Packaged Food Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.61 Trillion |

| Market Size (2031) | USD 8.15 Trillion |

| Growth Rate (2026 - 2031) | 4.28% CAGR |

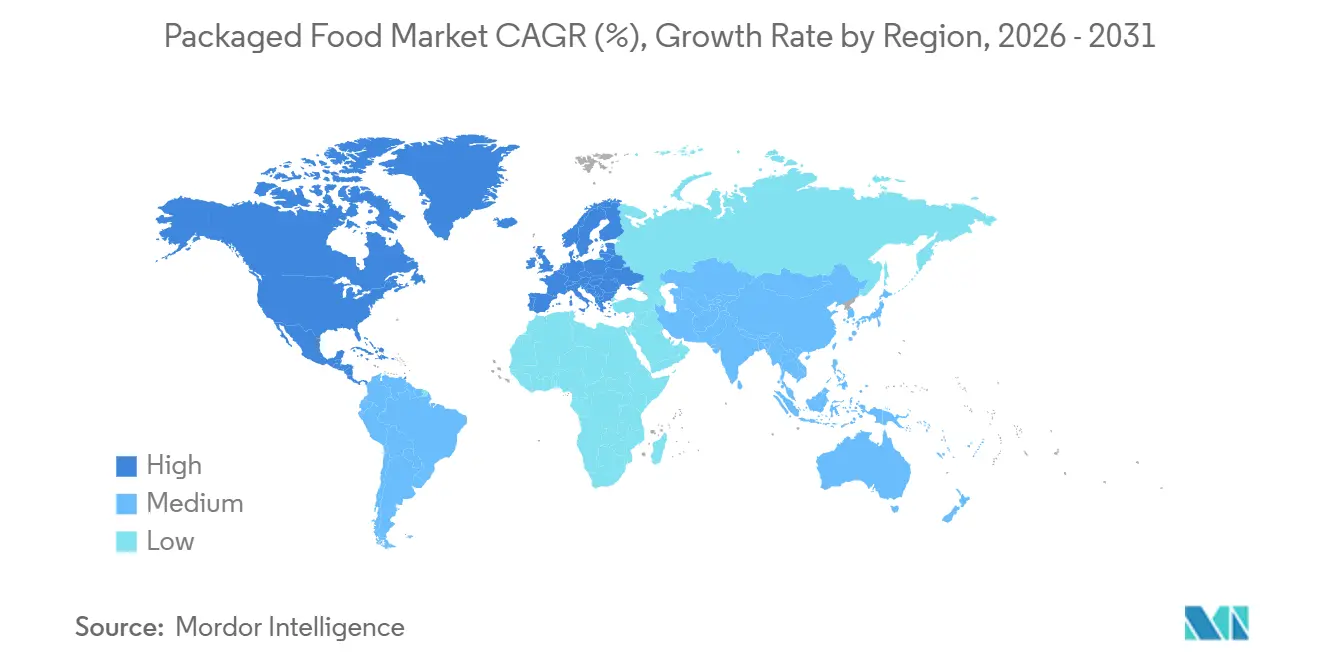

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

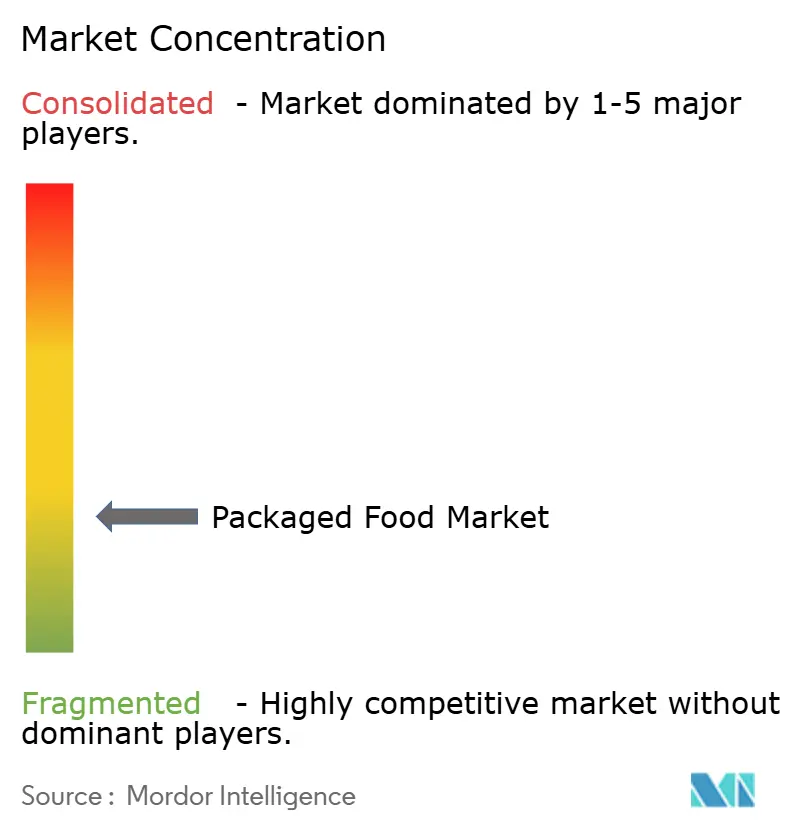

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Packaged Food Market Analysis by Mordor Intelligence

The packaged food market size was valued at USD 6.34 trillion in 2025 and estimated to grow from USD 6.61 trillion in 2026 to reach USD 8.15 trillion by 2031, at a CAGR of 4.28% during the forecast period (2026-2031). Rapid urbanization, rising disposable income in emerging economies, and consumers’ preference for convenient yet nutrient-dense products are redefining category dynamics. Demand is gravitating toward natural, organic, and free-from options, while functional claims such as probiotic, high-protein, and fortified benefits migrate from niche lines into mainstream shelves. Distribution patterns are fragmenting as e-commerce compresses delivery windows below fifteen minutes in dense cities, obliging supermarkets to retrofit micro-fulfillment zones. Meanwhile, sustainability mandates are accelerating material innovation, shifting packaging away from single-use plastics toward fiber-based or enzymatically recyclable substrates, even at a 15-25% cost premium. Competitive intensity in the packaged food market is rising as incumbents prune underperforming SKUs and acquire plant-based specialists to secure relevance with younger cohorts.

Key Report Takeaways

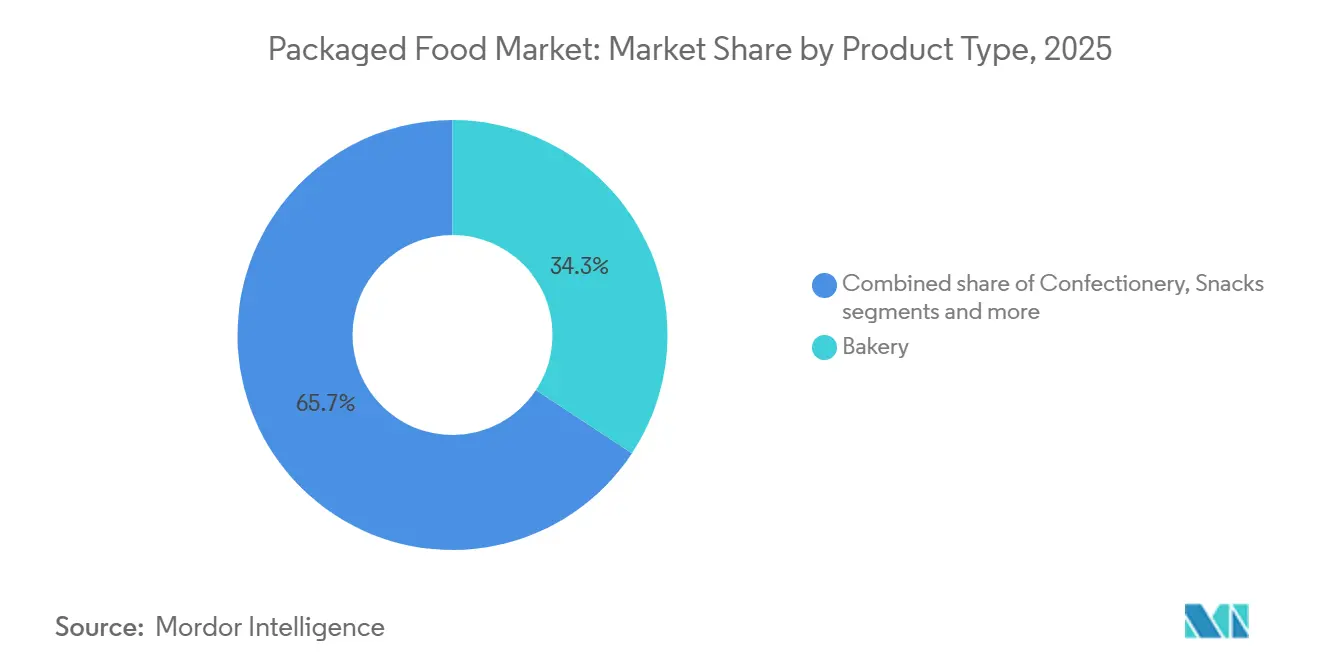

- By prodict type, bakery products led with 34.27% packaged food market share in 2025, whereas dairy and dairy alternatives are projected to grow at a 4.81% CAGR through 2031

- By category, conventional items controlled 76.38% of the packaged food market size in 2025, but the natural, organic, and free-from segment is expected to expand at a 5.43% CAGR to 2031.

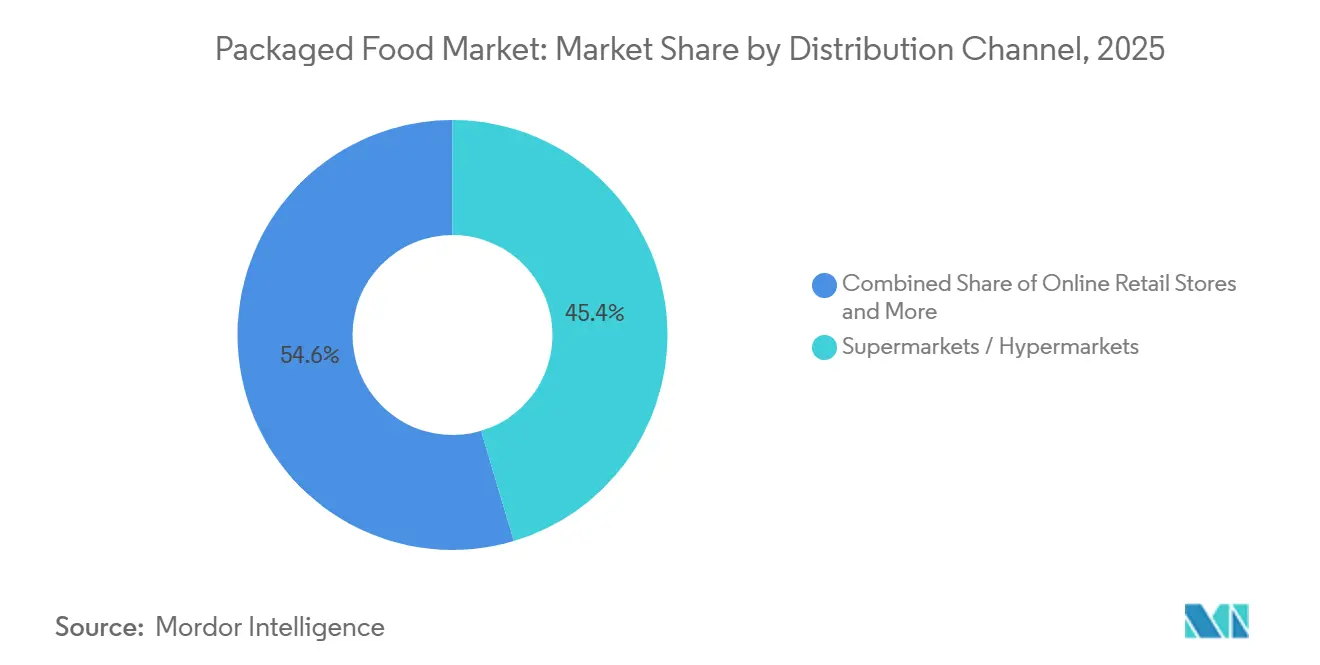

- By distribution channel, supermarkets and hypermarkets captured 45.38% share of the packaged food market in 2025, while online retail is forecast to advance at a 5.57% CAGR during 2026-2031.

- By geography, Asia-Pacific held the largest regional position at 33.67% in 2025, whereas South America is set to deliver the fastest 5.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Packaged Food Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ethnic and global flavor exploration | +0.6% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Increasing demand for functional and health-oriented foods | +0.9% | Global, strongest in North America, Europe, and developed Asia-Pacific markets | Long term (≥ 4 years) |

| Innovation in sustainable and recyclable packaging solutions | +0.5% | Europe (PPWR compliance), North America, spreading to Asia-Pacific | Medium term (2-4 years) |

| Rising consumer preference for clean-label and transparent ingredients | +0.7% | North America & Europe core, expanding to urban Asia-Pacific and South America | Medium term (2-4 years) |

| Growing personalization and dietary preference-based product development | +0.4% | North America, Europe, affluent Asia-Pacific urban centers | Long term (≥ 4 years) |

| Product innovation and premiumization across packaged food categories | +0.8% | Global, with premium tier concentration in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ethnic and global flavor exploration

Growing consumer interest in ethnic and global flavor exploration is significantly driving innovation and product development in the packaged food market. Increasing cultural exposure through travel, digital media, and multicultural urban populations has encouraged consumers to experiment with international cuisines and diverse taste profiles. Packaged food manufacturers are responding by introducing products inspired by Asian, Latin American, Middle Eastern, and Mediterranean flavors to meet evolving taste preferences. This trend is particularly strong among younger consumers seeking novel and authentic culinary experiences in convenient formats. Limited-edition launches, fusion flavors, and regionally inspired recipes are helping brands differentiate their offerings in competitive retail environments in the packaged food market. Additionally, the rising popularity of ready-to-eat meals and snack products featuring global seasonings supports higher consumer engagement and repeat purchases.

Increasing demand for functional and health-oriented foods

Consumers are driving growth in the packaged food market by prioritizing nutrition and preventive health in their daily diets. Rising awareness of lifestyle-related health issues, such as obesity, diabetes, and digestive concerns, is pushing demand for products with enhanced nutritional benefits. The International Diabetes Federation (IDF) reports that in 2024, 589 million adults aged 20-79 lived with diabetes, with projections reaching 853 million by 2050[1] Source: International Diabetes Federation, "Diabetes around the world in 2024”, idf.org. Manufacturers are introducing fortified foods, high-protein snacks, probiotic items, and products enriched with vitamins, minerals, and fiber. Health-conscious buyers increasingly prefer clean-label formulations, reduced sugar content, and natural ingredients. The International Food Information Council’s Food and Health Survey 2024 shows that 67% of Americans consider healthfulness crucial in food and beverage choices, highlighting wellness trends' strong influence on purchasing behavior[2]Source: The International Food Information Council, "2024 IFIC Food & Health Survey,"ific.org. Interest in immunity-boosting and functional ingredients continues to grow in the packaged food market, driven by a focus on long-term health management.

Rising consumer preference for clean-label and transparent ingredients

Consumers are showing a stronger preference for brands that adopt eco-friendly materials, reduce plastic usage, and promote recyclability or biodegradability in packaging formats. Manufacturers are investing in lightweight packaging, paper-based alternatives, and reusable designs to align with sustainability goals while maintaining product safety and shelf life. Sustainable packaging also enhances brand perception, particularly among environmentally conscious consumers seeking responsible consumption choices. According to the 2024 IFIC Food & Health Survey, foods labeled as “Natural,” “Organic,” or “Healthy” are among the top in-store signals, with 36% of American consumers preferring such attributes, reflecting the broader shift toward transparency and sustainability in food products[3]Source: International Food Information Council, “2024 IFIC Food & Health SURVEY”, ific.org. This preference encourages companies in the packaged food market to integrate sustainable packaging with clean-label positioning to strengthen product appeal. As regulatory pressure and consumer expectations continue to rise, sustainable packaging innovation remains a key strategic focus for packaged food manufacturers.

Innovation in sustainable and recyclable packaging solutions

Innovation in sustainable and recyclable packaging solutions is increasingly supporting growth in the packaged food market as environmental concerns influence consumer purchasing behavior. Food manufacturers are adopting recyclable, biodegradable, and compostable materials to reduce environmental impact while maintaining product safety and shelf stability. The shift toward lightweight packaging and reduced plastic usage also helps companies lower transportation costs and carbon emissions. In addition, sustainable packaging enhances brand value and strengthens consumer trust, particularly among environmentally conscious buyers. Governments and regulatory bodies are further encouraging the adoption of eco-friendly packaging through stricter waste management and recycling regulations. Companies in the packaged food market are also investing in packaging designs that improve recyclability without compromising convenience or product quality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns related to sugar, salt, and preservatives | -0.5% | Global, with stringent regulations in Europe, North America, and select Asia-Pacific markets | Short term (≤ 2 years) |

| Rising input, labor, energy, and production costs | -0.8% | Global, acute in energy-intensive manufacturing hubs in Europe and North America | Short term (≤ 2 years) |

| Supply chain disruptions and raw material price volatility | -0.6% | Global, with pronounced impact on commodity-dependent segments and emerging markets | Medium term (2-4 years) |

| Stringent regulatory requirements and compliance costs | -0.4% | Europe (EFSA, PPWR), North America (FDA), Asia-Pacific (FSSAI), South America (ANVISA) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health concerns related to sugar, salt, and preservatives

Growing health concerns related to high levels of sugar, salt, and preservatives are limiting the growth potential of the packaged food market as consumers become more cautious about ingredient consumption. Increasing awareness of lifestyle-related conditions such as obesity, hypertension, diabetes, and cardiovascular diseases has led consumers to scrutinize nutritional labels more carefully. Many packaged food products are often perceived as highly processed, which can discourage health-conscious consumers from frequent consumption. Regulatory bodies across several countries are also introducing stricter labeling requirements and reformulation guidelines to reduce sodium and sugar content in processed foods. This has increased pressure on manufacturers to reformulate products while maintaining taste, texture, and shelf life, often leading to higher production costs. Additionally, negative consumer perception toward artificial preservatives and additives is encouraging a shift toward fresh or minimally processed alternatives in the packaged food market.

Rising input, labor, energy, and production costs

Rising input, labor, energy, and production costs are posing significant challenges to the packaged food market, impacting profitability and pricing strategies for manufacturers. Fluctuations in the cost of raw materials such as grains, dairy, oils, and sweeteners directly affect production expenses, while increasing labor costs add to operational overheads. Energy-intensive processes, including manufacturing, refrigeration, and transportation, further contribute to higher production costs. These rising expenses often force companies to adjust product pricing, which can affect consumer demand, particularly in price-sensitive segments. Supply chain disruptions and inflationary pressures in key markets exacerbate cost volatility, making long-term planning more challenging for manufacturers. Additionally, smaller and mid-sized producers may face greater difficulty absorbing these costs compared to larger, integrated firms, potentially limiting their market competitiveness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dairy Alternatives Disrupt Legacy Categories

Bakery products accounted for the largest share of the packaged food market in 2025, contributing 34.27% of total market revenue, primarily driven by their widespread consumption and strong consumer familiarity across regions. Products such as bread, biscuits, cakes, pastries, and savory baked snacks continue to serve as convenient meal and snacking options for consumers with busy lifestyles. The segment benefits from frequent product innovation, including healthier formulations such as whole grain, high-fiber, and reduced-sugar variants, which help maintain strong demand among health-conscious consumers. In addition, the expansion of organized retail and online grocery platforms has improved product accessibility across the packaged food market and visibility, further strengthening sales performance.

Dairy and dairy alternatives are projected to be the fastest-growing segment in the packaged food market, expected to register a CAGR of 4.81% through 2031. Growth in this segment is largely supported by increasing consumer awareness regarding nutrition, protein intake, and functional health benefits associated with dairy-based products. At the same time, rising lactose intolerance awareness and the growing popularity of plant-based diets have accelerated demand for dairy alternatives such as almond, soy, oat, and coconut-based products. Manufacturers in the packaged food market are actively expanding product portfolios with fortified, low-fat, and probiotic-rich offerings to cater to evolving consumer preferences. The introduction of innovative flavors, convenient packaging formats, and ready-to-consume dairy beverages has further strengthened market expansion.

By Category: Natural and Organic Segments Gain Share

The natural, organic, and free-from category is forecast to grow at 5.43% through 2031, significantly outpacing the conventional segment, which held 76.38% of the market in 2025. This divergence reflects a structural shift in consumer priorities, where ingredient provenance and production methods are becoming primary purchase drivers, particularly among urban millennials and Gen Z cohorts who demonstrate higher willingness to pay for certified organic and non-GMO products. Conventional products remain dominant due to price sensitivity in emerging markets and rural areas, where income constraints limit access to premium-priced alternatives, yet even within this segment, manufacturers are introducing "better-for-you" sub-brands that incorporate whole grains, reduced sodium, and no artificial additives to capture trade-up demand.

Certification standards like USDA Organic, EU Organic, and India Organic are emerging as key differentiators. Retailers are now dedicating premium shelf space to these certified products. Meanwhile, e-commerce platforms are incorporating organic filters, enhancing product visibility. In a notable move, PepsiCo launched an organic snack line under its Frito-Lay brand in 2025. This line, made with non-GMO corn and sunflower oil, raked in USD 120 million in its inaugural year, underscoring the viability of organic positioning even in traditionally commodity-driven sectors. However, the category's expansion faces hurdles. Organic raw materials demand specialized handling and traceability, pushing logistics costs up by 10-15%. This added expense poses challenges, especially for smaller manufacturers looking to enter the market.

By Distribution Channel: E-Commerce Reshapes Retail Economics

Supermarkets and hypermarkets accounted for the largest share of the packaged food market in 2025, representing 45.38% of total sales, primarily due to their extensive product assortment and strong consumer trust. These retail formats offer consumers the advantage of one-stop shopping, allowing them to compare multiple brands, product types, and price ranges within a single location. The availability of promotional offers, bulk purchasing options, and private-label products further strengthens consumer preference for these channels. In addition, well-established supply chains and efficient inventory management enable supermarkets and hypermarkets to maintain consistent product availability, particularly for high-demand packaged food categories.

Online retail is projected to be the fastest-growing distribution channel in the packaged food market, expected to expand at a CAGR of 5.57% during 2026–2031. The increasing adoption of smartphones, improved internet penetration, and the growing popularity of digital payment systems have significantly accelerated online grocery purchases. Consumers are increasingly attracted to the convenience of home delivery, flexible ordering options, and access to a wider range of domestic and international packaged food products. E-commerce platforms in the packaged food market also provide personalized recommendations, subscription-based purchasing models, and competitive pricing, which enhance consumer engagement and loyalty.

Geography Analysis

Asia-Pacific accounted for the largest share of the packaged food market in 2025, holding 33.67% of the global market, driven by its large population base, rapid urbanization, and evolving consumer lifestyles. Rising disposable incomes across countries such as China, India, and other key markets are accelerating growth in the packaged food market. Indonesia and Vietnam have accelerated demand for convenient, ready-to-eat, and value-added food products. The expansion of modern retail infrastructure, including supermarkets, hypermarkets, and e-commerce platforms, has further improved product accessibility across urban and semi-urban areas. In addition, changing dietary patterns, increasing participation of women in the workforce, and growing demand for packaged snacks, dairy products, and frozen foods continue to support strong regional consumption.

South America is projected to register the fastest growth rate, with a CAGR of 5.03% through 2031, supported by improving economic stability, rising urban populations, and increasing adoption of packaged and convenience foods. Countries such as Brazil, Argentina, and Chile are witnessing a gradual shift from traditional fresh food consumption toward packaged alternatives due to changing work patterns and time constraints among consumers. The growing presence of international food brands alongside expanding domestic production capabilities has enhanced product availability and variety in the region.

Europe, North America, and the Middle East & Africa collectively represent mature yet evolving markets characterized by strong demand for premium, health-oriented, and sustainably packaged food products. In North America and Europe, consumer preferences are increasingly shaped by clean-label formulations, organic ingredients, and functional foods, driving innovation among established food manufacturers. Meanwhile, the Middle East & Africa region is experiencing gradual growth supported by rising urbanization, expanding retail infrastructure, and increasing reliance on imported packaged foods, particularly in Gulf Cooperation Council (GCC) countries.

Competitive Landscape

The packaged food market is highly fragmented, with the presence of numerous multinational corporations, regional manufacturers, and private-label brands competing across diverse product categories. Global players such as Nestlé SA, PepsiCo Inc., and Mondelez International maintain strong market positions through extensive product portfolios, strong brand recognition, and well-established distribution networks. However, regional and local manufacturers continue to capture significant market share by offering culturally relevant products, competitive pricing, and localized flavors tailored to regional consumer preferences. The fragmentation of the market encourages continuous innovation, as companies compete through product differentiation, packaging innovation, and value-added offerings to strengthen consumer loyalty and expand their market presence.

Competition in the packaged food market is primarily driven by changing consumer preferences, particularly the growing demand for healthier, clean-label, and functional food products. Leading companies in the packaged food industry are actively investing in research and development to reformulate products with reduced sugar, salt, and artificial additives while maintaining taste and convenience. Mergers, acquisitions, and strategic partnerships are frequently observed as companies seek to expand geographic reach and strengthen supply chain efficiencies. At the same time, private-label brands from large retailers are gaining traction due to competitive pricing and improved quality, intensifying competition for established brands.

The competitive landscape is also shaped by evolving retail channels and technological advancements in distribution and consumer engagement. The rapid growth of e-commerce and omnichannel retailing has enabled both large and small players in the packaged food market to reach wider consumer bases, increasing market accessibility and competition. Sustainability initiatives, including eco-friendly packaging and responsible sourcing, are becoming important differentiators among the packaged food industry participants. While major multinational companies continue to dominate in terms of revenue, the strong presence of regional and niche players ensures that the market remains highly competitive and innovation-driven.

Packaged Food Industry Leaders

-

PepsiCo, Inc.

-

The Coca-Cola Company

-

General Mills Inc.

-

Mondelez International

-

Nestlé SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Campco unveiled three new chocolate offerings at its head office in Mangaluru. The lineup includes Dark Delight dark chocolate, Dome Delight premium truffles, and the newly introduced orange-flavoured Campco Eclairs.

- June 2025: Beeup, the snack brand founded by David Beckham, made its debut at Target, a major US retailer. The brand's fruit snack line, featuring three flavors Very Berry, Tropical Mix, and Sour Watermelon boasts non-GMO credentials. Furthermore, it's marketed as being “free from synthetic dyes” and “fake flavours.” This emphasis on natural ingredients aligns strategically with growing legislative scrutiny on food dyes in the US.

- April 2025: Britannia Industries Ltd has launched its much-anticipated Greek yogurt range, underscoring a pivotal moment in the brand's innovation journey. With this debut, Britannia aims to expand the yogurt category while elevating consumer expectations, spotlighting its commitment to superior flavor, clear formulations, and a modern brand identity.

Global Packaged Food Market Report Scope

Packaged foods are convenience foods produced commercially and distributed for consumer use. The packaging does not just keep food protected to maintain its aesthetic appeal. It also keeps the food fresh so that the taste and quality of the product stay intact. It ensures that the food retains a good shelf life, too, so that customers can keep the item for a set period before it needs to be consumed. The packaged food market is segmented by product type, packaging type, category, distribution channel, and geography. By product type, the market is segmented into dairy and dairy alternatives, confectionery, bakery, snacks, breakfast cereals, meat, poultry and seafood and substitutes, baby food, food spread, ready meals, condiments and sauces and other product types. By category, the market is segmented by conventional and organic. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East & Africa. The market sizing has been done in value terms in USD and volume terms in Tons for all the above mentioned segments.

| Dairy and Dairy Alternatives |

| Confectionery |

| Bakery |

| Snacks |

| Meat, Poultry & Seafood and Substitutes |

| Breakfast Cereals |

| Baby Food |

| Food Spread |

| Ready Meals |

| Condiments and Sauces |

| Other Product Types |

| Conventional |

| Natural/Organic/Free-From |

| Supermarkets / Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Dairy and Dairy Alternatives | |

| Confectionery | ||

| Bakery | ||

| Snacks | ||

| Meat, Poultry & Seafood and Substitutes | ||

| Breakfast Cereals | ||

| Baby Food | ||

| Food Spread | ||

| Ready Meals | ||

| Condiments and Sauces | ||

| Other Product Types | ||

| By Category | Conventional | |

| Natural/Organic/Free-From | ||

| By Distribution Channel | Supermarkets / Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How big will packaged food revenues be by 2031?

The packaged food market is projected to reach USD 8.15 trillion by 2031, reflecting a 4.28% CAGR from 2026 to 2031.

Which product type is growing the fastest?

Dairy and dairy alternatives are forecast to post the highest 4.81% CAGR through 2031 as consumers shift toward plant-based and functional proteins.

What retail channel is expanding most quickly?

Online retail is expected to rise at 5.57% annually, outpacing all other channels due to direct-to-consumer models and rapid delivery services.

Which region offers the strongest growth outlook?

South America leads with an expected 5.03% CAGR to 2031, propelled by e-commerce expansion and improving macroeconomic stability in Brazil and Argentina.

How are brands responding to sustainability demands?

Manufacturers are investing in recyclable and compostable packaging, enzymatic recycling technologies, and blockchain traceability to meet regulatory and consumer expectations.

Page last updated on: