gaps faster than before, reinforcing consumer confidence while raising the cost of non-compliance. Throughout these shifts, the halal food and beverages market continues to pull investment toward poultry, dairy, and functional beverage sub-categories that pair higher margins with rapid certification scalability.

Key Report Takeaways

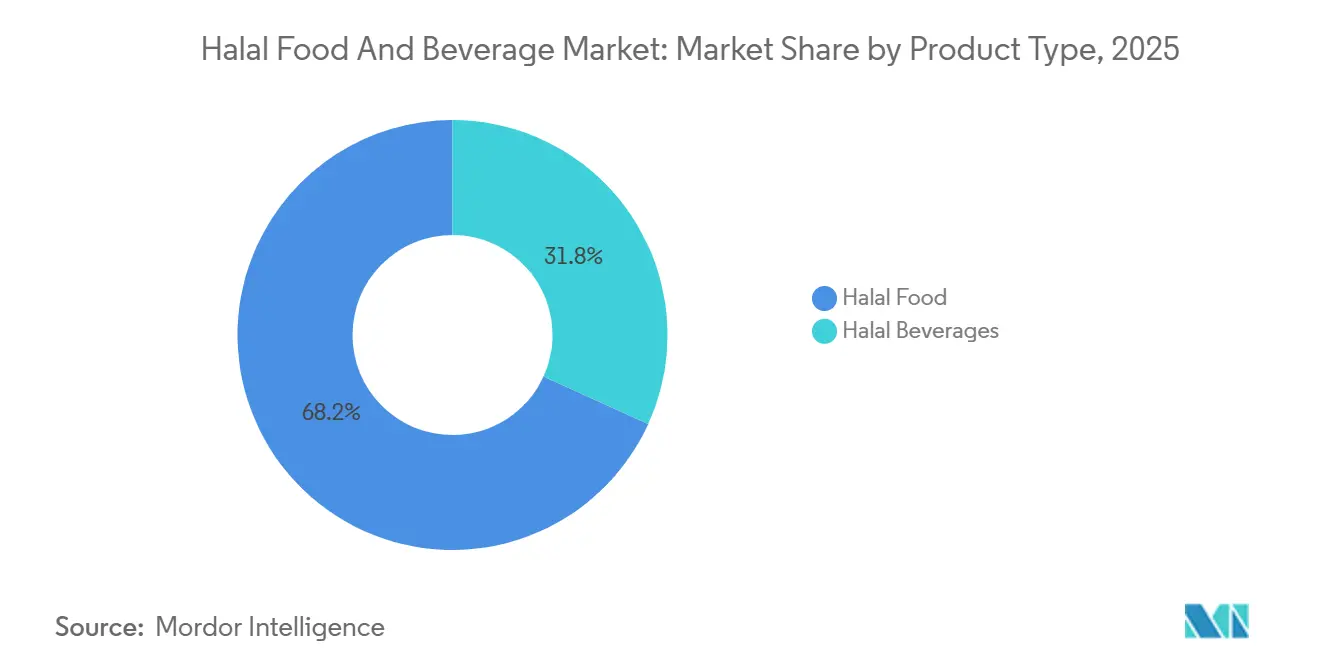

- By product type, halal food captured 68.21% of the halal food and beverages market share in 2025, while halal beverages are projected to advance at a 9.12% CAGR through 2031.

- By form, conventional products held a 72.35% share of the halal food and beverages market size in 2025, yet organic halal lines are forecast to grow at a 9.68% CAGR between 2026 and 2031.

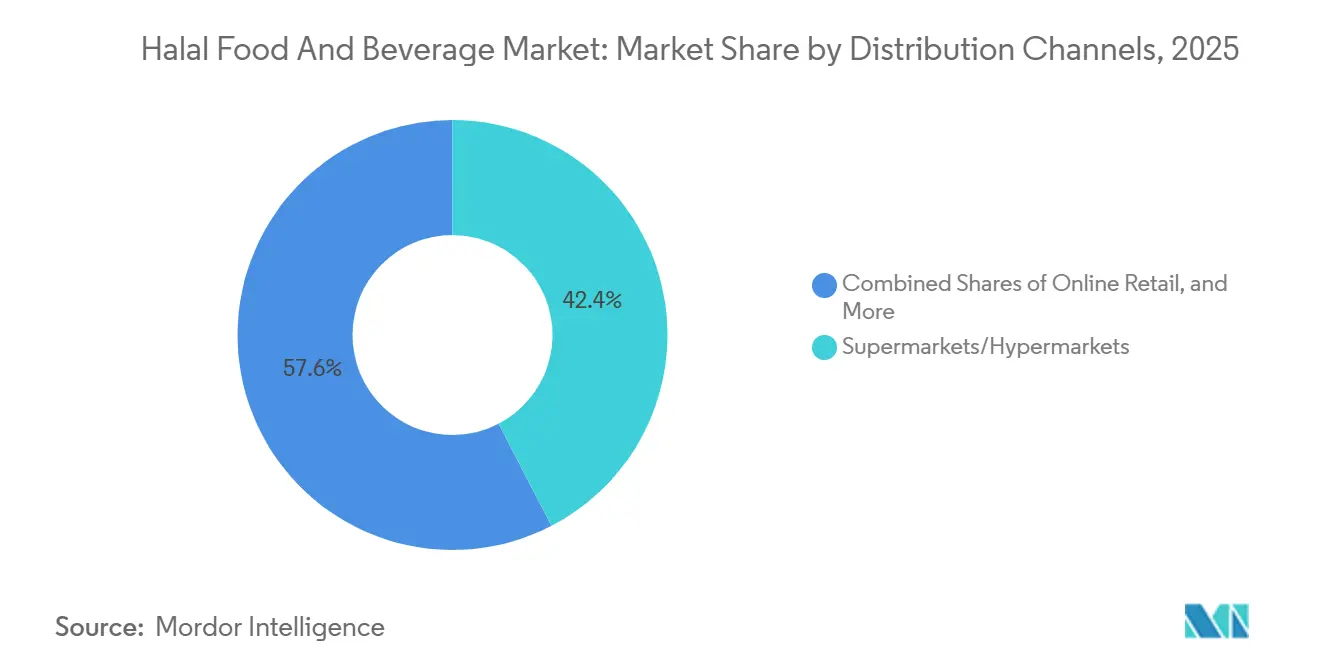

- By distribution channel, supermarkets and hypermarkets led with 42.38% revenue share in 2025, whereas online retail is set to expand at a 10.11% CAGR through 2031.

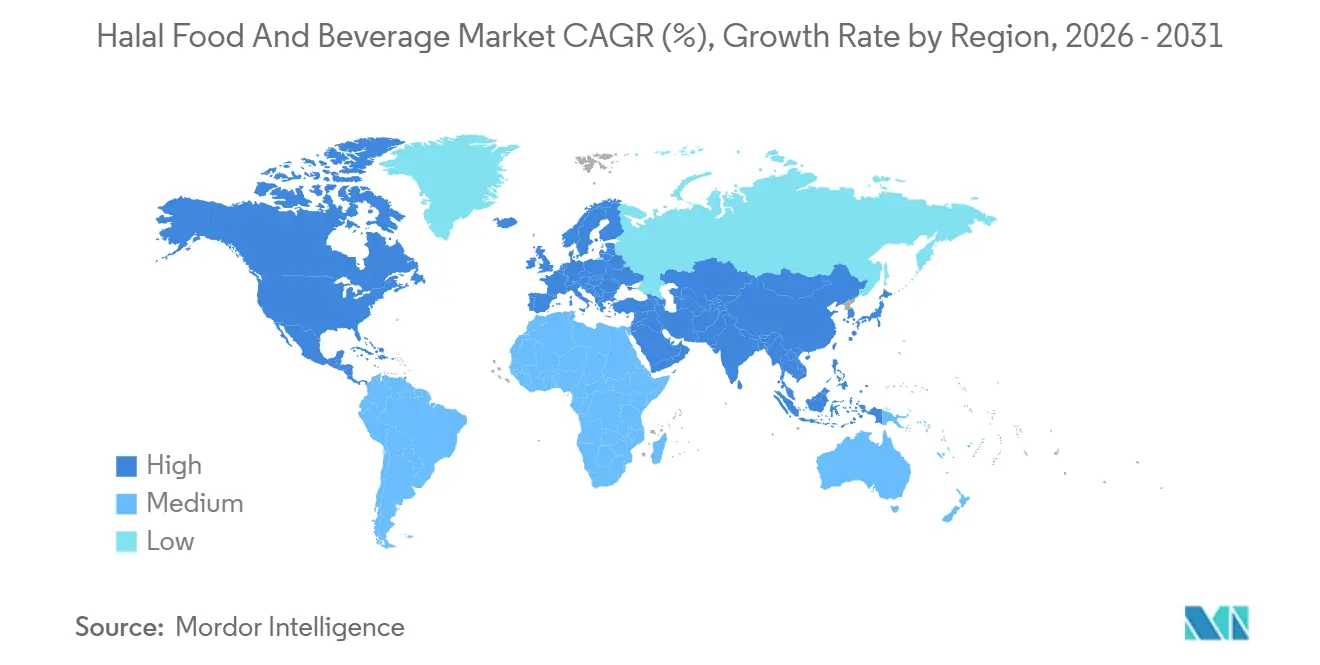

- By geography, Asia-Pacific commanded 55.69% revenue in 2025; the Middle East and Africa region is projected to record the fastest 10.37% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Halal Food And Beverage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Demand and Cultural Awareness for Halal Products | +2.1% | Global, with concentration in Asia-Pacific, Middle East and Africa, and diaspora communities in North America and Europe | Long term (≥ 4 years) |

| Halal Certification as a Symbol of Quality and Trust | +1.8% | Global, particularly Southeast Asia, Middle East, and emerging adoption in Europe and North America | Medium term (2-4 years) |

| Government Initiatives Supporting Halal Production Standards | +2.3% | Asia-Pacific, Middle East, spill-over to Africa | Short term (≤ 2 years) |

| Broadening Distribution Channels for Halal Goods | +1.6% | Global, with rapid e-commerce penetration in North America, Europe, and urban Asia-Pacific markets; traditional retail dominance in Middle East & Africa | Medium term (2-4 years) |

| Innovation and New Product Development in Halal Segments | +1.4% | Global, led by plant-based innovation in North America and Europe, functional beverages in Asia-Pacific, organic dual-certification in Western markets | Long term (≥ 4 years) |

| Impact of Digital Marketing and Social Media on Halal Branding | +1.2% | Global, with highest impact in Southeast Asia , Middle East youth demographics, and diaspora communities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Demand and Cultural Awareness for Halal Products

With the growth of the Muslim population and the expansion of its diaspora, retail assortments are undergoing significant changes, moving beyond the confines of traditional ethnic aisles. In the Asia-Pacific and Africa regions, Indonesia, where 87% of the population identifies as Muslim, and Nigeria, home to 110 million Muslim consumers, serve as key demand drivers. However, the most notable strategic shift is taking place in non-Muslim-majority markets. In these regions, halal certification has evolved beyond its religious roots to symbolize ethical slaughter, traceability, and hygiene standards. These attributes strongly appeal to flexitarian and health-conscious consumers. During 2024-2025, Tesco and Carrefour expanded their halal-certified private-label product ranges in the United Kingdom and France. This strategic move repositions halal certification as a mainstream quality indicator rather than a niche religious requirement. The growing elasticity in demand highlights a critical insight: brands that treat halal certification as a mere compliance formality risk losing market share to competitors who integrate it as a fundamental aspect of their product development and differentiation strategies.

Halal Certification as a Symbol of Quality and Trust

Certification bodies are transitioning from traditional paper-based audits to sophisticated digital verification systems that establish trust at the transaction level. In October 2025, the Islamic Religious Council of Singapore launched QR-code certificates, enabling consumers to scan product packaging to access real-time audit trails, abattoir video feeds, and ingredient sourcing maps. This innovation transforms certification from a static logo into an interactive assurance tool[1]Source: Islamic Religious Council of Singapore, “Halal Certification Services,” muis.gov.sg. Similarly, in 2025, JAKIM initiated a pilot project to integrate artificial intelligence and blockchain into its certification processes. This initiative aims to reduce audit cycle times from weeks to days while creating tamper-proof records to prevent counterfeit labels. These technological advancements highlight that certification premiums will increasingly favor bodies offering digital transparency over traditional theological endorsements. Consequently, brands are compelled to select certification partners based on their API compatibility and data-sharing capabilities.

Government Initiatives Supporting Halal Production Standards

Sovereign mandates are compressing certification timelines and raising compliance costs, but they simultaneously unlock scale by standardizing fragmented regional norms. Indonesia's mandatory halal certification, enforced from October 17, 2024, required all food and beverage products sold domestically to carry BPJPH approval, a policy shift that BPJPH met by processing over 1 million certificates within the first year. Malaysia's MyHalal Portal, launched in 2025, digitized application workflows and reduced average approval times by 30%, enabling small and medium enterprises to enter export markets previously dominated by multinationals with dedicated compliance teams[2]Source: Department of Islamic Development Malaysia, “Malaysia Halal Certification,” halal.gov.my. Saudi Arabia's Vision 2030 framework prioritizes domestic halal protein production, catalyzing JBS's USD 85 million poultry expansion in January 2026 and BRF's USD 160 million Jeddah facility, both designed to substitute imports with locally certified capacity. These initiatives reveal that regulatory harmonization, not fragmentation, is accelerating, rewarding firms that invest in multi-jurisdiction certification infrastructure.

Broadening Distribution Channels for Halal Goods

E-commerce is breaking down geographic barriers that once restricted halal products to ethnic grocers and specialty stores. In 2024-2025, Amazon expanded its halal-certified product offerings across North America and Europe. At the same time, platforms like Wehalal and HalalWorldDepot adopted direct-to-consumer subscription models, bypassing wholesale intermediaries to achieve higher margins. Online retail stores are expected to grow at the fastest CAGR through 2031, driven by digital-native Muslim consumers who value convenience and a wide assortment over physical proximity. This shift requires brands to adopt a dual fulfillment strategy—ensuring shelf presence in traditional retail while building direct connections through owned e-commerce platforms and third-party marketplaces that provide subscription services, auto-replenishment, and personalized curation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Regulatory and Safety Compliance Requirements | -1.1% | Global, with highest complexity in multi-jurisdiction exporters navigating, and emerging European standards | Medium term (2-4 years) |

| Elevated Costs Associated with Halal Certification Processes | -0.9% | Global, disproportionately affecting small and medium enterprises in Asia-Pacific, Africa, and South America lacking dedicated compliance budgets | Short term (≤ 2 years) |

| Low Awareness Levels Among Consumers in Non-Muslim Markets | -0.7% | North America, Europe, and Latin America, where halal remains conflated with ethnic food rather than quality assurance | Long term (≥ 4 years) |

| Challenges from Fraud and Mislabeling in Halal Supply Chains | -0.6% | Global, with acute incidents in fragmented supply chains across South Asia, Africa, and Eastern Europe lacking digital traceability | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory and Safety Compliance Requirements

Multi-jurisdiction exporters face a compliance labyrinth in which JAKIM, BPJPH, MUIS, and the Emirates Authority for Standardization and Metrology (ESMA) impose overlapping yet non-harmonized audit protocols, ingredient whitelists, and documentation formats. Organic halal products confront dual-certification complexity, requiring simultaneous adherence to USDA Organic or EU Organic standards alongside halal theological requirements, a process that extends time-to-market by 3-6 months and inflates certification fees by 40-60% relative to single-label products[3]Source: United States Department of Agriculture, “Organic Standards,” usda.gov. Small and medium enterprises in Africa and South America, lacking dedicated regulatory affairs teams, often abandon export ambitions or partner with certification consultants who command 15-20% of first-year export revenue, compressing margins and deterring market entry. This regulatory friction suggests that certification bodies offering mutual recognition agreements and unified digital portals will capture disproportionate market share, as brands prioritize jurisdictions that minimize redundant audits.

Elevated Costs Associated with Halal Certification Processes

Certification fees, annual audits, and supply-chain traceability infrastructure impose fixed costs that disproportionately burden small producers. Initial halal certification in Malaysia ranges from MYR 1,000 to MYR 10,000 (USD 220 to USD 2,200), with annual renewal audits adding 30-50% of the initial fee, while Indonesia's BPJPH charges vary by product category and production volume, creating cost unpredictability that deters long-term planning. Blockchain-based traceability pilots, though promising for fraud deterrence, require capital expenditures of USD 50,000 to USD 200,000 for enterprise resource planning integration, sensor deployment, and staff training, costs that only large multinationals can absorb without external financing. This cost asymmetry is concentrating market share among vertically integrated players such as Almarai, BRF, and JBS, who amortize certification expenses across high-volume production runs, while fragmented regional processors struggle to justify compliance investments against thin margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Beverages Outpace Traditional Food Growth

Halal beverages are projected to achieve a strong CAGR of 9.12% through 2031. This growth rate is expected to surpass the broader halal food and beverages market, reflecting a shift in consumer preferences toward energy drinks, functional waters, and non-alcoholic malt alternatives. In 2025, the energy drink brand Carabao, newly certified, expanded into Southeast Asian convenience chains and secured placements in Gulf hypermarkets, showcasing its cross-regional brand expansion. Halal food retained a dominant 68.21% share of the 2025 market value, supported by well-established certification processes and cold-chain logistics. Meanwhile, dairy products gained momentum from Arla's capacity expansion in Bahrain, which positioned European cheese under halal certification for Middle Eastern consumers.

The confectionery, bakery, and snack segment continues to deliver steady but commoditized volumes. However, the growing demand for ready meals and baby food, especially those with dual halal-organic certifications, demonstrates a premium elasticity of 25-40% compared to standard offerings. Halal-certified plant-based proteins, now approved in multiple jurisdictions, align with sustainability, animal welfare, and religious values, creating a new premium segment within the halal food and beverages market. While theological clarity on plant-based certifications is still developing, proactive audits are fostering acceptance and unlocking additional revenue opportunities for innovators in the alternative protein sector.

By Form: Organic Halal Commands Premium Despite Dual-Certification Complexity

In 2025, conventional products accounted for 72.35% of the revenue share, driven by simplified audit processes and pricing aligned with the purchasing power in Asia-Pacific and Africa. On the other hand, organic halal products are expected to grow at a CAGR of 9.68% from 2026 to 2031, surpassing the growth rate of the overall halal food and beverage market. Western consumers, motivated by higher disposable incomes and a focus on sustainability, are willing to pay a premium of 30-50% for products that guarantee both pesticide-free standards and religious compliance.

Although dual audits result in additional paperwork and costs, major brands spread these expenses across their global operations and recover them at the retail level. In Indonesia and Malaysia, SMEs often avoid entering the organic segment, despite their proximity to organic farms, due to financial limitations. This has allowed European and North American exporters to capitalize on the margins. As certification bodies work toward mutual recognition agreements, audit redundancies could decrease over time, potentially increasing participation in the organic segment of the halal food and beverage market.

By Distribution Channel: Online Retail Disrupts Traditional Shelf Dominance

Supermarkets and hypermarkets, spearheaded by major players such as Tesco, Carrefour, and Walmart, contributed 42.38% of the revenue projected for 2025. These retailers, along with prominent regional competitors, have allocated entire gondolas to certified goods, reflecting their commitment to catering to the growing demand for halal products. On the other hand, online stores are projected to achieve a robust 10.11% CAGR, marking the fastest growth among all distribution channels. This trend highlights the increasing reliance of digital-native Muslim millennials on subscription-based services and same-day delivery options, which align with their convenience-driven shopping preferences.

Direct-to-consumer models are emerging as a significant growth driver, capturing margins 40-50% higher than traditional wholesale channels. These models also generate valuable first-party customer data, enabling businesses to implement rapid iteration cycles and tailor offerings to consumer needs. While ethnic grocers and traditional butchers continue to hold cultural significance, they are facing challenges due to narrowing profit margins as e-commerce gains traction. To adapt to this shift, retailers are upgrading their loyalty applications with enhanced features such as recipe suggestions, QR-code-based product verification, and curated Ramadan bundle deals to attract and retain customers. In the evolving halal food and beverage market, the ability to seamlessly integrate omnichannel strategies will be a critical factor for long-term success.

Geography Analysis

In 2025, Asia-Pacific contributed 55.69% of global revenue, driven by Indonesia's mandatory certification, which resulted in over 1 million new approvals within a year. Malaysian SMEs utilized the MyHalal Portal to enhance export readiness, reducing approval times by a third and gaining access to Middle Eastern shelves. India's 2025 voluntary halal labeling amendment has the potential to reach 200 million Muslim consumers, but variations in state-level enforcement and disputes over certifying authority limit immediate gains. In China, processors in Xinjiang and Ningxia primarily focus on meeting domestic demand for the country's 25 million Muslims, avoiding politically sensitive exports.

The Middle East and Africa are expected to witness the highest growth, with a forecasted CAGR of 10.37% through 2031. Gulf states are expanding domestic poultry and dairy production to support food security initiatives. JBS has allocated USD 85 million to double poultry production in Saudi Arabia, while BRF has invested USD 160 million in a Jeddah facility with an annual capacity of 40,000 tonnes. West Africa, with its 110 million Muslim consumers and growing middle class, holds significant potential, though challenges such as cold-chain limitations and inconsistent enforcement remain. Egypt's strategic port location positions it as a potential distribution hub, but bureaucratic certification delays deter investment.

North America and Europe are experiencing slower growth rates but benefit from higher per-unit margins. Fragmented private certifications, including IFANCA and HMA, create consumer confusion but also provide opportunities for premium narratives linking animal welfare to halal principles. In 2025, retailers increased shelf space for private-label certified products, with Carrefour France reporting double-digit unit growth. South America remains focused on exports, with Brazil and Argentina supplying beef and poultry to Gulf and Southeast Asian markets, leveraging existing slaughter capacities despite low domestic awareness. Across these regions, integrating tech-enabled audits with local sourcing narratives will be critical for companies aiming to strengthen their competitive position in the halal food and beverages market.

Competitive Landscape

The competitive landscape is moderately concentrated. Almarai plans to invest USD 4.8 billion to increase Saudi poultry production from 250 million to 450 million birds annually by 2026, aligning with national self-sufficiency objectives. BRF's Jeddah plant, equipped with advanced high-pressure technology, is expected to produce 40,000 tonnes and achieve a 15-20% price premium over conventional imports. Tanmiah has enhanced its processing capabilities through agreements signed in March and February 2025 with Griffith Foods and Vibra, respectively. These partnerships incorporate seasoning and automation, enabling Tanmiah to launch a differentiated marinated line and improve per-kilo margins.

Sovereign capital investments are driving the next phase of industry growth. Marfrig, in collaboration with Saudi Arabia's Public Investment Fund, is developing the USD 2 billion Sadia Halal venture, which is targeting a 2027 IPO. This initiative secures upstream protein supplies while strengthening downstream retail operations. Additionally, smaller consultancies from Malaysia and Indonesia are leveraging their certification expertise. By acting as compliance partners for multinationals entering fragmented markets, they capture up to 15% of first-year export sales.

Innovation is centered around organic dairy alternatives, dual-sealed plant-based meats, and blockchain-based audit systems. Early adopters of this traceability, driven by JAKIM's AI-blockchain pilot, are likely to experience reduced counterfeiting risks and faster port clearances, creating a competitive advantage. Direct-to-consumer platforms such as Wehalal and HalalWorldDepot are utilizing subscription models to stabilize demand fluctuations and gather insights for product development, an edge that traditional wholesalers struggle to achieve without significant digital transformation. These agile players are pressuring established companies to modernize and remain competitive in the evolving halal food and beverage market.

Halal Food And Beverage Industry Leaders

Arla Foods A.m.b.A

Midamar Corporation

BRF S.A.

Nestlé S.A.

Al Islami Foods LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Deli Halal introduced a new range of halal-certified sliced meats. The products emphasize quality, transparency, and sustainability, using High Pressure Pasteurization (HPP) for natural preservation without excessive chemicals, aligning with both halal standards and mainstream trends for clean-label foods.

- October 2025: MMU alumnus Gisnervern Arikrishnan, through his company Leafhaus, launched the world's first halal sterilized Masala Tea in a can. This innovation blends traditional Malaysian masala tea with modern canning technology for convenience and extended shelf life, targeting health-conscious consumers with low-sugar, antioxidant-rich formulation.

- February 2025: Paris Baguette, under SPC Group, launched its first halal-certified Regional Halal Food Hub in Johor, Malaysia. The facility features seven advanced production lines capable of 100 million bakery products annually, strengthening global supply chains for halal breads, pastries, and frozen dough.

Global Halal Food And Beverage Market Report Scope

Halal food and beverages constitute products prepared strictly by Islamic dietary law. Halal products are considered lawful and hygienic. The halal foods and beverages market is segmented by type, distribution channel, and geography. By type, the market is segmented into halal food, halal beverages, and halal supplements. By distribution channel, the market is segmented into supermarkets and hypermarkets, convenience stores, online retail stores, and other distribution channels. Furthermore, by geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. The market sizing has been done in value (USD) for all the abovementioned segments.

Product Type

| Halal Food | Dairy and Dairy Alternatives | |

| Confectionery | Sugar Confectionery | |

| Chocolates | ||

| Snack Bars | ||

| Others | ||

| Bakery | ||

| Savory Snacks | ||

| Meat, Poultry, and Seafood | Red Meat | |

| Seafood | ||

| Poultry | ||

| Baby Food | ||

| Ready Meals | ||

| Condiments and Sauces | ||

| Other Product Types | ||

| Halal Beverages | ||

By Form

| Conventional |

| Organic |

By Distribution Channels

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| Product Type | Halal Food | Dairy and Dairy Alternatives | |

| Confectionery | Sugar Confectionery | ||

| Chocolates | |||

| Snack Bars | |||

| Others | |||

| Bakery | |||

| Savory Snacks | |||

| Meat, Poultry, and Seafood | Red Meat | ||

| Seafood | |||

| Poultry | |||

| Baby Food | |||

| Ready Meals | |||

| Condiments and Sauces | |||

| Other Product Types | |||

| Halal Beverages | |||

| By Form | Conventional | ||

| Organic | |||

| By Distribution Channels | Supermarkets/Hypermarkets | ||

| Convenience Stores | |||

| Online Retail Stores | |||

| Other Distribution Channels | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Sweden | |||

| Poland | |||

| Belgium | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Vietnam | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Peru | |||

| Colombia | |||

| Rest of South America | |||

| Middle East and Africa | United Arab Emirates | ||

| Saudi Arabia | |||

| South Africa | |||

| Nigeria | |||

| Rest of Middle East and Africa | |||

Key Questions Answered in the Report

What is the current value of the halal food and beverages market?

The halal food and beverages market size stood at USD 880.41 billion in 2026 and is projected to reach USD 1,304.21 billion by 2031.

How fast is online retail growing for halal products?

Online retail channels are forecast to grow at a 10.11% CAGR from 2026-2031, the fastest among all distribution formats.

Which region is expected to record the highest growth through 2031?

The Middle East and Africa region is projected to expand at a 10.37% CAGR, outpacing all other geographies.

Why are organic halal products gaining attention?

Organic halal lines combine pesticide-free assurance with religious compliance, drawing 30-50% price premiums and a 9.68% CAGR despite dual-audit costs.

Page last updated on: