Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

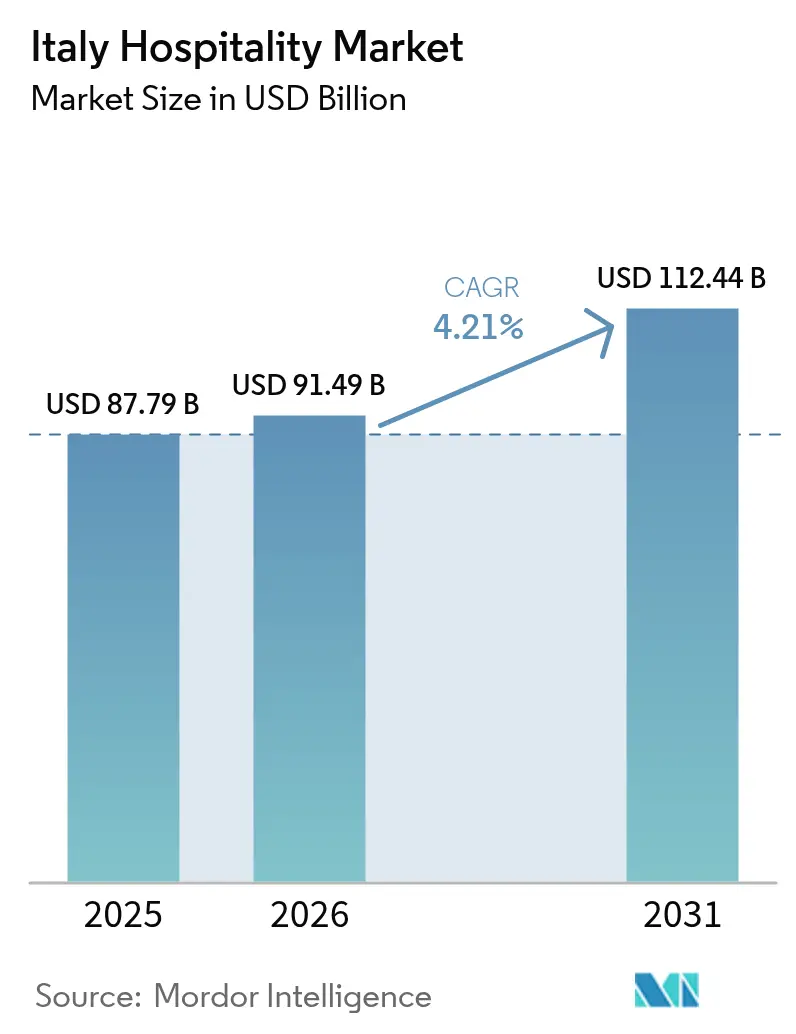

| Base Year Market Size (2025) | USD 87.79 Billion |

| Market Size (2026) | USD 91.49 Billion |

| Market Size (2031) | USD 112.44 Billion |

| Growth Rate (2026 - 2031) | 4.21% CAGR |

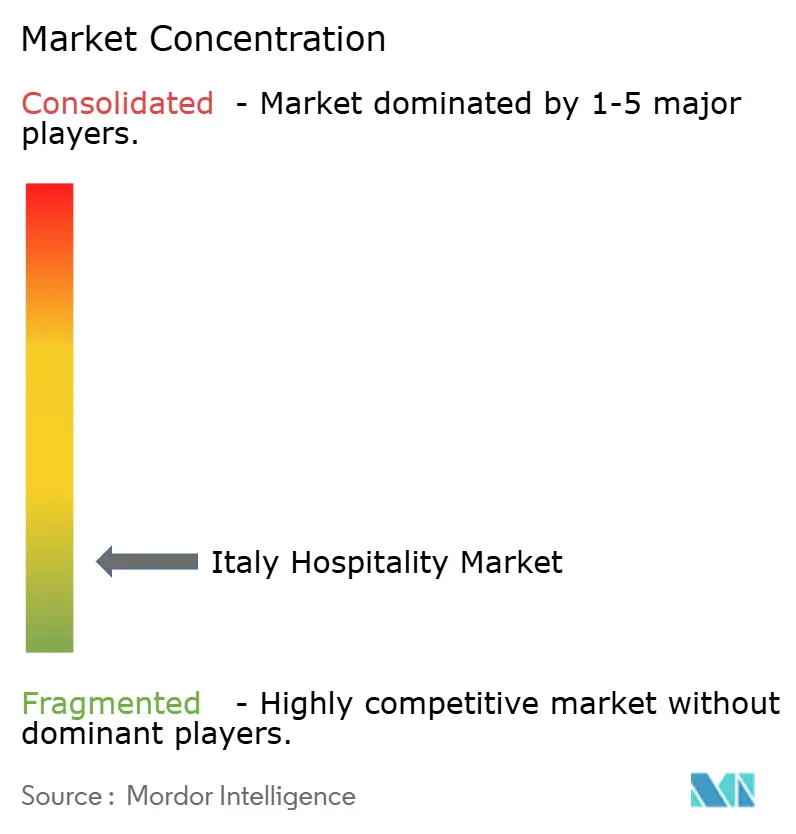

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Italy Hospitality Market Analysis by Mordor Intelligence

Italy Hospitality Market size in 2026 is estimated at USD 91.49 billion, growing from 2025 value of USD 87.79 billion with 2031 projections showing USD 112.44 billion, growing at 4.21% CAGR over 2026-2031.

Demand momentum flows from three intertwined factors: heritage tourism tied to Rome’s Jubilee 2025, visitor inflows projected for the Milan–Cortina Winter Olympics 2026, and the steady expansion of branded hotel supply that professionalizes a highly fragmented landscape. Large-scale tax credits under the Superbonus Turismo scheme accelerate asset refurbishment, giving independent operators a path to energy-efficient upgrades that hedge against volatile utility costs[1]DLAPiper, “Tax Incentives for Businesses in the Tourism Sector,” dlapiper.com. . Meanwhile, digital distribution reshapes customer acquisition; direct channels still generate half of all room revenue, yet online travel agencies (OTAs) are expanding at 9.81% CAGR as travelers favor mobile search, instant price comparison, and frictionless booking[2]HOTREC, “2024 Hotel Distribution Study,” hotrec.eu. . Labor shortages remain a pressing concern: unfilled hospitality positions tripled between 2019 and 2024, pushing payroll above 33% of revenue in many city-center properties. Finally, mandatory ESG reporting under Legislative Decree 125/2024 forces hotels, especially heritage buildings, to invest in metering, renewable energy, and transparent disclosures that add short-term cost but unlock green-finance opportunities.

Key Report Takeaways

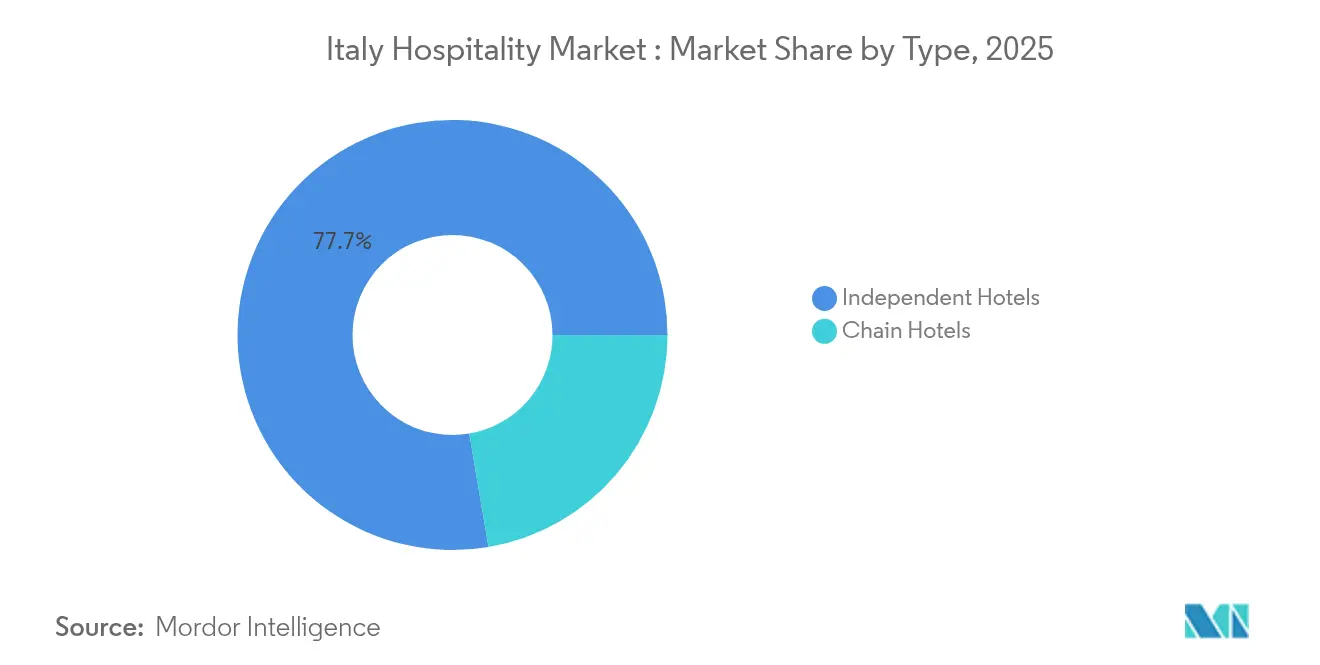

- By type, independent hotels held 77.68% of Italy hospitality market share in 2025, while chain hotels are advancing at a 7.14% CAGR through 2031.

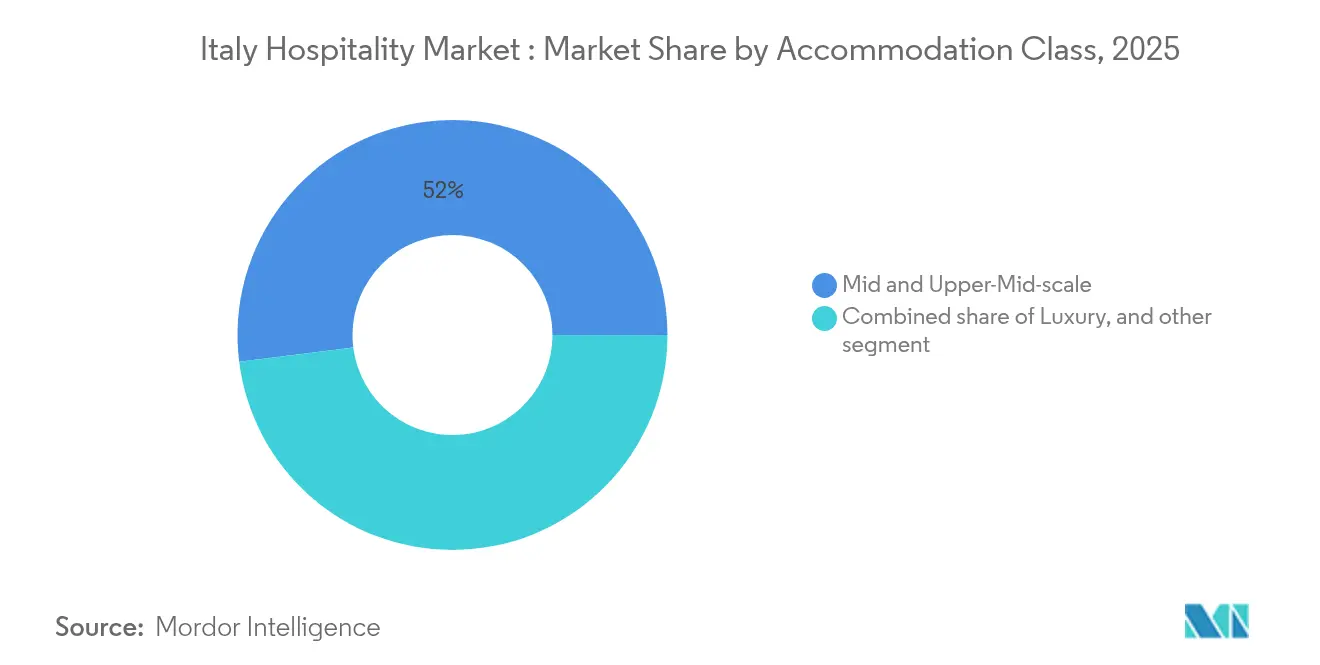

- By accommodation class, the mid & upper-mid segment led with 51.98% of Italy hospitality market share in 2025; luxury properties are set to expand at a 8.98% CAGR to 2031.

- By booking channel, direct bookings captured 49.88% of Italy hospitality market share in 2025, whereas digital OTAs are growing at a 9.73% CAGR to 2031.

- By geography, Northwest Italy commanded 26.14% of Italy hospitality industry share in 2025; the Islands region is projected to grow at a 6.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Italy Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Luxury tourism uplift from Jubilee 2025 & Winter Olympics 2026 | +1.2% | Central Italy and Lombardy, with spillover to major art cities | Short term (≤ 2 years) |

| International chain penetration ≥22% rooms by 2028 | +0.8% | Northwest and Central Italy, expanding to secondary cities | Medium term (2-4 years) |

| Digital-first booking behavior (84% online sales by 2029) | +0.7% | Nationwide, early adoption in Rome, Milan, Florence, Venice | Medium term (2-4 years) |

| Superbonus Turismo refurbishment tax credits | +0.5% | Nationwide, higher uptake in Northern and Central regions | Short term (≤ 2 years) |

| Short-stay rental curbs that shift demand to serviced apartments | +0.4% | Historic city centers and UNESCO areas | Short term (≤ 2 years) |

| Secondary-airport & high-speed-rail upgrades | +0.3% | South Italy and emerging rural destinations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in luxury inbound tourism linked to Jubilee 2025 & Winter Olympics 2026

The dual spotlight of Rome’s Jubilee 2025 and the Milan-Cortina Games lifts premium demand well beyond event months. Italy hosted 64.5 million arrivals in 2024, and luxury hotels alone generated EUR 9 billion (USD 9.9 billion) or 16.82% of total sector revenue, growing 9.23% year on year[3]ANSA, “Turismo in Hotel di Lusso,” ansa.it. . Average daily rates reached EUR 840 (USD 924) in Rome and EUR 910 (USD 1,001) in Milan, signaling substantial price-setting power relative to peer European capitals. High-spending visitors from Germany, the United States, and the United Kingdom contributed more than 65% of five-star room nights, reinforcing Italy’s reputation for experiential travel anchored in culture and cuisine. Up-market positioning extends to secondary destinations Lake Como, Taormina, and Bologna, where conversion of historic villas to boutique luxury formats attracts discerning guests. Because luxury assets operate at lower breakeven occupancy, operators can invest in wellness facilities and curated local experiences that lock in repeat visitation. The persistent premium signals sustainable upside even after the international spotlight shifts elsewhere.

Rapid penetration of international hotel chains

Branded supply crossed the 20% national threshold in 2024, double the penetration rate recorded a decade earlier. Roughly 155 international brands operate in Italy today, a 100% rise since 2015, underscoring investor appetite for stable cash-flow assets backed by global reservation systems. Conversion rather than new-build projects dominate pipelines; 73.40% of planned openings through 2026 involve upgrading family-owned properties into soft-brand or franchise formats, limiting zoning hurdles while elevating service standards. Marriott alone has 20 Italian projects announced, with heavy weighting toward full-service and luxury flags aimed at urban gateways. Accelerated chain growth introduces professional revenue-management tools, loyalty-program access, and unified ESG protocols that enhance asset value. Independent owners increasingly view brand affiliation as a hedge against market shocks, explaining the upward trajectory toward 22% room penetration by 2028.

Digital-first booking behavior

Digital bookings already account for 50.33% of Italy's hospitality market size, and OTAs are expanding at 9.81% CAGR on a path to 84% market penetration within four years. Booking.com controls 71% of OTA revenue, while Expedia sits near 15%, creating a two-platform dominance that compresses margin for smaller hotels. The European Union’s Digital Markets Act levels the playing field by banning price-parity clauses and mandating data transparency, allowing hoteliers to experiment with channel-exclusive offers and loyalty perks. Investments in cloud-based property-management systems, direct-booking engines, and upsell widgets accelerate, especially among mid-market independents seeking to reduce commission leakage. For travelers, mobile-first search and personalized content drive conversion; 65% of domestic guests and 78% of long-haul visitors complete at least one trip-planning task on a smartphone. Hotels that translate web traffic into owned-channel bookings realize up to a 12-percentage-point EBITDA uplift compared with OTA-dependent peers.s.

Tax incentives for hotel refurbishments

Italy’s Superbonus Turismo framework reimburses up to 80% of eligible renovation costs, while the IFIT grant adds a potential EUR 100,000 (USD 110,000) per project for digitalization and energy upgrades. The complementary FRI-Tur revolving fund disburses EUR 780 million (USD 852.5 million), supporting investment tickets between USD 546,500 and USD 10.93 million, and prioritizes projects that integrate renewable energy or seismic safety improvements. Mid-scale family hotels, traditionally capital-constrained, now close funding gaps without dilutive equity. Early adopters report 15-20% reductions in annual utility expenses after installing high-efficiency chillers and photovoltaic panels. Because legislation requires grant-funded assets to retain hospitality use for at least five years, the program stabilizes supply even if market conditions fluctuate. The refurbishment wave also boosts Italy’s compliance with the National Integrated Plan for Energy and Climate, advancing toward a 43.7% emissions reduction target by 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute talent shortage & wage inflation | −1.1% | Nationwide, acute in Central–Northern hubs | Short term (≤ 2 years) |

| Rising energy costs and ESG-compliance outlays | −0.8% | Nationwide, heavier on independents | Medium term (2-4 years) |

| Aging infrastructure & limited reinvestment | −0.6% | Predominantly in Southern Italy & rural areas | Medium term (2-4 years) |

| Bureaucratic hurdles & slow permitting processes | −0.4% | Nationwide, especially impacting small operators | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Acute talent shortage & wage inflation

Despite a record 1.5 million hospitality employees in 2024, Italy posted 604,000 hard-to-fill positions, triple the deficit recorded in 2019. Vacancy rates exceed 30% for chefs and pastry chefs, forcing many hotels to cap room inventory during peak summer months. Rising competition for bilingual front-office staff and revenue-management analysts pushes average monthly salaries 14% above pre-pandemic benchmarks, lifting labor cost to more than one-third of total revenue. Younger workers cite seasonal instability and limited career growth as primary deterrents; 40% of unemployed hospitality staff intend to exit the sector permanently. [4].MDPI, “Quitters from Hospitality Industry,” mdpi.com. Employers respond with signing bonuses, subsidized housing, and partnerships with vocational colleges, but scaled solutions remain elusive. Long-term exposure includes reputational risk: service shortfalls erode review ratings that heavily influence digitally savvy travelers. Unless the talent pipeline strengthens, capacity could lag demand, diluting growth across the Italy hospitality market.

Rising energy costs and ESG-compliance outlays

Natural-gas price volatility and strict sustainability mandates compress margins, particularly for stand-alone properties lacking hedging programs. Under the Corporate Sustainability Reporting Directive, large hotel groups must release audited ESG statements beginning fiscal 2026, driving investment in metering technology and third-party assurance. Heritage buildings face extra complexity: façade preservation limits insulation options, while windows often require custom retrofits priced 25% higher than mass-market frames. Access to green finance is improving; several banks offer discounted rates for projects that achieve at least 30% energy-use reduction, yet smaller operators struggle to meet collateral requirements. Without upgrades, some assets risk demand loss from corporate travel buyers whose policies exclude non-certified hotels. The combined pressure of utility bills and compliance spending subtracts an estimated 0.8 percentage point from forecast CAGR, underscoring the need for industry-wide efficiency gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Independent properties maintain scale advantage while chains professionalize operations

Independent hotels held 77.68% of Italy hospitality market share in 2025, preserving numerical dominance despite steady chain expansion at 7.14% CAGR. Family-run assets thrive on local storytelling, culinary authenticity, and flexible guest interaction that repeat visitors prize. Yet, the fragmented owner base confronts rising guest expectations for omnichannel service and unified loyalty benefits. Conversion pipelines reveal that 67% of upcoming branded openings involve taking over existing independent structures, signaling owner appetite for franchise or soft-brand agreements that retain architectural character. Chains leverage centralized purchasing, robust digital-marketing budgets, and advanced revenue-management software, securing RevPAR premiums of 10-12% over comparable unbranded peers. While independent ethos will remain a hallmark of the Italy hospitality market, it is increasingly augmented by selective brand alliances that marry authenticity with global reach.

By Accommodation Class: Mid-scale leads revenue, luxury accelerates value creation

Mid and upper-mid establishments represented 51.98% of aggregate revenue in 2025, capitalizing on leisure travelers who seek comfort yet remain price sensitive. These properties often operate in renovated historic structures that balance charm and modern amenities, attracting both domestic families and international tour groups. Luxury, though smaller in absolute volume, is the fastest-growing tier at 8.98% CAGR, fueled by ultra-high-net-worth demand for suite-only floors, private villa annexes, and curated cultural itineraries. Italy's hospitality market size for luxury properties exceeded EUR 9 billion (USD 9.9 billion) last year, and transaction data show investors allocating 45% of deal volume to five-star assets due to their resilient margins. Budget & economy hotels retain relevance for price-driven segments, but rising operating costs challenge profitability unless offset by ancillary revenue streams such as coworking spaces or self-service F&B kiosks. Serviced apartments, bolstered by tighter regulation of informal rentals, post double-digit growth and appeal to long-stay corporate travelers who require kitchenettes and flexible check-in.

By Booking Channel: Direct dominance erodes as OTAs consolidate power

Direct booking channels captured 49.88% of Italy hospitality market share in 2025, a testament to repeat visitation patterns in art-city destinations. Still, OTAs’ 9.73% CAGR trajectory indicates a power shift that compresses net rates for operators unable to pivot to dynamic pricing. The Italy hospitality market size attributable to OTA sales is forecast to exceed USD 50 billion by 2030 as consumer trust in user-generated reviews, bundled itineraries, and “pay later” options deepens. Corporate/MICE channels underpin occupancy during shoulder seasons, especially in Milan’s convention district, where large-room blocks are still contracted through global travel-management companies. Wholesale and traditional agents retain niche relevance for complex multi-city tours that package rail passes and museum tickets. Hotels that deploy customer-data platforms and loyalty apps steer guests back to owned channels, saving commission expenses that can otherwise top EUR 30 (USD 33) per night.

Geography Analysis

Northwest Italy leads the country’s hospitality market in 2025 with a 26.14% share, supported by strong demand for Alpine resorts and urban gateways such as Milan and Turin. Preparations for the Winter Olympics are channeling EUR 30 million (USD 32.79 million) into modernizing lodging and enhancing smart-mobility systems to accommodate international visitors. Central Italy follows with a 25.00% share, anchored by the timeless appeal of Rome’s cultural landmarks and Tuscany’s premium wine tourism. Together, these regions create a balanced mix of business, leisure, and heritage-driven demand that keeps occupancy levels high. Investment in transport infrastructure further reinforces their competitive advantage across both domestic and foreign visitor segments.

Northeast Italy, with Venice as its flagship destination, benefits from cruise-ship traffic regulations that have shifted demand toward overnight hotel stays. The average length of stay has increased above 2.4 nights, supporting steady revenue growth for hoteliers. Secondary cities such as Verona and Trieste are also seeing rising inbound traffic due to cultural festivals and cross-border tourism flows. South Italy, while still underpenetrated, is gaining momentum from the expansion of high-speed rail links. Travel time between Bari and Naples has been reduced to under two hours, improving accessibility and stimulating short-break tourism.

The Islands of Sicily and Sardinia represent the fastest-growing sub-segment, projected to expand at a CAGR of 6.90% between 2026 and 2031. Limited upscale room supply and the arrival of marquee international brands, including a forthcoming W Hotels resort in Poltu Quatu, are expected to drive rate premiums. Enhanced air connectivity, such as the upgrade of the Salerno-Costa d’Amalfi airport, is opening new Mediterranean routes for both regional and long-haul travelers. These improvements enable more seamless itineraries combining coastal retreats, cultural exploration, and rural experiences. As a result, the Islands are positioned to capture outsized share growth and elevate Italy’s hospitality market outlook.

Competitive Landscape

Italy’s hospitality market is characterized by high fragmentation, with leading international hotel chains holding only a modest share of the total room inventory. This results in a low market concentration, signaling ample opportunities for consolidation and strategic partnerships. A growing number of family-run and independent hotels are now exploring collaborations with professional management companies to improve competitiveness. While the fragmented landscape has traditionally favored local operators, it increasingly exposes them to disadvantages in areas such as global distribution reach, advanced revenue management, and operational efficiency. To capitalize on this dynamic, global hotel chains are prioritizing conversions of existing independent properties, offering the benefits of international branding while preserving local character.

Strategically, international operators are concentrating their efforts on the luxury and upscale segments, where strong brand equity supports higher management fees and capital investment. In contrast, domestic chains leverage their deep understanding of local markets and heritage-driven positioning to compete in boutique and resort categories. The role of technology is becoming central to competition, with independents investing in tools like revenue optimization systems, CRM platforms, and digital marketing to narrow the performance gap with larger chains. These innovations are critical in enhancing guest experience, driving direct bookings, and maintaining rate integrity. The push toward digital transformation is reshaping how hotels operate and engage with both domestic and international travelers.

White-space growth opportunities are emerging in secondary cities and underdeveloped luxury destinations where international brands remain underrepresented. Additionally, the serviced apartment segment is seeing increased demand due to tighter regulations on short-term rentals, pushing travelers toward professionally managed accommodations. Italy's evolving regulatory landscape, including the implementation of the Digital Markets Act and Corporate Sustainability Reporting Directive, is helping to level the playing field for independent operators. These changes encourage greater transparency, sustainability, and competitive fairness across the industry. As consolidation accelerates and technology adoption rises, Italy’s hospitality market is entering a new phase marked by modernization, strategic alignment, and cross-segment innovation.

Italy Hospitality Industry Leaders

Marriott International

Accor SA

Best Western Hotels & Resorts

NH Hotel Group

Hilton Worldwide

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Una Group unveiled a 176-room high-rise project near Milan’s convention center slated for mid-2026 opening.

- April 2025: Starhotels purchased the Hermitage Hotel & Resort in Forte dei Marmi, marking its inaugural resort entry with 59 rooms and expansive parkland.

- March 2025: Castello SGR acquired Sardinia’s Grand Hotel Poltu Quatu for EUR 70 million (USD 76.5 million), planning redevelopment under Marriott’s W Hotels label.

- January 2025: EY Italy reported that hotel transactions reached EUR 2.1 billion (USD 2.31 billion), a 30% annual jump, with five-star assets capturing 45% of volume.

Italy Hospitality Market Report Scope

The hospitality industry encompasses various services, including lodging, food and beverages, event management, theme parks, and travel. It also includes multiple establishments, such as hotels, tourism agencies, restaurants, and bars. A complete background analysis of the hospitality industry in Italy includes an assessment of industry associations, the overall economy, and emerging market trends by segment. Significant changes in the market dynamics and market overview are also covered in the report.

The hospitality industry in Italy is segmented by type and segment. By type, the market is segmented into chain hotels and independent hotels. By segment, the market is divided into service apartments, budget and economy hotels, mid- and upper-middle-scale hotels, and luxury hotels. The report offers market sizes and forecasts in value (USD) for all the above segments.

By Type

| Chain Hotels |

| Independent Hotels |

By Accommodation Class

| Luxury |

| Mid & Upper-Mid-scale |

| Budget & Economy |

| Service Apartments |

By Booking Channel

| Direct |

| Digital OTAs |

| Corporate / MICE |

| Wholesale & Traditional Agents |

By Geographic Region

| Northwest Italy |

| Northeast Italy |

| Central Italy |

| South Italy |

| Islands |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Accommodation Class | Luxury |

| Mid & Upper-Mid-scale | |

| Budget & Economy | |

| Service Apartments | |

| By Booking Channel | Direct |

| Digital OTAs | |

| Corporate / MICE | |

| Wholesale & Traditional Agents | |

| By Geographic Region | Northwest Italy |

| Northeast Italy | |

| Central Italy | |

| South Italy | |

| Islands |

Key Questions Answered in the Report

How large is the Italy hospitality market in 2026?

The Italy hospitality market size stands at USD 91.49 billion in 2026 and is forecast to grow at a 4.21% CAGR through 2031.

Which region currently leads revenue?

Northwest Italy captures 26.14% of national revenue in 2025, supported by Milan’s corporate demand and Lake Como’s luxury appeal.

What segment is expanding fastest?

Luxury hotels exhibit the highest growth with a 8.98% CAGR, buoyed by Jubilee 2025 and Winter Olympics-linked premium demand.

How are booking habits changing?

Digital OTAs are growing at 9.73% CAGR and are on track to control 84.00% of hotel revenue by 2030 as travelers favor mobile, comparison-rich platforms.

Why are international hotel chains accelerating in Italy?

Owners pursue brand affiliation for global distribution and professional management, driving chain penetration toward 22.00% of rooms by 2029.

What policy helps hotels finance renovations?

The Superbonus Turismo program offers up to 80% tax credits and supplemental grants for energy efficiency, seismic safety, and digital upgrades.

Page last updated on: