Hospitality Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 9.11 Trillion |

| Market Size (2031) | USD 11.95 Trillion |

| Growth Rate (2026 - 2031) | 5.58% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

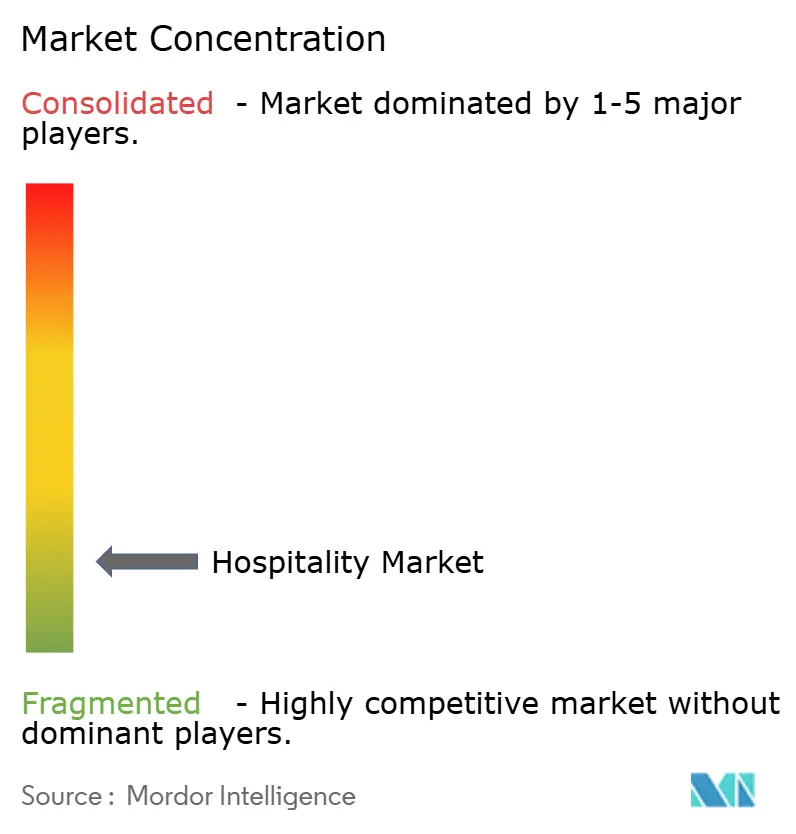

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hospitality Market Analysis by Mordor Intelligence

The Hospitality Market size is projected to be USD 7.47 trillion in 2025, USD 9.11 trillion in 2026, and reach USD 11.95 trillion by 2031, growing at a CAGR of 5.58% from 2026 to 2031.

International tourist arrivals in 2025 rose to 1.52 billion, a 4% increase from 2024, exceeding pre-pandemic levels in several regions[1]UN Tourism, “International Tourist Arrivals Up 4% in 2025 Reflecting Strong Travel Demand Around the World,” UN Tourism, unwto.org. The travel and tourism sector contributed USD 11.6 trillion to GDP, supported 366 million jobs, and recorded USD 2.02 trillion in international visitor spending in 2025, driving lodging demand and market expansion. Competitive intensity remained high, with the top five companies accounting for only 11.2% of market value in 2025. Marriott reported a pipeline of 4,056 properties and nearly 610,000 rooms, highlighting the importance of scale and global development. Growth opportunities were strongest in Asia-Pacific, the Middle East, extended-stay formats, and carbon-certified assets, where supply lagged evolving traveler demand. Labor inflation posed challenges, with hotel labor costs per occupied room rising from USD 42.82 in 2024 to USD 48.32 in 2025, underscoring the need to maintain margin discipline across the market.

Key Report Takeaways

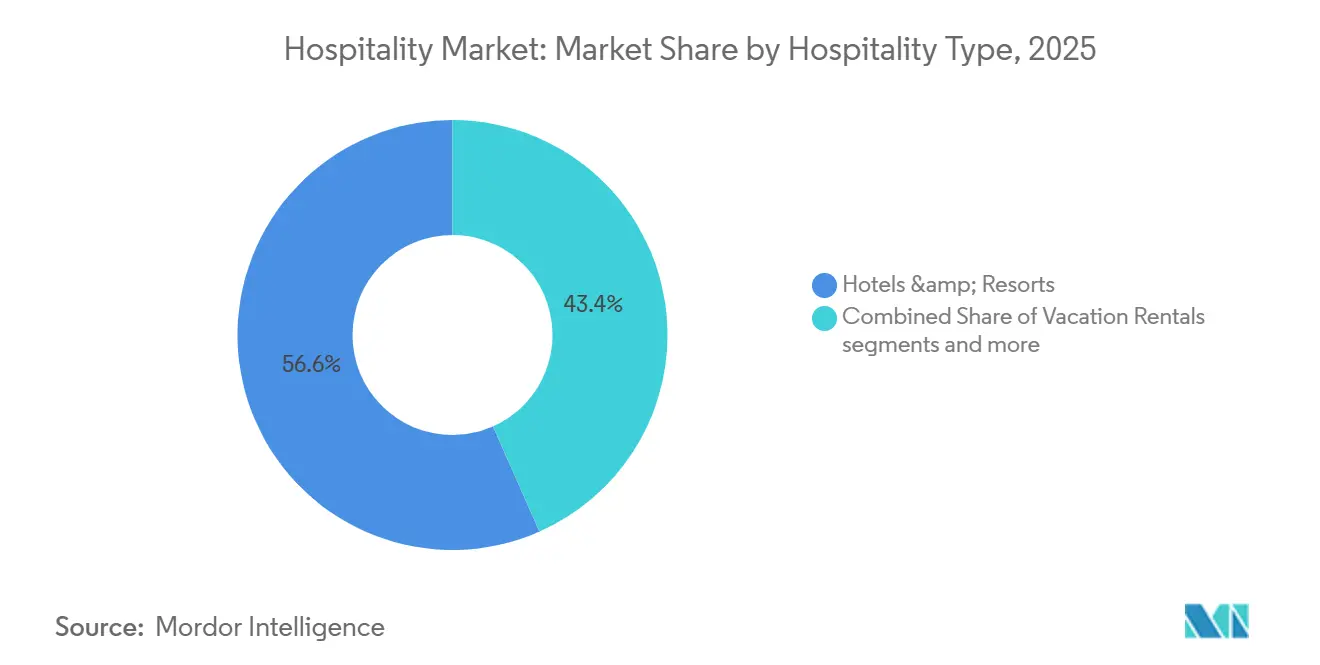

- By hospitality type, Hotels & Resorts held 56.63% of the Global Hospitality Market share in 2025, while Vacation Rentals & Alternative Accommodations are projected to expand at a CAGR of 6.83% through 2031.

- By property type, Chain / Branded Properties accounted for 61.94% share of the Global Hospitality Market size in 2025, while Independent Lifestyle & Boutique Properties are forecast to grow at a CAGR of 6.36% through 2031.

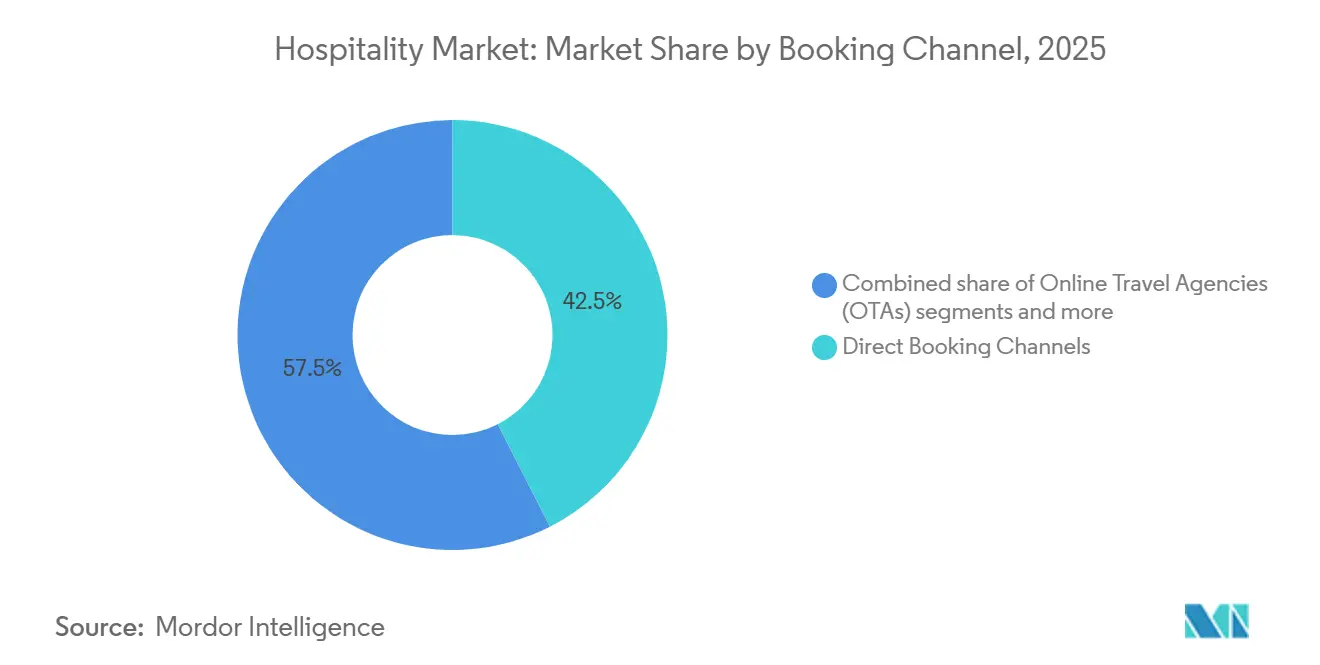

- By booking channel, Direct Booking Channels held 42.51% of transactions in 2025 in the Global Hospitality Market, while Mobile & Loyalty-App Based Bookings are expected to advance at a CAGR of 7.25% through 2031.

- By revenue stream, Room Revenue retained 56.63% share in 2025 in the Global Hospitality Market, while Wellness & Experience Revenue is projected to expand at a CAGR of 6.92% through 2031.

- By traveler type, Leisure Travelers held 52.64% share in 2025 in the Global Hospitality Market, while Bleisure & Long-Stay Travelers are forecast to rise at a CAGR of 6.65% through 2031.

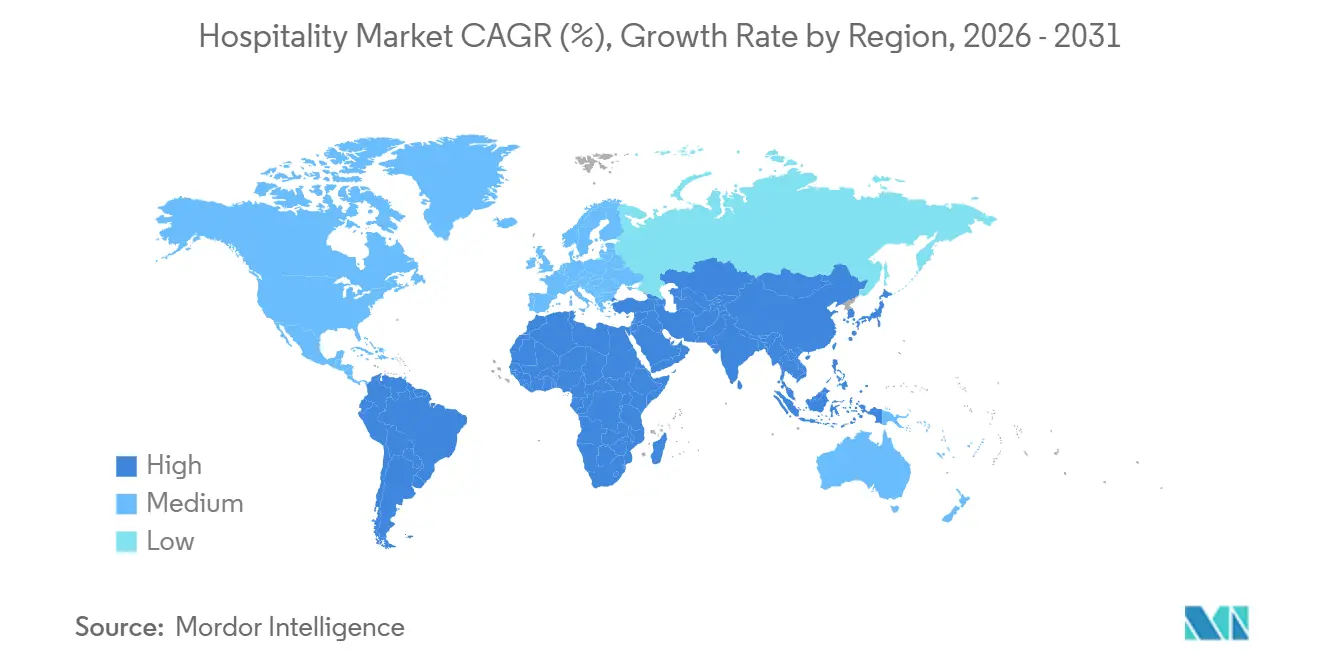

- By geography, Europe represented 31.15% share of the Global Hospitality Market size in 2025, while Asia-Pacific is projected to grow at a CAGR of 7.57% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Experiential and Lifestyle-Led Hospitality Concepts | +1.5% | Global, with stronger gains in Europe and Asia-Pacific | Medium term (2-4 years) |

| Rising Bleisure and Flexible Work-Driven Travel Demand | +1.2% | Global, with North America and Europe leading and Asia-Pacific accelerating | Short term (≤ 2 years) and Medium term (2-4 years) |

| Growth in Wellness, Medical, and Regenerative Tourism Stays | +1.3% | Global, with Asia-Pacific and Middle East and Africa as core demand centers | Medium term (2-4 years) |

| Digital Transformation Through AI-Based Revenue & Guest Management | +1.8% | Global, with stronger adoption in North America and Western Europe | Short term (≤ 2 years) |

| Rapid Expansion of Alternative Accommodation and Hybrid Stay Models | +1.4% | Global, with faster growth in Asia-Pacific and South America | Short term (≤ 2 years) and Medium term (2-4 years) |

| Increasing Middle-Class International Travel from Emerging Economies | +1.6% | Asia-Pacific led, with spillover into the Middle East, Europe, and other destination regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Experiential and Lifestyle-Led Hospitality Concepts

Experiential and lifestyle-led formats are reshaping the global hospitality market as travelers increasingly prefer properties that integrate design, local identity, and flexible social spaces. This trend gained traction with notable chain activities, including Marriott's acquisition of citizenM, IHG's purchase of Ruby Hotels, and Hilton's launch of its Select by Hilton platform through an exclusive agreement[2]InterContinental Hotels Group, “IHG Accelerates European Growth Expanding Its Portfolio by Over a Quarter in 3 Years,” IHG, ihgplc.com. Operators are prioritizing conversions over new builds, particularly in high-cost development areas. IHG reported that conversions significantly contributed to room openings and signings in Europe, reflecting a shift toward brand migration instead of greenfield expansion. This approach accelerates the refresh of older assets and enhances the appeal of the hospitality market across urban and resort locations.

Rising Bleisure and Flexible Work-Driven Travel Demand

The global hospitality market is adapting to the rise of "bleisure" travel and flexible work patterns, particularly in urban, mixed-use, and long-stay formats. "Bleisure" and long-stay travelers represent the fastest-growing segment, reflecting a shift in business travel beyond short weekday trips. Hotels, serviced apartments, and alternative accommodations are redesigning rooms, workspaces, food services, and connectivity to attract longer stays and increase ancillary spending. Airbnb reported growth in nights booked from Latin America, supporting the trend of blended work and leisure travel expanding beyond traditional North Atlantic business hubs. This shift is driving mid-week demand stability in some cities while causing sharper short-term occupancy fluctuations in others.

Growth in Wellness, Medical, and Regenerative Tourism Stays

Wellness-led travel is driving revenue growth in the global hospitality market as operators expand offerings to include spas, fitness, recovery, and immersive experiences. Wellness tourism achieved significant growth in 2024 and is expected to continue expanding through 2029, encouraging investments in wellness infrastructure across resorts and urban properties[3]Global Wellness Institute, “2025 Wellness Economy Monitor,” Global Wellness Institute, globalwellnessinstitute.org. Wellness & Experience Revenue is identified as the fastest-growing segment, with a strong CAGR through 2031, making it central to pricing and product strategies in the hospitality market. Marriott advanced this trend in 2026 by partnering with Lefay to enhance luxury wellness offerings globally, with planned properties in Tuscany, Southern Italy, and the Swiss Alps. This shift highlights the growing distinction between standard lodging formats and properties that effectively meet guest demand for wellness-focused experiences.

Digital Transformation Through AI-Based Revenue & Guest Management

Digital transformation is driving operations in the global hospitality market as pricing, staffing, guest communication, and maintenance increasingly rely on real-time decision systems. Choice Hotels partnered with Amazon Web Services to implement AI across revenue management, predictive maintenance, and guest communications, marking a shift from pilot projects to scaled deployment within franchise networks. Large operators benefit from integrating AI tools with loyalty systems, property management software, and centralized pricing teams across various markets. This digital capability is becoming a critical differentiator, especially as demand patterns fluctuate due to events, seasonality, and city-level supply changes. The adoption of AI enables faster inventory control, improved guest retention, and reduced manual effort, which is essential given ongoing challenges with labor availability and wage pressures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Operating and Labor Costs Across Hospitality Properties | -1.2% | Global, most acute in North America and Western Europe | Short term (≤ 2 years) and Medium term (2-4 years) |

| Economic Slowdowns Impacting Discretionary Travel Spending | -0.9% | Global, with higher sensitivity in mature markets | Short term (≤ 2 years) and Medium term (2-4 years) |

| Regulatory and Licensing Challenges in Short-Term Accommodation Markets | -0.7% | North America and Europe, with city-level and national compliance frameworks | Short term (≤ 2 years) and Medium term (2-4 years) |

| Seasonal Demand Volatility and Occupancy Fluctuations | -0.5% | Global, with greater exposure in resort and single-season destinations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Operating and Labor Costs Across Hospitality Properties

High operating and labor costs remain a significant short-term challenge for the global hospitality market, as room-rate increases do not directly translate into higher profit margins. Labor costs per occupied room have risen, with full-service hotel wage costs experiencing notable year-over-year growth[4]Actabl, “Hotel Labor Costs 2025,” Actabl, actabl.com. These pressures affect both branded chains and independent operators, particularly those with labor-intensive formats, limited pricing power, or inadequate digital systems. Regional disparities further complicate the issue, prompting more selective approaches to pricing, staffing, and service design. Without advancements in efficiency tools and process redesign, a portion of the recovering demand will likely be absorbed by wages, utilities, and supplies instead of contributing to operating profits.

Economic Slowdowns Impacting Discretionary Travel Spending

Economic slowdowns challenge the global hospitality market as discretionary travel declines with reduced consumer confidence, tighter corporate budgets, or weaker cross-border business conditions. International tourist arrivals are expected to grow modestly by 2026, reflecting a slower recovery compared to prior rebound years. This exposes the market to regional demand fluctuations and traveler type variability. Mature markets face added pressure due to high labor and financing costs alongside stabilizing demand growth. North America is projected to grow steadily through 2031, though the 2026 outlook remains cautious, with cost inflation and softer momentum limiting growth potential. Hotel owners and operators are likely to focus on rate discipline, asset-light strategies, and selective capital investments rather than broad expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Hospitality Type: Hotels Retain Scale Advantage as Alternatives Accelerate

Hotels & Resorts held 56.63% of 2025 value, which kept them as the largest format in the global hospitality market. Their scale advantage came from broad brand distribution, stronger corporate contracting, loyalty ecosystems, and more consistent service delivery across regions. These strengths remain important in urban centers, airport markets, business corridors, and large mixed-demand destinations where reliability still matters to both travelers and procurement teams. The global hospitality market also continues to favor hotel operators that can use central reservation systems and member programs to keep more bookings in direct channels. This gives formal hotel groups a structural advantage when costs rise or when demand becomes less predictable.

Vacation Rentals & Alternative Accommodations are projected to expand at a 6.83% CAGR through 2031, which makes them the fastest-growing hospitality type in the supplied draft. Airbnb’s 2026 footprint of more than 9 million active listings across more than 220 countries and regions shows the scale that alternative accommodation has achieved in the global hospitality market. Demand for space, privacy, and home-like amenities is supporting this segment, especially for families, extended stays, and blended work-leisure travel. Serviced apartments also benefit from this shift because they offer longer-stay functionality with a more formal operating model. At the same time, tighter short-term rental enforcement in several cities may redirect some demand back to licensed hotel inventory, which keeps the competitive balance in the global hospitality market fluid rather than one-directional.

By Property Type: Brand Conversion Reshapes the Development Model

Chain and branded properties held 61.94% of the global hospitality market share in 2025, reflecting the dominance of formal brand systems. This strength is attributed to loyalty programs, reservation networks, operational standards, procurement advantages, and appeal to owners in various financing scenarios. Companies like Marriott, Hilton, and IHG expanded their presence without relying solely on owned assets, reducing capital intensity while increasing brand reach. Marriott’s 2025 pipeline included 4,056 properties and nearly 610,000 rooms, with over half in international markets, highlighting the distribution advantage of major chains. Branded scale benefits owners by enabling efficient conversions, access to loyalty demand, and improved commercial visibility.

Independent lifestyle and boutique properties are projected to grow at a 6.36% CAGR through 2031, making them the fastest-growing segment. Large chains are adapting to this trend through acquisitions and new platforms, such as Marriott’s citizenM deal, IHG’s Ruby acquisition, and Hilton’s launch of its 'Select by Hilton' platform through an exclusive franchise agreement with YOTEL. China's hotel construction pipeline reached a record high of 3,608 projects and 644,938 rooms at the close of 2025, emphasizing the importance of branded supply in global hospitality development. Conversions are gaining traction due to shorter opening timelines and reduced development risks. Operators capable of repositioning assets under brand banners while preserving localized identity are well-positioned to capitalize on this shift.

By Booking Channel: Loyalty Deepens Direct Share as Mobile Accelerates

Direct Booking Channels accounted for 42.51% of transactions in 2025, maintaining their position as the largest distribution route in the global hospitality market. This reflects years of investment by major chains in loyalty programs, member rates, mobile apps, and direct engagement tools. Direct bookings help operators reduce third-party commission costs and retain guest data for pricing, upselling, and repeat targeting. They also provide large groups with better control over inventory allocation during sudden demand changes. Channel strategy has become a key profit driver in the global hospitality market, extending beyond its traditional commercial role.

Mobile & Loyalty-App Based Bookings are projected to grow at a 7.25% CAGR through 2031, making them the fastest-growing channel. Their growth is driven by faster booking processes, improved personalization, and stronger connections to loyalty benefits and in-stay services. Online Travel Agencies remain essential for independent operators and alternative accommodation providers seeking digital visibility and international reach. Corporate and travel management company channels retain importance for negotiated travel programs, group bookings, and managing business travel expenses. Offline agents, while representing a smaller share, continue to play a role in handling complex itineraries, group travel, luxury planning, and destination curation in the global hospitality market.

By Revenue Stream: Room Revenue Leads, Wellness Outgrows All Categories

Room revenue held a 56.63% share in 2025, maintaining its position as the largest revenue source in the global hospitality market. Core room demand continues to drive occupancy, average daily rates, and property economics across formats. Despite growth in ancillary categories, room pricing remains the primary driver of topline performance for most hotels and resorts. Operators focus on revenue management, direct booking optimization, and length-of-stay strategies. While revenue streams diversify, the market structure remains centered on room revenue.

Wellness & Experience Revenue is expected to grow at a 6.92% CAGR through 2031, making it the fastest-growing segment. The Global Wellness Institute projects wellness tourism to reach USD 1.4 trillion by 2029, supporting this category’s expansion. Hotels are incorporating spa, fitness, recovery, mindfulness, and destination-focused programs in both resort and urban settings. Food and beverage remain a key contributor but faces higher labor and input costs compared to experience-driven services. Events and conference revenue is improving but remain more cyclical and sensitive to geopolitical and corporate travel trends than room revenue.

By Traveler Type: Leisure Anchors Market, Bleisure Reshapes Product Design

Leisure travelers accounted for 52.64% of the global hospitality market share in 2025, highlighting the dominance of discretionary travel. This trend reflects a shift in consumer spending toward travel, experiences, and destination-focused stays across domestic and international routes. Leisure demand spans various property types, including resorts, boutique hotels, hostels, branded select-service hotels, and vacation rentals. It also drives revenue opportunities in wellness, dining, local programming, and diverse room categories. Leisure travel remains a key factor in maintaining occupancy during peak and shoulder periods in the global hospitality market.

Bleisure and long-stay travelers are projected to grow at a 6.65% CAGR through 2031, making them the fastest-growing segment. This group is influencing product design, with demand for work-ready rooms, shared workspaces, stronger connectivity, and flexible food and service options. It supports serviced apartments, extended-stay brands, and hybrid formats combining hotel convenience with long-term functionality. Business travel is shifting toward fewer but more intentional trips, often involving longer stays in specific regions. The global hospitality market is adapting inventory, pricing, and services to align with length-of-stay behavior rather than a simple business-versus-leisure distinction.

Geography Analysis

Europe accounted for 31.15% of the global hospitality market in 2025, making it the largest regional contributor by value. Europe recorded 793 million international tourist arrivals that year, representing a 4% increase from 2024 and 6% above 2019 levels. The region's dominance stems from dense air connectivity, ease of multi-country travel, diverse lodging options, and strong city and leisure demand. Europe is projected to grow at 4.1% through 2031, reflecting a mature yet steady trajectory. North America maintains significant revenue, while South America is expected to expand faster at a 6.4% CAGR, driven by rising tourism and regional travel flows.

Asia-Pacific is the fastest-growing region in the global hospitality market, with a forecast CAGR of 7.57% through 2031. India led the Asia-Pacific hotel development pipeline in Q1 2026 with 940 projects comprising 124,011 rooms, followed by Vietnam with 258 projects and 87,077 rooms. China led with 3,602 projects and 640,328 rooms in Q1 2026, with 1,111 new hotels expected in 2026. This growth reflects strong domestic travel, regional mobility, and outbound travel capacity. Oceania is forecast to grow at 4.9% through 2031, indicating steady progress.

The Middle East and Africa are among the highest-growth regions. The Middle East’s hotel pipeline reached 717 projects and 177,110 rooms in Q1 2026, led by Saudi Arabia with 385 projects and 105,598 rooms. Growth forecasts for the Middle East and Africa are 7.5% and 7.2%, respectively, through 2031. Africa saw 81 million tourist arrivals in 2025, up 8% year over year, with North Africa growing 11%. These regions offer opportunities in religious tourism, mid-market lodging, and underdeveloped urban areas.

Competitive Landscape

The global hospitality market remained highly fragmented, with major players holding small shares while independent hotels, regional chains, vacation rental operators, and alternative accommodation providers dominated the rest. Fragmentation increased competition as large companies leveraged brand systems, loyalty programs, technology, and asset-light strategies to expand without owning all assets. Marriott’s extensive pipeline of properties and rooms, with a significant portion in international markets, highlighted the challenges smaller competitors faced in achieving global reach.

Strategic initiatives focused on acquisitions, platform development, and conversion-led growth. Marriott strengthened its position in the select-service and lifestyle segment through acquisition. IHG expanded its European portfolio via acquisitions, conversions, and new signings, enabling faster growth in high-cost development areas. Hyatt pursued fee-based growth by acquiring a resort group, selling the real estate, and retaining long-term management agreements. Hilton expanded its lifestyle offerings by partnering with a design-focused brand, targeting younger demographics.

Technology-driven platforms and alternative accommodations continued to reshape the competitive landscape. Airbnb reported significant active listings and projected steady revenue growth, demonstrating the importance of platform-led lodging. However, stricter regulations in major cities reduced supply, creating opportunities for branded hotels in urban areas with limited licensed inventory. Growth opportunities include the mid-market branded segment in Asia-Pacific and the Middle East, accommodations for longer stays, and properties emphasizing sustainability practices. Operators combining flexible formats with strong branding, distribution, and operational systems are expected to gain an advantage in this fragmented market.

Hospitality Industry Leaders

Marriott International

Hilton Worldwide Holdings

Accor S.A.

InterContinental Hotels Group (IHG)

Wyndham Hotels & Resorts

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Choice Hotels International, in collaboration with Amazon Web Services, has integrated AI tools across thousands of franchise properties to optimize revenue management, predictive maintenance, and guest communications.

- April 2026: Hilton opened the Waldorf Astoria Rabat Salé, the first Waldorf Astoria in Morocco, and launched 131 hotels with 16,300 rooms across 26 new countries and territories in Q1 2026.

- March 2026: Marriott International partnered with the Leali family to integrate Italian luxury wellness brand Lefay into its global portfolio, with planned properties in Tuscany, Southern Italy, and the Swiss Alps.

- March 2026: Hilton signed an exclusive franchise agreement with YOTEL, integrating YOTEL’s 23 lifestyle hotels across 10 countries into Hilton Honors and introducing the 'Select by Hilton' category.

Global Hospitality Market Report Scope

| Hotels & Resorts |

| Vacation Rentals |

| Serviced Apartments |

| Hostels & Budget Accommodation |

| Boutique & Lifestyle Hotels |

| Luxury Hospitality Properties |

| Chain / Branded Properties |

| Independent Properties |

| Direct Booking Channels |

| Online Travel Agencies (OTAs) |

| Corporate / Travel Management Companies |

| Offline Travel Agents |

| Room Revenue |

| Food & Beverage Revenue |

| Events & Conference Revenue |

| Wellness & Recreation Revenue |

| Other Ancillary Revenue |

| Leisure Travelers |

| Business Travelers |

| Bleisure Travelers |

| Long-Stay / Digital Nomad Travelers |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Hospitality Type | Hotels & Resorts | |

| Vacation Rentals | ||

| Serviced Apartments | ||

| Hostels & Budget Accommodation | ||

| Boutique & Lifestyle Hotels | ||

| Luxury Hospitality Properties | ||

| By Property Type | Chain / Branded Properties | |

| Independent Properties | ||

| By Booking Channel | Direct Booking Channels | |

| Online Travel Agencies (OTAs) | ||

| Corporate / Travel Management Companies | ||

| Offline Travel Agents | ||

| By Revenue Stream | Room Revenue | |

| Food & Beverage Revenue | ||

| Events & Conference Revenue | ||

| Wellness & Recreation Revenue | ||

| Other Ancillary Revenue | ||

| By Traveler Type | Leisure Travelers | |

| Business Travelers | ||

| Bleisure Travelers | ||

| Long-Stay / Digital Nomad Travelers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of global hospitality in 2026?

The global hospitality market stands at USD 9.11 trillion in 2026 and is projected to reach USD 11.95 trillion by 2031 at an 5.58% CAGR.

Which region leads worldwide lodging demand today?

Europe led in 2025 with a 31.15% share, supported by 793 million international tourist arrivals.

Which accommodation format is growing the fastest?

Vacation Rentals & Alternative Accommodations are forecast to grow at a 6.83% CAGR through 2031, faster than other hospitality types in the supplied draft.

Why are direct bookings still important for hotel operators?

Direct channels held 42.51% of bookings in 2025, helping operators reduce commissions and keep stronger control over guest data and loyalty conversion.

What is the biggest near-term operating risk for hotel owners?

Labor and operating costs remain the main pressure point, with hotel labor cost per occupied room rising 12.8% in 2025.

What areas offer the strongest room for expansion over the next 5 years?

Asia-Pacific, the Middle East, extended-stay formats, wellness-led stays, and branded mid-market properties remain the clearest white-space opportunities in the supplied draft.

Page last updated on: