Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

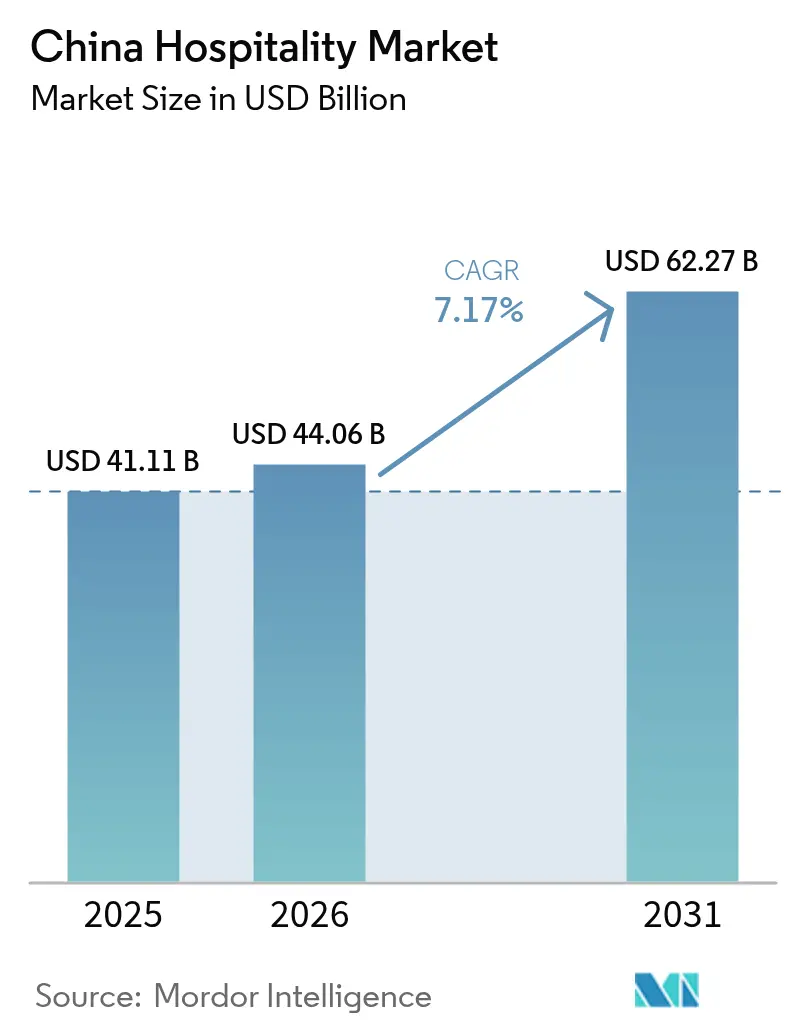

| Base Year Market Size (2025) | USD 41.11 Billion |

| Market Size (2026) | USD 44.06 Billion |

| Market Size (2031) | USD 62.27 Billion |

| Growth Rate (2026 - 2031) | 7.17% CAGR |

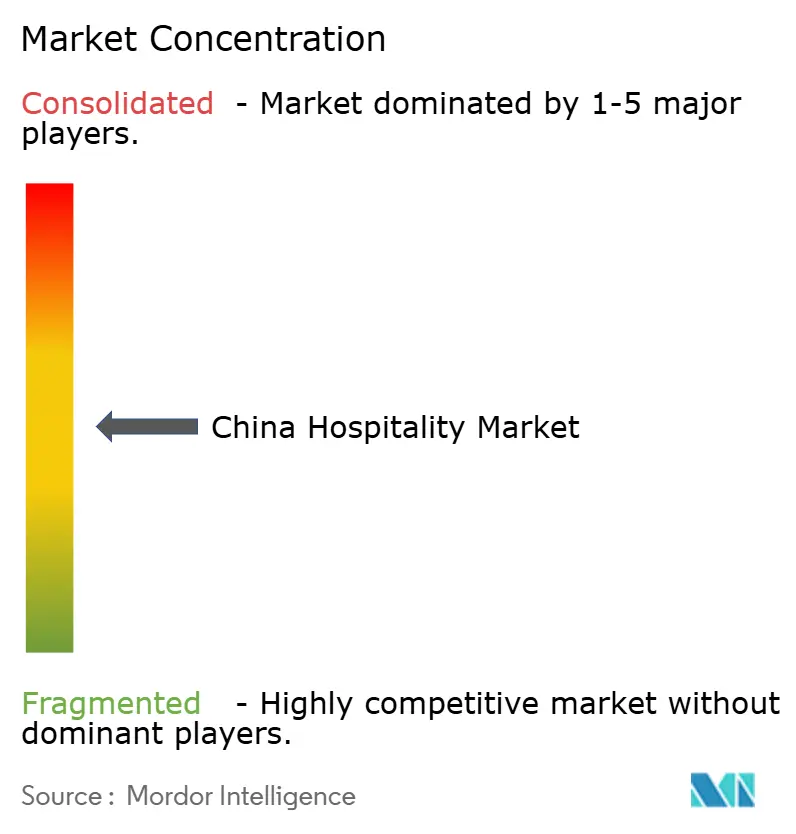

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Hospitality Market Analysis by Mordor Intelligence

The China Hospitality market size is expected to grow from USD 41.11 billion in 2025 to USD 44.06 billion in 2026 and is forecast to reach USD 62.27 billion by 2031 at 7.17% CAGR over 2026-2031.

This trajectory is underpinned by robust domestic leisure demand, rapid high-speed rail expansion, and government programs that promote night-time spending. Chain hotel expansion, service-apartment momentum, and smart-hotel technology gains are reinforcing profitability across property classes. Operators are also benefiting from structured cultural-tourism subsidies that stimulate regional travel, even as land-lease inflation and OTA commission pressure temper margins. Private-sector investments remain strong because loyalty programs, cost-saving automation, and experiential positioning are creating durable competitive moats. The sector's expansion aligns with China's broader economic recovery, where domestic tourism reached 2.725 billion trips in the first half of 2024, representing a 14.3% year-over-year increase[1]China Daily staff, “Hilton Expedites Expansion in China with Long-Term Market Optimism,” China Daily, chinadailyhk.com.

Key Report Takeaways

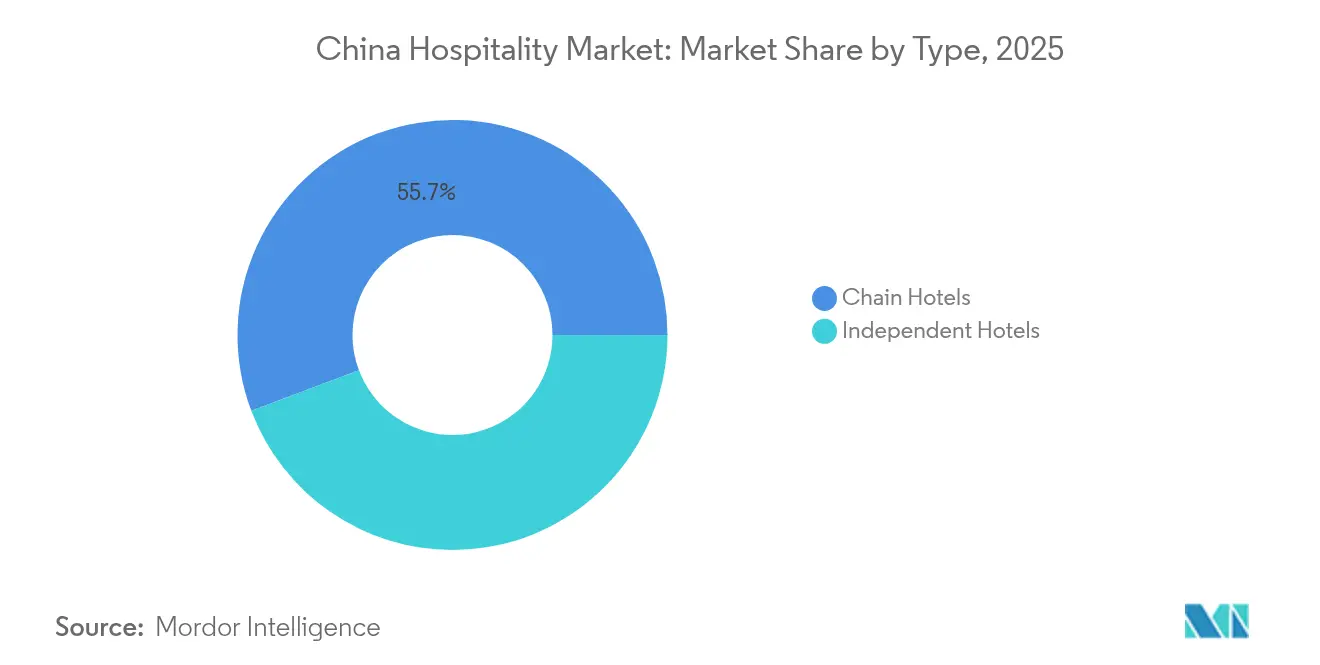

- By type, chain hotels captured 55.74% of the China hospitality market share in 2025, and are also projected to remain the fastest-growing sub-segment with a CAGR of 7.95% from 2026 to 2031.

- By accommodation class, mid & upper-mid-scale properties accounted for 29.86% of the China hospitality market share in 2025, while service apartments are expected to expand the fastest with a CAGR of 10.62% during 2026–2031.

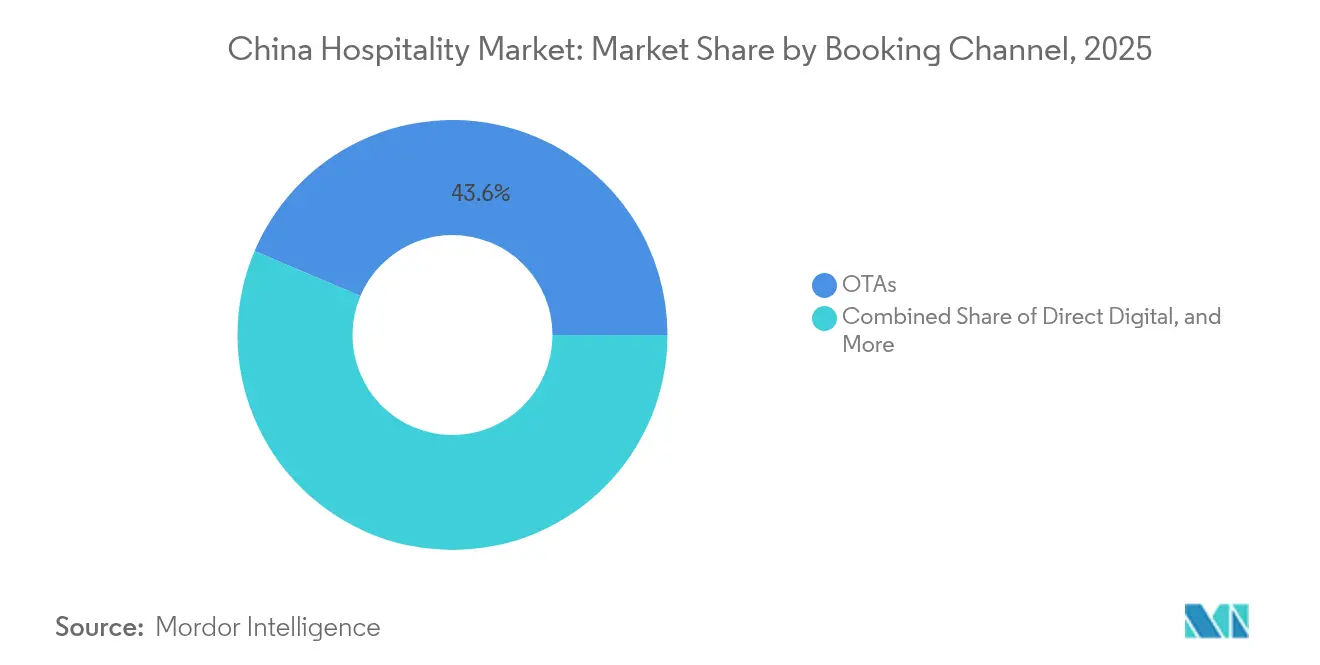

- By booking channel, OTAs represented 43.62% of the China hospitality market size in 2025, but direct digital platforms are forecasted to grow the fastest with a CAGR of 11.90% between 2026 and 2031.

- By geographic region, East China contributed 25.98% of the China hospitality market share in 2025, whereas South-Central China is anticipated to post the fastest growth with a CAGR of 10.88% in the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Hospitality Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic domestic leisure boom | +1.8% | National; strongest in tier-2 and tier-3 cities | Short term (≤ 2 years) |

| High-speed rail expanding weekend trips | +1.2% | East, South-Central, Southwest | Medium term (2-4 years) |

| Government push for night-time economy | +0.9% | Tier-1 cities, provincial capitals | Medium term (2-4 years) |

| Gen-Z demand for experiential stays | +0.7% | Urban centers, tourist hubs | Long term (≥ 4 years) |

| Smart-hotel tech cost savings | +0.5% | Chain hotels in major cities | Medium term (2-4 years) |

| Low-carbon certification as booking filter | +0.3% | Corporate segments, tier-1 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-pandemic Domestic Leisure Boom

Pent-up demand after border restrictions lifted ignited a sharp rebound in weekend and short-haul trips that has lifted occupancy across all lodging tiers. Domestic tourism revenue rose to CNY 4.91 trillion (USD 673 billio) in 2024, a 140.3% jump from 2023, and trip volume recovered to 81.44% of pre-pandemic levels. Service spending has been expanding twice as fast as goods purchases, confirming a durable experiential shift that favors properties with differentiated leisure offerings. Mid-scale and boutique hotels are capturing outsized gains because travelers prioritize unique settings and local immersion. Government cultural-tourism subsidies have magnified the surge by lowering barriers to off-peak travel. These demand characteristics make the China hospitality market unusually resilient against macro headwinds.

High-speed Rail Expanding Weekend Trips

China’s 50,000-kilometer HSR grid compresses travel times between mega-cities and secondary markets, adding more than 3.4 million incremental tourists per connected city[2]Research Team, “High-Speed Railway and City Tourism in China: A Quasi-Experimental Study on HSR Operation,” Sustainability, mdpi.com.. The Yangtze River Delta exemplifies the effect: inter-city travel times have fallen by about 50%, enabling two-night excursions that once required extra vacation days. Boutique and mid-scale hotels in regional clusters now draw demand once limited to primary urban cores. Occupancy uplift is strongest where rail stations sit near cultural landmarks, and many properties are realigning marketing calendars around rail-timetable peaks. The connectivity advantage supports a hub-and-spoke tourism pattern that spreads the benefits of the China hospitality market beyond coastal cities.

Government Push for Night-time Economy

Ministry designations have created 102 National Night Culture and Tourism Consumption Agglomeration Zones that welcomed 3.12 billion evening visitors in 2024[3]Editorial Board, “New Zones Help Push Nighttime Economy,” China Daily, chinadaily.com.cn.. Local authorities have extended transit hours, relaxed outdoor-dining permits, and introduced light-show festivals that lengthen dwell time in urban cores. Hotels positioned near these entertainment clusters report higher food-and-beverage revenue, stronger shoulder-night occupancy, and increased average length of stay. Sichuan’s model demonstrates the scale potential, with nighttime spending representing 50.8% of total consumption. Integration of cultural arts with retail and dining reinforces pricing power for lifestyle properties and elevates RevPAR even in competitive Tier-1 markets.

Gen-Z Demand for Experiential Stays

Travelers born after 1995 represent nearly 60% of arrivals to destinations such as Hainan. They value authenticity, social-media shareability, and wellness amenities more than legacy star ratings, which steers demand toward boutique and lifestyle formats. Properties that curate local art, culinary workshops, and sustainable practices command rate premiums and enjoy stronger loyalty. Instagrammable design elements and tech-enabled service touchpoints converge to form a competitive moat that shields rate integrity during low-season periods. This generational preference will underpin above-average growth for the China hospitality market well beyond 2030.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Land-lease cost inflation | -1.1% | Tier-1 cities, major tourist destinations | Medium term (2-4 years) |

| OTA marketing fee escalation | -0.8% | Independent hotels, smaller chains | Short term (≤ 2 years) |

| Rising labor shortages in Tier-1 cities | -0.6% | Beijing, Shanghai, Shenzhen, Guangzhou | Medium term (2-4 years) |

| Persistent local COVID-19 flare-up risk | -0.4% | Border regions, gateway cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Land-lease Cost Inflation

Urban land auction prices have created significant cost pressures for new hotel development, particularly in tier-1 cities where commercial real estate values have outpaced revenue growth potential. The commercial real estate market has experienced absorption pressure and downward rent adjustments in office segments, though hospitality assets in prime locations continue to command premium valuations[4] CBRE Research, “2024 China Real Estate Market Outlook Mid-Year Review,” CBRE, cbre.com.cn.. Rising land costs have shifted investment patterns toward renovation and repositioning of existing assets rather than ground-up development, as investors seek to optimize returns within constrained cost structures. This dynamic has particularly impacted independent hotel operators and smaller chains that lack the scale advantages of major groups in securing favorable lease terms. Overall, land-lease inflation weighs on pipeline diversity and slows supply growth in the densest nodes of the China hospitality market.

OTA Marketing Fee Escalation

Dominance of top booking platforms has enabled commission increases that squeeze hotel margins; smaller properties pay the highest effective rates relative to ADR. While domestic OTA commissions remain lower than global peers, dependency risk is rising because direct-booking infrastructure at many independent hotels is still underdeveloped. Loyalty programs and first-party mobile apps are mitigating exposure, but adoption requires technology spend that smaller chains cannot easily finance. Hotels are responding through technology investments in customer relationship management and loyalty programs to reduce channel dependency, though the transition requires significant upfront investment and operational restructuring. The trend toward higher commission rates reflects the broader digital transformation of travel booking, where platform economics favor aggregators over individual suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Chain Hotels Continue Consolidation Momentum

Chain hotels accounted for 55.74% of the China hospitality market share in 2025, underscoring a rising chainization rate that hit 40.95% by year-end. The cohort is expected to post an 7.95% CAGR to 2031 as franchise signings dominate new supply pipelines. The China hospitality market size attached to chain operations is therefore set to expand faster than that of independents, supported by loyalty ecosystems that funnel direct traffic and reduce OTA reliance.

Rapid roll-outs by H World Group and Jin Jiang are demonstrating the scalability of asset-light models, while occupancy levels above 80% signal strong brand equity. Independent operators continue to lose negotiating leverage on procurement and digital distribution, accelerating buy-out or conversion prospects. Technology scale, combined with membership data, gifts chains superior revenue-management precision, which further enlarges market-share gaps.

By Accommodation Class: Service Apartments Capture Extended-Stay Demand

Service apartments are the fastest-growing class, forecast at an 10.62% CAGR through 2031, a pace that outstrips every other lodging format in the China hospitality market. International brands such as Ascott have already surpassed 12,000 units locally, aligning stock with sustained corporate-relocation flows and digital nomad preferences. Mid- and upper-mid-scale hotels nonetheless hold the largest slice at 29.86% of the China hospitality market size, propelled by the spending power of an expanding middle class.

Luxury resorts exhibit resilient ADR, especially in Sanya and Chengdu-Chongqing mountain clusters where affluent Gen-Z and millennial travelers seek immersive wellness escapes. Budget and economy hotels face margin compression from wage escalation and utility costs; however, they remain critical for price-sensitive migrant labor and tier-3 demand. Regulatory leniency toward mixed-use zoning is smoothing the pipeline for new service-apartment supply, suggesting continued share gains.

By Booking Channel: Direct Digital Gains Against OTA Dominance

OTAs represented 43.62% of 2025 bookings, yet direct digital platforms are slated to grow 11.90% CAGR through 2031 as hotels elevate CRM and mobile app investments. Elevated China hospitality market size projections for direct sales correlate with rising loyalty-member enrollment; H World’s H Rewards surpassed 267 million subscribers, contributing high-margin transactions.

Trip.com’s robust revenue underscores OTA staying power, but commission sensitivity is prompting chains to sweeten direct-booking perks such as late checkout and member-only rates. Corporate and MICE channels have rebounded strongly, with business-travel spend projected at USD 211 billion, steering companies toward negotiated-rate platforms that bypass OTA tolls. Wholesale agents continue to erode as leisure group organizers pivot toward online aggregators.

Geography Analysis

East China dominates the market with 25.98% due to unrivaled infrastructure, a concentration of multinational headquarters, and iconic attractions from the Bund to West Lake. High-speed rail lines knit Shanghai, Hangzhou, and Nanjing into a two-hour tourism corridor that supports both leisure and meetings demand. Global brands prefer the region for first entries, evidenced by Marriott’s record 161 deal signings, many clustered in the delta. Elevated land prices and fierce competition compress margins for operators lacking differentiated brand propositions.

South-Central China is growing at the fastest CAGR with 10.88% of China hospitality market, powered by Hainan’s visa-free access and duty-free policy that lifted international bookings more than 200% year-over-year. Guangdong contributes resilient corporate demand and hotel pipeline depth, while Hunan leverages cultural-heritage circuits to stretch average length of stay. The region receives substantial public investment targeting integrated cultural and tourism zones, thereby amplifying room-night generation across multiple provinces.

Southwest China is transitioning from emerging to established destination status as Chengdu-Chongqing co-development reshapes western tourism economics. Luxury supply is scaling quickly; the Anantara Xiling Snow Mountain resort opening in 2025 underlines upscale positioning that taps the winter-sports and wellness niches. Yunnan’s top-100 county rankings confirm grassroots cultural-tourism momentum, yet infrastructural gaps and talent shortages still cap operating efficiency. North China, Northeast China, and Northwest China remain strategically relevant to government travel and heritage tourism, though slower GDP growth and population migration weigh on RevPAR trajectories.

Competitive Landscape

China’s hospitality sector remains moderately concentrated, with leading companies having a significant share of the market. Major players like Jin Jiang and Huazhu continue to strengthen their foothold through asset-light strategies, relying heavily on franchise and management contracts. In fact, franchise agreements made up 73% of hotel signings in 2024, reflecting a clear industry preference for capital-efficient growth. These models allow operators to scale rapidly while maintaining balance sheet flexibility. As competition intensifies, consolidation through acquisition and franchise partnerships is expected to accelerate.

Technology is becoming a key differentiator in determining profitability and market leadership across China’s hotel landscape. Early adopters of smart-hotel infrastructure are seeing 3–5 percentage point gains in gross operating profit margins, driven by automation, energy efficiency, and labor optimization. Brand loyalty ecosystems are also proving critical; platforms like H World’s H Rewards and Marriott Bonvoy are boosting occupancy while lowering customer acquisition costs by reducing reliance on OTAs. This creates a more resilient and margin-friendly revenue model. As technology continues to evolve, the performance gap between digitally advanced operators and legacy models is likely to widen.

Opportunities for growth are increasingly concentrated in China’s tier-3 and tier-4 cities, where branded chain penetration remains under 25%. Serviced apartments are a standout performer, growing at an 11.13% CAGR between 2025 and 2030, as they meet the extended-stay demand that traditional hotels often overlook. Companies like Ascott Limited are aggressively expanding in this space, capitalizing on unmet needs in secondary markets. Meanwhile, tighter regulations on service quality and operational compliance are placing pressure on independent operators, many of whom lack the resources to adapt. This dynamic is shifting market share toward scaled players with the systems and capital to navigate regulatory and operational complexity.

China Hospitality Industry Leaders

Jin Jiang International

Huazhu Group

BTG Homeinns

Dossen International

GreenTree Hospitality

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Minor Hotels set October 2025 for Anantara Xiling Snow Mountain Chengdu Resort debut with 111 rooms targeting luxury ski and wellness segments.

- February 2025: Marriott International recorded 161 new-build deals in Greater China during 2024, adding nearly 31,000 rooms and lifting luxury signings 73%.

- December 2024: Marriott and Delonix Group signed eight agreements to expand Tribute Portfolio across Mainland China, targeting 100 properties long term.

- October 2024: Ascott China and Jin Jiang created a 50:50 venture to propel asset-light roll-outs of Quest and Tulip Lodj apartment hotels nationwide.

China Hospitality Market Report Scope

A complete background analysis of the hospitality industry in China, which includes an assessment of the industry associations, overall economy, and emerging market trends based on segments, significant changes in the market dynamics, and the market overview, is covered in the report. The report offers market size and forecasts for the Hospitality Industry in China in value (USD Billion) for all the above segments.

The report on Hospitality Industry in China is segmented by Type (Chain Hotels and Independent Hotels) and Segment (Service Apartments, Budget and Economy Hotels, Mid and Upper Mid-scale Hotels, and Luxury Hotels).

By Type

| Chain Hotels |

| Independent Hotels |

By Accommodation Class

| Luxury |

| Mid & Upper-Mid-scale |

| Budget & Economy |

| Service Apartments |

By Booking Channel

| Direct Digital |

| OTAs |

| Corporate / MICE |

| Wholesale & Traditional Agents |

By Geographic Region

| North China |

| Northeast China |

| East China |

| South-Central China |

| Southwest China |

| Northwest China |

| Hong Kong & Macau |

| Taiwan |

| By Type | Chain Hotels |

| Independent Hotels | |

| By Accommodation Class | Luxury |

| Mid & Upper-Mid-scale | |

| Budget & Economy | |

| Service Apartments | |

| By Booking Channel | Direct Digital |

| OTAs | |

| Corporate / MICE | |

| Wholesale & Traditional Agents | |

| By Geographic Region | North China |

| Northeast China | |

| East China | |

| South-Central China | |

| Southwest China | |

| Northwest China | |

| Hong Kong & Macau | |

| Taiwan |

Key Questions Answered in the Report

What is the 2026 value of the China hospitality market?

The China hospitality market size stood at USD 44.06 billion in 2026.

What CAGR is forecast for China’s hospitality sector through 2031?

A 7.17% CAGR is projected over the 2026-2031 period.

Which accommodation class is growing fastest?

Service apartments lead with an 10.62% CAGR forecast.

Which region is expected to grow the quickest?

South-Central China is slated for an 10.88% CAGR through 2031.

Which is the dominating segment by type in China hospitality market?

The Chain Hotels is the dominating segment by 55.74% share of the market.

Page last updated on: