Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 49.91 Billion |

| Market Size (2026) | USD 51.93 Billion |

| Market Size (2031) | USD 63.32 Billion |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

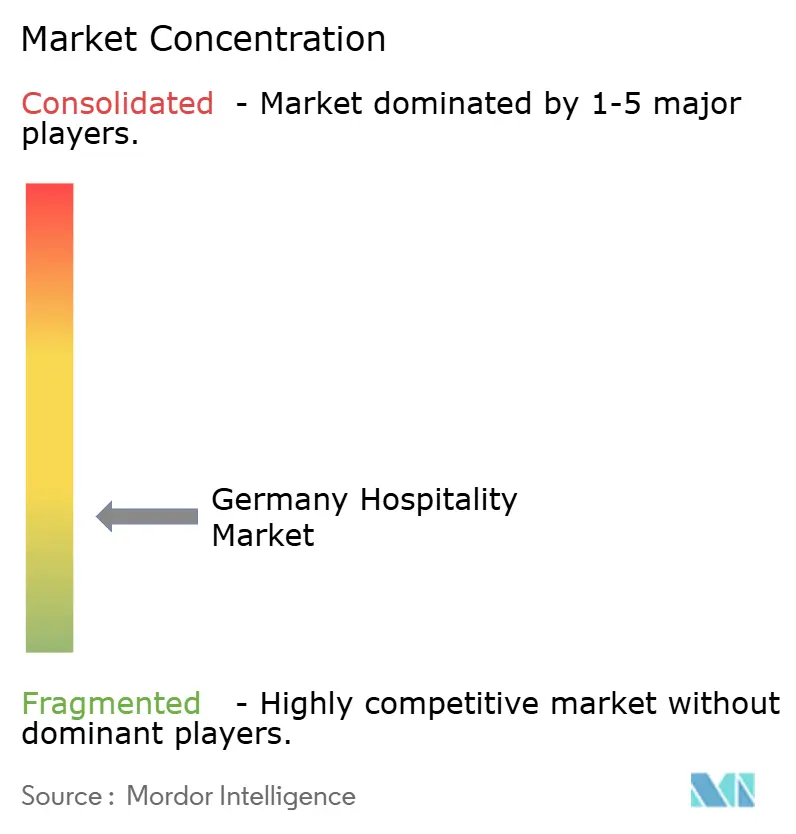

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Hospitality Market Analysis by Mordor Intelligence

The Germany Hospitality Market size was valued at USD 49.91 billion in 2025 and estimated to grow from USD 51.93 billion in 2026 to reach USD 63.32 billion by 2031, at a CAGR of 4.05% during the forecast period (2026-2031).

Record-high 496.1 million overnight stays in 2024, an 11.9% May 2025 RevPAR surge, and resilient domestic leisure demand confirm that the German hospitality market has regained, and slightly exceeded, its 2019 performance benchmarks. As global chains scale through franchising agreements, independent hotels continue to anchor supply, creating a dual-speed growth dynamic that intensifies competition for talent, sites, and distribution reach. Accelerated digital adoption, fuelled by the Digital Markets Act’s ban on price-parity clauses, shifts bookings toward direct online channels, boosting margins for properties that master CRM and loyalty economics. Structural constraints, shortages of skilled labor, fluctuating utility costs, and a decline in building permits are creating increasingly challenging operating conditions for the industry. However, these factors are simultaneously reinforcing rate integrity within an undersupplied market. This environment is expected to benefit from a forecasted 1.1% recovery in domestic GDP in 2025, presenting potential opportunities for growth despite current limitations[1].HSMAI Europe, “Europe’s Major Markets Are Not the Outperformers by MKG Consulting,” hospitalitynet.org

Key Report Takeaways

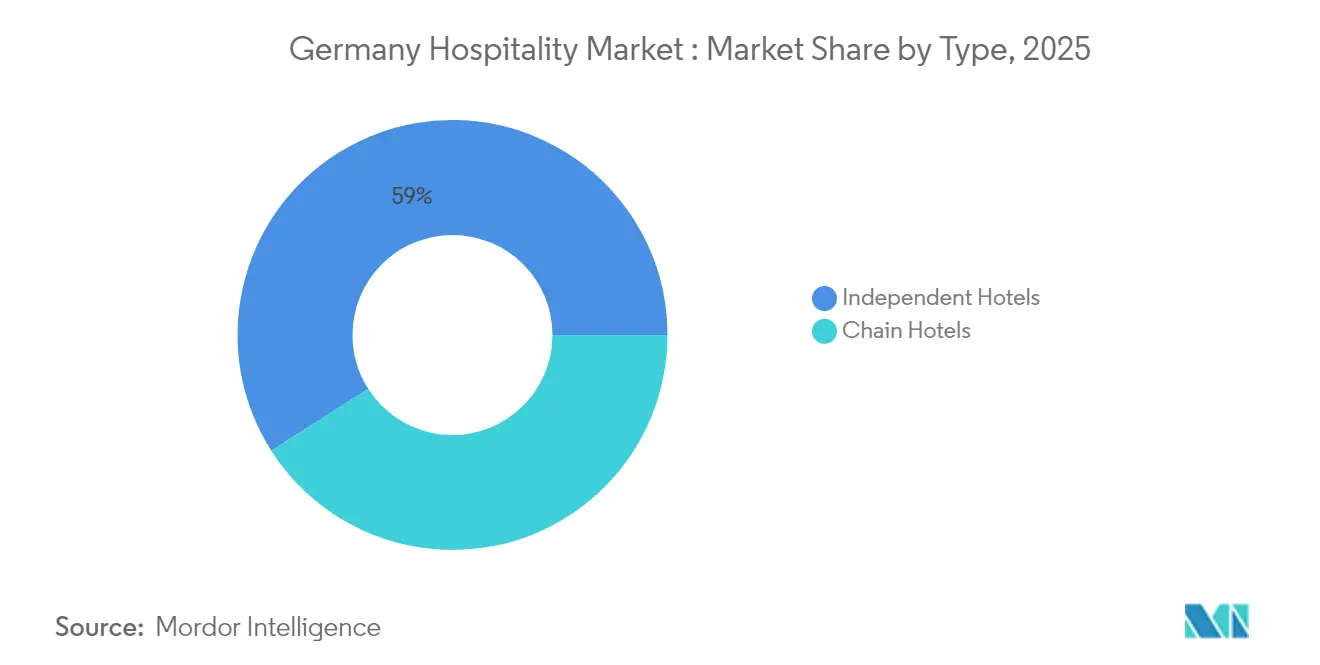

- By type, independent hotels led with 59.04% of Germany hospitality market share in 2025, while chain hotels are projected to grow at a 7.41% CAGR through 2031.

- By accommodation class, mid and upper-mid-scale properties captured 47.22% of Germany hospitality market share in 2025; serviced apartments are advancing at an 8.12% CAGR to 2031.

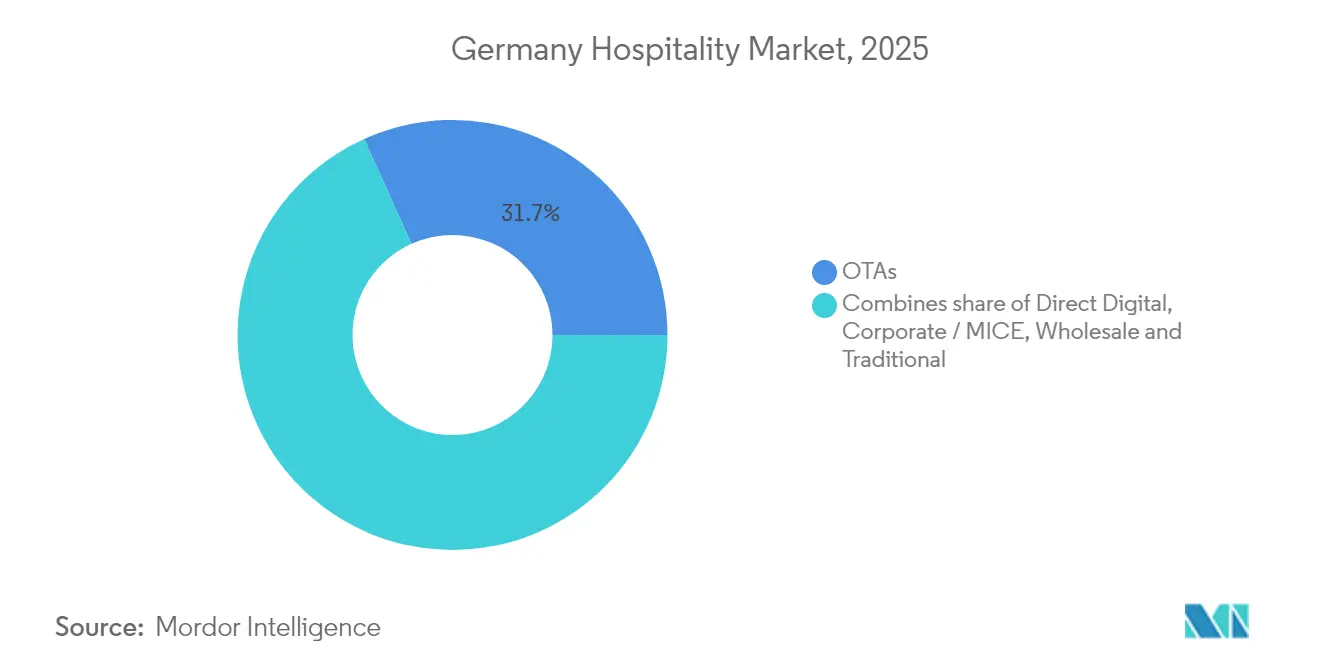

- By booking channel, OTAs held a 31.74% share of Germany hospitality market size in 2025, whereas direct digital bookings are set to expand at a 9.86% CAGR.

- By geography, South Germany generated 30.07% of Germany hospitality industry share in 2025, and East Germany is on track to deliver a 6.18% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industrial Cluster Network Generating Regional Hotel Demand | 0.80% | Southern automotive and industrial corridors | Medium term (2–4 years) |

| Trade Fair Infrastructure Supporting Event-Based Accommodation Peaks | 1.00% | Major German trade fair cities | Short term (≤ 2 years) |

| Rail Connectivity Supporting Domestic Leisure Mobility | 0.60% | ICE rail and leisure corridors | Short term (≤ 2 years) |

| Aparthotel Growth Driven by Extended Business Assignments | 0.70% | Major urban extended-stay districts | Medium term (2–4 years) |

| Hotel Consolidation Creating Investment and Modernization Opportunities | 0.50% | Secondary city hotel consolidation markets | Long term (≥ 4 years) |

| Regional Nature and Wellness Destinations Expanding Beyond Urban Markets | 0.60% | Black Forest and Alpine wellness regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Industrial Cluster Network Generating Regional Hotel Demand

Germany's industrial clusters generate stable year-round hotel demand from corporate travel, supplier visits, and business meetings. Manufacturing hubs such as Stuttgart, Munich, Cologne, and Düsseldorf attract domestic and international business travelers. Industry conferences, technical training, and supply chain activities further strengthen occupancy. Hotels near industrial zones benefit from consistent corporate bookings across economic cycles. This stable demand encourages continued investment in regional hospitality infrastructure[2]German Hotel Association (DEHOGA), "Market Overview: Hotel Demand in German Industrial Centers," Annual Market Report 2024, dehoga.de.

Trade Fair Infrastructure Supporting Event-Based Accommodation Peaks

Germany's global trade fair network generates recurring demand peaks in major exhibition cities, driving hotel demand. Events such as Hannover Messe and Messe Frankfurt attract large international business audiences. Hotels benefit from bookings, premium pricing, and high occupancy during exhibition periods[3]German Convention Bureau (GCB), "Exhibition Visitor Statistics and Peak Demand Patterns," Tourism Data Report 2024, gcb.de. Long-term agreements with exhibitors and organizers provide predictable revenue streams. Trade fairs remain a key driver of business hospitality demand.

Rail Connectivity Supporting Domestic Leisure Mobility

Germany's extensive rail network enhances domestic tourism by improving access to regional leisure destinations. High-speed rail connects major cities with wellness resorts, cultural attractions, and nature destinations. Convenient travel encourages weekend getaways and multi-night stays at regional hotels. Sustainable travel preferences further support the growth of rail-based tourism. Strong connectivity benefits both urban and rural hospitality markets[4]Serviced Apartment Association (SAA), "Extended-Stay Rental Market Analysis and Corporate Demand," Industry Report 2024, serviceapartmentassociation.com.

Aparthotel Growth Driven by Extended Business Assignments

Growing demand for extended business assignments is accelerating the expansion of Germany's aparthotel segment. Corporate travelers increasingly prefer accommodations offering residential amenities and flexible stay options. Multinational companies use aparthotels for relocations, project assignments, and long-term training programs. Developers continue expanding aparthotel supply across major business cities. The segment provides attractive long-term revenue opportunities for hospitality operators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Weakening Industrial Activity Affecting Corporate Travel Demand | −0.8% | Automotive and industrial business hubs | Short term (≤ 2 years) |

| High Regulatory and Compliance Requirements Increasing Operating Complexity | −0.6% | Berlin, Hamburg, Munich compliance burden | Medium term (2–4 years) |

| Rising Construction and Financing Costs Limiting New Hotel Supply Growth | −0.7% | Munich, Frankfurt, Berlin development constraints | Medium term (2–4 years) |

| Economic Uncertainty Affecting Corporate Travel and Business Hotel Performance | −0.7% | Major business travel destination risks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Weakening Industrial Activity Affecting Corporate Travel Demand

Slower industrial activity is reducing corporate travel demand across Germany's key manufacturing regions. Lower business investment and supply chain disruptions have weakened hotel occupancy in business destinations. Companies are tightening travel budgets and increasing the use of virtual meetings. Reduced supplier visits and corporate events further pressure hotel revenues. This volatility in demand impacts business-focused hospitality performance.

High Regulatory and Compliance Requirements Increasing Operating Complexity

Germany's strict regulatory environment increases compliance costs and operational complexity for hospitality operators. Labor laws, environmental standards, GDPR, and safety regulations require continuous investment. Older hotels face additional renovation costs to meet evolving compliance requirements. Administrative obligations also increase management workload and operating expenses. These factors reduce profitability and create barriers for smaller operators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Independent Dominance, Chain Momentum

Independent hotels accounted for 59.04% of Germany hospitality market share in 2025, epitomizing the country’s tradition of family ownership and regional flavour. Local operators leverage intimate knowledge of demand cycles, cultural events, and supplier networks to curate unique experiences that resonate with domestic travellers. Yet franchise adoption is rising legacy independents are increasingly partner with international brands on soft-brand conversions, accessing loyalty databases that unlock international demand while retaining design autonomy. Chain hotels, forecast at a 7.41% CAGR, benefit from multi-property economies of scale in procurement and technology. From 2026 to 2031, the German hospitality market is projected to experience notable growth in the chain-affiliated segment. This expansion is expected to reduce, though not eliminate, the market dominance held by independent establishments. The increasing presence of chain-affiliated inventory reflects a shift in market dynamics, driven by evolving consumer preferences and strategic investments by major players in the industry.

The chain surge is anchored in asset-light agreements that appease local owners wary of relinquishing control. IHG’s NOVUM deal alone will spread Holiday Inn Express and Hotel Indigo flags across secondary cities that historically lacked branded supply. Such penetration deepens competitive pressure on independents, especially in segments where brand standards, loyalty perks, and 24-hour digital assistance sway booking decisions. Independent groups respond by doubling down on hyper-local F&B concepts, art collaborations, and sustainability certifications that differentiate on authenticity rather than scale.

By Accommodation Class: Mid-Market Core, Serviced Apartment Upswing

Mid and upper-mid-scale hotels captured 47.22% of 2025 sales as German travellers favour reliable comfort without luxury premiums. These properties often occupy transport-linked plots, support corporate negotiated rates, and showcase efficient staff-to-room ratios. Their insulation from luxury’s cyclical whim and economy’s cost sensitivity secures steady occupancy across economic cycles. Serviced apartments, projected to grow at a CAGR of 8.12%, are anticipated to significantly enhance their contribution to the German hospitality market by 2031. Operators exploit minimal public-area footprints and extended-stay economics that smooth weekly RevPAR volatility.

Luxury remains vibrant, bolstered by international HNWI inflows and iconic castles-to-palace conversions. Kempinski’s EUR 25,000-per-night Nymphenburg Palace Royal Residence exemplifies price elasticity at the top. Budget and economy chains counter inflation pressures via standardized furnishings, self-check-in kiosks, and centralized laundry models. Motel One’s EUR 852 million (USD 887.41 million) turnover underscores the effectiveness of scalable design-forward economy positioning in capturing cost-conscious yet experience-seeking guests.

By Booking Channel: Digital Mix Optimization

OTAs retained 31.74% revenue share in 2025, but direct digital bookings will expand the fastest at a 9.86% CAGR as hotel marketers exploit CRM, retargeted ads, and anime-style chatbots to personalize user journeys. The size of the German hospitality market facilitated through proprietary booking engines has already surpassed expectations and is anticipated to grow further. This growth is attributed to the implementation of parity-free pricing strategies, which are driving a consistent shift toward direct booking behaviour among consumers. Loyalty platforms push exclusive member rates, while embedded fintech solutions facilitate post-stay upsells ranging from carbon-neutral offsets to late-checkout bundles.

Corporate and MICE channels are stabilizing amid trade-fair normalization, reinforcing weekday occupancy levels in Frankfurt and Munich. Wholesale and traditional agents shrink but gain relevance in niche group tours and cruise pre-/post-packages. Successful operators deploy channel-cost dashboards that visualize distribution profitability in real time, allowing revenue managers to allocate inventory dynamically, minimize OTA excess, and fortify customer data reservoirs.

Geography Analysis

South Germany delivered 30.07% of 2025 hospitality revenue, anchored by Bavaria’s Alpine resorts, Munich’s business corridors, and Stuttgart’s automotive backbone. Prominent events, such as Oktoberfest, significantly elevate ADRs beyond the typical annual benchmarks. Simultaneously, the presence of manufacturing clusters ensures a stable baseline for weekday occupancy, contributing to consistent demand within the hospitality market. Development controls around heritage centres restrict supply, enabling rate escalation even amid moderate volume growth.

East Germany’s 6.18% CAGR trajectory owes to transport upgrades, cultural renaissance, and competitive land pricing. Berlin, Leipzig, and Dresden advance lifestyle inventory pipelines that attract digital nomads and creative industries, adding depth to leisure-heavy seasonal demand. As capital reroutes toward these emerging hubs, the German hospitality market share of East Germany may climb two percentage points by 2031. North, West, and Central corridors balance maritime, industrial, and hub-and-spoke business travel, ensuring that aggregate national performance remains diversified across economic cycles and event calendars.

Competitive Landscape

The leading companies held modest share in 2024, highlighting a highly fragmented market. HR Group’s purchase of H-Hotels and PAI Partners’ majority stake in Motel One typify private-equity-backed platform plays that deliver purchasing leverage and shared-services savings. Global franchises pursue capital-light growth, offering German owners’ asset-management expertise and tech stacks unattainable at independent scale. This marriage of local real-estate know-how and global distribution muscle underpins chain hotels’ 7.77% CAGR.

Independents, although vulnerable to wage inflation and OTA dependency, retain competitive edges in localized storytelling, culinary authenticity, and quick decision cycles disconnected from corporate hierarchies. Some deploy soft-brand affiliations or cluster-level purchasing co-ops to defend profitability. Digital transformation is the new battleground: AI-powered revenue management systems enable businesses to forecast demand with granular accuracy at the postcode level. Automated bots efficiently manage guest inquiries, streamlining customer interactions, while IoT devices optimize energy consumption, leading to significant reductions in energy waste. Operators able to integrate tech with human-centric service will capture outsized share in the evolving Germany hospitality market.

Sustainability credentials increasingly influence corporate RFPs and meeting venue selection, making CSRD compliance and third-party eco-certifications table stakes. Early movers secure green-loan pricing advantages and preferential inclusion in multinational travel programs. Market participants that lag risk reputational penalties, restricted funding access, and exclusion from government-related events, underscoring ESG as a non-negotiable pillar of competitive strategy.

Germany Hospitality Industry Leaders

-

Accor SA

-

Marriott International

-

Hilton Worldwide

-

IHG Hotels & Resorts

-

Deutsche Hospitality (Steigenberger)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Four Points Flex by Sheraton opened its second German site in Koblenz after a EUR 10 million (USD 11 million) revamp.

- March 2025: IHG signed the 303-room Bristol Berlin, Vignette Collection, marking the brand’s German entry.

- March 2025: PAI Partners acquired an 80% stake in Motel One to accelerate global expansion of The Cloud One lifestyle banner.

- February 2025: HR Group finalized the acquisition of H-Hotels, adding 60+ properties to reinforce its European leadership.

Germany Hospitality Market Report Scope

The report covers a complete background analysis of the hospitality industry in Germany, including an assessment of the industry associations, overall economy, emerging market trends (by segment), significant changes in the market dynamics, and market overview.

By Type

| Chain Hotels |

| Independent Hotels |

By Accommodation Class

| Luxury |

| Mid & Upper-Mid-scale |

| Budget & Economy |

| Service Apartments |

By Booking Channel

| Direct Digital |

| OTAs |

| Corporate / MICE |

| Wholesale & Traditional Agents |

By Geographic Region

| North Germany |

| South Germany |

| West Germany |

| East Germany |

| Central Germany |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Accommodation Class | Luxury |

| Mid & Upper-Mid-scale | |

| Budget & Economy | |

| Service Apartments | |

| By Booking Channel | Direct Digital |

| OTAs | |

| Corporate / MICE | |

| Wholesale & Traditional Agents | |

| By Geographic Region | North Germany |

| South Germany | |

| West Germany | |

| East Germany | |

| Central Germany |

Key Questions Answered in the Report

What is the expected growth rate for the sector?

The market is projected to expand at a 4.05% CAGR between 2026 and 2031.

Which segment is expanding the fastest?

Serviced apartments, supported by bleisure demand, are advancing at an 8.12% CAGR.

Why are direct bookings gaining importance?

Direct distribution channels demonstrate a cost advantage in customer acquisition compared to online travel agencies (OTAs). This cost efficiency not only enhances profit margins but also provides businesses with greater control over customer data, enabling more strategic decision-making and personalized customer engagement.

What staffing challenges do hoteliers face?

In 2023, the labor market experienced a significant shortage of skilled professionals, which exerted upward pressure on wages. This trend prompted businesses to accelerate their investments in automation technologies as a strategic response to mitigate labour constraints and maintain operational efficiency.

How does CSRD affect hotel investment plans?

About 15,000 companies must publish standardized sustainability reports, triggering capital outlays for green certifications that now influence corporate travel procurement.

Page last updated on: