Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

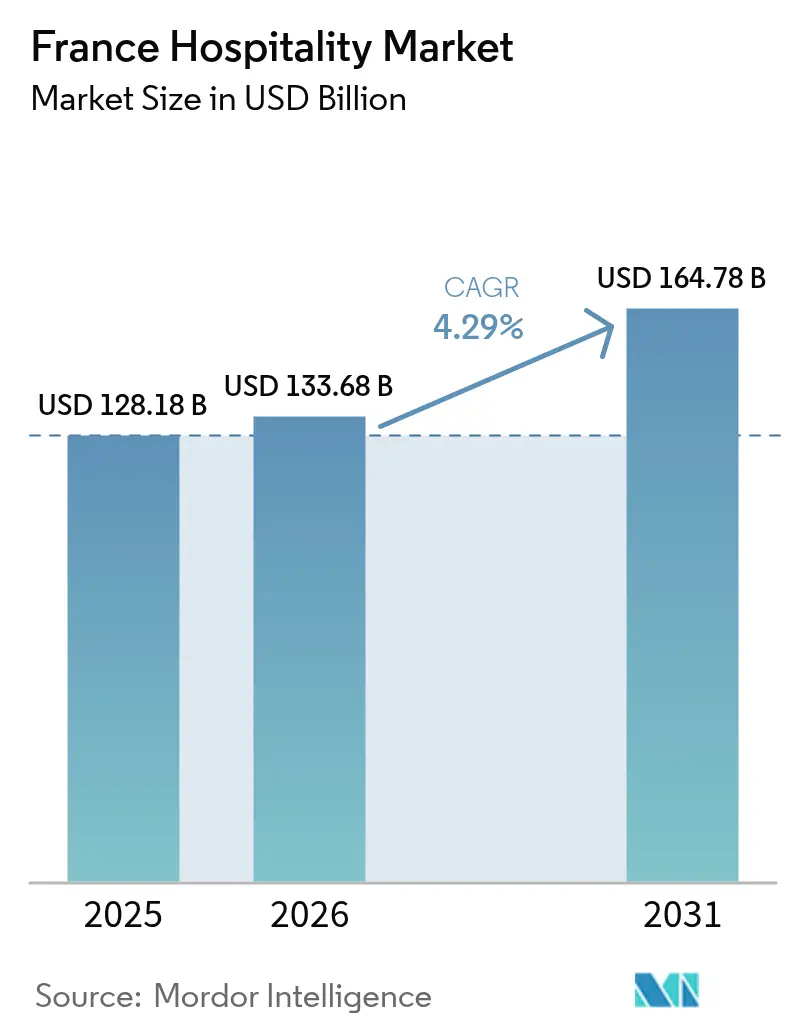

| Base Year Market Size (2025) | USD 128.18 Billion |

| Market Size (2026) | USD 133.68 Billion |

| Market Size (2031) | USD 164.78 Billion |

| Growth Rate (2026 - 2031) | 4.29% CAGR |

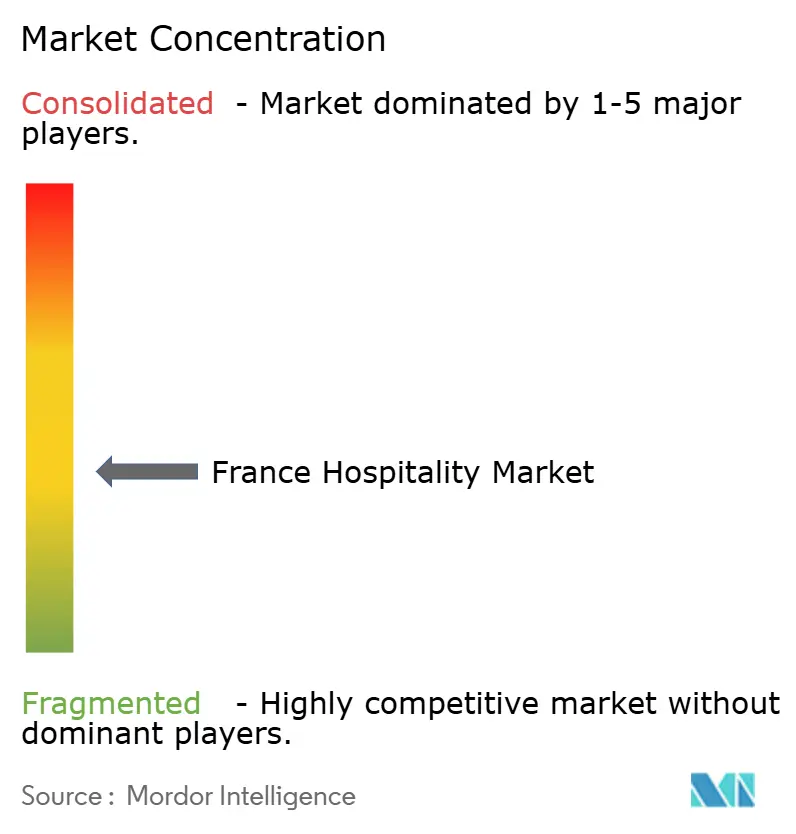

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

France Hospitality Market Analysis by Mordor Intelligence

The France Hospitality market size is expected to grow from USD 128.18 billion in 2025 to USD 133.68 billion in 2026 and is forecast to reach USD 164.78 billion by 2031 at 4.29% CAGR over 2026-2031.

Robust domestic demand, strong international arrivals, and purposeful government investments such as the EUR 1.9 billion (USD 2.071 billion) Destination France program are collectively reinforcing revenue visibility and underpinning this expansion path[1]Atout France, “Plan Destination France,” ATOUT-FRANCE.FR.. Competitive intensity is moderate because the five largest operators hold roughly 47% of national room capacity, leaving ample room for niche concepts and regional independents to flourish. Structural drivers include Olympic-legacy infrastructure upgrades, favorable work-from-anywhere policies that blur leisure and business trips, and tax incentives aimed at accelerating energy-efficient retrofits in aging hotel stock. At the same time, operators must navigate upward wage adjustments tied to union agreements and stricter municipal limits on short-term rentals that may restrict flexible accommodation models while cushioning traditional hotels from peer-to-peer competition. Taken together, the France hospitality market continues to demonstrate resilience and adaptability as it aligns with sustainability imperatives and evolving traveler expectations.

Key Report Takeaways

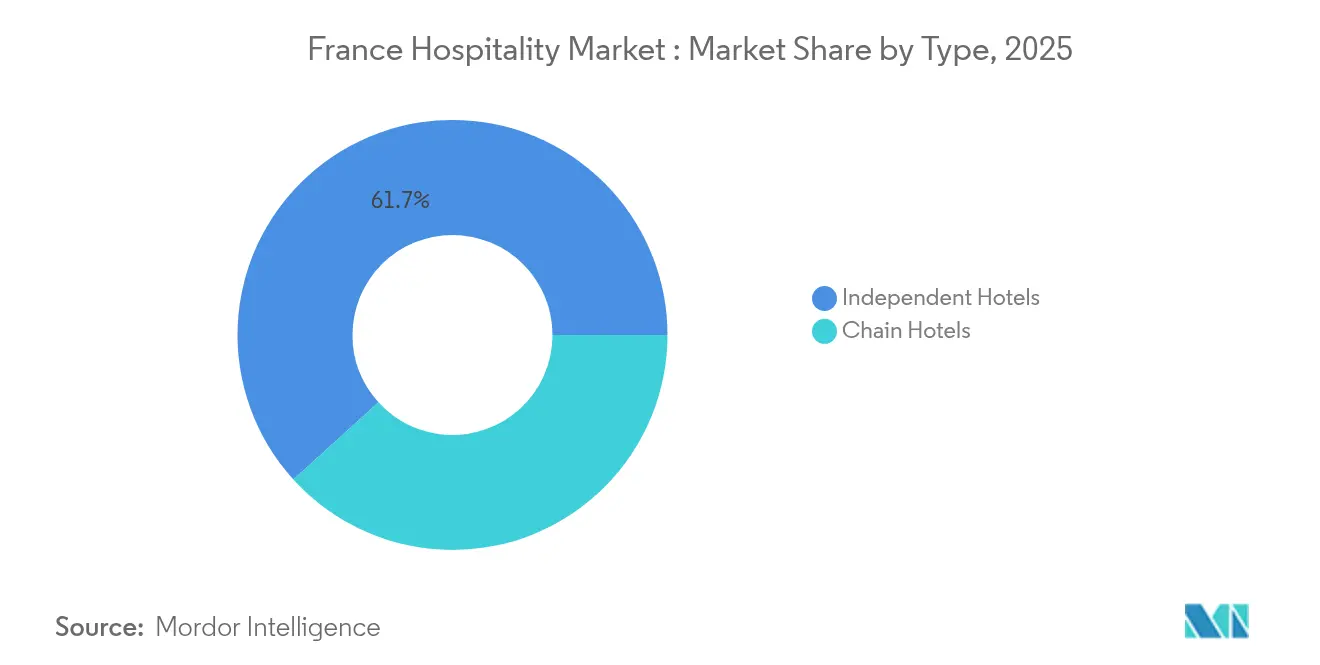

- By type, independent hotels led with 61.74% of the France hospitality market share in 2025, while chain hotels recorded the fastest 5.12% CAGR outlook to 2031.

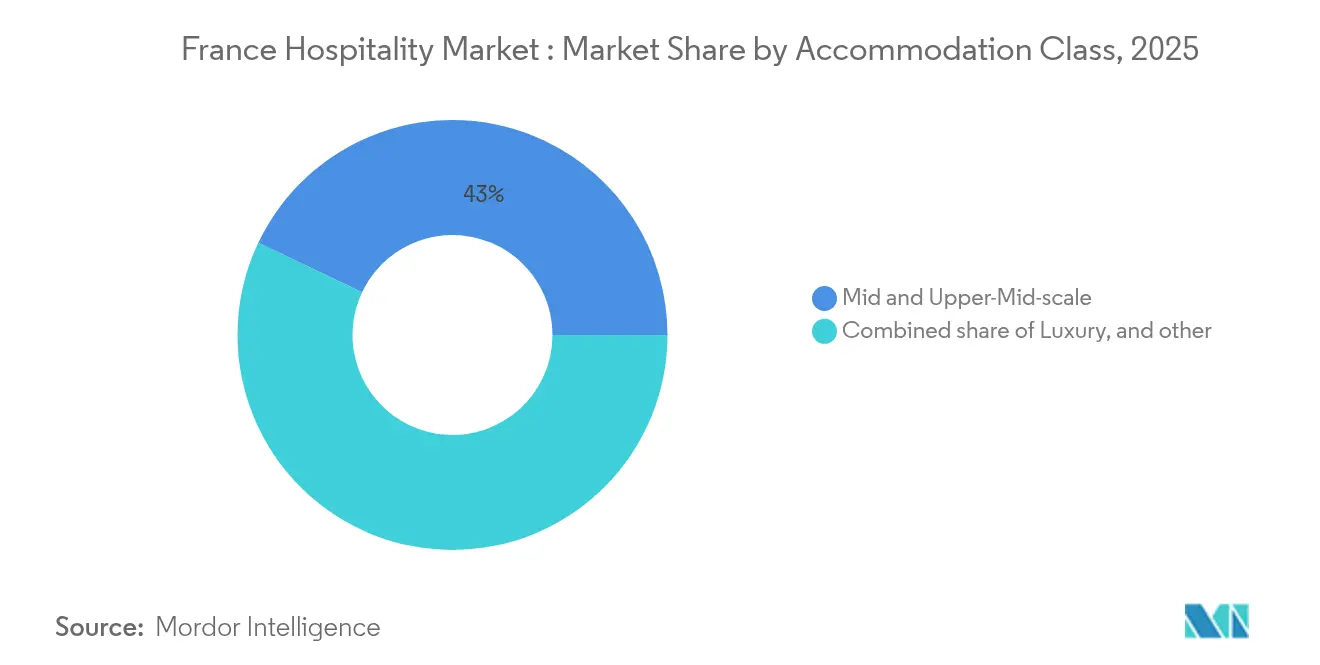

- By accommodation class, mid & upper-mid-scale properties accounted for 42.95% of the France hospitality market size in 2025, as service apartments advanced at a 6.00% CAGR through 2031.

- By booking channel, OTAs commanded 41.05% of the France hospitality market size in 2025, whereas direct digital bookings are poised for a 7.00% CAGR through 2031.

- By geography, Île-de-France held 33.05% of the France hospitality market share in 2025, and Provence-Alpes-Côte d’Azur is on track for a 5.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Paris Global Tourism Magnet Supporting Premium Urban Hospitality | 1.20% | Paris luxury and business districts | Short term (≤ 2 years) |

| Fashion and Luxury Ecosystem Enhancing Visitor Spending | 0.90% | Paris haute couture and fashion hubs | Short term (≤ 2 years) |

| Wine Region Tourism Creating Specialized Accommodation Demand | 0.70% | Bordeaux, Burgundy, Champagne wine regions | Medium term (2–4 years) |

| Heritage Property Conversion Supporting Boutique Hotel Growth | 0.60% | Loire, Provence, Normandy château regions | Long term (≥ 4 years) |

| International Event Calendar Supporting Visitor Inflows | 0.80% | Paris and Cannes event destinations | Short term (≤ 2 years) |

| Second-Home and Regional Leisure Culture Supporting Rural Hospitality | 0.50% | Provence, Brittany, Alpine leisure regions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Paris Global Tourism Magnet Supporting Premium Urban Hospitality

Paris remains France's primary hospitality demand engine, supported by record international tourism and strong premium hotel performance. High occupancy and ADR are continuing to drive RevPAR growth across luxury hotels. The reopening of Notre-Dame and the legacy of the 2024 Olympic Games further boosted visitor demand. Continuous infrastructure upgrades and strong air connectivity reinforce the city's global appeal. High-value hotel transactions reflect sustained investor confidence in Paris[2]Atout France, "Tourism Results 2025: France Surpasses 100 Million International Visitors," Atout France, atout-france.fr.

Fashion and Luxury Ecosystem Enhancing Visitor Spending

France's global leadership in luxury fashion and retail attracts high-spending international travelers year-round. Paris Fashion Weeks and luxury shopping districts generate recurring demand for premium hotels. Luxury properties continue to record strong ADR and RevPAR, supported by affluent visitors. Ongoing investment in luxury hotels strengthens France's upscale accommodation portfolio. The luxury ecosystem continues driving premium hospitality revenues.

Wine Region Tourism Creating Specialized Accommodation Demand

France's renowned wine regions generate year-round demand for hospitality through vineyard tourism and luxury culinary experiences. Boutique wine hotels combine heritage properties with Michelin dining and wellness offerings. Investments in Bordeaux, Burgundy, Champagne, and Provence continue to expand the supply of premium accommodation. Wine tourism experiences encourage longer visitor stays and higher guest spending. This segment supports regional hospitality growth beyond major cities[3]French Ministry of Economy, Finance and Industrial and Digital Sovereignty, "Wine Tourism: A Major Asset for the Attractiveness of French Regions," Direction Générale des Entreprises (DGE), entreprises.gouv.fr.

Heritage Property Conversion Supporting Boutique Hotel Growth

France's extensive historic building stock provides strong opportunities for boutique hotel development through adaptive reuse. Heritage conversions preserve cultural assets while expanding premium accommodation capacity. Government restoration incentives improve the viability of redevelopment projects. Most upscale hotel additions increasingly focus on renovation rather than new construction. Heritage hotels continue attracting experience-focused domestic and international travelers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mature Hospitality Market Limits Organic Supply Expansion in Prime Destinations | −0.7% | Paris, Riviera, Alpine supply constraints | Long term (≥ 4 years) |

| High Dependence on Paris Creating Geographic Demand Imbalance | −0.6% | Île-de-France revenue concentration | Medium term (2–4 years) |

| Regional Tourism Imbalance Creates Uneven Hospitality Performance | −0.5% | Coastal versus interior regional disparity | Long term (≥ 4 years) |

| Sustainability Regulations and Heritage Protection Increase Development Complexity | −0.6% | UNESCO heritage conservation zones | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Mature Hospitality Market Limits Organic Supply Expansion in Prime Destinations

France's mature hospitality market limits new hotel development in major destinations such as Paris. Growth increasingly depends on hotel renovations, repositioning, and rate optimization rather than new supply. High land values and limited development sites constrain expansion. Rising labor and operating costs further pressure hotel profitability. These factors reduce the pace of market capacity growth[4]Direction Générale des Entreprises, "Tourism in France: Key Figures," French Ministry of the Economy, entreprises.gouv.fr.

High Dependence on Paris Creating Geographic Demand Imbalance

Hospitality performance remains heavily concentrated in Paris, creating uneven growth across regional markets. The capital attracts the majority of international visitors, hotel investment, and demand for premium accommodation. Many secondary destinations continue recording lower occupancy despite strong tourism assets. Regional infrastructure and international marketing remain comparatively underdeveloped. Geographic concentration limits balanced national hospitality growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Independent hotels preserve cultural appeal while chains scale technology

Independent hotels held a commanding 61.74% of the France hospitality market share in 2025, anchored in the nation’s deep heritage of family-owned auberges and boutique establishments that deliver place-based authenticity. These properties capitalize on culinary storytelling, architectural character, and personalized service that resonate with travelers seeking immersive local experiences. Chains, however, are growing faster at a 5.12% CAGR because standardized operating playbooks, brand recognition, and loyalty ecosystems reassure risk-averse international guests and corporate travel buyers. Strategic mergers, such as Accor’s full acquisition of Paris Society, illustrate how large groups blend operational scale with experiential depth to compete on both efficiency and uniqueness. Independents respond by adopting cloud-based PMS solutions and consortium affiliations that unlock marketing reach without surrendering brand individuality. The interplay between authenticity and consistency is expected to define competitive positioning through 2031 as both segments pursue operational excellence while safeguarding guest intimacy.

The France hospitality market size for chain hotels is projected to expand as multinationals deploy premium-economy concepts like Spark by Hilton, which target value-conscious travelers who still demand modern design and digital convenience. Franchise and management contracts offer asset-light growth avenues that entice domestic owners seeking professional branding amid tightening regulatory oversight. Independent players counter by curating hyper-local partnerships and experiential add-ons such as chef residencies, artisan workshops, and heritage tours that chains often struggle to replicate at scale. Investors increasingly weigh asset-quality metrics alongside ESG credentials, rewarding operators that integrate energy-efficiency upgrades and equitable labor policies into value-creation plans. Consequently, a measured consolidation wave may emerge, especially among mid-market independents facing cap-ex obligations, thereby gradually increasing concentration without extinguishing France’s celebrated independent lodging tradition.

By Accommodation Class: Mid-scale steadiness meets service-apartment momentum

Mid & upper-mid-scale hotels captured 42.95% of the France hospitality market size in 2025, benefitting from steady demand by cost-conscious international visitors and domestic business travelers who prize reliability and balanced amenities. This segment’s ubiquity along transport corridors and in secondary cities safeguards occupancy rates and moderates ADR volatility. Service apartments, meanwhile, secure the fastest 6.00% CAGR because remote workers, relocating executives, and multi-generation families value apartment-style layouts, kitchenettes, and flexible stay lengths. Brands like Adagio, aiming for 200 sites by 2028, illustrate the category’s institutional traction and capacity to scale within urban footprints. Mid-scale operators defend share by upgrading F&B concepts, integrating coworking zones, and rolling out mobile guest apps that mirror apartment conveniences.

Luxury inventory enjoys favorable RevPAR uplift tied to international high-net-worth arrivals, yet it remains vulnerable to geopolitical demand shocks and elevated renovation costs required to meet evolving wellness and sustainability benchmarks. Budget properties confront margin pressure from wage inflation and energy-compliance mandates but leverage standardized modular designs and limited-service models to retain cost competitiveness. Service-apartment operators exploit regulatory clarity by aligning classification status with hotel norms, thereby side-stepping zoning caps while riding extended-stay demand. As traveler segmentation blurs, expect hybrid formats that combine mid-scale price points with service-apartment flexibility, reinforcing the France hospitality market’s ability to satisfy diverse stay purposes without cannibalizing core offerings.

By Booking Channel: OTAs dominate but direct digital channels accelerate

OTAs accounted for 41.05% of the France hospitality market size in 2025, leveraging sophisticated comparison tools, global brand awareness, and multilingual interfaces that simplify booking journeys for international audiences. Their bargaining power stems from high traffic volume, performance-marketing expertise, and ancillary upsell capabilities such as insurance and activities. Nonetheless, direct digital bookings advance at a robust 7.00% CAGR as hotels deploy AI-driven personalization engines, loyalty-linked discounts, and best-rate guarantees that narrow perceived value gaps. Chains capitalize on unified CRM platforms to cross-sell among brands, while independents exploit channel-management tools to optimize rate parity and reduce commission leakages.

Corporate/MICE platforms and GDS channels sustain relevance for negotiated rate programs and group allotments, especially in urban conference hubs like Paris and Lyon. Wholesale and traditional agents cater to long-haul markets and niche luxury itineraries, adding diversification to the distribution mix. The France hospitality market share held by OTAs may erode modestly as hoteliers master funnel conversion tactics, yet their marketing clout and mobile app stickiness ensure an indispensable role in demand aggregation. Over time, a symbiotic coexistence is likely, with OTAs driving incremental volume and hotels focusing on guest-lifetime value amplification through direct engagement.

Geography Analysis

In France's hospitality market, Île-de-France is the largest regional sub-segment in 2025, accounting for 33.05% of the market. Between 2026 and 2031, Provence-Alpes-Côte d’Azur is projected to be the fastest-growing sub-segment, with a CAGR of 5.52%. Île-de-France continues to anchor national hospitality revenues as enhanced intermodal hubs and improved signage systems translate Olympic investments into enduring visitor convenience. Hoteliers report occupancy rates that edge above 85% during peak cultural events, sustaining pricing power even amid fresh supply introductions. Travel corridors to provincial attractions shorten via high-speed rail expansions, encouraging tourist dispersal and multi-city itineraries that feed adjacent regional economies. Luxury and lifestyle openings, such as the forthcoming Maybourne Saint-Germain, cater to discerning clientele who seek Parisian grandeur blended with contemporary artistry. Simultaneously, mid-scale operators launch creative F&B concepts that resonate with digital nomads, ensuring product diversity across price bands. Local authorities collaborate with hoteliers to embed sustainability benchmarks into building codes, aligning economic development with environmental stewardship.

Provence-Alpes-Côte d’Azur enjoys top-line uplift as Mediterranean vistas combine with high-spend wellness seekers and burgeoning remote-work audiences. The Nice Airport rail-station overhaul boosts annual capacity to 23 million passengers by 2030, reducing transfer friction and stimulating year-round arrivals. Hoteliers in Marseille, Antibes, and Cannes renovate stock to integrate rooftop solar arrays, water-saving fixtures, and low-carbon menus, aligning with regional climate objectives. Luxury operators add private-residence components that diversify revenue streams and extend customer life cycles. Destination marketing campaigns emphasize cultural festivals, wine routes, and marine biodiversity excursions, broadening seasonal appeal. Public-private funding vehicles like Fonds Tourisme Côte d’Azur co-finance upgrades in heritage properties, preserving architectural integrity while modernizing guest amenities.

Auvergne-Rhône-Alpes, Nouvelle-Aquitaine, and other regions record consistent yet moderate growth as government stimulus targets rural rejuvenation and mountain diversification. The Avenir Montagnes program channels EUR 300 million (USD 327 million) into eco-lodges and multi-activity resorts that pivot from snow-dependent models toward four-season adventure tourism. Local entrepreneurs convert châteaux into experiential retreats featuring farm-to-table dining and wellness workshops, attracting urbanites looking to disconnect in authentic settings. Transport initiatives improve last-mile connectivity, shrinking travel times and boosting weekend visitation. Regional tourism boards leverage digital storytelling to highlight under-the-radar villages and UNESCO sites, further dispersing traveler flows and supporting artisanal supply chains. Collectively, these efforts enlarge the addressable France hospitality market size beyond traditional urban cores.

Regulatory Landscape

Hospitality regulation in France is anchored in the Code du tourisme and administered nationally through the Direction generale des Entreprises (DGE) under the Ministry of the Economy, with Atout France operating the accommodation classification system and associated quality frameworks. In January 2026, Decree No. 2026-14 updated procedures for the classification, renewal, and extension of tourist accommodation ratings, reinforcing the use of standardized, homologated criteria for establishments seeking official classification and visibility in formal tourism channels.

On the fiscal side, the taxe de sejour remains a key local levy, set by municipal councils or inter-municipal bodies (EPCI) and tied to an annual calendar in which rates must be decided before July 1 to apply from January 1 of the following year; for 2026, the tourist tax rate schedules were revalued by 1.8%. Together with tightening municipal oversight of short-term rentals in major cities and ongoing state emphasis on sustainable and inclusive tourism labels promoted via DGE and Atout France, these rules raise compliance and reporting intensity while continuing to support regulated accommodation supply and clearer quality positioning.

Value Chain Analysis

The France hospitality value chain starts with project development and asset ownership (family groups, family offices, hotel companies, and real-estate investors), followed by financing via banks and private debt/equity funds, then design, construction, and renovation led by contractors and specialist suppliers (HVAC, energy systems, furniture and fit-out, and digital infrastructure). Operations are run by hotel owners and operator-exploiters under owned, leased, franchise, or management models, supported by tech vendors (PMS, channel managers, revenue management, and payments), staffing intermediaries, and professional federations that structure training and labor practices. Demand is distributed through direct digital channels and OTAs, plus corporate/MICE intermediaries, with destination bodies and public agencies shaping demand through promotion and program funding.

Bottlenecks are concentrated in labor availability and capital deployment. Recruiting and retaining staff is constrained by housing affordability in tourist zones and the seasonality of roles, increasing reliance on training mechanisms and employer support programs coordinated via OPCOs. Governance also runs through national policy coordination bodies such as the Comite Interministeriel du Tourisme (CIT). On the capital side, higher interest rates and rising compliance and renovation costs have increased selectivity in deal flow, with tourism investment activity falling to EUR 18.7 billion in 2024 from an annual average of EUR 21 billion over 2022-2024. Ownership dynamics remain a structural feature of the chain, with private family capital representing about 70% of hotel transactions in 2024, supporting long-horizon refurbishment and repositioning strategies despite tighter funding.

Competitive Landscape

Competition in the France hospitality market is best described as moderately fragmented. The five largest operators hold a significant portion of the market, yet a dynamic independent segment continues to thrive, preserving the unique character of French hospitality. Accor stands out as the market leader, leveraging a broad multi-brand portfolio that ranges from luxury landmarks to budget-friendly options. Its ALL loyalty program strengthens its position by encouraging customer retention and driving demand across various market segments. Louvre Hotels and B&B Hotels follow with nationwide footprints, each leveraging franchise expansion to accelerate asset-light growth. International chains like Hilton and Choice Hotels deepen exposure via long-term strategic agreements, adding both premium-economy and mid-scale properties to capitalize on demand niches. Simultaneously, service-apartment specialists such as Adagio and Citadines scale quickly, responding to extended-stay momentum.

Strategic moves illustrate an industry focused on portfolio optimization and ESG alignment. Henderson Park’s purchase of five Novotel Suites demonstrates investor appetite for mid-market refurbishments that meet carbon-reduction standards and uplift RevPAR through design refreshes. Accor’s data-sharing alliance with Pernod Ricard and JCDecaux signals a pivot toward sophisticated analytics that inform hyper-personalized offers while respecting privacy regulations. Technology vendors like Mews gain traction as hotels automate back-office workflows and boost self-service adoption, freeing labor for high-touch guest interactions. Market entrants deploy asset-light models and soft-brand collections to harness independent charm without forsaking global distribution, thereby intensifying competitive benchmarking on both experience and efficiency.

Outlook discussions center on potential consolidation among mid-scale independents that confront sizable cap-ex tied to energy mandates and digital upgrades. Private-equity funds evaluate roll-up opportunities that unlock operating synergies through centralized procurement, standard operating procedures, and advanced revenue-management systems. Simultaneously, ultra-luxury projects like Maybourne Saint-Germain underscore persistent investor confidence in France’s capacity to absorb top-tier ADRs, particularly when paired with branded residences that monetize residential demand for hotel-serviced living. Consequently, the France hospitality market is poised for dynamic realignment that balances local authenticity with global professionalism.

France Hospitality Industry Leaders

-

Louvre Hotels Group

-

B&B Hotels

-

Marriott International

-

IHG Hotels & Resorts

-

Accor

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key whitespace in France is professionally managed extended-stay and aparthotel supply that can capture remote-work, relocation, and multi-generational travel demand while staying compatible with regulated accommodation frameworks. Market actions point to the continued institutionalization of this format: in May 2026, Eurazeo took a majority stake in Babylon, an integrated aparthotel platform in Paris and Greater Paris, highlighting investor appetite for scalable operating platforms rather than single-asset exposure. This creates room for owners and operators to pursue conversions, including underperforming hotels and other assets, into service-apartment style inventory with standardized operations, stronger direct-digital distribution, and clearer compliance pathways.

Premium and mixed-use hospitality linked to branded residences is another expansion lane, particularly in high-demand leisure corridors beyond Paris where longer-stay owner-occupier demand can support luxury positioning. In July 2026, Marriott International signed an agreement to bring The Luxury Collection to Southern France with the brands first residences in the country, reinforcing how residences can diversify revenue streams and extend customer lifetime value. Alongside these private moves, state-backed transformation programs such as Destination France, targeting EUR 20 billion in sector investment by 2030, and the national roadmap aiming for EUR 100 billion in international tourism receipts by 2030 keep modernization and product-quality upgrades central, creating practical openings for operators that combine energy-focused refurbishment, digital distribution improvements, and differentiated experiences in secondary cities and regional destinations.

Recent Industry Developments

- June 2026: Louvre Hotels Group opened a TULIP Hotels & Residences property in Valence, marking one of the brands early steps in its home market. The opening strengthens midscale, residence-style positioning and adds competitive pressure on extended-stay and hybrid formats outside Paris.

- December 2025: Accor outlined a pipeline of new destinations, hotels, resorts, and hospitality offerings for the 2026 calendar year. Framing the network plan around new openings supports forward contracting with owners and suppliers and signals continued brand and format diversification across France and nearby feeder markets.

- June 2025: Accor reported opening around 20 establishments in France in the first half of 2025, adding more than 1,700 rooms across economic, mid-range, and luxury brands. The expansion underscores an asset-light growth engine that raises competitive benchmarking for independents and regional chains on distribution, loyalty, and renovation cadence.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the France hospitality market is defined as revenue generated from paid stays and related guest services in commercial accommodation across France, counted at the point of service delivery and captured in current US dollars.

Scope exclusions: We exclude private, non-commercial stays and informal rentals that are not consistently reported through official or audited channels.

Segmentation Overview

-

By Type

- Chain Hotels

- Independent Hotels

-

By Accommodation Class

- Luxury

- Mid & Upper-Mid-scale

- Budget & Economy

- Service Apartments

-

By Booking Channel

- Direct Digital

- OTAs

- Corporate / MICE

- Wholesale & Traditional Agents

-

By Geographic Region

- Île-de-France

- Provence-Alpes-Côte d’Azur

- Auvergne-Rhône-Alpes

- Nouvelle-Aquitaine

- Rest of France

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building the demand and supply backdrop for France, so the model does not depend on one single dataset. We reference public sources such as INSEE tourism and services statistics, Banque de France macro series, Eurostat tourism indicators, UNWTO arrival trends, and Ministry of Economy and Finance releases that touch tourism spending and business conditions.

To connect these signals to market revenue, we also review company annual reports and investor presentations from listed operators, plus trade association publications and reputable press coverage on occupancy, ADR shifts, and pipeline additions. In a few places, paid subscriptions are used for company financials and intelligence, and for cross-checking corporate actions and major property openings that can shift supply. This list is illustrative only, and many other sources were used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary inputs come from structured conversations and surveys with accommodation operators, distribution and booking channel specialists, property-level managers, and advisors who track tourism flows across key French regions. We use these discussions to confirm pricing progression, mix changes between chain and independent supply, and practical booking-channel splits, and then we re-check any outlier assumptions until a consistent story is reached.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 17% | |

| Mid tier: 53% | Functional/Unit leaders: 24% | |

| Smaller Players: 18% | Managers: 59% |

Market-Sizing & Forecasting

Sizing uses a top-down build that reconstructs national accommodation revenue by tying travel volume and stay behavior to monetization, and then narrowing it to the defined hospitality boundary. Inputs that help anchor the model include inbound and domestic trip volumes, room supply and openings, occupancy and length of stay patterns, average daily rate direction by class, and booking-channel mix (direct digital, OTAs, corporate and MICE, and wholesale).

After the top-down total is formed, selective bottom-up checks are used to test reasonableness, such as sampled property revenue math (occupied room nights multiplied by observed ADR bands) and operator-level rollups where disclosures are clear. If parts of the market are not directly observable, we fill gaps with conservative proxy ratios that are validated through expert feedback, and we adjust only when multiple signals point in the same direction.

Forecasts are produced using multivariate regression, where the main drivers are macro demand indicators and lodging operating metrics, and then tuned using scenario analysis for shocks like travel disruptions or abrupt pricing resets. Assumptions for ADR growth and utilization are reviewed with interviewees so the outlook stays practical, not purely statistical.

Data Validation & Update Cycle

Outputs are checked against independent signals, including tourism arrival trends, accommodation performance indicators, and major supply additions that should show up as capacity changes over time. Variance checks are run across years and across regions, and any step-change is reviewed by another analyst before sign-off.

The model is refreshed annually, and interim updates are triggered when material events occur, such as policy shifts that affect tourism demand or large-scale capacity changes. Before delivery, we do a final pass to ensure the latest public releases and any recent primary feedback are reflected in the numbers.

Mordor Intelligence's France Hospitality Market Size Compared With Other Published Estimates

Published market sizes for France hospitality can differ a lot, even when they sound like they are measuring the same thing, because the boundary and revenue capture point are not always consistent. Differences also come from how pricing is treated through time, which parts of accommodation are counted, and how often the underlying assumptions are refreshed.

Tourism arrivals, lodging performance indicators like occupancy and ADR, and region-level supply additions are the evidence used to keep Mordor Intelligence's 2025 estimate tied to commercial accommodation revenue in France, instead of broader travel spending or narrow hotel-only definitions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 128.18 B (2025) | |

| Global Consultancy A | USD 96.50 B (2024) | This figure appears to use a narrower accommodation-led scope and a different base year, and it may apply simplified service buckets that do not fully reconcile with France-wide channel mix and class-level price dispersion. |

| Industry Research Desk B | USD 3.30 B (2024) | The value is presented as an incremental growth or a subset definition, rather than total market revenue, which can happen when only select hospitality segments or a delta over the forecast period is reported. |

The spread mainly comes from scope boundaries and what is treated as total revenue versus a partial slice or a growth increment. By anchoring the model on observable demand and operating metrics, and then checking them with primary inputs, the final number stays traceable to clear drivers and repeatable steps.

Key Questions Answered in the Report

How large is the France hospitality market in 2026?

The France hospitality market size reaches USD 133.68 billion in 2026 and is forecast to expand at a 4.29% CAGR to 2031.

What segment grows fastest through 2031?

Service apartments register the highest 6.00% CAGR as remote work and extended-stay demand accelerate.

Which region shows the strongest growth outlook?

Provence-Alpes-Côte d’Azur leads with a projected 5.52% CAGR driven by luxury investments and airport upgrades.

Why are labor costs a challenge for French hotels?

Sector-specific wages rose to USD 13.08 per hour in 2025, surpassing the general minimum wage and increasing payroll burdens.

How will energy regulations affect hotel operators?

The Le Meur Law links operating licenses to energy performance, pushing hotels to invest in retrofits or risk closure, yet tax credits help offset costs.

Are OTAs losing share to direct bookings?

OTAs still command 41.05% share, but direct digital channels grow faster at 7.00% CAGR as hotels invest in personalized web and mobile experiences

Page last updated on: