Market Overview

| Study Period | 2020 - 2031 |

|---|---|

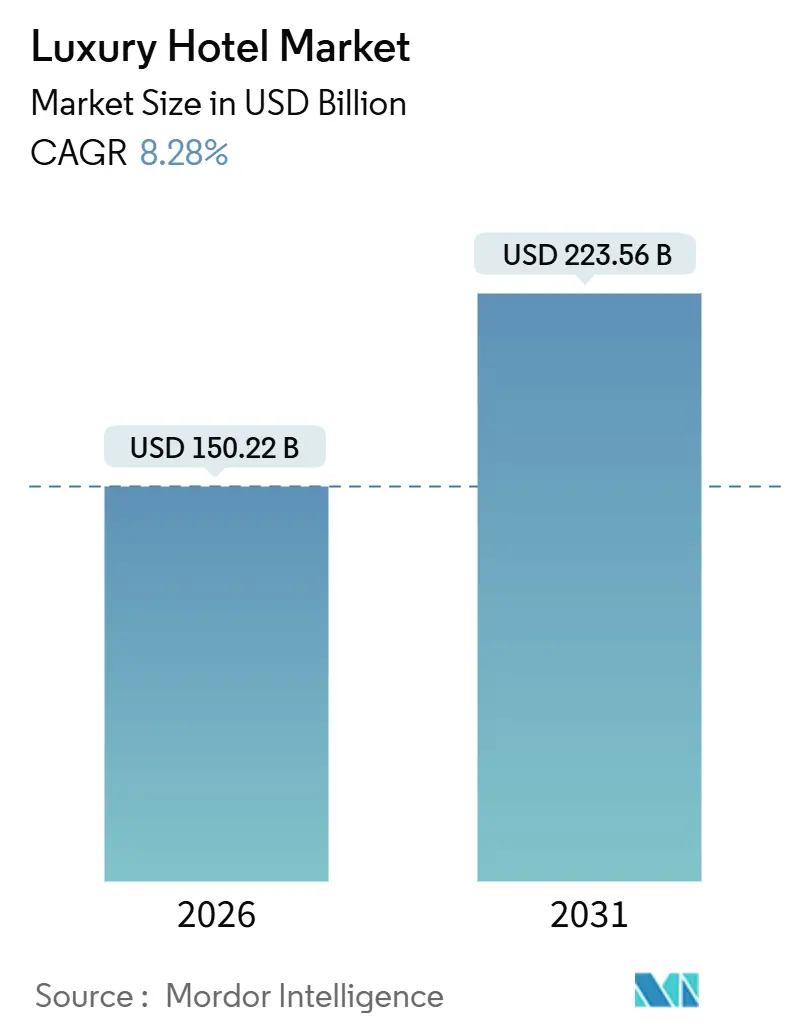

| Market Size (2026) | USD 150.22 Billion |

| Market Size (2031) | USD 223.56 Billion |

| Growth Rate (2026 - 2031) | 8.28% CAGR |

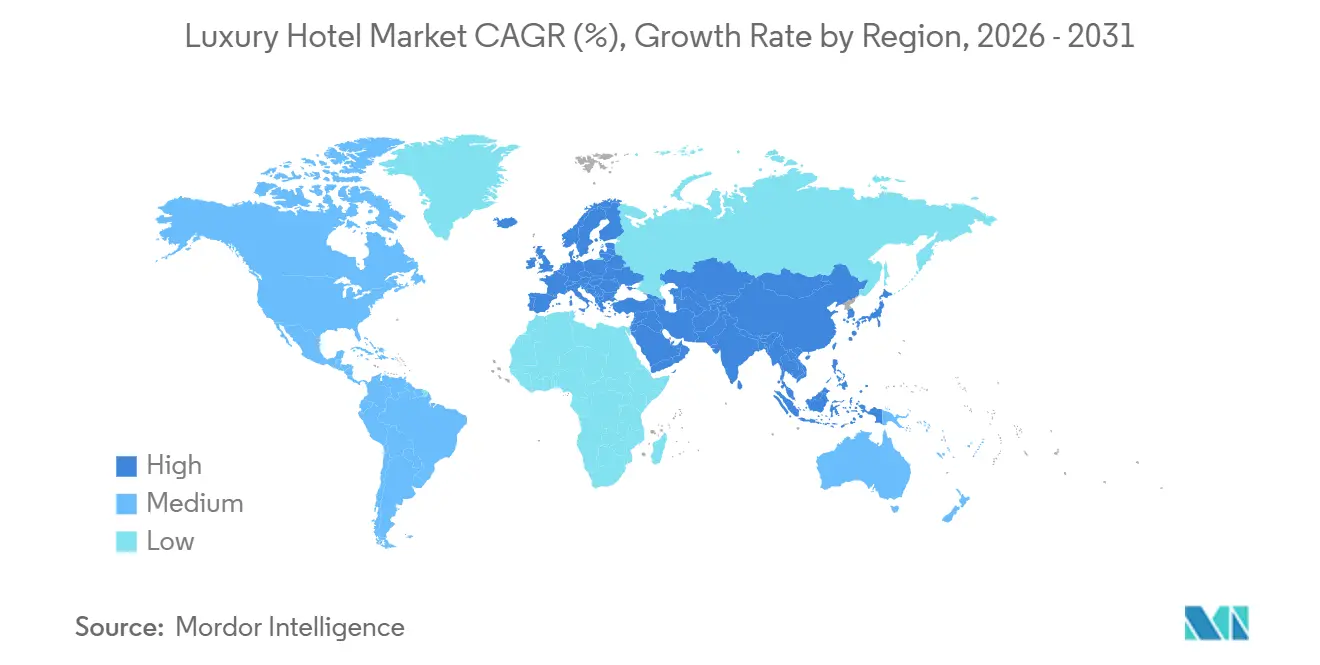

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Luxury Hotel Market Analysis by Mordor Intelligence

The luxury hotel market size is USD 150.22 billion in 2026 and is projected to reach USD 223.56 billion by 2031, reflecting an 8.28% CAGR over the forecast period. Momentum builds as high-end travel continues to scale on the back of steady international arrivals, renewed corporate budgets, and wider adoption of experiential and wellness-led itineraries that sustain rate power in both urban and resort settings. Operators enhance digital touchpoints around discovery, booking, and in-stay personalization, while aligning with procurement preferences that favor verifiable sustainability credentials and third-party certifications. The recovery in international travel is broad-based, with Europe welcoming 625 million tourists through September 2025 and Asia-Pacific reaching 90% of its 2019 baseline, which sustains occupancy and mix in key destinations and supports the rate-led strength now visible in upscale and luxury categories.[1]Source: UN Tourism, “International Tourist Arrivals Up 5% in the First Nine Months of 2025,” UN Tourism, untourism.int Certification programs such as LEED and Green Key continue to expand across upscale portfolios, giving certified properties procurement advantages, efficiency benefits, and reputational gains that reinforce competitive positioning in the luxury hotel market.

Key Report Takeaways

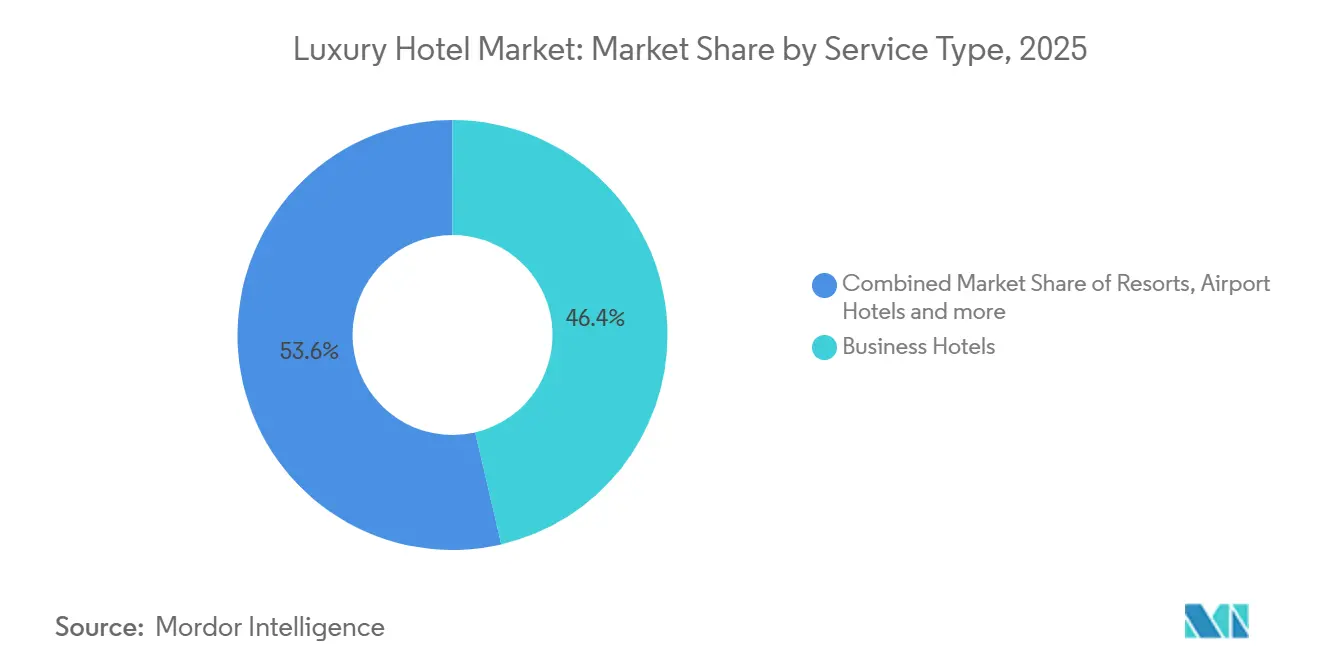

- By service type, Business Hotels led with 46.36% of the luxury hotel market share in 2025, while resorts are forecast to expand at a 13.47% CAGR through 2031.

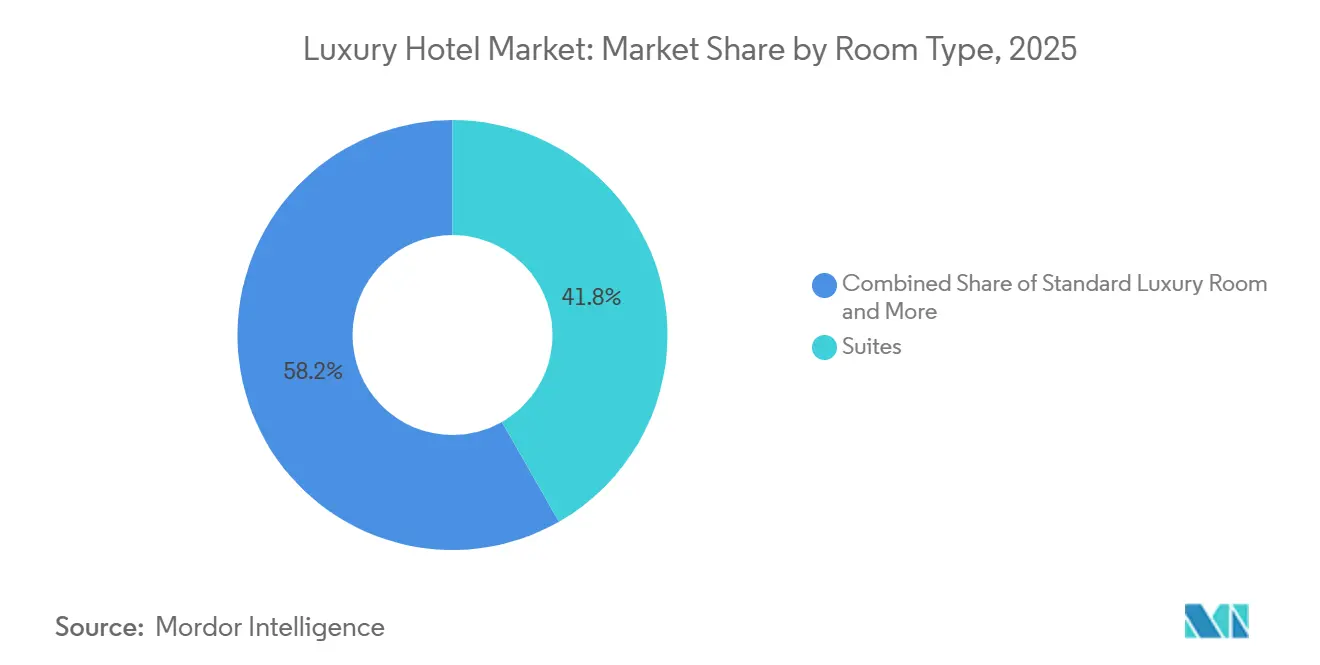

- By room type, Suites accounted for 41.76% of the luxury hotel market share in 2025, and villas/bungalows are projected to grow at an 11.74% CAGR through 2031.

- By booking channel, direct booking captured 43.75% of reservations in 2025, whereas online travel agencies are projected to record a 13.78% CAGR to 2031.

- By geography, Europe held 37.38% of the luxury hotel market share in 2025, with Asia-Pacific expected to post the fastest regional CAGR at 11.43% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Luxury Hotel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rebound of international tourism post-pandemic | +2.3% | Global, strongest in Europe and Asia-Pacific, with the Middle East ahead of 2019 | Medium term (2-4 years) |

| Rising disposable incomes in emerging Asian economies | +1.8% | Asia-Pacific core with spillover to the Middle East and Africa | Long term (≥ 4 years) |

| Expansion of branded luxury chains into tier-2 cities | +1.2% | Global, concentrated in India, China, the United States, secondary markets, and Latin America | Medium term (2-4 years) |

| Hybrid work trends boosting long-stay bleisure demand | +1.5% | North America, Europe, Asia-Pacific urban and resort hubs | Short term (≤ 2 years) |

| Growth of ultra-high-net-worth individuals from tech IPOs | +0.9% | Global wealth hubs in the United States, China, and Gulf markets | Long term (≥ 4 years) |

| Carbon-neutral certification premiums influencing bookings | +0.6% | Global, with early traction in Europe, North America, and Singapore | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rebound Of International Tourism Post-Pandemic

International travel has reset at higher levels, with global tourist arrivals up 5% year over year through September 2025 and above 2019 by 3%, which provides a strong demand base for the luxury hotel market as premium travelers return to cross-border itineraries. Europe captured 625 million tourists over the same period, while Asia-Pacific recovered to 90% of 2019 levels, signaling that both traditional gateways and fast-rising leisure hubs can support length-of-stay and rate integrity as connectivity improves and visa regimes stabilize.[2]Source: UN Tourism, "International Tourist Arrivals up 5% in the First Nine Months of 2025", https://www.untourism.int/news/international-tourist-arrivals-up-5-in-the-first-nine-months-of-2025 Luxury portfolios gain additional lift from the reorientation toward more purposeful travel, including wellness, culinary immersion, and culture-led programming that deepens spend per stay and sustains a premium mix in the luxury hotel market. Procurement preferences also evolve alongside travel normalization, with many buyers screening for credible sustainability credentials where third-party certification qualifies properties for corporate programs and travel-policy compliance. This alignment between traveler intent and supplier capability narrows the performance gap between mature city centers and secondary destinations as more operators bring certified, experience-rich offerings to market, reinforcing a positive outlook for the luxury hotel market. As capacity returns and airlift broadens, the channel mix continues to diversify, with operators using data-driven personalization to defend direct relationships while leveraging the discovery reach of intermediaries, adding resilience to the demand base that supports the sector’s forecast CAGR.

Rising Disposable Incomes in Emerging Asian Economies

Broadening middle and upper-middle cohorts across Asia reinforces the growth runway for the luxury hotel market as intra-regional trips scale and premium segments migrate from goods toward experience-led spending, raising the ceiling for resort and lifestyle assets in tier-1 and select tier-2 cities. Operators are positioning ahead of this curve, with signings across Asia-Pacific accelerating in 2024 and 2025 as brands seek first-mover advantage in under-supplied leisure corridors and fast-growing urban nodes. Pipeline breadth in Greater China and Southeast Asia suggests that a broader base of affluent households will support premium ADRs in coastal resorts, nature-led destinations, and urban lifestyle districts as connectivity and retail ecosystems expand around these investments. At the same time, Europe and North America continue to attract Asian outbound travelers, which further balances geographic demand in the luxury hotel market as flight capacity stabilizes and traveler confidence improves. The demand mix also benefits from younger affluent cohorts who prioritize wellness, design, and culinary experiences, elevating brands that can tailor offerings with flexible inventory and integrative programming. This interplay of rising affluence and brand expansion into new nodes supports both occupancy stability and rate growth in the forecast period for the luxury hotel market.

Expansion Of Branded Luxury Chains into Tier-2 Cities

Branded luxury penetration into tier-2 urban centers represents a calculated arbitrage of supply-demand imbalances and operational efficiencies that metro markets can no longer deliver. India's tier-2 hospitality wave saw international chains like Taj, Marriott, and Radisson customize formats for Jaipur, Kochi, and Lucknow, where lower land acquisition costs and operational expenses yield 20-30% higher margins versus established metros.[3]Source: Brigade Group, "Why Tier-2 Cities Are Becoming India’s New Hospitality Hotspots", https://www.brigadegroup.com/blog/hospitality/why-tier-2-cities-are-indias-new-hospitality-hotspots Large-scale programs, including mixed-use coastal destinations and regenerative resort clusters, add to the region’s long-term supply story and expand the addressable audience for certified, high-amenity properties. Success in these locations depends on consistent talent pipelines, reliable utilities, and consistent project phasing, with operators often pairing brand standards with local design and community integration to boost authenticity and guest satisfaction in the luxury hotel market. Portfolios that match brand recognition with locally relevant programming and credible sustainability credentials tend to command more resilient pricing power across both peak and shoulder periods. These dynamics collectively point to a steady pipeline of tier-2 openings that reinforce the sector’s growth trajectory and widen geographic diversification at the portfolio level in the luxury hotel market.

Growth Of Ultra-High-Net-Worth Individuals from Tech IPOs

The expansion of ultra-high-net-worth (UHNW) households, now controlling USD 107 trillion in assets, a fourfold increase since 2000, directly correlates with sustained luxury hotel investment and RevPAR premiums. The United States holds 35% of global wealth and 39.7% of millionaires. This capital influx fueled trophy-asset transactions. Germany's Munich Mandarin Oriental deal set a 5.8% prime yield benchmark at USD 270 million (EUR 260 million) and accelerated branded-residence pipelines, where Marriott generated USD 2.1 billion in residential sales in 2024, and Four Seasons reported identical figures.[4]Source: Bay Street Hospitality, "German Hotel Investment Hits €4.2B in H1 2025: Munich Mandarin Deal Sets 5.8% Prime Yield Benchmark", https://www.baystreethospitality.com/post/german-hotel-investment-hits-eur4-2b-in-h1-2025-munich-mandarin-deal-sets-5-8-percent-prime-yield-benchmark Younger affluent travelers give preference to wellness-centric design, residential-style privacy, and distinctive culinary programs, which puts a premium on operators who can tailor service while integrating technology into high-touch experiences for the luxury hotel market. These factors ensure the high-spend segment remains a stabilizer across cycles, particularly in destinations with strong airlift, safety, and a rich calendar of cultural and sporting events that encourage repeat visits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex & long ROI cycles | -1.4% | Global, acute in greenfield and premium urban projects, where costs are elevated | Long term (≥ 4 years) |

| Geopolitical instability on key luxury corridors | -0.8% | Middle East conflict-adjacent markets and select Europe-Asia corridors | Short term (≤ 2 years) |

| Regulatory scrutiny on landmark ownership | -0.8% | North America, Europe, Australia | Medium term (2-4 years) |

| Talent scarcity in bespoke service roles | -0.6% | Global prestige destinations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex & Long ROI Cycles

Luxury projects require significant capital and multi-year delivery timelines, which stretch payback periods and expose owners to interest-rate and construction-cost risk as projects move from design to opening in the luxury hotel market. Renovations and repositionings can depress near-term profitability even for high-performing assets, although the long-run value proposition remains intact once new products and amenities reset price ceilings. Owners balance new-build risk with conversion strategies, leaning into brand upgrades that lower time-to-market while retaining the benefits of scale, loyalty, and distribution that come with major flags in the luxury hotel market. Even so, conversions require targeted property-improvement plans and capital outlays to align with brand standards and to compete effectively for premium guests, especially in gateway cities where benchmarks are exacting. Business disruption from extreme weather and demand shocks can complicate forecasting and underwriting for luxury portfolios, as seen in reporting from leading United States REITs that detail renovation impacts and insurance dynamics in quarterly results. Workforce constraints can further elevate operating costs and slow ramp schedules, with staffing shortages still widely reported by United States properties, which adds friction to opening timelines and service deployment in the luxury hotel market.

Geopolitical Instability on Key Luxury Corridors

Ongoing geopolitical risks temper confidence in selecting long-haul corridors, translating to demand volatility and uneven recovery patterns at the destination and sub-destination level for the luxury hotel market. Expert surveys tracked by intergovernmental bodies through late 2025 cite conflict-related concerns among the factors shaping inbound flows, which push operators to build portfolio resilience through diversification and flexible commercial strategies. At the same time, the Middle East overall registered visitor levels above 2019 by 2025, indicating that regional strength is concentrated in certain hubs and new resort developments, rather than across conflict-adjacent markets. Luxury operators mitigate risk by pacing openings, calibrating opening inventories, and emphasizing domestic and regional demand pools in early years while long-haul confidence rebuilds in the luxury hotel market. Transparent communications and flexible policies help maintain brand equity, while targeted marketing and strategic partnerships sustain mix quality during periods of uncertainty. The net effect has a steady impact on the luxury hotel market as leading brands allocate capital and operating attention across markets with different risk profiles and demand drivers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Resorts Lead Growth Amid Post-Pandemic Wellness Surge

Business Hotels retained the largest position with 46.36% in 2025, while resorts are the fastest-expanding service type with a projected 13.47% CAGR through 2031, underscoring the shift toward experience-led leisure in the luxury hotel market. This gap reflects diverging demand patterns, where integrated wellness, nature-forward design, and high-amenity beachfront and mountain resorts sustain premiums that are accretive to portfolio ADRs. Urban luxury continues to benefit from the return of corporate travel, with high-end groups optimizing mix by combining group, corporate, and premium leisure, yet the resort thesis grows faster as travelers prioritize rejuvenation and immersion in the luxury hotel market. Leading groups are also activating multi-format strategies that weave in branded residences and curated journeys, which expand the spend universe around flagship resorts. Large-scale projects in emerging leisure destinations, including regenerative resort clusters, further anchor the medium-term growth narrative for resort-led offerings in the luxury hotel market.

The performance spread across service types depends on place, positioning, and programming, with certified resorts showing procurement advantages and operating efficiencies that strengthen cash flow over time in the luxury hotel market. Operators that align guest journeys with local culture, design integrity, and sustainability measures can support both occupancy and rate across peak and shoulder months. Urban luxury retains pricing influence in global gateways where airlift, events calendars, and corporate activity stabilize demand, yet resort inventory remains the momentum leader as new supply opens in secondary leisure corridors. This mix of stable city demand and accelerating resort growth contributes to the broader durability observed in the luxury hotel market. As portfolios scale across formats, loyalty ecosystems help cross-sell urban and resort stays, raising retention and lifetime value as the cycle advances in the luxury hotel industry.

By Room Type: Villas/Bungalows Surge as Privacy Commands Premium

Suites held 41.76% of 2025 revenue, but Villas and Bungalows are set to expand at an 11.74% CAGR through 2031, reflecting rising preference for space and seclusion within the luxury hotel market. Villas create room for multi-generational travel and allow operators to layer in private chefs, butlers, and in-villa wellness, which boosts ancillary revenue beyond rate alone. Developers integrate villa clusters into resort master plans to monetize land with low-density configurations that balance guest privacy with sustainability objectives, which differentiates the product beyond square footage and view corridors. The resulting inventory supports long-stay behavior, blended work and leisure, and event-driven demand, providing operational flexibility for revenue management in the luxury hotel market. As portfolios extend into branded residences adjacent to hotels, premium real estate further deepens engagement with high-spend guests and repeats, sustaining visibility in the luxury hotel industry.

Standard luxury rooms remain essential for group blocks and conferences, yet the margin profile skews toward villas when ancillary services and privacy-led premiums are counted within the luxury hotel market. In many resorts, smart-home systems and wellness infrastructure are enhanced in-villa experiences and support price realization without diminishing service levels. Guests respond to private settings that enable family time, relaxation rituals, and curated activities, reinforcing the case for mixed-inventory resorts. Operators that combine villas, suites, and branded residences can serve diverse cohorts across seasons and rate bands, while protecting ADR with value-added inclusions in the luxury hotel market. Over the forecast period, villa growth adds a resilient pillar to resort revenue models, balancing city-led recovery patterns seen elsewhere in the luxury hotel industry.

By Booking Channel: OTAs Outpace Direct Despite Loyalty Push

Direct Booking reached 43.75% of reservations in 2025, supported by loyalty and mobile investments, while Online Travel Agencies are projected to post a 13.78% CAGR through 2031 as discovery at scale and bundling sustain share growth in the luxury hotel market. Hotels continue to enhance first-party channels by emphasizing value adds, flexible policies, and personalized offers, which lift conversion and lower acquisition costs. OTA partnerships remain critical for reach and demand diversification, while hotels deploy metasearch tactics to shape shopper choice at the point of decision. Longer-stay formats and apartment-style offerings give brands new room to compete for blended-trip demand, making direct channel performance more durable in the luxury hotel market. The interplay of direct, OTA, travel-agent, and corporate channels will continue, with data-driven merchandising and rate integrity practices helping operators maintain balance across segments.

Channel strategies now rely on modular technology stacks that unify inventory, rates, and content across touchpoints, which support consistent brand presentation and efficient performance optimization in the luxury hotel market. Hotels integrate loyalty in ways that make membership valuable during booking and in-stay, tightening the feedback loop between guest behavior and offer design. Corporate procurement adds a stability layer as budgets normalize and travel policies evolve, supporting weekday occupancy and ancillary spend. Across all channels, content quality and search visibility increasingly shape funnel performance, raising the bar for media, pricing transparency, and service clarity. As hotels improve first-party experiences, OTAs will still provide complementary reach that remains important for new customer acquisition in the luxury hotel market.

Geography Analysis

Europe retained 37.38% of the luxury hotel market share in 2025, with international arrivals through September reaching 625 million, which reinforces the region’s mix of gateway city strength and destination leisure momentum. Major groups maintain robust development plans across Europe’s capitals and cultural hubs, supported by investment in premium renovations, brand refreshes, and targeted conversions that keep product fresh. Sustainability credentials see consistent adoption, with many properties engaging third-party certification programs to align with procurement requirements and consumer expectations. Luxury portfolios continue to balance leisure destinations in Southern Europe with business-oriented stock in Northern Europe, while extending into secondary cities on the back of improved air and rail connectivity. As festival, sports, and culture calendars fill out, Europe remains a core anchor for the luxury hotel market through the forecast period.

Asia-Pacific is projected to be the fastest-growing region with an 11.43% CAGR to 2031, supported by intra-regional travel growth and an expanding base of affluent consumers who favor experience-led stays in premium resorts and urban lifestyle hotels. The region reached 90% of 2019 arrival levels by September 2025, reflecting the late-but-strong rebound that is now translating into sustained room-night demand for the luxury hotel market. Development pipelines highlight strategic emphasis on coastal leisure corridors, nature-led retreats, and tier-2 cities where infrastructure upgrades compress travel friction. International brands are broadening their footprints and formats, with signings in Greater China, Japan, and Southeast Asia pointing to multi-year supply growth, mixed-use plays, and branded residence integration. As certification programs and national sustainability roadmaps gain traction, premium assets with verifiable progress are set to capture procurement-led demand advantages across the region.

North America remains a stable pillar of demand, supported by resilient high-income household spending, a deep group calendar, and a balanced mix across urban and resort destinations in the luxury hotel market. Portfolio activity includes renovations, selective conversions, and expansion of longer-stay and apartment-style offerings that target hybrid work patterns and family travel. Transaction and development strategies remain disciplined, with owners calibrating capital programs and phasing to align with demand pacing in urban cores and leisure destinations. In the Middle East and Africa, arrivals by late 2025 exceeded pre-pandemic baselines in several hubs, with large-scale coastal and desert projects creating new destination clusters that elevate the region’s profile in the luxury hotel market. New luxury openings and branded residences play in flagship developments reinforce the region’s long-run demand thesis and deepen global brand exposure across high-spend segments.

Regulatory Landscape

Regulation affecting luxury hotels is tightening across accommodation licensing, operating standards, and sustainability-related disclosure, with several 2026 updates pointing to more unified frameworks. In Europe, the European Commission highlighted the application of Regulation (EU) 2024/1028 in May 2026, increasing transparency requirements around short-term rentals through platform display of unique registration numbers, which affects how destinations manage accommodation supply and data. At the property level, new and updated accommodation rules also emerged, including Malta Tourism Authority's Tourism Accommodation Regulations 2026 (Legal Notice 92 of 2026), effective June 15, 2026, which consolidated multiple prior instruments into a single operational framework.

Jurisdictions are also moving toward more formalized licensing and inspection regimes that can affect luxury renovation, conversion, and opening timelines. Wales passed the Development of Tourism and Regulation of Visitor Accommodation (Wales) Act 2026 (assent in April 2026), establishing a licensing system and fitness standards for visitor accommodation providers, while Wisconsin's updated lodging requirements under DATCP Chapter ATCP 72 became effective January 25, 2026, reinforcing inspection and license renewal compliance. In emerging destinations, legislative modernization is visible through proposals such as Fiji's Tourism Act 2026 bill to replace the Hotels and Guest Houses Act 1973 with updated tourism standards and classification alignment, while India saw policy reform emphasis in NITI Aayog's June 2026 recommendations focused on license rationalization and the National Single Window system for the tourism and hospitality sector.

Value Chain Analysis

The luxury hotel value chain runs from development (owners, investors, developers, architects, and contractors) to brand affiliation and management (global chains, soft brands, and third-party operators), with a supply network that covers FF&E, OS&E, food and beverage, wellness, and technology systems. Procurement and supplier selection increasingly connect to brand standards and corporate travel requirements, with third-party sustainability certifications such as LEED and Green Key shaping materials choices, energy systems, and operating processes from design through day-to-day delivery. Distribution and demand capture sit downstream through direct booking, OTAs, travel advisors, and corporate contracts, where content, pricing integrity, and loyalty integration influence conversion and customer acquisition costs.

Recent supply-side actions show luxury operators using partnerships and centralized procurement to reduce volatility while embedding sustainability and traceability into inputs. The Luxury Collection (Marriott) partnered with MAD Academy in March 2025 to roll out culinary sustainability training and local sourcing frameworks across 120 properties, and Accor expanded its Astore procurement platform in December 2025 to third-party independent hotels with AI-enabled supplier performance management under a Responsible Procurement Charter. Operational consumables and compliance-linked inputs are also being redesigned through partnerships such as Rotana's June 2025 collaboration with Ecolab and Stella Hospitality to phase out single-use plastics and improve efficiency, while broader bottlenecks cited across the ecosystem include freight and tariff uncertainty and commodity price volatility impacting F&B and FF&E lead times and cost control.

Competitive Landscape

The luxury hotel market remains structurally fragmented at a global level, with scale advantages accruing to large brand families while independent and regional champions continue to compete effectively on authenticity and service. Leading groups execute asset-light growth strategies that balance organic signings, conversions, and brand extensions into residences and long-stay formats, which expands their exposure to premium demand pools in multiple geographies. Portfolio momentum is fueled by record pipelines, targeted openings, and brand refreshes in top-tier cities and leisure destinations, which support revenue growth and loyalty expansion in the luxury hotel market. Operators elevate signature experiences and curated programming to stand apart in high-ADR markets, while expansion into tier-2 nodes reduces concentration risk and improves cross-sell opportunities. Sustainability adoption deepens across brands with LEED and other frameworks enabling measurable efficiencies and procurement access, particularly for corporate travel. As the cycle evolves, portfolios that combine strong brand equity with credible sustainability progress and agile distribution are positioned to outpace category averages in the luxury hotel market.

Technology and product innovation now create clear competitive separation in the luxury hotel market, as operators deploy advanced booking engines, modular tech stacks, and CRM-linked personalization to manage mix and enhance conversion. Brand families extend into apartment-style and long-stay offerings to serve hybrid work patterns and multi-generational travel, with new formats improving both occupancy resilience and ancillary revenue capture. Conversions remain a significant portion of development activity at several leading groups, which allows faster market entry and leverages existing structures while maintaining brand standards that sustain rate power. In parallel, curated residences and experiential products extend the brand ecosystem and give luxury guests multiple ways to engage across seasons and destinations. These moves keep the competitive field dynamic while preserving the category’s diversity across independent and chain-affiliated operators in the luxury hotel market.

Capital discipline and risk management remain central themes for owners and operators as they navigate renovations, project phasing, and geopolitical uncertainty in the luxury hotel market. Public disclosures from leading owners illustrate how large-scale capital programs and weather-related disruptions can affect short-term profitability, while laying the groundwork for long-term value creation after completion. Cross-functional sustainability programs drive both cost efficiencies and reputational upside, strengthening bids for corporate travel while aligning with consumer expectations. On the commercial side, balanced distribution strategies and loyalty investments help defend direct relationships while maintaining the reach that intermediaries provide during periods of uneven demand. As product and brand portfolios stretch into new geographies and formats, execution capability and consistent service delivery become differentiators that shape long-run share outcomes in the luxury hotel market. Operators that remain focused on experience quality, sustainability, and tech-enabled service are positioned to capture the most resilient demand over the forecast period.

Luxury Hotel Industry Leaders

-

Marriott International (The Ritz-Carlton, St. Regis)

-

Hilton Worldwide (Waldorf Astoria, Conrad)

-

Accor (Fairmont, Raffles)

-

Hyatt Hotels Corporation (Park Hyatt, Andaz)

-

Four Seasons Hotels & Resorts

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Luxury operators and owners have a clear whitespace in wellness-led differentiation and in scaling verifiable sustainability practices that corporate procurement and affluent travelers screen for, where third-party credentials such as LEED and Green Key provide a comparable signal across destinations. Marriott integrating the Lefay luxury wellness hospitality brand through a completed joint venture transaction in June 2026 highlights active portfolio repositioning around wellness as a core luxury proposition rather than an add-on amenity. On the investment side, institutionally financed ultra-luxury projects continue to signal destination-defining capital formation, including Aman closing USD 4.3 billion in financing in March 2026 for Aman One Beverly Hills through a mix of senior and mezzanine capital.

Opportunity is also visible in conversions and brand-led upgrades of landmark or high-recognition assets, where operators can accelerate market entry relative to greenfield timelines while refreshing rate ceilings through repositioning. Four Seasons planned work at the Hotel Danieli in Venice (reopening scheduled in 2026 with a staged capacity increase) and Accor's intent to upgrade and convert prominent China assets, including a planned shift of Fairmont Peace Hotel in Shanghai to Raffles and conversion activity in Dalian, point to luxury supply growth being pursued through rebrandings and repositionings alongside new-builds. Technology is a practical lever for margin protection and experience consistency at scale, with operator priorities focused on AI use cases in revenue management, labor scheduling, and conversational guest services. Large integrated resort builds such as Wynn Al Marjan Island in the UAE, a USD 5.1 billion, 1,530-key project under construction, also function as a high-profile test case for complex, tech-enabled operations in resort environments.

Recent Industry Developments

- July 2026: Hilton announced a management agreement with Reuben Brothers to bring Waldorf Astoria to Miami Beach through the transformation of an existing property, targeting a Winter 2027 relaunch. The agreement expands Waldorf Astoria's presence in a high-demand leisure and lifestyle market while using conversion-led execution to compress time to entry versus new-build delivery.

- June 2026: Marriott International completed a joint venture transaction with the Leali family to bring the Lefay luxury wellness hospitality brand into its global portfolio. Adding a specialist wellness brand strengthens Marriott's ability to compete in experience-led luxury and supports cross-selling through its distribution and loyalty ecosystem.

- October 2025: Four Seasons announced Four Seasons Private Residences Red Sea at Shura Island in partnership with Red Sea Global, extending the brand within Saudi Arabia's flagship destination development corridor. The branded residence component broadens the monetization model beyond room revenue and deepens owner alignment in large-scale resort ecosystems.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the luxury hotel market is the value of paid guest stays sold by luxury properties, captured as room-led lodging revenue that is realized through direct and indirect booking routes across major geographies.

Scope exclusions: It excludes airline and cruise tourism spend, short-term rentals, and most off-property luxury experiences that are not sold as part of the lodging transaction.

Segmentation Overview

-

By Service Type

- Business Hotels

- Airport Hotels

- Suite Hotels

- Resorts

- Other Service Types

-

By Room Type

- Standard Luxury Room

- Suites

- Villas / Bungalows

- Penthouses & Presidential Suites

-

By Booking Channel

- Direct Booking (Brand Website, Call Center)

- Online Travel Agencies (OTA)

- Travel Agents / Tour Operators

- Corporate Contracts

-

By Geography

-

North America

- Canada

- United States

- Mexico

-

South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

-

Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

-

Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- Rest of Asia-Pacific

-

Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base map of supply and demand for luxury lodging and to anchor key ratios that later flow into the market model. We mainly reviewed public tourism arrival statistics and accommodation indicators from sources such as UN Tourism, the World Bank, national statistics agencies, and central bank travel receipts series, and then cross-checked directionally with airport traffic disclosures from airport authorities.

To keep the model practical, we also relied on company annual reports, investor presentations, and regulatory filings for revenue mixes and performance commentary, and we reviewed hospitality association and destination marketing organization publications for pipeline and event-led demand signals. Where needed, paid subscriptions were used for company financials and intelligence, news and financials, and a patent database to screen technology adoption claims tied to smart rooms and guest experience tools. The sources listed are illustrative only, and many other public and paid references were reviewed to collect data, validate assumptions, and resolve research questions.

Primary Interviews and Surveys

Primary work focused on validating what portion of total hotel demand and pricing truly sits in the luxury bracket in each region, and how that mix is moving year to year. We spoke with a mix of luxury hotel owners, operators, consultants, distribution specialists, and corporate travel and event buyers across APAC, EMEA, and the Americas, which helped clarify occupancy seasonality, ADR progression, and channel commissions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 14% | APAC: 49% |

| Mid tier: 58% | Functional/Unit leaders: 37% | EMEA: 33% |

| Smaller Players: 16% | Managers: 49% | Americas: 18% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where tourism receipts, hotel room supply, and lodging utilization indicators are used to reconstruct the addressable luxury lodging value pool by region, followed by a luxury share filter based on property grading practices and observed price positioning. The totals are then checked with selective bottom-up approximations, such as sampling ADR and occupancy for luxury properties in key cities, applying room inventory counts, and stress-testing results with channel mix and commission assumptions.

Key inputs that shape the model include luxury room inventory and pipeline additions, occupancy rates and length-of-stay patterns, ADR and RevPAR movement, the mix of direct versus OTA bookings (and take rates), and cross-border versus domestic traveler shares. For forecasting, scenario analysis is used so demand and price can be flexed separately, and the chosen path is aligned to what interviewees expect for travel recovery pacing, premiumization, and new supply absorption. Where bottom-up data is sparse, we interpolate using comparable destination groups and then re-validate using updated tourism and lodging indicators before finalizing.

Data Validation & Update Cycle

Outputs are validated through multiple checks so the final number ties back to observable travel and lodging signals. We compare implied room nights, ADR, and occupancy trends against independent indicators, and unusual jumps are reworked by revisiting inputs like pipeline timing, currency conversion windows, and channel share.

Before sign-off, the model and assumptions go through multi-step analyst reviews, and re-contact is triggered when a variance cannot be explained by documented events such as new openings, major demand shocks, or regulatory changes. The report is refreshed annually, and interim updates are made when material events shift demand, pricing, or supply. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Luxury Hotel Market Size Compared Against Other Published Estimates

Published market sizes for luxury hotels can vary a lot, even when they seem to talk about the same thing, because the scope and the revenue line being counted are not always consistent. Differences in what is treated as luxury, how indirect channels are handled, and how currency timing is applied can all move the final value.

The benchmark table shows a wide spread for 2025 to 2026, and in Mordor Intelligence's model the value is tied to luxury hotel lodging revenue across regions, with business hotels, airport hotels, suite hotels, resorts, and similar property formats included only when they meet the luxury positioning used in the study period. Other estimates often shift the number by blending adjacent upscale categories, using different ADR uplift assumptions for premiumization, or applying a shorter refresh cycle that captures a temporary spike in rates as a structural step-up.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 150.22 B (2026) | |

| Global Consultancy A | USD 110.87 B (2025) | Uses an earlier base year and a different starting revenue pool, and the luxury cut may be anchored more heavily on category labels like chain versus independent, which can undercount luxury-leaning resorts and suites in mixed portfolios. |

| Industry Publisher B | USD 112.90 B (2025) | Runs on a shorter forecast horizon and can apply a lower price and demand progression path, which reduces the implied ADR and occupancy recovery in high-spend destinations and limits the lift from direct-booking growth. |

Taken together, the spread is mainly explained by what gets classified as luxury, which years are chosen as the starting point, and how rate growth is carried forward. By keeping assumptions traceable to room supply, occupancy, ADR, and booking channel economics, we end up with a balanced number that can be reproduced and monitored as new travel data comes in.

Key Questions Answered in the Report

What is the luxury hotel market size in 2026 and its growth outlook through 2031?

The luxury hotel market size is USD 150.22 billion in 2026 and is projected to reach USD 223.56 billion by 2031 at an 8.28% CAGR, signalling robust multi-year expansion across regions.

Which service type grows fastest within the luxury hotel market through 2031?

Resorts are the fastest-expanding service type with a projected 13.47% CAGR through 2031, supported by wellness and experience-led travel preferences.

Which room type is gaining the most momentum in premium properties?

Villas and Bungalows are projected to grow at an 11.74% CAGR as travelers prioritize privacy, space, and residential-style amenities in luxury settings.

What booking channels will see the strongest growth for luxury stays?

Online Travel Agencies are projected to post a 13.78% CAGR through 2031, although Direct Booking remains a large share due to loyalty and mobile investments.

Which region leads today, and which is growing the fastest for luxury hotels?

Europe held a 37.38% share in 2025, while Asia-Pacific is set to grow the fastest with an 11.43% CAGR through 2031, reflecting a broad-based recovery and rising affluence.

How are sustainability certifications influencing luxury hotel demand?

Certified properties gain procurement advantages and efficiency benefits, with LEED and Green Key programs contributing to operating resilience and guest preference in premium categories.

Page last updated on: