Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

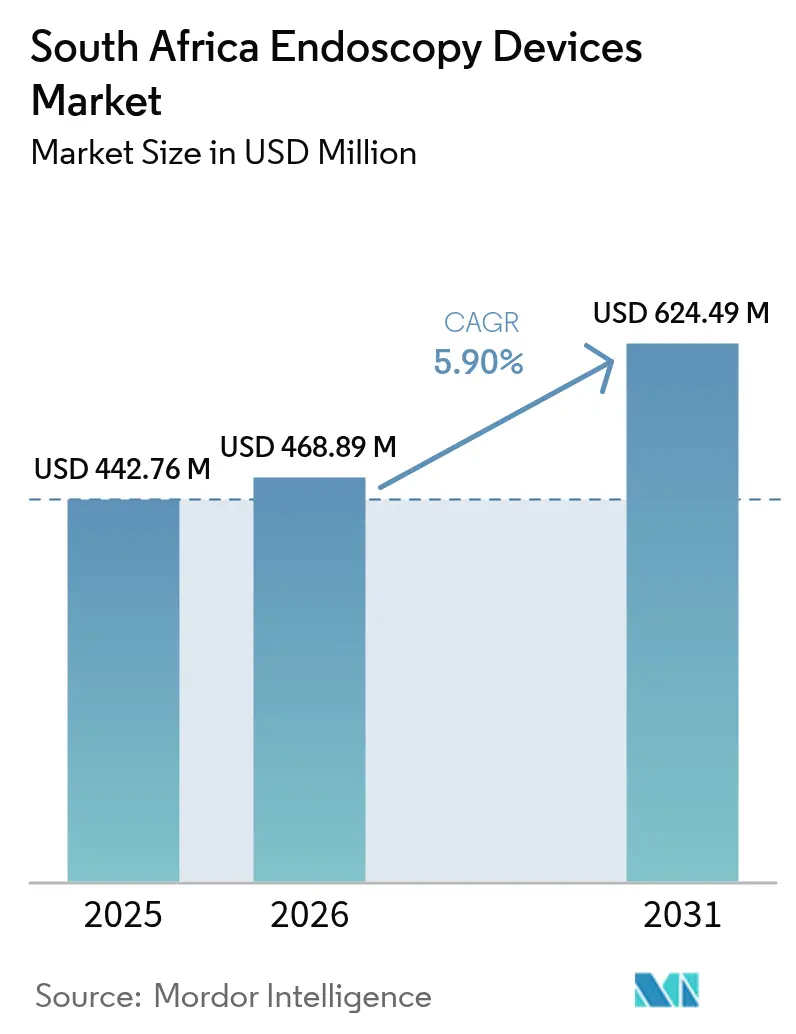

| Base Year Market Size (2025) | USD 442.76 Million |

| Market Size (2026) | USD 468.89 Million |

| Market Size (2031) | USD 624.49 Million |

| Growth Rate (2026 - 2031) | 5.90% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Endoscopy Devices Market Analysis by Mordor Intelligence

The South Africa endoscopy devices market size is expected to grow from USD 442.76 million in 2025 to USD 468.89 million in 2026 and is forecast to reach USD 624.49 million by 2031 at 5.90% CAGR over 2026-2031. Intensifying healthcare infrastructure upgrades under the National Health Insurance (NHI), rising gastrointestinal disease prevalence, and sustained private-sector capital expenditure are jointly reshaping demand for flexible and rigid scopes. Life Healthcare’s USD 115 million capital plan, together with city-center hospital expansions, boosts equipment procurement pipelines while creating headroom for premium visualization systems. Infection-control imperatives following reusable-scope contamination incidents have elevated single-use options, and artificial-intelligence-enabled imaging continues to raise diagnostic accuracy thresholds, especially in colorectal cancer screening. Regulatory clarity from SAHPRA’s September 2024 medical-device schedules now shortens product-registration lead times, encouraging multinational technology roll-outs. However, escalating compliance expenses for scope reprocessing, a nationwide shortage of 27,000 healthcare workers, and public-sector budget ceilings temper the near-term adoption curve.

Key Report Takeaways

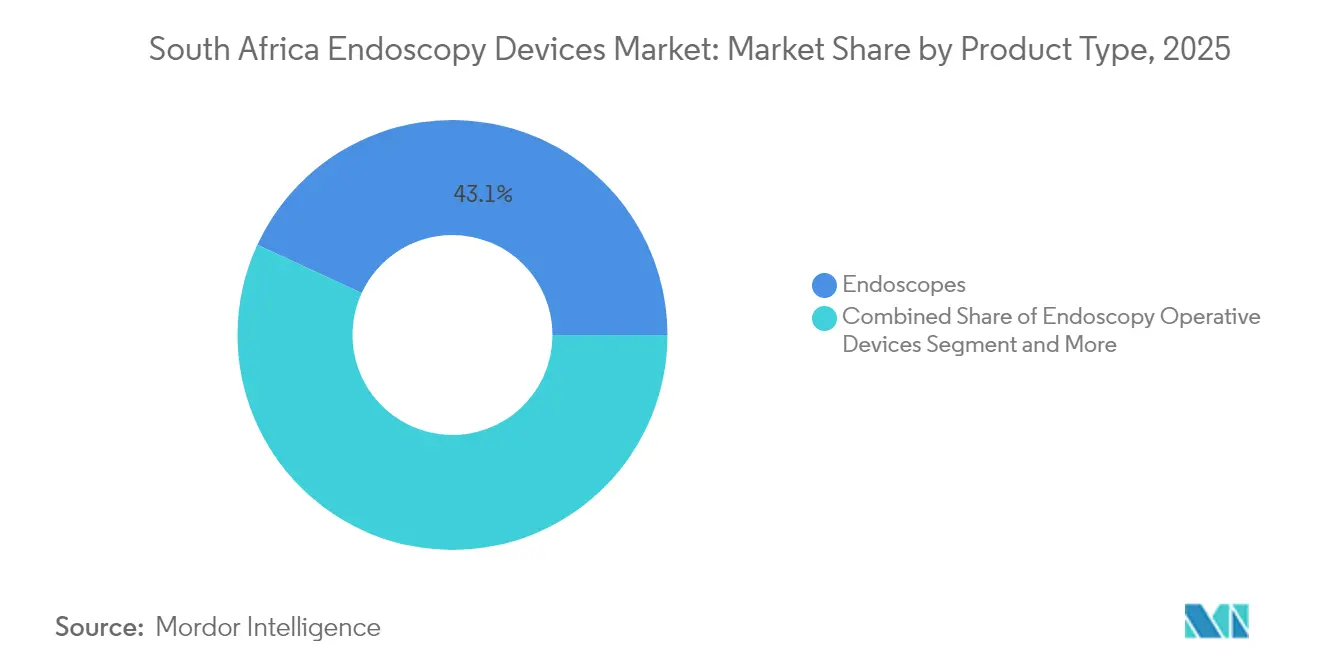

- By product type, endoscopes led with a 43.11% South Africa endoscopy devices market share in 2025; visualization systems are forecast to post an 8.42% CAGR through 2031.

- By application, gastroenterology accounted for 52.05% of the South Africa endoscopy devices market size in 2025, while ENT surgery is advancing at an 8.63% CAGR to 2031.

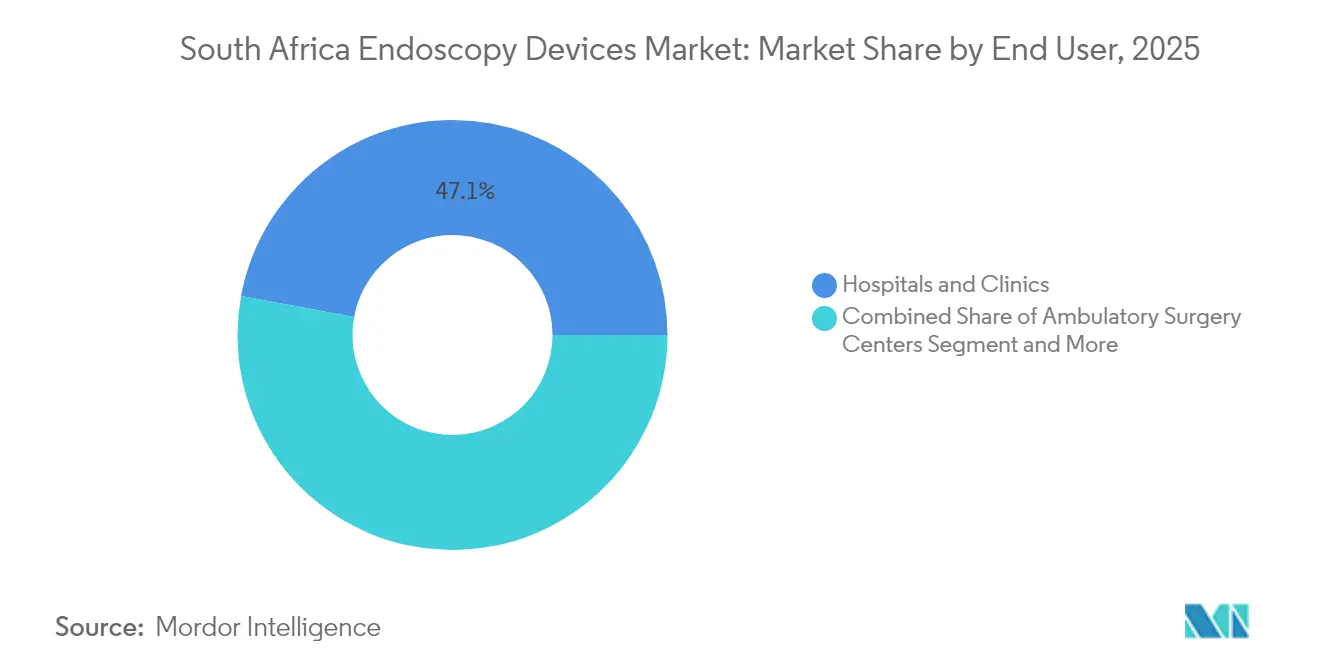

- By end user, hospitals & clinics held 47.10% share of the South Africa endoscopy devices market size in 2025, yet ambulatory surgery centers record the highest projected 8.99% CAGR through 2031.

- By hygiene, reusable scopes dominated with 83.60% South Africa endoscopy devices market share in 2025; single-use scopes are rising at a 9.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Endoscopy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of GI diseases & aging population | +1.8% | Urban hubs (Cape Town, Johannesburg) | Medium term (2-4 years) |

| Advancements in endoscopic technologies | +1.5% | Private tertiary hospitals nationwide | Long term (≥ 4 years) |

| Expansion of day-surgery centers | +1.2% | Metro areas, secondary cities | Medium term (2-4 years) |

| Growing awareness of minimally invasive care | +0.9% | National, led by private insurers | Short term (≤ 2 years) |

| Improved NHI reimbursement for therapeutic scopes | +0.6% | Nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Gastrointestinal Diseases Coupled with Growing Aging Population

Dyspepsia drives 52.4% of upper-GI endoscopy indications in Africa, and gastritis is the most frequent finding at 33.3%, underscoring persistent procedural demand. South Africa’s demographic shift toward an older population amplifies colonoscopy screening requirements, as colorectal-cancer cases are projected to rise sharply by 2050. Early detection via endoscopy improves survival odds, embedding the modality within routine chronic-disease management pathways. Urban lifestyles linked to Helicobacter pylori infection and gastroesophageal reflux disease escalate case volumes in major metros. Consequently, the South Africa endoscopy devices market benefits from a consistent flow of diagnostic and interventional procedures despite macroeconomic headwinds.

Advancements in Endoscopic Technologies

Artificial-intelligence-assisted detection now elevates adenoma-detection rates and reduces inter-observer variability during colonoscopy sessions, narrowing diagnostic gaps between public and private facilities[1]Jean-Francois Rey, “How artificial intelligence is revolutionizing endoscopy,” Clinical Endoscopy, clinicalendoscopy.org. Robotic-assisted platforms extend minimally invasive access to complex GI and bariatric procedures, with flagship programs operational in Johannesburg’s teaching hospitals. Olympus’ EVIS X1 launch integrates machine-learning-based texture and color-pattern recognition, supporting early neoplasia identification. Video-processing upgrades and high-definition chip-on-tip optics stimulate replacement cycles across tertiary centers. While high acquisition costs slow penetration in smaller facilities, leasing models and vendor-backed training accelerate broader technology diffusion within the South Africa endoscopy devices market.

Expansion of Day-Surgery Centers Accelerates Flexible Endoscope Adoption

Ambulatory surgery centers (ASCs) deliver shorter turnaround times and 20%–25% lower procedure costs compared with inpatient settings, a value proposition attractive to payers and patients alike. High-volume colonoscopy and upper-GI lists improve scope utilization rates, justifying investment in premium visualization towers and automated reprocessors. Cape Town and Johannesburg ASCs report the region’s highest surgical-capacity indices, driven by streamlined scheduling protocols and reduced cancellation rates. As NHI benefit schedules broaden, secondary cities such as Bloemfontein and Polokwane are planning ASC build-outs, further enlarging the addressable base for flexible scopes and related consumables.

Growing Awareness and Patient Preference for Minimally Invasive Procedures

Predictive-analytics tools like Discovery Health’s Personal Health Pathways deliver tailored screening prompts to 2.1 million members, boosting preventive colonoscopy uptake rates. Patient education campaigns emphasize faster recovery, reduced scarring, and lower infection risk relative to open surgery, tilting decision matrices toward endoscopic solutions. In facilities where waiting lists strain capacity, minimally invasive techniques free inpatient beds more quickly, aligning clinical efficiencies with administrative imperatives. Social-media amplification of celebrity endoscopy experiences further normalizes procedures, encouraging earlier physician consultations. This demand-side momentum underpins robust volume growth within the South Africa endoscopy devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced equipment | -1.1% | Public-sector hospitals countrywide | Short term (≤ 2 years) |

| Shortage of trained endoscopy staff | -0.8% | Rural & secondary urban facilities | Medium term (2-4 years) |

| Economic constraints & budget limitations | -0.6% | Public healthcare system | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Endoscopy Equipment

Premium visualization stacks and robotic platforms can exceed USD 1 million per installation, stretching procurement budgets even in leading private groups. Updated AAMI reprocessing standards add USD 52–67 to every reusable-scope procedure, increasing total cost of ownership. Public hospitals frequently postpone upgrades or rely on donations, creating a two-tier technology landscape. While single-use scopes address contamination risk, their per-unit pricing remains higher than amortized reusable alternatives, challenging adoption in price-sensitive settings.

Shortage of Trained Endoscopy Support Staff in Hospitals

Vacancies across endoscopy technicians, GI nurses, and sterile-processing specialists limit procedural volumes, even where equipment capacity is adequate. Competition from the private sector accelerates workforce migration away from rural facilities, lengthening waiting lists and undermining NHI equity goals[2]Haseena Ismail, “27,000 Critical Skills Shortages in Health Sector,” Democratic Alliance, da.org.za. Advanced platforms such as AI-guided colonoscopy require additional training, which intensifies the skills deficit and delays roll-outs in resource-constrained provinces.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Endoscopes Lead Despite Visualization Growth

Endoscopes accounted for 43.11% of the South Africa endoscopy devices market share in 2025, underlining their central role in diagnostic and therapeutic pathways. High prevalence of GI indications ensures stable baseline demand for flexible gastroscopes and colonoscopes, while rigid arthroscopes and laparo-endoscopes support surgical volumes in orthopedics and bariatrics. Visualization systems are projected to log an 8.42% CAGR through 2031, reflecting rapid replacement of standard-definition camera heads with 4K and 3D modules. The South Africa endoscopy devices market benefits from vendor-provided managed-service contracts that bundle towers, light sources, and processors into predictable monthly fees, easing capital-budget pressures.

Disposable single-use scopes gain momentum where contamination concerns outweigh cost differentials; FDA-backed designs are now applied in ERCP and bronchoscopy with comparable technical success. Operative accessories—from electrocautery snares to fluid-management pumps—experience rising throughput as therapeutic endoscopy expands. Robot-assisted flexible platforms remain nascent but attract early adopters in academic centers aiming to deliver incisionless NOTES (natural-orifice transluminal endoscopic surgery). These dynamics collectively tilt the product mix toward higher-value categories, sustaining revenue expansion beyond pure volume growth.

By Application: Gastroenterology Dominance Challenged by ENT Growth

Gastroenterology held 52.05% of the South Africa endoscopy devices market size in 2025, supported by established colorectal-cancer screening guidelines and high peptic-ulcer prevalence. Routine surveillance for Barrett’s esophagus and inflammatory bowel disease further entrenches GI demand. ENT surgery, however, is set to outpace at an 8.63% CAGR through 2031, driven by endoscopic sinus-surgery adoption and the popularity of office-based laryngoscopy.

Pulmonology volumes rise amid persistent tuberculosis caseloads; therapeutic bronchoscopy now incorporates cryo-biopsy and airway-stenting kits that enlarge accessory revenues. Urology leans toward single-use ureteroscopes that mitigate cross-infection in renal-stone management. Arthroscopy and cardiology remain specialized niches characterized by high reimbursement values, while bariatric-endoscopy services such as intragastric-balloon placement reflect burgeoning obesity prevalence. Cross-disciplinary growth diversifies revenue streams, ensuring that the South Africa endoscopy devices market is not overly reliant on any single therapeutic area.

By End User: Hospitals Dominate While Ambulatory Centers Surge

Hospitals & clinics commanded 47.10% of the South Africa endoscopy devices market size in 2025, leveraging integrated care pathways and intensive-care back-up essential for advanced therapeutic cases. Their in-house sterile-processing departments enable large reusable-scope fleets, spreading reprocessing costs over high daily volumes. Yet ambulatory surgery centers will post the fastest 8.99% CAGR to 2031 as payers push lower-acuity procedures into outpatient settings.

The ASC business model aligns with bundled payments and capitation schemes under NHI, encouraging investors to green-light new builds in growing peri-urban markets. Specialized endoscopy centers focusing on GI or ENT lines exploit high-throughput efficiencies and shorter patient turnover to achieve superior economics. Such diversification of care venues reshapes procurement patterns, favoring portable towers and slim-line scopes optimized for fast case-mix changes.

By Hygiene: Reusable Dominance Faces Single-Use Disruption

Reusable scopes still controlled 83.60% of the South Africa endoscopy devices market share in 2025, reflecting entrenched reprocessing infrastructure and lower per-procedure costs at high volumes. Automated endoscope reprocessors with integrated drying cabinets reduce microbial risk, yet outbreaks linked to Pseudomonas and multidrug-resistant organisms continue to surface globally. Single-use scopes, growing at 9.21% CAGR, bypass cleaning entirely and simplify logistics for remote outreach programs.

Cost-benefit models now factor in AAMI-mandated micro-inspection borescope checks and detergent upgrades, narrowing the lifetime expense gap between reusable and disposable options. Sustainability debates ruminate over medical-plastic waste, yet clinical-governance committees increasingly prioritize patient safety over environmental trade-offs. As procurement authorities consolidate under NHI, volume-discount negotiations may tip the balance in favor of single-use platforms for high-risk ERCP and bronchoscopy procedures.

Geography Analysis

Metropolitan hubs—Johannesburg, Pretoria, and Cape Town—absorb a majority share of procedural volumes, buoyed by tertiary hospitals, private-sector capital flows, and proximity to import logistics corridors. These provinces adopt AI-enhanced towers earlier, accelerating replacement cycles. NHI legislation, enacted in 2024, aims to equalize service availability by centralizing procurement and funding nationwide. Yet roll-out complexities and fiscal constraints may delay uniform equipment distribution until beyond 2027, preserving short-term geographic disparities.

Coastal provinces benefit from medical-tourism inflows; private hospitals in Durban and Port Elizabeth advertise package colonoscopy screenings with same-day histology reporting, attracting regional travelers. Inland provinces face greater staff shortages, with vacancy rates for GI technicians surpassing 35% in Limpopo and the Northern Cape. Infrastructure commitments totaling ZAR 943.8 billion (USD 53.28 billion) for 2024-2026 allocate funds for rural clinic refurbishments, including modular endoscopy suites and tele-mentoring platforms that extend urban expertise to remote sites.

Mobile endoscopy units equipped with generator-powered towers are piloting cross-district colorectal-screening drives, demonstrating 40% higher participant compliance versus centralized referral models. Provincial health departments evaluate cloud-based image-archiving systems to enable real-time consults with university gastroenterologists, mitigating specialist scarcity. Over the forecast horizon, incremental infrastructure build-outs and technology transfer schemes are expected to lift penetration rates outside the top three metro areas, broadening the revenue canvas for the South Africa endoscopy devices market.

Competitive Landscape

International manufacturers dominate through long-standing distributor alliances that navigate SAHPRA registration and tender prerequisites. Olympus, Karl Storz, and Boston Scientific collectively account for significant unit shipments, leveraging bundled service contracts and on-site engineer coverage. Local firms concentrate on reprocessing detergents and low-cost accessory ranges, supplying public hospitals under price-sensitive bids.

Technological differentiation around AI-embedded detection algorithms, 4K/3D imaging, and robotic steerable tips sets leading brands apart, enabling premium pricing. Strategic moves include Olympus’ FY 2024 launch of the EVIS X1 system, which has secured early adoption at two Johannesburg teaching hospitals. Boston Scientific expanded its distribution partnership in 2025 to cover single-use duodenoscopes, anticipating NHI-linked infection-control mandates. Meanwhile, Karl Storz introduced a managed-service lease model, bundling towers, scopes, and consumables under fixed monthly fees, appealing to ASC operators seeking predictable cash-flows.

Training remains a decisive competitive lever; vendors sponsor fellowships and simulation labs to address the critical technician shortage. Digital platforms offering augmented-reality troubleshooting guide on-site staff through scope maintenance, reducing downtime. Such wrap-around services elevate switching costs and entrench incumbent positions, maintaining a moderate concentration score within the South Africa endoscopy devices industry.

South Africa Endoscopy Devices Industry Leaders

Olympus Corporation

KARL STORZ SE & Co. KG

Boston Scientific Corporation

Fujifilm Holdings Corporation

Pentax Medical (HOYA Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Discovery Health unveiled Personal Health Pathways, an AI-powered recommendation engine for 2.1 million members, designed to nudge preventive colonoscopy uptake.

- September 2024: SAHPRA released updated medical-device schedules clarifying classification and licensing rules for endoscopy equipment.

South Africa Endoscopy Devices Market Report Scope

Endoscopes are minimally invasive devices and can be inserted into natural openings of the body to observe an internal organ or a tissue in detail. Endoscopic surgeries are performed for imaging procedures and minor surgeries.

The South Africa endoscopy devices market is segmented by type of device (endoscopes, endoscopic operative devices, and visualization equipment) and application (gastroenterology, pulmonology, orthopedic surgery, cardiology, ENT surgery, gynecology, neurology, and other applications).

The report offers the value in USD for the above segments.

By Product Type

| Endoscopes | Flexible Endoscopes |

| Rigid Endoscopes | |

| Capsule Endoscopes | |

| Robot-Assisted Endoscopes | |

| Disposable (Single-Use) Endoscopes | |

| Visualization Systems | Camera Heads |

| Light Sources | |

| Video Processors | |

| Monitors & Displays | |

| Data Recorders & Storage | |

| Endoscopy Operative Devices | Energy Systems |

| Insufflators & Suction Pumps | |

| Endoscopic Staplers & Suturing Devices | |

| Retrieval Devices | |

| Fluid Management Systems | |

| Accessories & Consumables |

By Application

| Gastroenterology |

| Pulmonology |

| Urology |

| Gynecology |

| Orthopedic Surgery (Arthroscopy) |

| Cardiology |

| ENT Surgery |

| Neurology |

| Bariatric & Metabolic Surgery |

| Other Applications |

By End User

| Hospitals & Clinics |

| Ambulatory Surgery Centers |

| Other End Users |

By Hygiene

| Reusable Endoscopes |

| Single-Use Endoscopes |

| By Product Type | Endoscopes | Flexible Endoscopes |

| Rigid Endoscopes | ||

| Capsule Endoscopes | ||

| Robot-Assisted Endoscopes | ||

| Disposable (Single-Use) Endoscopes | ||

| Visualization Systems | Camera Heads | |

| Light Sources | ||

| Video Processors | ||

| Monitors & Displays | ||

| Data Recorders & Storage | ||

| Endoscopy Operative Devices | Energy Systems | |

| Insufflators & Suction Pumps | ||

| Endoscopic Staplers & Suturing Devices | ||

| Retrieval Devices | ||

| Fluid Management Systems | ||

| Accessories & Consumables | ||

| By Application | Gastroenterology | |

| Pulmonology | ||

| Urology | ||

| Gynecology | ||

| Orthopedic Surgery (Arthroscopy) | ||

| Cardiology | ||

| ENT Surgery | ||

| Neurology | ||

| Bariatric & Metabolic Surgery | ||

| Other Applications | ||

| By End User | Hospitals & Clinics | |

| Ambulatory Surgery Centers | ||

| Other End Users | ||

| By Hygiene | Reusable Endoscopes | |

| Single-Use Endoscopes | ||

Key Questions Answered in the Report

What is the current value of the South Africa endoscopy devices market?

It stands at USD 468.89 million in 2026 and is projected to reach USD 624.49 million by 2031.

How fast is single-use endoscope adoption growing?

Single-use scopes are expanding at a 9.21% CAGR through 2031, driven by infection-control priorities.

Which product category is growing fastest?

Visualization systems are slated to grow at an 8.42% CAGR, propelled by AI-enabled imaging.

Why are ambulatory surgery centers important in this space?

ASCs offer 20%-25% lower procedure costs and are expected to grow at a 8.99% CAGR, absorbing routine GI volumes.

What key restraint could slow market growth?

High capital costs and increased reprocessing-compliance expenses raise barriers for public hospitals.

Page last updated on: