Hotels Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.37 Trillion |

| Market Size (2031) | USD 1.89 Trillion |

| Growth Rate (2026 - 2031) | 6.55% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hotels Market Analysis by Mordor Intelligence

The Global Hotels market size is expected to increase from USD 1.29 trillion in 2025 to USD 1.37 trillion in 2026 and reach USD 1.89 trillion by 2031, growing at a CAGR of 6.55% over 2026-2031. The Global hotel market is now being shaped less by simple recovery and more by operators' ability to protect rates, improve mix, and lift revenue per stay. Record international tourism volumes continue to support demand, with global arrivals reaching 1.52 billion in 2025 and the United Nations World Tourism Organization expecting a further 3% to 4% increase in 2026[1]UN Tourism, “International Tourist Arrivals up 4% in 2025 Reflecting Strong Travel Demand Around the World,” UN Tourism, untourism.int. Across the Global Hotels market, higher-value travel patterns, such as bleisure, wellness-led stays, and experience-led vacations, are driving longer stays and stronger ancillary spending. The Hotels market is also seeing a structural shift toward asset-light management models, direct booking investments, and AI-enabled revenue management as operators seek better margins rather than pure occupancy gains. Even so, geopolitical stress, labor cost pressure, and tighter sustainability-linked financing standards continue to limit how evenly the Hotels market can translate demand growth into profit growth.

Key Report Takeaways

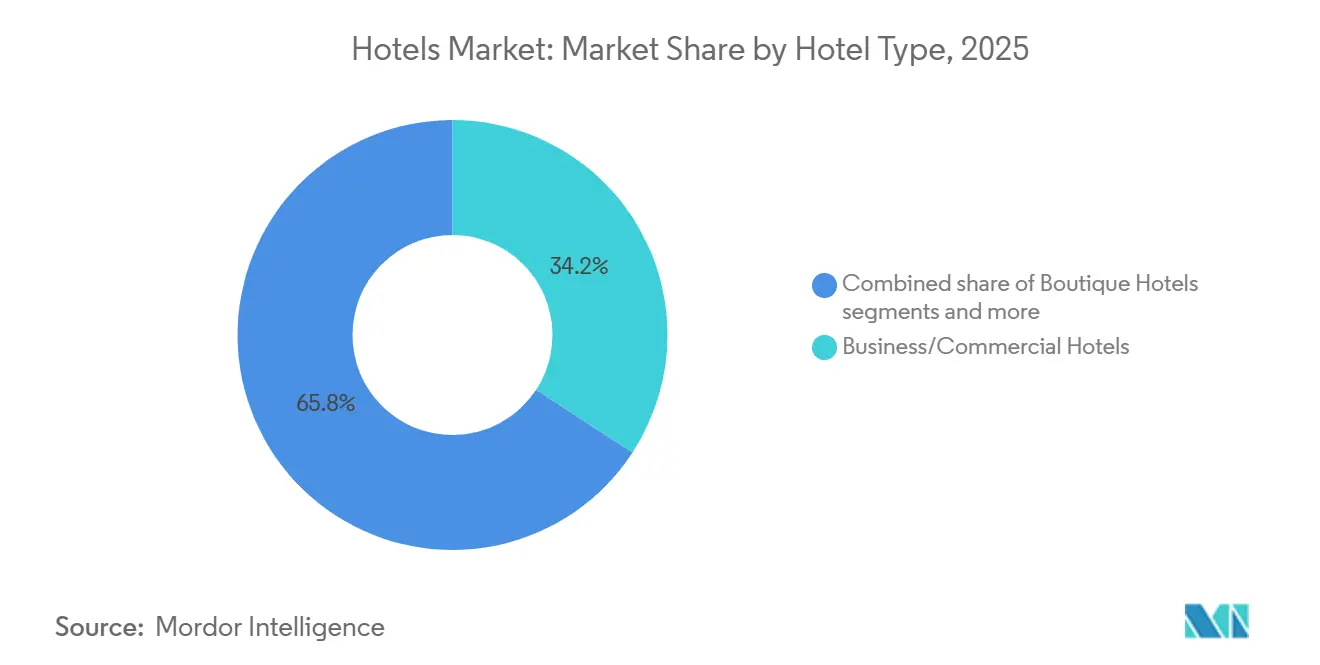

- By hotel type, Business/Commercial Hotels held 34.20% of the Hotels market share in 2025, while Resort Hotels are projected to expand at an 8.84% CAGR through 2031.

- By price category, Midscale properties accounted for 45.10% share of the Hotels market size in 2025, while Luxury hotels are forecast to grow at an 8.96% CAGR through 2031.

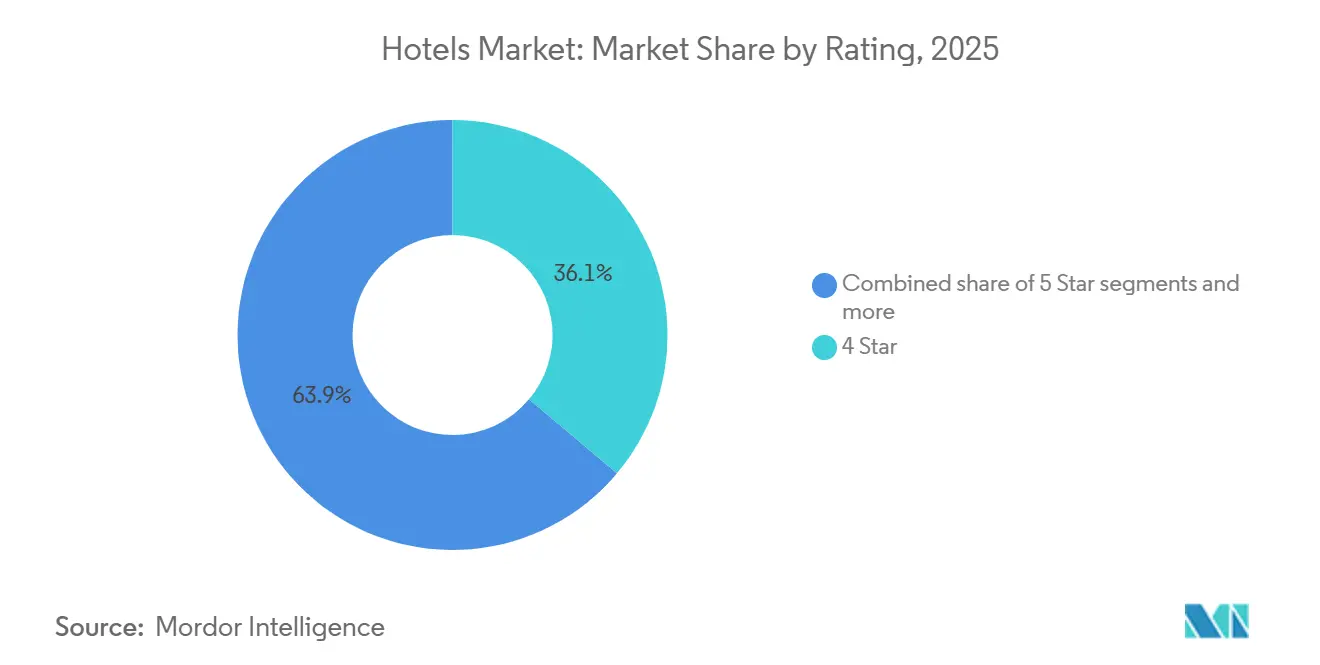

- By rating, 4-Star hotels led with a 36.85% share of the Hotels market size in 2025, while 5-Star hotels are expected to record the highest CAGR of 9.12% through 2031.

- By ownership model, Chain Hotels captured 53.40% share of the Hotels market size in 2025, while Managed Hotels are set to grow at an 8.42% CAGR through 2031.

- By booking channel, Online Travel Agencies held 39.15% share of the Hotels market size in 2025, while Direct Booking is projected to advance at an 8.73% CAGR through 2031.

- By end-user, Leisure travelers represented 57.20% of the market in 2025, while Bleisure is expected to post the fastest CAGR at 10.04% through 2031.

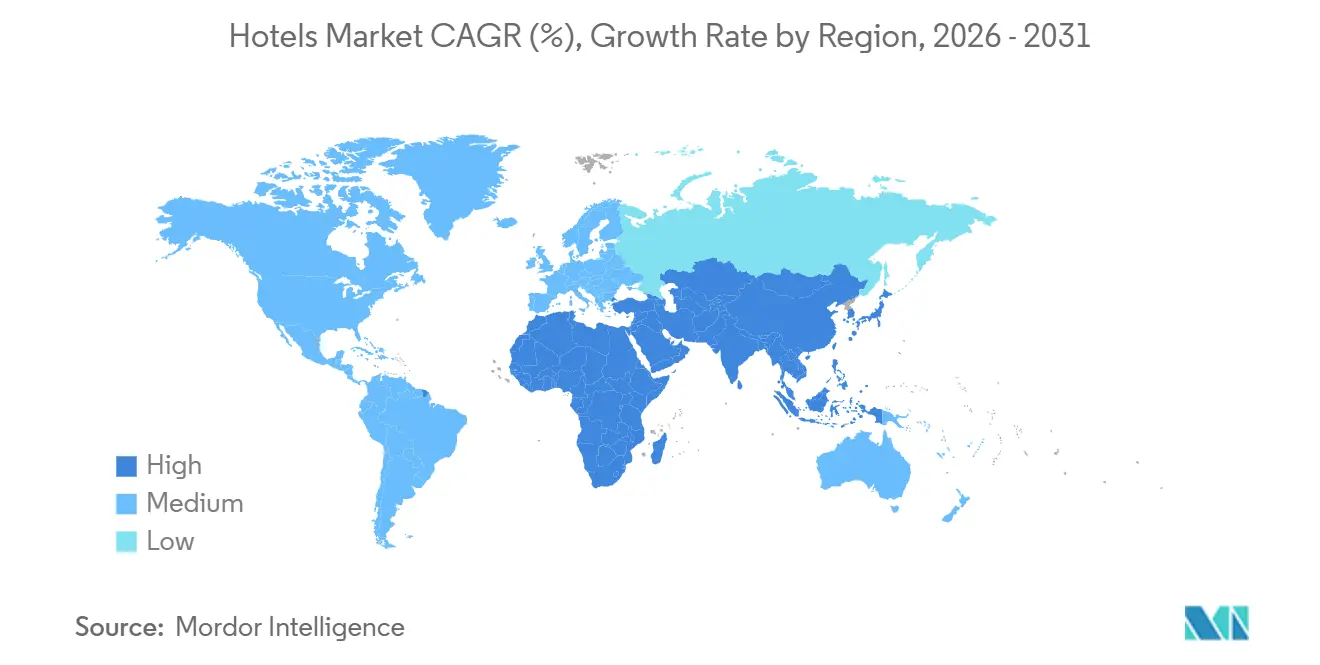

- By geography, North America held 31.10% of the Hotels market share in 2025, while Asia-Pacific is forecast to grow at the fastest CAGR of 8.91% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hotels Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising International Tourist Arrivals Post-Pandemic | +1.5% | Global, with strongest uplift in Europe and Asia-Pacific | Medium term (2-4 years) |

| Growing Disposable Incomes in Emerging Economies | +1.0% | Asia-Pacific core, spill-over to Middle East and Africa, and South America | Long term (≥ 4 years) |

| Increasing Corporate Travel & MICE Demand | +0.9% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Boom in Domestic Staycation Tourism Sustaining Occupancy | +0.7% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Regulatory Clamp-Downs on Alternative Lodging Spurring Hotel Innovation | +0.5% | North America and Europe, with early gains in gateway cities | Medium term (2-4 years) |

| AI-Driven Dynamic Pricing Lifting RevPAR | +0.6% | Global, with early gains in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising International Tourist Arrivals Reshaping Demand Dynamics

The Global hotel market continues to benefit from the full reopening of global travel corridors and the normalization of cross-border leisure and business movement. International tourist arrivals reached 1.52 billion in 2025, which was a new post-pandemic high and a 4% increase over 2024. United Nations Tourism also expects global arrivals to grow by another 3% to 4% in 2026, which keeps demand visibility favorable for hotel operators across major destination markets. This matters because broad-based arrival growth supports occupancy, improves pricing confidence, and helps chains spread fixed operating costs over a wider room base. In the Hotels market, the benefit is strongest for operators that can convert higher footfall into restaurant, wellness, event, and local-experience revenue rather than relying solely on room sales.

Growing Disposable Incomes in Emerging Economies Expanding Travel Spend

The Global hotel market is drawing support from rising travel intent in emerging economies, especially where domestic and regional mobility is increasing faster than long-haul travel. This pattern is visible in the stronger role of Asia-Pacific, where higher-income and aspirational travelers are moving into branded leisure, premium, and hybrid work-leisure stays. Agoda’s 2026 survey showed that 76% of Asia-Pacific business travelers plan to combine work and leisure travel, suggesting a traveler base with greater flexibility and a willingness to spend across trip types. Company expansion activity also supports this shift, with Hyatt, IHG, and Hilton all increasing their exposure to China, India, and Vietnam in 2025 and 2026[2]Hyatt Hotels Corporation, “Hyatt Announces Master Franchise Agreement with Dossen Group to Debut Hyatt Select Brand in the Chinese Mainland,” Hyatt Newsroom, newsroom.hyatt.com. Over time, that shift should widen the demand base in the Hotels market from gateway cities into secondary business and leisure destinations.

Increasing Corporate Travel and MICE Demand Supporting Hotel Revenues

The Global Hotels Market still relies on corporate travel as a core demand layer, particularly for city hotels, airport hotels, and premium business-led assets. Business/Commercial Hotels remained the largest hotel type in 2025, which shows that transient work travel, meetings, and commercial stays still provide an important demand anchor. The return of project-based travel and the blending of work with short leisure extensions are increasing the value of each booking, even when trip frequency is not fully back to its former levels. In the Hotels market, this is especially relevant for properties with strong meeting space, loyalty reach, and weekday demand capture. That demand profile also supports corporate contracts and direct channels because repeat business travelers are more likely to respond to brand distribution and loyalty offers than purely price-led vacation guests.

Boom in Domestic Staycation Tourism Sustaining Occupancy

The Global Hotels Market has also been supported by domestic leisure travel, which remains important even as international tourism strengthens. Domestic demand is helping operators fill short breaks, long weekends, and shoulder periods that are less dependent on airline capacity or visa conditions. This is one reason leisure remains the largest end-user segment, with 57.20% share in 2025, even while other travel categories recover. In the Hotels market, staycation demand also supports regional resorts, drive-to destinations, and city properties that package dining, wellness, and weekend experiences for local guests. The result is a steadier occupancy base that reduces dependence on a single traveler type and gives operators more scope to manage rates across the week.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Macroeconomic & Geopolitical Volatility Dampening Travel Sentiment | -0.8% | Global, acute in Middle East and Africa, and North America inbound | Short term (≤ 2 years) |

| High Capex Requirements With Long Pay-Back Periods | -0.5% | Global, most acute in North America and Europe | Long term (≥ 4 years) |

| Acute Labour Shortages & Wage Inflation in Tourism Hubs | -0.6% | North America, Europe, Asia-Pacific core | Medium term (2-4 years) |

| ESG-Linked Financing Headwinds for Non-Sustainable Hotel Assets | -0.4% | Europe and North America, with spill-over to Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Macroeconomic and Geopolitical Volatility Creating Demand Uncertainty

The Global Hotels Market remains exposed to abrupt demand swings when geopolitical events alter traveler confidence, airline schedules, or regional investment plans. Marriott stated in its first quarter 2026 results that conflict-related pressure in the Middle East was expected to reduce RevPAR at its Middle East properties by nearly 50% in the second quarter of 2026[3]Marriott International, “Marriott International Reports First Quarter 2026 Results,” Marriott Investor Relations, marriott.gcs-web.com. The same filing noted a full-year drag of 100 to 125 basis points on global RevPAR, which shows that local disruption can quickly pass through to global hotel performance. In the Hotels market, this kind of volatility affects not only occupancy but also average stay length, booking windows, and cancellation behavior. It is therefore a margin risk as much as a demand risk, especially for operators with high fixed costs or large exposure to international gateway markets.

High Capex Requirements With Long Pay-Back Periods Limiting Expansion Flexibility

The Global Hotels Market continues to face heavy capital needs because new builds, renovations, sustainability upgrades, and brand conversions all require long-dated investment. That burden is one reason many global chains prefer management and franchise structures rather than holding large asset positions on their balance sheets. IHG’s investor materials show that the business model now strongly leans toward fee-based structures, with 73% of rooms franchised and 27% managed. In the Hotels market, owners that cannot access low-cost capital may delay refurbishments, which can weaken pricing power and brand relevance over time. The long pay-back profile also slows supply response, which supports incumbents in strong locations but raises risk for smaller owners in weaker financing conditions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Hotel Type: Resort Momentum Outpaces the Business Segment

Business/Commercial Hotels held 34.20% of the market in 2025, making them the largest hotel type in the Global Hotels Market. That position reflects the steady role of business travel, urban commercial stays, and the stability of demand offered by gateway cities and large domestic corporate corridors. Even with some changes in trip frequency, business-led demand still gives hotels stronger weekday occupancy and supports meeting space, food service, and premium room categories. This also helps branded operators because repeat corporate travelers are more responsive to loyalty programs and standardized service delivery. The segment therefore remains a structural anchor for the Hotels market, even as the mix of business travel becomes more project-led and less reliant on long uninterrupted stays.

Resort Hotels are forecast to grow at a 8.84% CAGR through 2031, making them the fastest-growing hotel type in the Global Hotels Market. That pace reflects the stronger pull of leisure-led travel, longer experience-based stays, and the rise of bleisure, where work trips expand into personal vacations. Agoda found that 76% of Asia-Pacific business travelers plan to add leisure time to work travel in 2026, a behavior that directly supports resort demand in destinations with strong weekend and wellness appeal. Boutique Hotels continue to benefit from travelers seeking differentiated stays, while transit and B&B formats maintain a more stable, narrower role. Casino Hotels and other formats remain relevant in specialized corridors. Still, the main growth shift in the Hotels market is toward leisure-rich formats that can capture spending on rooms, food, wellness, and local experiences in a single stay.

By Price Category: Midscale Scale Meets Luxury Growth Premium

Midscale properties accounted for 45.10% of the Global Hotels Market size in 2025, underscoring the importance of value-for-money positioning across the broader traveler base. The segment benefits from wide geographic coverage, balanced pricing, and suitability for both business and leisure demand. It also fits well with domestic travel and short-stay demand, where affordability matters but service consistency still carries weight. In many destinations, midscale supply is the main bridge between fully budget-led formats and premium chains with higher daily rates. That keeps midscale central to the hotel market because it serves the largest practical pool of travelers across cities, highways, airport zones, and secondary tourist destinations.

Luxury hotels are projected to expand at a 8.96% CAGR through 2031, making them the fastest-growing price category in the Global Hotels Market. This reflects better pricing resilience among affluent travelers and stronger exposure to wellness, destination, and experience-led demand. Regulatory pressure on some alternative lodging models also favors premium hotels, as higher-spending travelers often value service consistency, security, and branded amenities more. Luxury growth is also supported by chain investment in distinctive concepts, such as Marriott’s move into dedicated luxury wellness through its 2026 Lefay partnership, which underlines how premium positioning is being refined rather than expanded. Economy and budget formats remain essential for volume. Still, the growth premium in the Hotels market is clearly shifting toward travelers who are less price-sensitive and more willing to spend across the full stay experience.

By Rating: Five-Star Growth Anchored by Premium Guest Spend

The 4-Star segment led with a 36.85% share of the Global Hotels Market in 2025, demonstrating the scale advantage of hotels that combine broad appeal with dependable service standards. This category sits between business policy compliance, aspirational leisure demand, and broad distribution reach. It can capture travelers who want a recognizable quality without moving into full luxury rate levels. In practical terms, 4-Star hotels often perform well because they can serve meetings, short breaks, family leisure, and corporate stays under a single operating model. That balanced demand mix keeps the segment important to the Hotels market across both mature and emerging destinations.

The 5-Star segment is expected to record the highest CAGR of 9.12% through 2031, which reflects stronger premium spending and higher ancillary revenue opportunities in the Hotels market. Growth in this tier is supported by wellness, branded experience curation, and a wider willingness among affluent travelers to pay for destination-led stays. Hyatt, Hilton, and Marriott have all continued to deepen premium or luxury positioning through expansions and partnerships in 2025 and 2026. Lower-star segments continue to serve necessary value demand, but their ability to expand revenue per guest is much more limited because they have fewer premium add-on categories. That is why the Hotels market is seeing faster value creation at the top end of the rating ladder even when lower-rated hotels still account for significant room volume.

By Ownership Model: Asset-Light Momentum Reshapes the Value Chain

Chain Hotels captured 53.40% of the Global Hotels Market in 2025, reflecting the enduring importance of brand reach, loyalty programs, and system-wide distribution. Large chains can spread technology investment, standards, and commercial partnerships across many geographies and traveler segments. They also gain from repeat customer data and stronger visibility on global search and booking platforms. This gives them an advantage in converting demand through direct channels and in protecting rate during mixed trading conditions. The scale edge is therefore not only operational, but also commercial and technological across the Hotels market.

Managed Hotels are forecast to grow at an 8.42% CAGR through 2031, making them the fastest-growing ownership model in the Global Hotels Market. The shift is linked to owners seeking brand and operating expertise without fully relinquishing asset ownership, especially in markets that are still deepening institutional hospitality capabilities. IHG’s current model provides a clear signal here, with its room base split between 73% franchised and 27% managed, while management remains important in several growth markets. This structure lowers balance sheet intensity for operators while keeping fee income attractive and scalable. As a result, the Hotels market is moving further toward a model where brand power, systems, and management capability matter more than direct asset ownership.

By Booking Channel: OTA Scale Faces a Stronger Direct Booking Push

Online Travel Agencies held a 39.15% share of the Global Hotels Market in 2025, making them the leading booking channel in the Hotels market. OTAs remain important because they aggregate demand, improve hotel visibility, and support traveler discovery when comparing destinations, dates, and rates across brands. They are especially influential for independent hotels and for consumers who begin with destination search rather than a specific property or brand. This broad reach gives OTAs a durable role even as hotels try to improve channel mix. The hotel market, therefore, continues to rely on OTAs for demand generation, particularly in fragmented destinations and for first-time or infrequent guests.

Direct Booking is projected to grow at an 8.73% CAGR through 2031, which shows that the Global Hotels Market is steadily improving at converting demand into lower-cost channels. A Report says that 18% of travelers who start their search on an OTA ultimately book directly with the hotel, and that rate rose by 3.3 percentage points year over year[4]SiteMinder, “Changing Traveller Report 2026,” SiteMinder, siteminder.com. That shift reflects years of investment by the major chains in loyalty programs, branded apps, mobile booking, and member-only offers. Direct channels also improve data capture, reduce the commission burden, and create more room for upsell once the guest is already in the brand ecosystem. In the Hotels market, OTAs will remain powerful, but the strongest profit improvement is likely to come from chains that use those platforms for discovery and then convert more demand through their own websites and apps.

By End-User: Bleisure Emerges as the Strongest Growth Pool

Leisure travelers accounted for 57.20% of the Global Hotel Market in 2025, confirming that leisure remains the broad occupancy foundation of the hotel market. This segment benefits from holiday travel, family trips, seasonal breaks, and experience-led destination demand across resort, city, and regional formats. It also aligns closely with the midscale and resort categories, as those formats can serve both planned vacations and short domestic getaways. Leisure demand is valuable not only because of volume, but also because it supports ancillary categories such as dining, recreation, and package-based selling. That makes it the core volume engine of the Hotels market, even when premium and hybrid traveler types are growing faster.

Bleisure is expected to expand at a 10.04% CAGR through 2031, making it the fastest-growing end-user group in the Global Hotels Market. A recent report says that 76% of Asia-Pacific business travelers plan to combine work and leisure this year, with even higher intent in several Southeast Asian markets. This matters because bleisure travelers often stay longer, spend more across the property, and are more likely to mix weekday business demand with weekend resort or city leisure demand. That behavior supports both urban hotels and leisure destinations by improving occupancy distribution across the week. In the Hotels market, bleisure is no longer a side theme and has become a structural demand bridge between corporate and leisure travel.

Geography Analysis

North America accounted for 31.10% of the market in 2025, making it the largest regional contributor to the Global Hotels Market. The region remains supported by a broad domestic travel base, deep brand penetration, and strong chain-led commercial infrastructure. It also benefits from a wide mix of urban, resort, highway, airport, and convention-oriented properties that spread demand across formats. In the Hotels market, North America is important not only for its current scale but also because many operating, loyalty, and pricing practices that later spread globally are tested here first. South America remains smaller in scale, but it continues to offer selective opportunities where domestic demand and regional tourism are improving faster than long-haul inbound dependence.

Europe remains central to the Global Hotels Market, recording 793 million international tourist arrivals in 2025, up 4% from 2024 and 6% above 2019 levels. That arrival depth supports city hotels, heritage destinations, and cross-border short-haul travel more than most other regions. Europe is also one of the clearest examples of how regulation is beginning to reshape accommodation competition, as seen in France’s tighter approach to furnished tourist rentals. Sustainability-linked financing standards are gaining influence across Europe as well, underscoring the strategic value of efficient, compliant, and well-capitalized hotel assets. For the Hotels market, Europe remains large and resilient, but performance is becoming more uneven across countries depending on regulation, refurbishment cycles, and traveler mix.

Asia-Pacific is forecast to grow at the fastest CAGR of 8.91% through 2031, which makes it the most dynamic regional growth engine in the Global Hotels Market. The region is benefiting from stronger domestic and regional travel, rising bleisure intent, and continued brand expansion by global hotel groups. Hyatt’s Chinese Mainland franchise agreement with Dossen Group and IHG’s Indian airport portfolio deal both show how global operators are positioning for long-term demand in high-growth corridors. The Middle East and Africa also offer meaningful long-term opportunities, but near-term volatility is higher, as Marriott’s 2026 Middle East guidance makes clear. Across the Global Hotels Market, Asia-Pacific stands out because demand growth, ownership model evolution, and brand expansion are all moving in the same direction.

Competitive Landscape

The Global Hotels Market shows a two-layer structure, with a concentrated branded tier led by Marriott, Hilton, IHG, Accor, and Hyatt, and a far larger independent base spread across local and regional operators. This means scale is strong at the top, but total market ownership and property count remain widely dispersed. The leading chains continue to win through loyalty reach, global distribution, operating systems, and their ability to expand without owning every asset. In the Hotels market, the strategic contest is less about adding hotels at any cost and more about adding the right hotels under the right contractual model. That is why management contracts, franchising, direct booking, and revenue systems now matter as much as physical footprint.

Pipeline expansion remains active among major groups, but the growth model is increasingly selective and asset-light in the Global Hotels Market. Hyatt ended 2025 with a record global pipeline of approximately 148,000 rooms, which signals continued confidence in branded growth. Marriott reported a worldwide pipeline of nearly 618,000 rooms in the first quarter of 2026, with conversions accounting for more than 35% of signings, underscoring the importance of brand conversions to global expansion. In the Hotels market, chains with strong brand architecture, owner relationships, and the ability to quickly absorb existing hotels into their commercial platforms are favored. It also creates space for independent hotels to use technology tools to defend rates and visibility without surrendering ownership or identity.

Strategic moves by leading companies show where the hotel market is heading over the next few years. Hyatt’s master franchise agreement with Dossen Group in the Chinese Mainland points to deeper interest in upper-midscale growth and local-scale partnerships. IHG’s agreement with Adani Airport Holdings and its Vietnam partnership with Vinhomes Green Paradise Can Gio demonstrate how airport, urban, and destination-led projects are increasingly tied to mixed-use and infrastructure-led development. Cloudbeds’ Signals launch also highlights how technology providers are becoming more influential in performance management, especially for independent hotels. The overall result is a Hotels market where scale still matters, but technology, contract structure, and channel control increasingly shape competitive advantage.

Hotels Industry Leaders

Marriott International Inc.

Jin Jiang International Holdings Co. Ltd.

Hilton Worldwide Holdings Inc.

InterContinental Hotels Group PLC

Accor S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Hyatt Hotels Corporation announced a master franchise agreement with Dossen Group's subsidiary to exclusively develop and operate Hyatt Select brand hotels across the Chinese Mainland, targeting the fast-growing upper-midscale segment as domestic guest expectations sophisticate.

- May 2026: IHG Hotels & Resorts signed a landmark managed hotel portfolio agreement with Adani Airport Holdings Limited for the development of approximately 1,500 keys across 5 hotels in key Indian gateway cities and airport destinations, meaningfully strengthening IHG's 98-hotel India pipeline.

- April 2026: Hilton reported Q1 2026 results, opening 131 hotels totalling 16,300 rooms and raising its full-year RevPAR and earnings outlook, key openings included Waldorf Astoria Rabat Sale, the first Waldorf in Morocco, and Motto by Hilton Recife Antigo, the brand debut in Brazil.

- April 2026: IHG Hotels & Resorts and Vinhomes Green Paradise Can Gio signed a strategic partnership to introduce four IHG brands across more than 1,000 rooms at a world-class coastal mega-development in Ho Chi Minh City, Vietnam.

Global Hotels Market Report Scope

| Business/Commercial Hotels |

| Boutique Hotels |

| Resort Hotels |

| Casino Hotels |

| Transit Hotels |

| Bed & Breakfast Hotels |

| Others |

| Economy/Budget |

| Midscale |

| Luxury |

| 1 Star |

| 2 Star |

| 3 Star |

| 4 Star |

| 5 Star |

| Chain Hotels |

| Independent Hotels |

| Managed Hotels |

| Others |

| Direct Booking (Brand Website, Call Center) |

| Online Travel Agencies (OTA) |

| Travel Agents / Tour Operators |

| Corporate Contracts |

| Leisure |

| Bleisure |

| Business |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Hotel Type (Value) | Business/Commercial Hotels | |

| Boutique Hotels | ||

| Resort Hotels | ||

| Casino Hotels | ||

| Transit Hotels | ||

| Bed & Breakfast Hotels | ||

| Others | ||

| By Price Category (Value) | Economy/Budget | |

| Midscale | ||

| Luxury | ||

| By Rating | 1 Star | |

| 2 Star | ||

| 3 Star | ||

| 4 Star | ||

| 5 Star | ||

| By Ownership Model (Value) | Chain Hotels | |

| Independent Hotels | ||

| Managed Hotels | ||

| Others | ||

| By Booking Channel (Value) | Direct Booking (Brand Website, Call Center) | |

| Online Travel Agencies (OTA) | ||

| Travel Agents / Tour Operators | ||

| Corporate Contracts | ||

| By End-User | Leisure | |

| Bleisure | ||

| Business | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Global Hotels market?

The Hotels market stands at USD 1.37 trillion in 2026 and is projected to reach USD 1.89 trillion by 2031 at a CAGR of 6.55%.

Which hotel type is growing the fastest through 2031?

Resort Hotels are the fastest-growing hotel type, with an expected CAGR of 8.84% through 2031, supported by leisure and bleisure demand.

Which booking channel leads hotel reservations today?

Online Travel Agencies lead in 2025 with a 39.15% share, although Direct Booking is growing faster at an 8.73% CAGR through 2031.

Why is bleisure important for hotel operators?

Bleisure is growing at a 10.04% CAGR through 2031, and A report says that 76% of Asia-Pacific business travelers plan to mix work and leisure in 2026.

Which region leads global hotel demand and which grows the fastest?

North America held the largest share at 31.10% in 2025, while Asia-Pacific is the fastest-growing region with an 8.91% CAGR through 2031.

What are the main risks affecting hotel profitability?

The main risks are geopolitical volatility, high capital requirements, labor cost pressure, and tighter ESG-linked financing standards for non-sustainable assets.

Page last updated on: