Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

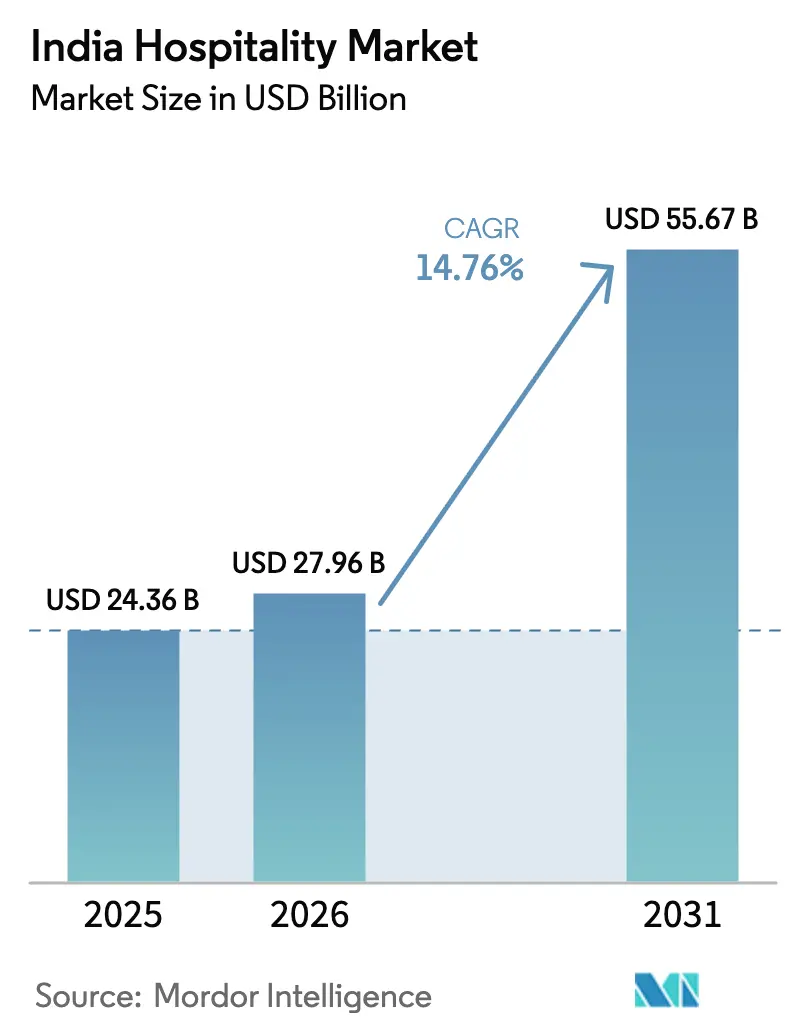

| Base Year Market Size (2025) | USD 24.36 Billion |

| Market Size (2026) | USD 27.96 Billion |

| Market Size (2031) | USD 55.67 Billion |

| Growth Rate (2026 - 2031) | 14.76% CAGR |

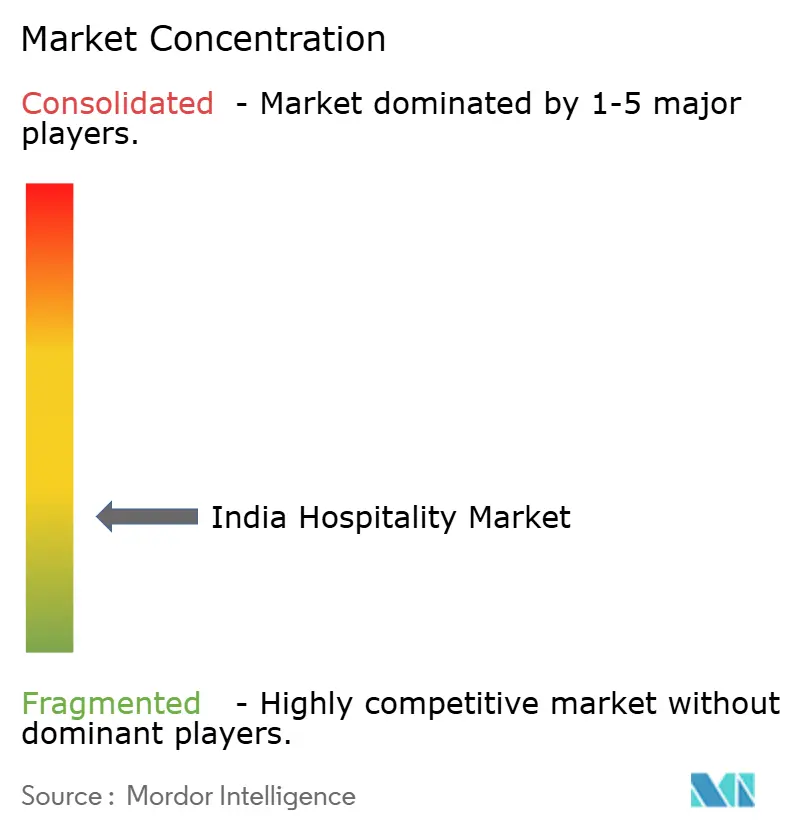

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Hospitality Market Analysis by Mordor Intelligence

The India Hospitality Market size is projected to be USD 24.36 billion in 2025, USD 27.96 billion in 2026, and reach USD 55.67 billion by 2031, growing at a CAGR of 14.76% from 2026 to 2031.

Growth of the hospitality industry in India is driven by a larger domestic travel base, a rising middle-income population, and improved air and road connectivity that increases travel frequency. Domestic visitor spending has been rising and is expected to continue, highlighting the sector’s reliance on local travelers across leisure, pilgrimage, and business segments. Airports in India have more than doubled over the past decade, while government programs are expanding destination and pilgrimage infrastructure, creating new investable locations. Foreign tourist arrivals are recovering, supported by destination marketing and digital tools that simplify planning and booking. Hospitality operators are adopting asset-light models to reduce capital risk and leveraging digital strategies to retain repeat customers through proprietary channels. Overall, the market demonstrates strong growth potential fueled by domestic demand, improved connectivity, and strategic industry adaptation.

Key Report Takeaways

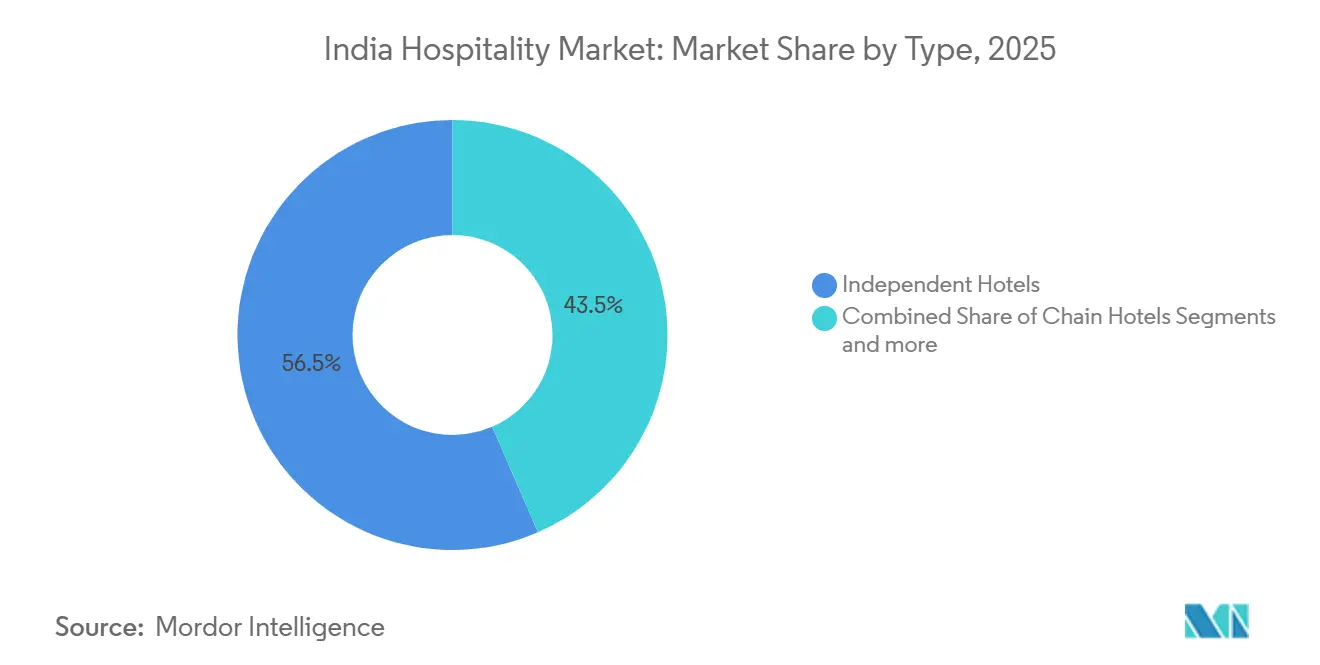

- By type, Independent Hotels led with 56.45% of the India hospitality market share in 2025, while Chain Hotels are forecast to expand at a 16.76% CAGR through 2031.

- By accommodation class, Mid and Upper-Mid-scale properties held 38.55% of the India hospitality market share in 2025, while Luxury is projected to grow at a 15.13% CAGR through 2031.

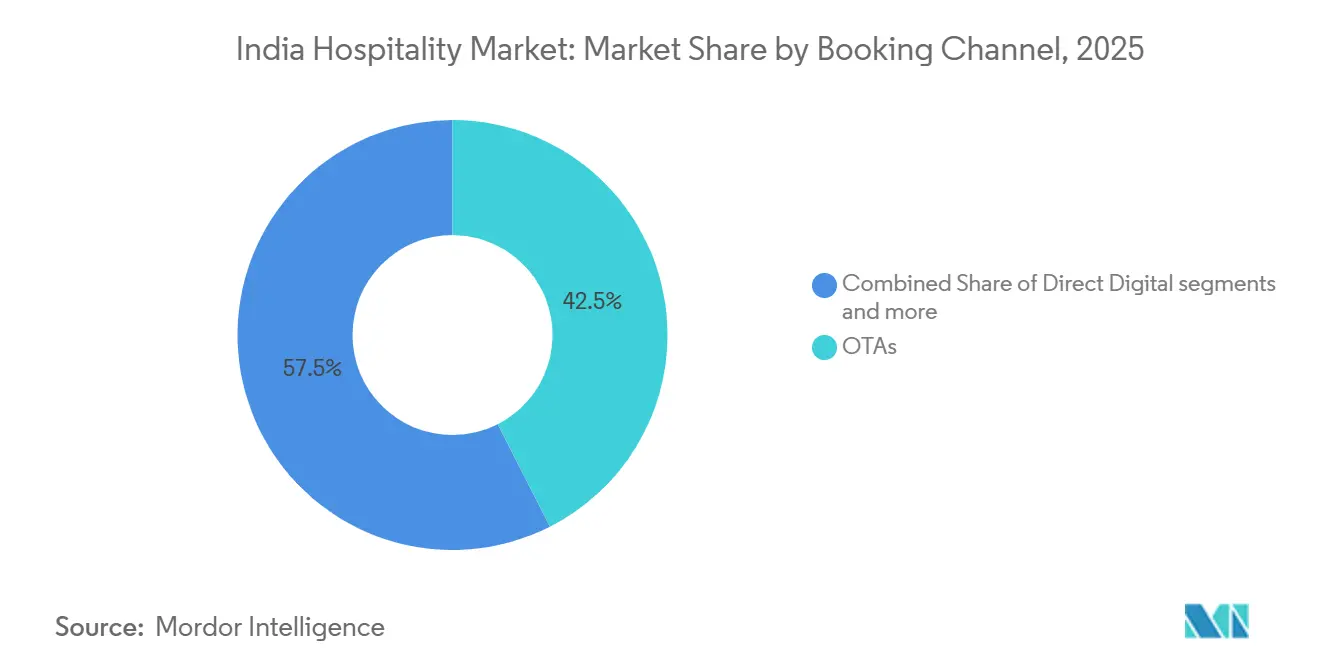

- By booking channel, Online Travel Agencies accounted for 42.51% of the India hospitality market share in 2025, while Direct Digital is forecast to grow at a 15.53% CAGR through 2031.

- By geography, West India held 30.13% of the India hospitality market share in 2025, while North-East India is projected to post the fastest growth at a 16.46% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

India Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Domestic Middle-Class Leisure Spend | +3.8% | National, concentrated in metros and emerging Tier-1 cities (Ahmedabad, Pune, Kochi) | Medium term (2-4 years) |

| Government Initiatives Supporting Market Growth | +2.7% | National, with flagship infrastructure in North (Ayodhya) and North-East (air connectivity) | Long term (≥ 4 years) |

| Budget & Mid-Scale Chain Expansion | +2.5% | National, spill-over to Tier-2/3 cities (Gandhidham, Ranchi, Udaipur) | Short term (≤ 2 years) |

| Upgraded Pilgrimage Circuits Driving Spiritual & Wellness Tourism | +2.9% | North India core (Varanasi, Ayodhya, Haridwar), extending to South (Tirupati, Rameswaram) | Medium term (2-4 years) |

| Hybrid-Work Long-Stay Demand in Hill & Beach Towns | +1.4% | Kerala, Goa, Himachal, with early gains in Munnar, Coorg, Manali | Short term (≤ 2 years) |

| e-Visa Expansion to 166 Countries Shortening Booking Lead-Times | +1.5% | Global inbound, strongest impact in gateway cities (Delhi, Mumbai, Bengaluru) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Domestic Middle-Class Leisure Spend

Rising incomes among India’s growing middle class are driving strong growth in domestic leisure travel. According to the India Tourism Data Compendium 2025, domestic tourism far exceeds inbound travel, with spending reaching around USD 185 billion in 2024. Younger travelers are increasingly opting for experience-led trips, including cultural, adventure, and wellness travel, boosting per-trip expenditure. Supportive government initiatives like improved connectivity and Dekho Apna Desh campaigns have made travel more accessible, making the middle class a key driver of India’s tourism growth. [1] Ministry of Tourism, Government of India, “India Tourism Data Compendium 2025,” Ministry of Tourism, tourism.gov.in. Operators benefit from greater spend per trip and more frequent weekend getaways, trends that support occupancy and allow careful revenue management during peak seasons. The dispersion of demand beyond metros into Tier-1 and key Tier-2 cities strengthens local corridors, lifts room-night absorption, and encourages conversions of unbranded properties into organized flags. The India hospitality market, therefore, draws strength from domestic leisure resiliency, which limits volatility from corporate cycles and inbound shocks. These shifts support steady pricing power in urban and leisure clusters where branded supply is still building out.

Government Initiatives Supporting Market Growth

Tourism programs focused on circuits, destinations, and digital discovery continue to expand the investable landscape in the India hospitality market. The Ministry of Tourism has sanctioned projects under Swadesh Darshan 2.0 and PRASHAD to strengthen infrastructure at high-traffic religious and cultural sites, and it is rolling out connectivity projects that improve access to secondary destinations. The government’s Incredible India initiatives and the digital platform have enhanced awareness and discovery, with large volumes of domestic visits recorded on official platforms in 2024 as part of sustained promotion of top destinations. [2]Press Information Bureau, “PRASHAD Scheme Press Release,” Press Information Bureau, pib.gov.in. Expansion in operational airports has improved airlift into multiple state capitals and leisure hubs, reinforcing traffic into both business and holiday markets. Budget allocations to tourism infrastructure in FY26 underscore a steady policy impetus that helps de-risk investment planning for operators and developers. Over time, these measures are expected to distribute demand more evenly across regions, reduce seasonality, and drive a healthier mix of trip purposes.

Budget & Mid-Scale Chain Expansion

Asset-light growth is transforming India’s hospitality market, with chains prioritizing management contracts and franchise conversions to scale rapidly. Organized brands currently represent a small share of total room inventory, leaving significant unbranded capacity available for conversion. Mid-scale global brands are expanding with locally adapted offerings, such as Marriott’s Series, targeting corporate and pilgrimage corridors at accessible price points. Growth in Tier-2 and Tier-3 cities formalizes grey-market inventory and improves hygiene and safety standards, boosting guest confidence. This approach reduces capital intensity for operators, allows faster market entry, and increases repeat bookings through direct channels. Expansion of budget and mid-scale chains is supported by rising domestic travel and demand for affordable, quality stays, with organized hotel inventory projected to exceed 300,000 branded rooms by 2029. Government initiatives, including lower GST on rooms under USD 90.35, further enhance investment, occupancy, and overall market growth. [3]India Brand Equity Foundation, “Tourism & Hospitality,” India Brand Equity Foundation, ibef.org.

Upgraded Pilgrimage Circuits Driving Spiritual & Wellness Tourism

Pilgrimage circuits continue to create multi-night stay opportunities that lift room-night demand near major temples and spiritual hubs. Government programs have directed spending toward religious corridors and amenities that ease travel for families and elderly visitors, which translates to longer stays and higher per-visit spending at destination-adjacent hotels. Ayodhya’s 2024 consecration created a surge of pilgrim movement that lifted room demand, and enhanced airport and road links are unlocking similar trends in Varanasi and other spiritual centers. A segment of guests now seeks premium lodging with wellness add-ons such as Ayurveda-based treatments and yoga experiences, which further supports higher-rate inventory around leading spiritual destinations. Operators are responding by refurbishing heritage buildings and adding boutique properties calibrated to high-spend spiritual travelers. The hospitality industry in India gains a durable demand spine from spiritual and wellness travel that complements urban corporate traffic and beach-leisure segments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High GST on Premium Room Tariffs | -1.8% | National, acute in luxury/premium urban hotels (Mumbai, Delhi, Bengaluru) | Short term (≤ 2 years) |

| Transport Infrastructure Gaps in Tier-2/3 Airports & Rail | -1.3% | Tier-2/3 cities, North-East India, islands (Lakshadweep, Andamans) | Long term (≥ 4 years) |

| Skilled-Talent Drain to Gig Economy & GCCs | -1.1% | Metro hubs with competing gig platforms (Bengaluru, Gurugram, Pune, Hyderabad) | Medium term (2-4 years) |

| Land-Acquisition & CRZ Compliance Delays for Resorts | -0.9% | Coastal zones (Goa, Kerala, Andamans), states with fragmented land records | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High GST on Premium Room Tariffs

The current GST structure imposes a higher tax on rooms above a certain tariff threshold, which reduces net yields for premium city hotels and upscale leisure resorts. This limits India’s price competitiveness compared to some Southeast Asian destinations for high-value leisure and MICE travelers. Margin pressures also arise for operators when input costs and tax credits are restricted at lower tariff bands, affecting pricing flexibility for budget and mid-scale hotels. These challenges are particularly pronounced in top metros, where mid-tier average daily rates often approach or exceed the GST threshold. Operators must carefully balance occupancy and rate strategies to maintain demand while protecting profitability. In the near term, the market needs to design offerings that preserve rate integrity while ensuring value for guests managing higher trip expenses.

Transport Infrastructure Gaps in Tier-2/3 Airports & Rail

Connectivity challenges continue to constrain supply expansion in smaller cities and remote destinations with high leisure potential. Limited flight options, inadequate last-mile road infrastructure, and inconsistent local utilities can increase project timelines and development costs, delaying hotel openings and discouraging private investment. Regions like the North-East remain under-penetrated despite rich cultural and biodiversity assets, reflecting access and perception barriers. Even where new airports are operational, workforce readiness often lags, requiring operators to invest in training and relocation to maintain service standards. Until connectivity programs mature and transportation links stabilize, these infrastructure gaps will continue to limit the growth of the hospitality market in Tier-2 and Tier-3 locations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Asset-Light Franchise Models Accelerate Chain Rollouts

Independent Hotels held 56.45% of the India hospitality market share in 2025, while Chain Hotels are projected to grow at a 16.76% CAGR through 2031 as asset-light models support wider, faster expansion. Operators are converting unbranded inventory into standardized flags that leverage loyalty, distribution technology, and brand quality audits to lift visibility and rate realization. The hospitality sector in India benefits from conversions that enhance hygiene and safety standards, which increases trust among family travelers and international visitors. Global chains are also positioning mid-scale brands in Tier-2 and Tier-3 cities to close the quality gap in corporate corridors and pilgrimage circuits. Organized brands continue to add management contracts that reduce upfront capital needs for developers while creating fee-based revenue streams for operators.

Independent operators still anchor local markets where entrepreneurial ownership and location advantages remain strong. Even so, brand affiliation is gaining traction because it can reduce marketing and distribution spends and help stabilize occupancy across seasons. With organized hotels representing a small portion of total rooms, conversion-led growth remains a durable theme for the hospitality industry in India. Digital reviews and meta-search comparisons also reward standardization, nudging independents to adopt brand systems to protect demand from OTA-driven price wars. As a result, Chain Hotels’ share should rise as conversions accelerate and new management agreements add keys in strategically important nodes.

By Accommodation Class: Luxury Premiumization Meets Mid-Scale Workhorse Growth

Mid and Upper-Mid-scale properties commanded 38.55% share in 2025, serving demand from corporate travelers, domestic leisure families, and small meeting groups at accessible price points. The India hospitality market size advantage for this class rests on dense urban distribution and proximity to industrial and IT hubs, which provide weekday volume and steady event traffic. At the same time, Luxury is projected to grow at 15.13% CAGR through 2031 as affluent guests seek heritage stays, wellness immersion, and high-touch service near key spiritual and leisure destinations. Spiritual-circuit upgrades and destination marketing improve destination appeal for premium guests who prefer curated experiences and short-stay renewals. These trends support rate integrity at the top end while mid-scale continues to deliver volume.

Service Apartments are maturing as a flexible option for long-stays, relocations, and hybrid-work professionals. International brands operate multiple residences in India that offer kitchenettes, flexible leases, and loyalty integration, which complement traditional hotels in gateway and secondary cities. Budget and economy hotels provide essential coverage for price-conscious travelers, though staffing and input-cost pressures can limit service upgrades without tariff changes. Operators balance these realities by focusing on efficiency, select-service design, and technology for lean operations. The India hospitality market benefits from this layered supply, which matches diverse price points and trip purposes across regions.

By Booking Channel: Direct Digital Platforms Reclaim Margin from OTA Dominance

Online Travel Agencies accounted for 42.51% of bookings in 2025, having improved discovery and price transparency for travelers and independents alike. The India hospitality market's exposure to OTAs remains significant for seasonal spikes and last-minute segments, where mobile discovery drives quick conversion. Direct Digital is projected to grow at a 15.53% CAGR through 2031 as brands deepen loyalty benefits, improve websites and apps, and offer member-only rates to shift repeat guests to proprietary channels. Brands are pairing direct offers with targeted communications and better user experiences to reduce friction at checkout and improve retention. Corporate and MICE contracts continue to be valuable for city hotels due to bundled room and F&B commitments that can stabilize weekday utilization.

Traditional agents remain relevant in inbound leisure because language support and itinerary curation reduce planning complexity for long-haul travelers. For premium properties, direct concierge relationships support bespoke packages, destination experiences, and tailored wellness add-ons that OTAs do not deliver. The India hospitality industry will continue to use a mix of OTA reach for discovery and direct channels for repeat conversion and margin protection. Over time, operators that successfully blend the two can optimize RevPAR, balance occupancy and rates, and build higher lifetime value across cohorts. This multi-channel balance is now a core strategic pillar in most branded chains’ commercial playbooks.

Geography Analysis

West India accounted for a 30.13% share in 2025, combining Mumbai’s corporate traffic, Goa’s leisure draw, and Gujarat’s industrial corridor demand. As India’s financial capital, Mumbai supports year-round business stays and sustained premium ADRs at top business districts. Goa continues to attract heavy seasonal leisure traffic from domestic and international visitors, while improved airlift supports better year-round occupancy for resorts and boutique properties. Gujarat’s hubs provide steady weekday demand sourced from manufacturing and services, extending the business travel network that underpins regional performance. The India hospitality market remains resilient in West India as diversified demand streams and strong infrastructure protect base occupancy.

South India presents balanced growth drivers that span IT services, pharmaceuticals, manufacturing, wellness, and pilgrimage. Bengaluru captures a high share of corporate room nights due to its technology base and meeting infrastructure, while Chennai and Hyderabad add export-led and research-led traffic to the regional mix. Kerala’s wellness positioning sustains high-spend inbound demand, and a supportive policy stance continues to promote culture and nature-based experiences that lengthen stays. CRZ rules in coastal states influence resort footprints by capping height and floor area parameters in designated zones, which shape new project economics and push some developments to inland locations. The Indian hospitality market benefits from South India’s diverse demand profile, which helps mitigate single-sector cyclicality.

North, East, and North-East India together add depth and newly addressable demand pools. North India balances pilgrimage, leisure, and government-seat business travel, with Ayodhya and Varanasi drawing high pilgrim volumes and Delhi-NCR anchoring international gateways. East India’s mix of temple tourism in Odisha and heritage-led leisure around Kolkata sustains occupancy, though growth rates can lag due to slower industrial expansion. The North-East holds a smaller 2025 base but is projected to grow at 16.46% CAGR through 2031 as regional connectivity and accommodation options improve from a low starting point. As airport capacity and hospitality training expand, new keys are expected across Guwahati, Shillong, and other gateways, with early moves by selected chains and boutique players. West India’s position remains strong, and North-East India’s acceleration illustrates how connectivity unlocks latent cultural and adventure demand in the broader India hospitality market.

Competitive Landscape

The India hospitality market is moderately fragmented, with the top five operators together accounting for 34.8% RevPAR or room share in 2024. This structure supports a two-track opportunity set where nimble entrants can differentiate in niches while large chains consolidate unbranded inventory and scale asset-light pipelines. Organized rooms remain a smaller share of the total base, which leaves scope for conversions and new management contracts that improve service consistency across cities and spiritual corridors. International brands are intensifying mid-scale expansion, including Series by Marriott, which is tailored to corporate and pilgrimage nodes at accessible price points. [4]Marriott International, “Marriott Bonvoy Expands Portfolio in India with the Launch of Series by Marriott,” Marriott News, news.marriott.com. Domestic leaders are balancing premiumization through heritage and palace formats with select-service growth calibrated to Tier-2 corporate clusters, reinforcing a broad-based presence in the India hospitality market.

Sustainability-linked operations and technology enable cost control and quality at scale. Energy management initiatives at large chains demonstrate efficiency gains on utilities, which support margin resilience during cost inflation cycles. Portfolio strategies increasingly blend city business hotels, pilgrimage-adjacent properties, resorts, and serviced residences, which spreads risk and taps distinct demand pools across the year. Expansion roadmaps by major global chains target deeper penetration into secondary industrial towns where international and domestic corporate travel supports weekday rates. Domestic and international brands both emphasize loyalty, direct booking benefits, and data-driven pricing decisions to optimize conversion while reducing distribution costs. These shared priorities frame a competitive race to scale and standardize service across emerging micro-markets within the India hospitality market.

State-level regulation and land-use policies shape operating realities and can create localized moats for experienced players. Coastal resort projects must comply with CRZ rules on height and floor area, which affects beachfront supply options and timing. Destination campaigns led by governments direct attention to select nodes, which can quickly shift city-level demand toward newly promoted circuits. As brands secure strategic locations in key gateway and pilgrimage cities, early movers can lock in location advantage in the India hospitality market. Over the forecast period, expect conversion-led consolidation in mid-tier independents and a steady rise in management contracts that reinforce asset-light networks. Competitive positioning will also reflect the ability to recruit, train, and retain skilled staff to maintain service consistency at scale.

India Hospitality Industry Leaders

Indian Hotels Co. Ltd. (Taj)

OYO Hotels & Homes

Marriott International India

ITC Hotels

Lemon Tree Hotels

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Marriott International launched Series by Marriott in India with 26 properties targeting primary trade centers, pilgrimage towns, and select Tier-2 cities. The brand aims to capture mid-scale corporate and leisure demand with price points tailored to local markets.

- October 2025: Radisson Hotel Group India announced an accelerated expansion strategy with a focus on Tier-2 and Tier-3 cities via franchise and management contracts, leveraging improved regional air connectivity and rising corporate demand in secondary hubs.

- August 2025: ITC Hotels deployed AI-enabled energy management systems across select properties, reporting double-digit reductions in utility consumption through smart HVAC controls, predictive maintenance, and occupancy-linked lighting.

- June 2025: Hilton announced expansion of its Hampton by Hilton brand in India, with properties under development in Bengaluru, Hyderabad, Ahmedabad, Pune, and Jaipur to serve corporate travelers and domestic leisure guests at mid-scale price points.

India Hospitality Market Report Scope

The hospitality industry encompasses businesses offering accommodation, food and beverages, travel, and leisure services to both domestic and international tourists. This sector is pivotal for generating employment, boosting tourism, and bolstering the nation's service-driven economy. A complete background analysis of the hospitality industry in India, which includes an assessment of the industry associations, overall economy, emerging market trends by segments, significant changes in the market dynamics, and market overview, is covered in the report.

The India Hospitality Market Report is Segmented by Type (Chain Hotels, Independent Hotels, Alternate Accommodations), Accommodation Class (Luxury, Mid & Upper-Mid-scale, Budget & Economy, Service Apartments), Booking Channel (Direct Digital, Online Travel Agencies, Corporate/MICE, Wholesale & Traditional Agents), and Geography (North, West, South, East, North-East India).

By Type

| Chain Hotels |

| Independent Hotels |

| Alternate Accommodations (Serviced Apts, Branded Hostels) |

By Accommodation Class

| Luxury |

| Mid & Upper-Mid-scale |

| Budget & Economy |

| Service Apartments |

By Booking Channel

| Direct Digital |

| Online Travel Agencies (OTAs) |

| Corporate / MICE |

| Wholesale & Traditional Agents |

By Geographic Region

| North India |

| West India |

| South India |

| East India |

| North-East India |

| By Type | Chain Hotels |

| Independent Hotels | |

| Alternate Accommodations (Serviced Apts, Branded Hostels) | |

| By Accommodation Class | Luxury |

| Mid & Upper-Mid-scale | |

| Budget & Economy | |

| Service Apartments | |

| By Booking Channel | Direct Digital |

| Online Travel Agencies (OTAs) | |

| Corporate / MICE | |

| Wholesale & Traditional Agents | |

| By Geographic Region | North India |

| West India | |

| South India | |

| East India | |

| North-East India |

Key Questions Answered in the Report

What is the current size and projected growth of the India hospitality market by 2031?

The India hospitality market size is USD 27.96 billion in 2026 and is projected to reach USD 55.67 billion by 2031 at a 14.76% CAGR.

Which segments lead and grow fastest in the India hospitality market?

Independent Hotels lead by share and Chain Hotels grow fastest by type, Mid and Upper-Mid-scale lead by share and Luxury grows fastest by class, OTAs lead by bookings and Direct Digital grows fastest by channel, and West India leads by share while North-East India grows fastest by region.

How are government programs influencing the India hospitality market?

Infrastructure, destination, and pilgrimage schemes under Swadesh Darshan 2.0 and PRASHAD, alongside digital promotion, are improving accessibility and demand across new and existing nodes, supporting private investment and capacity additions.

What strategies are operators using to scale in the India hospitality market?

Operators are pursuing asset-light growth through management contracts and franchise conversions, improving service consistency and reach while limiting capital intensity, and they are strengthening direct digital channels to enhance margins and loyalty.

What are the most significant constraints for development and operations?

Higher GST on premium room tariffs and connectivity gaps in Tier-2 and Tier-3 locations constrain pricing competitiveness and delay new openings, while compliance in coastal zones shapes project footprints and timelines.

Which regions present the largest and fastest-growing opportunities?

West India remains the largest due to Mumbai and Goa, while North-East India is the fastest-growing region as improving connectivity and new supply unlock adventure and cultural tourism potential.

Page last updated on: