Extended Stay Hotel Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Market Size (2026) | USD 59.86 Billion |

| Market Size (2031) | USD 99.15 Billion |

| Growth Rate (2026 - 2031) | 10.62% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

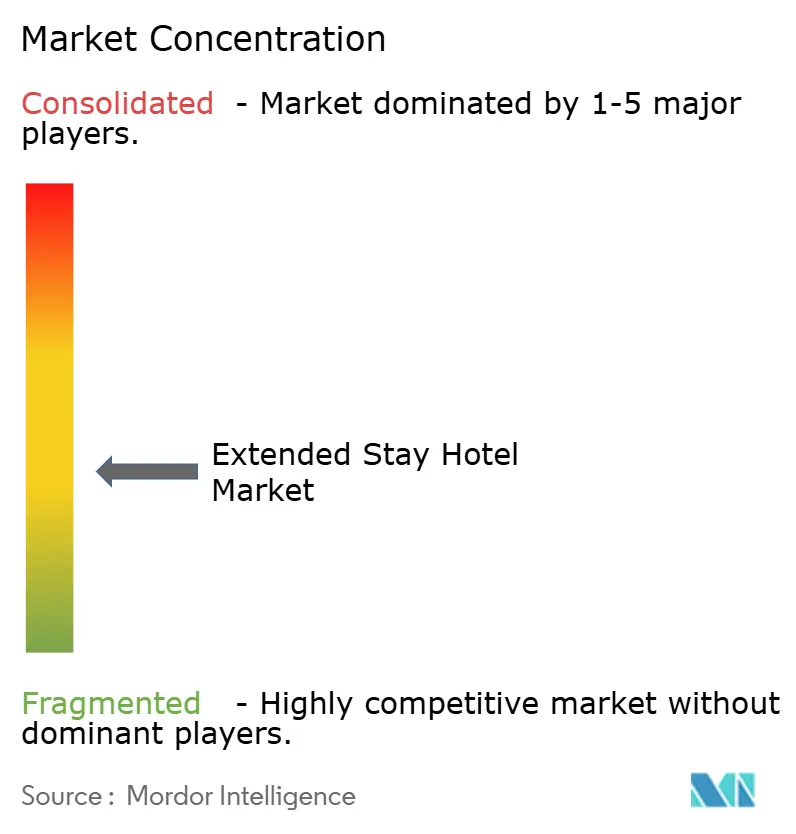

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Extended Stay Hotel Market Analysis by Mordor Intelligence

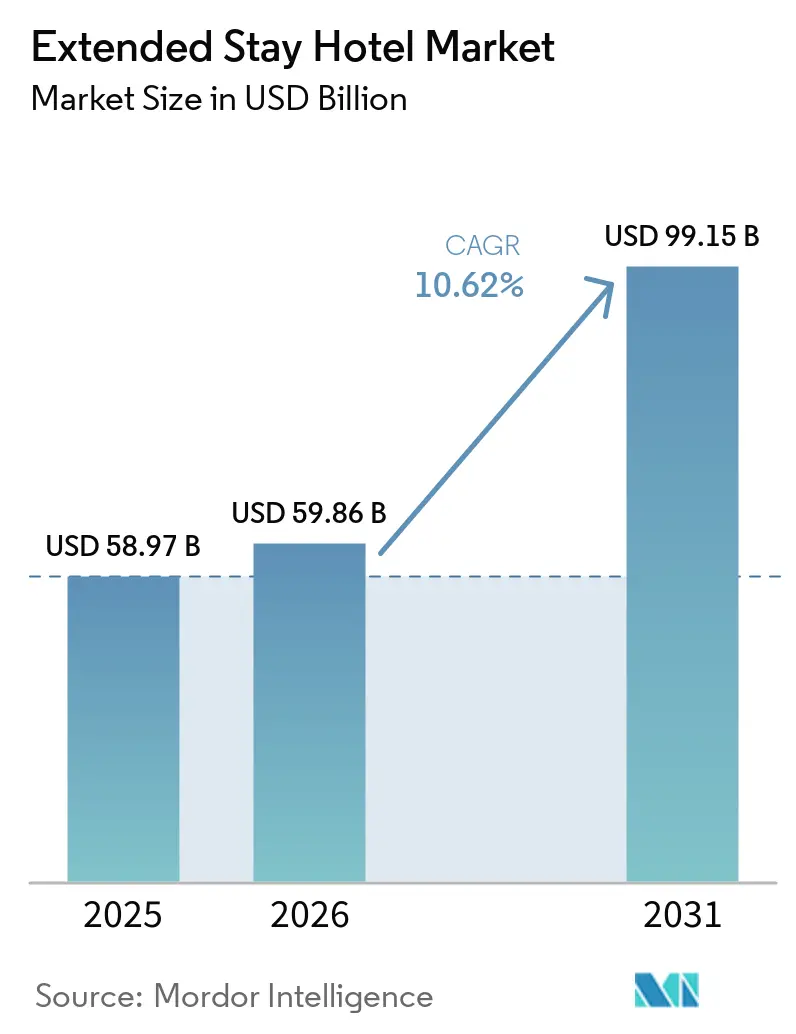

The Extended Stay Hotel Market was valued at USD 58.97 billion in 2025 and is estimated to grow from USD 59.86 billion in 2026 to reach USD 99.15 billion by 2031, at a CAGR of 10.62% during the forecast period (2026–2031). This growth reflects a shift in lodging demand driven by project-based employment, hybrid work patterns, and workforce housing gaps, leading to longer booking durations. Developers favor this segment due to its operational model requiring less labor, lighter food service, and standardized layouts compared to full-service hotels. Demand now extends beyond corporate relocations to include weekly project stays, bleisure extensions, and temporary displacements, enhancing year-round occupancy. The market benefits from rising branded pipelines, improved direct booking capabilities, and conversion-led developments, which enhance cost control and speed to market. Despite financing pressures and construction inflation affecting new openings, the market continues to attract investment due to its revenue model, supported by longer average stays and lower room turnover.

Key Report Takeaways

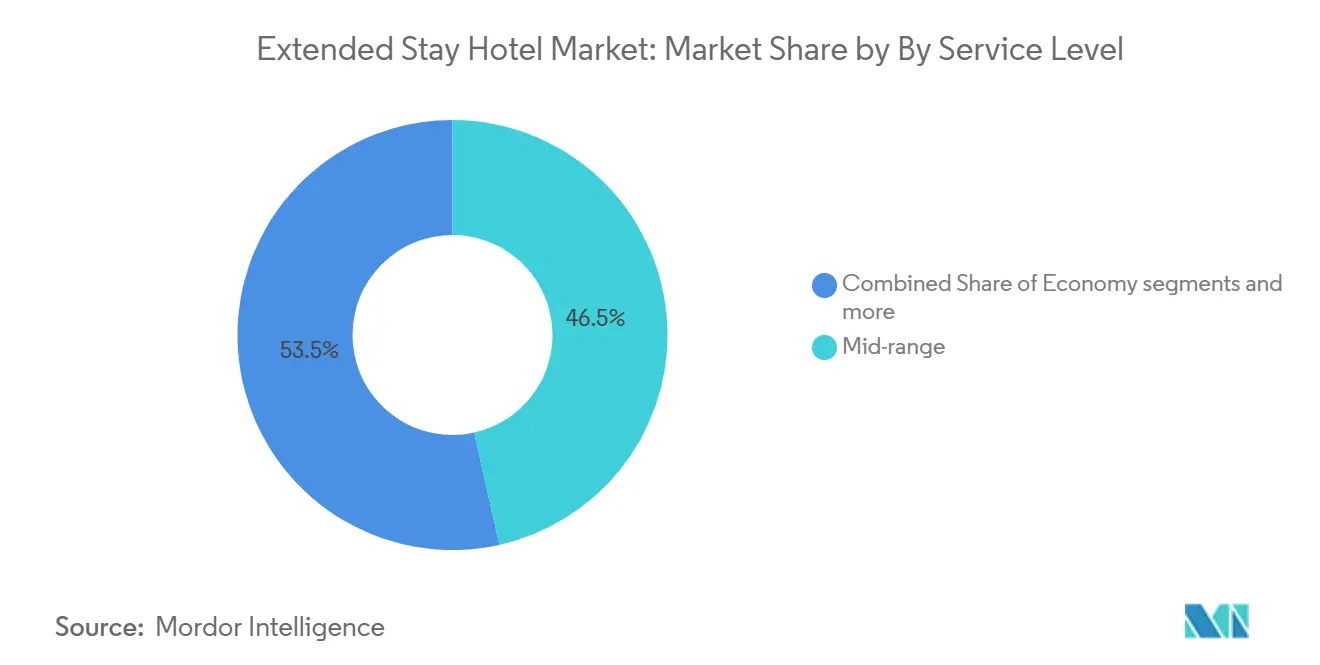

- By service level, mid-range properties led with 46.52% of the Extended Stay Hotel Market share in 2025, while upscale and luxury properties are projected to grow at an 11.13% CAGR through 2031.

- By stay duration, monthly stays accounted for 40.14% of the Extended Stay Hotel Market share in 2025, while weekly stays are projected to grow at an 11.73% CAGR through 2031.

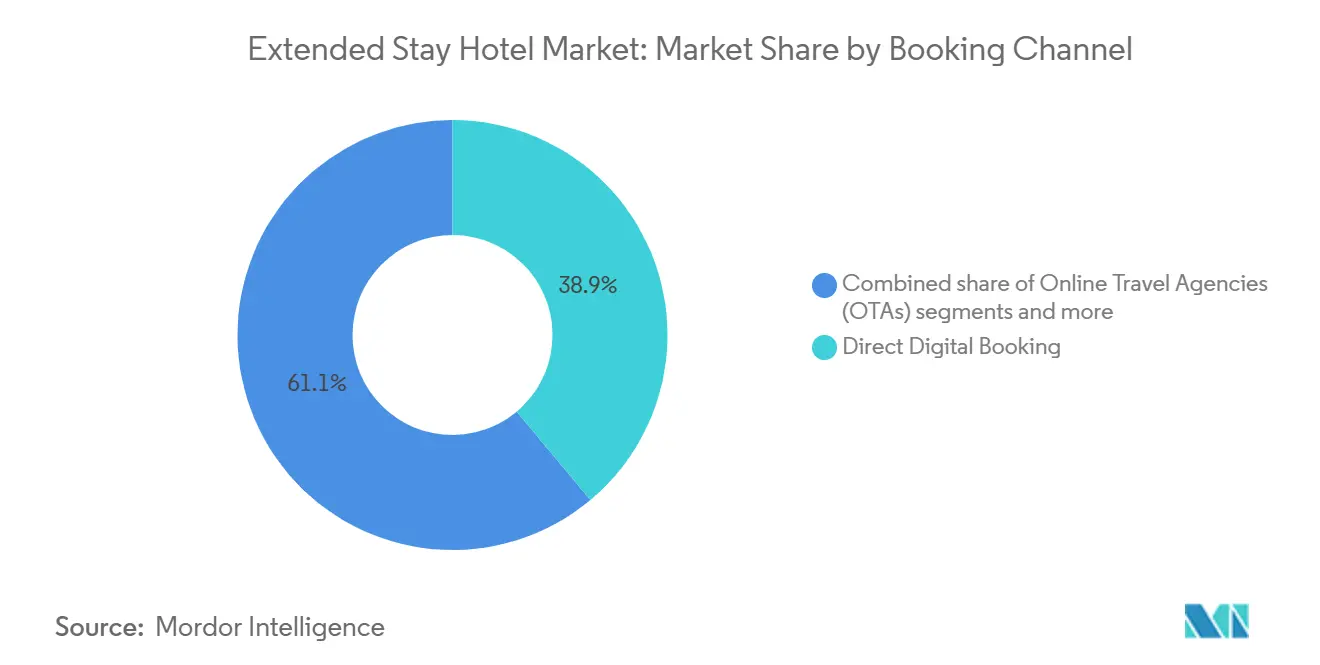

- By booking channel, direct digital bookings represented 38.92% of transactions in the Extended Stay Hotel Market in 2025, while Online Travel Agencies (OTAs) are projected to grow at a 12.94% CAGR through 2031.

- By end user, business customers contributed 34.31% of demand in the Extended Stay Hotel Market in 2025, while relocating residents and insurance-displaced guests are projected to grow at a 12.57% CAGR through 2031.

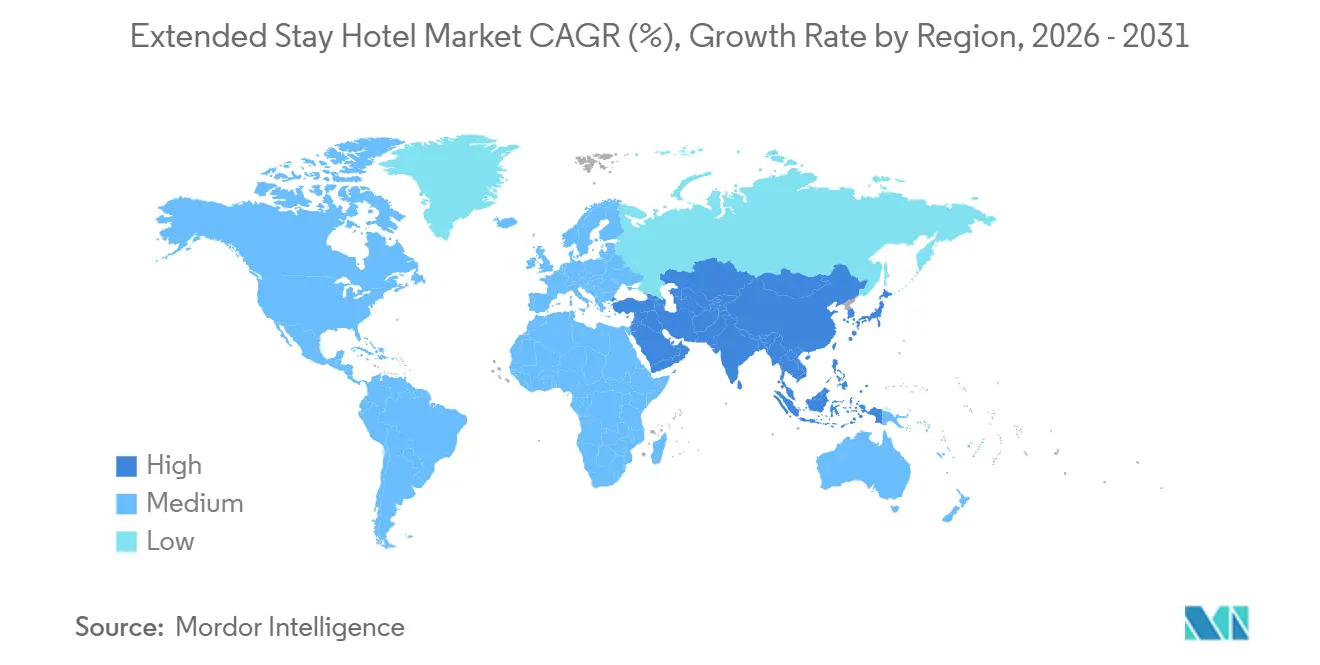

- By geography, North America led with 36.86% share in the Extended Stay Hotel Market in 2025, while Asia-Pacific is projected to grow at an 11.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Extended Stay Hotel Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Corporate relocation and project-based lodging demand | +2.5% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Hybrid work and bleisure extending length of stay | +1.8% | Global | Medium term (2-4 years) |

| Kitchen-equipped suites value advantage | +1.2% | Global | Short term (≤ 2 years) |

| Labor-light operating model attracts developers | +1.5% | Global | Medium term (2-4 years) |

| Workforce housing spillover from industrial megaprojects | +2.0% | North America, Middle East and Africa | Long term (≥ 4 years) |

| Insurance displacement and recovery-worker stays | +0.8% | North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Corporate relocation and project-based lodging demand

Corporate mobility is shifting from short hotel stays to longer assignments aligned with project schedules. Corporate demand for extended stays, beyond traditional relocations, has grown significantly, reflecting a preference for accommodations tied to execution work rather than meetings. This demand is less likely to be delayed, as roles like engineering teams and specialized installers require proximity to worksites until tasks are completed. Operators with strong corporate sales teams and dedicated account structures are better positioned than those relying on open-market distribution. Nearshoring and friend-shoring are driving manufacturing activity to secondary cities, where branded supply has historically been limited. This trend enhances contract visibility for owners and stabilizes occupancy rates, even during fluctuations in transient travel.

Hybrid work and bleisure extending length of stay

Hybrid work has increased opportunities for travelers to combine leisure with business, leading to longer stays in the extended stay hotel market. A survey indicated growing employer support for remote work and a rise in employees extending international work trips for personal time. Corporate travel managers reported more trip extension requests, with a significant portion of work-related travel now including weekends. This trend boosts room nights without proportionally increasing housekeeping or check-in costs, maintaining the model's margin advantage. Additionally, guests now compare extended-stay properties with flexible apartments and short-term rentals. As a result, kitchen functionality, room design, and neighborhood accessibility are becoming critical for guest retention and repeat bookings[1]Arrivia, “2026 Bleisure Travel Trends (and What They Mean for Loyalty),” Arrivia, arrivia.com.

Kitchen-equipped suites value advantage

Built-in kitchens are a key differentiator in the extended stay hotel market, reducing overall trip costs for guests staying longer durations. This feature is particularly valuable for workforce travelers, relocating families, and corporate guests seeking predictable daily expenses over lower room rates. It also enhances price resilience for operators, as guests save on dining, laundry, and convenience purchases. Kitchen-equipped suites make extended stay hotels more competitive against standard hotels and furnished apartments, especially when employers or insurers assess total stay costs rather than nightly rates. Additionally, this design aligns with the segment's operating model by supporting independent guest routines without requiring extensive on-site food-and-beverage services. This combination of guest utility and reduced service demands ensures the format remains relevant across economy, mid-range, and upscale properties.

Labor-light operating model attracts developers

Developers favor the extended stay hotel market due to its efficient operating model, which requires fewer labor hours and maintains a controlled cost structure. Features like periodic housekeeping, limited restaurant services, and reduced front-desk demands simplify staffing, making it easier to manage during labor shortages and wage inflation. The segment has gained investor confidence as a defensive lodging option with strong return visibility. Development benefits from conversion opportunities, as assets like apartments or offices can often be repurposed faster than building new hotels. Noble Investment Group is adopting modular construction in its long-term accommodations to reduce build times, improve labor availability, and enhance cost predictability in challenging capital markets[2]Noble Investment Group, “How Noble Is Integrating Modular Construction Into Its Branded Long-Term Accommodations Platform,” Noble Investment Group, nobleinvestment.com. These operational and developmental efficiencies continue to attract new brands, innovative prototypes, and conversion-focused owners to the extended stay hotel market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High interest rates and construction-cost inflation | -1.5% | Global | Medium term (2-4 years) |

| Occupancy dilution in fast-expanding metros | -0.8% | Asia- Pacific Core, Spill-over To North America | Short term (≤ 2 years) |

| Economy-brand launch wave creates localized oversupply | -0.6% | North America | Short term (≤ 2 years) |

| Aging assets face resident-like wear and maintenance drag | -0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High interest rates and construction-cost inflation

High borrowing costs and persistent construction inflation are key challenges for the extended stay hotel market. Lenders are demanding more equity and applying conservative underwriting, slowing project progress despite favorable demand signals. This issue is particularly significant in the economy tier, where room rates often fail to meet the returns required for new developments under expensive financing conditions. Room growth projections have been adjusted downward, with operators anticipating moderate annual increases in rooms through the forecast period. In Europe, serviced-apartment transactions in Germany are expected to decline, reflecting institutional caution amid limited interest-rate visibility. As debt remains costly, the market is focusing on conversions, selective brand support, and phased project pipelines rather than aggressive new developments.

Occupancy dilution in fast-expanding metros

Rapid room additions in urban markets are challenging occupancy absorption, especially where converted supply outpaces long-stay demand normalization. Extended-stay hotel supply recently experienced its strongest annual growth in years, while economy supply increased significantly due to apartment-to-hotel conversions. Annual occupancy dropped to its lowest level since 2020, and RevPAR declined monthly after the first quarter as supply exceeded demand. This issue is most evident in metro areas with concentrated lower-priced inventory, where leisure demand fails to offset reduced corporate volume. The extended-stay hotel market faces localized risks, with pricing pressures emerging before new rooms are fully absorbed. Residential conversions may also attract regulatory scrutiny if cities view them as impacting long-term rental availability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Level: Mid-Range Anchors Demand, Upscale Tier Gains Fastest Momentum

Mid-range properties held 46.52% of the extended stay hotel market in 2025, generating the highest revenue among service tiers. This tier caters to workforce travelers, project-cycle employees, relocating staff, and corporate guests seeking functional amenities at moderate costs. Franchisors find mid-range supply scalable due to standardized room layouts, kitchen-focused designs, and manageable development budgets. Choice Hotels reported 66 domestic openings in 2025 across its four extended-stay brands, with United States extended-stay net rooms increasing by 11.7% from the end of 2024[3]Choice Hotels International, “Choice Hotels International Reports First Quarter 2026 Results,” Choice Hotels Media, media.choicehotels.com. These developments highlight the mid-range tier's role in balancing affordability, guest comfort, and operational efficiency. Economy properties are expanding through conversions, but mid-range properties maintain a strong position.

Upscale and luxury segments are projected to grow at an 11.13% CAGR through 2031. Rising accommodation standards for international assignees and senior project managers are driving demand for higher-tier long-stay formats. The trend of combining work and leisure is also influencing preferences, with guests seeking better design, communal spaces, and prime locations. Adagio plans to establish 180 aparthotels across 25 countries by 2030, supported by its upward portfolio structure. The extended stay hotel market is increasingly segmented by traveler expectations rather than price alone. Growth in these segments is expected to concentrate in gateway cities and corporate hubs, where compliance, lifestyle, and brand assurance are key factors.

By Stay Duration: Monthly Cycle Leads Volume, Weekly Stays Accelerate Fastest

Monthly stays captured 40.14% of demand in 2025, making the 30-day cycle the largest duration band in the extended stay hotel market. This tier aligns with relocation assignments, project deployments, and temporary housing needs, offering guests an alternative to short trips or leases. Operators benefit from reduced re-booking friction, lower front-desk turnover, and improved housekeeping schedules. Monthly guests provide steadier occupancy compared to transient travelers, as bookings are tied to ongoing needs rather than single events. This stability position lasts monthly stays as a key operational component of the extended stay hotel market, despite faster growth in other segments. Quarterly stays, though smaller in volume, offer strong visibility on room nights and lower turnover-related costs.

Weekly stays are projected to grow at an 11.73% CAGR through 2031, driven by short-cycle assignments in technology, healthcare, logistics, and advanced manufacturing. These guests fall between transient travelers and those requiring full relocation solutions. Weekly stays represent a valuable segment, as guests appreciate brand reliability while favoring direct bookings, repeat visits, and loyalty programs. Data links weekly demand to software teams, commissioning crews, and traveling healthcare staff, fostering repeat business across project phases. This segment is expected to gain strategic importance by attracting high-frequency travelers and maintaining occupancy between monthly contracts.

By Booking Channel: Direct Digital Holds Lead, OTAs Expand Reach Faster

Direct digital channels accounted for 38.92% of transaction volume in 2025, driven by loyalty programs, operator-owned websites and apps, and corporate portals offering tailored rate visibility and stay conditions for long-duration guests. These channels are crucial for extended stays, as OTA commissions become costlier for multi-week bookings. This cost dynamic supports investments in loyalty integration, member pricing, and brand-owned digital platforms. Adagio aims to increase direct sales to 30% of total network revenue by 2030 through Adagio-city.com and the ALL (Accor Live Limitless) platform. The extended stay hotel market focuses on guest acquisition strategies that protect margins throughout the stay, not just at booking.

OTAs are the fastest-growing channel, with a projected 12.94% CAGR through 2031, as they connect extended-stay inventory to guests outside hotel loyalty ecosystems. Growth is supported by leisure travelers, bleisure guests, and temporary housing users who often start searches on broad travel platforms. Rising weekend-inclusive work travel and OTAs’ discovery role for extended-stay formats further drive this trend. For operators, OTAs expand reach and fill rooms during low-demand periods but also shift price expectations toward vacation rental benchmarks instead of corporate rates. As the extended stay hotel market attracts more non-corporate guests, brand owners must balance OTA visibility with retention strategies to bring repeat guests back to direct channels.

By End User: Corporate Demand Remains Core, Displacement-Led Demand Rises Fastest

Business customers accounted for 34.31% of demand in the extended stay hotel market in 2025. This group includes corporate relocations, project deployments, training activities, and public-sector assignments, which are typically more stable than leisure demand. The segment reflects the core value of extended stay hotels, catering to guests with travel needs exceeding the practicality of standard hotel rooms. Corporate bookings offer predictability, driven by project schedules, staff movements, and operational commitments. Despite the entry of new traveler groups, business-driven bookings remain critical. Trainers and trainees also contribute, particularly near major campuses, industrial training centers, and employer hubs.

Relocating residents and insurance-displaced guests represent the fastest-growing segment, projected to expand at a 12.57% CAGR through 2031. This growth diversifies the market beyond corporate use, introducing urgent, location-specific, and multi-week demand. Properties collaborating with insurers, offering flexible bookings, and featuring practical layouts with kitchens and laundry facilities are well-positioned. This trend highlights the extended stay hotel market’s relevance to temporary housing ecosystems. The accommodation format, resembling long-term living more than short stays, aligns well with displaced-household demand, particularly in regions prone to weather, fire, or housing disruptions.

Geography Analysis

North America accounted for 36.86% of the global extended stay hotel market revenue in 2025. The region benefits from extensive branded inventory, mature franchising networks, and concentrated industrial and corporate travel hubs. In the United States, the segment’s growing share within lodging has enhanced customer familiarity and distribution reach. Investments in semiconductors, energy, data centers, and logistics drive long-duration accommodation demand in inland and Sun Belt markets. Both urban demand and workforce-driven areas with limited long-stay housing support the market.

Brand development and conversion programs are shaping the North American market. Marriott’s StudioRes brand opened its first property in Fort Myers, Florida, in 2025, with 85 properties in the pipeline by year-end. Hilton launched Apartment Collection by Hilton in January 2026 with Placemakr, adding furnished apartment options. Wyndham reported in April 2026 that its extended-stay pipeline, including ECHO, Hawthorn, and WaterWalk, reached 45,000 rooms[4]Vidle Housing and Blueground, “Vidle Housing and Blueground Expand Housing Partnership,” PR Newswire, prnewswire.com. These developments reflect growth across economy and higher-end formats. In South America, Brazil, Chile, and Peru are formalizing long-stay supply around corporate hubs.

Europe has an established aparthotel and serviced-apartment market, while Asia-Pacific is the fastest-growing region with an 11.04% CAGR through 2031. Europe’s growth is driven by corporate relocations, professional stays, and city-based demand, with operators expanding under regulated formats. Adagio’s FIRST plan targets 180 aparthotels across 25 countries by 2030. In Asia-Pacific, Japan’s travel activity, new apartment-hotel formats, and demand for long-stay options in business hubs drive growth. Relocation trends in Southeast Asia and long-stay demand in major cities further support the market. The Middle East and Africa are seeing increased workforce accommodation demand due to megaprojects in previously underserved markets.

Competitive Landscape

The extended-stay hotel market remains moderate, with major operators maintaining significant brand presence and geographic reach. Marriott International, Hilton Worldwide Holdings, Extended Stay America, IHG, and Choice Hotels International collectively accounted for a substantial share of global revenue in 2025. However, no single company dominates pricing or development decisions across the sector. This fragmentation allows aparthotel specialists, regional operators, tech-enabled furnished apartment platforms, and conversion-focused brands to compete alongside global hotel groups. Factors such as product positioning, corporate account access, brand trust, and development speed are critical, enabling both global chains and niche operators to succeed in specific markets or use cases.

Large companies are expanding platforms, restructuring brand portfolios, and forming partnerships to reduce distribution challenges. Marriott advanced StudioRes into the midscale segment while integrating citizenM and licensing Sonder. Hilton introduced Apartment Collection by Hilton in early 2026, focusing on residential-hospitality hybrids with furnished apartments under its standards. Choice Hotels reported consecutive quarters of extended-stay net room growth in the United States, with extended-stay projects forming a significant portion of its domestic pipeline. BWH Hotels entered the segment with the launch of @HOME by Best Western in the United States, planning additional properties globally by the end of 2026. These developments highlight the market's evolution through brand diversification, partnerships, and increased focus from established hotel groups.

Opportunities are evident in secondary cities near industrial projects, long-stay supply in select Asia-Pacific locations, and accommodations tied to insurance or workforce partnerships. Blueground expanded its housing partnerships, offering healthcare travelers access to thousands of furnished apartments across multiple cities. This platform model competes with hotels by appealing to guests seeking flexibility, apartment-style living, and digital booking ease. Meanwhile, large hotel companies leverage loyalty programs, franchise systems, and brand credibility to retain corporate demand and accelerate project pipelines. The market is unlikely to consolidate around a single model, as diverse guest preferences drive demand for varied formats and pricing structures.

Extended Stay Hotel Industry Leaders

Marriott International

Hilton Worldwide Holdings

Extended Stay America

InterContinental Hotels Group

Choice Hotels International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Marriott International and The Fern Hotels & Resorts (Series by Marriott) celebrated 75 hotel signings and 50 openings across India in under six months since the brand's November 2025 debut, adding over 3,556 rooms; the milestone establishes India as the primary growth platform for the Series by Marriott global rollout.

- May 2026: Caliber Cos. is advancing Hyatt Studios development in three high-growth United States markets, including Steamboat Springs, CO. The Steamboat Springs project is fully entitled, with construction financing secured in April 2026. Hyatt contributed approximately USD 1.14 million in brand capital support.

- April 2026: LivAway Suites has started construction on its first Nevada location in North Las Vegas, marking its 22nd site nationwide. Supported by strong capital and an integrated operating model, the brand plans to announce 10 additional markets in 2026.

- April 2026: BWH Hotels, in partnership with Prime Hospitality, opened the first @HOME by Best Western extended-stay property in St. George, Utah. The brand's global pipeline is expected to reach 34 hotels and 2,791 rooms by late 2026, with a debut near Atlanta, Georgia, planned for the same period.

Global Extended Stay Hotel Market Report Scope

| Economy |

| Mid-range |

| Upscale and Luxury |

| Weekly |

| Monthly |

| Quarterly and Longer-term |

| Online Travel Agencies (OTAs) |

| Direct Digital Booking |

| Offline / Corporate Contract Booking |

| Business Customers |

| Trainers and Trainees |

| Government and Defense Personnel |

| Leisure Travelers and Families |

| Relocating Residents and Insurance-displaced Guests |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East And Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Service Level | Economy | |

| Mid-range | ||

| Upscale and Luxury | ||

| By Stay Duration | Weekly | |

| Monthly | ||

| Quarterly and Longer-term | ||

| By Booking Channel | Online Travel Agencies (OTAs) | |

| Direct Digital Booking | ||

| Offline / Corporate Contract Booking | ||

| By End User | Business Customers | |

| Trainers and Trainees | ||

| Government and Defense Personnel | ||

| Leisure Travelers and Families | ||

| Relocating Residents and Insurance-displaced Guests | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East And Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the current size of the extended stay hotel market?

The extended stay hotel market size stood at USD 58.97 billion in 2025 and is expected to reach USD 59.86 billion in 2026 before rising to USD 99.15 billion by 2031.

What is driving growth in extended stay hotels worldwide?

Growth is being supported by project-based lodging demand, hybrid work, bleisure travel, workforce housing shortages, and rising demand from relocating and insurance-displaced guests.

Which region leads global revenue in extended stay hotels?

North America led the extended stay hotel market with a 36.86% share in 2025, supported by deep branded supply and strong industrial and corporate travel corridors.

Which region is growing fastest in long-stay lodging?

Asia-Pacific is forecast to grow fastest at an 11.04% CAGR through 2031, supported by strong travel flows, relocation activity, and rising long-stay product development.

Which service tier is largest in extended stay hotels?

Mid-range properties led with 46.52% share in 2025 because they match the needs of workforce travelers, project employees, and value-focused corporate guests.

Which guest segment is expanding fastest?

Relocating residents and insurance-displaced guests are expected to grow fastest at a 12.57% CAGR through 2031, reflecting the segment’s rising role in temporary housing demand.

Page last updated on: