Gastrointestinal Endoscopy Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 22.24 Billion |

| Market Size (2031) | USD 30.70 Billion |

| Growth Rate (2026 - 2031) | 6.66% CAGR |

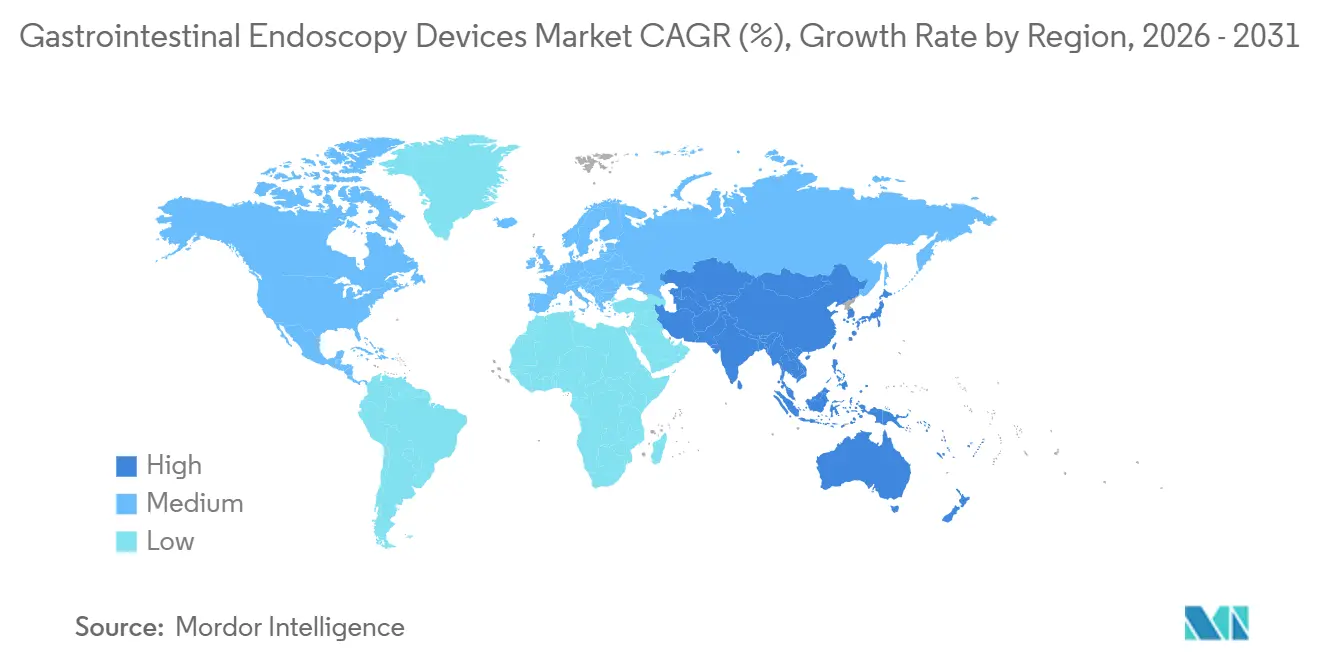

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

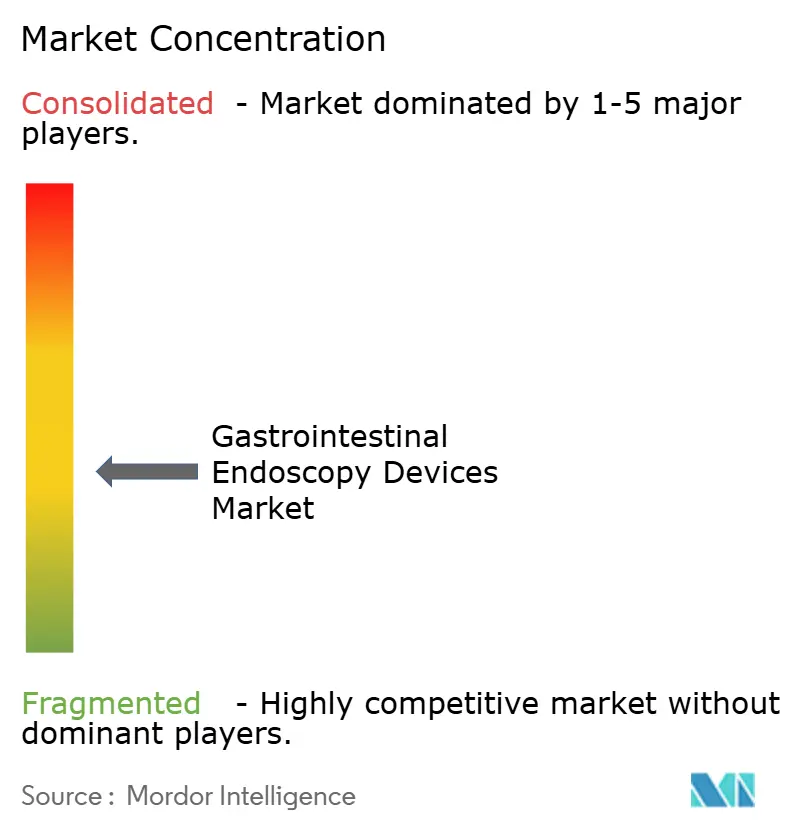

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gastrointestinal Endoscopy Devices Market Analysis by Mordor Intelligence

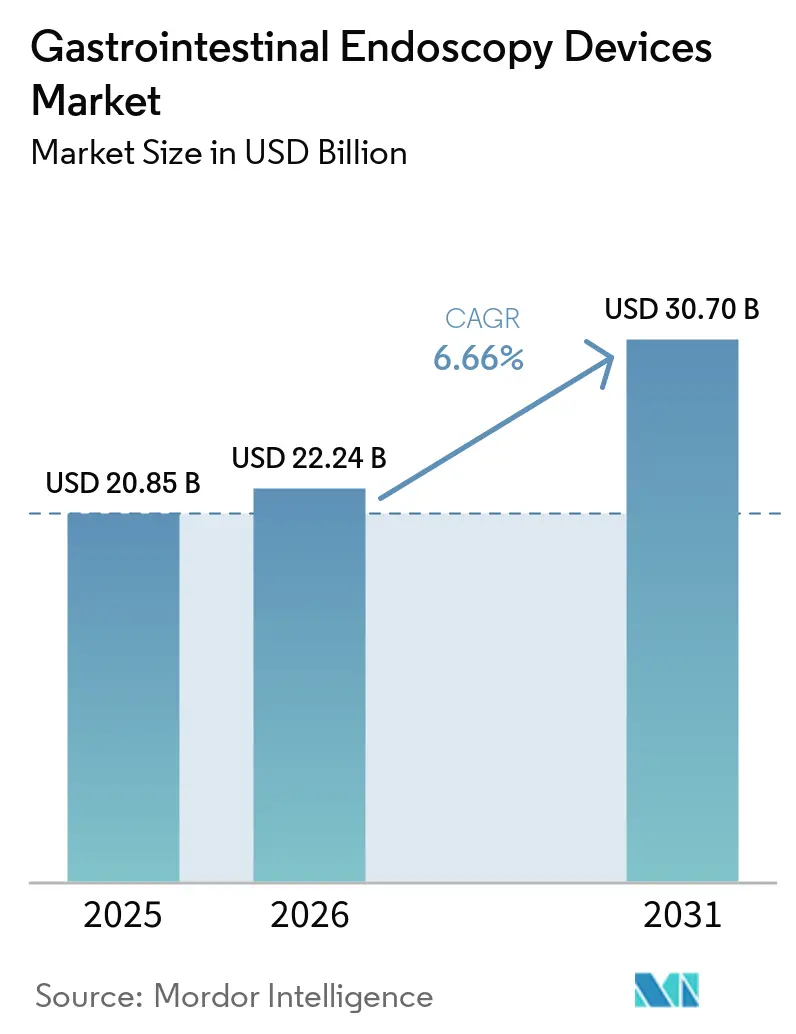

The Gastrointestinal Endoscopy Devices Market size is projected to be USD 20.85 billion in 2025, USD 22.24 billion in 2026, and reach USD 30.70 billion by 2031, growing at a CAGR of 6.66% from 2026 to 2031.

The market is being supported by the steady rise in colorectal and upper gastrointestinal cancer screening demand, as the American Cancer Society estimates 158,850 new colorectal cancer cases in the United States in 2026, including 49,990 rectal cancer cases, which keeps procedure demand firm across both diagnostic and therapeutic use cases. The gastrointestinal endoscopy devices market is also benefiting from a younger screening pool, because incidence in adults aged 20 to 49 has been rising by 1% to 2% a year since the mid-1990s, which extends future procedure volume beyond the older screening base that once defined demand. The gastrointestinal endoscopy devices market gained another volume tailwind after CMS expanded preventive coverage for CT colonography and blood-based biomarker tests from January 1, 2025, since positive findings from those tests still move patients into follow-on colonoscopy pathways. The gastrointestinal endoscopy devices market is further shaped by the move toward outpatient care and AI-enabled imaging, because gastroenterology remains among the faster-growing ambulatory surgery center specialties and AI-assisted colonoscopy continues to raise adenoma detection performance enough to justify platform upgrades and software subscriptions. The gastrointestinal endoscopy devices market therefore remains commercially attractive, although capital spending pressure at hospitals, tighter price competition, and staffing gaps in reprocessing and endoscopy support still favor companies that can sell compact systems, disposable products, and software-led workflows rather than rely only on large tower replacement cycles.

Key Report Takeaways

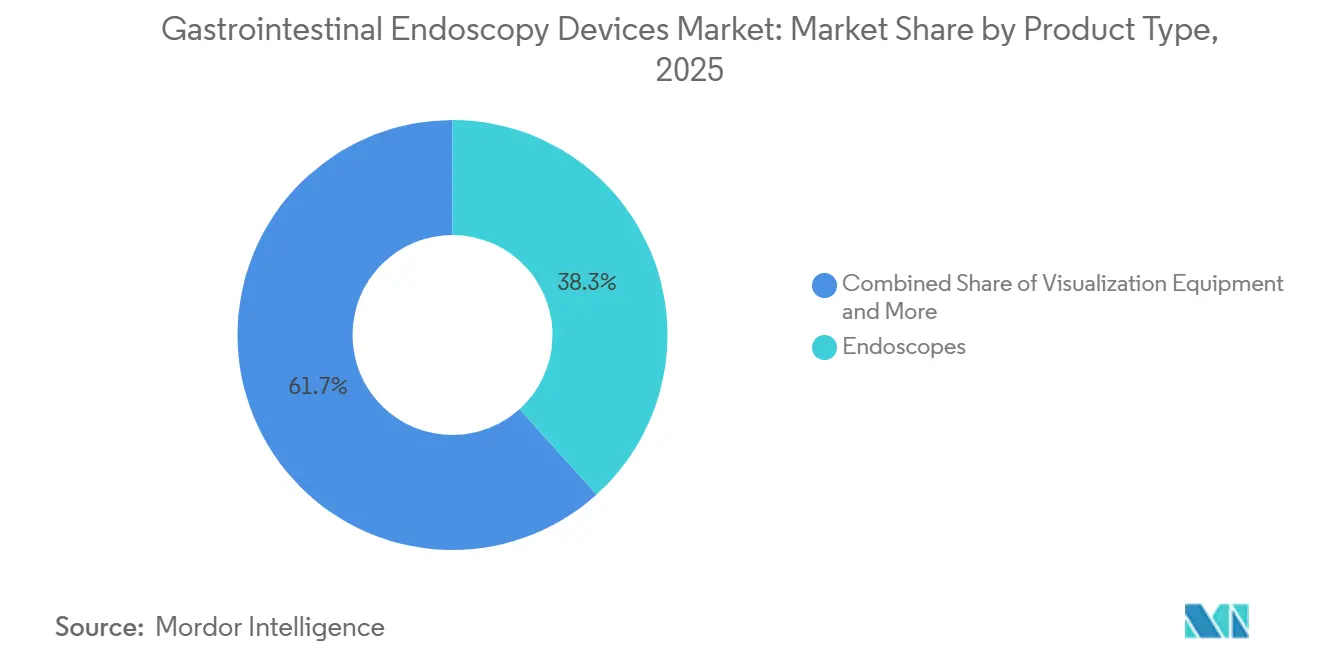

- By product type, endoscopes held 38.31% of gastrointestinal endoscopy devices market share in 2025, while visualization equipment is projected to expand at an 8.38% CAGR through 2031.

- By reusability, reusable endoscopes held 80.24% revenue share in 2025, while single-use endoscopes are forecast to grow at a 7.52% CAGR through 2031.

- By age group, adults accounted for 65.52% share in 2025, while geriatrics is projected to record the highest CAGR at 7.25% through 2031.

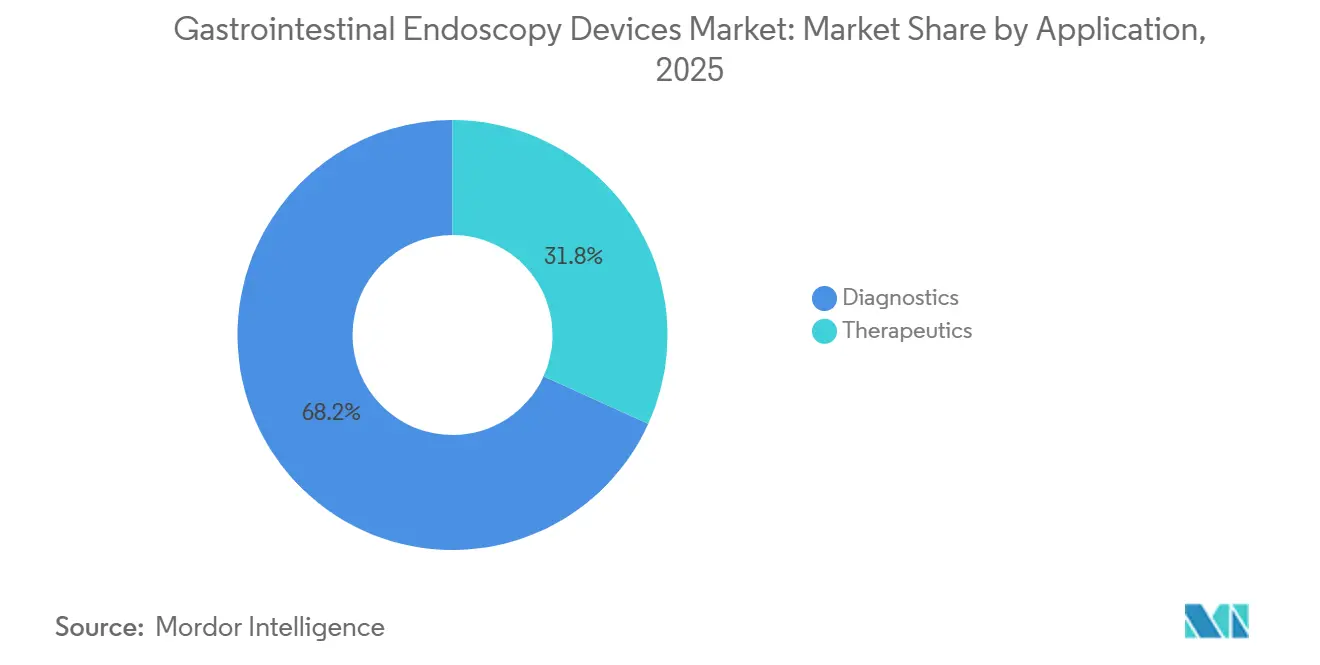

- By application, diagnostics accounted for 68.22% of the gastrointestinal endoscopy devices market size in 2025, while therapeutics is forecast to grow at a 7.15% CAGR through 2031.

- By end user, hospitals held 54.34% share in 2025, while ambulatory surgery centers are projected to expand at an 8.85% CAGR through 2031.

- By geography, North America held 38.22% of gastrointestinal endoscopy devices market share in 2025, while Asia-Pacific is projected to grow at an 8.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gastrointestinal Endoscopy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Colorectal And Gastric Cancer Screening Demand | +1.5% | Global, with high concentration in North America, East Asia, and Western Europe | Long term (≥ 4 years) |

| Rapid Shift Toward Single-Use Endoscopy For Infection Control | +0.8% | Global, most acute in North America and Northern Europe where HAI reporting is mandatory | Medium term (2-4 years) |

| AI-Assisted Lesion Detection And Documentation | +0.7% | North America and EU as early adopters, with APAC following after a lag | Medium term (2-4 years) |

| Expansion Of Ambulatory And Outpatient GI Procedure Capacity | +0.6% | North America, with spillover to Australia and Gulf states | Short term (≤ 2 years) |

| Reimbursement Support For Preventive And Early-Detection Procedures | +0.4% | North America, EU national payer frameworks, and early-stage coverage in South Korea and Australia | Long term (≥ 4 years) |

| Hidden Backlog From Deferred GI Procedures And Diagnostic Delays | +0.3% | Global, most measurable in North America and Western Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Colorectal And Gastric Cancer Screening Demand

The gastrointestinal endoscopy devices market continues to draw its core volume from colorectal and upper gastrointestinal cancer screening, and that demand base remains durable in 2026. The American Cancer Society estimates 158,850 new colorectal cancer cases in the United States in 2026, and one-third of the expected 55,230 deaths is projected to occur in patients younger than 65, which is pushing payers and health systems to broaden screening access across more age groups[1]American Cancer Society and American Society for Gastrointestinal Endoscopy, “2026 Colorectal Cancer Statistics,” ASGE Journal Scan, asge.org. A second demand layer comes from younger adults, because 22% of colorectal cancer cases in 2022 were diagnosed in people younger than 55, up from 11% in 1995, which increases lifetime screening and surveillance needs for a larger patient pool. Screening uptake is also moving in the right direction, as the U.S. rate rose from 59% in 2021 to 65% in 2023 among adults aged 45 and older, and total patients screened at health centers reached 3,617,246 in 2024. Positive results from noninvasive tests still drive patients into colonoscopy, so newer screening formats are not removing procedures from the gastrointestinal endoscopy devices market, but are instead adding a wider referral funnel into it. Fujifilm’s 2026 investor material also supports that longer demand picture, as it expects the global gastrointestinal endoscopy field to sustain 4% to 6% annual growth on the back of aging populations and rising cancer incidence in both mature and developing markets.

Rapid Shift Toward Single-Use Endoscopy For Infection Control

The gastrointestinal endoscopy devices market is also being lifted by the wider shift toward single-use devices for infection control. The original case for disposable endoscopes began with duodenoscopes, but the same purchasing logic is now moving into bronchoscopy and selected gastrointestinal procedures where contamination risk carries greater clinical and legal weight. Evidence published in 2025 showed that high-level disinfection does not reliably eliminate microorganisms in real-world practice, with high-concern organisms and multidrug-resistant organisms still found on reprocessed devices. That evidence is shaping policy discussions and technology review work, including the AHRQ review of disposable endoscope use that was updated in September 2025[2]Agency for Healthcare Research and Quality, “Disposable Endoscope Use,” Effective Health Care Program, ahrq.gov. Another practical driver is training consistency in teaching hospitals, because single-use devices remove wear-related variation from one procedure to the next and reduce uncertainty linked to reprocessing quality. As more manufacturers widen indications and product lines, the gastrointestinal endoscopy devices market is likely to see durable demand for disposable systems in settings where safety assurance matters more than reuse economics.

AI-Assisted Lesion Detection And Documentation

The gastrointestinal endoscopy devices market is entering a software-led upgrade phase as AI-based detection and documentation tools become more central to endoscopy purchasing decisions. A randomized controlled trial published in 2025 found that a cloud-based AI system detected 33% more adenomas than standard care, with adenoma detection rate rising from 35.9% to 43.2%, which is large enough to affect hospital buying choices and clinical quality programs. A 2024 meta-analysis also showed that AI-assisted colonoscopy improved adenoma detection by 20%, and the benefit was present regardless of the endoscopist’s experience level, which broadens adoption potential beyond major academic centers. Olympus strengthened that commercial path in September 2025 when it launched its OLYSENSE CAD/AI portfolio in the United States and Europe after earlier regulatory clearance, which signals that AI tools are now moving from pilot use to platform-level commercialization. The revenue effect is important because AI does not just support image quality, it also adds recurring software and cloud income on top of installed hardware. That makes the gastrointestinal endoscopy devices market more favorable to vendors that can combine scopes, processors, software, and data services into one long-term account relationship.

Expansion Of Ambulatory And Outpatient GI Procedure Capacity

The gastrointestinal endoscopy devices market is also being pushed by the steady expansion of ambulatory and outpatient gastrointestinal procedure capacity. Gastroenterology remains among the specialties expected to add meaningful ambulatory surgery center volume during the current decade, and that keeps demand high for systems that fit faster turnover, lower footprint requirements, and tighter per-case cost controls. This setting changes the purchasing logic because centers often choose equipment at the physician or site level, rather than through slower integrated hospital committees, which shortens evaluation cycles and creates room for newer suppliers. It also changes product mix because room utilization and speed matter more in outpatient settings, which supports compact visualization systems, single-use accessories, and products that reduce reprocessing time. CMS support for preventive screening is reinforcing this shift by keeping the outpatient procedure funnel active and predictable. As more gastrointestinal work moves into these centers, the gastrointestinal endoscopy devices market will likely see a larger share of growth come from products designed around throughput, standardization, and lower setup burden rather than only around hospital-grade capital systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost Of Capital Equipment And Imaging Towers | -1.1% | Global, most acute in emerging markets and cost-constrained U.S. community hospitals | Long term (≥ 4 years) |

| Reprocessing Burden And Infection-Control Compliance Costs | -0.7% | North America and EU, with spillover to APAC | Medium term (2-4 years) |

| Shortage Of Skilled Endoscopists And Procedural Support Staff | -0.5% | Global, critical in South and Southeast Asia, rural North America, and Sub-Saharan Africa | Long term (≥ 4 years) |

| Pricing Pressure From GPOs, Tenders, And ASP Compression | -0.4% | North America, EU, and APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost Of Capital Equipment And Imaging Towers

The gastrointestinal endoscopy devices market still faces a clear ceiling from the cost of premium imaging systems, processors, AI modules, and full tower setups. New platforms are adding clinical value, but they also raise acquisition cost at a time when many community hospitals and public systems remain careful with capital budgets. Fujifilm’s ELUXEO 8000 reflects that direction, with 4K imaging, triple noise reduction, and Amber-Red Color Imaging aimed at more advanced procedures, yet the price of system-level adoption can limit uptake outside higher-volume facilities. Replacement timing adds another constraint because many hospitals refresh imaging equipment on a 7 to 10 year cycle, which is slower than the current push toward AI-ready platforms. The problem is more pronounced in emerging markets, where weaker service support and tighter procurement budgets can shift demand toward lower-cost local systems or modular components instead of full integrated platforms. This keeps part of the gastrointestinal endoscopy devices market tied to slower conversion cycles even when clinical demand remains healthy.

Reprocessing Burden And Infection-Control Compliance Costs

The gastrointestinal endoscopy devices market also carries a growing cost burden from reprocessing, because reusable systems require labor, chemicals, maintenance, quality checks, and documented compliance after every procedure. Hospitals in the United States and Europe face increasingly detailed standards for reprocessing, and 2025 evidence showed how difficult it is to maintain consistent high-level disinfection in routine practice across all devices and all teams. Staff turnover makes this harder, since repeated retraining and competency gaps can raise infection risk and increase the operating cost per reusable procedure. Administrative workload is also rising because documented compliance is now a bigger part of quality systems and procurement review. These costs do not always appear in initial equipment budgets, but they shape the real ownership decision and can slow adoption of reusable premium systems even when hospitals prefer them clinically. That pressure keeps the gastrointestinal endoscopy devices market tilted toward solutions that reduce workflow burden, simplify cleaning risk, or move part of the cost from capital budgets into per-procedure spending.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Visualization Equipment Gains Commercial Ground on Hardware

Endoscopes held the largest product type share at 38.31% in 2025, reflecting the central role of flexible colonoscopes and gastroscopes across diagnostic and therapeutic gastrointestinal workflows. Their scale is supported by routine use in screening, surveillance, and intervention, which gives them a broader demand base than any other product group in the gastrointestinal endoscopy devices market. Flexible products remain dominant inside this category, while disposable formats are expanding faster within specific infection-sensitive settings. Operative devices and accessories continue to provide recurring sales, because biopsy forceps, snares, clips, and electrosurgical tools are used across a large installed base and are less exposed to hospital capital delays.

Visualization equipment is projected to record the highest CAGR at 8.38% through 2031, which shows that the current upgrade cycle is increasingly tied to processors, monitors, towers, and software-ready platforms rather than only to scopes. Olympus supported that cycle when it received FDA 510(k) clearance in May 2025 for the EZ1500 series with Extended Depth of Field technology, which improved image sharpness at closer distances and created a practical reason to refresh compatible installed systems. Fujifilm’s ELUXEO 8000 further reinforced the same pattern in 2026 with 4K imaging and Amber-Red Color Imaging aimed at more complex endoscopy work. The commercial appeal is stronger because imaging processors are now increasingly paired with annual AI software licenses, which raises total contract value and keeps customers inside one vendor ecosystem for a longer period.

By Reusability: Single-Use Expansion Tests the Reusable Installed Base

Reusable endoscopes commanded 80.24% of revenue in 2025, supported by the deep installed base in hospital gastrointestinal labs and the lower cost per procedure that high-volume centers can still achieve with reuse. That installed base remains important because clinicians are familiar with reusable handling, hospitals already own the supporting infrastructure, and many advanced procedures still depend on reusable systems. Even so, the gastrointestinal endoscopy devices market is seeing faster growth in single-use formats where contamination risk is less acceptable or patient profiles are more sensitive. Adoption is strongest in procedures and settings where a reprocessing failure would create disproportionate clinical, financial, or legal exposure.

Single-use endoscopes are projected to grow at a 7.52% CAGR through 2031, and that pace reflects a broader move from narrow rescue use into more regular procurement planning. A 2024 Delphi consensus on disposable endoscopy linked current adoption most clearly to patients with multidrug-resistant organism exposure and noted that broader use will depend on more cost-effectiveness and clinical evidence, which suggests a steady but still selective expansion path. The competitive issue is not limited to disposable versus reusable, because hybrid formats with reusable bodies and single-use distal mechanisms could become an attractive option in medium-volume sites. Micro-Tech also showed continued momentum in disposable and endotherapy-linked innovation with multiple FDA 510(k) clearances through April 2026, which points to a wider accessory and intervention ecosystem developing around less reuse-intensive workflows. As manufacturing scale improves and more procedure types become eligible, the gastrointestinal endoscopy devices market is likely to keep shifting part of infection-control spending away from reprocessing infrastructure and toward device replacement.

By Age Group: Geriatric Demand Underpins Long-Term Volume Growth

Adults captured 65.52% of revenue in 2025, which reflects the large screening and surveillance base in the 45 to 64 age group across major healthcare systems. This segment remains central because organized screening programs, symptomatic workups, and routine surveillance continue to concentrate in adult populations. Pediatric procedures remain smaller in volume, but they require specialized instruments and can still command premium pricing due to design complexity and limited supply. Those characteristics keep pediatric demand important even though it does not set the overall revenue direction of the gastrointestinal endoscopy devices market.

Geriatrics is projected to expand at a 7.25% CAGR through 2031, supported by aging populations in North America, Europe, Japan, and South Korea where procedure intensity rises with age. The effect is not limited to higher case numbers, because older patients often present with more comorbidities, longer procedure times, and greater need for advanced visualization and hemostatic tools. That raises average device value per case and makes the gastrointestinal endoscopy devices market more dependent on products that help with therapeutic complexity rather than only basic imaging. Device design is also adjusting, since frailer patients can benefit from softer insertion tubes, variable stiffness, and water-jet-assisted navigation. In Japan, where the older patient mix is already high, endoscopy capacity planning is increasingly extending beyond tertiary hospitals into community-linked settings, which creates a distinct channel for future equipment placement.

By Application: Therapeutic Endoscopy Outpacing Diagnostics on Growth

Diagnostics accounted for 68.22% of the gastrointestinal endoscopy devices market size in 2025, reflecting the large global volume of colonoscopies, gastroscopies, and other examinations used for screening and gastrointestinal disorder workup. This remains the volume foundation of the category because every screening expansion, symptom referral, and follow-up pathway still begins with diagnostic use. Basic diagnostic kits also tend to be more standardized, which keeps unit economics more stable but limits per-procedure revenue growth. That means the gastrointestinal endoscopy devices market still relies on diagnostic scale for revenue stability even while higher-value growth is shifting elsewhere.

Therapeutics is projected to grow at a 7.15% CAGR through 2031 as more lesions are treated in the same session through polypectomy, EMR, ESD, ERCP, and other advanced techniques. AI-assisted lesion detection strengthens this shift because better detection can lead to more resection activity within the same procedure and higher use of clips, snares, and related tools. The application mix is also broadening into procedures that once sat with surgery or were not treated at all, including POEM, ESD for early gastric cancer, and bariatric endoscopy. Olympus added to that direction in May 2026 when it signed a global distribution agreement with EndoRobotics for robot-assisted technologies linked to third-space endoscopy. CONMED’s exit from gastroenterology in December 2025 also shows that the gastrointestinal endoscopy devices market is becoming harder for mid-tier players that cannot fund the move toward more complex therapeutic capability.

By End User: ASCs Redefine the Procurement Model

Hospitals retained a 54.34% share of end-user revenue in 2025 because they remain the main setting for complex therapeutic cases, inpatient gastrointestinal procedures, and patients who need general anesthesia or closer post-procedure monitoring. Their role is still strong in advanced intervention, multidisciplinary care, and high-acuity cases that smaller centers cannot always handle. Specialty clinics and other users continue to serve a growing share of outpatient surveillance work and capsule endoscopy, especially where office-based or community-linked gastroenterology practice is well established. Even with that spread, hospital demand still anchors the installed base across the gastrointestinal endoscopy devices market.

Ambulatory surgery centers are projected to grow at an 8.85% CAGR through 2031, helped by reimbursement support for preventive care and steady investment in new outpatient capacity. This matters because purchasing decisions in these centers are often made by a small physician-led group rather than a large hospital committee, which changes how vendors sell and how quickly equipment decisions move. Evidence and peer referrals therefore carry more weight, and manufacturers with strong clinical support and shorter demonstration cycles can perform better in this channel. ASCA has also pointed to meaningful decade-long growth in adult ASC volume, with gastroenterology among the specialties contributing to that increase. As the customer base broadens, the gastrointestinal endoscopy devices market is becoming less dependent on hospital purchasing consortia and more exposed to site-level buying behavior in outpatient care.

Geography Analysis

North America held 38.22% of the gastrointestinal endoscopy devices market size in 2025, making it the largest regional contributor by revenue. The region benefits from high screening colonoscopy uptake, a mature ambulatory surgery center network, and payer support that increasingly favors preventive gastrointestinal procedures. The United States remains the main national driver because CMS expanded colorectal screening coverage from January 2025 to include CT colonography, blood-based biomarker tests, and Cologuard Plus, which widened the front end of the procedure funnel and preserved follow-on colonoscopy demand after positive results. Canada adds steadier public-system demand as provinces continue to address wait times and capacity needs, while Mexico is benefiting from private healthcare investment in urban markets. The gastrointestinal endoscopy devices market in North America is also being reshaped by physician-led ASC development in states such as Texas, Florida, and Arizona, which is shortening the shift from hospitals to outpatient care and creating a nearer-term replacement opportunity for mid-tier imaging systems.

Europe remains an important source of premium device demand, with Germany, France, and the United Kingdom supporting adoption of next-generation imaging and AI-linked platforms. EU MDR 2017/745 has lengthened market entry requirements for smaller suppliers, but it has also strengthened the position of larger companies that can support broader clinical evidence and post-market surveillance obligations. Italy and Spain are moving ahead with colorectal cancer screening modernization, which should support both colonoscopy volume and demand for single-use accessories over time. Central and Eastern Europe still offer room for penetration as public procurement cycles and healthcare infrastructure investment improve across parts of the region.

Asia-Pacific is projected to grow at an 8.65% CAGR through 2031, which makes it the fastest-growing regional segment in the gastrointestinal endoscopy devices market. Growth is being supported by broader screening efforts in China, India, and South Korea, alongside demand for both premium and value-tier systems as capacity expands across different hospital tiers. Japan remains a structurally important market because aging demographics and the wider use of ESD for early gastric cancer continue to support gastrointestinal endoscopy demand. Middle East and Africa and South America remain smaller, but they are moving along a similar path with a lag as health system modernization and public-private endoscopy expansion gradually improve procedure access.

Competitive Landscape

The gastrointestinal endoscopy devices market remains moderately concentrated at the premium tier, with Olympus, Fujifilm, and KARL STORZ holding strong positions in imaging systems and scopes, while Boston Scientific remains important in therapeutic accessories and EUS-linked procedures. Leadership in this field comes from installed base depth, imaging quality, regulatory execution, service support, and the ability to bundle software with hardware. Olympus has strengthened that position by extending the EVIS X1 platform with the EZ1500 series endoscopes and then adding the OLYSENSE CAD/AI suite, which helps it build recurring software revenue on top of existing hardware relationships[3]Olympus Corporation, “Olympus Launches OLYSENSE CAD/AI in the US and Europe,” Olympus Corporation, olympus-global.com. That platform approach makes switching harder for hospitals that already rely on one installed ecosystem across imaging, workflow, and service support.

Competitive pressure is becoming more visible in China and other value-sensitive markets, where domestic companies are gaining ground in lower-tier hospitals with lower-priced systems and stronger alignment with local procurement conditions. This is widening the split between premium and value segments rather than creating one uniform competitive field. Olympus acknowledged continued pressure in China in its FY2026 financial disclosures, where regulatory timing for new products weighed on near-term performance even as bidding activity improved. The gastrointestinal endoscopy devices market is also seeing strategic divergence, with larger incumbents leaning further into AI, ecosystem control, and adjacent procedures while smaller or mid-tier players face rising pressure from tenders, group purchasing structures, and the cost of keeping pace with premium innovation. CONMED’s exit from gastroenterology in December 2025 reflects that pressure and shows that product lines without enough differentiation are becoming harder to sustain.

Strategic moves since 2025 show how major companies are trying to widen their position beyond traditional scope sales. Olympus signed a global distribution agreement with EndoRobotics in May 2026 to add robot-assisted capabilities for third-space endoscopy, which points to a more intervention-heavy future for advanced gastrointestinal procedures. Olympus also announced the BioProtect acquisition in May 2026, showing a willingness to use deals to deepen adjacent technology positions and protect long-term account access. Fujifilm, meanwhile, continues to push premium imaging through ELUXEO 8000, which supports its position in centers that are moving toward 4K visualization and higher-complexity endoscopy workflows.

Gastrointestinal Endoscopy Devices Industry Leaders

Olympus Corporation

Boston Scientific Corporation

Fujifilm Holdings Corporation

Medtronic plc

Johnson and Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: FUJIFILM Healthcare Americas Corporation announced that its ELUXEO 8000 Endoscopic Imaging System coupled with its EG-840TP ultra slim therapeutic gastroscope selected as the winner of the “Best New Endoscopy Technology Solution” award in the 10th annual MedTech Breakthrough Awards program.

- October 2025: Olympus Canada Inc. (OCI), a player in medical technology for gastrointestinal endoscopy, announced the launch of the EZ1500 series endoscopes featuring Extended Depth of Field (EDOF) technology.

Global Gastrointestinal Endoscopy Devices Market Report Scope

As per the scope of the report, gastrointestinal endoscopy devices are specialized medical instruments used to visualize, diagnose, and sometimes treat conditions within the gastrointestinal (GI) tract. These devices typically include endoscopes, flexible or rigid tubes equipped with a camera, light source, and working channels to perform various therapeutic interventions.

The gastrointestinal endoscopy devices market is segmented by product type, reusability, age group, application, end user, and geography. By product type, the market includes endoscopes (flexible endoscopes, rigid endoscopes, and disposable endoscopes), visualization equipment, and operative devices & accessories. By reusability, the market is divided into reusable endoscopes and single-use endoscopes. By age group, the segmentation covers adults, geriatrics, and pediatrics. By application, the market is categorized into diagnostics and therapeutics. By end user, the segmentation includes hospitals, ambulatory surgery centers, specialty clinics, and other end users. By geography, the market is analyzed across North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Endoscopes | Flexible Endoscopes |

| Rigid Endoscopes | |

| Disposable Endoscopes | |

| Visualization Equipment | |

| Operative Devices and Accessories |

| Reusable Endoscopes |

| Single-Use Endoscopes |

| Adults |

| Geriatrics |

| Pediatrics |

| Diagnostics |

| Therapeutics |

| Hospitals |

| Ambulatory Surgery Centers |

| Specialty Clinics |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Endoscopes | Flexible Endoscopes |

| Rigid Endoscopes | ||

| Disposable Endoscopes | ||

| Visualization Equipment | ||

| Operative Devices and Accessories | ||

| By Reusability | Reusable Endoscopes | |

| Single-Use Endoscopes | ||

| By Age Group | Adults | |

| Geriatrics | ||

| Pediatrics | ||

| By Application | Diagnostics | |

| Therapeutics | ||

| By End User | Hospitals | |

| Ambulatory Surgery Centers | ||

| Specialty Clinics | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the gastrointestinal endoscopy devices market in 2026?

The gastrointestinal endoscopy devices market stands at USD 22.24 billion in 2026 and is forecast to reach USD 30.70 billion by 2031 at a 6.66% CAGR.

Which product segment leads revenue in gastrointestinal endoscopy devices?

Endoscopes led product revenue with a 38.31% share in 2025 because flexible scopes remain essential across both diagnosis and treatment.

Which product area is growing the fastest through 2031?

Visualization equipment is projected to grow the fastest at an 8.38% CAGR through 2031 as providers upgrade to 4K and AI-ready imaging systems.

Why are single-use endoscopes gaining attention?

They are benefiting from infection-control concerns, reprocessing cost pressure, and demand in higher-risk procedures, which supports a 7.52% CAGR through 2031.

Which end-user setting is expanding the fastest for gastrointestinal procedures?

Ambulatory surgery centers are projected to grow at an 8.85% CAGR through 2031 as preventive care coverage and outpatient capacity continue to expand.

Which region shows the strongest growth outlook through 2031?

Asia-Pacific is forecast to grow the fastest at an 8.65% CAGR through 2031, supported by broader screening activity and rising demand across both premium and value-tier systems.

Page last updated on: