Connected Hotel Systems And Solutions Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 12.69 Billion |

| Market Size (2030) | USD 17.93 Billion |

| Growth Rate (2025 - 2030) | 7.16% CAGR |

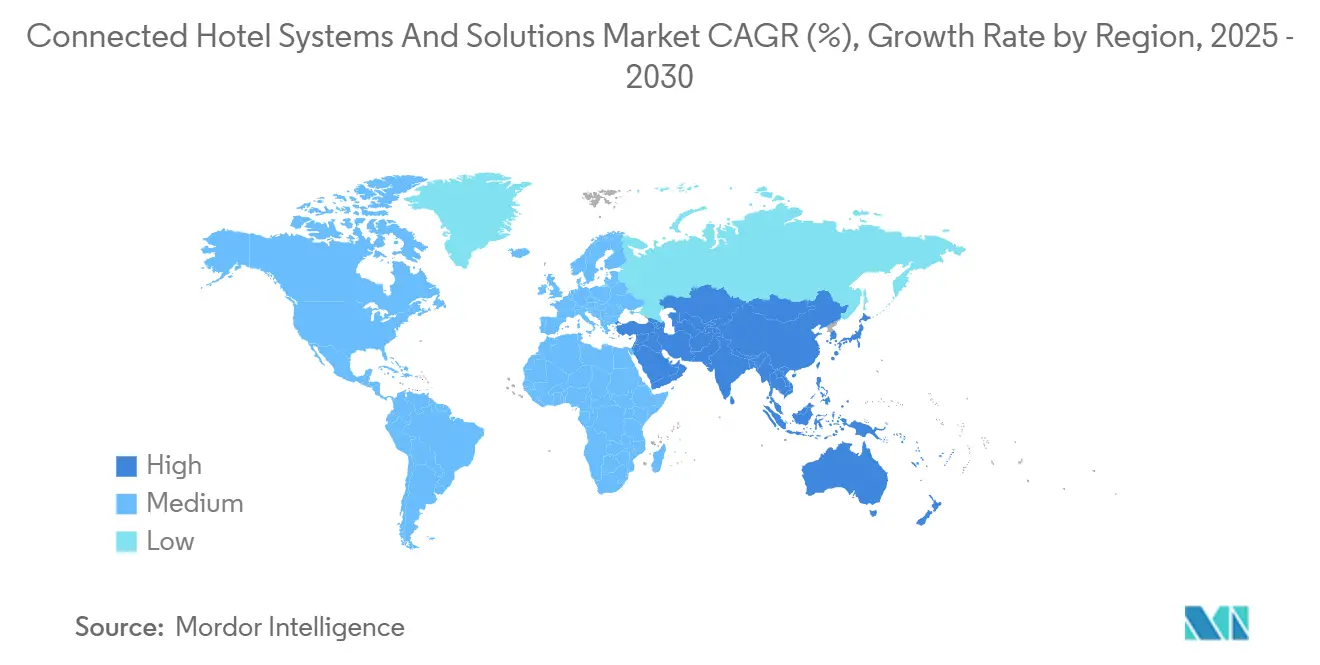

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

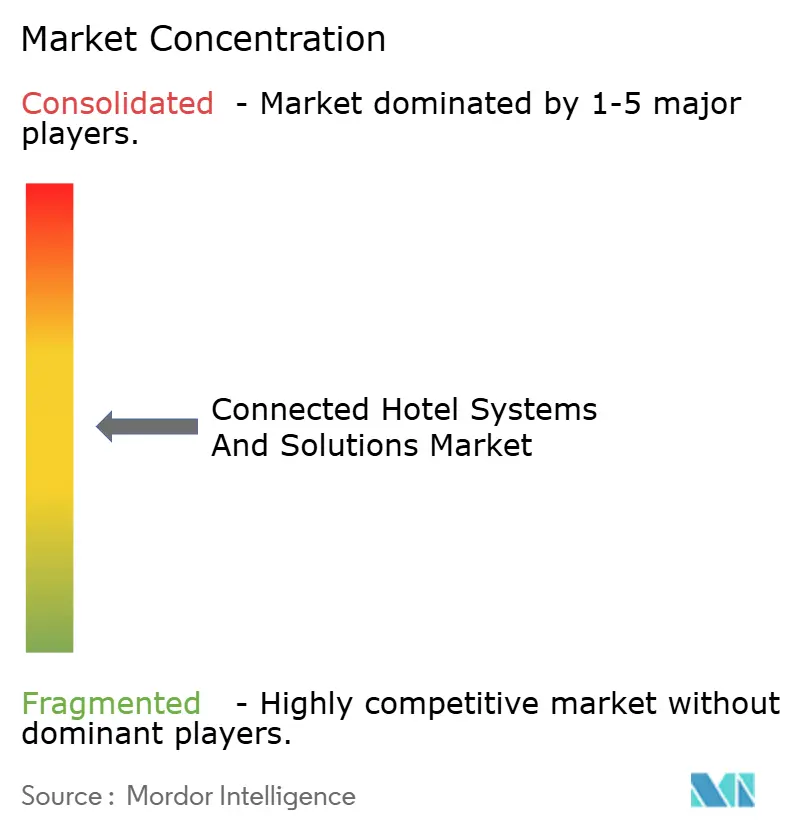

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Connected Hotel Systems And Solutions Market Analysis by Mordor Intelligence

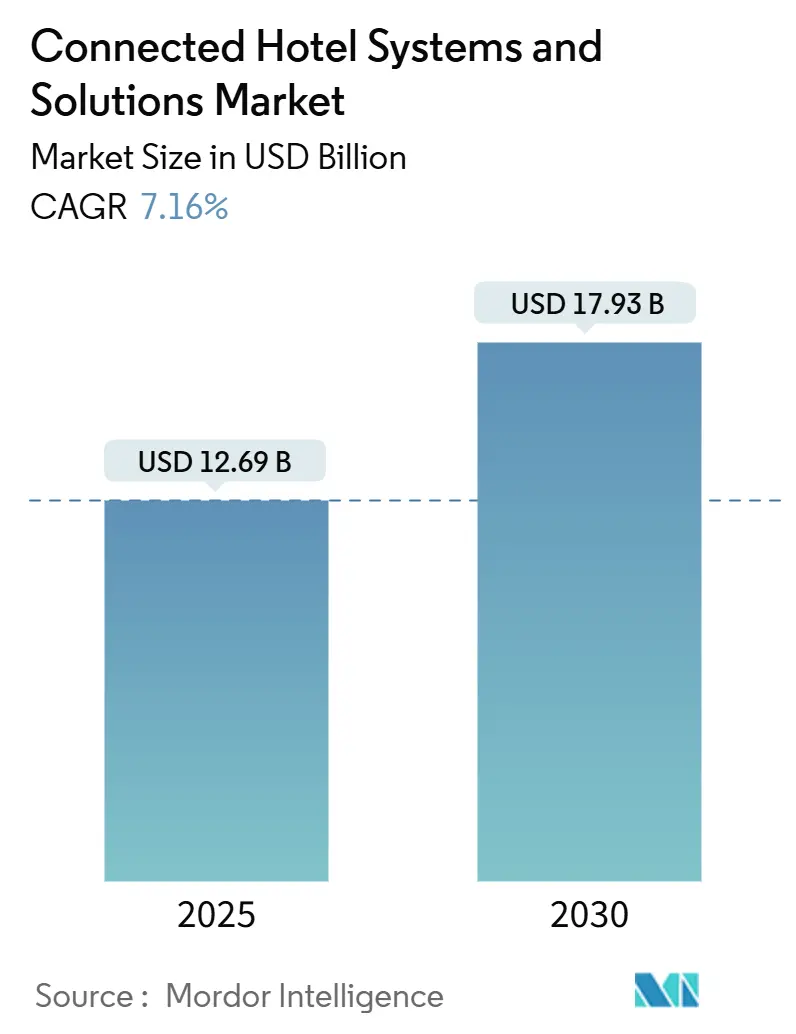

The connected hotel systems and solutions market size stood at USD 12.69 billion in 2025 and is projected to reach USD 17.93 billion by 2030, registering a 7.16% CAGR. The increasing demand for unified technology stacks that integrate property management, guest engagement, building automation, and security is prompting buyers to replace isolated point solutions. Cloud-native deployments enable chains and independents to scale while avoiding capital outlays for on-premise data centers, and the real-time analytics generated by these platforms power dynamic pricing, personalized offers, and energy optimization. North America remains the revenue leader, thanks to early migration to cloud PMS and high discretionary tech budgets. However, the Asia-Pacific region is widening its influence as large pipelines in China and India integrate mobile check-in, keyless entry, and IoT room controls from the outset. Competitive intensity is rising as cloud specialists deliver transparent subscription pricing and open API marketplaces that shorten integration timelines and lower switching costs. Cybersecurity readiness and data-privacy compliance have moved to the forefront, driving vendors to embed encryption, audit trails, and SOC 2 certifications as standard features.

Key Report Takeaways

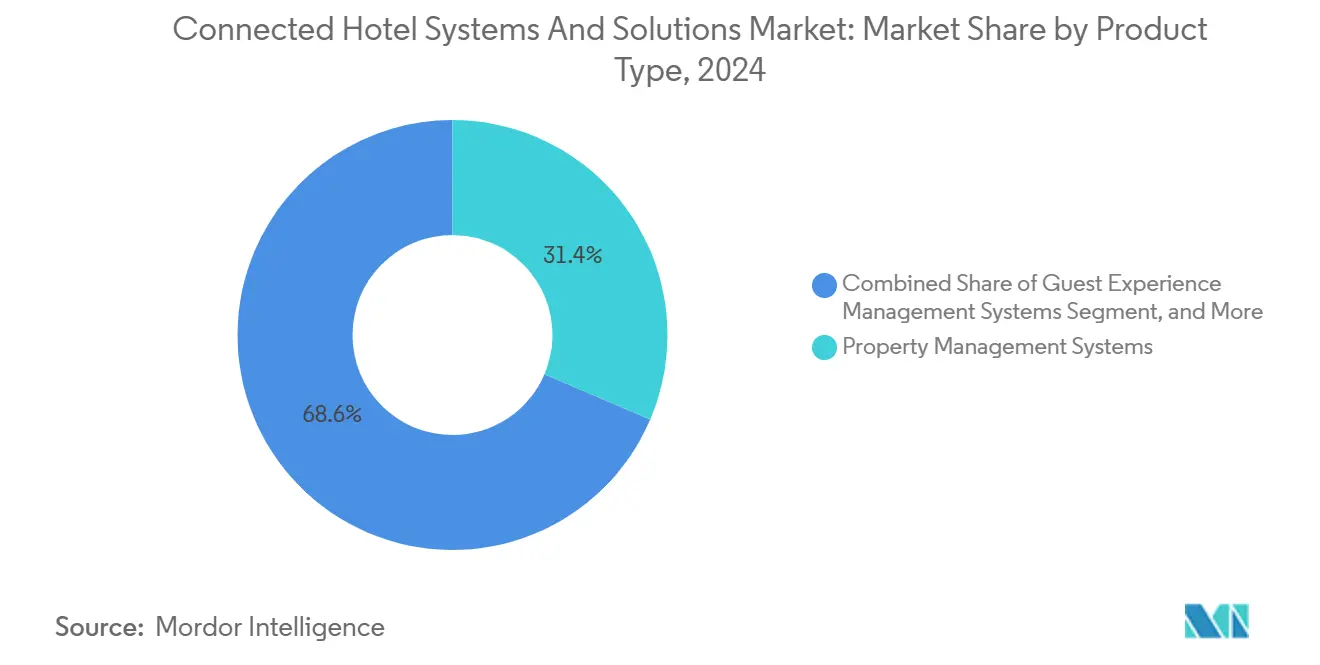

- By product type, property management systems led with a 31.43% revenue share in 2024, while guest experience management systems are expected to advance at an 8.19% CAGR through 2030.

- By deployment mode, cloud-based platforms commanded 61.89% of the revenue in 2024 and are expected to continue growing at the fastest rate of 7.91% through 2030.

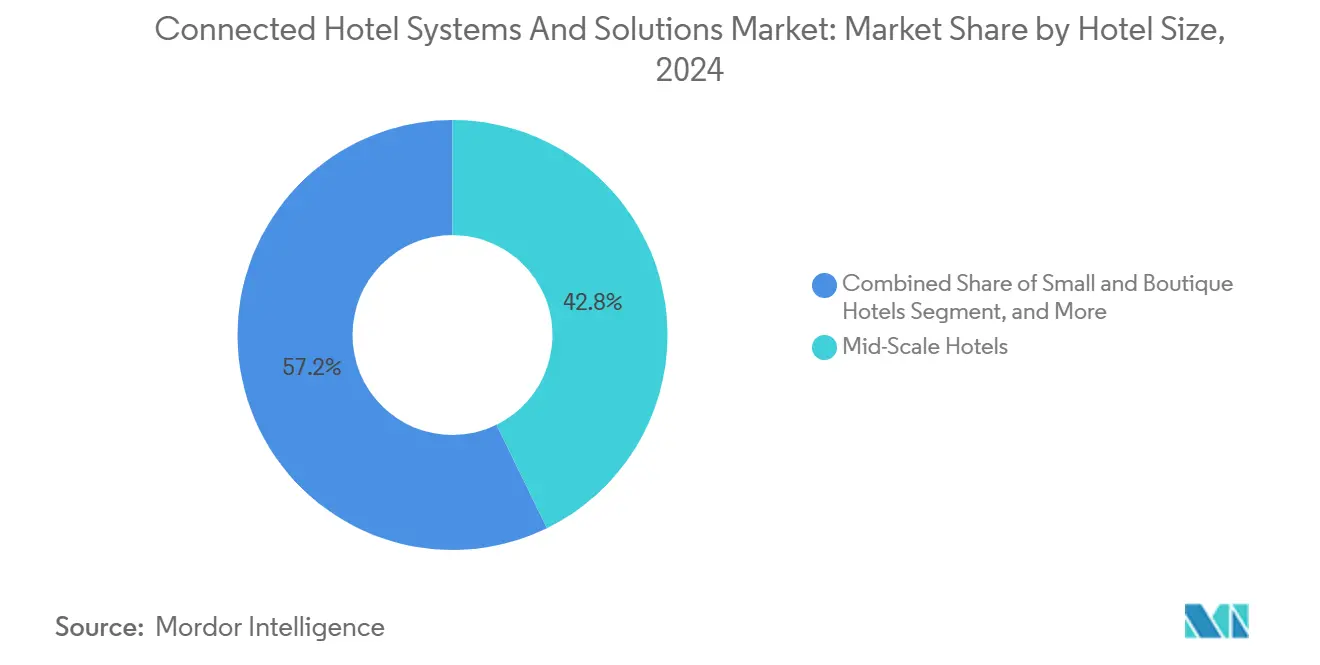

- By hotel size, mid-scale hotels accounted for 42.76% of 2024 installations, while small and boutique hotels are expanding at a rate of 7.83%, the highest rate in the segment.

- By end user, luxury and upscale hotels generated 38.91% of 2024 demand, whereas budget hotels and hostels are forecast to rise at an 8.27% CAGR.

- By geography, North America captured 43.72% of the revenue in 2024, while the Asia-Pacific region is on track for the fastest growth at 8.23% through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Connected Hotel Systems And Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Cloud Native PMS Platforms | +1.2% | Global with early concentration in North America and Europe | Medium term (2-4 years) |

| Integration of AI-Powered Revenue Optimization Engines | +1.1% | North America and Europe core, expanding to Asia-Pacific | Medium term (2-4 years) |

| Demand for Mobile-First and Contactless Guest Journeys | +0.9% | Global, accelerated in Asia-Pacific and urban North America | Short term (≤2 years) |

| Rising Deployment of IoT-Based Smart Room Controls | +0.8% | Asia-Pacific and Middle East lead, spill-over to North America luxury segment | Long term (≥4 years) |

| Government Tourism Stimulus Boosting Tech Budgets | +0.7% | Middle East, South Asia, select Latin America | Short term (≤2 years) |

| Expansion of Open API Marketplaces Among Vendors | +0.6% | Global, strongest uptake in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Cloud Native PMS Platforms

Cloud property management systems have become the default architecture for new hotels and refresh projects, displacing client-server models that required on-site servers and specialized IT staff. Hyatt migrated its global estate to Oracle OPERA Cloud in 2024, underscoring how large chains now view PMS subscriptions as ongoing service models rather than depreciating assets.[1]Oracle Corporation, “Hyatt Selects Oracle OPERA Cloud Property Management,” oracle.com Choice Hotels has extended a regional deal with Mews, allowing European franchisees to launch on cloud-first stacks with minimal capital. Centralized data enables chain-wide revenue management and real-time pricing updates that monolithic on-premise systems cannot match without costly middleware. Compliance burdens tied to payment security frameworks, such as PCI-DSS, now shift to the vendor, further tilting adoption toward the cloud. As vendors retire perpetual licenses, the connected hotel systems and solutions market is likely to see continuous feature rollout, faster innovation cycles, and growing gaps between early adopters and laggards.

Demand for Mobile-First and Contactless Guest Journeys

Contactless check-in and mobile keys transitioned from pandemic stop-gaps to baseline expectations. Canary Technologies processed more than 10 million contactless check-ins in 2024, a milestone that highlights scale beyond luxury properties.[2]Canary Technologies, “10 Million Contactless Check-Ins Processed,” canarytechnologies.com Marriott’s integrated mobile app combines keyless entry, service requests, and loyalty earning, enhancing guest loyalty across its 8,700-plus hotels. Asia-Pacific travelers, whose smartphone penetration exceeds 80%, are driving chains to deploy mobile workflows even in budget segments, with OYO mandating cloud PMS and self-service check-in across its network. Mobile transactions generate real-time data for upsell engines, enabling operators to push personalized offers, such as late checkout, at conversion-optimized moments. Properties without mobile workflows risk losing revenue and guest loyalty to competitors that deliver seamless digital experiences.

Integration of AI-Powered Revenue Optimization Engines

Machine-learning revenue tools have moved from niche to mainstream. IHG embedded predictive pricing models that ingest local events, competitor rates, and historical occupancy trends to adjust room tariffs dynamically across its portfolio. Amadeus launched a chatbot that surfaces booking intent and funnels insights into rate recommendations, linking guest engagement directly to topline performance.[3]Amadeus IT Group, “AI-Powered Guest Service Chatbot Launch,” amadeus.com Hilton and Accor rolled out similar AI modules within their central reservation systems, enabling franchisees to leverage chain-level data science without hiring quantitative analysts. Cloudbeds and Mews bundle AI pricing into subscription tiers, democratizing advanced analytics for independents. The connected hotel systems and solutions market is thus compressing performance gaps between small and large operators, intensifying competition for high-value transient and group demand.

Rising Deployment of IoT-Based Smart Room Controls

Hoteliers are using IoT sensors not only as luxury amenities but as operational efficiency tools amid rising utility costs. Six Senses Kyoto reduced energy consumption by 25% in 2024 by utilizing in-room sensors that modulate HVAC, lighting, and shades based on occupancy. Honeywell’s new Forge for Hospitality links IoT devices with PMS data, allowing rooms to transition to economy mode immediately after checkout, while predictive maintenance alerts minimize equipment downtime. Middle East megaprojects such as Atlantis The Royal integrate IoT layers into building blueprints, creating showcase properties for energy-efficient guest personalization. As sustainability certifications influence travel procurement, IoT-enabled energy savings strengthen both cost structures and brand positioning.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Integration and Migration Costs | −0.8% | Global, most acute in mid-market and independent properties | Short term (≤2 years) |

| Data Privacy and Cybersecurity Compliance Risks | −0.7% | North America and Europe primary, expanding to Asia-Pacific | Medium term (2-4 years) |

| Interoperability Gaps With Legacy On-Premise Systems | −0.6% | North America and Europe legacy properties, select Asia-Pacific chains | Medium term (2-4 years) |

| Skills Shortage in Hotel IT and Change Management | −0.5% | Global, highest impact in secondary markets and budget segments | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Upfront Integration and Migration Costs

A 300-room mid-scale property shifting from an on-premise PMS to a cloud solution can incur USD 150,000-250,000 in consulting, dual-run, and training costs, a sum that strains thin operating margins. Properties must often maintain legacy and new platforms in parallel for up to a year to safeguard revenue integrity, essentially doubling technology overhead during migration. Independent hotels lacking in-house IT staff face proportionally higher burdens, leading some to defer upgrades despite being aware of the revenue upside. Franchise groups have attempted to offset costs through volume discounts; however, multi-year lock-ins reduce flexibility. These dynamics temper replacement cycles and lengthen the sales lead time for vendors, which in turn pulls down near-term growth for the connected hotel systems and solutions market.

Data Privacy and Cybersecurity Compliance Risks

Successive breaches at global chains have made security spending unavoidable. Marriott’s multi-episode breach series triggered GDPR fines and class actions, convincing boards that encryption, multi-factor authentication, and zero-trust architectures are critical operating expenses. MGM Resorts’ 2023 ransomware attack revealed how interconnected hotel systems broaden attack surfaces and can halt front-of-house operations. New legislation, such as the European Union’s Digital Operational Resilience Act, places direct obligations on cloud service providers, thereby increasing the effective cost of compliance. Smaller operators struggle to finance annual PCI-DSS audits or 24-hour security monitoring, which hinders the adoption of integrated stacks and can prompt them toward point solutions perceived as less risky.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Guest Experience Platforms Outpace Core PMS

Property management systems retained 31.43% of 2024 revenue, anchoring transaction flows across reservations, payments, and housekeeping. Guest experience management platforms, however, are scaling at an 8.19% CAGR as operators pivot from back-office automation to revenue-per-guest optimization. Salesforce expanded its hospitality CRM to integrate with leading PMS vendors, giving chains real-time preference insights across stays. Building automation systems are gaining share as energy prices rise, with Honeywell and Siemens offering occupancy-driven climate control that yields 15-25% utility savings. Security and access solutions, such as mobile keys and biometrics, are standard in luxury pipelines and are filtering into mid-scale developments across the Asia-Pacific region. Altogether, the connected hotel systems and solutions market is shifting its spending mix toward guest-centric applications that directly influence top-line growth.

The fastest-growing product lines bundle CRM, upsell engines, and messaging into unified interfaces, enabling frontline staff to push personalized offers without needing to toggle between systems. Vendors with open APIs are winning because they enable operators to plug in specialized tools such as spa booking, gift card sales, or restaurant reservation widgets without requiring custom coding. As sustainability rises on investor agendas, building automation modules that verify carbon savings are moving from optional to mandatory in RFPs issued by corporate travel buyers. Over the forecast period, guest experience suites that sit natively on cloud PMS architecture are expected to capture an incremental share, especially in the Asia-Pacific region, where new construction often avoids retrofits.

By Deployment Mode: Cloud Dominance Reshapes Vendor Economics

Cloud-based deployments captured 61.89% of 2024 revenue and continue to expand at a rate of 7.91%, as vendors sunset on-premise license models. Chains prize the ability to roll out new functionality across estates overnight, pushing laggard properties toward platform upgrades to maintain brand standards. Hybrid arrangements appeal to casinos and resorts that require local servers for point-of-sale continuity during connectivity outages, but these designs still rely on cloud analytics for reporting. The connected hotel systems and solutions market share for on-premise installations will continue to contract as engineering focus and support windows shrink.

Subscription pricing stabilizes vendor cash flow yet lowers switching costs for hotels, so providers are doubling down on ecosystem lock-ins through developer marketplaces and bundled AI modules. Oracle, Infor, and Agilysys leverage large install bases to upsell analytics and integration packs, while Mews, Cloudbeds, and Apaleo court independents with month-to-month terms and self-service onboarding. Regulatory data-residency mandates in China and the Middle East give hybrid architectures a tailwind, but the trajectory remains cloud-first.

By Hotel Size: Boutique Properties Close the Technology Gap

Mid-scale hotels with 100-299 rooms accounted for 42.76% of 2024 installations, reflecting their numerical dominance in global hotel inventories. The connected hotel systems and solutions market size serving small and boutique properties is accelerating at 7.83%, fueled by modular subscription tiers that align technology spending with fluctuating occupancy. RoomRaccoon and Cloudbeds allow independents to stand up PMS, channel management, and automated revenue tools without hiring IT staff. Large chains have largely finished first-wave migrations, so incremental license growth now comes from secondary markets and conversions.

Smaller hotels are using cloud integrations to achieve parity in guest experience. Mobile check-in, keyless entry, and automated upsell modules, once exclusive luxuries, are now available for a fraction of their prior costs. This democratization intensifies competition in urban leisure corridors where boutique design alone is no longer a differentiator. Venture-funded vendors see boutiques as a land-grab segment and are rolling out rapid-implementation packages that go live in weeks rather than months.

By End User: Budget Segment Accelerates Digital Adoption

Luxury and upscale hotels generated 38.91% of 2024 demand, underpinned by premium pricing power and early adoption of AI personalization, IoT automation, and biometric access. Budget hotels and hostels are forecast to climb fastest at an 8.27% CAGR, reflecting mandates from franchisors such as OYO that require mobile check-in and cloud PMS for brand compliance. Mid-market properties are upgrading their revenue management systems to reduce rate volatility and fill shoulder nights, while resorts and vacation clubs require integrated communications to orchestrate complex itineraries.

Across all end-user tiers, operators now judge platforms by the breadth of guest-facing and back-office modules rather than by any single feature. The connected hotel systems and solutions market will continue to tilt toward solutions that allow staff reallocation from repetitive administration to high-touch service. In the Asia-Pacific region, rising wages are accelerating this shift as properties rely on automation to sustain service standards without proportionate increases in headcount.

Geography Analysis

North America retained 43.72% of 2024 revenue, buoyed by mature cloud ecosystems and aggressive AI rollouts among the large chains. The United States dominated spending, while Canada and Mexico saw independent properties adopt cloud PMS to compete with flagged hotels. Regulatory momentum, including state-level data privacy laws, makes security certifications a decisive factor in vendor selection.

Asia-Pacific is projected to grow at 8.23% through 2030, the fastest pace globally. China and India are adding thousands of rooms linked to national tourism corridors, and most new keys launch on cloud PMS with integrated IoT controls. Japan and South Korea are favoring building automation to offset labor shortages, while Australia’s resort pipeline is adopting AI-driven price optimization to smooth seasonal demand swings. Government tourism funds in the Middle East and South Asia subsidize smart-hotel pilots that bundle PMS, sensors, and AI concierges, propelling uptake among new entrants.

Europe remains an innovation hub, with the GDPR driving the development of secure-by-design platforms. Germany, the United Kingdom, and France prioritize open APIs to interconnect loyalty, upsell, and payment modules. Eastern European markets are modernizing as regional chains pursue inbound tourism, often beginning with channel management tools before implementing a full PMS. South America, paced by Brazil and Argentina, is smaller but growing as international brands and local operators alike replace aging on-premise stacks with cloud subscriptions tuned for volatile exchange rates.

Competitive Landscape

The connected hotel systems and solutions market remains highly fragmented, with no vendor exceeding a double-digit share. Enterprise incumbents, such as Oracle, Infor, and Agilysys, leverage their legacy relationships with top chains to bundle PMS, distribution, and point-of-sale solutions. Cloud-native challengers Mews, Cloudbeds, and StayNTouch differentiate themselves through transparent pricing, pre-built integrations, and rapid onboarding, capturing independents and mid-market groups that previous license costs had shut out. A third tier of regional specialists, including Protel in Europe, Clock Software in Central Europe, and eZee in South Asia, wins deals by providing localized compliance and language support.

Strategic moats are shifting toward API ecosystems. Vendors with open marketplaces attract third-party innovators who extend the platform's scope without requiring vendor engineering resources. Oracle’s 2024 joint venture with Shiji combines enterprise scale with regional distribution to deepen its reach in the Asia-Pacific region, signaling further consolidation as platforms race to fill geographic gaps. AI and cybersecurity features are emerging as competitive battlegrounds; SOC 2 certifications and embedded encryption sway chains under regulatory pressure, while AI revenue modules level the playing field for smaller hotels.

Pricing models are converging toward subscription, eroding historical lock-ins and forcing vendors to prioritize customer success to curb churn. This pressure stimulates feature velocity, creating a virtuous cycle for adopters, yet it raises the risk of technical debt for operators who delay upgrades. Vendors targeting serviced apartments and extended-stay formats are carving new whitespace by solving long-term billing and lease complexities that traditional hotel PMS cannot handle cleanly.

Connected Hotel Systems And Solutions Industry Leaders

Cloudbeds Inc.

Mews Systems B.V.

StayNTouch Inc.

Maestro PMS (Northwind Canada Inc.)

Agilysys Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Cloudbeds launched “Cloudbeds Connect,” an open API marketplace that debuted with more than 100 third-party apps available for self-service integration.

- August 2025: SiteMinder acquired rate-intelligence firm RateGuardian for USD 45 million, embedding real-time competitor pricing analytics into its channel manager.

- May 2025: Accor signed a multi-year deal with Honeywell to retrofit 200 Asia-Pacific hotels with IoT energy-management systems that integrate with the Accor Key platform.

- March 2025: Infor released an AI housekeeping optimization add-on for HMS Cloud, with Hyatt’s pilot properties reporting 15% faster room turnaround.

Global Connected Hotel Systems And Solutions Market Report Scope

The Connected Hotel Systems And Solutions Market Report is Segmented by Product Type (Property Management Systems, Guest Experience Management Systems, Building Automation Systems, Security and Access Control Solutions, Integrated Communication Solutions), Deployment Mode (Cloud Based, On-Premise, Hybrid), Hotel Size (Large Hotel Chains, Mid-Scale Hotels, Small and Boutique Hotels), End User (Luxury and Upscale Hotels, Mid-Market Hotels, Budget Hotels and Hostels, Resorts and Vacation Clubs, Serviced Apartments and Extended Stay), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Property Management Systems |

| Guest Experience Management Systems |

| Building Automation Systems |

| Security and Access Control Solutions |

| Integrated Communication Solutions |

| Cloud Based |

| On-Premise |

| Hybrid |

| Large Hotel Chains (≥300 Rooms) |

| Mid-Scale Hotels (100-299 Rooms) |

| Small and Boutique Hotels (<100 Rooms) |

| Luxury and Upscale Hotels |

| Mid-Market Hotels |

| Budget Hotels and Hostels |

| Resorts and Vacation Clubs |

| Serviced Apartments and Extended Stay |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Product Type | Property Management Systems | ||

| Guest Experience Management Systems | |||

| Building Automation Systems | |||

| Security and Access Control Solutions | |||

| Integrated Communication Solutions | |||

| By Deployment Mode | Cloud Based | ||

| On-Premise | |||

| Hybrid | |||

| By Hotel Size | Large Hotel Chains (≥300 Rooms) | ||

| Mid-Scale Hotels (100-299 Rooms) | |||

| Small and Boutique Hotels (<100 Rooms) | |||

| By End User | Luxury and Upscale Hotels | ||

| Mid-Market Hotels | |||

| Budget Hotels and Hostels | |||

| Resorts and Vacation Clubs | |||

| Serviced Apartments and Extended Stay | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the connected hotel systems and solutions market in 2025?

The connected hotel systems and solutions market size is valued at USD 12.69 billion in 2025.

What is the growth outlook through 2030?

Revenue is projected to reach USD 17.93 billion by 2030, translating to a 7.16% CAGR.

Which deployment model is growing fastest?

Cloud-based platforms hold 61.89% of 2024 revenue and are expanding at 7.91% through 2030 as vendors retire on-premise licenses.

Which region offers the highest growth potential?

Asia-Pacific leads with an 8.23% projected CAGR, supported by rapid hotel construction and mobile-centric traveler preferences.

What segment of hotels is adopting technology most quickly?

Small and boutique hotels are accelerating adoption at 7.83% as modular, API-first solutions lower entry barriers.

How are cybersecurity concerns shaping purchasing decisions?

Data-privacy compliance and recent breaches are forcing operators to prioritize platforms with encryption, SOC 2 certification, and zero-trust architectures.

Page last updated on: