Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

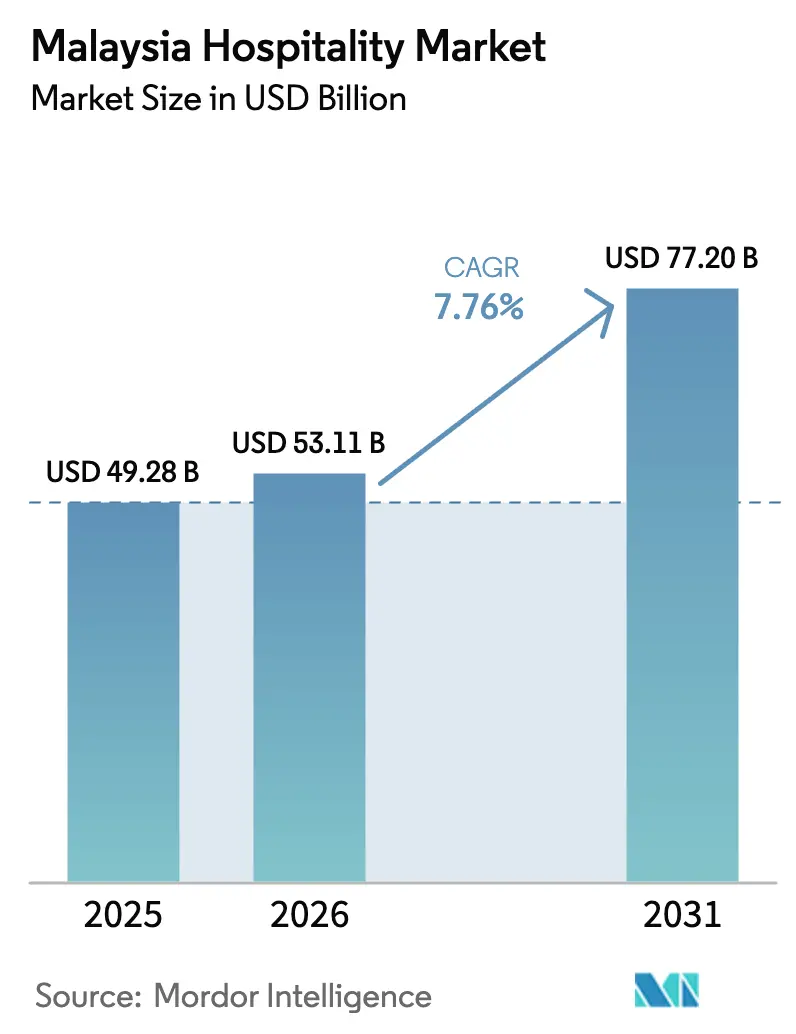

| Base Year Market Size (2025) | USD 49.28 Billion |

| Market Size (2026) | USD 53.11 Billion |

| Market Size (2031) | USD 77.20 Billion |

| Growth Rate (2026 - 2031) | 7.76% CAGR |

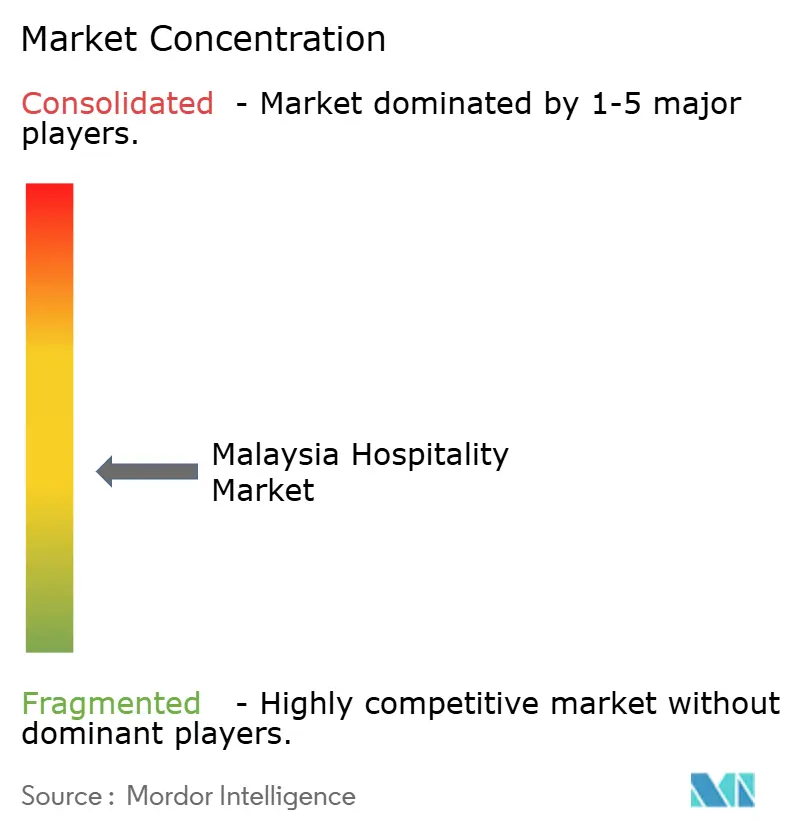

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Hospitality Market Analysis by Mordor Intelligence

The Malaysia Hospitality Market size was valued at USD 49.28 billion in 2025 and is estimated to grow from USD 53.11 billion in 2026 to reach USD 77.20 billion by 2031, at a CAGR of 7.76% during the forecast period (2026-2031).

The growth path aligns with the Visit Malaysia 2026 program’s fiscal commitment, the acceleration of luxury supply in Kuala Lumpur and Penang, and major transport projects that improve access to secondary cities along the ECRL and the RTS Link. Operators are leaning into loyalty ecosystems, AI-enabled direct digital sales, and premium positioning to lift revenue quality while moderating acquisition costs. The Malaysia hospitality market benefits from policy clarity around tourism promotion and infrastructure delivery that reduces travel friction and extends visitor dispersion beyond core hubs. These tailwinds position upscale and luxury assets to push rates without dampening demand as supply adds depth in city cores and resort corridors.

Key Report Takeaways

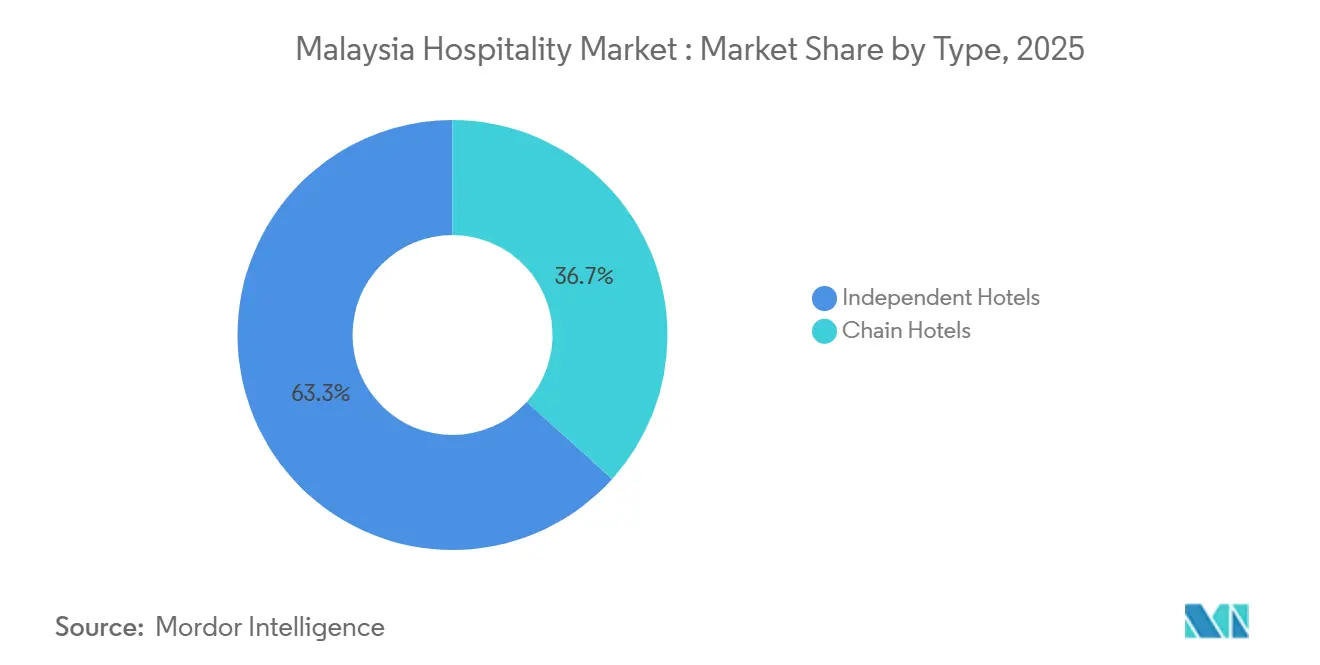

- By type, independent hotels led with 63.32% of the Malaysia hospitality market share in 2025, while chain hotels are projected to record the fastest expansion at a 10.75% CAGR through 2031.

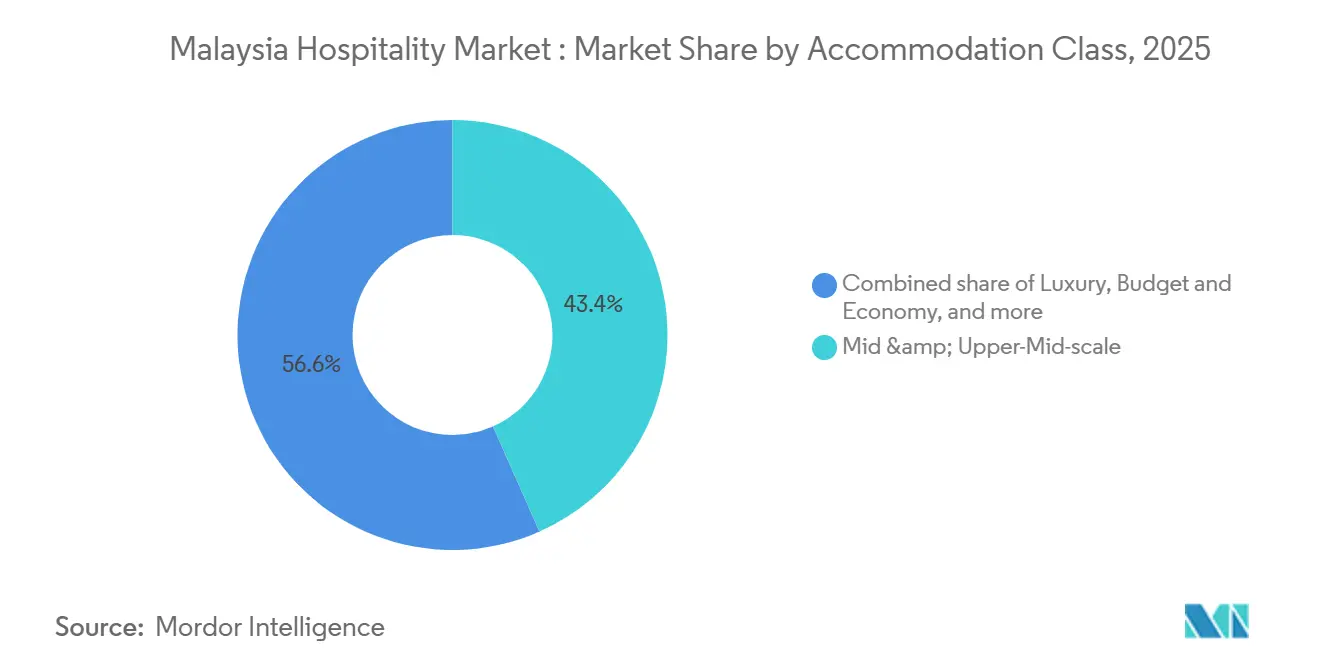

- By accommodation class, mid and upper‑mid‑scale properties accounted for 43.37% of the Malaysia hospitality market share in 2025, and the luxury tier is set to grow the fastest at a 13.74% CAGR through 2031.

- By booking channel, OTAs held 57.35% of the Malaysia hospitality market share in 2025, while direct digital channels are expected to grow the fastest at a 15.73% CAGR through 2031.

- By geography, Central Malaysia retained 49.37% of the Malaysia hospitality market share in 2025, and East Malaysia is set to expand the fastest at an 11.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Malaysia Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-COVID "Visit Malaysia 2026" tourism push | +1.8% | Global | Short term (≤ 2 years) |

| Accelerated luxury pipeline in Kuala Lumpur & Penang | +1.5% | Central, Northern | Medium term (2-4 years) |

| OTA dominance boosts room-night conversion | +1.2% | Global, particularly Central & Southern | Short term (≤ 2 years) |

| Infrastructure roll-outs (RTS Link, ECRL), unlocking secondary cities | +1.6% | Southern (RTS), East Coast (ECRL) | Medium term (2-4 years) |

| Niche ESG-certified resorts capturing premium ADR | +0.8% | Central, East Malaysia, particularly luxury resorts | Medium term (2-4 years) |

| E-sports-themed hotels tapping millennial demand | +0.4% | Central, Southern (Melaka) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-COVID "Visit Malaysia 2026" Tourism Push Delivers Fiscal Commitment and Visa Liberalization

Visit Malaysia 2026 is supported by USD 135.7 million (MYR 550.0 million) in promotional funding and USD 27.1 million (MYR 110.0 million) for infrastructure, which signals fiscal commitment to demand recovery and destination marketing[1]Ministry of Finance Malaysia, “Budget Speech 2025,” investmalaysia.gov.my. The campaign commenced operations at Kuala Lumpur International Airport and key entry points nationwide on January 1, 2026, which marks an operational inflection for coordinated arrivals handling and event activation. The visa exemption program for Chinese nationals has been extended by five years, while Indian nationals can avail it until December 31, 2026. Eligible Chinese nationals may now stay in Malaysia for up to 90 days, previously 30 days[2]Fragomen Global, “Malaysia: Visa Exemption Implemented for Chinese and Indian Nationals,” fragomen.com. The launch also aligns with a calendar of nationwide cultural and festive events that push room-night demand into shoulder periods and distribute travel beyond a few hubs within the Malaysia hospitality market. This policy clarity lowers perceived risk for hotel investments in secondary corridors that also benefit from transport upgrades, which helps the Malaysia hospitality market attract capital for new builds and conversions.

Accelerated Luxury Pipeline in Kuala Lumpur and Penang Reshapes Revenue-Per-Available-Room Benchmarks

Kuala Lumpur’s pipeline includes 1,970 luxury rooms within a 6,209-room under-construction base, which adds depth to the Golden Triangle and supports premium rate ceilings in the Malaysia hospitality market[3]CoStar News Team, “Signing of Langham Hotel Signals Luxury Segment’s Coming of Age in Kuala Lumpur,” costar.com. Park Hyatt Kuala Lumpur opened in August 2025, within Merdeka 118 and reinforced the city’s positioning for high-net-worth travellers and global corporate accounts[4]Hyatt Newsroom, “Park Hyatt Kuala Lumpur Opens in Malaysia,” newsroom.hyatt.com. An additional five-star supply led by Waldorf Astoria Kuala Lumpur and Conrad Kuala Lumpur is set to widen choice and strengthen brand-led pricing power as the luxury tier scales. Luxury rate traction was already evident as ADR reached USD 183.52 (MYR 743.78) in August 2024, which supported RevPAR at USD 146.18 (MYR 592.45), during peak months. Penang’s pipeline and mixed-use luxury entries complement Kuala Lumpur and extend premium appeal into the Northern region, which is supported by new executive apartments and branded residences that lengthen stays.

OTA Dominance Boosting Room-Night Conversion While Eroding Operator Margins

OTAs held 57.35% of booking share in 2025, which kept occupancy elevated for independents and smaller brands that rely on aggregated demand within the Malaysia hospitality market. The commission structure raises acquisition costs and compresses profits for price-sensitive segments, which leaves fewer funds for refurbishment or digital investment during recovery. Direct costs for optimized websites and payment processing can be materially lower than typical platform fees, which lifts net ADR as channel mix rebalances in the Malaysia hospitality market. As operators regain customer data through direct bookings, they unlock targeted remarketing that improves repeat rates and reduces reliance on intermediaries over time.

Infrastructure Roll-Outs Unlock Secondary Cities and Reduce Travel Friction

The Johor Bahru–Singapore RTS Link is planned to carry 10,000 passengers per hour per direction and cut cross-border travel time to 5 minutes, which expands weekday and weekend flows into Johor’s hotel nodes. The 665-kilometer East Coast Rail Link will cut Gombak–Kota Bharu travel time to 4 hours, which opens year-round access to beach and nature destinations across Pahang, Terengganu, and Kelantan. By 2030, the ECRL is expected to carry a sizable share of Kuala Lumpur International Airport passengers to the East Coast, which improves dispersal and supports new hotel development near stations within the Malaysia hospitality market. These links reposition secondary cities into practical short-stay destinations for Singapore-based professionals and Klang Valley residents, which adds new addressable demand. Developers align pipelines to transit nodes to capture commuter, corporate, and leisure flows as operations begin.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labour-cost inflation after 2024 minimum-wage hike | -0.8% | Nationwide, acute for independent budget hotels | Short term (≤ 2 years) |

| Slow visa processing for emerging markets | -0.3% | Global, particularly affecting African and South Asian markets | Short term (≤ 2 years) |

| Strain on urban utilities from rapid hotel densification | -0.5% | Central (KL Golden Triangle), Northern (George Town, Gurney Drive) | Medium term (2-4 years) |

| High OTA commission squeezes on independents' margins | -0.6% | Nationwide, acute for independent properties without pricing power | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Labour-Cost Inflation After 2024 Minimum-Wage Hike Compresses Budget-Segment Operating Margins

On February 1, 2025, Malaysia’s minimum wage increased to USD 419.46 (MYR 1,700) per month, for employers with five or more workers, then extended to all employers on August 1, 2025, which lifted fixed labour costs across hotel classes. Budget independents feel the sharpest pressure because payroll can exceed 30% of operating expenses, and price sensitivity on platforms limits room for rate increases in the Malaysia hospitality market. Operators are deploying cross-training to enable multitasking, installing self-check-in kiosks, and reallocating service-charge pools to reduce the shock to take-home pay while managing staffing levels. Luxury and upper-upscale assets have more pricing latitude to protect margins, which creates a widening performance gap between tiers within the Malaysia hospitality market. Enforcement timelines and progressive wage policy discussions will shape the medium-term cost base for labour-intensive properties.

Slow Visa Processing for Emerging Markets Creates Friction Despite Liberalization Gains

Visa-free policies for China and India through the end of 2026 lower friction for two major sources, but applicants from other emerging markets can face uncertain processing windows that hinder short-notice travel. The Malaysia Digital Arrival Card is mandatory within three days before arrival for most foreign nationals, which adds an administrative step that some travellers find unfamiliar. Corporate planners evaluating regional conferences weigh visa predictability alongside venue quality, which can shift events if approval risk is high in the Malaysia hospitality market. Consistent embassy capacity during seasonal surges and clear guidance for documentation improve conversion of interest into bookings. The net effect is that headline liberalization helps top sources immediately, while smaller markets require channel education and lead-time management to secure demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Chain Hotels Leverage Standardized Systems to Capture Growth

Independent hotels held 63.32% of Malaysia's hospitality market share in 2025, while chain hotels are projected to grow at a 10.75% CAGR through 2031 as brand systems and loyalty scale distribution. The expansion of flags across Kuala Lumpur, Penang, and Johor improves access to corporate and MICE accounts that prize standardized service and rate predictability in the Malaysia hospitality market. Marriott’s milestone of 50 properties in September 2024 shows how a broad portfolio and loyalty program deepen weekday base business across cities. Hilton’s Southeast Asia signings underscore appetite for luxury and lifestyle keys that lift rate ceilings and drive brand-led demand. Independents defend niche positions through heritage assets and local immersion, but platform fees and wage cost inflation increase the appeal of conversions or soft-brand affiliations in the Malaysia hospitality market.

As chains grow within the Malaysia hospitality market, standardized procurement and revenue management unlock cost and yield benefits that are hard to match individually. Soft brands and collections offer a middle path that preserves identity while accessing global distribution and loyalty. IHG’s platform exemplifies how development-focused pathways enable owners to reflag and upgrade operations to contemporary standards. Over the forecast period, institutional capital remains attracted to asset-light models and branded operating platforms, which support the chain segment’s share gains in the Malaysia hospitality market. Independents that sharpen positioning and modernize distribution can maintain performance, especially in leisure-first destinations where character and location drive choice.

By Accommodation Class: Luxury Tier Outpaces Mid-Scale Through Premium ADR and Pipeline Depth

Mid and upper-mid-scale properties captured 43.37% in 2025, yet the luxury tier is projected to advance at a 13.74% CAGR through 2031 as flagship openings widen premium choice in the Malaysia hospitality market. Kuala Lumpur’s luxury ADR reached USD 183.52 (MYR 743.78) in peak 2024 months, and RevPAR hit USD 146.18 (MYR 592.45), which indicates headroom for rate without occupancy loss at the top end. Park Hyatt Kuala Lumpur’s 2025 debut at Merdeka 118 lifts the city’s ultra-luxury profile and anchors a cluster of high-end flags. The combination of premium product, wellness, and culinary programming further extends the length of stay for high-yield travellers within the Malaysia hospitality market.

Budget and economy operators face wage and distribution cost pressure, which pushes process efficiency and targeted upgrades to sustain rate integrity. Service apartments retain strong appeal with corporate relocations and medical travel because kitchens and laundry reduce trip friction for extended stays. ESG certifications and efficiency retrofits strengthen positioning at the upper tiers, where corporate buyers increasingly require documented sustainability in RFPs in the Malaysia hospitality market. The Malaysia hospitality market size in premium classes expands as pipeline assets open and create compression across events and peak periods.

By Booking Channel: Direct Digital Channels Gaining Ground Through AI and Loyalty Programs

OTAs accounted for 57.35% of bookings in 2025, while direct digital channels are projected to grow at a 15.73% CAGR. Hotels are enhancing AI webchat, best-rate guarantees, and loyalty-linked benefits to boost conversions. Chain platforms reduce acquisition costs and improve data collection by guiding repeat guests to owned channels through perks, apps, and points. Independent hotels focus on website upgrades, chat, and payment improvements to remain competitive and increase net Average Daily Rate (ADR). A balanced channel mix is becoming a strategic advantage. OTAs provide visibility, while owned channels enhance profitability. Operators using channel managers, dynamic pricing, and CRM systems can shift more repeat guests to direct bookings, increasing lifetime value. Improved content, speed, and checkout processes reduce friction and raise conversion rates. OTA share is expected to stabilize as direct booking capabilities mature, especially in city hotels with strong loyalty programs.

Corporate and MICE bookings provide weekday occupancy and additional Food & Beverage (F&B) and event revenue, stabilizing cash flows for city hotels. New luxury properties in Kuala Lumpur with large ballrooms and flexible spaces attract regional conferences and product launches. Sustainability-certified venues appeal to corporate clients with documented standards. Wholesale and traditional agents support group bookings from regions with limited online infrastructure, filling shoulder periods.Visit Malaysia 2026 boosts event calendars, favoring hotels with flexible meeting spaces and strong sales capabilities. Direct contracts with multinational firms ensure rate consistency and repeat events, reducing reliance on transient peaks. Investments in event technology and sustainable operations enhance competitiveness for high-value corporate bookings planned.

Geography Analysis

Central Malaysia held 49.37% of the market, supported by a strong luxury pipeline in the Golden Triangle and TRX financial district, reinforcing Kuala Lumpur’s premium status. Openings like Park Hyatt Kuala Lumpur and upcoming brands such as Waldorf Astoria and Conrad Kuala Lumpur enhance corporate and high-yield leisure appeal. Increased room supply highlights the need for efficiency retrofits and municipal upgrades to maintain guest satisfaction. Improved connectivity between airport arrivals and city/intercity rail services helps disperse visitors to nearby hubs.

Northern Malaysia expands its supply, led by Penang’s room inventory and pipeline catering to leisure, culinary, and corporate demand. Mixed-use developments on Gurney Drive, including hotels and executive apartments, support longer stays. Langkawi’s updated resort pipeline boosts its international appeal for premium beach tourism. Secondary cities like Ipoh add branded inventory to capture corporate and leisure demand, diversifying flagged supply. Effective traffic and transit planning in George Town and coastal areas is crucial to avoid congestion.

Southern Malaysia benefits from the RTS Link, reducing Johor Bahru–Singapore travel time and increasing cross-border traffic for transit-proximate hotels. Developers focus on reflags and conversions, while Melaka combines heritage with lifestyle concepts to attract younger travelers. The ECRL reduces Gombak–Kota Bharu travel time, enabling year-round tourism to beach and nature destinations. East Malaysia sees rapid growth with new branded supply in Kota Kinabalu and sustainability-focused repositioning in Miri. Infrastructure upgrades and self-sufficiency systems are vital in areas with electricity and water challenges.

Regulatory Landscape

Malaysia hospitality is governed primarily under the Tourism Industry Act 1992 (Act 482) and related subsidiary regulations, which cover licensing and oversight of tourism businesses. MOTAC also administers frameworks for tourist accommodation premises registration, classification, and rating. Licensing and industry interactions are increasingly digitized through the TOURLIST platform (Malaysia.gov.my), which is used for tourism license applications and renewals, including hotel grading-related processes and other tourism permits. This approach tightens traceability of compliance for operators.

Policy emphasis in 2026 has been placed on service quality and standards ahead of Visit Malaysia 2026, with MOTAC publicly directing four and five-star hotels to strengthen accountability, operational standards, and refurbishment discipline. MOTAC also confirmed it is reviewing the feasibility of standardizing hotel check-in and check-out hours via local council licensing conditions, which would affect operating policies for accommodation providers if adopted. On the fiscal and compliance side, the Tourism Tax (TTx) regime under the Tourism Tax Act 2017 remains active, with enforcement guided by the Tourism Tax (Rate of Tax) Order 2025 and related public rulings referenced through mid-2026.

Value Chain Analysis

Malaysia's hospitality value chain starts with policy, licensing, and destination marketing led by MOTAC and Tourism Malaysia, which coordinate campaign programming, overseas promotions, and industry engagement to drive demand (notably under the Tourism Malaysia Marketing Plan 2022-2026 and Visit Malaysia 2026 execution). Demand then flows into travel trade intermediaries (tour operators and travel agencies regulated under the Tourism Industry Act 1992), OTAs and direct digital channels, airlines and ground transport connectors, and finally into accommodation operators across independent and chain hotels that monetize stays through rooms, meetings, and F&B.

On the supply side, owners and developers procure design and fit-out, technology systems, furnishings, and operational labor, then contract hotel management and brand systems where relevant to access loyalty and distribution. Partnerships between Tourism Malaysia and large operators, such as its strategic collaboration with Sunway Hospitality Group, show how marketing, loyalty ecosystems, and joint sales missions connect upstream destination selling to downstream room inventory conversion. Key friction points include labor-cost inflation following the 2025 minimum wage increase and distribution economics where OTA commissions pressure independent operators, which is accelerating adoption of property tech, channel managers, and direct booking capabilities to protect net ADR and margins.

Competitive Landscape

The Malaysia hospitality market is moderately concentrated in key urban areas, with international chains competing for prime locations and independent operators dominating secondary cities and resort destinations. Marriott's 50-property portfolio highlights the benefits of brand distribution and loyalty programs in attracting repeat bookings. Hilton's addition of nearly 4,000 luxury and lifestyle rooms across Southeast Asia reflects investment in premium segments, enhancing pricing potential. IHG's strategy of property conversions preserves local character while meeting global standards, offering owners opportunities to improve operations and access loyalty-driven demand.

Transit-oriented developments near RTS stations in Johor Bahru and ECRL stations on the East Coast create opportunities for mid-upscale business hotels and wellness retreats. In Kuala Lumpur, Park Hyatt’s opening at Merdeka 118 is set to elevate luxury standards, complementing the premium ecosystem of TRX and KLCC. ESG initiatives and certifications are increasingly vital, helping hotels secure corporate RFPs, access green financing, and reduce utility costs, enhancing competitiveness.

Operational excellence and channel strategies are critical as costs rise and demand shifts. Chain-affiliated hotels use loyalty programs, mobile apps, and data-driven pricing to optimize ADR and occupancy. Independent hotels focus on local positioning, reputation management, and direct bookings to maintain rates and reduce platform fees. Technology investments, such as digital keys and self-check-in, improve guest satisfaction and staff efficiency. Properties integrating sustainability, digital capabilities, and strong commercial strategies are expected to outperform as the market grows.

Malaysia Hospitality Industry Leaders

Marriott International

Hilton Worldwide

Accor

InterContinental Hotels Group (IHG)

Shangri-La Hotels and Resorts

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Transit-linked hotel and mixed-use development along the RTS Link and ECRL corridors remains a clear whitespace. These projects reposition Johor Bahru and East Coast nodes into practical short-stay and weekend markets, while also supporting corporate and leisure dispersion beyond Kuala Lumpur. The opportunity is reinforced by ongoing capacity and brand moves outside the core, including IHG signing a 350-key Kimpton Kota Kinabalu, Hilton opening Hilton Burau Bay Langkawi Resort, and YTL Hotels scheduling a JW Marriott in Johor Bahru, which point to active owner and operator appetite to add upper-upscale supply in secondary gateways.

Service-quality and product-upgrade programs tied to Visit Malaysia 2026 create room for operators to differentiate through standardized guest experience, refurbishment cycles, and sustainability positioning aligned with corporate and high-yield leisure demand. Investment-led repositioning includes Tropicana partnering with Accor on the RM1.06 billion Mercure Living Genting Highlands project and iKHASAS Group committing RM90 million to expand ibis Styles Sepang KLIA capacity, while MOTACs Mesra Malaysia campaign adds an official push for consistent frontline standards. With OTAs still the largest booking channel, operators also have a defined margin-improvement pathway through direct digital capability upgrades (AI-enabled service tools, integrated reservations, and loyalty-driven conversion), supported by sector-focused initiatives such as Unifi Business offerings for hospitality connectivity and guest experience systems.

Recent Industry Developments

- July 2026: ECM Libra Group announced a joint venture with TP Real Estate Holdings, taking a 50% stake in Ormond Group and signing management contracts for The RuMa Hotel and Residences and Ormond Hotel Sandakan. The move pairs a capital partnership with operating control, supporting refurbishment and performance optimization while expanding Ormond's managed footprint in both Kuala Lumpur and East Malaysia.

- May 2026: AMTD Group completed the acquisition of Upper View Regalia Hotel in Kuala Lumpur for about USD 38 million. The transaction highlights continued inbound capital interest in KL hotel assets, supporting repositioning and potential brand or service upgrades to capture higher-yield demand.

- August 2025: Hyatt Hotels Corporation opened Park Hyatt Kuala Lumpur at Merdeka 118, marking Hyatt's entry into Malaysia with a flagship luxury property. The opening raises the benchmark for ultra-luxury supply in Kuala Lumpur and strengthens the city's appeal for high-net-worth leisure travelers and premium corporate accounts.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Malaysia hospitality market is treated as spending tied to paid accommodation stays, covering hotels, resorts, and serviced apartments that serve domestic and international travelers across the country.

Scope exclusions: We exclude standalone foodservice and attractions, and we also avoid counting informal home-stays and most peer-to-peer short-term rentals unless they operate as serviced accommodation.

Segmentation Overview

- By Type

- Chain Hotels

- Independent Hotels

- By Accommodation Class

- Luxury

- Mid & Upper-Mid-scale

- Budget & Economy

- Service Apartments

- By Booking Channel

- Direct Digital

- OTAs

- Corporate / MICE

- Wholesale & Traditional Agents

- By Geographic Region

- Central (Kuala Lumpur, Selangor, Putrajaya)

- Northern (Penang, Kedah, Perlis, Perak)

- Southern (Johor, Melaka, Negeri Sembilan)

- East Coast (Pahang, Terengganu, Kelantan)

- East Malaysia (Sabah, Sarawak, Labuan)

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the demand context and to anchor the model with observable travel and lodging signals. We leaned on public sources such as Tourism Malaysia visitor statistics, Department of Statistics Malaysia releases, Bank Negara Malaysia macro series, World Bank indicators, and UNWTO tourism dashboards, along with airport and port authority traffic disclosures where relevant.

To translate activity into value, we also reviewed hotel supply and operating indicators from open association publications and reputable press coverage, plus company filings and investor presentations for larger listed groups with Malaysia exposure. A paid subscription for company financials and news was used selectively to validate revenue direction and major expansions, and patent databases were checked only when technology changes could alter operating economics. These desk sources are illustrative, and many other public and paid references were also used for cross-checking, clarification, and validation.

Primary Interviews and Surveys

Primary work focused on verifying what is actually being sold in the market and how pricing and occupancy moved by season and location. We spoke with accommodation operators, property managers, booking channel participants, and travel buyers, and coverage was balanced across key Malaysian travel corridors and demand types (leisure, business, and MICE) so assumptions from desk findings could be adjusted where needed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 12% | |

| Mid tier: 55% | Functional/Unit leaders: 36% | |

| Smaller Players: 16% | Managers: 52% |

Market-Sizing & Forecasting

Market sizing was built using a top-down demand pool reconstruction, where travel arrivals and domestic trip activity are translated into room nights and then valued through observed room rates, occupancy patterns, and mix by property class. Once the national total was established, it was distributed across Malaysia regions using supply indicators like room inventory and openings, and then checked against channel and operator feedback.

To keep results grounded, bottom-up approximations were used as a control rather than the main build. This included sampled property revenue per available room logic, a roll-up of representative capacity additions, and channel checks on booking mix between direct and online agents. When coverage gaps appeared (for example, smaller independent properties with limited disclosure), assumptions were filled using interview ranges and then stress-tested against tourism and macro signals.

For forecasting, we used scenario analysis supported by exponential smoothing on key time series, with drivers such as international arrivals, domestic travel intensity, airline seat capacity trends, ADR progression, and occupancy normalization. The final trajectory was adjusted only after these drivers were aligned with what interviewees expected for recovery pace, event calendars, and investment timing.

Data Validation & Update Cycle

Outputs were validated through multiple checks so that no single data point could overly influence the market value. We compared modeled totals against independent signals such as tourism receipts direction, accommodation performance indicators, and disclosed revenue trends from major operators, and any large variance was reviewed before sign-off.

If an anomaly appeared, assumptions were re-tested and targeted re-contacts were triggered to confirm whether the change was real or a data artifact. The report is refreshed annually, and interim updates are made when material events occur, such as policy shifts, major capacity additions, or demand shocks. Before delivery, a final pass is completed so clients receive an updated view aligned to the latest available indicators.

Mordor Intelligence's Malaysia Hospitality Market Size Compared Against Other Published Estimates

Published market sizes for Malaysia hospitality can look far apart because each publisher draws the line around what counts as hospitality revenue, and because base years and currency choices are not always consistent. The table below summarizes that spread using the closest comparable years that were publicly visible.

The benchmark table shows a higher value mainly when the scope is limited to paid accommodation services and valued through room-night and rate based modeling, and in Mordor Intelligence's model, standalone foodservice and wider travel experiences are kept out even if they sit within a broader tourism spend narrative.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 49.28 B (2025) | |

| Global Advisory A | USD 1.31 B (2024) | This estimate appears to use a narrower revenue pool and may mix hospitality categories without clearly scaling room-night demand, which can understate lodging value when ADR and occupancy are rising. |

| Industry Data Publisher B | USD 16.88 B (2024) | This figure is presented as revenue for short-term accommodation under an industry classification, which can exclude parts of organized hotels and resorts coverage, and it does not clearly state how pricing mix and class-level upgrades are treated. |

Taken together, the comparison points to scope and value conversion as the main drivers of the differences, rather than a single right or wrong number. By tying the total to room-night demand, observable rate trends, and interview-checked booking and class mix, we keep the result traceable to clear steps that can be repeated as new travel data comes in.

Key Questions Answered in the Report

What is the Malaysia hospitality market outlook to 2031?

The Malaysia hospitality market size is USD 53.11 billion in 2026 and is projected to reach USD 77.20 billion by 2031 at a 7.76% CAGR, supported by tourism promotion and transport upgrades.

Which segments lead by type and class in the Malaysia hospitality market?

Independent hotels led with 63.32% in 2025, and chain hotels posted a 10.75% CAGR, while mid and upper-mid-scale held 43.37% and the luxury tier advances at 13.74% CAGR.

How are connectivity projects shaping demand in the Malaysia hospitality market?

The Rapid Transit System Link (RTS Link) and ECRL East Coast Rail Link (ECRL) reduce travel times and improve dispersal to Johor and the East Coast, which expands short-stay and leisure flows into secondary cities.

How are hotels shifting bookings away from OTAs in the Malaysia hospitality market?

Operators build direct digital with AI webchat, best-rate guarantees, and loyalty perks to improve conversion and lower acquisition costs versus third-party platforms.

Which regions are positioned to outperform within the Malaysia hospitality market?

East Malaysia is set to grow fastest, while Central Malaysia maintains the largest share due to premium openings and a strong MICE ecosystem.

How will higher wages affect operators in the Malaysia hospitality market?

The minimum wage at USD 419.46 (MYR 1,700) per month raises labour costs, which encourages cross-training, automation, and channel optimization to protect margins.

Page last updated on: